Sample Category Title

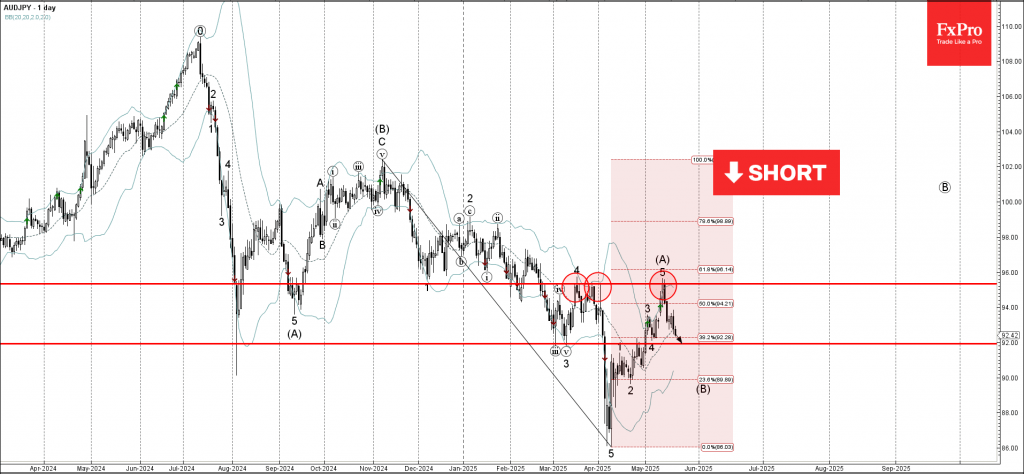

AUDJPY Wave Analysis

AUDJPY: ⬇️ Sell

- AUDJPY reversed from key resistance level 95.30

- Likely to fall to support level 92.00

AUDJPY currency pair recently reversed down from the key resistance level 95.30 (which has been reversing the price from the middle of March).

The downward reversal from the resistance level 95.30 started the active intermediate correction (B).

Given the strength of the resistance level 95.30 and clear daily downtrend, AUDJPY currency pair can be expected to fall to the next support level 92.00.

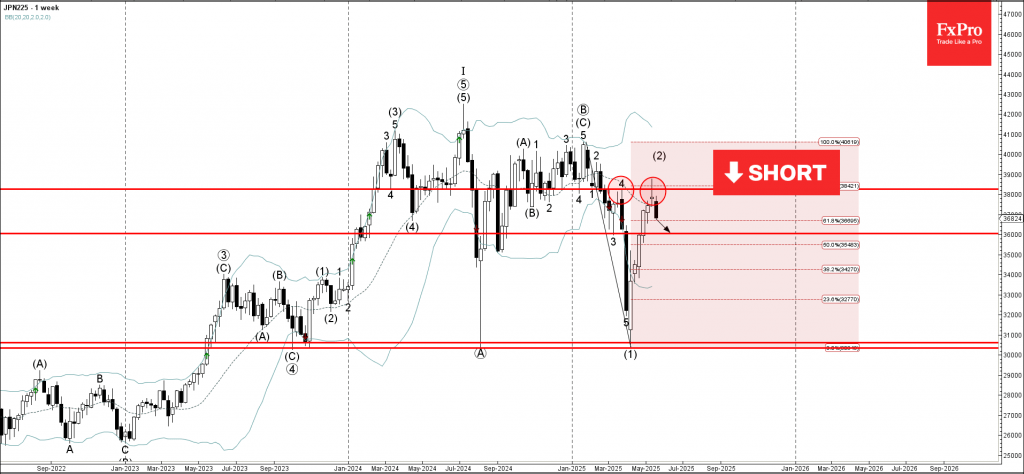

Nikkei 225 Wave Analysis

Nikkei 225: ⬇️ Sell

- Nikkei 225 reversed from the resistance level 38280.00

- Likely to fall to support level 36000.00

Nikkei 225 index recently reversed down from the pivotal resistance level 38280.00 (former top of wave 4 from the start of this year).

The downward reversal from the resistance level 66.00 created the daily Japanese candlesticks reversal pattern, Shooting Star.

Given the strength of the resistance level 38280.00, Nikkei 225 index can be expected to fall to the next support level 36000.00.

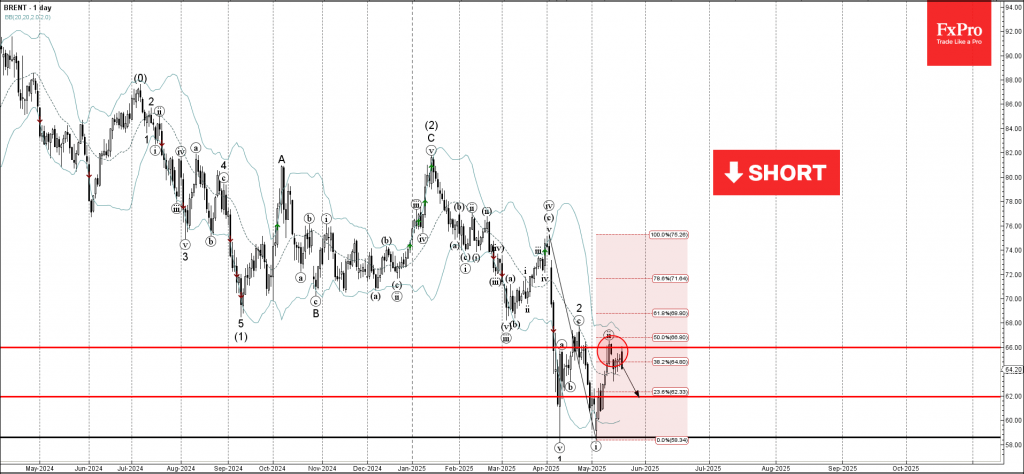

Brent Crude Oil Wave Analysis

Brent crude oil: ⬇️ Sell

- Brent crude oil reversed from key resistance level 66.00

- Likely to fall to support level 62.00

Brent crude oil recently reversed down from the key resistance level 66.00, which has been reversing the price from the start of April, as can be seen from the daily Brent crude oil chart below.

The downward reversal from the resistance level 66.00 created the daily Japanese candlesticks reversal pattern Evening Star.

Given the clear daily downtrend, Brent crude oil can be expected to fall to the next support level 62.00.

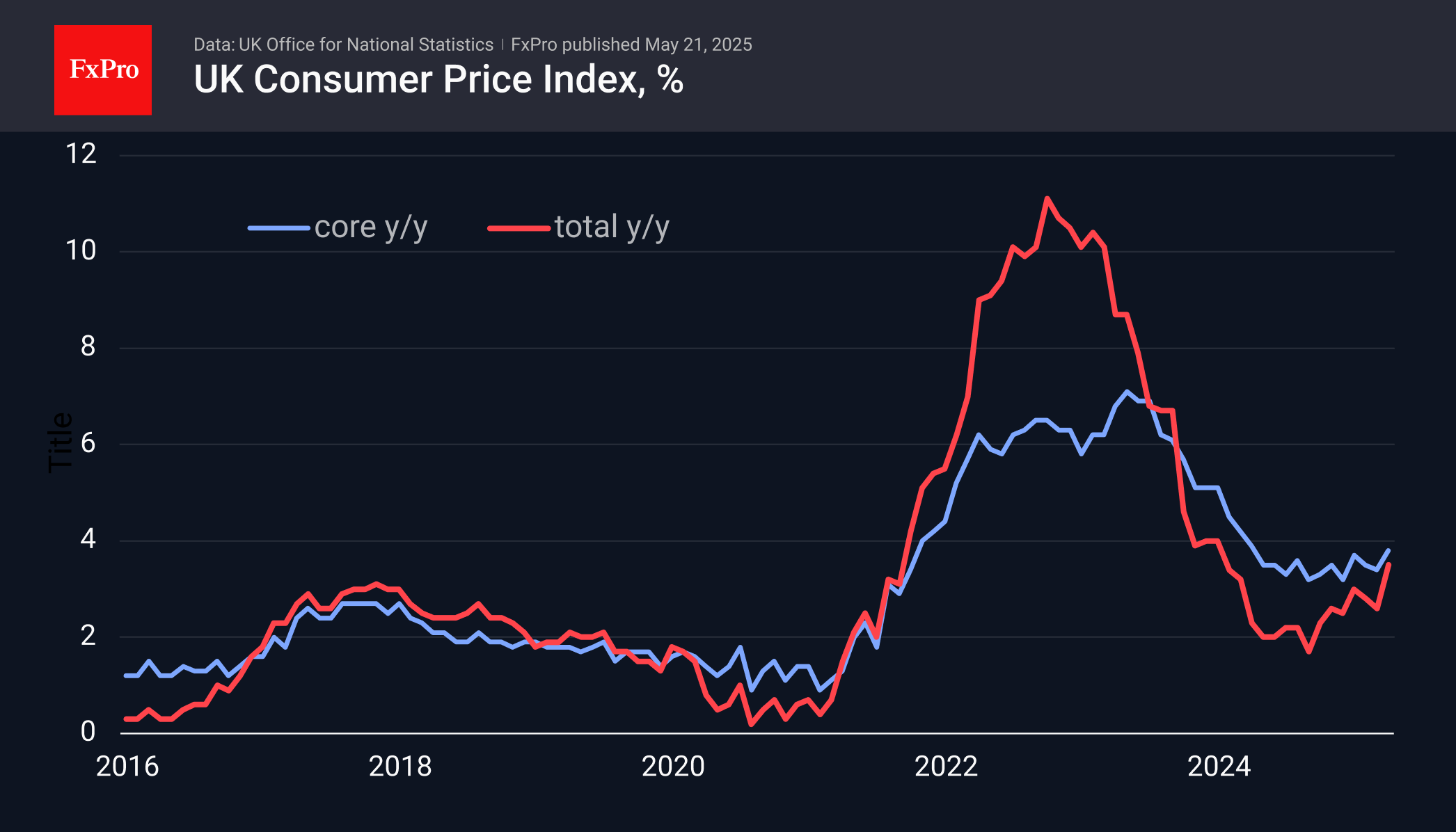

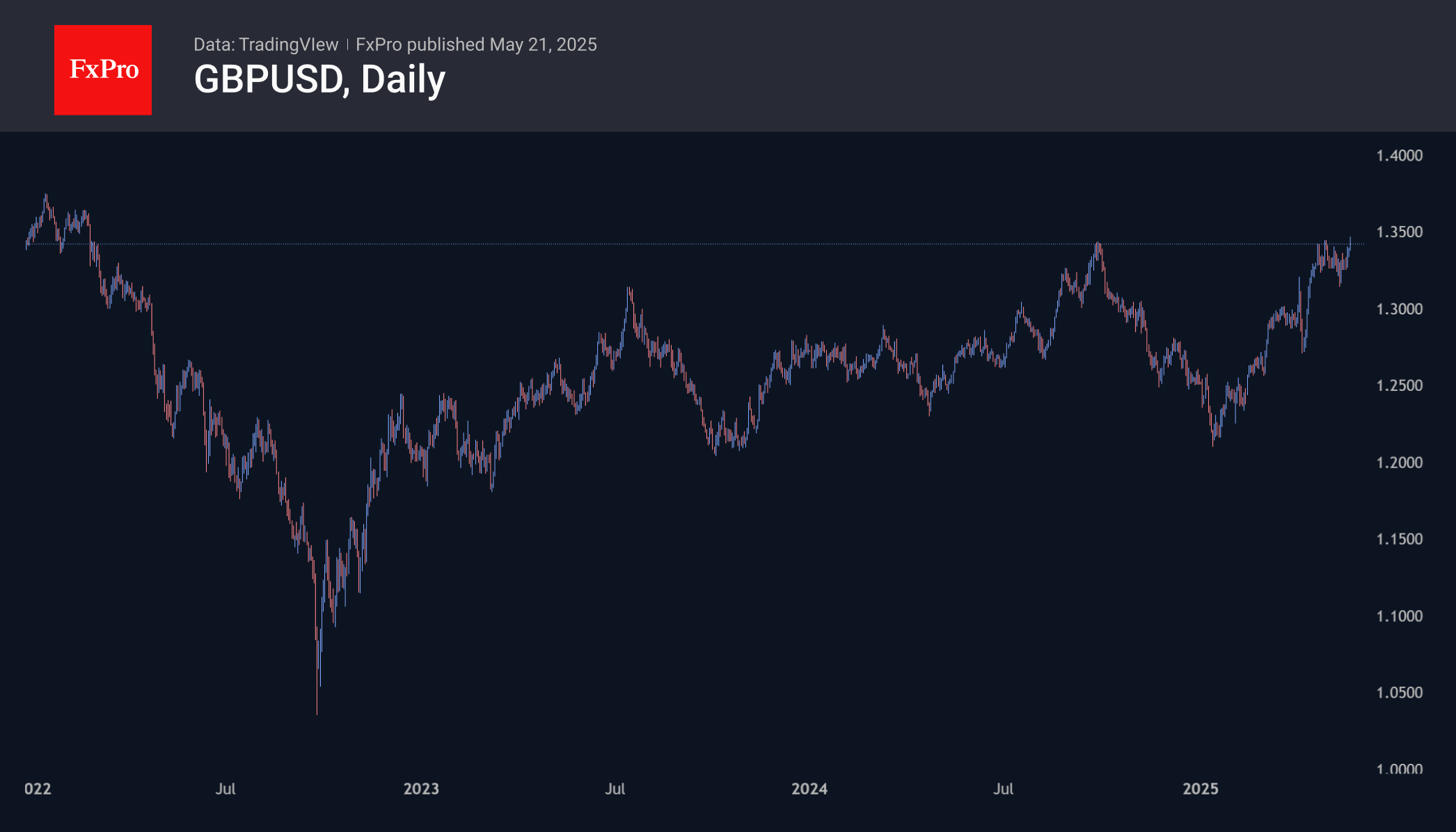

UK’s Inflation Surge Puts BoE Closer to Fed

UK inflation accelerated more strongly than forecast, casting doubt on the likelihood of a rate cut by the Bank of England any time soon. The overall consumer price index increased 1.2% in April, the strongest monthly jump since April 2022. The annual rate of growth accelerated from 2.6% to 3.5%, the highest since January 2024. Core inflation accelerated to an annual rate of 3.8%, the highest in 13 months.

What is most worrying about the current situation is the persistently positive trend in inflation. The overall rate hit a low of 1.7% in September 2024, confirming the correctness of the Bank of England’s decision to kick off the monetary easing cycle shortly before. Further policy easing will now require more justification from the central bank.

Housing, household services, leisure, and culture are the drivers of inflation in Britain right now. These are difficult categories for monetary policy. Unlike commodity and energy prices, we should not expect markets to cool sharply. In these circumstances, the Bank of England needs to pursue a policy of cooling economic growth.

This is good news for the pound, so nothing is surprising in GBPUSD updating its three-year highs. Nevertheless, it’s not easy for the pound to move upwards given the 11% rise from the lows at the start of the year. The latest news is a good signal to get ready for the bulls. However, for the rally to resume, it is still better to wait for hawkish signals from the Bank of England that it is ready to take a pause, like the Fed is now.

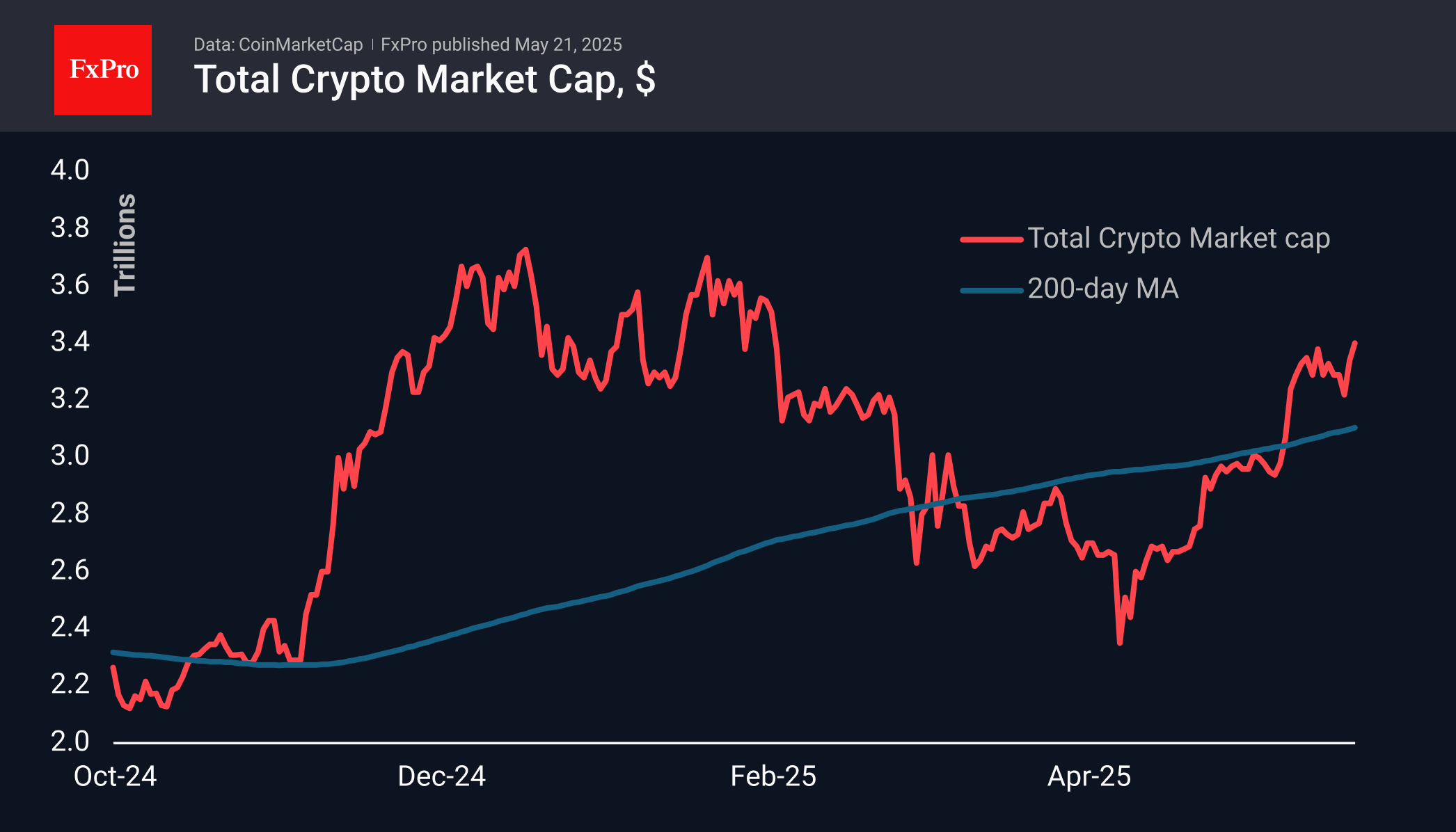

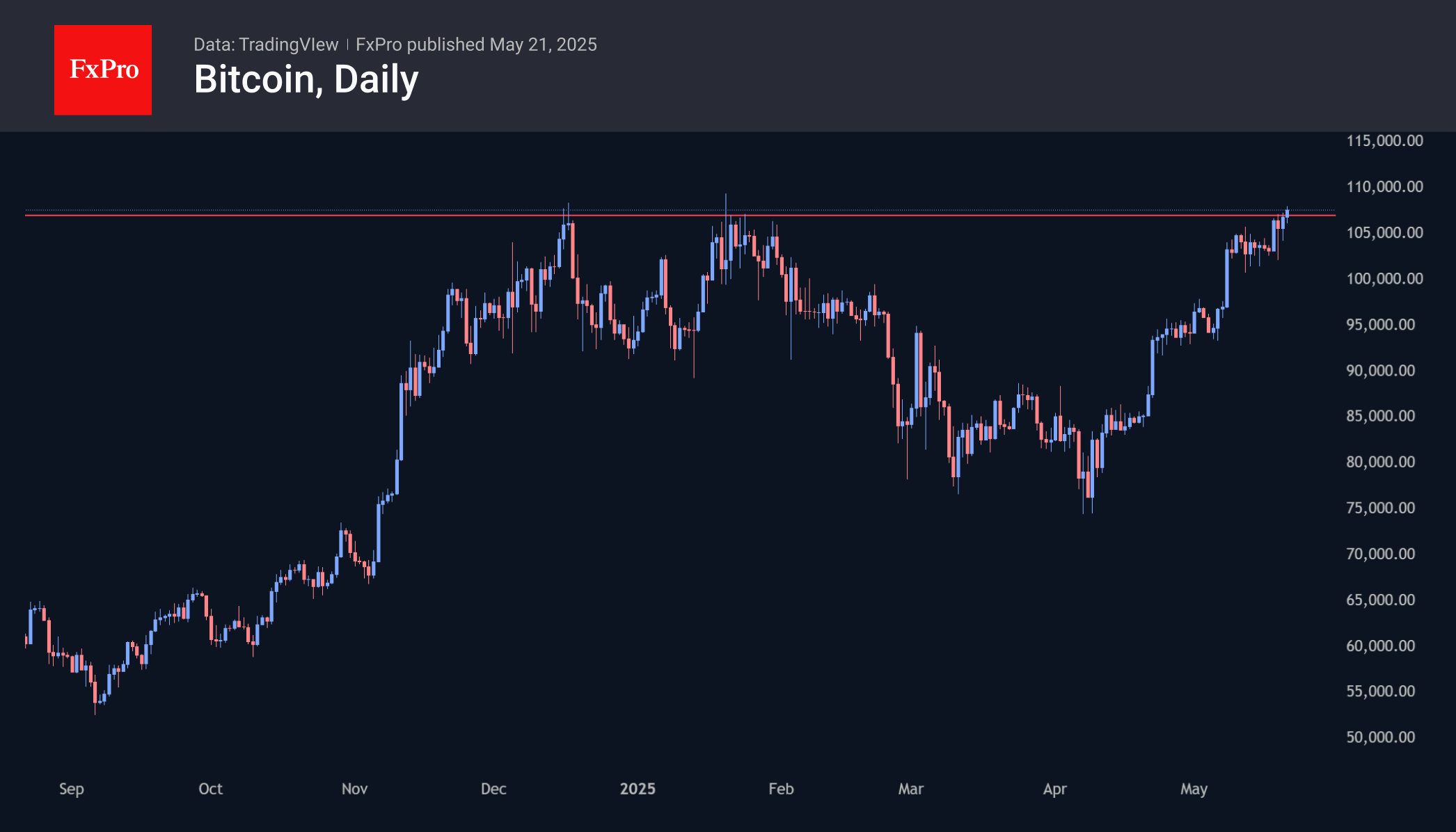

Bitcoin Close to the Top

Market Picture

Market capitalisation has risen 2% in the last 24 hours to $3.37 trillion, 8.5% below January’s all-time peaks. However, Bitcoin buyers are showing more confidence, trading above the $107k area (+2.9%). Ethereum and many other altcoins saw stronger intraday gains but still have a lot to recover after retreating significantly following the broader market pullback after Trump’s inauguration.

Bitcoin is forming its fourth consecutive daily growth candle. Bulls continue their attempts to secure a foothold above the $107K level. While the first cryptocurrency has briefly reached higher levels, it has yet to establish a sustained hold above them.

Last week, there was a stabilisation around $103k, which now looks like a foundation for further growth. The realistic near-term target for the bulls looks to be the area of $113K, which would be an extension to 161.8% of the growth impulse from early May and the subsequent mini correction at the beginning of last week.

Bitcoin’s upward move is gradually waking up altcoins, although they still have considerable room to rise to previous highs, making them increasingly attractive to retail traders. The trend of a weakening dollar can also be seen as a breeding ground for growth.

News Background

On-chain signals and market data for Bitcoin remain constructive. Buying sentiment continues to support further growth, indicating that it may not yet be time to cash in, according to CryptoQuant.

Strategy bought an additional 7,390 BTC ($764.9 million) last week at an average price of $103,498 per coin. The company now owns 576,230 BTC bought at an average price of $69,726. The total investment is valued at $40.18 billion.

Major players via options have bet on Ethereum’s significant growth, said CoinDesk analyst Omkar Godbole. The strategy will yield the biggest profits if ETH rises to $6,000 or higher by 26 December.

The Binance exchange has filed a motion to dismiss FTX’s $1.76 bn lawsuit. The company’s lawyers called the claims ‘legally untenable’ and asked for the case to be dismissed.

According to Fortune, Circle’s IPO may not take place as the USDC issuer is in talks with Coinbase and Ripple to sell the business for at least $5bn.

Sunset Market Commentary

Markets

Investor focus remains centered on public finances as trade wars shifted to the background following the US-Sino truce. Global yield curves extend their bear steepening run with attention obviously on the US. US President Trump’s big beautiful bill cleared another hurdle today as House Republicans reached an agreement on raising the deduction cap for state and local taxes. The SALT increase paves the way to meet Republican House Speaker Johnson’s self-imposed deadline to pass the legislation in the House Rules Committee by Thursday and in the lower house by end of this week, ahead of Memorial Day. House Republicans currently hold a narrow 220-213 majority in the lower house (2 vacancies) suggesting they need everyone, also the spending hawks, on board to pass legislation. Markets rightly worry that these expansionary fiscal proposals will further damage already unsustainable public finances. US yields today add 3 bps to 5.3 bps (30-yr) as investors also eye tonight’s $16bn 20-yr Bond sale. Weak demand at a Japanese sale with a similar majority triggered a massive sell-off in JGB’s earlier this week. We believe that it’s only a matter of time before the US 30-yr yield tests the 2023 top at 5.17% and even takes it out to hit highest level since 2007. German Bund yields follow the bear steepening move with yields 2.7 bps to 6.2 bps up on the day. UK gilts even slightly underperform, especially at the front end of the curve following this morning’s April CPI report. Daily changes vary between +4.1 bps (2-yr) and +6.8 bps (30-yr). The UK 30-yr yield is only 10 bps away of reaching its highest level since 1998. Headline inflation accelerated to 1.2% M/M (vs 1% expected) with the annual number rising from 2.6% Y/Y to 3.5% Y/Y. Core and services inflation respectively surged to 3.8% Y/Y and 5.4% Y/Y, pushing expectation on the next BoE rate cut to November. Sterling failed to profit as the pressure on long term (core) bonds starts spilling to general risk sentiment. Main European indices cede 0.5% today with US stock markets opening up to 0.75% lower. USD/JPY (143.71) drifts towards the key 140 support area. EUR/USD extends this week’s rebound, from 1.1283 to currently 1.1335. Brent crude prices hold this morning’s gains on the back of CNN reports of plans of a potential Israeli attack against Irani nuclear facilities.

News & Views

South African inflation by rose 0.3% M/M and 2.8% Y/Y in April, in line with March (0.4% M/M and 2.7%% Y/Y) and marginally higher than expected. The increase was mainly due substantially higher food prices (1.3% M/M and 4% Y/Y). Fuel prices (-3.2% M/M & -13.4% Y/Y) partly offset the increase. The trimmed mean core inflation measure printed at 0.1% M/M and 3.1% Y/Y. The Reserve Bank of South Africa has an inflation target range of 3%-6% and its policy rate stands at 7.5%. Current low inflation in theory allows the SARB to cautiously ease its policy rate at the May 29 policy meeting. However, inflation might again pick up in H2. Recently, there were also indications from the Deputy Finance Minister that the government might consider lowering the SARB inflation target, but there is no consensus yet on the issue. The Government also published its third revised budget proposal. It downwardly revised the growth projection for this year from 1.9% in March to 1.4%. Growth for next year is seen at 1.6% from 1.7%. The new budget plans take into account spending cuts of ZAR 69.4bn over 3 year. The budget deficit now is seen at 4.8% from 4.6% in March and is declining to 3.8% in 2027/28. The debt to GDP ratio is expected to peak at 77.4% of GDP at the end of this year, from 76.2% at the previous proposal. After a brief weakening after Liberation Day to near USD/ZAR 20, the ZAR fully reversed these losses against the dollar, currently trading at the best levels YTD near USD/ZAR 17.9. The rand trades mainly stable after today’s budget announcement.

Swedish Riksbank deputy governor Anna Siem indicated that “monetary policy is currently well-balanced and that it is at present wise to await further information to obtain a clearer picture of the outlook for inflation and economic activity” as the erratic trade and security policy creates uncertainty both with respect to demand and inflation. In this situation, the need to wait for reliable signals should not be interpreted as a reluctance to act. “The neutral interest rate level we are starting from provides us with favourable conditions to navigate the uncertain road ahead’. At its May 08 policy meeting the RB left its policy rate unchanged at 2.25%, but signaled that inflation might be somewhat lower than previously assessed. This could still suggest a slight easing going forward.

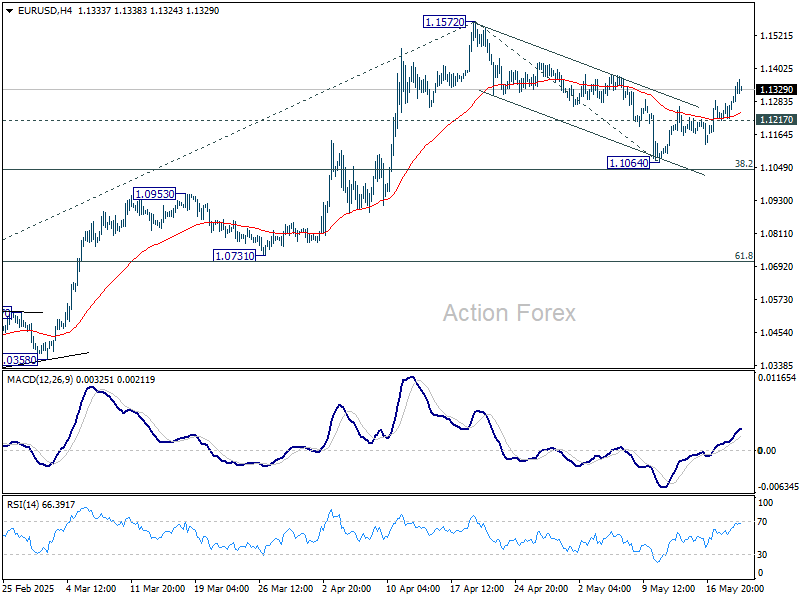

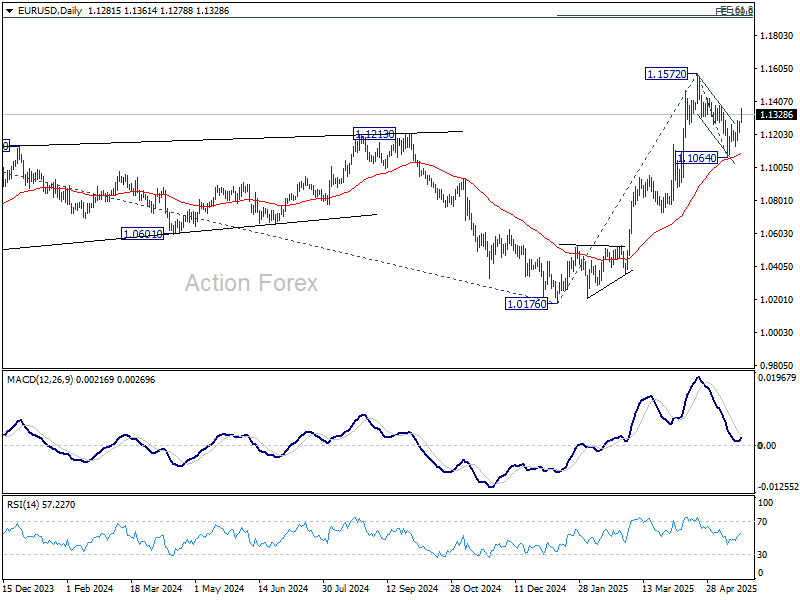

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1239; (P) 1.1263; (R1) 1.1307; More...

Intraday bias in EUR/USD remains on the upside at this point. Correction from 1.1572 could have completed at 1.1064 already. Further rise should be seen to retest 1.1572 high first. Firm break there will resume larger up trend. Next near term target will be 61.8% projection of 1.0176 to 1.1572 from 1.1064 at 1.1927. On the downside, break of 1.1217 minor support will delay the bullish case and turn intraday bias neutral again.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.

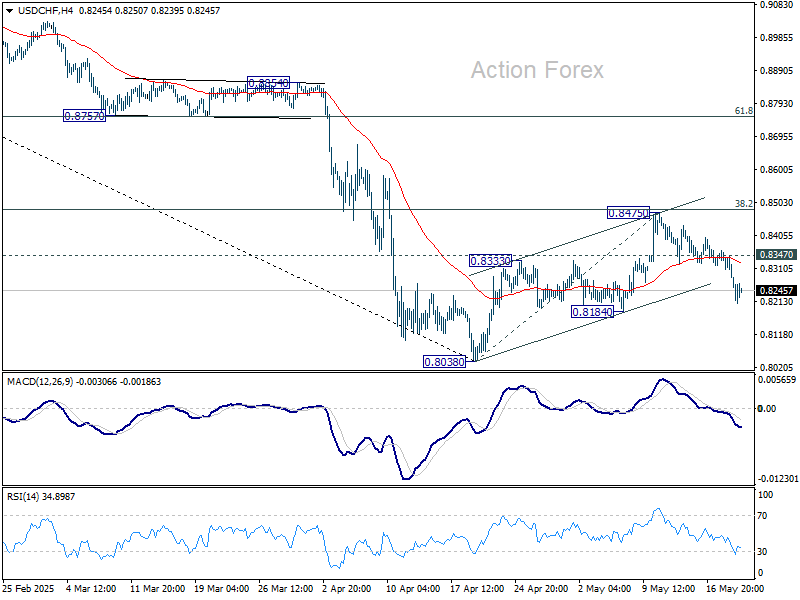

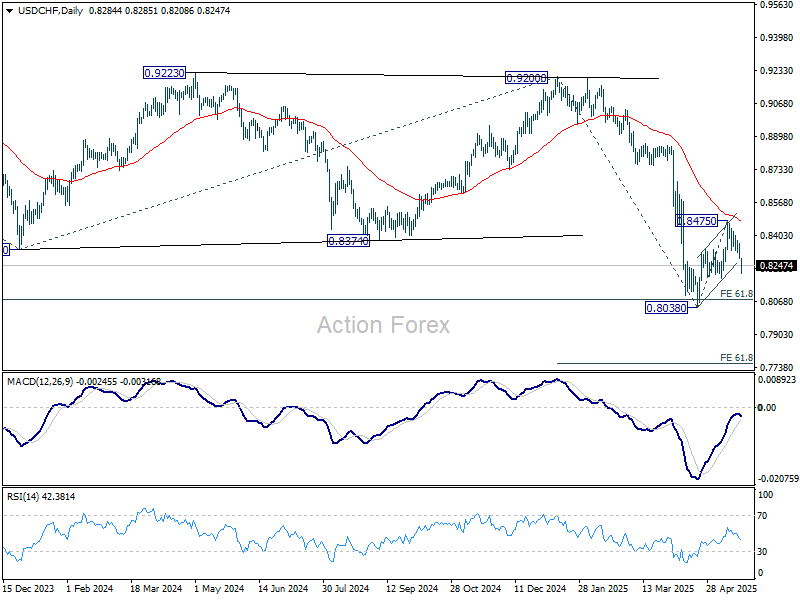

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8256; (P) 0.8309; (R1) 0.8337; More….

Intraday bias in USD/CHF remains on the downside for the moment. Corrective recovery from 0.8038 could have completed at 0.8475 already. Break of 0.8184 support will solidify this bearish case. Further break of 0.8038 will resume larger down trend to 61.8% projection of 0.9200 to 0.8038 from 0.8475 at 0.7757 next. On the upside, above 0.8347 minor resistance will delay the bearish case and turn intraday bias neutral again first.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8765) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

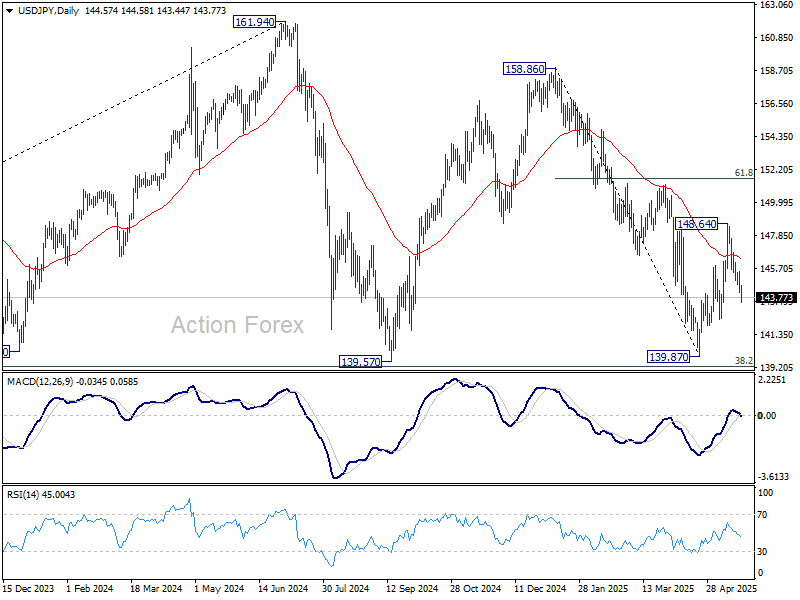

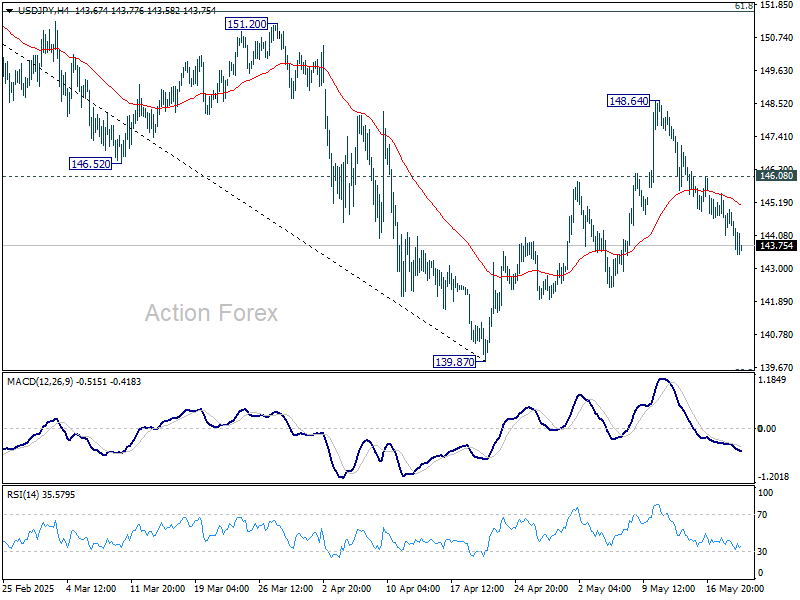

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.89; (P) 144.70; (R1) 145.31; More...

Intraday bias in USD/JPY stays on the downside at this point. Rebound from 139.87 could have completed as a correction to 148.64 already. Deeper fall would be seen back to retest this support. For now, risk will stay on the downside as long as 146.08 minor resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.