Sample Category Title

EUR/USD Stalls Below Key Highs as ECB Meeting Looms — What’s Next?

The picture for currencies today is the exact reverse of yesterday - with traders fading extremes and booking profits before events like the upcoming NFP.

Safe-Haven majors like the CHF and JPY are lagging on the day with the USD leading, closely followed by the CAD - the Euro is right in the middle of the currency board down 0.55% on the day.

The ECB Meeting is coming up on Thursday 5th of June with broad expectations of a 25 bps cut before pausing in the July meeting - taking the Deposit Rate from 2.25% to 2%. We will get the Rate Decision at 8:15.

We got the overnight Eurozone Inflation report with the Headline CPI coming in just below 2% - the ECB will want to make sure to push these numbers up slightly, although the Central Bank probably has taken into account the lag for new inflationary boosts from Tariffs on exports to the US.

Let’s take a look at the levels from Daily to Hourly charts to prepare for what’s next.

EUR/USD Technical Analysis

Daily Timeframe

EURUSD Daily Chart, June 3, 2025. Source: TradingView

The Daily timeframe is showing mixed signs in terms of strength - the trend is still bullish for the currency pair though candles have been overlapping in the past few weeks.

This story gets confirmed with the Daily RSI not showing signs of expansion - bulls will have to monitor the tone from the ECB at the press conference 30 minutes after the release.

Less cuts are expected going forward therefore action will be focused on better data for the Eurozone.

The daily MA 50 has caught up to the current prices and is currently acting as immediate support, accompanied with the trendline.

In the meantime, the action is constrained within the Main resistance and support zones which we will see in more detail promptly.

4H Timeframe

EURUSD 4H Chart, June 3, 2025. Source: TradingView

Taking a closer look at the 4H timeframe emphasizes the lack of clarity going into the ECB Meeting.

Prices have been seesawing through the current main pivot situated at 1.1330 and constrained in a slightly above 1000 pip range between the 1.1270 - 1.13 to 1.1420 - 1.1440.

The RSI is neutral and the MA 50 and 200 are immediate support, though we are looking more at holding the trendline from the hourly upward channel formed last week. Expect rangebound prices going into Thursday.

Any breakout from the range is pointing towards these main zones:

- Main Support Zone : 1.1050 to 1.1120

- Main Resistance Zone: 1.1530 to 1.15730

Hourly Timeframe

EURUSD 4H Chart, June 3, 2025. Source: TradingView

Prices just rejected the higher bound of the range and are now consolidating at the low of the upward channel.

Broad USD strength seems to be more on a mean-reversal basis therefore I am not expecting to see much direction.

Prices may try to test the MA 200 situated 300 pips from here therefore keep that one on your 1H charts.

Momentum is close to oversold on the hourly timeframe - keep in mind that markets tend to fade extremes going into key data, and NFP will still be looming on Friday - keep a close eye on the language from the ECB on Thursday, the conference is at 8:45 A.M. on the 5th of June.

Safe Trades!

How to Trade AUDCAD effectively – Exploiting the Range

While AUDCAD isn’t among the highest-volume pairs in Forex, it’s often in the lesser-traded instruments that sharp traders find unique opportunities.

Commodities heavily influence the Australian and Canadian dollars, as both nations are major exporters. The AUD tends to react more to moves in industrial metals—especially copper—while the CAD is tied to oil price fluctuations.

Beyond commodities, the currencies are driven by their respective economic ties: Canada is closely linked to trends in the U.S., whereas Australia is more sensitive to developments in China. In the absence of fresh geopolitical shocks, traders are focusing on central bank policy divergence and incoming economic data.

On that front, the Bank of Canada paused its rate-cutting cycle at its last meeting after starting in June 2024. Its next decision is due Wednesday, June 4, and markets widely expect another hold, as the BoC remains in wait-and-see mode following the latest U.S. tariff changes.

Meanwhile, the Reserve Bank of Australia kicked off its own cutting cycle in May 2025 with a 25 bps cut and signaled more may follow. This gives the pair a bearish tilt, though sentiment remains cautious until the economic impact of tariffs becomes clearer.

Let’s dive into the charts and examine AUDCAD across higher timeframes, starting from the weekly view to the 4-hour chart.

AUDCAD Weekly Timeframe

AUDCAD Weekly Chart, June 3, 2025. Source: TradingView

AUDCAD has been in a broader downtrend since 2016, though that long-term move has been marked by multiple intermediate upswings and pullbacks.

Given both currencies’ sensitivity to industrial commodity prices, they generally move in tandem with broader risk sentiment, resulting in relatively stable correlation patterns.

The pair often trades within well-defined ranges on the weekly chart rather than trending aggressively. At current levels, AUDCAD sits near the midpoint of that range—there is less technical direction at the current levels;

This is a good moment to zoom into the daily chart for more precise context and to identify shorter-term opportunities.

AUDCAD Daily Timeframe

AUDCAD Daily Chart, June 3, 2025. Source: TradingView

The pair wasn’t immune to the volatility that shook Forex markets earlier this year.

AUDCAD had been trading up throughout 2024, profiting from the dovish stance and data coming out of Canada - the BoC started its cutting cycle almost a full year before the RBA! Weakness in the CAD was generally a theme of last year though and this weakness may be found in the current theme of cutting from the Australian Central Bank.

The Pair also had a major selloff on Liberation Day, forming the yearly lows at 0.8450 after coming right back into the current range.

For current trading, look at the range between the 0.8800 lower band and the 0.9050 higher band.

On a purely technical look, the pair is not showing major signs of volatility with the RSI in the neutral range - we are closer to the lower band - the situation may evolve with the upcoming BoC Meeting.

Let's take a closer look.

AUDCAD 4H Timeframe

AUDCAD 4H Chart, June 3, 2025. Source: TradingView

After coming back from the extremes hit at the beginning of April, the currency pair has been contracting in volatility throughout the month of May.

The most immediate price action has been constrained in a 500 pip range between 0.8850 to 0.89 in the waiting for the release of the Bank of Canada Rate decision at 9:45 on Wednesday.

A break above this tight range hints at the Intermediate Resistance Zone around 0.8950 and a break below would look towards the lower Band at the key 0.88 psychological level.

Momentum is calm though expect more volatility as we progress through the week.

Safe Trades!

Silver (XAG/USD) Cools from 7-Month High on Profit Taking, Remains Bullish

Boasting a remarkable gain of 5.38% yesterday, silver prices have retraced somewhat in today’s session, owing to natural profit-taking and better-than-expected US labor data. XAG/USD currently trades around ~34.55350 per troy ounce, down -0.60% for the day.

XAG/USD: Key Takeaways

- Failing to find support around ~99.131, a weaker U.S. dollar (DXY) made way for massive silver gains in yesterday’s session, representing the metal’s best daily performance since October of last year.

- Silver has retraced from its highs in today’s session as markets look to secure profits alongside a positive JOLTS report, beating consensus by 290,000 thousand job openings.

Silver (XAG/USD): Precious metals gain on continued dollar weakness

Perhaps somewhat overshadowed by its yellow peer regarding performance and all-time highs in recent memory, yesterday’s session marks silver’s largest daily gain in over eight months, rising 5.38% in value compared to a more modest 2.80% gain for gold.

Looking to challenge previous highs made in October 2024, a trend of dollar weakness has allowed precious metals to rise in value, which are already pacing well for the year amid continued worries of global trade relations, geopolitical tensions, and uncertainty surrounding US monetary policy.

Markets now look ahead to speeches from various Fed policymakers in the next twenty-four hours and a rumoured phone call between Trump and Xi Jinping to discuss trade relations, as current negotiations prove unproductive.

Silver (XAG/USD): Fed policy dilemma boosts precious metal pricing

With various conflicting signals from recent economic data points, the Fed is currently in an unenviable position ahead of its June 18th meeting.

While recent releases showing a declining GDP and lower inflation would typically support rate cuts, today’s JOLTs report shows the US Labour market is more buoyant than once thought, suggesting that rates should remain unchanged.

At least in part due to recent tariff announcements, the Fed remains cautious owing to fears of ‘stagflation’, in which both inflation and unemployment would remain high. Highlighting “heightened risks to both employment and inflation targets” as justification for leaving rates unchanged in their previous meeting, the Federal Reserve is now faced with the following dilemma:

- Leave rates unchanged, prioritise an otherwise buoyant jobs market and low inflation, but risk further economic contraction.

- Cut rates, prioritise economic growth, but risk higher inflation and job market health.

Under current circumstances, at least in some regard, both outcomes can be seen as supportive of silver pricing. While lower rates typically favour non-yielding assets like silver, leaving rates unchanged risks further economic slowdown, boosting market uncertainty, and, by extension, safe-haven flows into precious metals.

A chart showing the recent price action of XAGUSD. OANDA,TradingView, 03/06/2025

XAG/USD: Technical analysis

- As of June 3rd, silver has had its best year-to-date performance in over five years, aside from 2024. If it can break previous yearly highs around ~34.86900, silver will trade at its highest level since 2011 during the height of the Euro sovereign debt crisis.

- If price remains above 33.02574, we can expect silver to stage a move higher. Bulls will first aim to take out previous highs, then aim towards $36 per troy ounce, representing the next level of daily resistance.

S&P 500 Approaches 6000 Ahead of NFP

US Indices, which have started the day mixed, have appreciated this morning’s JOLTS report.

The data came out better than expected, with 7,391M Job Openings vs 7,200 Expected, a rise of 191,000 on the month.

This data set is still proving the strength of US Data amid geopolitical uncertainties.

Sentiment is positive throughout markets as gold did not maintain yesterday’s momentum, and indices are green all around.

Let’s look at the S&P 500 intra-day charts, as prices are less than 30 points from the 6,000 level.

S&P 500 Technical Analysis

S&P 500 4H Charts

S&P 4H Chart, June 3, 2025. Source: TradingView

The S&P caught some decent momentum into the beginning of the week as US data has been coming better than expected.

A month-end bounce on the Immediate Pivot at 5,846 has led to a 125 point rally, forming an upward trendline consolidated by the 4H 100 period moving average.

Any breakout higher will look to test the all-time highs of 6,152- though more positive news and economic data will be required.

Let's take a closer look.

S&P 1H Chart, June 3, 2025. Source: TradingView

The S&P approached current levels with bullish impulsive measured moves, forming what resembles a Cup & Handle pattern - typically seen as bullish.

The overall bullish structure, held by the MA 200 at 5,891 within the current support zone, will meet some hurdles.

We are approaching the 5,990 to 6,000 resistance zone which may generate position closing as this month's Non-Farm Payroll report is looming.

A positive report may break through this level in a swing towards a test of the ATH, although a bad surprise might just do the reverse to revisit the 5,730 May Lows.

Safe Trades!

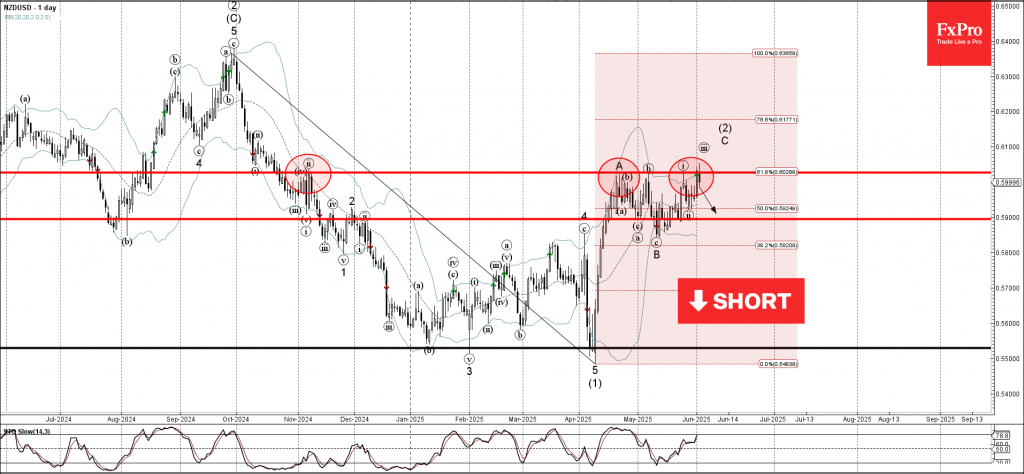

NZDUSD Wave Analysis

NZDUSD: ⬇️ Sell

- NZDUSD reversed from the resistance zone

- Likely to fall to support level 0.5900

NZDUSD currency pair recently reversed down from the resistance zone between the resistance level 0.6030 (which has been reversing the price from November), the upper daily Bollinger Band and the 61.8% Fibonacci correction of the downward impulse from September.

The downward reversal from this resistance zone stopped the C-wave of the previous ABC correction (2).

Given the strength of the resistance level of 0.6030 and the bearish divergence on the daily Stochastic, the NZDUSD currency pair can be expected to fall to the next support level of 0.5900.

Fed’s Bostic urges patience, in no hurry to adjust rates

Atlanta Fed President Raphael Bostic emphasized a patient approach to monetary policy in light of heightened uncertainty across trade, fiscal, and regulatory fronts. In an essay published today, Bostic noted that the US economy remains "broadly healthy", with inflation still above target but showing limited response—so far—from rising tariffs. “I am in no hurry to adjust our policy stance,” he wrote.

While macroeconomic indicators remain generally strong, Bostic flagged increasing caution among business leaders. Surveys conducted by the Atlanta Fed point to rising pessimism in the corporate sector, though this shift in sentiment was "not yet visible in hard economic data".

Bostic acknowledged that tariffs may eventually exert upward pressure on inflation, but reiterated that current readings do not yet reflect such an impact. "We might see upward pressure on prices over the coming weeks", he added.

Beyond trade, Bostic warned that broader policy shifts, in fiscal and regulatory domains, add to the difficulty of making reliable forecasts. With multiple potential shocks on the horizon, the best course, he argued, is to remain steady and flexible. external risks.

Sunset Market Commentary

Markets

European inflation numbers offered the proverbial “go” for Thursday’s ECB rate cut. Prices flatlined in May with both the headline and core (ex. food and energy prices) index coming in at 0% m/m. This resulted in a 1.9% and 2.3% y/y reading, missing estimates by 0.1 ppt. The services inflation gauge is closely watched because of its ties to wage growth and eased to the slowest pace since March of 2022 at 3.2%. It’s a sharp drop from April’s 4% but not one that’s necessarily going to be repeated in coming months when the (labour intensive) tourism season kicks in. It’s nevertheless silences the likes of Austria’s Holzmann, who last week argued for skipping the June meeting. We do expect the ECB to lay the groundwork for a pause after this week’s cut to 2% to see how the fiscal spending and trade war narrative pans out in the weeks thereafter. The impact of the CPI print on FI was limited. Markets did the math already, based amongst others on earlier misses in the French and Spanish outcome. Their too aggressive positioning (terminal rate seen between 1.5-1.75%) limits the scope for even lower yields as well, particularly at the front end. European yields are down around 2 bps on the day. Bunds slightly outperform Treasuries. US yields ease less than a basis point across the curve. Gilt in the UK are well bid, pushing the longest-term yields more than 6 bps down. Bank of England’s Mann helped shape this outperformance with her speech late Monday. She said that the central bank’s QT programme is offsetting some of the BoE’s efforts to reduce restrictiveness via rate cuts. Mann thereby opened the debate on downsizing the current £100bn per year bond portfolio reduction pace. The BoE discusses the matter always at its September meeting.

The US dollar gets some reprieve on FX markets, recouping most of its setback yesterday and ignoring the OECD’s downward growth revision (see below) in an otherwise dull trading session. EUR/USD descends from it’s one-month high around 1.145 to change hands around 1.387 currently. USD/JPY got no further than 143.35 and the trade-weighted dollar index rises to back above 99. The technical picture looks dire still though with the April multiyear low around 98 dangerously close. The dollar’s lingering vulnerability was exposed by last week’s second-tier US eco data (eg. second Q1 GDP reading and jobless claims). The eco calendar for the US starts heating up today with the JOLTS report scheduled for release after wrapping up this report. FX moves ex. USD in most cases are rangebound.

News & Views

The OECD published its latest global economic outlook. They point to weakening global economic prospects with substantial barriers to trade, tighter financial conditions, diminishing confidence and heightened policy uncertainty all projected to have an adverse impact on growth. Global growth is expected to slow from 3.3% last year to 2.9% in both 2025 & 2026. The US, Canada, Mexico and China will take the brunt of the slowdown. The OECD pencils in 1.6% and 1.5% growth for this year and next for the US (from 2.8%) whereas EMU growth is projected to strengthen from 0.8% in 2024 to 1% in 2025 and 1.2% in 2026. Higher trade costs in countries raising tariffs are expected to push inflation up further, although the impact will be partially offset by weaker commodity prices. Downside risks around the OECD scenario include further trade fragmentation, more persistent inflation and more fiscal pressure coming from higher debt payments. Upside risks are a reversal of new trade barriers, peaceful resolutions in Ukraine and the Middle East.

Swiss inflation rose by 0.1% M/M in May, but prices fell compared with a year ago (-0.1%) for the first time since March 2021. On a monthly basis, rising prices for housing rentals, international package holidays, fruiting vegetables and stone fruits contrasted with lower prices for air transport, supplementary accommodation and heating oil. Core inflation printed at 0.1% M/M and +0.5% Y/Y. Goods prices rose 0.2% M/M to be down 1.9% Y/Y. Services inflation stood at 0.1% M/M and 1.1% Y/Y. Today’s CPI print leaves the Swiss National Bank little choice but to further reduce its policy rate, from 0.25% to 0% at the June 19 policy meeting. The Swiss franc loses slightly ground today, trading at EUR/CHF 0.9365.

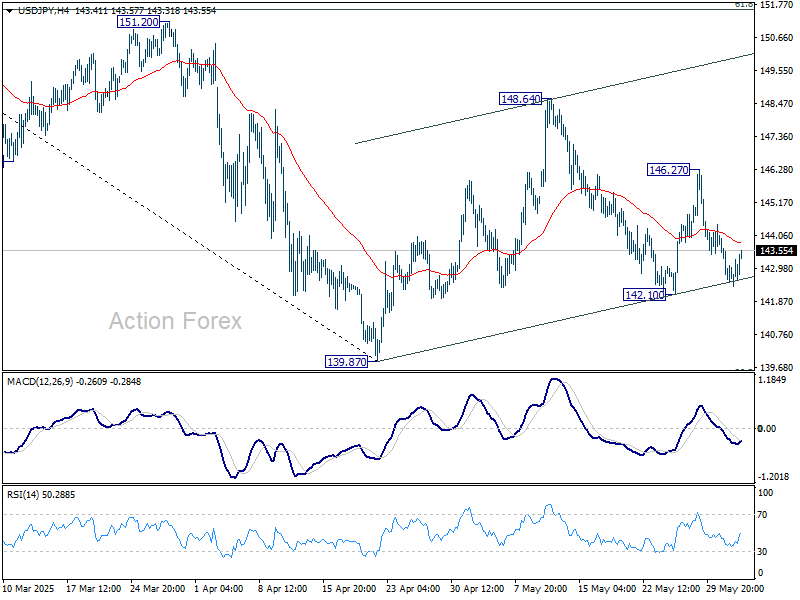

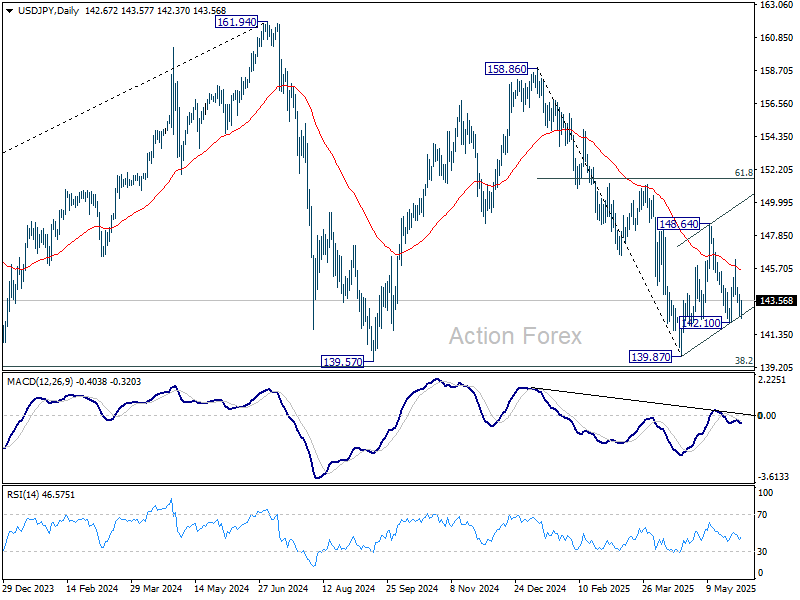

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.16; (P) 143.08; (R1) 143.61; More...

No change in USD/JPY's outlook and intraday bias remains neutral. On the upside, above 146.27 will target 148.64 resistance first. Firm break there will resume the rebound from 139.87. Nevertheless, break of 142.10 will bring deeper fall back to 139.87 low.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

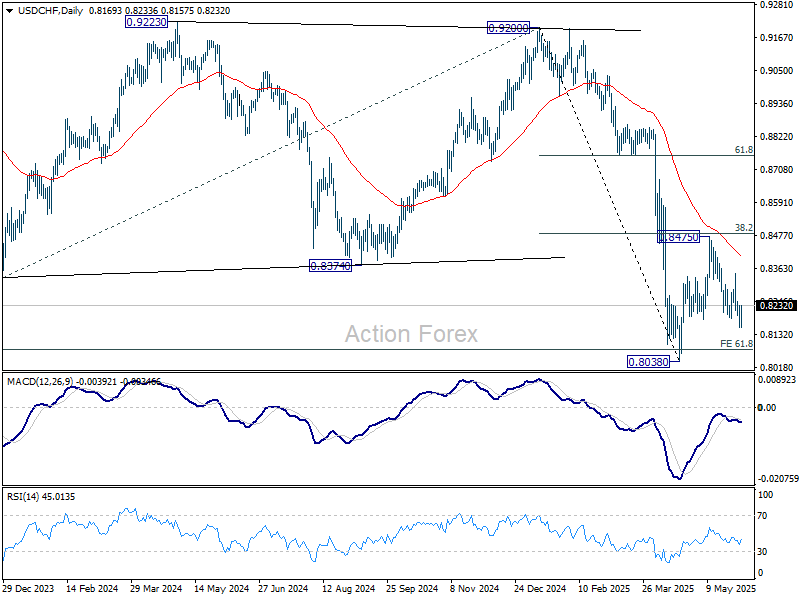

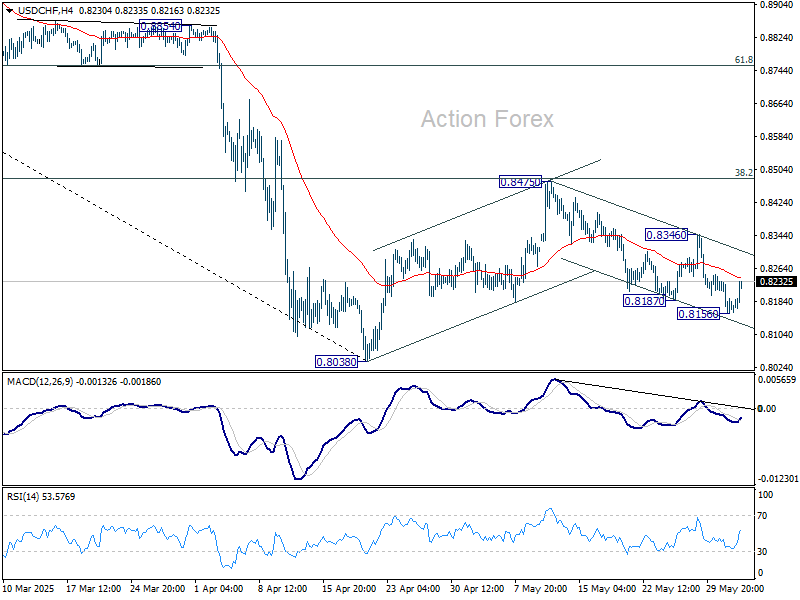

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8139; (P) 0.8189; (R1) 0.8222; More….

Intraday bias in USD/CHF is turned neutral with current recovery. Fall from 0.8475 could still extend lower, and break of 0.8156 will target 0.8038 low. But strong support should be seen from there to bring rebound, at least on first attempt. On the upside, break of 0.8346 resistance will extend the corrective pattern from 0.8038 with another rising leg.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8732) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.