Sample Category Title

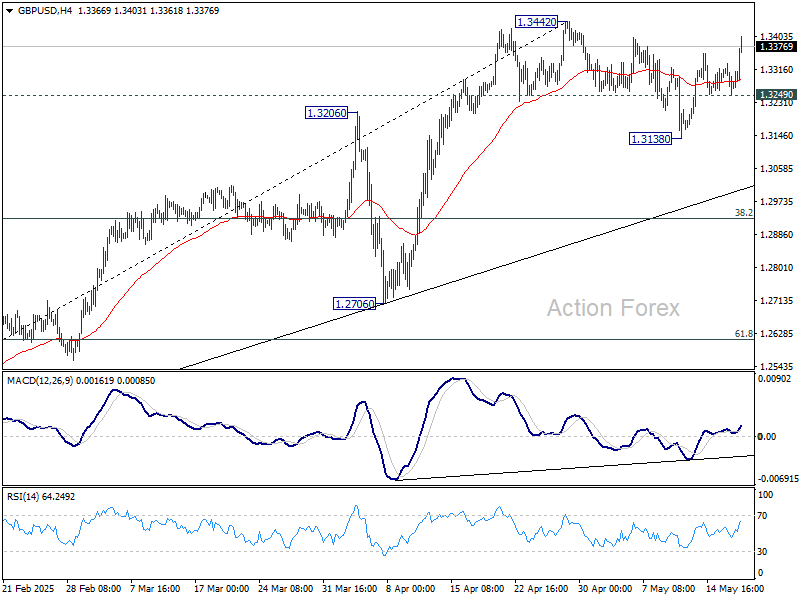

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3242; (P) 1.3288; (R1) 1.3325; More...

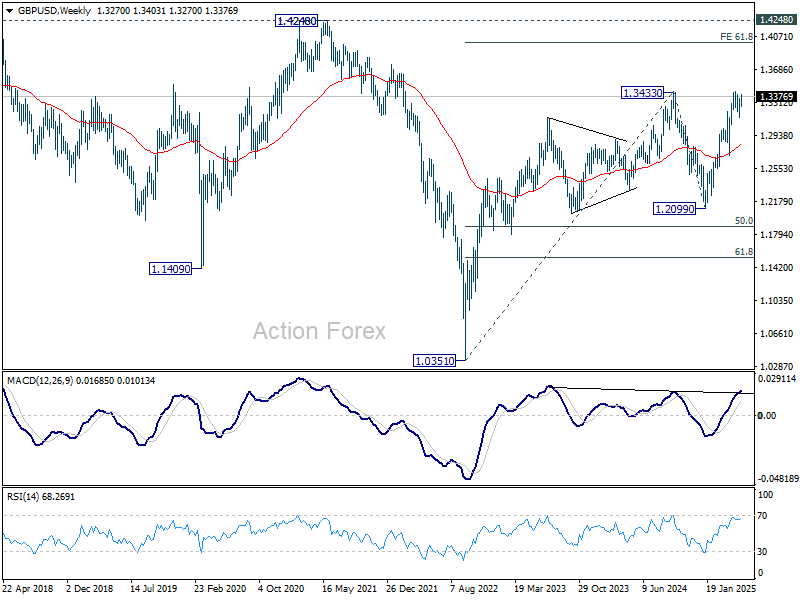

Immediate focus is now on 1.3433/42 key resistance zone as rebound from 1.3138 resume. Decisive break there will confirm larger up trend resumption. On the downside, though, below 1.3249 support will extend the corrective pattern from 1.3442 with another falling leg.

In the bigger picture, up trend from 1.3051 (2022 low) is still in progress. Decisive break of 1.3433 (2024 high) will confirm resumption. Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004. Nevertheless, sustained trading below 55 D EMA (now at 1.3102) will delay the bullish case and bring more consolidations first.

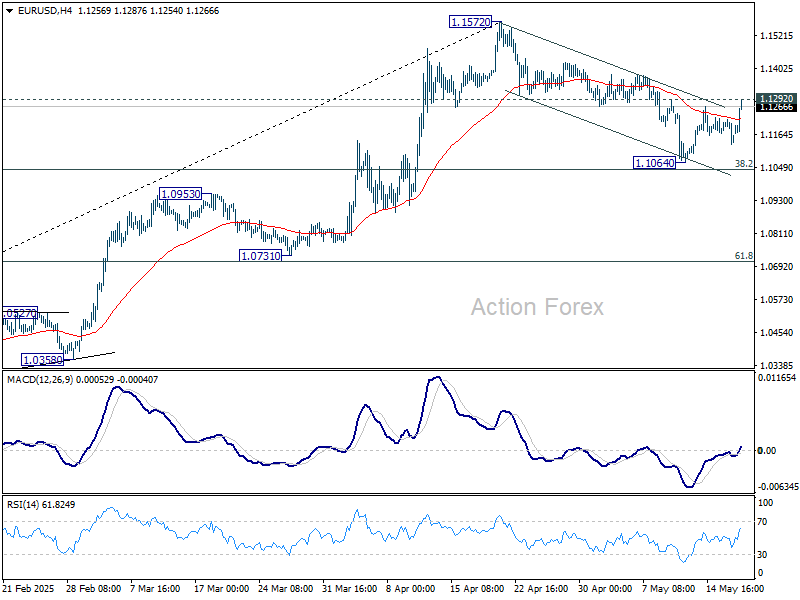

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1123; (P) 1.1171; (R1) 1.1212; More...

Immediate focus is now on 1.1292 resistance in EUR/USD as rebound from 1.1064 resumes. Decisive break there will indicate that correction from 1.1572 has already completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be turned back to the upside for retesting 1.1572 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.

Euro and Pound Rally on UK-EU Pact, Dollar Wobbles

Euro and Sterling surged today after the UK and EU unveiled a sweeping new agreement resetting their defence and trade relationship, the most substantial since Brexit in 2020. The comprehensive deal spans key sectors including security, energy, travel, trade, and fisheries. UK Prime Minister Keir Starmer hosted European Commission President Ursula von der Leyen in London for the high-stakes summit, highlighting the UK’s shift toward pragmatic diplomacy while respecting key post-Brexit red lines.

The UK Labour government was quick to clarify that this reset does not mark a reversal of Brexit. Officials emphasized that the agreement avoids returning to the EU single market, customs union, or freedom of movement. Still, the new deal is being hailed as a boost to corporate confidence and may pave the way for fresh investment flows into the UK, especially following other trade breakthroughs this month with the US and India.

While optimism lifted the Euro and Pound, US assets are under renewed pressure following last week’s credit downgrade by Moody’s. Dollar weakness was notable, with the greenback falling to the bottom of the major currency pack. Treasury yields, however, surged as bond markets reeled from the implications of a swelling fiscal deficit. 10-year yield broke through the key 4.5% level, while 30-year yield topped 5% for the first time in months.

Part of the angst stems from fresh momentum behind President Donald Trump’s multitrillion-dollar domestic policy package. Passed by the House Budget Committee on Sunday, the bill includes major increases in immigration and defense spending, along with an extension of the 2017 tax cuts. It’s now headed for floor debate later this week. Markets are interpreting this as a structural shift toward higher deficits, particularly as tariff revenue is unlikely to fully compensate for lost tax income.

In the currency markets, Euro leads the day’s gains, followed by Sterling and Aussie. Dollar is the weakest performer, trailed by Loonie and Swiss Franc. The Japanese Yen and New Zealand Dollar are trading more mixed.

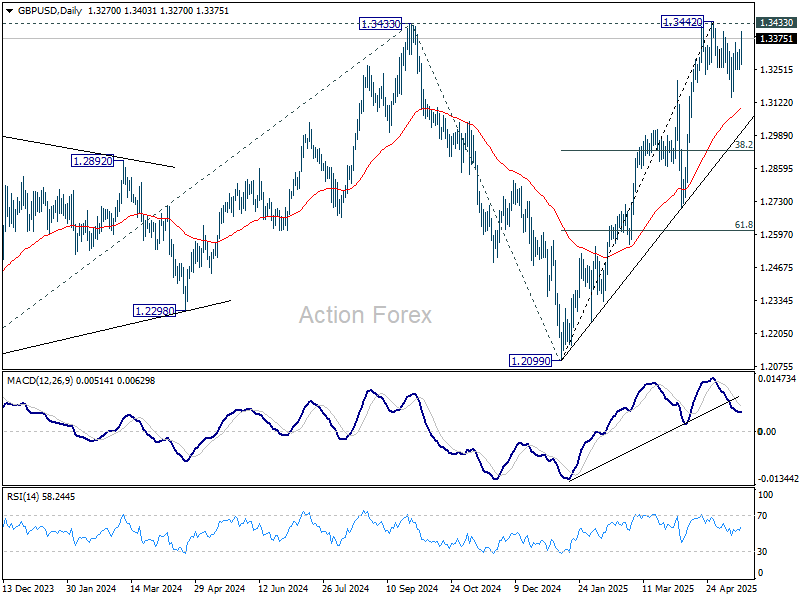

Technically, GBP/USD is now in focus as it approaches key resistance level at 1.3433 (2024 high) again. Decisive break of 1.3433 will confirm resumption of whole up trend from 1.0351 (2022 low). Next medium term target is 61.8% projection of 1.0351 to 1.3433 from 1.2099 at 1.4004.

In Europe, at the time of writing, FTSE is down 0.44%. DAX is down -0.09%. CAD is down -0.74%. UK 10-year yield is up 0.059 at 4.706. Germany 10-year yield is up 0.057 at 2.645. Earlier in Asia, Nikkei fell -0.68%. Hong Kong HSI fell -0.05%. China Shanghai SSE closed flat. Singapore Strait Times fell -0.56%. Japan 10-year JGB yield rose 0.033 to 1.488.

Fed’s Bostic leans toward one rut in 2025 as inflation expectations turn concerning

Atlanta Fed President Raphael Bostic said on CNBC today that he currently favors just one interest rate cut this year, citing persistent inflation pressures and growing concern over shifting inflation expectations.

“I worry a lot about the inflation side,” Bostic said, noting that recent data shows expectations are beginning to drift upward again "in a troublesome way", which “will make our job harder.”

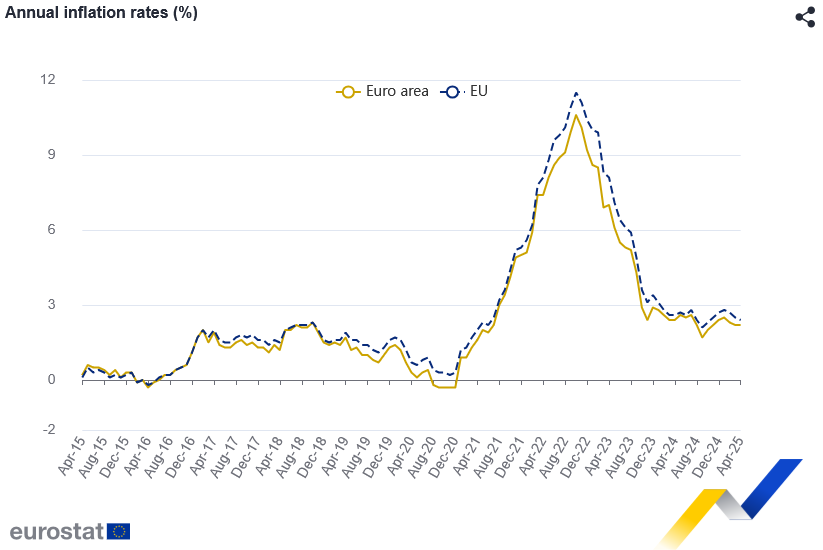

Eurozone CPI finalized at 2.2% in April, core at 2.7%

Eurozone headline CPI was finalized at 2.2% yoy in April. CPI core, which excludes energy, food, alcohol, and tobacco, accelerated, to 2.7%, up from 2.4% previously.

Services remained the primary driver of inflation, contributing 1.80 percentage points to the overall figure, followed by food, alcohol and tobacco at 0.57 pp. Energy continued to exert a dampening effect, subtracting -0.35 pp.

At the EU level, annual inflation was slightly higher at 2.4% yoy. Inflation disparities remained wide across the bloc, with France posting the lowest annual rate at 0.9% and Romania the highest at 4.9%.

BoJ's Uchida notes strain on consumers as food and import costs climb

BoJ Deputy Governor Shinichi Uchida noted in parliamentary remarks that recent inflation has been driven primarily by higher import and food costs, particularly staples like rice.

He acknowledged the burden on households, saying the price increases are “having a negative impact on people’s livelihood and consumption”. The bank remains prepared to continue raising rates if its current forecast holds.

However, Uchida stressed the “extremely high uncertainty” around global trade policies and their economic consequences. Given these risks, he emphasized that the BoJ would assess whether the economy and inflation align with projections before taking further steps.

China's retail sales growth slows to 5.1% in April, misses expectations

China’s economic data for April revealed a patchy recovery, with retail sales rising by 5.1% yoy, falling short of the 6.0% yoy forecast and slowing from March’s 5.9% yoy. Stripping out automobiles, consumer goods sales rose 5.6% yoy.

National Bureau of Statistics spokesperson Fu Linghui remained upbeat, saying that consumption momentum continues to build and will remain a key driver of economic growth.

On the production side, industrial output grew by 6.1% yoy, exceeding expectations of 5.7% yoy but decelerating from March’s robust 7.7% expansion. Meanwhile, fixed asset investment came in at 4.0% year-to-date, below the expected 4.4%.

NZ BNZ services slips to 48.5, sector remains under pressure

New Zealand’s services sector showed further signs of strain in April, with the BusinessNZ Performance of Services Index dipping from 48.9 to 48.5, well below the long-term average of 53.0.

Key components of the survey highlighted persistent weakness: activity/sales was stagnant at 47.3. Employment slipped back into contraction territory at 48.2. New orders showed only marginal improvement, rising from 50.8 to 50.9.

BNZ Senior Economist Doug Steel noted the PSI paints a more sobering picture than broader recovery narratives might suggest, highlighting that New Zealand’s services sector is underperforming relative to key global peers.

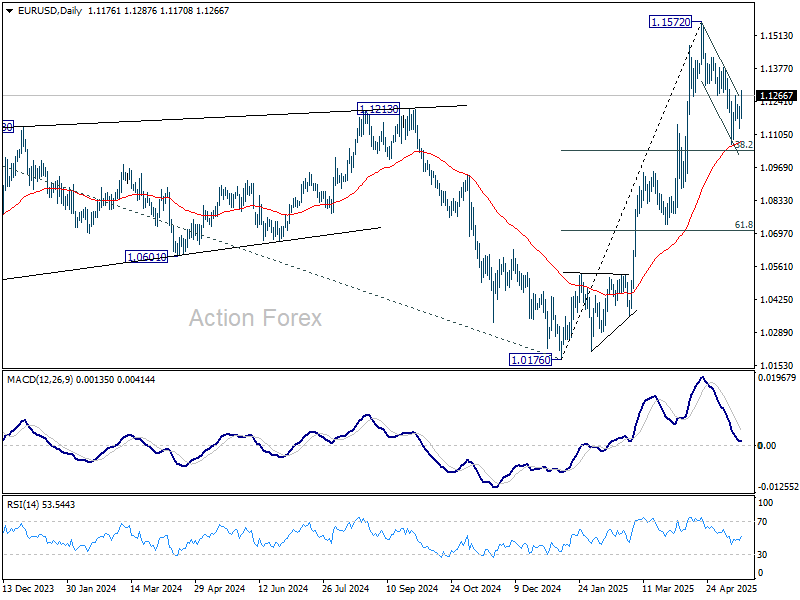

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1123; (P) 1.1171; (R1) 1.1212; More...

Immediate focus is now on 1.1292 resistance in EUR/USD as rebound from 1.1064 resumes. Decisive break there will indicate that correction from 1.1572 has already completed after defending 38.2% retracement of 1.0176 to 1.1572 at 1.1039. Intraday bias will be turned back to the upside for retesting 1.1572 next.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0818) holds.

Fed’s Bostic leans toward one rut in 2025 as inflation expectations turn concerning

Atlanta Fed President Raphael Bostic said on CNBC today that he currently favors just one interest rate cut this year, citing persistent inflation pressures and growing concern over shifting inflation expectations.

“I worry a lot about the inflation side,” Bostic said, noting that recent data shows expectations are beginning to drift upward again "in a troublesome way", which “will make our job harder.”

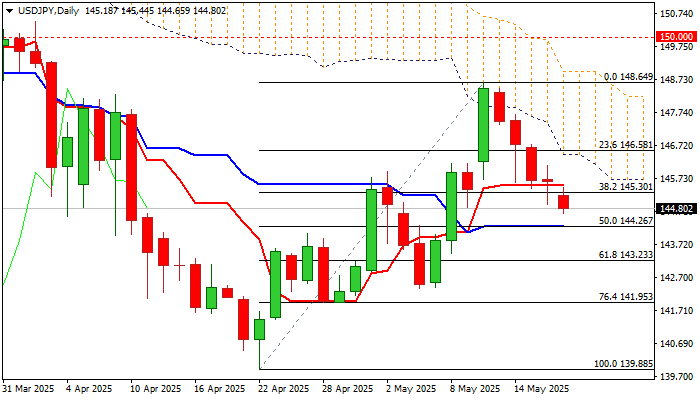

USDJPY: Bears Hold Grip and Eye Key Support

USDJPY continues to descend for the fifth consecutive day, after a double upside rejection and a bull-trap at 148.49 Fibo barrier (76.4% of 151.15/139.88) contributed to the change of direction.

Weaker dollar (which acted as a safe haven on trade uncertainty) following relief on US-China trade agreement and signal that BoJ may resume with tightening (which boosts demand for yen) were the main drivers.

Bears eye pivotal support at 144.26 (50% retracement of 139.88/148.64 recovery leg, reinforced by daily Kijun-sen and bull-trendline off 139.88), loss of which would further weaken near-term structure and risk deeper drop.

The action remains weighed by falling thick daily cloud, daily MA’s in predominantly bearish configuration and long upper shadow weekly candle of last week which points to growing offers and potential formation of reversal pattern on weekly chart.

However, bears are likely to face increased headwinds at 144.26 support that may keep the price in consolidation before attempts through 144.26 trigger.

Near-term action is expected to remain biased lower while below daily Tenkan-sen (145.51).

Res: 145.30; 145.51; 146.10; 146.58

Sup: 144.26; 143.84; 143.23; 142.38

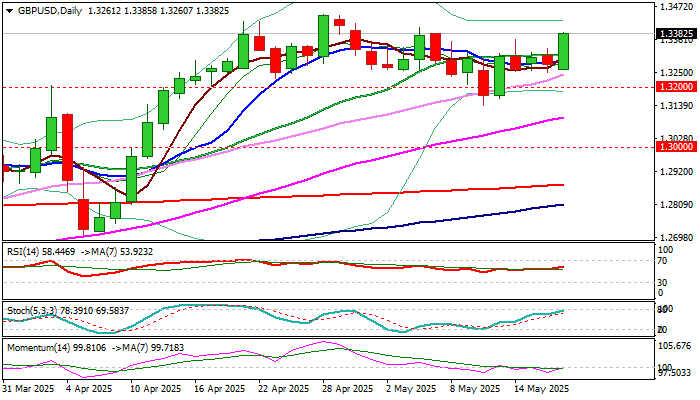

GBP/USD: Fresh Recovery Acceleration Opens Way for Retest of Key Barriers at 1.3443/44

Cable jumped around a hundred pips on Monday morning, lifted by weaker dollar on surprise US credit rating downgrade and the latest EU/UK agreement on defense.

Fresh advance attempts to break above three-day congestion that would signal continuation of recovery from 1.3139 (correction low of May 12) which has already retraced 76.4% of 1.3444/1.3139 pullback.

Improving daily studies (MA’s returned to bullish setup / rising 14-d momentum is pressuring the centreline and on track to break into positive territory) while firmly bullish weekly studies add to the notion, particularly with bear-trap under Fibo support at 1.3163.

Close above 1.3400 zone (May 6 lower top / round-figure) is needed to validate fresh bullish signal and open way for retest of key barriers at 1.3443/44 (2024/2025 tops) where bulls are likely to face increased headwinds.

Res: 1.3402; 1.3444; 1.3500; 1.3557.

Sup: 1.3360; 1.3307; 1.3250; 1.3200.

Australian Dollar Rebounds, RBA Expected to Lower Rates

The Australian dollar has started the week in positive territory, after losses in three straight trading days. In the European session, AUD/USD is trading at 0.6449, up 0.65% on the day.

RBA widely expected to lower rates

The Reserve Bank of Australia is widely expected to lower the cash rate to 3.85% from 4.1% on Wednesday, which would be the lowest rate since May 2023. The blowout employment report last week, which saw the economy add 89 thousand jobs, hasn't changed the view of the markets about a rate cut.

There are two key factors that support a rate cut on Wednesday. First, core CPI, which is considered a more reliable indicator of inflation trends than headline inflation, cooled to 2.9% y/y in the first quarter. This marked a milestone as it was the first time that core CPI fell within the RBA's target band of 2%-3%.

Second, the wide-ranging US tariffs have roiled the financial markets and dampened global growth. This will mean reduced demand for Australian exports which would hurt the domestic economy. The RBA is expected to lower rates another two or three more times after the expected cut on Wednesday. These projections are fluid, as a permanent tariff deal with China would lessen the pressure on the RBA to lower rates.

China records mixed numbers

China posted mixed data for April to start the week. Industrial Production dropped to 6.1% from 7.7% but beat the market estimate of 5.5%. Retail sales fell to 5.1%, down from 5.9% and below the market estimate of 5.9%. Consumers are anxious about the economic uncertainty, especially the impact of the US-China trade war.

AUD/USD Technical

- AUD/USD has pushed above resistance at 0.6409 and 0.6430. Above, there is resistance at 0.6457

- There is support at 0.6382 and 0.6361

AUDUSD 1-Day Chart, May 19, 2025

Eurozone CPI finalized at 2.2% in April, core at 2.7%

Eurozone headline CPI was finalized at 2.2% yoy in April. CPI core, which excludes energy, food, alcohol, and tobacco, accelerated, to 2.7%, up from 2.4% previously.

Services remained the primary driver of inflation, contributing 1.80 percentage points to the overall figure, followed by food, alcohol and tobacco at 0.57 pp. Energy continued to exert a dampening effect, subtracting -0.35 pp.

At the EU level, annual inflation was slightly higher at 2.4% yoy. Inflation disparities remained wide across the bloc, with France posting the lowest annual rate at 0.9% and Romania the highest at 4.9%.

S&P 500 Falls Following Downgrade of US Credit Rating

On Friday, 16 May, after markets had closed, Moody’s Ratings announced a downgrade of the long-term sovereign credit rating of the United States from the highest level of Aaa to Aa1. The key reasons cited by Moody’s were the rising national debt and interest payments, as well as expectations of a further increase in the budget deficit. Notably:

→ The downgrade was hardly a surprise. A similar move was made by Standard & Poor’s back in 2011, while Fitch Ratings followed suit in August 2023.

→ The official response may be seen as reassuring for market participants. US Treasury Secretary Scott Bessent played down concerns about the downgrade in an interview with NBC News, calling credit ratings “lagging indicators” and placing the blame on the previous administration.

→ Despite the downgrade, Moody’s acknowledged the US dollar’s role as the world’s reserve currency and stated that the United States “retains exceptional credit strengths, such as the size, resilience, and dynamism of its economy.”

Stock Market Reaction

The announcement triggered a negative market reaction, reflected in falling prices during Monday morning’s opening session. E-mini S&P 500 futures (US SPX 500 mini on FXOpen) retreated, as indicated by the arrow on the chart, pulling back from the highs reached by Friday’s close.

Last week, we pointed out signs of slowing momentum in the S&P 500 rally. Could the decline continue further?

Technical Analysis of the S&P 500 Chart

By drawing lines A, B, and C through the May rally peaks, we can observe a gradual flattening of the slope — suggesting that the bulls are losing momentum and confidence.

The price is currently trading between local lines C and C1, but it is reasonable to assume that the opening of the US session may bring renewed bearish pressure — potentially pushing the price lower, towards the bottom boundary of the broader upward channel (marked in blue).

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Japanese Yen Strengthens as US Dollar Weakens Following Credit Downgrade

The USD/JPY pair declined for a fifth consecutive day, touching 145.25, as the US dollar faced sustained pressure following Moody’s decision to downgrade the US credit rating.

Key drivers affecting USD/JPY

On Friday, Moody’s cut the US credit rating from Aaa to Aa1, citing a deteriorating fiscal outlook and a lack of “effective measures” to curb the widening budget deficit.

Meanwhile, domestic data revealed that Japan’s economy contracted in Q1 2025, shrinking by 0.2% month-on-month and 0.7% year-on-year, falling short of expectations in both cases. This marks the first economic contraction of the year, driven primarily by a decline in exports.

Investors are now closely monitoring Japan’s trade figures, particularly as the potential impact of new US tariffs looms.

In a recent statement, Prime Minister Shigeru Ishiba stressed that Japan would not accept an unconditional preliminary trade deal, especially concerning automobiles. The country remains wary of a potential 25% US tariff on Japanese car imports. While Japanese diplomats are keen to finalise a trade agreement with the US swiftly, they acknowledge that the outcome is not entirely within their control.

Technical analysis: USD/JPY

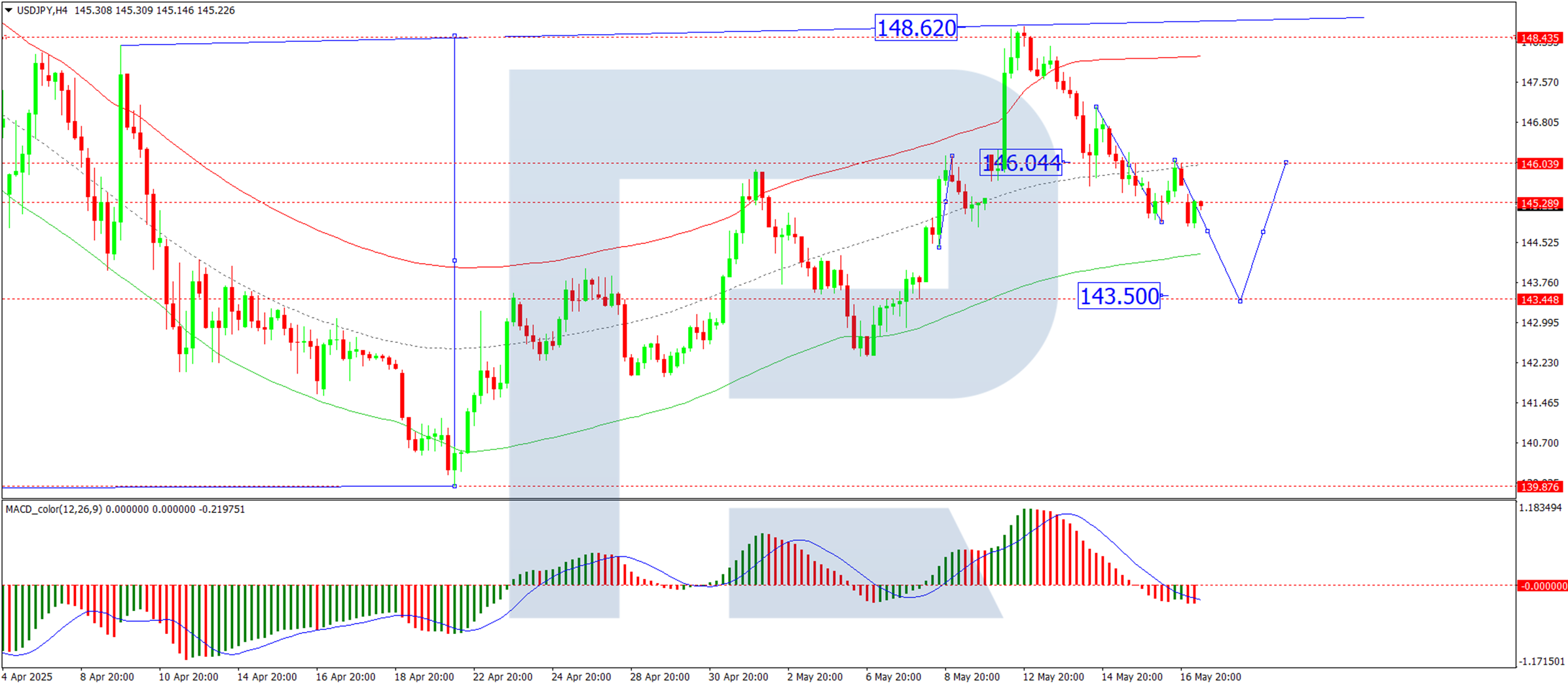

On the H4 chart, USD/JPY has corrected to 146.04, with the fifth wave of decline now in motion. The immediate downside target is 143.50, with further downward momentum expected today. Once this target is achieved, a potential rebound towards 146.04 may follow. This scenario is supported by the MACD indicator, where the signal line remains below zero and points firmly downward.

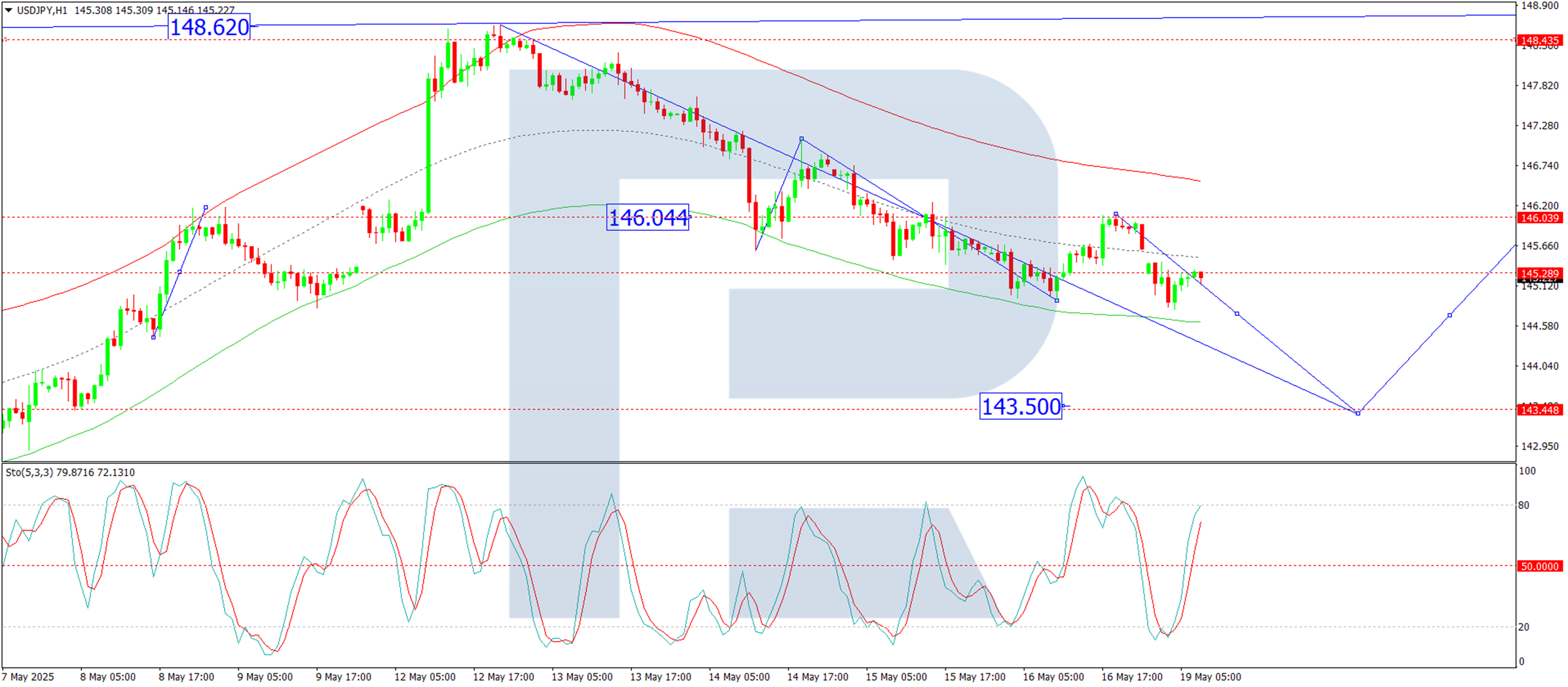

On the H1 chart, the pair consolidated around 146.04 before breaking downward. The current focus is on completing the fifth decline wave towards 143.50. So far, the pair has reached 144.80, followed by a minor correction to 145.30. The next expected move is a further drop to 144.15, with an eventual extension towards 143.50. This outlook is reinforced by the Stochastic oscillator, where the signal line has dipped below 80 and is trending sharply downward towards 20.

Conclusion

The US dollar’s weakness, exacerbated by Moody’s downgrade, continues to drive USD/JPY lower, while Japan’s economic contraction adds further complexity. Traders should monitor trade developments and technical levels for near-term direction.