Sample Category Title

WTI Oil Futures Slide on OPEC Supply Outlook

- WTI Crude Oil pulls below 64.00 on supply increase prospects.

- Technical risk tilted to the downside; support at 60.50 tested.

WTI crude oil futures were rejected near the 64.00 psychological level on Wednesday and moved lower, as reports of a significant upcoming output hike by OPEC outweighed concerns about a potential Israeli strike on Iranian nuclear facilities.

From a technical standpoint, the short-term bias is leading bearish. The RSI is retreating below its neutral 50 mark, and the stochastic oscillator is falling but still positioned well above the 20 oversold threshold. This suggests that selling pressure could persist, especially if the 20-day simple moving average (SMA), currently near 60.50, fails to hold. A breakdown at that level could extend the decline toward the 57.50 support area.

Further losses could target the critical double bottom 53.94–55.00 zone, where the 61.8% Fibonacci retracement of the 2020–2022 uptrend coincides with the long-term descending trendline from 2023.

Conversely, if the price manages to break decisively above the 64.00–64.93 resistance band, the next obstacle could emerge around the tentative resistance trendline at 67.00. The 200-day SMA may also act as a barrier ahead of the 69.92 level.

In summary, downside risks remain prominent in the WTI crude oil market, despite the ongoing broad consolidation phase. A drop below 60.50 could play the next bearish episode.

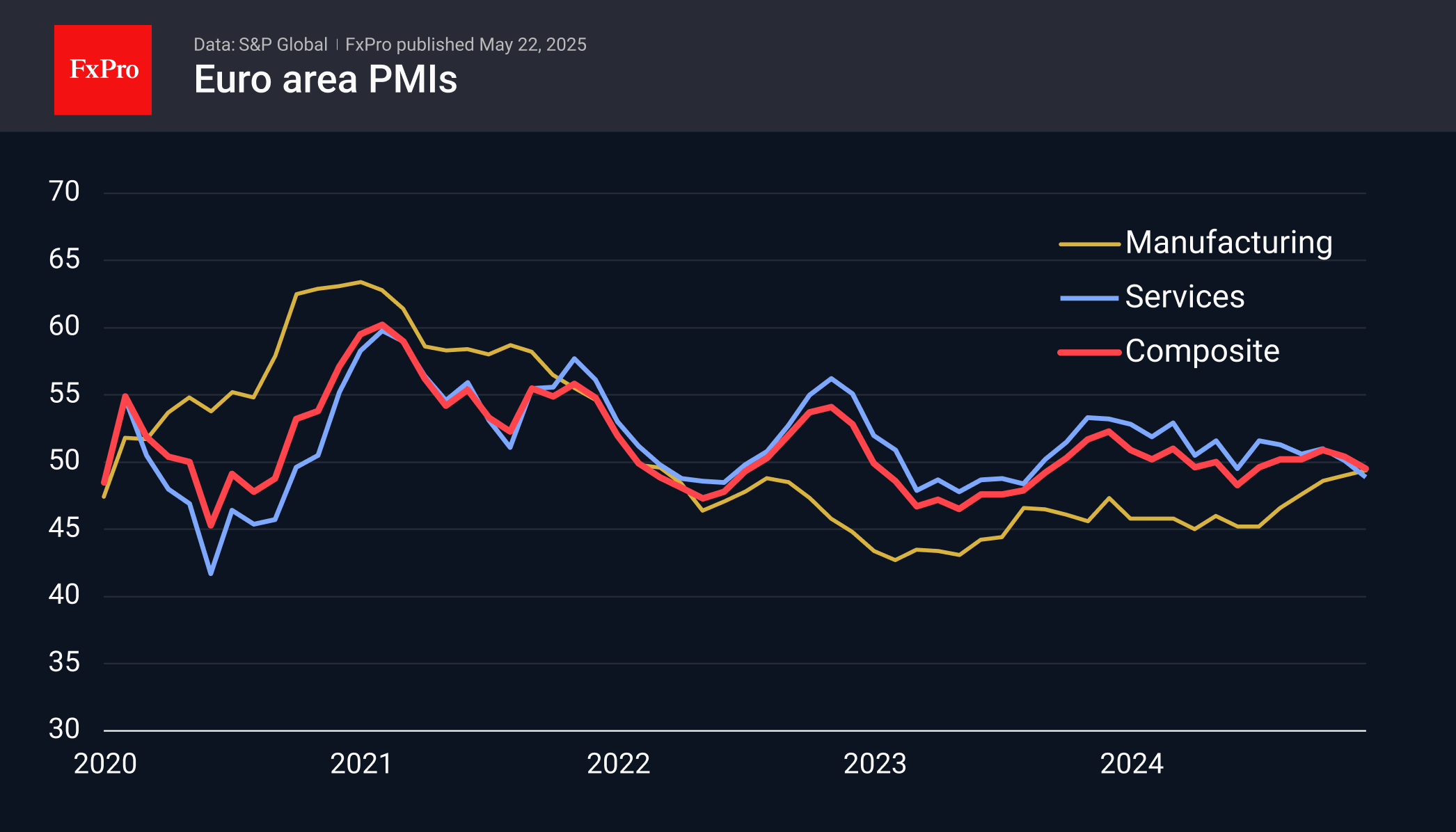

Services Dragging Eurozone PMI Down

Flash Eurozone business activity moved into contractionary territory due to a sharp dip in the services sector.

The Euro-region manufacturing PMI rose to 49.4, the highest reading since August 2022, but still in contractionary territory as it is below 50. The index shows that the sector has been gaining momentum since last December, which can easily be linked to expectations of lavish spending by the new German government and potential repetition by other countries.

Interestingly, the strengthening euro is still not hurting manufacturers. We think it is a fallacy to think that eurozone manufacturers are sensitive to such 10% exchange rate fluctuations. Our observations suggest the opposite: the appreciation of the exchange rate does not hurt the economy, lowering energy costs and generally boosting demand.

The services sector, on the other hand, is not doing so well. The index has fallen back to 48.5, its lowest level since January 2024, and has been drifting downwards all this time. With this setback, the composite index went into contraction territory, below 50. The service sector and the general state of the economy were worse than economists’ expectations, pulling the Euro.

EURUSD pulled back to 1.1300, losing about a third of a cent from intraday highs before publication. The same area worked as strong resistance, and the latest data favoured the bears in the pair.

RBA’s Hauser: Post-tariff China outlook positive but incomplete

In a speech focused on his recent visit to China following the sweeping tariff shifts of “Liberation Day”, RBA Deputy Governor Andrew Hauser noted there was a sense of "strong hand" in managing the economic fallout from US-imposed tariffs. Additionally, Australian firms operating in China perceived "opportunities amidst the risks", as trade patterns began to shift.

However, Hauser was quick to stress that this view was inherently limited, anchored to a moment in time and shaped by a single national perspective.

Hauser laid out four key caveats. First, global tariff settings remain fluid, and data on their real-world economic effects is just beginning to emerge. Second, the assessments he heard may prove overly optimistic, domestic stimulus in China may underperform, and public tolerance for economic pain may be lower than expected.

Third, indirect “general equilibrium” effects could emerge, including the possibility of intensified competition from Chinese firms offloading excess supply originally intended for US markets. While sectoral overlap with Australia is limited, it is a concern shared across the Asia-Pacific region.

Finally, Hauser acknowledged the broader strategic uncertainties at play—factors beyond economics that could shape Australia's position.

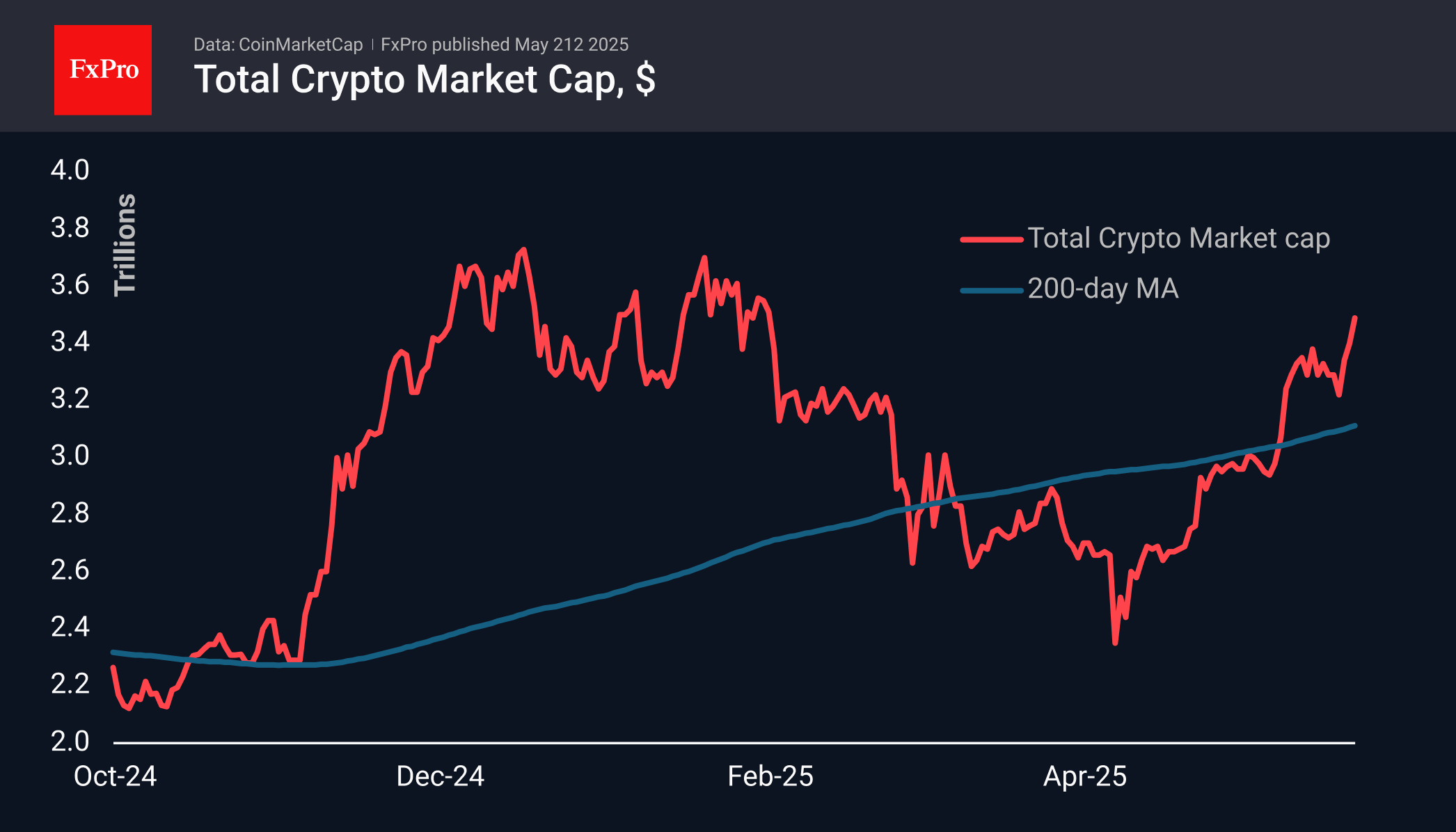

Bitcoin Confidently Updates Highs

Market Picture

Market capitalisation topped $3.5 trillion on Thursday morning, later retreating slightly below that round level. Interestingly, Bitcoin’s all-time highs have yet to spark FOMO. The historical highs of the first cryptocurrency keep the market positive, but the growth rate of altcoins is still commensurate with the dynamics of BTC.

The sentiment index at 72 remains on the cusp of entering the area of extreme greed, which often corresponds to periods of robust market growth when FOMO has yet to turn on, making growth vulnerable to corrective pullbacks.

Bitcoin was climbing to $111.8K on Thursday morning, recording a new all-time high. This slip was followed by a tidy giveaway, with early buyers cautiously locking in profits. Working against Bitcoin right now is the exit from risk assets in financial markets due to the sell-off in US government bonds. In such an environment, institutional clients could be net sellers, although at first glance, cryptocurrencies may appear to be a safe haven.

News Background

Bitcoin’s $3 billion rise in realised bitcoin capitalisation overnight to new records reflects the continuation of the accumulation phase ahead of another momentum over the coming week, CryptoQuant noted.

States are investing in the first cryptocurrency through shares of Strategy, the largest public holder of BTC, according to Standard Chartered. Government entities increased their investment in Strategy stock in the first quarter.

The Texas House of Representatives approved a bill to create a strategic bitcoin reserve. The document has been sent to the governor for his signature. Texas is likely to become the third US state after New Hampshire and Arizona with such an initiative.

Strive Asset Management, a company linked to Vivek Ramaswamy, intends to acquire 75,000 BTC at a discount from the bankrupt Mt. Gox exchange to create a bitcoin reserve.

River said the US could be a major beneficiary of bitcoin’s growth due to its regulatory advantages, advanced mining infrastructure, and state-level support. The country already controls 79.2% of global assets in spot bitcoin ETFs and more than 38% of the BTC network hash rate. Nearly 50 million Americans own bitcoins.

Bitcoin Hits All-Time High, Surges Above $110K

As shown on the BTC/USD chart, the Bitcoin price has broken above the $110K mark, setting a new all-time high around $111,800.

This move highlights the strength of the leading cryptocurrency, which has surged nearly 50% in just over one and a half months, rising from a low near $75K recorded in early April.

What’s Driving Bitcoin’s Price Higher?

One of the key drivers is weakness in the US dollar. In April, the US Dollar Index hit its lowest level in three years and remains close to that low at the end of May. According to Reuters, downward pressure on the dollar is being caused by:

→ a lacklustre Treasury bond auction yesterday;

→ currency traders’ expectations surrounding the potential impact of President Donald Trump’s proposed legislation on significant tax and spending cuts.

On the other hand, crypto enthusiasts welcomed the news that the Texas House of Representatives has passed a bill allowing state investments in Bitcoin. Once signed by the governor, the law could make Texas the first US state to hold Bitcoin in its reserves.

Technical Analysis of the Bitcoin Chart

In our previous analysis on 8 May, we:

→ extended the long-term upward channel (marked in blue);

→ suggested that momentum had shifted in favour of the bulls and focused on how BTC/USD might behave when testing the key psychological level of $100K.

As indicated by the arrow, the break above $100K was strong — marked by a wide bullish candle that closed at its high — after which the bulls continued to push BTC/USD higher. This has resulted in the formation of a new ascending channel (shown in black).

Reaching a new all-time high may prompt some buyers to take profit following the May rally, which could lead to a correction — potentially down towards the dotted black line, which runs parallel to the current black channel but sits lower.

In the most optimistic scenario, the price of the leading cryptocurrency could rise toward the upper boundary of the long-standing blue channel, whose relevance we have been highlighting for many months.

FXOpen offers the world's most popular cryptocurrency CFDs*, including Bitcoin and Ethereum. Floating spreads, 1:2 leverage — at your service. Open your trading account now or learn more about crypto CFD trading with FXOpen.

*Important: At FXOpen UK, Cryptocurrency trading via CFDs is only available to our Professional clients. They are not available for trading by Retail clients. To find out more information about how this may affect you, please get in touch with our team.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

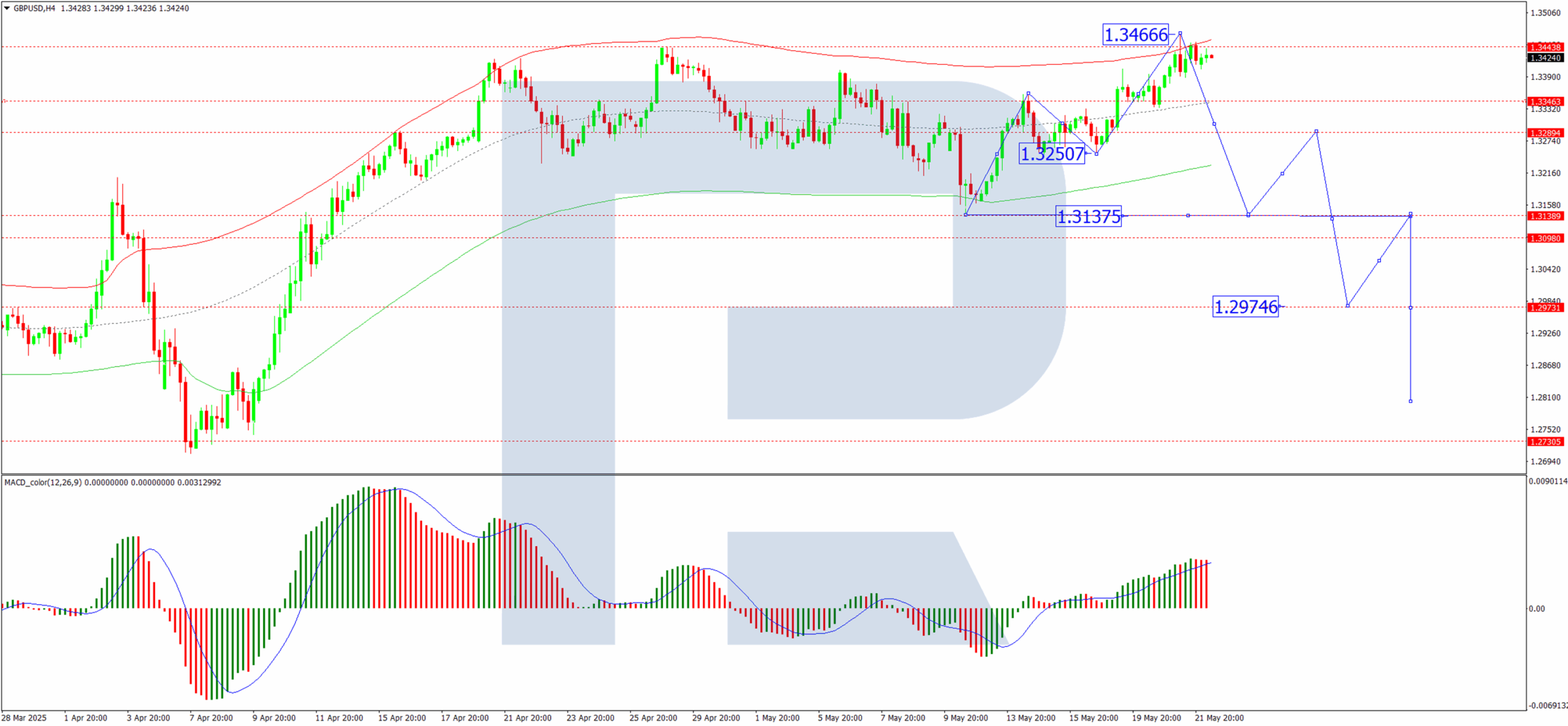

Sterling Strengthens Weak US Dollar and UK Inflation Provide Support

The GBP/USD pair continues its upward trajectory, reaching 1.3429 by Thursday. It is now trading just below yesterday’s peak, its highest level since February 2022.

Key drivers behind GBP/USD’s rise

The rally follows the release of stronger-than-expected UK inflation data. The annual Consumer Price Index (CPI) accelerated to 3.5% in April, the highest reading since January 2024, exceeding both market forecasts (3.3%) and the Bank of England’s projection (3.4%). Contributing factors included:

- An increase in Ofgem’s energy price cap

- Higher vehicle tax rates

Notably, services sector inflation surged from 4.7% to 5.4%, signalling persistent underlying price pressures.

Market expectations for monetary policy easing have adjusted significantly. Investors now anticipate just one 25-basis-point rate cut by the end of 2025. The likelihood of a rate cut in August has fallen from 60% to 40%.

The Bank of England reduced interest rates by 25 basis points in May, although policymakers were divided on the decision.

Technical analysis: GBP/USD

H4 Chart:

- The GBP/USD pair completed an upward wave, peaking at 1.3466

- Today, we expect consolidation below this level

- A downward breakout could initiate a decline towards 1.3131, with 1.3300 acting as the first target

- The MACD indicator supports this view, with its signal line exiting the histogram zone and trending lower

H1 Chart:

- The pair reached 1.3466 before correcting to 1.3388, establishing a consolidation range

- A downward breakout today could see a move towards 1.3300

- The Stochastic oscillator confirms this scenario, with its signal line below 80 and pointing decisively downward towards 20

Conclusion

Sterling’s strength persists amid weaker US dollar dynamics and persistent UK inflation. While technical indicators suggest a potential pullback, the broader trend remains influenced by monetary policy expectations and economic data.

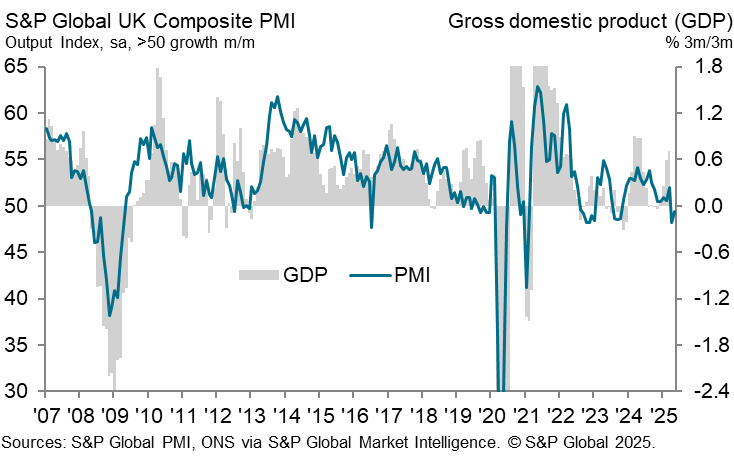

UK PMI composite ticks up to 49.4, price pressures ease from April spike

UK PMI Services rose modestly from 49.0 to 50.2, while Manufacturing PMI edged lower from 45.4 to 45.1. As a result, the Composite PMI ticked up from 48.5 to 49.4, still below the 50-mark that separates expansion from contraction.

According to S&P Global’s Chris Williamson, business confidence has improved since April, helped in part by easing trade tensions. However, output across the private sector shrank for a second consecutive month, suggesting that the UK economy may be slipping into contraction for Q2.

On a more encouraging note, inflationary pressures appear to have cooled significantly from April’s spike. This moderation in price growth, combined with lackluster output and emerging job losses, strengthens the case for further monetary easing by BoE in the coming months.

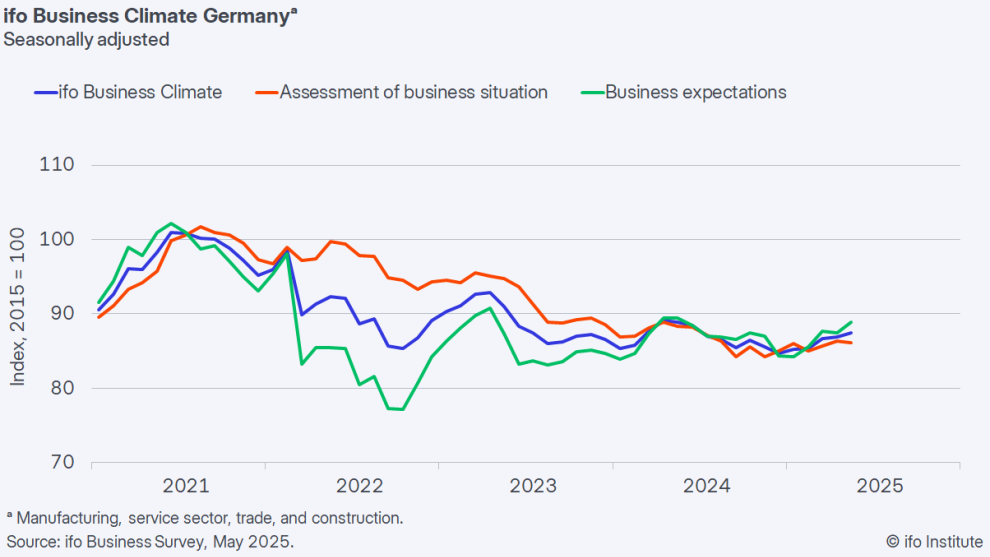

German Ifo rises to 87.5, economy stabilizing with uncertainty eased

Germany’s Ifo Business Climate Index rose to 87.5 in May, up from 86.9 in April, offering cautious optimism that the economy may be stabilizing.

The improvement was driven by a notable rise in the Expectations Index, which climbed from 87.4 to 89.9, a sign that firms are growing more confident about future conditions. However, the Current Situation Index dipped slightly from 86.4 to 86.1.

The Ifo Institute noted that "sentiment among German companies has improved" and that the recent surge in uncertainty has begun to ease.

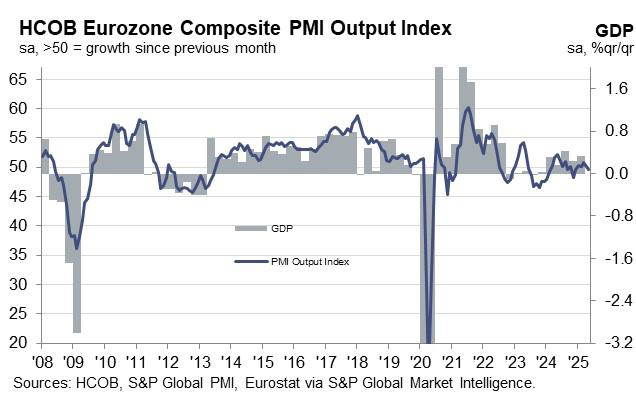

Eurozone PMI composite falls to 49.5, services falter, manufacturing holds tentatively

Eurozone’s private sector returned to contraction in May, with PMI Composite falling from 50.4 to 49.5, a six-month low. The drag came from the services sector, where the PMI dropped from 50.1 to 48.9, its weakest reading in 16 months. While the manufacturing index rose modestly from 49.0 to 49.4, marking a 33-month high, it remained in contractionary territory.

According to HCOB Chief Economist Cyrus de la Rubia, the region’s economy “cannot seem to find its footing,” as growth signals remain elusive and sentiment subdued.

The modest improvement in manufacturing may reflect front-loaded activity as firms seek to get ahead of US tariffs, rather than underlying demand strength. However, the downturn in services, typically more domestically oriented and less exposed to global trade, raises concern about internal demand softness.

For the ECB, the numbers are "likely to leave it with mixed feelings". While service sector inflation appears to be moderating, input costs — likely driven by wages — are ticking higher again. Manufacturing purchase prices, by contrast, continue to fall.

Bad US Auction Weighed on Wall Street and Dollar

Markets

Yesterday’s US 20-yr $16bn bond sale was a rough one. The auction tailed 1.2 bps vs the 5.035% WI yield with lower-than-average demand. US yields ripped higher, extending earlier gains. Net daily changes varied between +4.8 bps in the 2-yr to 12.9 bps for the 20-yr. The US 30-yr yield added 12.3 bps to 5.09% and rapidly closes in on the 2023 high of 5.17%. The 5% coupon, the highest since the 20-yr tenor was reintroduced in 2020, wasn’t considered enough and is a writing on the wall. Investors shun long-term US debt given fiscal risks to an already unsustainable deficit situation. Conditions ahead of the auction were suboptimal, to put it mildly. Shortly before the sale, House Speaker Mike Johnson said there was agreement on one of the last remaining hurdles (SALT, Medicaid), potentially paving the way for Trump’s bill to be approved by the House later today. Adding to the negative vibes was a Japanese sale that flopped on Tuesday. The tenor was the same, market concerns similar. It launched Japanese yields with maturities from 20 year on to the highest levels since at least 25 years. That prompted calls on the Bank of Japan to revise its bond buying taper plans, specifically those affecting the long end of the curve. But one of the most dovish BoJ board members said this morning he currently sees no need to. In the plan laid out last year and which is up for an interim review at June’s policy meeting, monthly buying should halve to JPY 3tn by March 2026. Japanese yield again add several bps. The bad US auction weighed on Wall Street with losses mounting to 2% (Dow Jones) as well as on the dollar. The trade-weighted index closed sub 100, EUR/USD rose to 1.133. USD/JPY eased to 143.7 and drops further to 143.3 in Asian trading this morning. JPY largely ignores an understanding between finance minister Kato and his US counterpart Bessent that FX rates should be determined by the market. Both met in the sidelines of the G7 summit in Canada and ongoing FX talks with the likes of South Korea and Taiwan is fueling speculation of the US using tariffs to arm-wrestle the broader region in letting local currencies strengthen.

The calendar has the sole important economic data for this week on offer: PMI business confidence indicators. We suspect the European reading to come in to the better side of expectations as trade fever eased over the last couple of weeks. We keep a close eye at the price subseries. Input cost increased slowed last month but selling prices continued to pick up. The combination of improving economic conditions and still-strong price pressures keeps European yields supported. They have been joining the broader move higher, particularly at the long end of the curve. The 30-yr swap is the one to watch for today, with the yield currently testing the 1.5 year high seen in March. We expect EUR/USD to move higher with 1.1573 (April high) serving as the first technical resistance level.

News & Views

Lower growth than previously expected slowed the efforts of fiscal consolidation by New Zealand, the proposal of the new budget showed this morning. The government expects a budget deficit at 2.6% of GDP in the fiscal year 2025/2026 (NZD 12.1 bln), compared to the expected 2.3% at in December last year. The government intends to return to a budget balance in the fiscal year 2028/29. Treasury takes a 1.2% growth into account for 2025 (from 2.1%) before accelerating to 3.1% in 2026. Both are still higher than the projections of the central bank. The lower deficit reduction plan also slowed the decline in the government debt ratio. This is expected to peak at 46.0% in 2027/28. In a first comment after the budget presentation, rating agency S&P indicated that the elevated fiscal and current account deficits weigh on the credit rating. S&P nevertheless expects that the country’s public debt will stabilize at a favourable level compared to most rating peers. New-Zealand has AA+ rating with a stable outlook. The kiwi dollar eases slightly this morning against the dollar to NZD/USD 0.5925.

The Japanese composite PMI in May slipped back in contraction territory, from 51.2 in April to 49.8 in May. The decline in the overall index was driven by a further contraction in out in the manufacturing sector (48.0 from 48.9) while activity in the services sector slowed materially from 524 to 50.4. S&P Global comments that demand conditions looked more fragile, with new business across both manufacturing and service sectors falling for the first time in nearly a year and foreign demand declining for the second straight month. Cost pressures remained elevated in May, but there were tentative signs that input price inflation is cooling. Business confidence is the second lowest recorded since the initial wave of the COVID-19 pandemic, due to uncertainty on the future trade environment and foreign demand clouding the outlook for the year ahead.