Sample Category Title

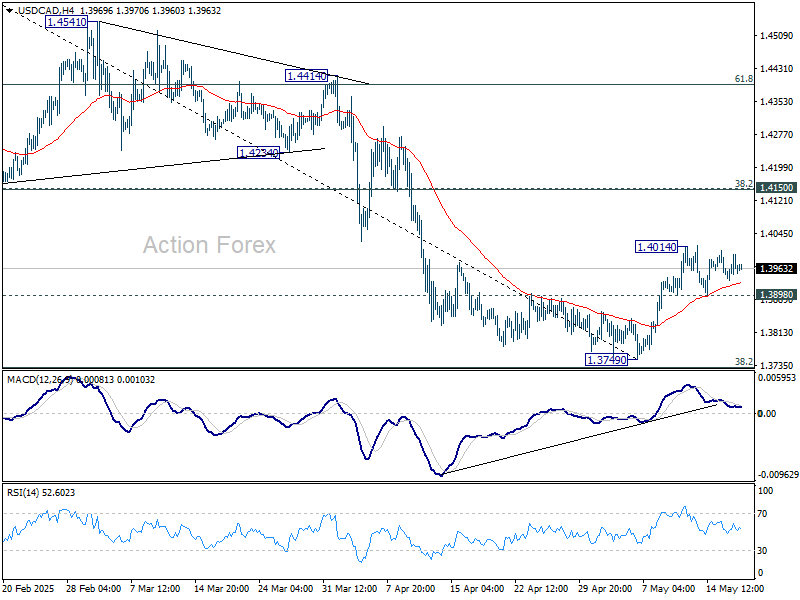

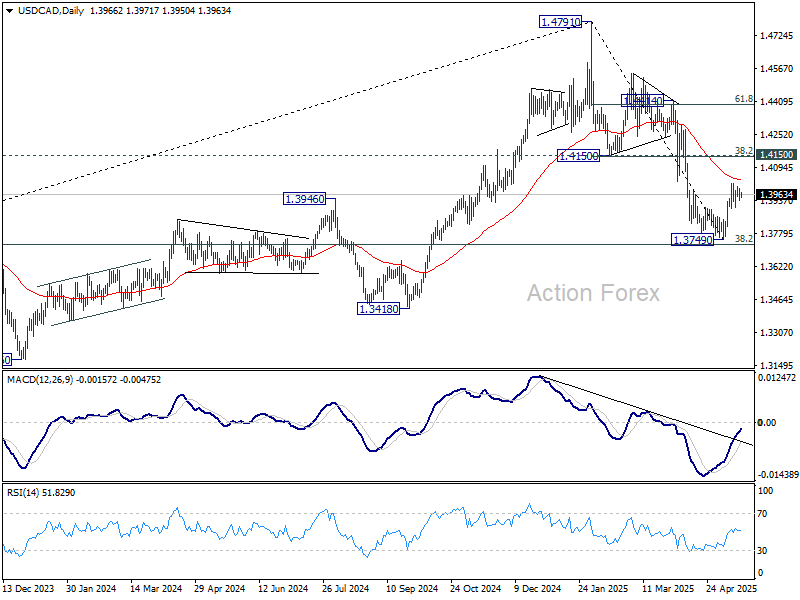

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3937; (P) 1.3967; (R1) 1.3998; More...

Intraday bias in USD/CAD remains neutral and further rise is expected with 1.3898 support intact. Above 1.4014 will resume the rebound from 1.3749 short term bottom to 1.4150 cluster resistance (38.2% retracement of 1.4791 to 1.3749 at 1.4147). However, firm break of 1.3898 will bring retest of 1.3749 low instead.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

Moody’s Downgrade Largely a Symbolical One

Markets

Rating agency Moody’s dropped a little bombshell in late US dealings last Friday. It stripped the US of its top notch AAA-rating over, unsurprisingly, the budgetary situation: “We do not believe that material multi-year reductions in mandatory spending and deficits will result from current fiscal proposals under consideration. Over the next decade, we expect larger deficits as entitlement spending rises while government revenue remains broadly flat.” Moody’s kept a stable outlook. Its decision is largely a symbolical one with the two other rating agencies already having cut the rating before (Fitch in 2011, S&P in 2023). It nevertheless triggered an immediate kneejerk upleg in longer-term yields. The US 30-yr yield shot up 6 bps towards 4.96% and is extending gains this morning back towards the high-profile 5% barrier. The front-end of the curve added around 4 bps, mainly after the release of the May U. of Michigan consumer confidence indicator earlier in the day. Confidence unexpectedly dropped to a record low of 50.8 while inflation expectations shot up to a whopping 7.3% for the year ahead and 4.6% for the longer-term gauge (5-10yr). The latter is on the Fed’s radar, with policymakers looking closely for spillovers to financial market expectations. Favourable interest rate differentials outweighed the downgrade and pushed EUR/USD into a slightly lower close around 1.116 but only to reverse course in current Asian trading hours again. Moody’s decision and with it the long-term US yield rise, is dampening the risk mood. US stock futures point at a 1% lower open. FI is zooming in on the US 30-yr yield today. Trump’s Big Beautiful Bill cleared a hurdle late on Sunday in the key US House Budget Committee, allowing it to advance further. To the extent it’s risk premia driving yields higher, we don’t think higher yields per se are dollar supportive. The eco calendar is pretty empty in terms of data today but features a lot of talks. US President Trump has scheduled a phone call with his Russian counterpart Putin to discuss the ongoing war with the aim of securing a truce to allow for broader and in-depth negotiations. The EU and UK meanwhile are having their first summit since Brexit took effect in 2020 during which they’ll sign a security and defence partnership. It’s the centerpiece of what should be a reset in the post-Brexit relationship that involves deeper economic co-operation. The Financial Times reported of a breakthrough in Sunday night talks over politically sensitive subjects such as fishing, food trade and youth mobility. We’re also on the lookout for trade talks after US Treasury Secretary Bessent warned that tariff rates would go back to the levels Trump announced on Liberation Day if countries are “not negotiating in good faith”. The Financial Times in this respect reported that the EU and US in recent days have begun exchanging negotiation documents, finally kickstarting serious talks.

News & Views

In Romania, the centrist major of the capital of Bucharest, Nicusor Dan won the presidential elections. Dan gained almost 54% of the votes. His national rival, George Simion a eurosceptic advocating a Trump-style policy and in favour of withdrawing support for Ukraine in its war against Russia, only secured 46% of the votes. The election result came amid the highest voter turnout in any election in the country in more than 25 years. First indications suggest that the Romanian currency, the leu, this morning might regain part of the losses from the sell-off on the political turmoil from twee weeks ago after the first round of the elections. In presidential elections in Poland yesterday, the candidate of the ruling centrist coalition, Rafal Trzaskowski was reported to have secured 31.2% of the votes. Trzaskowski is an ally of prime minister Donald Tusk and supports a pro-EU policy, contrary to the approach of outgoing president Duda. Karol Nawrocki of the Nationalist Law and Justice parity PiS received 29.7%. The advance of Trzaskowski was smaller than forecasted in pols in the run-up to the election. Both candidates now will face each other in a run-off election on June 1.

According to the Financial Times reporting, referring to French and German officials, Germany has dropped its opposition against nuclear power. In concreto, German has indicated to France that it will no longer block efforts of France that should lead to nuclear power to be treated again in par with renewable energy in EU legislation. Germany backtracking on its opposition against nuclear power is also seen as signal that the new German government of Chancellor Merz is seeking closer cooperation between the two countries. The move is also cited as opening to way to explore Germany to join France’s nuclear defense shield again potential Russian aggression.

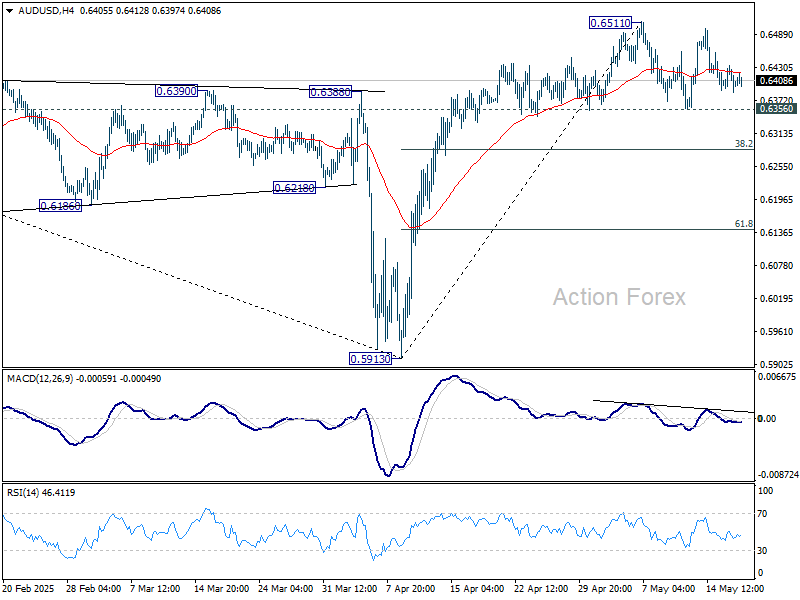

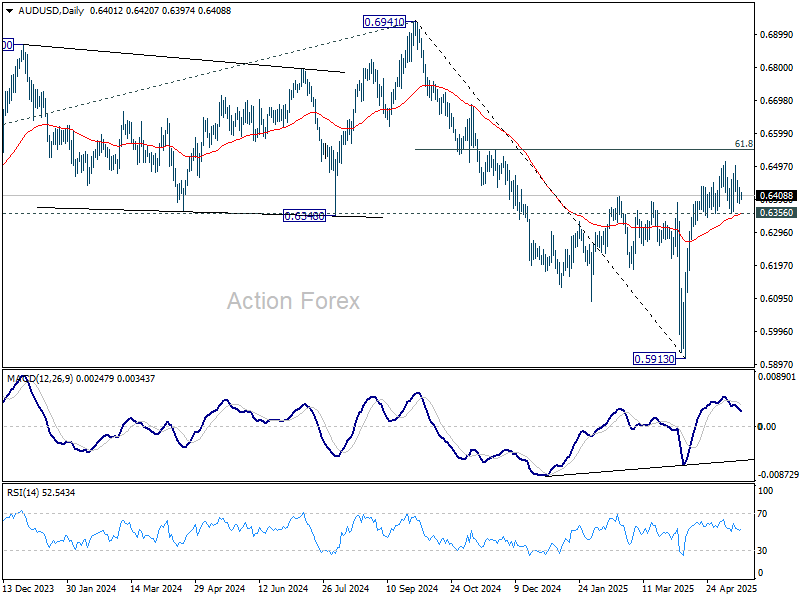

AUD/USD Daily Report

Daily Pivots: (S1) 0.6382; (P) 0.6409; (R1) 0.6430; More...

Intraday bias in AUD/USD remains neutral as range trading continues. Further rise is in favor as long as 0.6356 support holds. One the upside, break of 0.6511 will resume the rise from 0.5913 and target 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6356 will bring deeper pullback to 38.2% retracement of 0.5913 to 0.6511 at 0.6283 first.

In the bigger picture, as long as 55 W EMA (now at 0.6438) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

Risk Mood Softens as Moody’s US Downgrade and Mixed China Data Dent Confidence

Global markets kicked off the week with a mild risk-off tone, driven by renewed concerns over US creditworthiness and mixed economic data out of China. Moody’s downgrade of the U.S. sovereign rating from Aaa to Aa1 late last Friday has cast a shadow over investor sentiment. Meanwhile, China’s latest data highlighted a fragile recovery with industrial output holding up but retail sales and investment disappointing. Still, losses in Asian equities have been relatively contained so far, suggesting caution more than panic.

The more notable market movement is in US futures, where the DOW is down over 200 points in early trade. However, since US cash markets are yet to reopen, the true extent of investor reaction remains to be seen. Currency markets are relatively quiet, with Dollar trading on the soft side, but there’s no sign of a broad-based selloff. Nearly all major currency pairs and crosses are hovering within Friday’s ranges.

Trade policy developments will continue dominate this week's narrative. In a Sunday interview, US Treasury Secretary Scott Bessent reiterated the administration’s readiness to reinstate reciprocal tariffs at the April 2 rate on countries that fail to negotiate “in good faith.” However, he offered little clarity on what qualifies as “good faith” or when decisions might be announced.

Bessent noted that the US is currently focused on its 18 most important trading relationships, and letters will be sent out to those nations deemed to be stalling or resisting negotiations. The threat of reactivating the more extreme tariff brackets imposed in April looms large and could provoke renewed volatility.

On the economic calendar, RBA’s expected rate cut will headline central bank action. Meanwhile, inflation data from Canada, the UK, and Japan will offer fresh insight into price dynamics amid global tariff pressures. Retail sales from the UK, Canada, and New Zealand will help gauge consumer resilience. ECB’s meeting accounts may shed light on the internal debate ahead of its anticipated June rate cut.

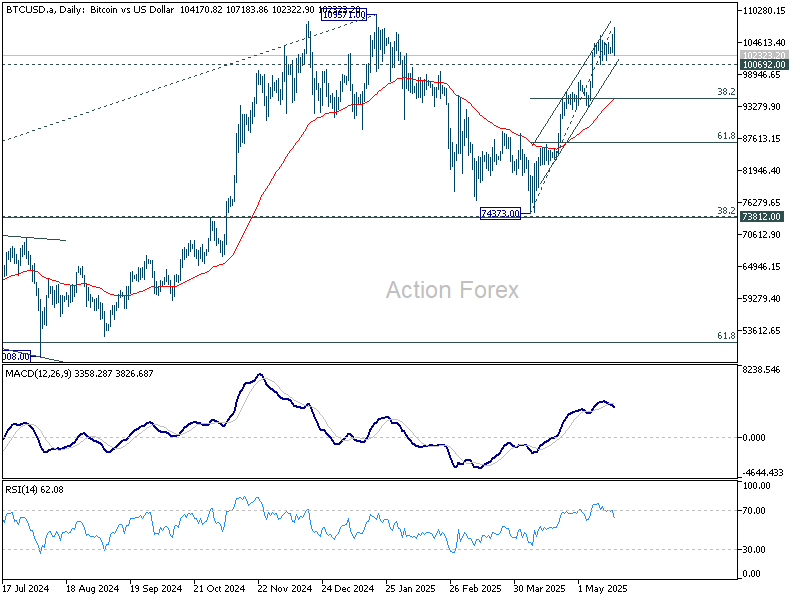

Technically, Bitcoin reversed quickly after initial surge earlier today. Upside momentum is also unconvincing as seen in D MACD. Break of 100692 support should confirm rejection by 109571 higher. Deeper pullback should at least be seen to 55 D EMA (now at 94361), with risk of near term bearish reversal.

In Asia, Nikkei fell -0.73%. Hong Kong HSI is down -0.02%. China Shanghai SSE is up 0.02%. Singapore Strait Times is down -0.25%. Japan 10-year JGB yield is up 0.03 at 1.485.

BoJ's Uchida notes strain on consumers as food and import costs climb

BoJ Deputy Governor Shinichi Uchida noted in parliamentary remarks that recent inflation has been driven primarily by higher import and food costs, particularly staples like rice.

He acknowledged the burden on households, saying the price increases are “having a negative impact on people’s livelihood and consumption”. The bank remains prepared to continue raising rates if its current forecast holds.

However, Uchida stressed the “extremely high uncertainty” around global trade policies and their economic consequences. Given these risks, he emphasized that the BoJ would assess whether the economy and inflation align with projections before taking further steps.

China's retail sales growth slows to 5.1% in April, misses expectations

China’s economic data for April revealed a patchy recovery, with retail sales rising by 5.1% yoy, falling short of the 6.0% yoy forecast and slowing from March’s 5.9% yoy. Stripping out automobiles, consumer goods sales rose 5.6% yoy.

National Bureau of Statistics spokesperson Fu Linghui remained upbeat, saying that consumption momentum continues to build and will remain a key driver of economic growth.

On the production side, industrial output grew by 6.1% yoy, exceeding expectations of 5.7% yoy but decelerating from March’s robust 7.7% expansion. Meanwhile, fixed asset investment came in at 4.0% year-to-date, below the expected 4.4%.

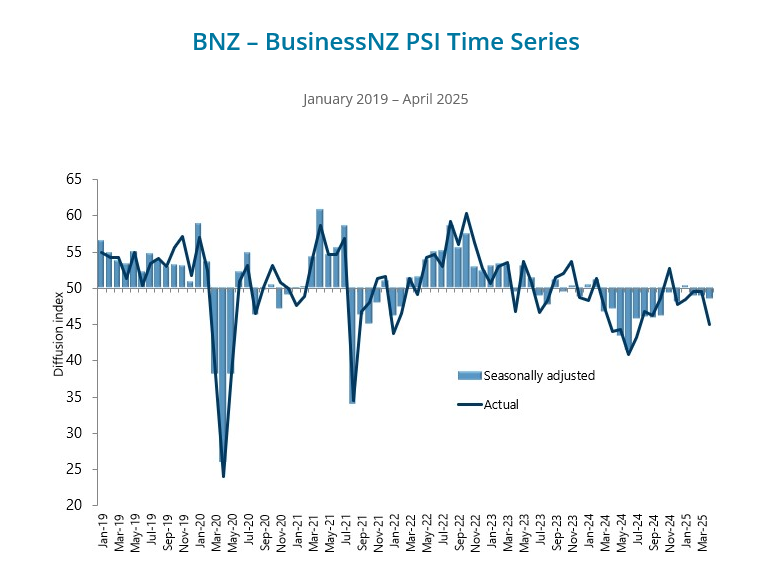

NZ BNZ services slips to 48.5, sector remains under pressure

New Zealand’s services sector showed further signs of strain in April, with the BusinessNZ Performance of Services Index dipping from 48.9 to 48.5, well below the long-term average of 53.0.

Key components of the survey highlighted persistent weakness: activity/sales was stagnant at 47.3. Employment slipped back into contraction territory at 48.2. New orders showed only marginal improvement, rising from 50.8 to 50.9.

BNZ Senior Economist Doug Steel noted the PSI paints a more sobering picture than broader recovery narratives might suggest, highlighting that New Zealand’s services sector is underperforming relative to key global peers.

ECB's Lagarde attributes Euro strength to waning confidence in US policy amid uncertainty

ECB President Christine Lagarde has described the Euro’s recent appreciation against Dollar as “counter-intuitive,” but ultimately a reflection of growing global unease over US political and economic direction.

In an interview with La Tribune Dimanche, Lagarde said that parts of the financial markets appear to be "losing confidence" in the US, due to economic and financial chaos during the first 100 days of President Donald Trump's term.

By contrast, Lagarde highlighted Europe’s comparative stability, both economic and institutional, as a key driver behind the Euro’s unexpected strength.

“Uncertainty is a constant [in the US],” she noted, while Europe is being recognized as “a stable economic and political region with a solid currency and an independent central bank.”

That divergence in perceived reliability, she argues, has led markets to favor the Euro even in a climate where risk aversion would normally boost Dollar.

RBA rate cut, inflation data from Canada, UK and Japan to highlight the week

RBA is widely expected to deliver a 25 bps rate cut, bringing the cash rate down to 3.85%. While all of Australia’s big four banks agree on the need for further easing, there’s some divergence on the pace. NAB stands out with a bolder forecast, projecting a larger 50bps reduction.

Looking ahead, ANZ anticipates two more cuts in July and August to bring the cash rate to 3.35% by then. Commonwealth Bank shares a similar view but sees the final cut coming in November. NAB expects a more dovish sequence, projecting three further cuts by year-end, followed by one more in early 2026. Westpac also forecasts two cuts in H2 2025.

Yet, with global tariff negotiations still unresolved, particularly regarding China, Australia's economic outlook remains highly fluid, leaving room for policy recalibration in the months ahead.

On the data front, inflation will dominate. Canada, the UK, and Japan are all set to release April CPI figures.

In Canada, headline inflation could be significantly distorted by the recent removal of the consumer carbon tax on energy products. As a result, attention will shift to the ex-energy components, which could offer clearer guidance for the BoC. Economists generally expect another rate cut in June, provided the CPI report shows subdued underlying pressures, especially as tariff effects begin to bite.

In the UK, inflation is projected to rebound above 3%, largely due to previously flagged increases in energy prices and regulated items like water bills. BoE has already accounted for this temporary surge, so a surprise in either direction is unlikely to alter its current pace of easing, generally one 25bps cut per quarter.

Japan’s CPI will also attract attention after Q1 GDP revealed a deeper-than-expected contraction, causing markets to dial back BoJ rate hike bets. Even if core inflation picks up again in April, BoJ is likely to remain on hold for now, especially given the dual headwinds of weak growth and global trade uncertainty. However, an upside surprise could test BoJ's tolerance.

Beyond inflation, retail sales from the UK, Canada, and New Zealand will provide insight into consumer resilience in face of tariff threats. Germany’s Ifo Business Climate and a batch of Chinese data, including retail sales, industrial production, and fixed asset investment, will also be in focus. Additionally, ECB will publish the minutes of its latest policy meeting, offering more clues on the anticipated June rate cut.

Here are some highlights for the week:

- Monday: New Zealand BNZ services, PPI; China industrial production, retail sales, fixed asset investment; Japan tertiary industry index; Eurozone CPI final.

- Tuesday: China rate decision; RBA rate decision; Germany PPI; Eurozone current account; Canada CPI.

- Wednesday: New Zealand trade balance; Japan trade balance; UK CPI; Canada new housing price index.

- Thursday: Australia PMIs; Japan PMIs, machine orders; Eurozone PMIs, ECB accounts; Germany Ifo business climate; UK PMIs; Canada IPPI and RMPI; US jobless claims, PMIs, existing home sales.

- Friday: New Zealand retail sales; Japan CPI; UK retail sales; Germany GDP final; Canada retail sales; US new home sales.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6382; (P) 0.6409; (R1) 0.6430; More...

Intraday bias in AUD/USD remains neutral as range trading continues. Further rise is in favor as long as 0.6356 support holds. One the upside, break of 0.6511 will resume the rise from 0.5913 and target 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6356 will bring deeper pullback to 38.2% retracement of 0.5913 to 0.6511 at 0.6283 first.

In the bigger picture, as long as 55 W EMA (now at 0.6438) holds, down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

Dual Rate Cuts Expected in China and Australia

In focus today

Today, the European Commission will release its spring economic forecast, likely revising euro area growth expectations from November's 1.3% y/y to align with private banks' consensus expectations of 0.8% y/y and the ECB's 0.9% y/y projection from March. Attention will also be on the German fiscal package's inflationary impact, viewed by some ECB members as a potential medium-term price pressure risk. We will also receive euro area final inflation for April, set to clarify the drivers of unexpectedly high core services inflation. Final data from Germany showed that it was largely attributed to the timing of Easter, affecting package holidays and airfares, indicating a one-off increase rather than a resurgence.

Overnight, China's central bank is set to announce the 1-year and 5-year Loan Prime Rates of Chinese banks. They are expected to drop by 10bp to 3.0% and 3.5% respectively, following the reverse repo rate cut by 10bp on 6 May. This should thus be seen as a mechanical transmission rather than new easing.

Early tomorrow, the Reserve Bank of Australia (RBA) is expected to deliver its second 25bp rate cut of the cycle, with markets pricing around a 90% probability. The RBA will likely keep its forward guidance cautious, avoiding pre-committing to further easing.

Economic and market news

What happened overnight

China's economic data for April sent mixed signals. Retail sales growth fell short of expectations, increasing by 5.1% y/y (cons: 5.5%, prior: 5.9%). In contrast, industrial production surpassed expectations with growth of 6.1% y/y (cons: 5.5%, prior: 7.7%). Home prices remained steady, experiencing a 4% y/y decline, underscoring the ongoing vulnerability in the housing market. This data precedes the trade agreement between the US and China reached on 11-12 May, so it can be regarded as 'old news'.

What happened over the weekend

In the US, consumer sentiment dopped to nearly a three-year low in May, accompanied by rising inflation expectations, with one-year expectations reaching their highest level since 1981 and five-year expectations rising to 4.6% (prior: 4.4%). Notably, the survey period began on 22 April, preceding recent optimism about a US-China deal (survey ended last Tuesday).

On Friday, Moody's downgraded the US sovereign credit rating to "Aa1" due to concerns over the nation's, growing, USD 36trn debt pile. This move underscores the grim US fiscal outlook and highlights the absence of political willingness in Washington to tackle the issue.

In Romania, centrist Nicușor Dan secured the presidency, garnering 54% of the vote and defeating nationalist contender George Simion. Dan's victory is perceived as a reaffirmation of Romania's commitment to EU and Nato alignment, easing concerns of nationalist shifts. His win is expected to enhance investor confidence, backed by promises of anti-corruption reforms and economic stability.

In Poland, liberal candidate Rafał Trzaskowski narrowly won the first round of the presidential election with 30.8% of the vote, edging out right-wing opponent Karol Nawrocki, who secured 29.1%. The upcoming runoff on 1 June is crucial for Prime Minister Tusk's pro-EU agenda, as the presidency holds veto power over legislation matters.

Equities: Equity markets extended their positive momentum on Friday, closing the week with five consecutive days of gains. We saw notable outperformance from cyclicals throughout the week, although that narrative slightly reversed on Thursday and Friday, with defensive sectors catching up into the weekend. It was more a case of defensives closing the gap than cyclicals selling off meaningfully. As a result, we are now just a few percentage points from all-time highs in equities and around 5% above the level we saw prior to 'Liberation Day' on 2 April. In this "risk-on" environment, implied volatility has dropped further - the VIX is now at 17. Cross-asset correlations last week continued their move back toward normalised or historical "standards". Frankly, we are a bit surprised at how rapidly markets - across assets - have recovered to pre-'Liberation Day' levels. However, this morning we are seeing a clear reversal: equities are trading lower across Asia, and futures are pointing lower in both Europe and the US. Notably, tech futures are taking the largest hit today. But equity moves do not live in a vacuum - we are also seeing a sharp rise in US Treasury yields and a weaker dollar. The moves are being driven by a combination of budget gridlock in the US and Moody's credit rating downgrade of the US.

FI&FX: Late on Friday, Moody's downgraded the US credit rating from Aaa (neg. outlook) to Aa1 (stable). The credit agency motivated its decision by a worsening public debt outlook and the Republican plans to extend the TCJA tax cuts. 10y USTs now trade above 4.50% and is some 6-7bp higher than before the announcement. Overall, we believe that the market impact should be limited, but the downgrade serves as further evidence of the dire US fiscal outlook and the lack of political willingness in Washington to address it. The dollar has also weakened somewhat on the announcement with EURUSD moving from 1.1150 before the announcement to around 1.1185. The risk-off sentiment overnight has also supported USDJPY reaching a low of 144.81 but it has since stabilised around 145.25.

Trade Optimism Evaporates

The week starts with a jump in US yields and a weaker dollar after Moody’s downgraded the US credit rating from the top Aaa to Aa1, citing concerns about the US’ rapidly rising debt toward the $37 trillion mark and a budget deficit reaching 7% — the highest in peacetime. Moody’s decision is unsurprising, as S&P and Fitch had already downgraded the US below AAA. If Moody’s hadn’t followed suit, it risked undermining its own credibility.

Now, there are some unverified posts suggesting that Trump threatened credit agencies with tariffs — a claim that, even if true, wouldn’t make much sense. The Treasury Secretary, Bessent, downplayed the downgrade and attempted to shift attention to the sharp tariff hikes that may be announced in the next two to three weeks. Negotiations with most nations have proven complicated, and the US administration has started accusing its partners of not negotiating ‘in good faith’ — likely shocked by countries defending their own interests. As such, tariffs could be reimposed before the end of the 90-day pause, potentially helping refill government coffers in the short term. Whether it could help improve appetite for US sovereign papers is yet to be seen... The Trump administration is once again proving that there is no predictability or reliability in its announcements. Promises can be reversed unilaterally at any time. Negotiations are unlikely to go smoothly, given that what the US administration expects from its partners often comes at a significant cost to the rest of the world.

This means that the market optimism seen just a week ago — following an agreement between the US and China to talk while lowering tariffs during a 90-day window — could be derailed at any moment. The realization that such optimism may be premature should trigger a return to safe-haven assets, including gold (which had retreated over the past two weeks), the Swiss franc, and the Japanese yen. The euro could also see inflows, along with European sovereign bonds. The German 10-year bund yield ended last week below 2.60% on increased demand for its AAA-rated debt — offering a stronger alternative to US Treasuries than it did a week ago.

Before looking ahead to this week, it’s important to remember that credit ratings have tangible implications for portfolios. Investors often use their holdings as collateral to leverage investments. The riskier the asset, the less valuable it is as collateral. The lower the collateral value, the higher the return investors demand — which explains why the US 10-year yield is up 1.7% in Asia today and the 30-year yield is up by nearly 2% at the time of writing.

Consequently, higher yields are weighing on sentiment this Monday. US futures are pointing to a negative open, while European futures are also under pressure — though to a lesser extent than their US counterparts. Last week’s Big Tech rally may also lose steam after pushing Nvidia past $135 per share following the announcement of massive deals with Middle Eastern governments.

Trade risks persist. Apple was told that moving production from China to India wouldn’t satisfy Mr. Trump — who wants iPhones manufactured in the US. Meta, Google, and Microsoft, which had been spared from the tariff crossfire so far, could come under pressure if US-EU talks fail before the 90-day pause ends. In that case, Europe may retaliate against US Big Tech.

In Asia, the week begins with losses across major indices. The Nikkei is pressured by a stronger yen, and the CSI is down. China posted a smaller-than-expected slowdown in April industrial production, but retail sales fell more than forecast — dampening hopes that domestic demand might offset weakening global trade. The Hang Seng Index also started on a bearish note, though dip-buying emerged ahead of earnings from Baidu and Xpeng this week — and ahead of CATL’s Hong Kong IPO, the biggest of the year so far. The world’s largest EV battery maker — with clients including Tesla, Ford, BMW, Mercedes, and Volkswagen — is expected to announce its final offer price today and begin trading tomorrow.

On the economic calendar, both China and Australia are expected to cut rates this week to counter the fallout from trade uncertainties. Meanwhile, UK inflation data out Wednesday is expected to show a sharp increase in headline CPI. Flash PMI data on Thursday will offer a sense of field-level sentiment. The US manufacturing PMI is forecast to slip into contraction, according to Bloomberg’s consensus. While soft data could revive Federal Reserve (Fed) cut expectations, whether the Fed can deliver depends on inflation — and with tariffs back on the table, markets may struggle to find confidence in rate-cut bets.

BoJ’s Uchida notes strain on consumers as food and import costs climb

BoJ Deputy Governor Shinichi Uchida noted in parliamentary remarks that recent inflation has been driven primarily by higher import and food costs, particularly staples like rice.

He acknowledged the burden on households, saying the price increases are “having a negative impact on people’s livelihood and consumption”. The bank remains prepared to continue raising rates if its current forecast holds.

However, Uchida stressed the “extremely high uncertainty” around global trade policies and their economic consequences. Given these risks, he emphasized that the BoJ would assess whether the economy and inflation align with projections before taking further steps.

China’s retail sales growth slows to 5.1% in April, misses expectations

China’s economic data for April revealed a patchy recovery, with retail sales rising by 5.1% yoy, falling short of the 6.0% yoy forecast and slowing from March’s 5.9% yoy. Stripping out automobiles, consumer goods sales rose 5.6% yoy.

National Bureau of Statistics spokesperson Fu Linghui remained upbeat, saying that consumption momentum continues to build and will remain a key driver of economic growth.

On the production side, industrial output grew by 6.1% yoy, exceeding expectations of 5.7% yoy but decelerating from March’s robust 7.7% expansion. Meanwhile, fixed asset investment came in at 4.0% year-to-date, below the expected 4.4%.

NZ BNZ services slips to 48.5, sector remains under pressure

New Zealand’s services sector showed further signs of strain in April, with the BusinessNZ Performance of Services Index dipping from 48.9 to 48.5, well below the long-term average of 53.0.

Key components of the survey highlighted persistent weakness: activity/sales was stagnant at 47.3. Employment slipped back into contraction territory at 48.2. New orders showed only marginal improvement, rising from 50.8 to 50.9.

BNZ Senior Economist Doug Steel noted the PSI paints a more sobering picture than broader recovery narratives might suggest, highlighting that New Zealand’s services sector is underperforming relative to key global peers.

ECB’s Lagarde attributes Euro strength to waning confidence in US policy amid uncertainty

ECB President Christine Lagarde has described the Euro’s recent appreciation against Dollar as “counter-intuitive,” but ultimately a reflection of growing global unease over US political and economic direction.

In an interview with La Tribune Dimanche, Lagarde said that parts of the financial markets appear to be "losing confidence" in the US, due to economic and financial chaos during the first 100 days of President Donald Trump's term.

By contrast, Lagarde highlighted Europe’s comparative stability, both economic and institutional, as a key driver behind the Euro’s unexpected strength.

“Uncertainty is a constant [in the US],” she noted, while Europe is being recognized as “a stable economic and political region with a solid currency and an independent central bank.”

That divergence in perceived reliability, she argues, has led markets to favor the Euro even in a climate where risk aversion would normally boost Dollar.