Sample Category Title

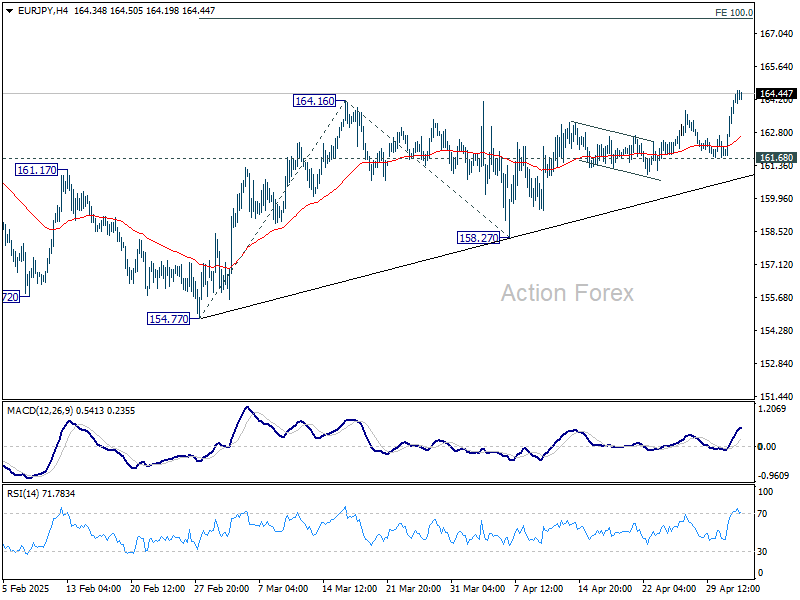

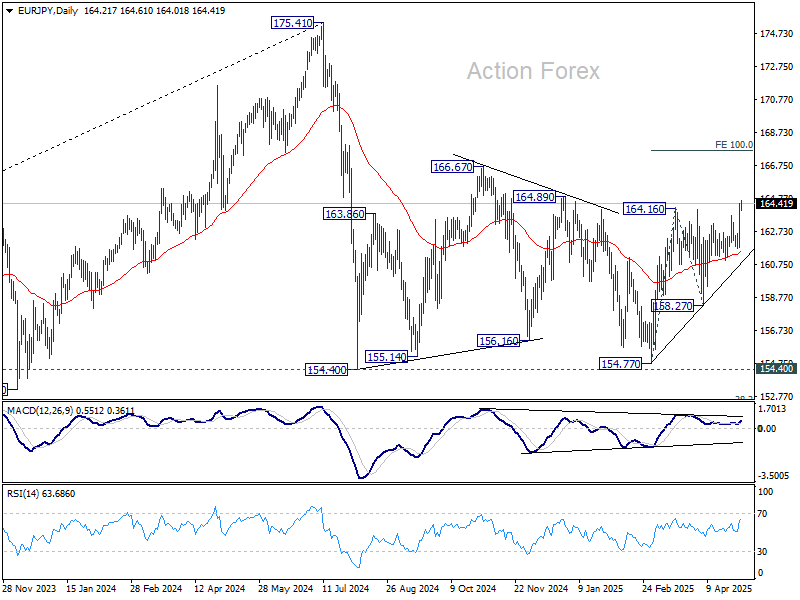

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.52; (P) 163.49; (R1) 165.18; More...

EUR/JPY's break of 164.16 indicates resumption of whole rise from 154.77. Intraday bias is now on the upside for 100% projection of 154.77 to 164.16 from 158.27 at 167.66. For now, further rally will remain in favor as long as 161.68 support holds, in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

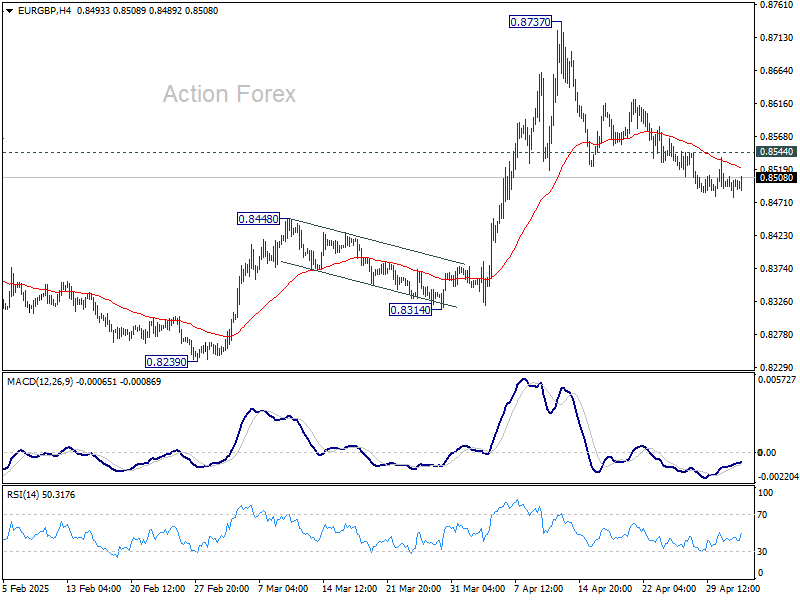

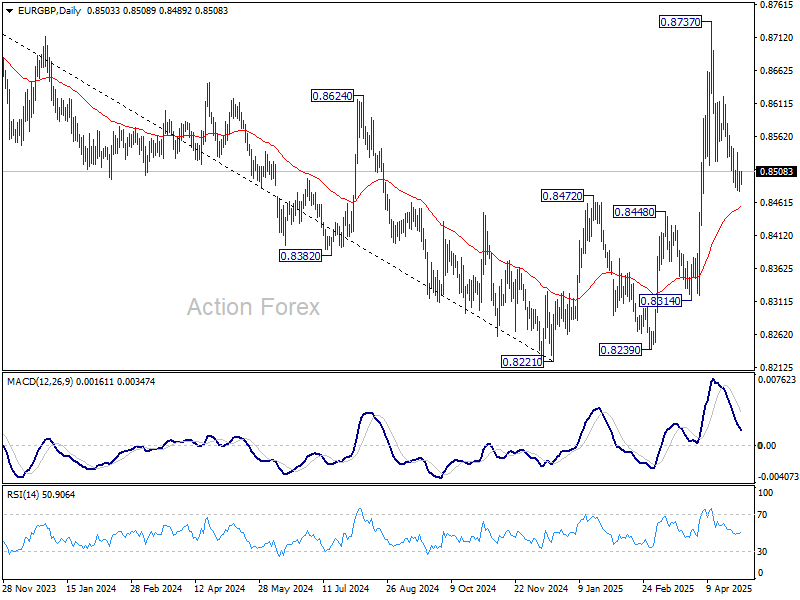

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8486; (P) 0.8498; (R1) 0.8517; More...

EUR/GBP's fall from 0.8737 should still be in progress for 55 D EMA (now at 0.8451). Sustained break there will argue that whole rebound from 0.8221 has completed and turn near term outlook bearish. On the upside, though, break of 0.8544 resistance will turn bias back to the upside fro retesting 0.8737.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds.

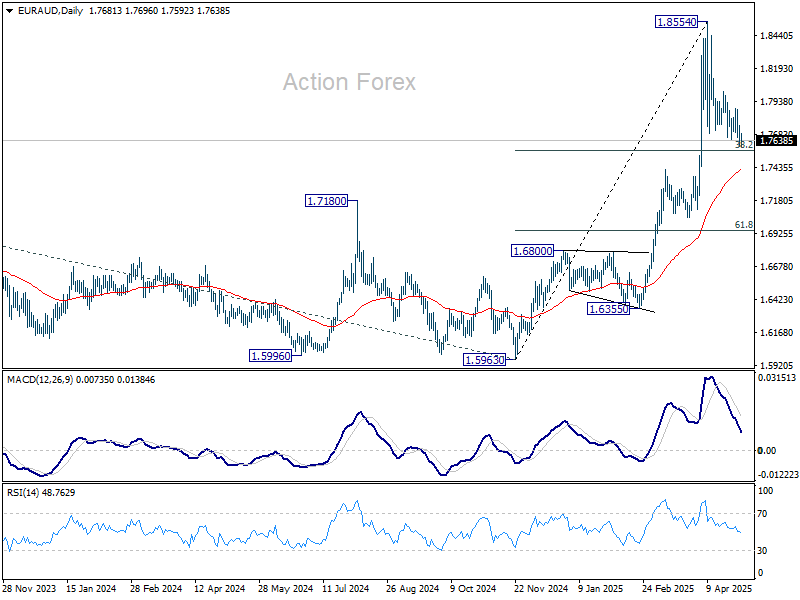

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7606; (P) 1.7680; (R1) 1.7760; More...

Outlook in EUR/AUD is unchanged and intraday bias stays neutral. Corrective pattern from 1.8554 could extend, but downside should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, above 1.8014 minor resistance will bring retest of 1.8554 first. Firm break there will resume larger up trend. However, firm break of 1.7750 will bring deeper fall to 55 D EMA (now at 1.7414) and possibly below.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress for 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7062 resistance turned support (2023 high) holds even in case of deep pullback.

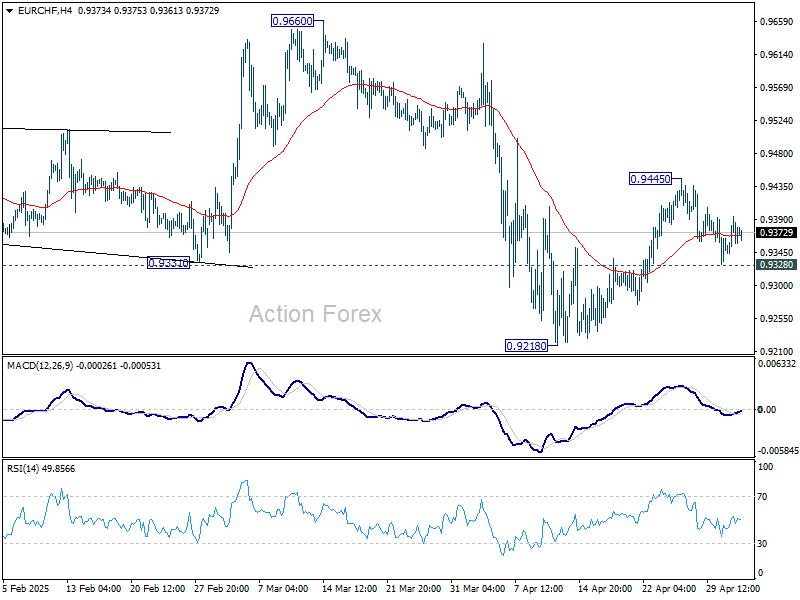

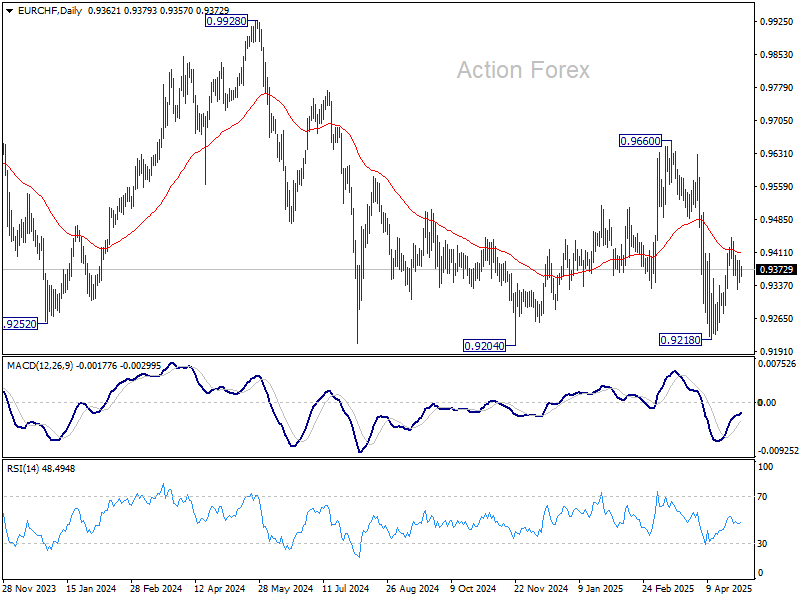

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9330; (P) 0.9362; (R1) 0.9395; More....

Intraday bias in EUR/CHF stays neutral and outlook is unchanged. Rebound from 0.9218 is either a corrective move, or the third leg of the pattern from 0.9204. Break of 0.9445 will resume the rebound towards 0.9660 resistance. However, on the downside, firm break of 0.9328 support will bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

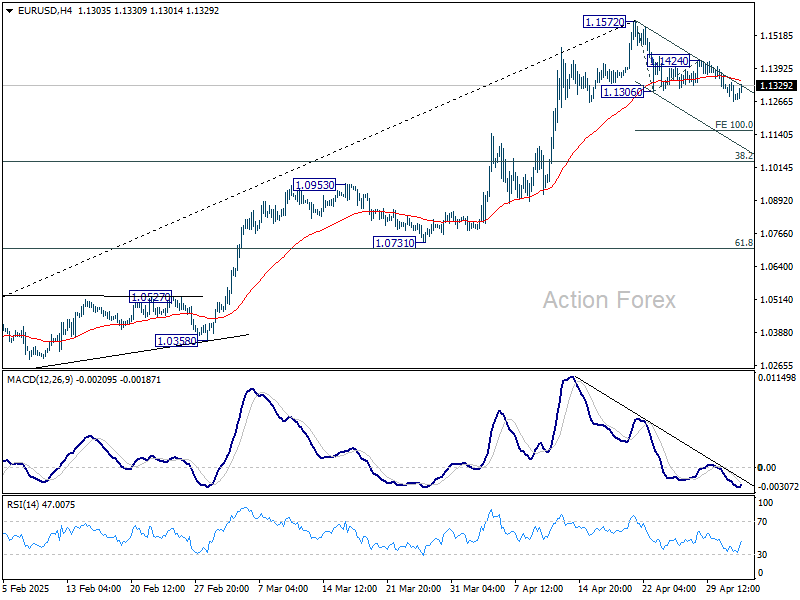

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1257; (P) 1.1299; (R1) 1.1332; More...

EUR/USD's corrective fall from 1.1572 could extend lower to 100% projection of 1.1572 to 1.1306 from 1.1424 at 1.1158. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039 to complete the correction. On the upside, break of 1.1424 will bring retest of 1.1572 high first.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0792) holds.

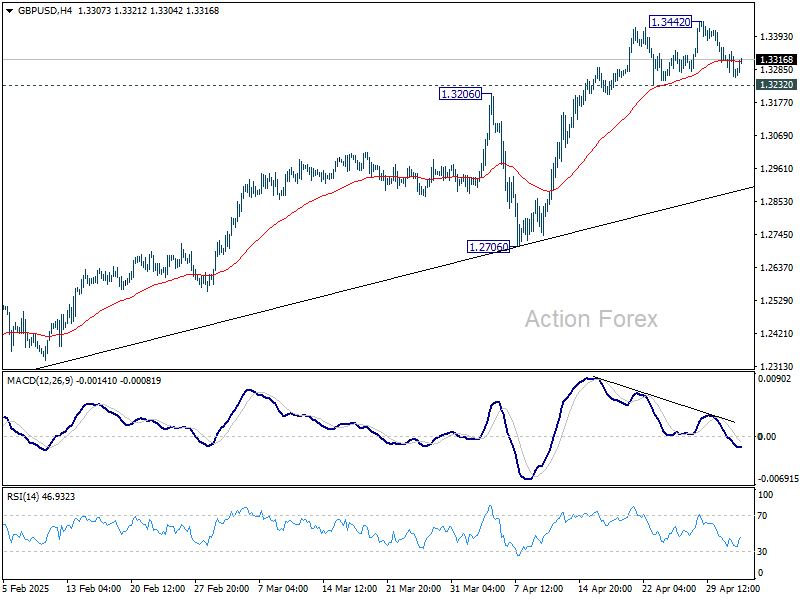

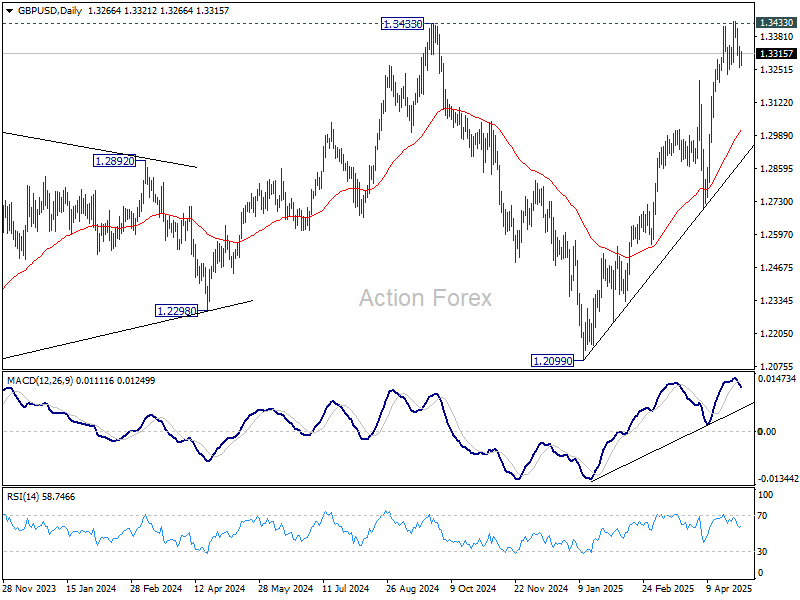

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3244; (P) 1.3295; (R1) 1.3328; More...

Intraday bias in GBP/USD stays neutral at this point. On the downside, firm break of 1.3232 support will indicate short term topping and rejection by 1.3433 key resistance. Intraday bias will be back on the downside for deeper pullback to 55 D EMA (now at 1.3012) and possibly below. On the upside, firm break of 1.3433 key resistance confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

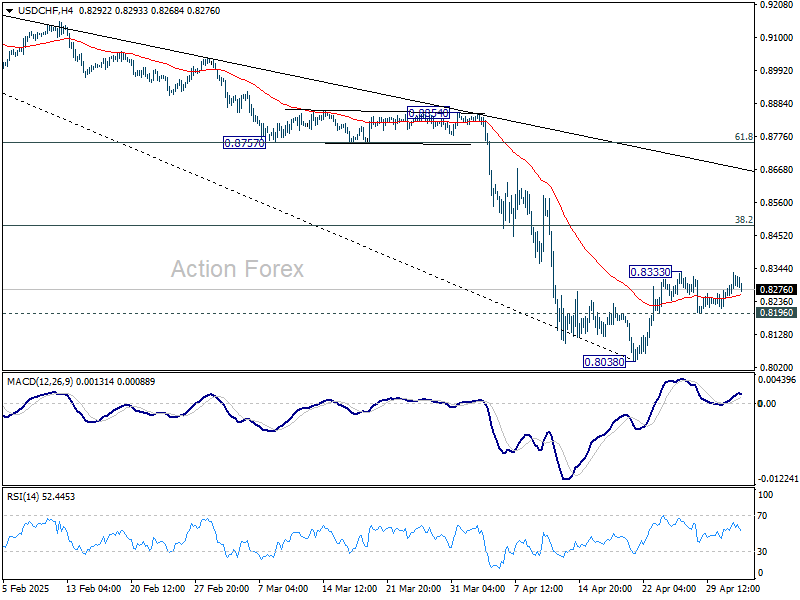

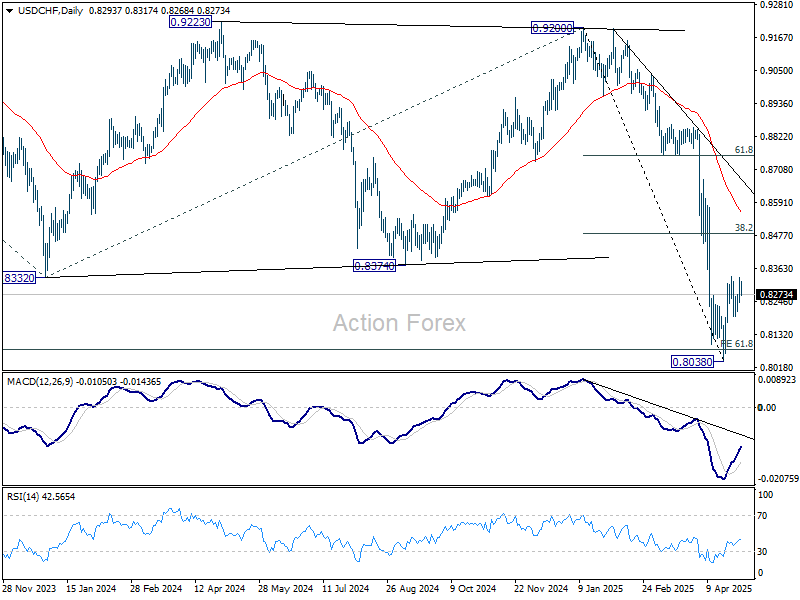

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8248; (P) 0.8290; (R1) 0.8339; More….

Intraday bias in USD/CHF remains neutral as range trading continues. On the upside, above 0.8333 will resume the rebound from 0.8038 short term bottom. But upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8783) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

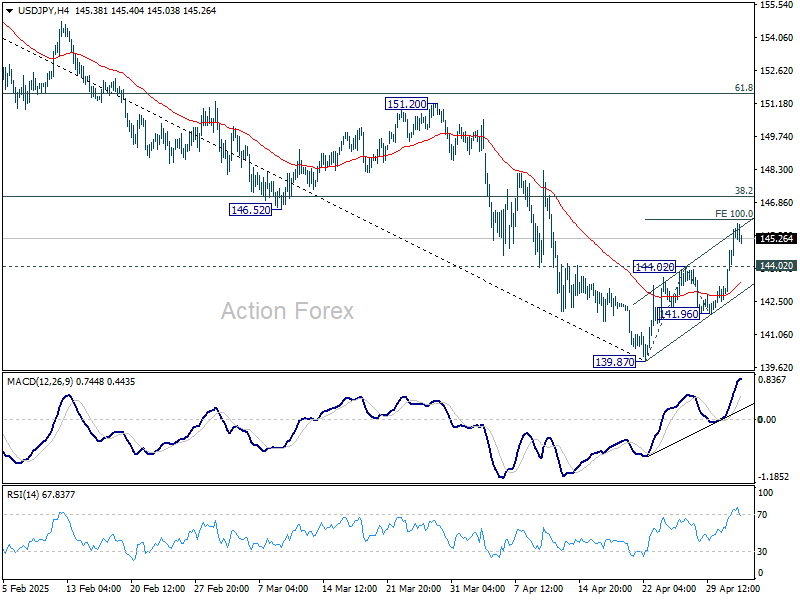

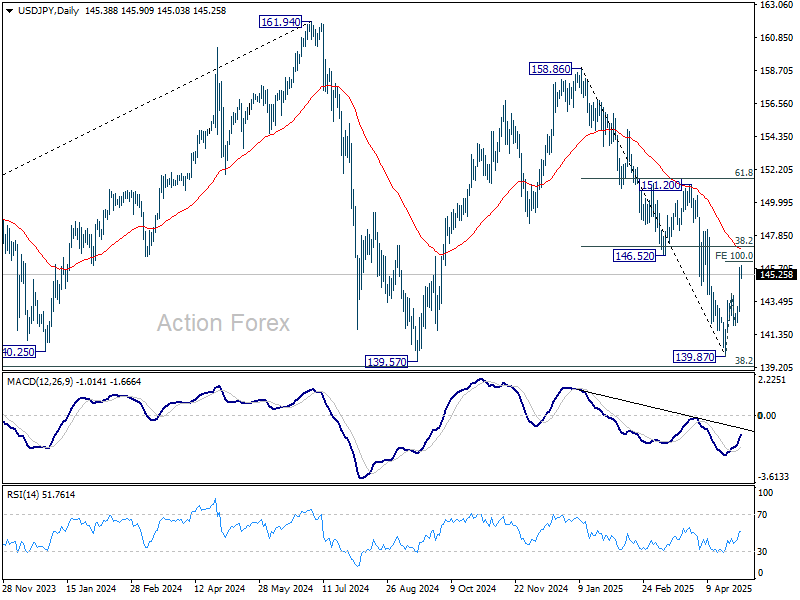

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.60; (P) 144.67; (R1) 146.46; More...

USD/JPY's rebound from 139.87 is in progress and intraday bias stays on the upside for 100% projection of 139.87 to 144.02 from 141.96 at 146.11. But still, near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. On the downside, below 144.02 will turn intraday bias neutral first. Further break of 141.96 will argue that the rebound has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

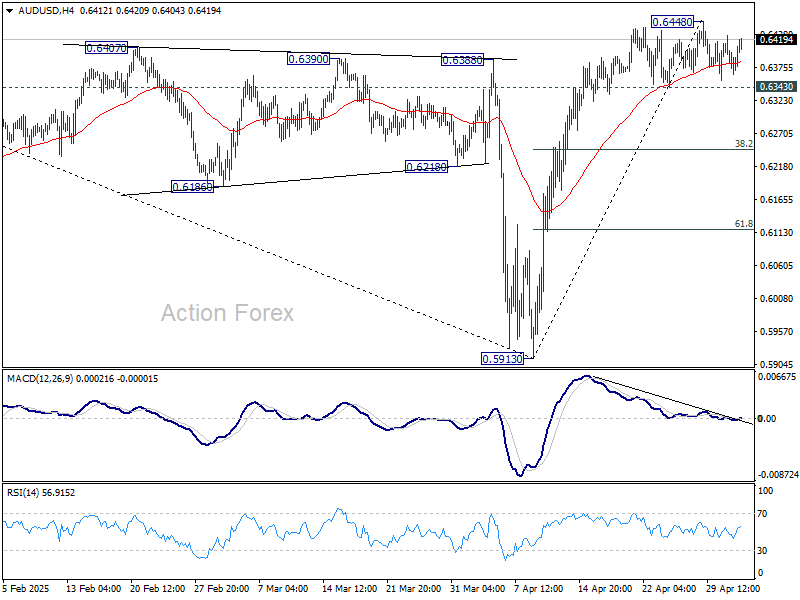

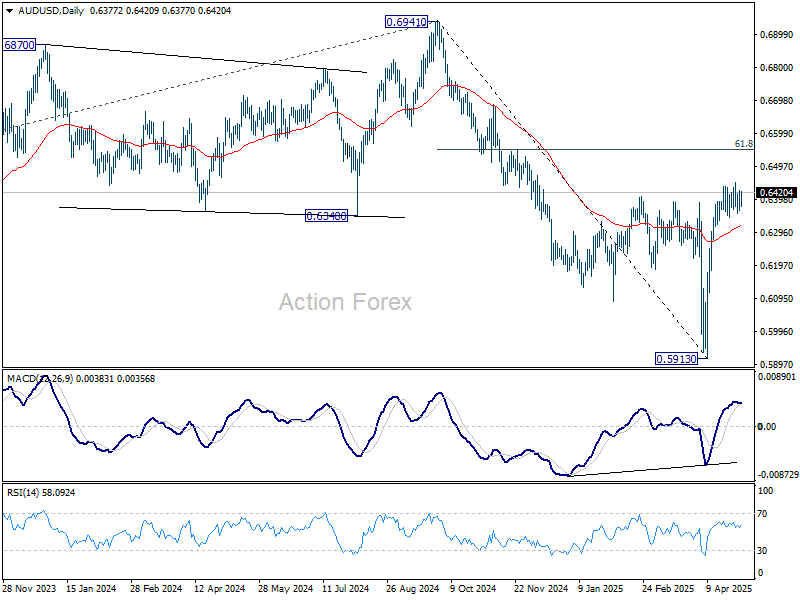

AUD/USD Daily Report

Daily Pivots: (S1) 0.6358; (P) 0.6392; (R1) 0.6419; More...

Intraday bias in AUD/USD remains neutral at this point. On the upside, above 0.6448 will resume the rebound from 0.5913 to 61.8% retracement of 0.6941 to 0.5913 at 0.6548. However, firm break of 0.6343 support will confirm short term topping. Intraday bias will be turned back to the downside for 38.2% retracement of 0.5913 to 0.6448 at 0.6244.

In the bigger picture, as long as 55 W EMA (now at 0.6440) holds, the down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

Futures in Positive Despite Post-Earnings Declines in Apple, Amazon

The S&P 500 gained for the eighth consecutive session despite a set of soft economic data and cautious earnings forecasts. The lack of escalation in the trade war over the past week and dovish Federal Reserve (Fed) expectations certainly explain a major part of the recent gains. But optimism remains fragile, and the Fed’s ability to help depends on the trajectory of inflation.

No-escalation feels good

It’s been roughly a week since Donald Trump and his administration last added fuel to the trade fire—and it feels good. The immediate relief from that sweet calm has brought a rebound across equities despite mixed news. Mixed, because Meta and Microsoft announced stronger-than-expected Q1 results, as did Amazon and Apple after the bell yesterday. However, statements from Apple and Amazon sounded cautious—more cautious than analysts expected.

Apple, which found itself in the crossfire of the US-China trade war, saw a 2.3% decline in iPhone sales to China. Meanwhile, Amazon gave a soft guidance for the current quarter, highlighting that tariffs and trade policies make forecasting complicated. Complicated indeed—when nearly 20% of the goods sold on your platform come from China, and 60% of third-party sellers have China exposure (according to MS). With tariffs imposed at 145% by the Trump administration and Chinese buyers unwilling to absorb those costs, forecasting becomes a nightmare. Both companies fell more than 3% in after-hours trading.

But optimism remains fragile

Still, US futures remain in positive territory this morning, with Nasdaq lagging behind S&P 500 futures. Yet optimism is fragile, as Amazon is far from the only company struggling with forecasting. In fact, many firms have softened their guidance this earnings season—or refrained from giving one altogether. Companies like McDonald's and Starbucks reported declining sales. That could be a sign households are preparing for higher prices and potential recession, as the latest consumer surveys all pointed to a sharp drop in sentiment and a significant rise in medium- to long-term inflation expectations.

Indeed, a first look at Q1 GDP data confirmed that the US economy contracted 0.3% last quarter while price pressures mounted. And the Q2 numbers look dull. Yesterday’s data showed US manufacturing activity shrank the most in five months in April. Orders have been falling since the start of the year, production is diving, and jobs are coming under pressure. Data released earlier this week hinted at lower job openings, a soft ADP report, and a jump in US initial jobless claims to the highest level since February.

Today’s official US jobs data is expected to show 138,000 new nonfarm job additions last month. Last month’s NFP report surprised to the upside, but given the recent string of weak data, there’s a higher chance we see a soft report this time. Of course, soft numbers fuel dovish Fed expectations—and dovish Fed expectations fuel risk appetite. The declining 2-year yield explains part of the recent S&P 500 rebound.

Yet there’s a red line that shouldn’t be crossed: inflation. If inflation heats up due to tariffs, the Fed may not be able to provide the necessary support, and sentiment could quickly reverse. Therefore, a soft NFP read could fuel the Fed doves and push the S&P 500 higher into the weekly close—if wage growth remains reasonable.

The Fed is expected to hold rates steady at next week’s meeting, but expectations for June remain uncertain. Fed funds futures currently suggest a 58% chance of a cut, and a 42% chance of no change. Inflation will determine which way the balance tilts.

FX & Commodities

The US dollar was better bid this week, though it’s softer in Asia this morning. The EURUSD is back at the 1.13 mark after dipping to 1.1265. This week’s CPI update hinted at higher-than-expected price pressure across the major eurozone economies. The eurozone aggregate CPI is due this morning; a stronger-than-expected read could soften the hands of European Central Bank (ECB) doves and trigger further retreat in the euro. But ultimately, the EURUSD’s trajectory will depend heavily on the dollar’s performance. Easing trade tensions could trigger a broad-based US dollar rebound and lead to a period of consolidation in the majors. But only sustained easing in trade tensions could justify a lasting dollar rally.

Elsewhere, the no-escalation of the trade war and improved risk appetite pulled gold prices lower throughout the week. The price of an ounce dropped to $3,200 yesterday after peaking at $3,500 last week—highlighting just how volatile gold has become. Meanwhile, the USDCHF printed a double top near the 0.8335 level, which could be easily broken on further de-escalation in the trade war.

Crude oil was sent on a rollercoaster ride this week. The barrel of US crude fell below the $57 mark yesterday on reports that Saudi Arabia is ready to tolerate lower prices. But dip buyers quickly stepped in as Trump threatened to expand sanctions on buyers of Iranian crude. Day-to-day moves in crude are tough to catch, but the outlook remains negative given rising supply and weakening demand prospects. A further decline to $50pb is likely.

Lower oil prices will likely weigh on energy companies’ earnings. BP reported lower-than-expected Q1 results and reduced its stock buyback due to economic uncertainties. Exxon, and Chevron are due to report earnings today and are expected to announce EPS declines between 15% and 20%. In fact, energy stocks have been underperforming despite an initial Trump boost, and falling oil prices, the trade war, and broader economic uncertainties suggest that pressure could persist.