Sample Category Title

Risk-On Sentiment Regains Control as Data Downplays Severity of Tariff Shock

Global risk sentiment continued to improve last week, with major equity indices staging robust rallies as investor anxiety over the fallout from tariffs eased. The solid US non-farm payroll data was a key turning point, reassuring markets that the early economic impact of the trade shock was not as damaging as initially feared. Added to that, there were signs of progress on multiple trade negotiation fronts, including a potential thaw in US-China relations.

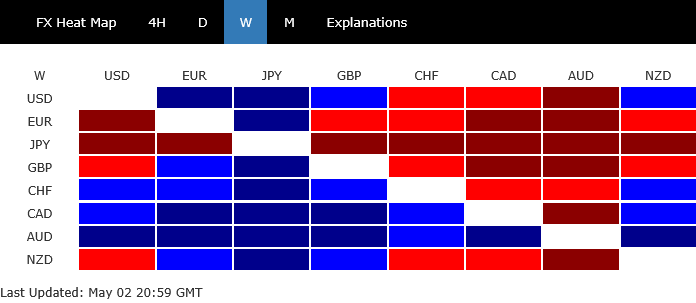

In the currency markets, Aussie was the top performer, buoyed not only by improving risk appetite but also by stronger-than-expected inflation data, which suggests the RBA’s easing path may remain gradual. Loonie followed as second benefiting from political stability after the Canadian elections. Swiss Franc ranked third.

On the other hand, Yen fell the most, under pressure from a dovish BoJ that downgraded its growth outlook. Euro was the second weakest performer, reversing some of its earlier strength despite a sharper-than-expected acceleration in core inflation. Sterling also lagged as third worst. Dollar and New Zealand Dollar ended the week in the middle of the pack.

US Stocks Erase April Losses as Payrolls Soothe Growth Fears, Fed Cut Odds Fall

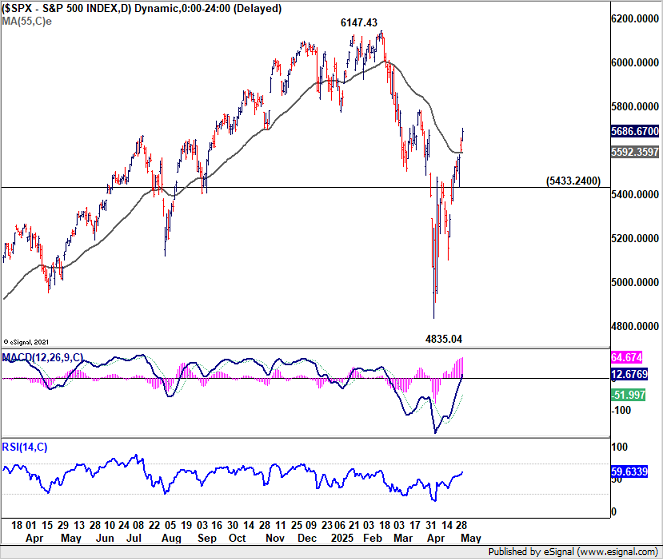

The US markets have decisively moved past the turmoil sparked by the reciprocal tariff announcements in April. Investor confidence has fully recovered, especially in equities with both S&P 500 and NASDAQ reversed all losses from April. S&P 500 even notched a remarkable nine consecutive days of gains, its longest winning streak since 2004. DOW is also on track to complete a full reversal.

Sentiment had wavered briefly after Q1 GDP showed an unexpected contraction. However, those concerns were largely alleviated by April’s non-farm payroll report, which showed solid job creation and stable unemployment. The data suggests that while trade disruptions remain a concern, the labor market is resilient and the broader economy is still on strong footing. This has helped markets conclude that the immediate economic damage from the tariff standoff is more modest than feared.

Looking ahead, the 90-day tariff truce, set to expire in early July, becomes the next major milestone for investors. There are tentative signs of progress on trade negotiations, including fresh signals from China that it may be open to returning to the table. While expectations for a zero-tariff outcome remain low, the fear of escalation to a worst-case scenario has clearly eased. Markets appear to be pricing in a more constructive path, even if slow-moving and politically complex.

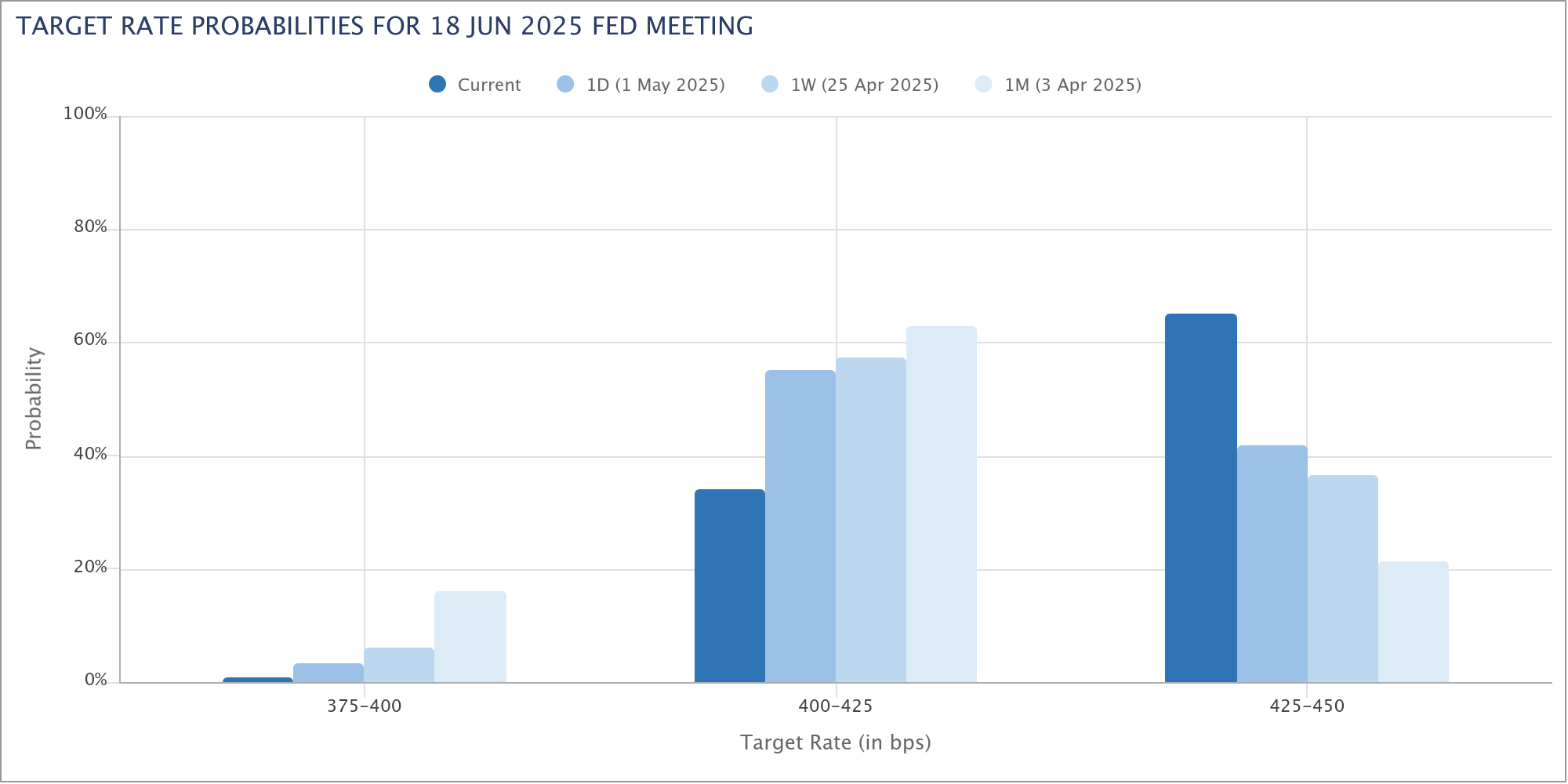

At the same time, expectations for Fed policy are undergoing a recalibration. With the labor market holding firm and inflation still persistent, the urgency for another rate cut has diminished. Fed fund futures are now pricing just a 35% chance of a cut in June — down sharply from 63% a week ago and nearly 80% at the start of April. Importantly, this moderation in rate cut bets is being absorbed without negative market reaction, signaling that investors are comfortable with Fed remaining on hold for longer.

Technically, S&P 500's rally from the 4835.04 low is seen as the second leg in the medium-term pattern from 6147.43 record high. Further upside is favored in the near term as long as 5433.24 support holds. But significant resistance around 6147.43 to bring the third leg of the pattern.

In the bigger picture, the long term up trend remains intact. S&P 500 is well supported by long term rising channel, and managed to defend 4818.62 resistance turned support (2022 high).

An upside breakout is possible during the second half of the year. But that would depend on two key elements: the resolution of trade uncertainty and continued economic resilience.

If July’s truce deadline passes without escalation — or better yet, with concrete de-escalation — and economic data remains firm, then a new record would be on the horizon.

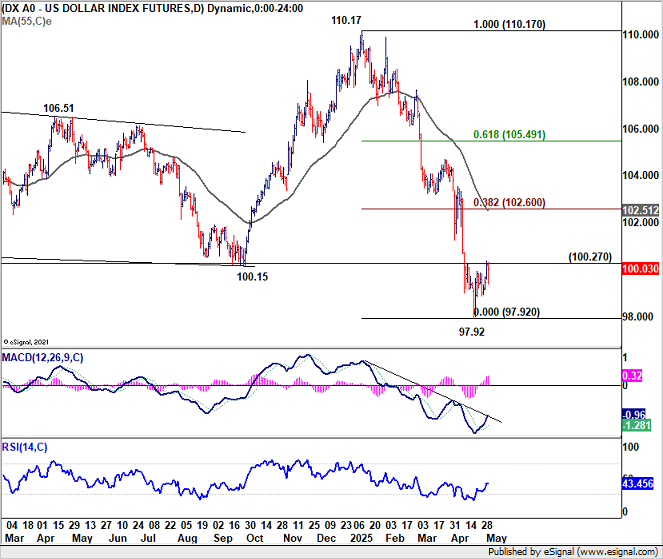

Yields Rise on Risk-On Flow, But Dollar Fails to Ride the Wave

US 10-year Treasury yield staged a rally rebound on Friday, in tandem with equities. Unlike previous yield spikes driven by capital flight, this surge appears rooted in a rotation out of safe-haven assets and into equities, as risk appetite returned.

Technically, 10-year yield's pull back from 4.592 has likely completed with three waves down to 4.124. Break of 4.407 resistance will solidify this bullish case. Rise from 3.886 could then be resuming through 4.592 resistance to 100% projection of 3.886 to 4.592 from 4.124 at 4.830.

In contrast, Dollar has failed to capitalize on either yield strength or reduced recession anxiety. Expectations for Fed to keep interest rates elevated longer may provide some underlying support. But if risk sentiment continues to improve, demand for USD as a defensive play may continue to weaken, even as yield support holds.

Technically, firm break of 100.27 resistance in Dollar Index will bring stronger rebound back to 55 D EMA (now at 102.51). But strong resistance should be seen from 38.2% retracement of 110.17 to 97.92 at 102.60 to limit upside.

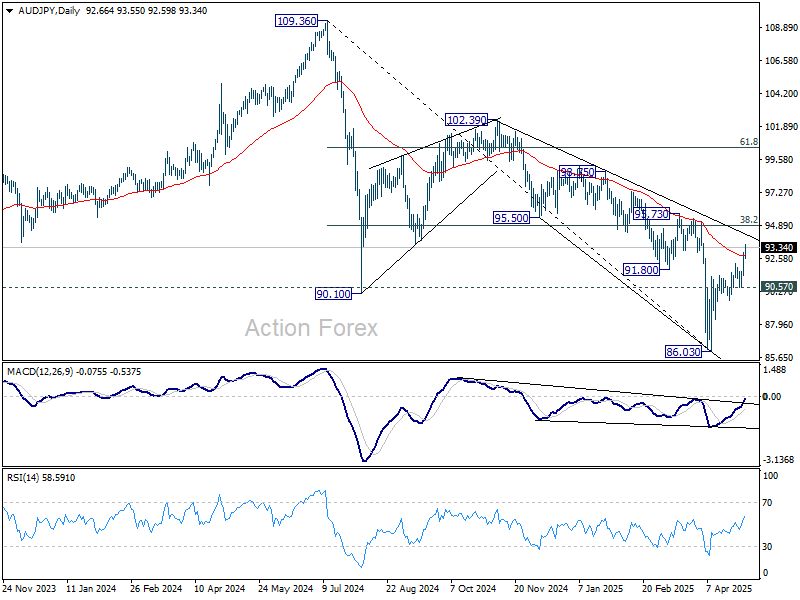

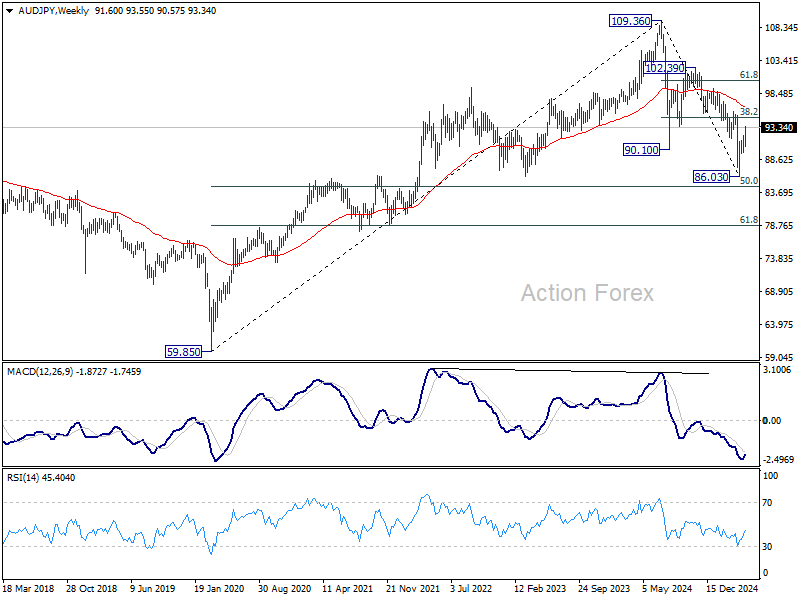

Bullish Case Continue to Build for AUD/JPY, with 94.94 Fibonacci Target in Insight

AUD/JPY ended last week as the top winner and gained 1.56%, on a potent mix of risk-on sentiment and changes in monetary policy outlooks.

Aussie's strength was reinforced by Q1 inflation data from Australia. On the one hand, the trimmed mean CPI returned to RBA’s 2–3% target range for the first time since 2021, cementing expectations of a May rate cut. However, stronger than expected headline CPI reading, and renewed goods inflation pressures points to a cautious and gradual easing path, rather than an aggressive cycle.

In contrast, Yen suffered after BoJ left rates unchanged and sharply downgraded its growth forecast for fiscal 2025, slashing it by more than half. Additionally, core inflation projections were revised lower, raising the risk of falling short of the 2% target again. The downgrade has pushed back expectations of any near-term rate hikes. A June move now looks off the table.

Technically, the developments continue to affirm the case that corrective fall from 109.36 (2024 high) has completed with three waves down to 86.03.

Further rally should be seen in the near term as long as 90.57 support holds, to 38.2% retracement of 109.36 to 86.03 at 94.94. Sustained break there will pave the way to 61.8% retracement at 100.44.

However, rejection by 94.94 fibonacci resistance, followed by break of 90.57 support, will dampen this bullish view and bring retest of 86.03.

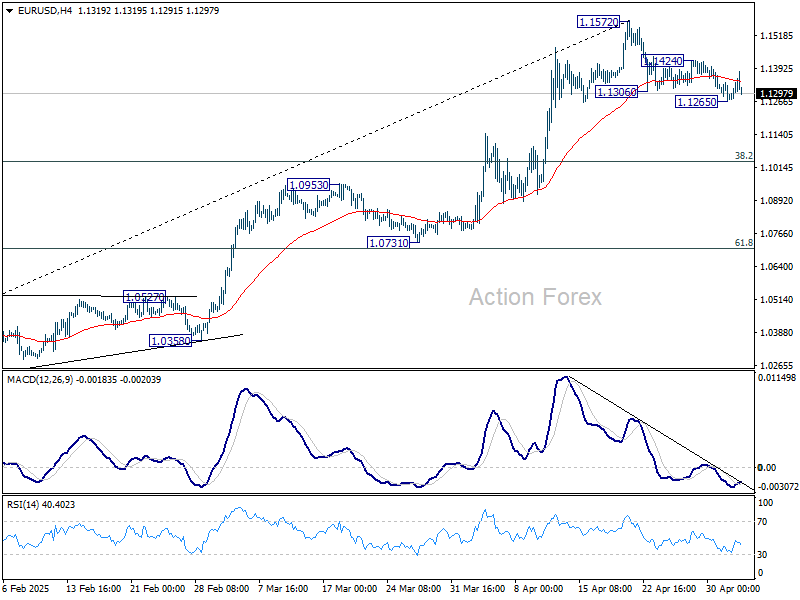

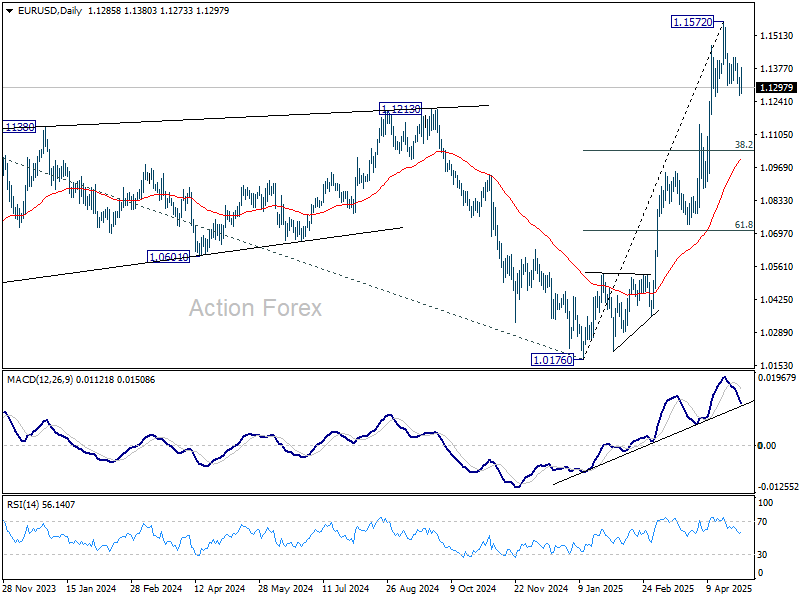

EUR/USD Weekly Outlook

EUR/USD gyrated lower last week but recovered after hitting 1.1265. Initial bias remains neutral this week first. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

In the long term picture, the case of long term bullish reversal is building up. Sustained break of falling channel resistance (now at around 1.1300) will argue that the down trend from 1.6039 (2008 high) has completed at 0.9534. A medium term up trend should then follow even as a corrective move. Next target is 38.2% retracement of 1.6039 to 0.9534 at 1.2019.

EUR/USD Weekly Outlook

EUR/USD gyrated lower last week but recovered after hitting 1.1265. Initial bias remains neutral this week first. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0776) holds.

In the long term picture, the case of long term bullish reversal is building up. Sustained break of falling channel resistance (now at around 1.1300) will argue that the down trend from 1.6039 (2008 high) has completed at 0.9534. A medium term up trend should then follow even as a corrective move. Next target is 38.2% retracement of 1.6039 to 0.9534 at 1.2019.

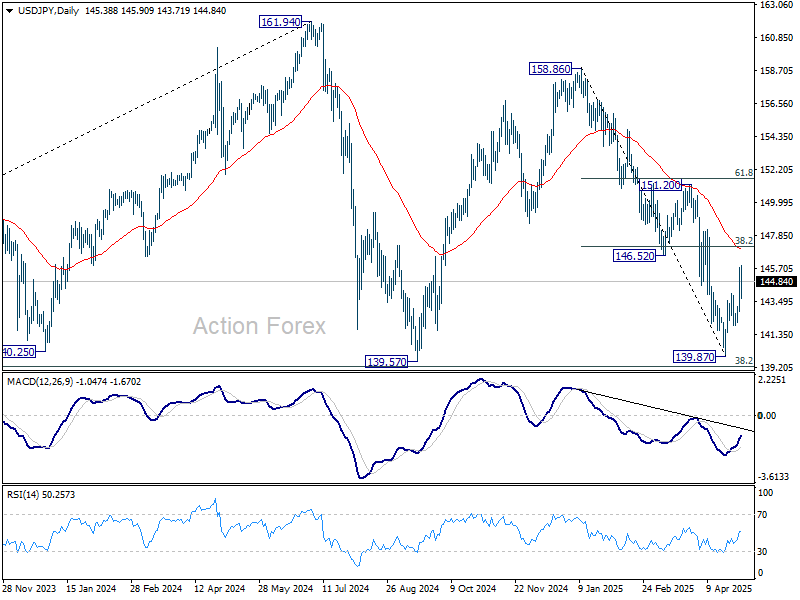

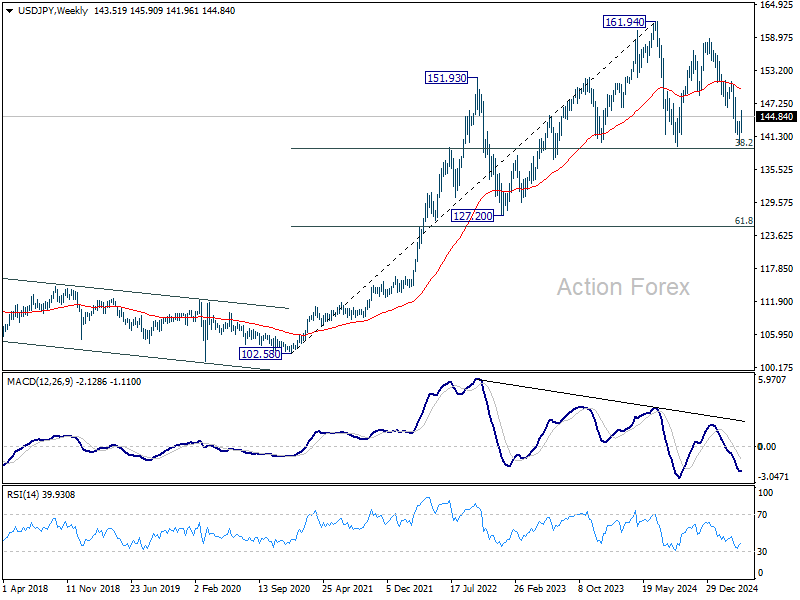

USD/JPY Weekly Outlook

USD/JPY's rebound from 139.87 short term bottom continued last week but retreated after hitting 145.90. Initial bias remains neutral this week first. Overall near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. Break of 141.96 will argue that the rebound has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

In the long term picture, it's still early to conclude that up trend from 75.56 (2011 low) has completed. A medium term corrective phase should have commenced, with risk of deep correction towards 55 M EMA (now at 137.44) and even below.

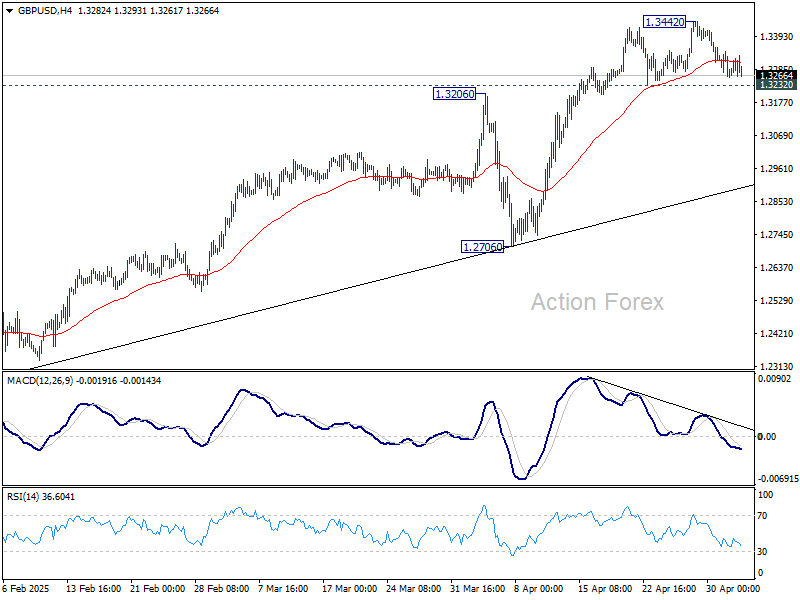

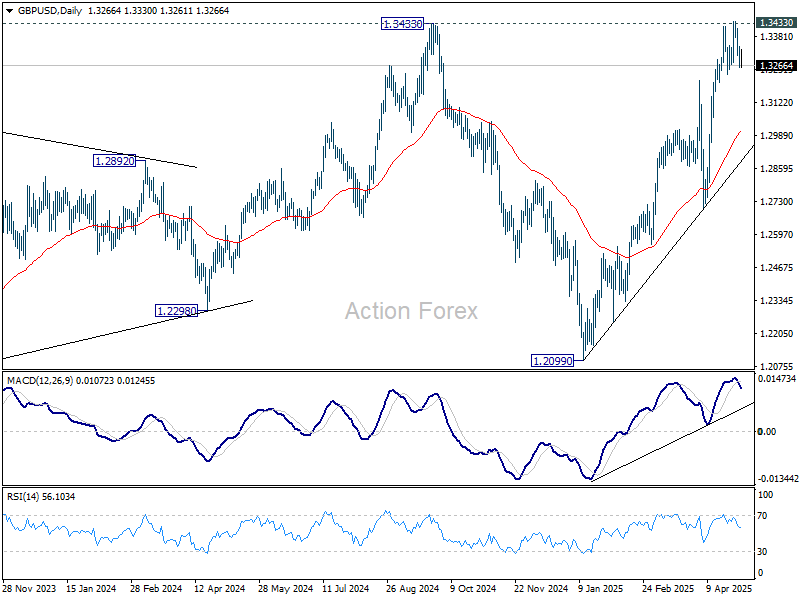

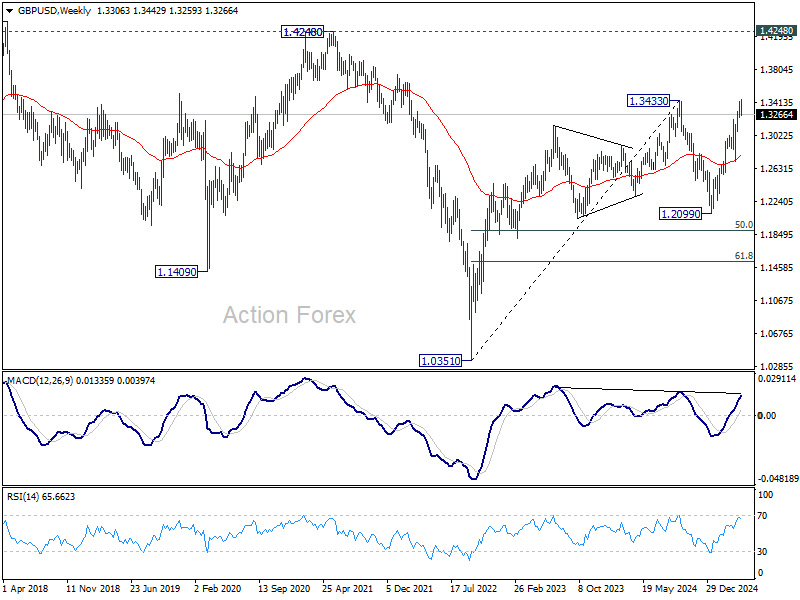

GBP/USD Weekly Outlook

GBP/USD edged higher to 1.3442 last week but failed to sustain above 1.3433 resistance. Initial bias remains neutral this week first. On the downside, firm break of 1.3232 support will indicate short term topping and rejection by 1.3433 key resistance. Intraday bias will be back on the downside for deeper pullback to 55 D EMA (now at 1.3010) and possibly below. On the upside, firm break of 1.3433 key resistance confirm larger up trend resumption.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could either be resuming the up trend, or the second leg of a consolidation pattern. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on decisive break of 1.3433 at a later stage.

In the long term picture, price actions from 1.0351 (2022 low) are seen as a corrective pattern to the long term down trend from 2.1161 (2007 high) only. Outlook will be neutral at best as long as 1.4248 structural resistance holds, even in case of strong rebound.

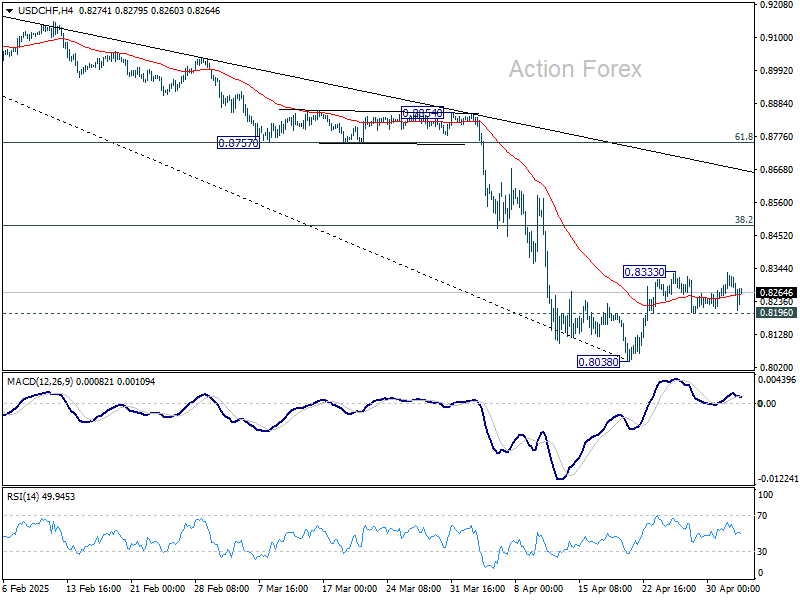

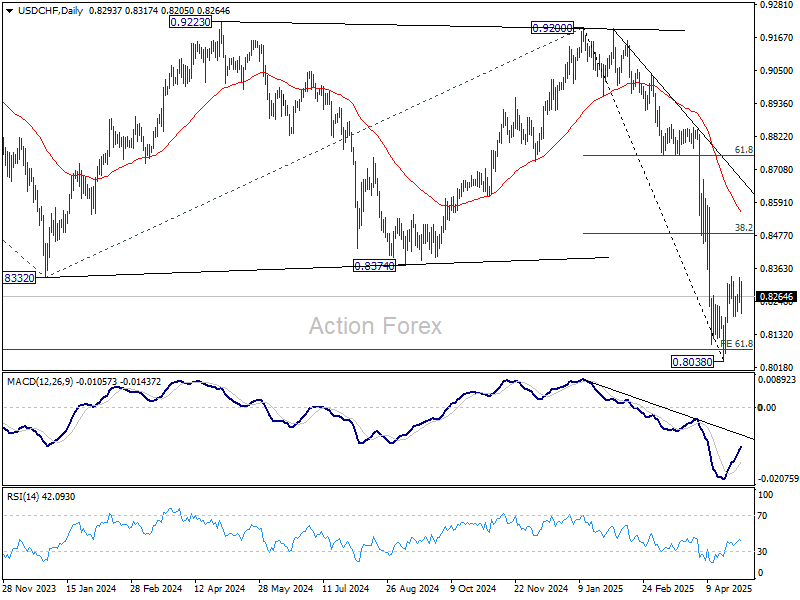

USD/CHF Weekly Outlook

USD/CHF stayed in range below 0.8333 last week and outlook is unchanged. Initial bias remains neutral this week first. On the upside, above 0.8333 will resume the rebound from 0.8038. However, upside should be limited by 38.2% retracement of 0.9200 to 0.8038 at 0.8482. On the downside, below 0.8196 minor support will bring retest of 0.8038. Firm break there will resume larger down trend.

In the bigger picture, long term down trend from 1.0342 (2017 high) is still in progress and met 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.8079 already. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.8801) holds. Sustained break of 0.8079 will target 100% projection at 0.7382.

In the long term picture, price action from 0.7065 (2011 low ) are seen as a corrective pattern to the multi-decade down trend from 1.8305 (2000 high). It's uncertain if the fall from 1.0342 is the second leg of the pattern, or resumption of the down trend. But in either case, sustained trading below 61.8% retracement of 0.7065 to 1.0342 at 0.8317 will pave the way back to 0.7065.

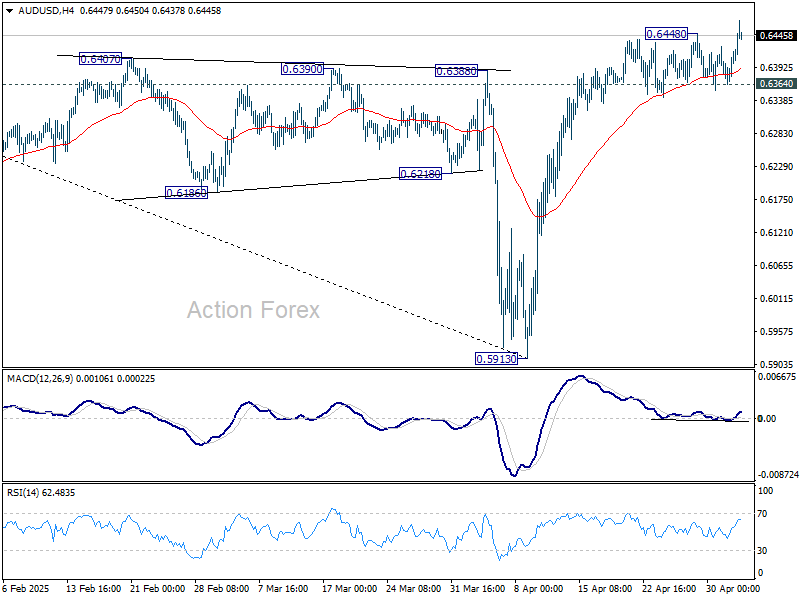

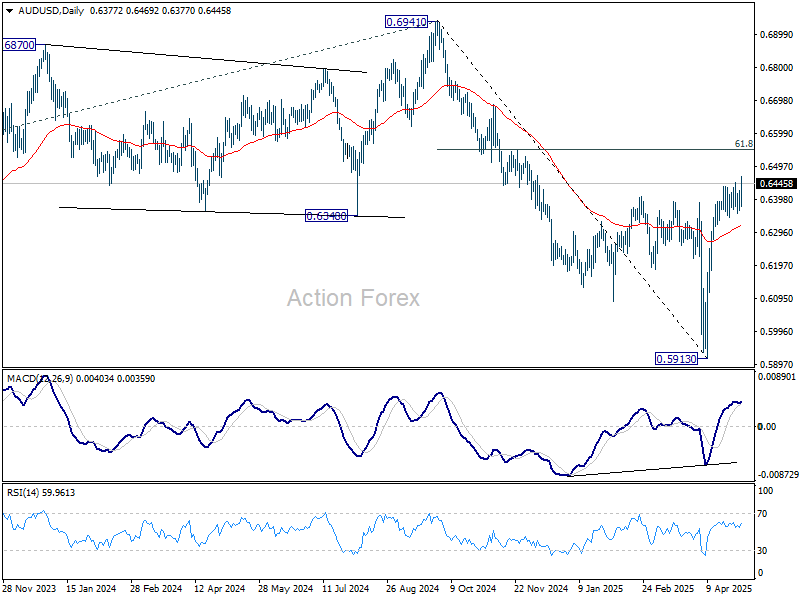

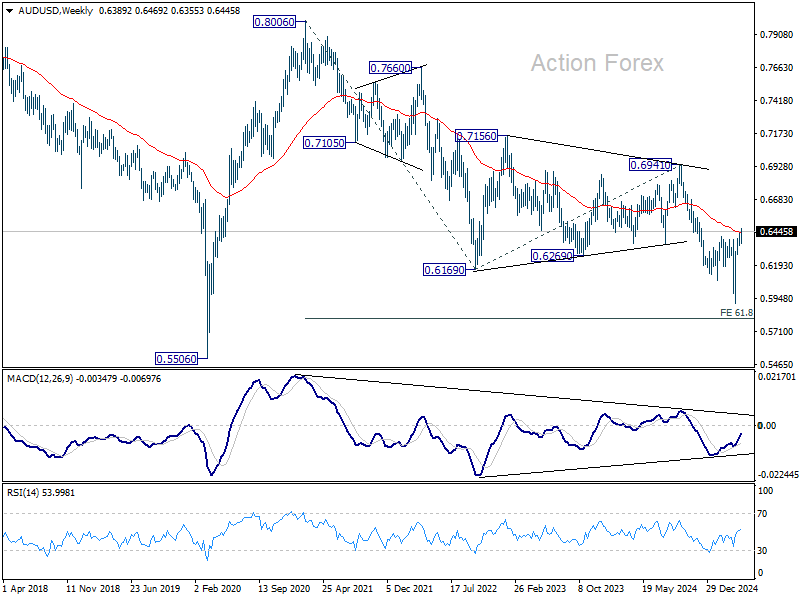

AUD/USD Weekly Report

AUD/USD's rise from 0.5913 resumed last week with late upside breakout. Initial bias is now on the upside this week for 61.8% retracement of 0.6941 to 0.5913 at 0.6548. On the downside, though, break of 0.6364 support will indicate short term topping, and turn bias to the downside for 55 D EMA (now at 0.6319).

In the bigger picture, as long as 55 W EMA (now at 0.6443) holds, the down trend from 0.8006 (2021 high) should resume later to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. However, sustained trading above 55 W EMA will argue that a medium term bottom was already formed, and set up further rebound to 0.6941 resistance instead.

In the long term picture, prior rejection by 55 M EMA (now at 0.6764) is taken as a bearish signal. But for now, fall from 0.8006 is still seen as the second leg of the corrective pattern from 0.5506 long term bottom (2020 low). Hence, in case of deeper decline, strong support should emerge above 0.5506 to contain downside to bring reversal.

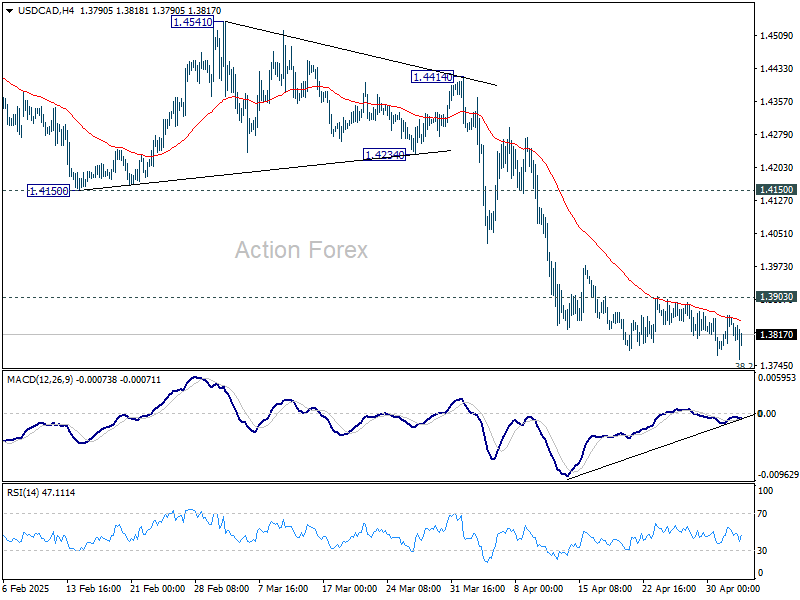

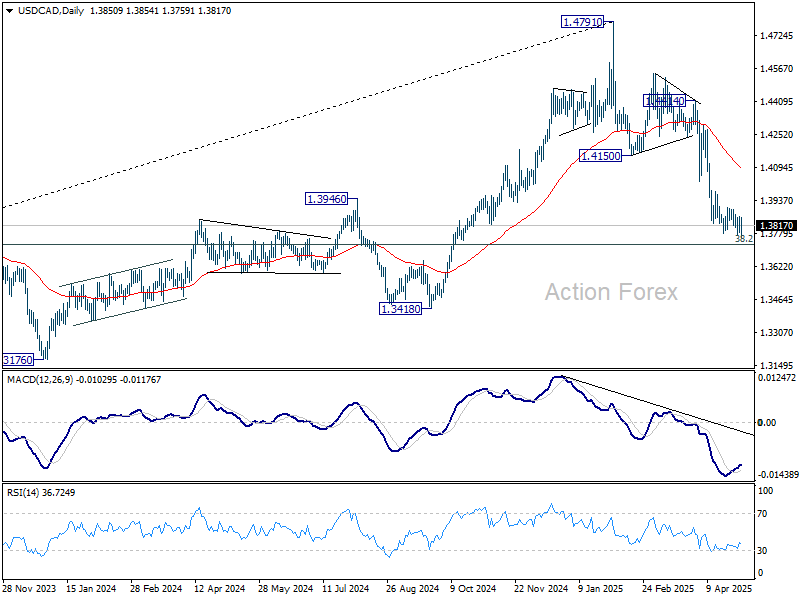

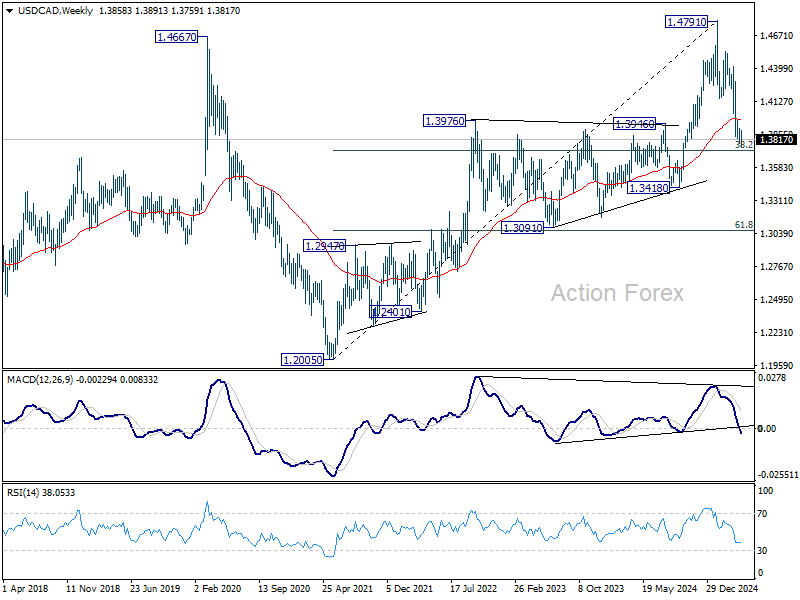

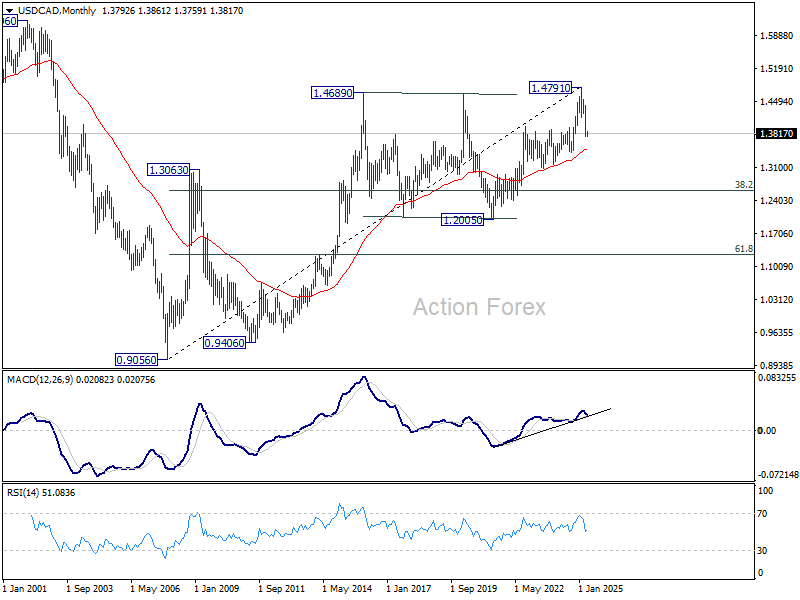

USD/CAD Weekly Outlook

USD/CAD gyrated lower last week despite weak momentum. Initial bias is mildly on the downside this week for 1.3727 fibonacci level next. On the upside, however, firm break of 1.3903 resistance should indicate short term bottoming, and turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 1.4791 medium term top could either be a correction to rise from 1.2005 (2021 low), or trend reversal. In either case, further decline is expected as long as 1.4150 resistance turned support holds. Firm break of 38.2% retracement of 1.2005 (2021 low) to 1.4791 at 1.3727 will pave the way back to 61.8% retracement at 1.3069.

In the long term picture, as long as 55 M EMA (now at 1.3488) holds, up trend from 0.9056 (2007 low) should still resume through 1.4791 at a later stage. However, sustained trading below 55 M EMA will argue that the up trend has already completed, with rise from 1.2005 to 1.4791 as the fifth wave. 1.4791 would then be seen as a long term top and deeper medium term down trend should then follow.

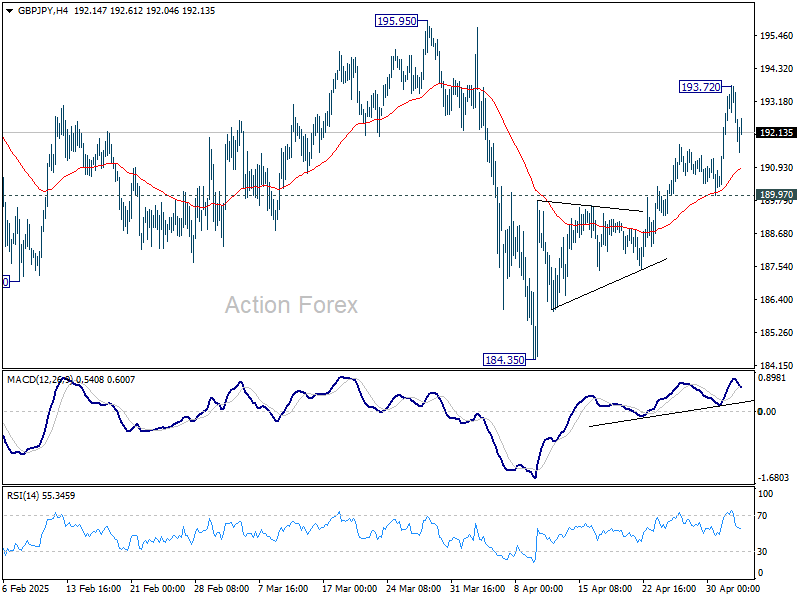

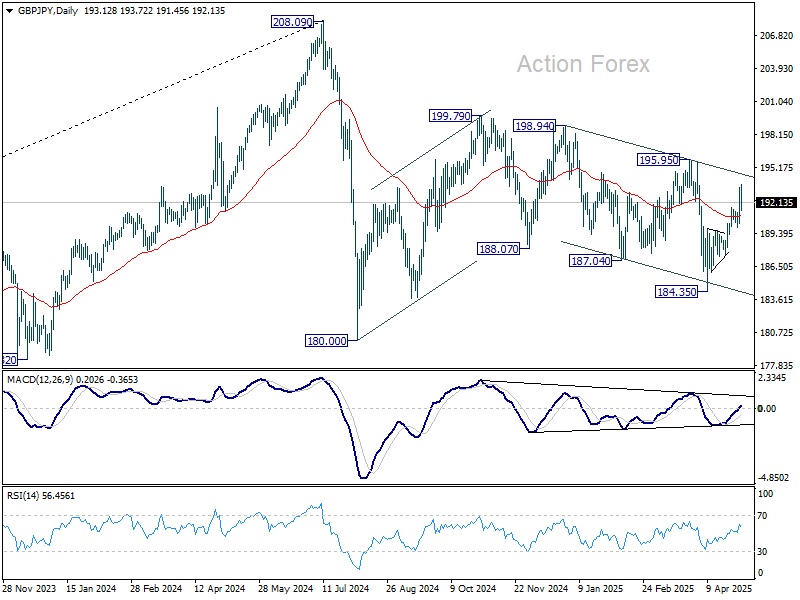

GBP/JPY Weekly Outlook

GBP/JPY's rebound from 184.35 extended higher last week but retreated after hitting 193.72. Initial bias is turned neutral this week first. Further rise is expected as long as 189.97 support holds. Above 193.72 will target 195.95 resistance next.

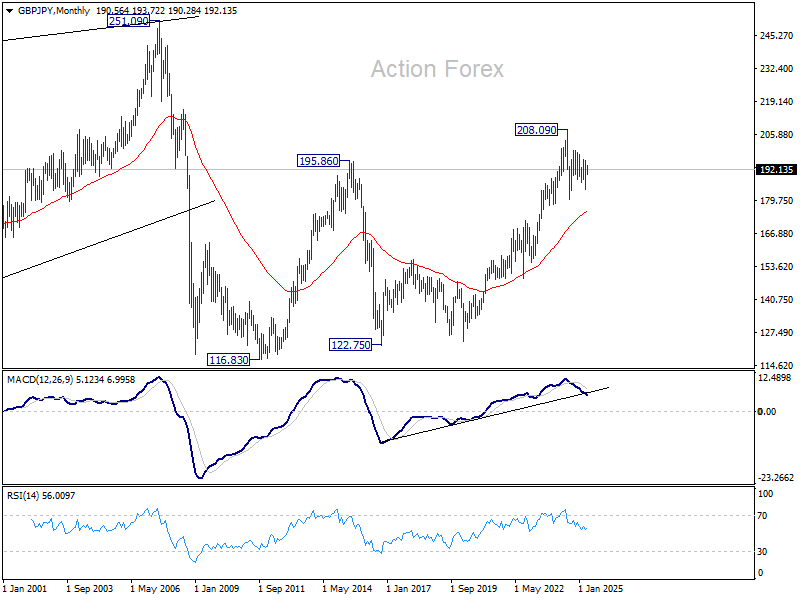

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

In the longer term picture, while a medium term top was formed at 208.09 (2024 high), it's still early to conclude that the up trend from 122.75 (2016 low) has completed. But GBP/JPY is at least in a medium term corrective phase, with risk of correction to 55 M EMA (now at 175.85).

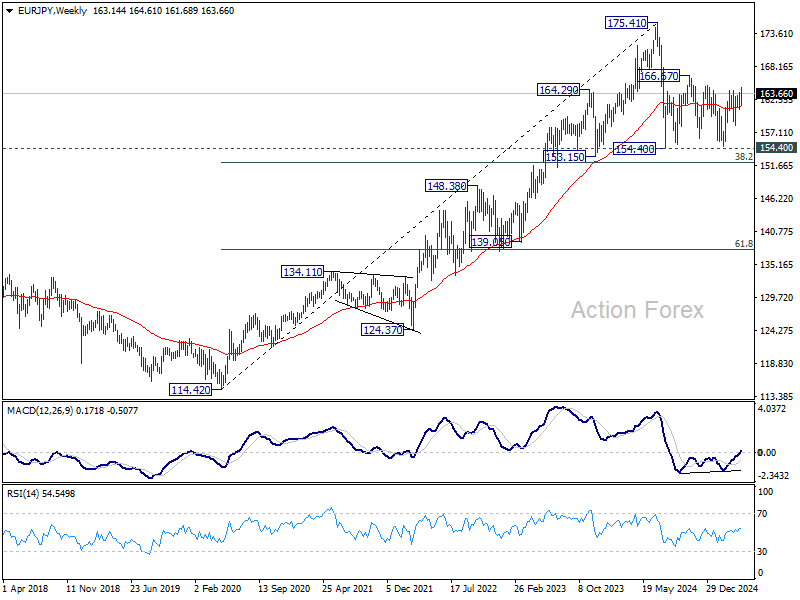

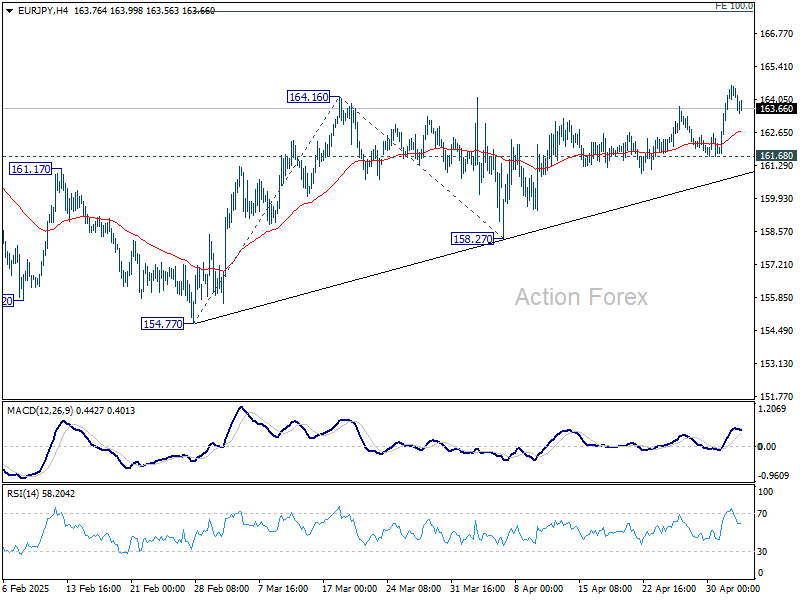

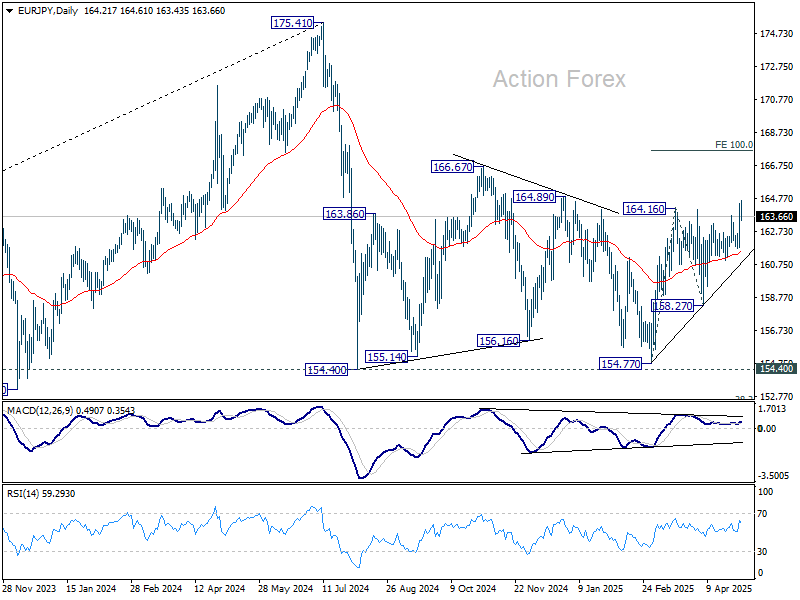

EUR/JPY Weekly Outlook

EUR/JPY's break of 164.16 resistance last week indicates that rise from 154.77 is resuming. Initial bias stays on the upside this week. Next target is 100% projection of 154.77 to 164.16 from 158.27 at 167.66. On the downside, break of 161.68 support is needed to indicate short term topping. Otherwise, further rally is still expected in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

In the long term picture, while 175.41 is at least a medium term top, it's still early to conclude that up trend from 94.11 (2012 low) has completed. A medium term corrective phase is in progress with risk of deeper fall back to 55 M EMA (now at 149.91).