Sample Category Title

Price of a Barrel Brent Oil Slumps to April Lows

Markets

The risk rally continued on Friday. European stocks soared by over 2%, catching up with US gains on Thursday (strong Q1 earnings from the likes of Microsoft and Meta). US stock markets gained over 1%. Late on Thursday, Chinese media reported that the US has been proactively reaching out to China through various channels, seeking to negotiate on tariff issues. These vibes spilled into Friday’s session with the WSJ reporting that Beijing is considering ways to address the US administration’s concerns over the country’s role in the fentanyl trade as an icebreaker to get onto speaking terms. An official statement from China’s Commerce Ministry also indicated that it was weighing starting talks with the US, expressing Beijing’s wish to “show sincerity” to talk. In previous official comments, China set slashing steep tariffs as a first condition for negotiations. Gradually walking back on the most dramatic trade talk triggered a huge short squeeze on stock markets since April 9 (90-day pause) with investors and markets putting worst case scenarios to bed. The US is expected to land some first bilateral trade deals (eg India) this week which could give some guidance on how far early tariff rates can be effectively reduced. In the meantime, it helps that economic hard data confirm that thinking, though we agree that quite some frontloading is involved and that sentiment data paint a grim picture. Friday’s strong April payrolls report was testament to the hard data narrative. The US economy added 177k jobs, beating 138k consensus (but 58k downward revision to previous two month’s numbers). The unemployment rate stabilized at 4.2% with a slightly higher participation rate (62.6% from 62.5%). Wage growth was broadly in line with consensus as well (+0.2% M/M & +3.8% Y/Y). The big market reaction to the numbers shows that it was still positioned for worse news. The US yield curve bear flattened with yields rising by 6.6 bps (30-yr) to 12.4 bps (2-yr). US money markets slashed June Fed rate cut bets from around 60% to 30%. Our preferred scenario remains one of the extended pause stretching at least over Summer given outsized US inflationary risks and the Fed’s hawkish, but ignored, tone. The dollar erased earlier losses against the euro, falling back from EUR/USD 1.1380 to 1.13. German Bund yields rose by 7.6 bps (2-yr) to 9.4 bps (5-yr) last Friday with an upward surprise in EMU April inflation popping out. Lower energy prices prevented an even bigger increase. Headline, core and services inflation increased by 0.6% M/M, 1% M/M and 1.3% M/M respectively to 2.2% Y/Y, 2.7% Y/Y and 3.9% Y/Y. EMU money markets still bank on aggressive ECB rate cuts, starting in June. We are still in favour of pause to see how the tariff narrative unfolds. The 90-day pause stretches beyond the June meeting. Today’s eco calendar is empty apart from the April services ISM and a $58bn 3-yr Note auction. We expect a wait-and-see attitude going into Wednesday’s FOMC decision. Risk sentiment is reliant on ongoing trade talk/discussions.

News & Views

The price of a barrel Brent oil slumped to the April lows just north of $59 this morning. Losses could stack up all the way to $50 (2018 low) should the April support break. The collapse follows OPEC+’s decision on Saturday to raise supply next month by another 411k barrels. The surprise move follows last month’s one where the oil cartel announced a similar-sized restoration of output, which was three times more than expected. It raises concerns over a supply glut at a time where global demand is tepid. Saturday’s call, just as April’s, is at least partially designed to punish nations including Kazakhstan and Iraq that are producing beyond their quota with lower prices.

Australia’s Labor Party secured a landslide victory in Sunday’s federal elections. It’s on track to win 86 seats, well over the 76 needed to retain its majority, compared to the 2022 election outcome of 77 seats. Sunday’s outcome gives the current and next prime minister Albanese a strong mandate, which seemed unlikely only two months ago. Labor was trailing the Liberal Party in the polls until early March. Albanese during the campaign had pledged a major boost to public spending, covering amongst others billions of dollars on healthcare, increased wage for care workers, subsidies for home solar batteries and childcare services. On the foreign front, Albanese has to cope with Trump’s trade war and an economically weakening Chinese partner. Australian markets approved the clear-cut election results with a rise of the Aussie dollar against an overall weaker USD. AUD/USD appreciates towards the 0.65 area. Australian sovereign yields rise between 2.7 and 5 bps in a bear flattening move.

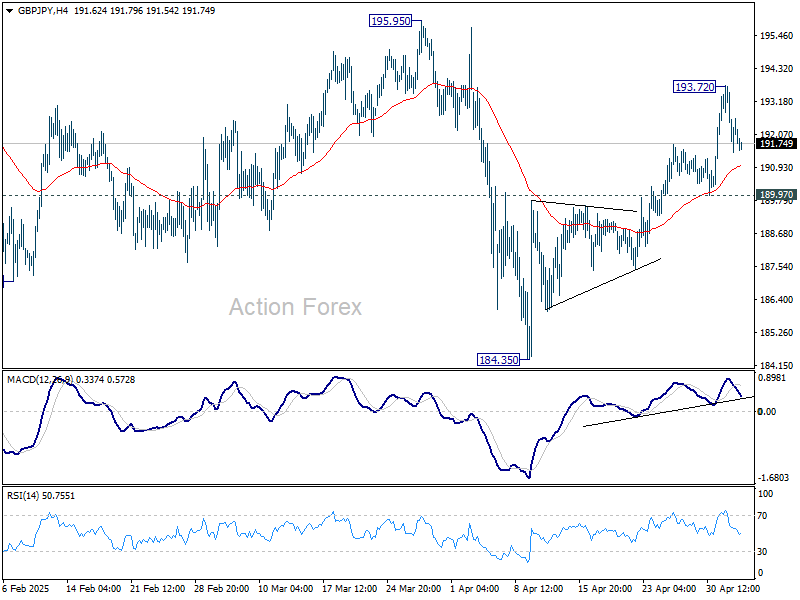

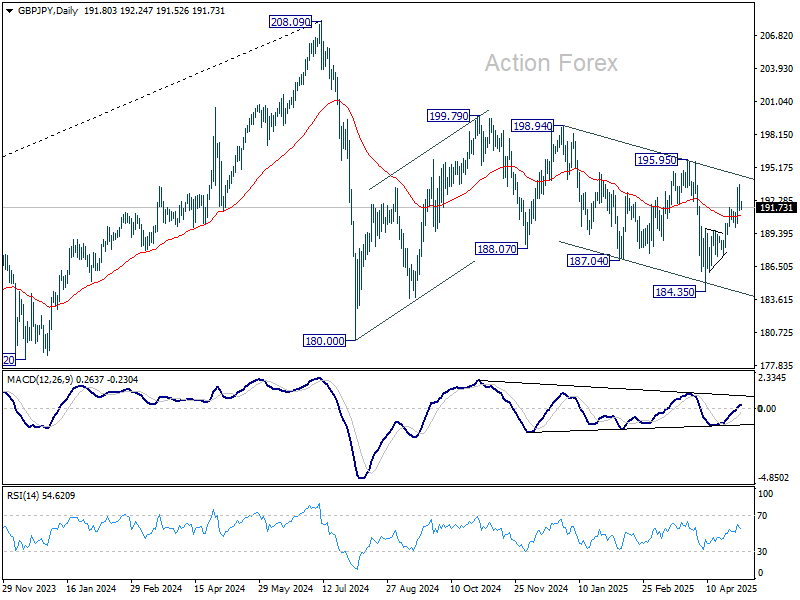

GBP/JPY Daily Outlook

Daily Pivots: (S1) 191.09; (P) 192.83; (R1) 194.17; More...

Intraday bias in GBP/JPY stays neutral for consolidations below 193.72. Further rise is expected as long as 189.97 support holds. Above 193.72 will resume the rise from 184.35 and target 195.95 resistance next.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

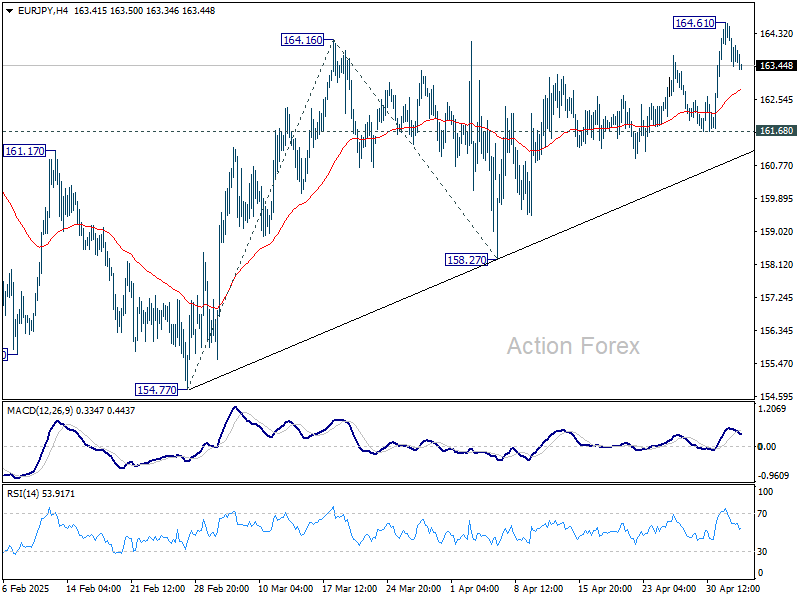

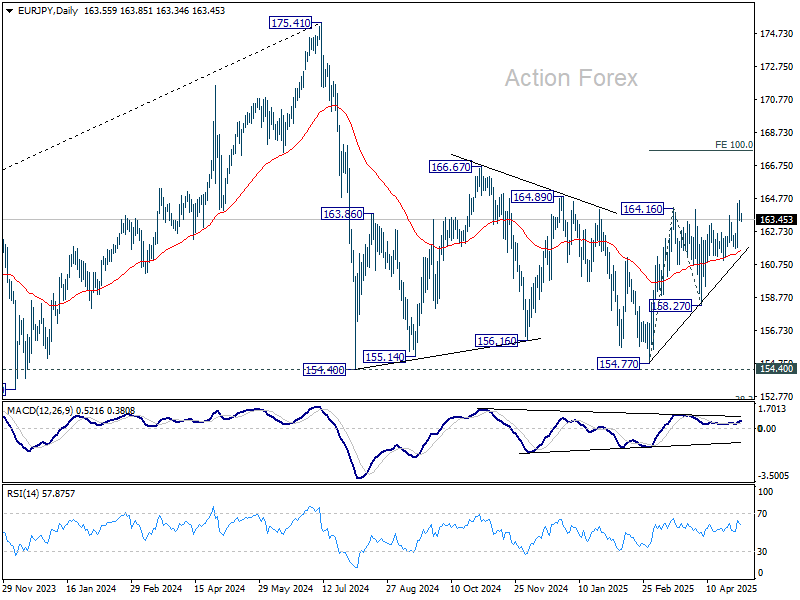

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.36; (P) 164.00; (R1) 164.54; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat, and some consolidations would be seen. Further rally is expected as long as 161.68 support holds. Above 164.61 will resume the rise from 154.77 to 100% projection of 154.77 to 164.16 from 158.27 at 167.66.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

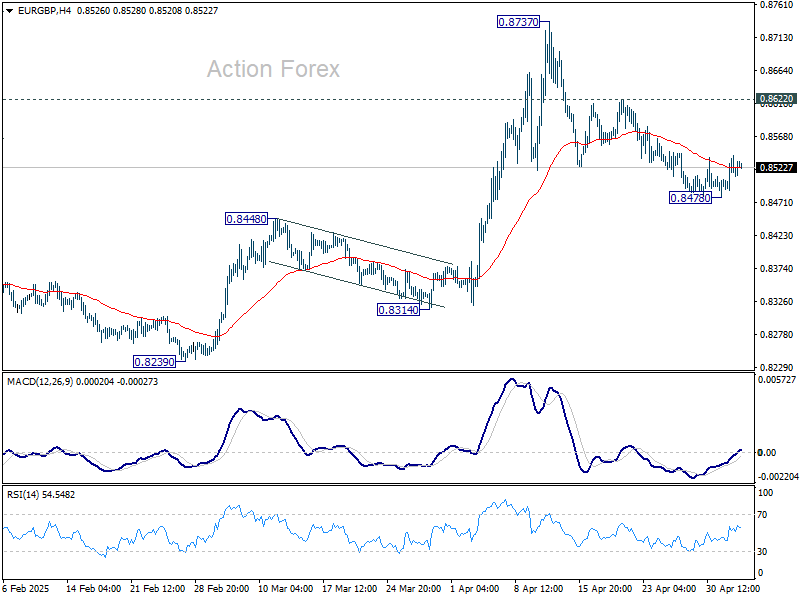

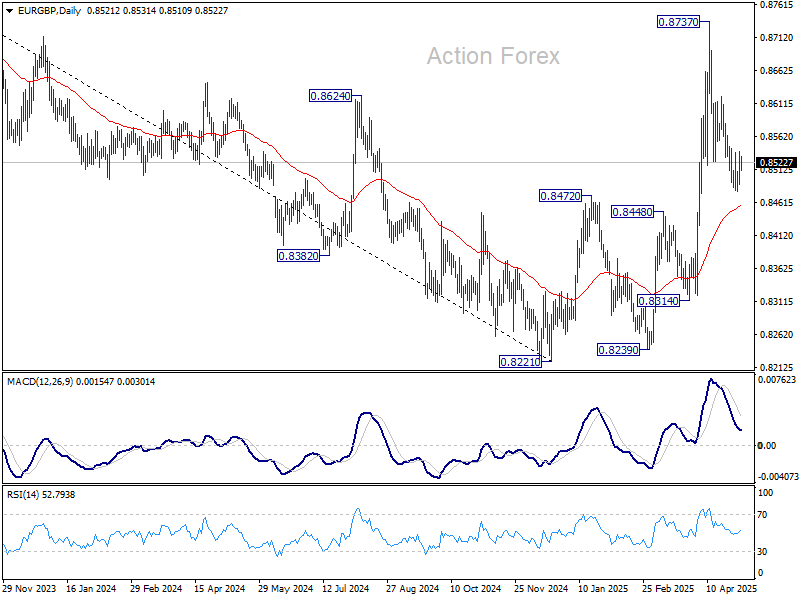

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8491; (P) 0.8516; (R1) 0.8541; More...

Intraday bias in EUR/GBP remains neutral for the moment. On the downside, below 0.8478 will target 55 D EMA (now at 0.8455). Sustained trading below there will suggest that whole rise from 0.8221 has already complete and turn outlook bearish. However, break of 0.8622 resistance will suggest that the correction from 0.8737 has completed, and retain near term bullishness.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will remain the favored case as long as 0.8472 resistance turned support holds.

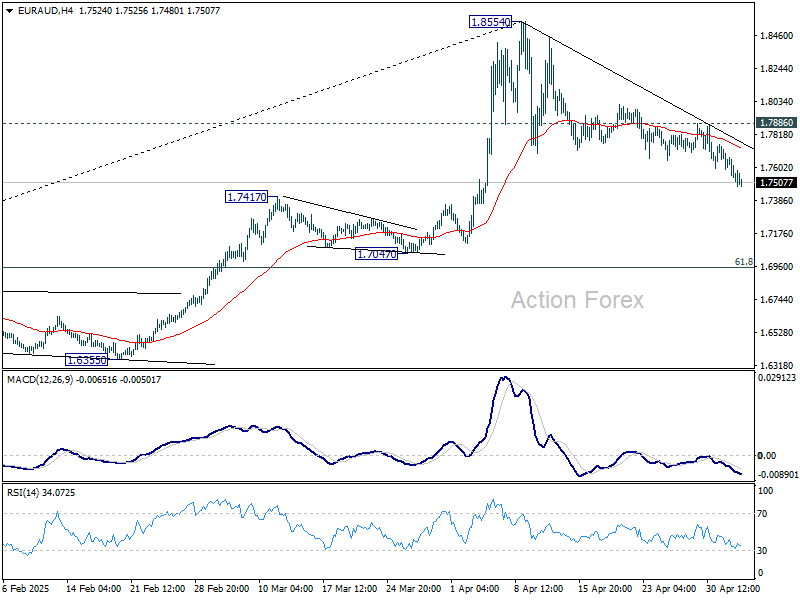

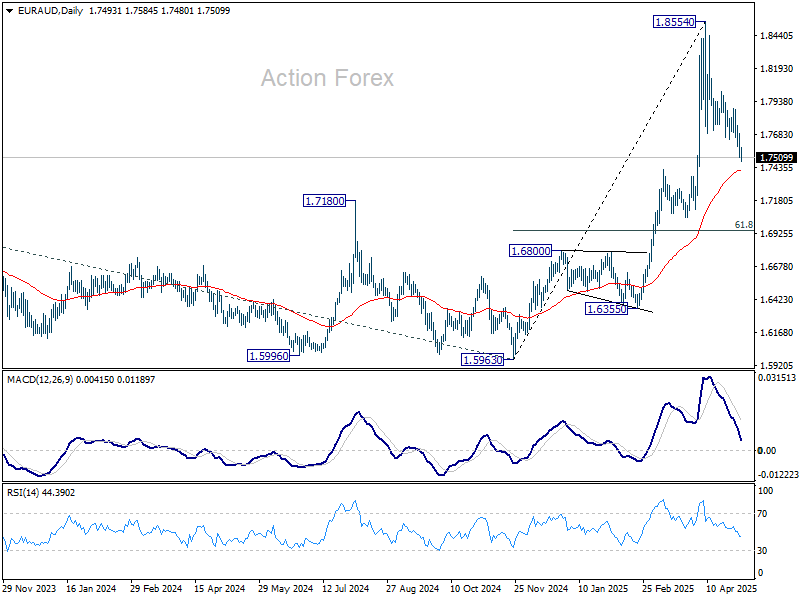

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7467; (P) 1.7588; (R1) 1.7668; More...

Intraday bias in EUR/AUD remains on the downside as fall from 1.8554 is in progress. Sustained break of 55 D EMA (now at 1.7410) will target 61.8% retracement at 1.6953. On the upside, though, break of 1.7886 resistance will turn bias back to the upside for retesting 1.8554 high.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress for 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7062 resistance turned support (2023 high) holds even in case of deep pullback.

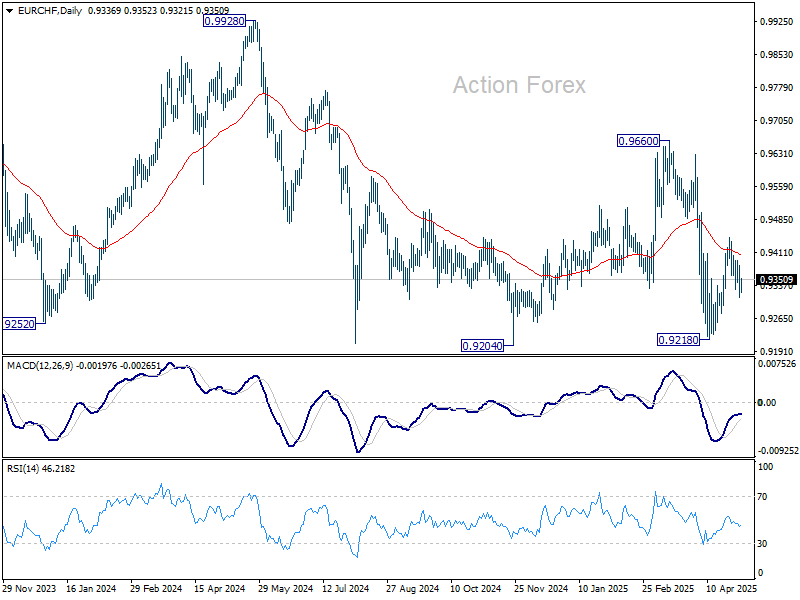

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9306; (P) 0.9347; (R1) 0.9382; More....

Intraday bias in EUR/CHF remains neutral at this point. On the upside, above 0.9445 will resume the rebound from 0.9218, either as a corrective move or the third leg of the pattern from 0.9204. However, break of 0.9274 will suggest that that recovery has completed, and bring retest of 0.9204/18 support zone.

In the bigger picture, prior rejection by long-term falling channel resistance (now at 0.9555) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. This will remain the favored case as long as 0.9660 resistance holds.

Oil Tumbles on OPEC+ Decision to Accelerate Output Restoration

The week begins with a sharp decline in oil prices – around 4% at the time of writing – as OPEC+ announced it would accelerate output restoration by 411K barrels per day, taking the total hike for April, May, and June to nearly 1mbpd, almost half of the 2.2mbpd cuts put in place since October 2022. Since then, OPEC countries have had quotas to limit oil production in order to support prices. The idea was to stabilize oil prices near – and ideally above – the $80pb level.

Now, remember that Saudi Arabia was doing the heavy lifting – cutting an additional 1mbpd at some point – to help the group achieve its goals, while Kazakhstan and Iraq were often accused of not complying fully with their promises. And last week, Saudi Arabia was already hinting that something big was about to happen when it said it was ready to tolerate lower oil prices for a prolonged period. So the weekend news wasn’t a shocker, but the reasons behind the move remain uncertain.

The official communication says the group is bringing barrels back to the market because ‘fundamentals are healthy and inventories are low’. Yet global growth expectations have been crumbling due to a heated trade war between the US and the rest of the world, and rising output only worsens oversupply concerns.

So the real reason must be something else. Some argue Saudi Arabia is punishing OPEC members who showed poor cooperation. Others point to Donald Trump wanting lower oil prices to support his Made-in-US plans and to hurt Russian finances, speeding up the end of the war in Ukraine. Some warn that lower oil prices will do nothing but destroy the US shale industry, which becomes profitable above around $40–50pb. Including capex, land, debt, etc., the breakeven rises to $55–65pb, and for some small companies, fracking costs could reach $70pb – versus just $3–5pb for Saudi Arabia. And remember, around 90% of crude production growth in the last two decades has come from US shale. So that doesn’t align with Trump’s ‘frack frack frack’ energy policy. Meanwhile others wonder whether Saudi is also aiming to push US shale players out of business to increase its market share. We don’t know for sure. The exact motive remains unclear. But the direction of oil prices is clearer than the reasons behind OPEC’s move. If Saudi is ready to dive, oil prices have room to dive further.

US crude tanked to $55.50pb at the open. Brent is down by 3.8%. The bears’ $50pb price target looks easier to reach now than three days ago, and any price rallies will likely offer interesting opportunities to strengthen bearish positions.

PS: Lower oil prices are obviously a straight positive for bringing inflation lower. And last week’s data from the Eurozone showed that any factor helping to tame inflation pressures would be more than welcome, as early reports warned that Eurozone inflation remained unexpectedly steady in April. Core and services inflation – closely watched by the European Central Bank (ECB) – rose, softening dovish ECB expectations.

Still, the combination of falling energy prices, a stronger euro, ECB support, and higher government spending continues to support the view that euro area growth will probably pick up more momentum.

Across the Channel, the Bank of England (BoE) is preparing to announce a 25bp cut when it meets this week due to tariff uncertainties. The British 2-year gilt yield fell more than 35bp since April 2nd – when Trump revealed his mind-blowing tariff rates. The UK is hit by only a 10% tariff, but that’s enough to weigh on growth. However, the strong sterling and expectations that the US tariff war will be disinflationary for Europe and the UK (if nothing due to stronger currencies and Chinese redirecting products to Europe) and give the BoE and the ECB room to cut more than they otherwise would this year.

In the US, the Federal Reserve (Fed) doves are much less optimistic about any imminent rate cut. Chair Powell has made it clear in recent weeks that the inflation trajectory remains highly uncertain due to tariff policy, pushing the Fed to be cautious. Some Fed members seem more open to action, but any move must be driven by data.

Speaking of which, Friday’s jobs data came in mixed. The headline NFP figure beat expectations, and wage growth slowed more than expected – both positives. But the previous two months’ data were revised down by a combined 58K. The unemployment rate remained steady near 4.2%, while the participation rate rose, hinting that more Americans are looking for work. It’s too early to see the full impact of tariffs on the US job market, but it will likely be negative – which supports a dovish Fed policy, to the extent inflation allows.

The next CPI update is due next week. Until then, the Fed will remain in focus, as it is expected to announce no change to its policy this week. But June expectations could change.

The US dollar kicks off the week on a bearish note. Asian currencies are soaring against the broadly weaker greenback, forcing authorities in Hong Kong to step in and buy dollars to protect the USDHKD peg.

Remember, last week was marked by softer trade news. Trump toned down his rhetoric, and there are reports that China is ready to resume talks. The week starts with news that the US will impose 100% tariffs on foreign films. Potential escalation could bring the S&P 500’s 9-day winning streak – its longest since November 2004 – to an end. Futures point to a downside correction at the start of the week.

Euro Area Investor Confidence Set to Regain Lost Ground

In focus this week

Today in the euro area, we receive the Sentix investor confidence indicator, which will give the first status of sentiment in May. The index fell greatly in April as it was conducted just after Trump's "Liberation Day". Now, that equities have rebounded and the tariff outlook seems to be less aggressive compared to a month ago, it is expected that sentiment will recover some of the lost ground.

Additionally, we receive the final euro area PMI data for April on Tuesday and March retail sales data on Wednesday.

On Wednesday in the US, the FOMC meeting takes place, and markets have now almost fully priced out any change for a Fed cut this week following the strong jobs report Friday last week.

On Thursday, we expect the Bank of England (BoE) to cut the Bank Rate to 4.25% in line with consensus and market pricing. Inflation has surprised to the downside over the past months and combined with elevated uncertainty and downside risks to growth from the trade war, we expect the MPC to deliver slightly dovish commentary. Read more in our Bank of England Preview, 2 May.

Also on Thursday, consensus expects Norges Bank to stay on hold at 4.50% at their monetary policy meeting. Recent data figures have been to the neutral side as of late, but if anything to the hawkish side.

Economic and market news

What happened overnight

In oil markets, ICE Brent Crude prices declined some 3.7% due to downwards pressure from the OPEC+ announcement over the weekend to increase oil production in June.

In the trade war, US President Trump initiated a 100% tariff rate on foreign made movies as he seeks to protect Hollywood. This could impact several big media companies significantly, as Walt Disney, Netflix and Universal Pictures all film in foreign countries.

In the US, President Trump stated that he would not remove Fed Chair Powell, despite continuing to call for further rate cuts from the Federal Reserve. This marks a complete reversal from his previous stance on considering Powell's removal.

What happened over the weekend

In the trade war, Beijing said it was considering how to address the concerns about China's involvement in the fentanyl trade to restart trade talks. This follows China's commerce ministry stating that it was assessing recent US requests to engage in discussions. Especially equity markets rallied on the back of both Chinese statements.

In the euro area, HICP inflation remained at 2.2% y/y in April, slightly above initial consensus expectations of 2.1% y/y. The stronger-than-expected data was due to core inflation that rose more than expected to 2.7% y/y from 2.4% y/y in March, presumably a result of Easter occurring in April. We expect headline inflation to average just above the 2% target in the coming months, which supports further rate cuts from the ECB at the upcoming three meetings.

Final euro area manufacturing PMI was revised slightly up in April to 49.0 from 48.7 in the preliminary release. This takes the index on the highest level since August 2022 and makes April data significantly higher than the preliminary consensus expectation of a decline to 47.4. Hence, April did not show the immediate negative impact on growth that was feared in the manufacturing sector, which is most directly affected by tariffs.

In the US, the April Jobs Report was stronger than expected with April NFP at +177k (forecast +130k, Mar. 185k, revised by -58k). Average hourly earnings growth slowed to +0.2% m/m SA (from +0.3) and the unemployment rate remained steady at 4.2%. At the same time, labour supply experienced a significant increase of +518k. Interestingly, while Trump's immigration policies are starting to have an effect on foreign-born labour supply (-700k), domestic labour supply increased very sharply (+1.2M). All-in-all, it was a solid report, pushing EUR/USD lower and UST yields higher. Markets have now almost fully priced out any change for a Fed cut this week, and markets are also pricing in less than a 50% chance for a Fed cut in June.

In Norway, the non-seasonally adjusted unemployment rate dropped to 1.9% in April, below expectations at 2.0%. New vacancies rose significantly to above 50', the highest since 2022 so demand for labour continued to be very solid into Q2. Figures should be neutral ahead of Norges Bank next week, but if anything to the hawkish side.

Manufacturing PMI dropped to 46.1 in April, indicating a sharp slowdown in manufacturing activity into Q2. Details were also weak, as new orders dropped to 38.2 and production to 46.5, whereas employment was more stable from 54.2 to 53.0. The Norwegian PMI can be very volatile on a monthly basis, especially in an Easter month like April. Hence, we assess the numbers with a pinch of salt.

Equities: Last week delivered yet another remarkably strong performance for equities, with gains recorded across all five trading days. Once again, the US led the charge, underpinned by renewed optimism and increasingly constructive expectations around the trajectory of the trade war. With the rally, markets are now clearly above the 2 April (Liberation Day) levels. Notably, Friday marked the ninth consecutive positive session for the S&P 500. Cyclicals continue to outperform in the current environment, though in Europe, defensives performed broadly in line with cyclicals last week. This was due to the notable shift in the pharma sector performance, which staged a significant comeback, likely reflecting reduced investor concern over trade-related risks and tariff threats to the industry. In the US on Friday, Dow +1.4%, S&P 500 +1.5%, Nasdaq +1.5%, Russell 2000 +2.3%. Asian equities are trading higher this morning, while futures in both the United States and Europe point slightly lower.

FI&FX: Global bond yields rose on Friday on the back of stronger US Labour market data and ahead of this week's main event the FOMC meeting on Wednesday, where the Federal Reserve is expected to stay on hold despite the political pressure from the White House. There will again be focus on the US Treasury market as the Treasury has to sell USD 125bn in 3Y, 10Y and 30Y bonds during the week. In the currency market, EUR/USD continues to be range-trading. Oil prices declined as OPEC agreed on increasing production.

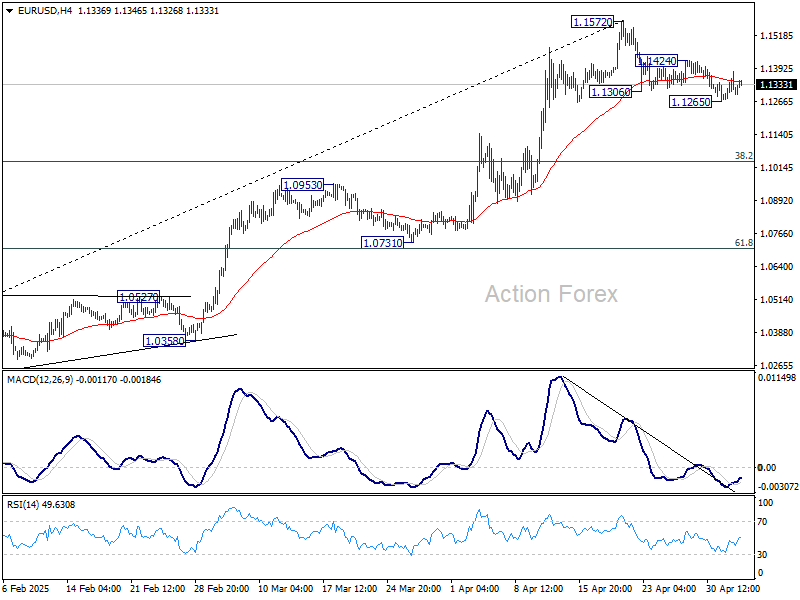

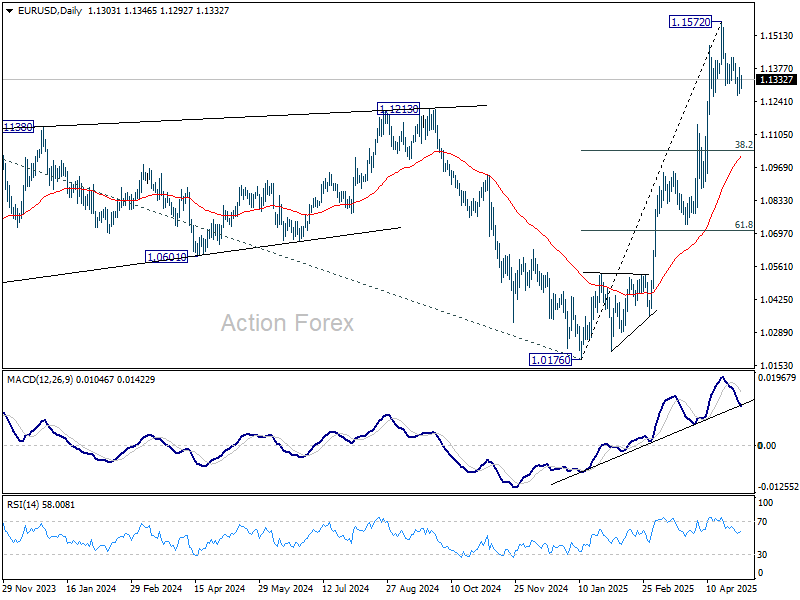

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1257; (P) 1.1319; (R1) 1.1364; More...

Intraday bias in EUR/USD remains neutral at this point. On the downside, below 1.1265 will resume the corrective fall from 1.1572 short term top. But downside should be contained by 38.2% retracement of 1.0176 to 1.1572 at 1.1039. On the upside, break of 1.1424 will suggest that the correction has completed and bring retest of 1.1572 high.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0808) holds.

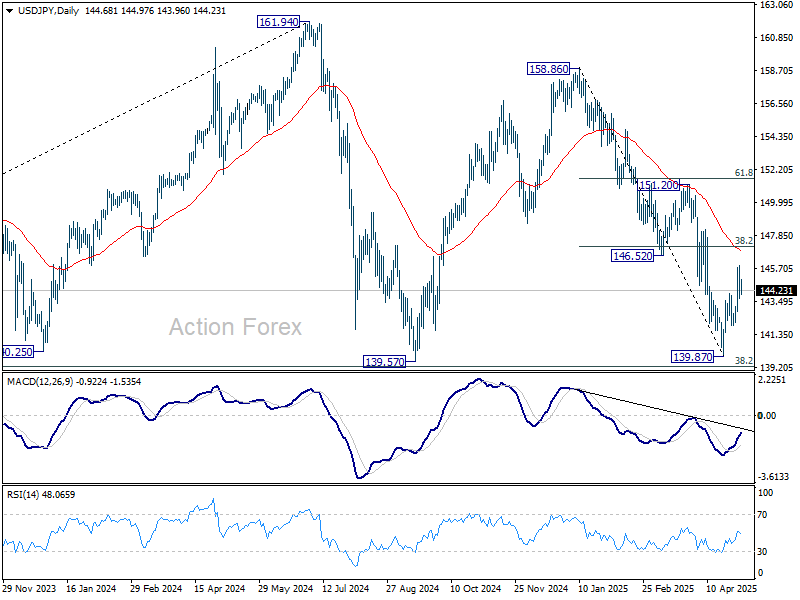

USD/JPY Daily Outlook

Daily Pivots: (S1) 143.82; (P) 144.87; (R1) 146.01; More...

Intraday bias in USD/JPY remains neutral for the moment. Overall near term outlook will stay bearish as long as 38.2% retracement of 158.86 to 139.87 at 147.12 holds. Break of 141.96 will argue that the rebound has completed as a corrective move. Retest of 139.87 should then be seen next in this case.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.