Sample Category Title

Europe’s Opening Bell: Stock Indices Rise on Positive US-Japan Talks, ECB Meeting Comes into Focus

Asian stocks rose slightly on Thursday, and the dollar gained a bit as traders evaluated trade talks between the U.S. and Japan, while concerns over tariffs introduced by President Donald Trump kept the mood cautious.

Markets were also digesting comments by Federal Reserve Chair Jerome Powell yesterday.

Fed Chair Jerome Powell gave a firm hawkish message, dismissing hopes for rate cuts despite inflation worries. He projected higher inflation and a weaker jobs market due to tariffs, while focusing mainly on inflation control. This stance, paired with Trump tolerating market volatility, is likely to leave equities under pressure.

Gold prices took a breather in the Asian session after printing a fresh high around $3357/oz in early Asian trade. At the time of writing Gold is trading at $3325/oz, down about 0.50% on the day. The move does not appear to be down to sentiment but could be due to profit taking ahead of the Easter break.

Oil prices rose slightly after US Treasury Secretary Scott Bessent made a comment that President Trump is ready to ensure Iran's oil exports drop to zero. Oil is on course for another weekly gain.

As we head into the European session, sentiment remains fragile after TSMC noted that Trump policies would hurt growth.

TSMC’s net income jumped 60.3% from last year to NT$361.56 billion, and its revenue grew 41.6% in the March quarter to NT$839.25 billion. However, the company is facing challenges due to U.S. President Donald Trump's trade policies, which include tariffs on Taiwan and stricter export rules for its clients Nvidia and AMD.

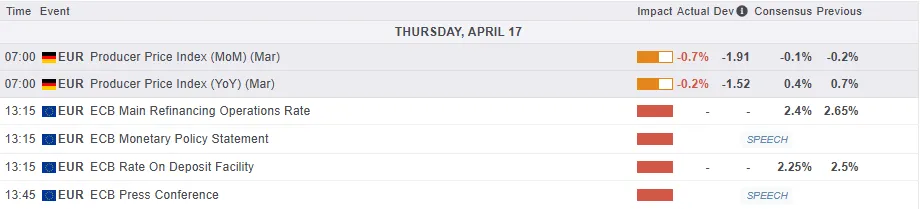

Economic data releases

From a data perspective, the major event for the European session will be the ECB meeting today with a rate cut likely in my opinion. Market participants have for a long period been pricing in a 25bps cut, so the euro is unlikely to be strongly affected.

There is no reason why the Euro cannot extend its gains against the US Dollar, barring a strong recovery from the Greenback.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - Crude Oil

From a technical standpoint, crude oil prices have broken above a significant resistance level after comments on Iranian oil by US Treasury Secretary Bessent.

After a period of consolidation, are oil prices ready to explode?

Explode might be the wrong word given the fragile sentiment markets are currently experiencing. From a technical standpoint though the break of the 66.42 handle is significant as crude has spent the majority of April testing this level.

There is significant resistance ahead and with global dynamics still a worry there is a chance that the breakout may not have the legs to continue.

If a move higher materializes, immediate resistance may be found at 68.17, 68.58 and of course the psychological 70.00 handle.

A move lower which we are seeing in early European trade, could bring support at 64.36, 62.81 and 61.00 into focus.

Crude Oil Four-Hour (H4) Chart, April 17, 2025

Source: TradingView.com (click to enlarge)

Pound Among the Winners Boosted by US Dollar Weakness and Rate Cut Prospects

The GBP/USD pair climbed for seven consecutive days, reaching 1.3210, before experiencing a slight dip on Thursday. This marks the longest sustained rise for the currency pair since July last year, with the pound’s strength primarily driven by a weakening US dollar.

Key factors influencing GBP/USD movements

Fundamentally, the outlook remains mixed. The UK’s Consumer Price Index (CPI) fell more than anticipated in March, with annual inflation dropping to 2.6% and services sector inflation easing to 4.7%. This has alleviated some pressure on the Bank of England (BoE), prompting markets to adjust their expectations for monetary policy easing.

Traders are now pricing in rate cuts of around 85 basis points by year-end, with the first reduction widely expected in the coming months. By December, there is a greater than 50% probability of a further cut, as slowing inflation could give the BoE more flexibility to support the economy and households amid ongoing trade uncertainties.

Technical analysis: GBP/USD outlook

H4 Chart Perspective

- The GBP/USD pair recently completed an upward wave, peaking near 1.3290

- A downward impulse is now unfolding, targeting 1.3165

- A potential rebound towards 1.3222 may follow before a possible decline to 1.2990

- This outlook is supported by the MACD indicator, where the signal line has exited the histogram area and is trending sharply downward

H1 Chart Perspective

- The pair consolidated around 1.3222 before breaking lower

- The immediate downside target is 1.2880, followed by a potential retest of 1.3222 from below

- The Stochastic oscillator reinforces this view, with its signal line below 50 and descending towards 20

Conclusion

While the pound benefits from a softer dollar and shifting rate expectations, technical indicators suggest potential near-term volatility. Traders should monitor both macroeconomic developments and key technical levels for further directional cues.

Cliff Notes: Patient Posture

Key insights from the week that was.

In Australia, the RBA Minutes from the April meeting provided some extra colour around the Policy Board’s deliberations. Despite pre-dating President Trump’s ‘Liberation Day’ tariff announcements and the subsequent volatility in markets, many of the statements around the potential impact on Australia remain relevant, especially that “the effects on GDP growth and inflation in Australia could be relatively modest… reflect[ing] Australia’s limited direct trade exposure to the United States, additional policy support in China and Australia’s flexible exchange rate.” Still, they note that the risks to inflation were “more two-sided” depending on the balance between upside factors such as supply-side disruptions and a weaker exchange rate, and downside factors like weaker global demand and trade diversion away from the US. The Board noted that having a fresh set of forecasts alongside new information around inflation, wages and the labour market will “have a considerable bearing on their decision” at the next policy meeting on May 19-20. At that meeting, Westpac anticipates the Board will deliver a 25bp rate cut, bringing the cash rate to 3.85%.

On the data front, this week’s labour force data, was a bit of a mixed bag. There was only a partial bounce-back in labour supply, seeing the participation rate hold broadly steady at 66.8%. Labour demand looks to have largely moved in tandem, with employment rising +32k, falling short of expectations. Measures of labour market slack were therefore little changed, with the unemployment rate increasing only 0.01ppt. Overall, the RBA are likely to see this data as broadly in line with their expectations, still reflecting a degree of ‘tightness’ relative to full employment. Ultimately, the Q1 CPI data, due April 30, will prove to be a critical input to their May decision.

This week was not short of excitement. FOMC Chair Powell had a clearer tone. In a speech to the Economic Club of Chicago, he noted that the Fed’s “obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing problem”. This, alongside his previous references to Teal Book modelling through Trump’s first term, reaffirms his commitment to prioritising managing inflation risks over growth. This sentiment has been echoed by the Bank of England and Bank of Canada who have been quick to point out that they will allow fiscal policy to support growth, particularly if its decline is caused by supply-side factors.

The Bank of Canada kept rates steady this meeting after seven consecutive rate cuts. The pause comes as the central bank assesses the impact of trade policy with the US and its uncertain impact on the Canadian economy. Governor Tiff Macklem noted that the BoC would be ‘less proactive than usual until we have greater clarity.’ Macklem doubled down on prior comments that monetary policy cannot offset the impact of a trade war, only maintain price stability. Instead of a central forecast, the monetary policy report published two forecasts one which had minor deviations from the previous set of forecasts and another showing a recession caused by trade tensions. The overall messaging suggests the balance between growth and inflation is once again slowly being nudged towards inflation. Further moves down will come after careful consideration and confidence that inflation and inflation expectations are contained.

In the UK, CPI data for March showed a downtick in inflation. The headline rate fell by 0.2ppt to 2.6%yr while the core rate ticked down to 3.4%yr. The deceleration came from the services component, which rose 4.7%yr down from 5.0%yr. These figures came after a mixed labour market report. While the official labour force statistics indicated employment increased by 206k in February, administrative data from tax authorities was down 78k in the month. Average weekly earnings growth over the three months to February were unchanged at a downwardly revised 5.6%yr. Private sector wages excluding bonuses were also unchanged at 5.9%. While progress on inflation is being made, stubbornness in wages will keep the BoE attentive to inflation risks. Still, we expect the central bank to cut rates in the May meeting by 25bps justified by the progress on inflation and emerging growth risks from a slowdown in global trade.

In China, Q1 GDP came in stronger than anticipated at 5.4%yr and rose 1.2% in the quarter. The official press release was quick to attribute the 'positive momentum' to effective macro policy by authorities. Monthly activity data for March also painted a solid picture of the economy. Retail sales rose 4.6%yr on a year-to-date basis supported by spending generally seen during the Lunar New Year -- household appliances, furniture and services. Industrial production lifted 6.5%yr/ytd far exceeding expectations. While the high-tech manufacturing sector continues to expand at a solid pace, this quarter also saw a solid uptick in coal and crude oil production. The 4.2% gain in fixed asset investment was supported not only by state-owned enterprises but also by private investment which has been declining since August 2024. All this offset the 9.9%yr decline in property investment. The data played well into the narrative authorities in China want to convey -- China is a thriving economy and a solid trade partner. Authorities can point to its solid manufacturing sector and their policy decisions to back up their claims. We retain our view that the Chinese economy will hit its growth target of 5.0% for 2025 supported by further policy measures as the authorities see fit and growth in the high tech manufacturing sector.

Our updated views on the domestic and global economy alongside forecasts can be found in our Market Outlook for April 2025.

TINA McRAE Says ‘Watch Out Ahead!’

While on a client trip through Europe and North America, I have seen investors go through all five stages of financial market grief about the US: confusion, fatalism, denial, revulsion – and reallocation

What a time to be on a client trip through Europe and North America. The ‘US exceptionalism’ narrative that prevailed between the election and inauguration had already broken by mid-March. As the news unfolded in April and daily market convulsions ensued, I noticed a deeper thread in the questions and observations from clients, and also from peer chief economists at an international meeting in Basel: the mood has shifted from ‘US exceptionalism’ to ‘US revulsion’.

Prior to ‘Liberation Day’, and in the first few days after, many institutional and official sector investors simply didn’t know which way to jump. They had little conviction about the direction of the market and were therefore taking little risk. The next stage of market grief after the freeze of confusion was a kind of fatalism. Yes, the US looks a lot less attractive and the US dollar is overvalued, they would say, but nothing is deeper and more liquid than the US Treasury market; one can’t get out of it. This is the ‘TINA problem’ – There Is No Alterative – that we have discussed previously.

A couple of US-based clients were detouring through the denial phase of grief. They highlighted the US’s entrepreneurial dynamism and were holding on to the prospect that the US would continue to enjoy a growth differential over other Western economies, perhaps following some unspecified deregulation by the Trump administration. Most US-based contacts, though, were even more strongly in the Revulsion phase than their European peers. As one US-based client commented, “America is cooked”.

That’s the thing with narratives. Once you start to see the cracks in a narrative, you start to question things more broadly. Tariff policy and bullying of close allies opened up the crack. But then the high valuations in the equity market, previously shrugged off, start to look more concerning. So does the parlous fiscal position of the US government and the incapacity of the US political system to solve this and other problems. Then some of the wilder ideas of Trump administration officials – like coercively converting US Treasury bonds to non-marketable zero-coupon paper – start to be seen as genuine – and alarming – possibilities. The previously unthinkable becomes plausible.

Then came the revulsion, the simultaneous sell-off in the US dollar, bonds and equities. There is still a TINA issue – There Is No Alternative to the US Treasury market. Selling out of US markets entirely is infeasible, for all the talk about US markets becoming uninvestible. There is, however, also McRAE – Markets Can Reallocate Easily. Right now everyone wants to be at least a bit less long US markets. Thus the final stage of market grief is reallocation. And because it is flows that determine pricing, not legacy stocks, with reallocation comes repricing: TINA McRAE.

What, then, are investors and asset managers looking to reallocate into as they reallocate out of the US? Everywhere, but for now mostly Europe; it is the ‘adjacent possible’. Even before Liberation Day, we heard, equity investors were looking at Europe in a more positive light. This is especially true for the defence sector. The Trump administration’s treatment of Ukraine, Canada and its NATO allies has been as much behind investor revulsion as the chaotic tariff policies. Germany’s constitutional change and pivot to increased defence spending was something of a catalyst for the shift in thinking, too.

More broadly, people are noticing that Greater Europe – including not just the euro area or even the EU but also others in the region such as the UK, Switzerland and Norway – represents an enormous and reasonably integrated economic market, even if not an integrated and homogeneous bond market. It is also a region that has been driven by the Trump administration’s behaviour to seek ways to extricate itself from dependence on US defence and tech sector vendors. On this front, broader cooperation with Canada and Australia – a kind of ‘Eurovision plus one’ grouping – was widely discussed in my recent meetings with clients. (Canadian clients were already aware and others interested to hear about Canada’s decision to purchase Australia’s JORN over-the-horizon radar technology.)

Within this broader pivot of views, a lot depends on how the trade dispute plays out from here. The tariff rates announced on Liberation Day are too self-destructive to stand. It was therefore no surprise that a 90-day pause on most of the highest rates came soon after, and a further carve-out for certain tech items. Expect more unilateral concessions by the Trump administration, though probably dressed up to look like a deal. And if the result is that most countries, including Asia outside China, end up being tariffed at 10% like Australia, New Zealand and the penguins, all that will happen is that US consumers end up paying more. Nobody will shift the location of production for the sake of a 10% tariff, not when the currency of the tariffing nation is already at least 20% overvalued.

The Chinese reaction and escalated bilateral tariffs will be a tougher nut to crack. Clearly the Chinese authorities have assessed that China can outlast the US and withstand the disruption to trade. At these tariff levels, trade between the two nations will simply stop, other than in items already exempted. While US demand for Chinese exports is an important engine of China’s growth, it is not the only one. Autonomous domestic demand in the rest of Asia is becoming at least as big a driver of China’s export growth lately. And together with some inevitable domestic stimulus, this could be enough to ride out the hit to growth while it redirects trade elsewhere. The US, on the other hand, will only have a few months before the pre-tariff rush to build up inventories is depleted, prices spike and shelves start to empty.

It is because we expect the Trump administration to crack and roll back its tariffs further that we see the US as teetering on the brink of recession but not necessarily falling in. Meanwhile, China will again stimulate, including by boosting capacity in advanced manufacturing. This is disinflationary for the rest of the world and – importantly for Australia – when coupled with measures targeting infrastructure and residential property, supportive of iron ore demand. China’s high levels of debt, deflation and sub-national fiscal imbalances are all genuine medium-term challenges. In the short term, though, China looks better placed to muddle through than the US.

The deeper reason for this is that, like Europe, China retains state capacity to respond to challenges, even when the necessary actions are uncomfortable. By contrast, the policy chaos of the Trump administration is in many ways the culmination of a decades-long decline in capacity for collective action. Consider that the President’s power to impose tariffs stems from an Act of Congress. Congress could amend or repeal that Act, but almost certainly won’t.

A consequence of that loss of state capacity – and loss of trust – is the current revulsion phase of market repricing. The tariffs may well be rolled back quickly; if so, some of the current sell-off may prove overdone. Even in that event, though, lasting damage has been done to the US’s reputation as a reliable partner and investment destination. TINA McRAE is out there: a more volatile financial landscape, more diversified and less centred on the US. Asset allocations, hedging strategies and business models will all need to adapt, and soon.

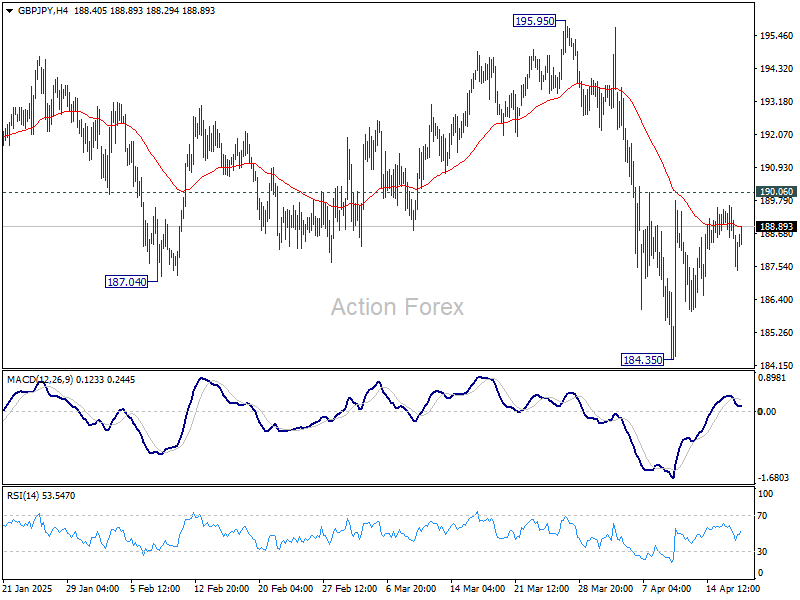

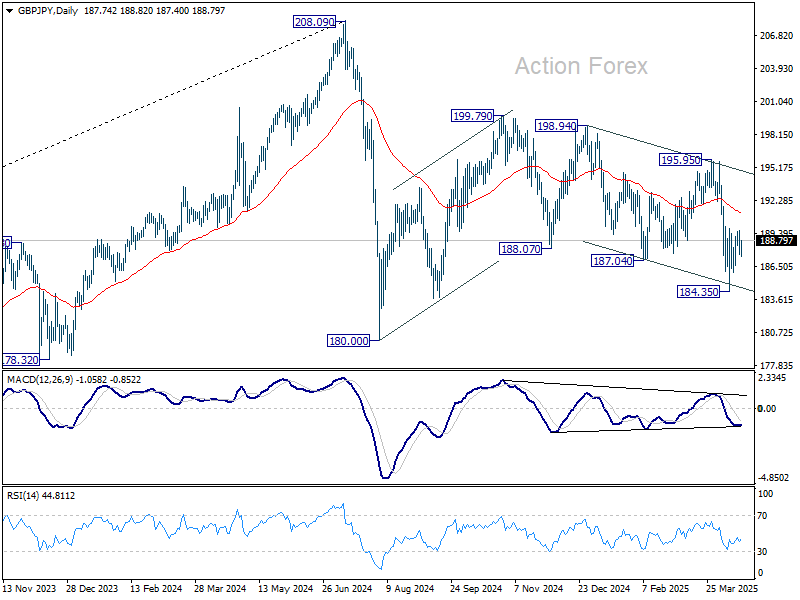

GBP/JPY Daily Outlook

Daily Pivots: (S1) 187.02; (P) 188.34; (R1) 189.11; More...

Intraday bias in GBP/JPY stays neutral for the moment,, and more consolidations would be seen above 184.35. Risk will remain on the downside as long as 190.06 resistance holds. Below 184.35 will target 180.00 low. Nevertheless, break of 190.06 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

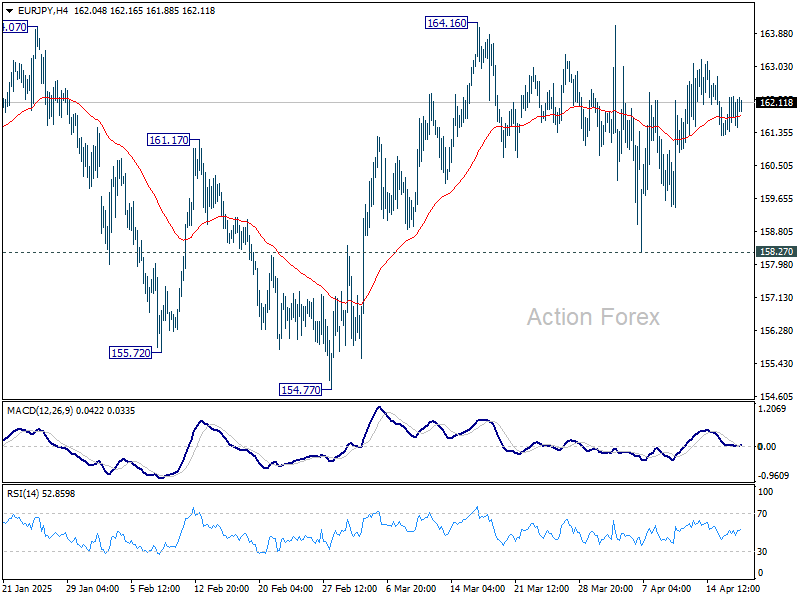

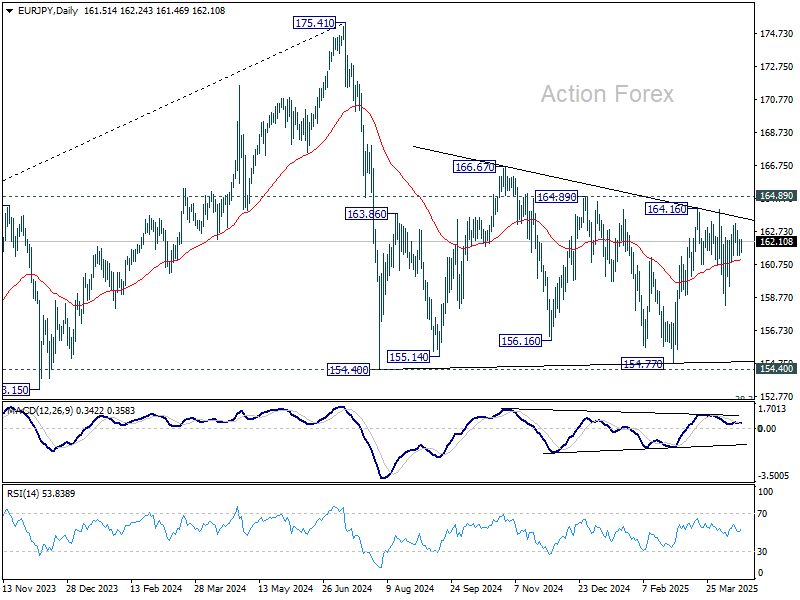

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.24; (P) 161.76; (R1) 162.18; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

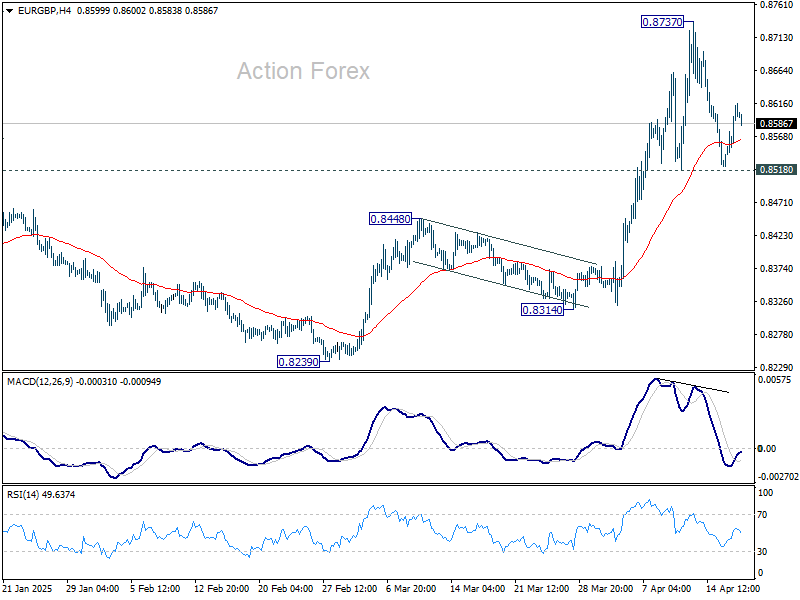

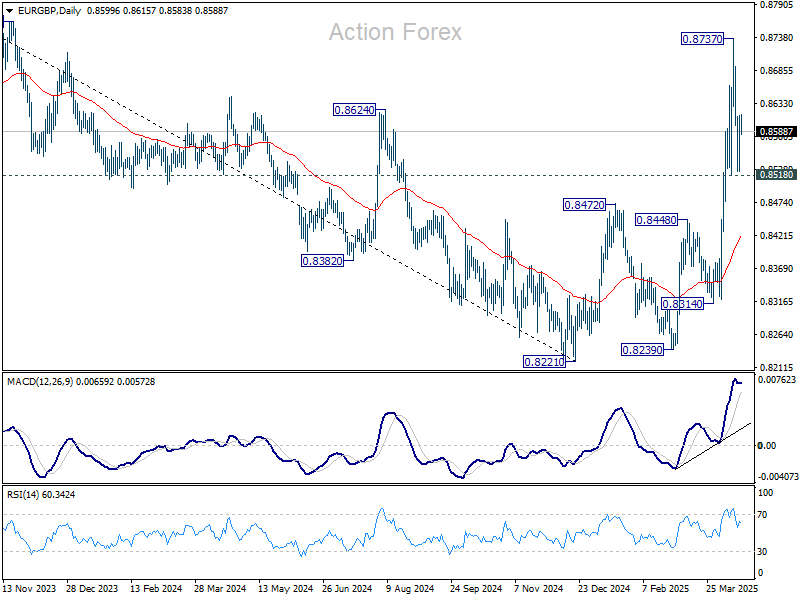

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8553; (P) 0.8584; (R1) 0.8640; More...

Intraday bias in EUR/GBP remains neutral for the moment. Consolidations from 0.8737 could extend but further rise is still expected as long as 0.8518 support holds. On the upside, break of 0.8737 will resume the larger rally from 0.8221.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will now remain the favored case as long as 0.8472 resistance turned support holds.

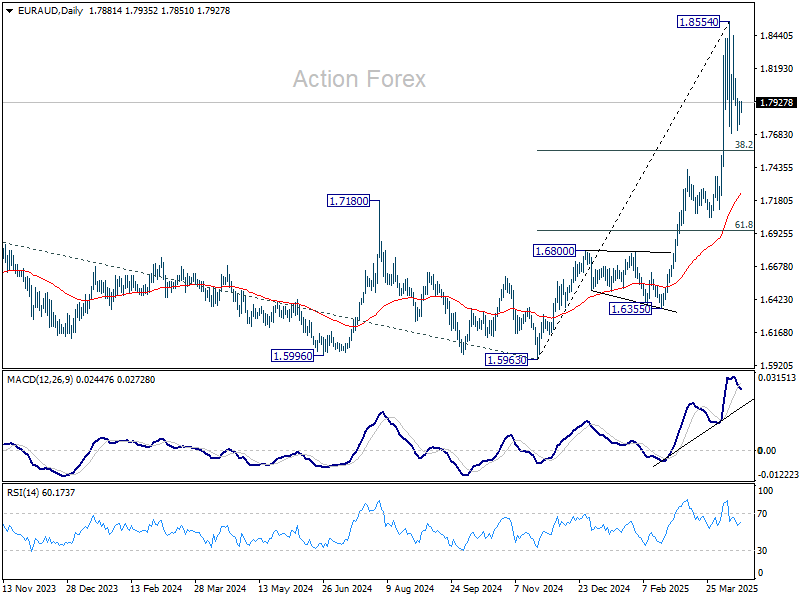

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7772; (P) 1.7858; (R1) 1.7976; More...

EUR/AUD is still extending the consolidation pattern from 1.8554 short term top and intraday bias remains neutral. Downside of the pull back should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, firm break of 1.8554 will resume larger up trend.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.

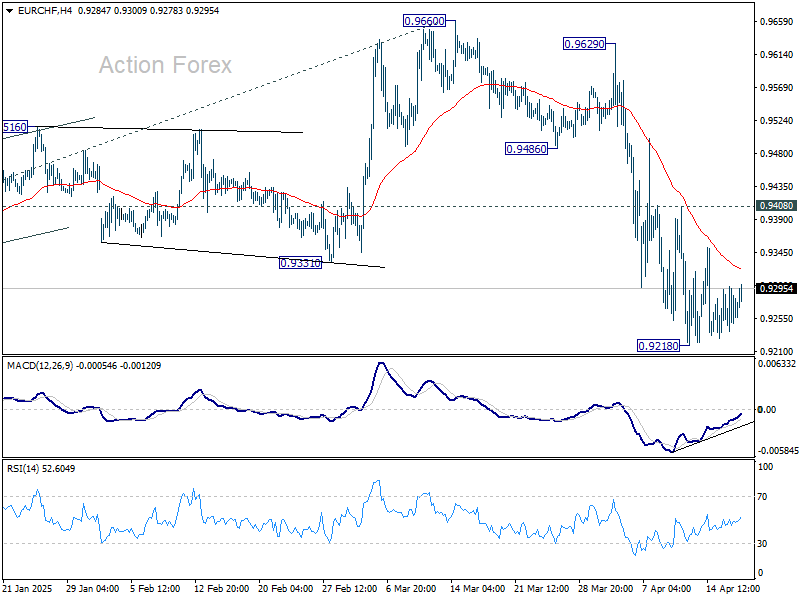

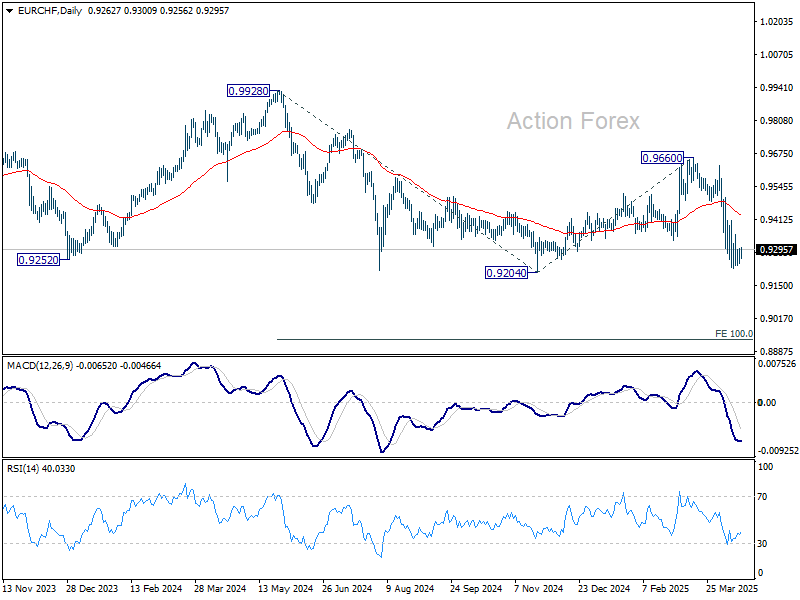

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9210; (P) 0.9255; (R1) 0.9317; More....

No change in EUR/CHF's outlook as consolidations continue above 0.9218. Intraday bias remains neutral for the moment. Outlook will remain bearish as long as 0.9408 resistance holds. On the downside, firm break of 0.9204 low will confirm larger down trend resumption.

In the bigger picture, rejection by long-term falling channel resistance (now at 0.9600) retains medium term bearishness. That is, down trend from 1.2004 (2018 high) is still in progress. Firm break of 0.9204 (2024 low) will confirm resumption. Next target is 100% projection of 0.9928 to 0.9204 from 0.9660 at 0.8936.

Focus Shifts to Frankfurt Where We Expect ECB to Cut

Markets

Fed Chair Powell sent a clear signal to markets in a keynote speech for the Economic Club of Chicago. He started by pointing out that the level of the tariff increases announced so far by the new Administration is significantly larger than anticipated. The same is likely to be true of the economic effects, which will include higher inflation and slower growth. The Fed’s obligation is to keep longer-term inflation expectations well anchored and to make certain that a one-time increase in the price level does not become an ongoing inflation problem. As the central bank acts to meet that obligation, they will balance their maximum employment and price-stability mandates, keeping in mind that, without price stability, it cannot achieve the long periods of strong labor market conditions that benefit all Americans. The Fed may find itself in the challenging scenario in which their dual-mandate goals are in tension. If that were to occur, Powell suggests that they consider how far the economy is from each goal, and the potentially different time horizons over which those respective gaps would be anticipated to close. During the Q&A he stressed on multiple occasions that the Fed’s goals aren’t in tension right now with the labour market still being strong. That’s a very strong hint that the Fed is well positioned to wait for greater clarity before considering any adjustments to its policy stance. Over the course of the year, Powell thinks that both metrics (unemployment & inflation) will on balance move away from target. Taking in mind that they’ll see how far away each is from target, this also suggests in first instance a clear focus on inflation. We feel strengthened in our base case scenario of a long pause, stretching at least into September and probably even into December. US money and interest rate markets turned a blind eye to Powell’s message yesterday. The Fed fund futures forward curve still suggests a 75% probability of a 25 bps rate cut in June with a cumulative 100 bps of rate cuts discounted by March of next year. Daily changes on the US yield curve yesterday ranged between -8.6 bps (3-yr) and -3.9 bps (30-yr). Powell’s message did leave traces on stock markets, pushing key indices to losses of 1.75% (Dow) to 3% (Nasdaq). They already started on the backfoot after US President Trump threw in Nvidia as a bargaining chip with China in the trade war. EUR/USD closed at 1.1399 from a start at 1.1283.

Focus shifts to Frankfurt today where we expect the ECB to cut its policy rate by another 25 bps to 2.25% and dropping any reference to a restrictive policy rate. Those settings allow for the central bank to, like the Fed, turn into wait-and-see mode as the tariff story develops. The 90-day pause in the worst case reciprocal tariff narrative stretches beyond the central bank’s June meeting, arguing against extending the rate cycle. As in the US, inflation is above target with both tariffs and fiscal stimulus being deployed posing upside risks which in the short-run outweigh downside growth risks. We are aware that this view goes against current market thinking of multiple additional ECB rate cuts, bringing the deposit rate towards 1.5%-1.75% by year-end but stick with our call. This dovish positioning nevertheless calls for asymmetric risks today. The front end of European yield curves might underperform, further supporting the single currency.

News & Views

The Bank of Canada left its policy rate unchanged at 2.75% yesterday. It’s the first pause since it embarked on an easing cycle in June 2024. The central bank offered no guidance for future policy, only that it will proceed carefully. The BoC considers two scenarios. In the first one, uncertainty is high but tariffs are limited in scope. Canadian growth weakens temporarily and inflation (2.3% in March) remains around the 2% target. In the second scenario, a protracted trade war causes a recession this year and inflation rises temporarily above 3% in mid-2026 before returning to target. Some 40% of a rate cut was priced in going into the meeting yesterday, triggering minor CAD appreciation after the status quo decision. Money markets expect less than two additional rate cuts for this year.

Australian labour market numbers for March were strong but slightly underwhelming. Employment grew by 32.2k (vs 40k expected) after February’s 57.5k drop, almost equally split in full time and part time jobs. The 2.2% annual employment growth was slightly above the 20-year pre-pandemic average of 2. The unemployment rate barely budged with rounding effects pushing the figure up from 4% to 4.1%. The same effects lifted the participation rate 1bp to 66.8%. First quarter inflation in New Zealand rose by 0.9% q/q to 2.5% y/y, up from 2.2%. Both were slightly above consensus but remain within the 1-3% central bank target range for a third consecutive quarter. Rent was the largest contributor. The 3.7% increase was the first sub 4% reading since 2021. Non tradeable CPI, a gauge for domestic price pressures, accelerated from 0.7% to 1.1% q/q, as did tradeable CPI from 0.3% to 0.8%. Despite the inflation quickening, markets expect the central bank to further cut rates at the May meeting (to 3.25%).