Sample Category Title

(BOC) Bank of Canada holds policy rate at 2¾%

The Bank of Canada today maintained its target for the overnight rate at 2.75%, with the Bank Rate at 3% and the deposit rate at 2.70%.

The major shift in direction of US trade policy and the unpredictability of tariffs have increased uncertainty, diminished prospects for economic growth, and raised inflation expectations. Pervasive uncertainty makes it unusually challenging to project GDP growth and inflation in Canada and globally. Instead, the April Monetary Policy Report (MPR) presents two scenarios that explore different paths for US trade policy. In the first scenario, uncertainty is high but tariffs are limited in scope. Canadian growth weakens temporarily and inflation remains around the 2% target. In the second scenario, a protracted trade war causes Canada’s economy to fall into recession this year and inflation rises temporarily above 3% next year. Many other trade policy scenarios are possible. There is also an unusual degree of uncertainty about the economic outcomes within any scenario, since the magnitude and speed of the shift in US trade policy are unprecedented.

Global economic growth was solid in late 2024 and inflation has been easing towards central bank targets. However, tariffs and uncertainty have weakened the outlook. In the United States, the economy is showing signs of slowing amid rising policy uncertainty and rapidly deteriorating sentiment, while inflation expectations have risen. In the euro area, growth has been modest in early 2025, with continued weakness in the manufacturing sector. China’s economy was strong at the end of 2024 but more recent data shows it slowing modestly.

Financial markets have been roiled by serial tariff announcements, postponements and continued threats of escalation. This extreme market volatility is adding to uncertainty. Oil prices have declined substantially since January, mainly reflecting weaker prospects for global growth. Canada’s exchange rate has recently appreciated as a result of broad US dollar weakness.

In Canada, the economy is slowing as tariff announcements and uncertainty pull down consumer and business confidence. Consumption, residential investment and business spending all look to have weakened in the first quarter. Trade tensions are also disrupting recovery in the labour market. Employment declined in March and businesses are reporting plans to slow their hiring. Wage growth continues to show signs of moderation.

Inflation was 2.3% in March, lower than in February but still higher than 1.8% at the time of the January MPR. The higher inflation in the last couple of months reflects some rebound in goods price inflation and the end of the temporary suspension of the GST/HST. Starting in April, CPI inflation will be pulled down for one year by the removal of the consumer carbon tax. Lower global oil prices will also dampen inflation in the near term. However, we expect tariffs and supply chain disruptions to push up some prices. How much upward pressure this puts on inflation will depend on the evolution of tariffs and how quickly businesses pass on higher costs to consumers. Short-term inflation expectations have moved up, as businesses and consumers anticipate higher costs from trade conflict and supply disruptions. Longer term inflation expectations are little changed.

Governing Council will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs. Our focus will be on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval. This means we will support economic growth while ensuring that inflation remains well controlled.

Governing Council will proceed carefully, with particular attention to the risks and uncertainties facing the Canadian economy. These include: the extent to which higher tariffs reduce demand for Canadian exports; how much this spills over into business investment, employment and household spending; how much and how quickly cost increases are passed on to consumer prices; and how inflation expectations evolve.

Monetary policy cannot resolve trade uncertainty or offset the impacts of a trade war. What it can and must do is maintain price stability for Canadians.

Information note

The next scheduled date for announcing the overnight rate target is June 4, 2025. The Bank will publish its next MPR on July 30, 2025.

US Opening Bell: Tech Stocks Falter but Dow Jones Turns Green as US Session Begins, BoC Meeting Ahead

Tech stocks fell globally after the Trump administration imposed new restrictions on Nvidia’s chip exports to China, worsening trade tensions.

Nasdaq 100 futures dropped 1.5%, and Nvidia shares fell about 6% in premarket trading. ASML shares plunged over 7% after reporting fewer-than-expected orders, blaming weakness in the chip industry. European markets also felt the pressure, with the Stoxx 600 index down 0.8%.

In the European session market moves appeared more measured compared to recent swings, as hopes grew for possible talks on Trump’s reciprocal tariffs.

Gold prices are back above the $3300 handle following a brief pullback. Risks are elevated following a report that the US administration plans to make countries choose between the US and China and offer favorable tariffs as an incentive.

This came about after a brief improvement in sentiment as news filtered through that Chinese authorities are asking the Trump administration to take certain actions before agreeing to talks, including showing more respect and curbing offensive comments from cabinet members, according to a source close to the Chinese government.

China's Foreign Ministry issued a statement earlier in the day saying that If the US wants to solve issues through dialogue, it should stop exerting maximum pressure

For now, tariff developments continue to sway markets back and forth as news filters through. This will continue in the US session with President Trump confirming Japan is to negotiate today with the US regarding tariffs & the cost of military support. President Trump said he will attend the meeting himself along with treasury & commerce secretaries and hopefully something can be worked out.

Economic data ahead

The US session will bring US retail sales data into focus but the bigger news is likely to be a speech by Fed Chair Jerome Powell. The Federal Reserve has the unenviable task of planning their monetary policy and decisions in the current climate which is rife with uncertainties.

Depending on the nature of Powell's testimony, markets could react as well but any news about monetary policy is unlikely to have a lasting impact.

The Bank of Canada (BoC) interest rate decision is due later in the day with forecast split on whether the Central Bank will cut rates. Currently markets are pricing in 55% probability of a rate cut.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

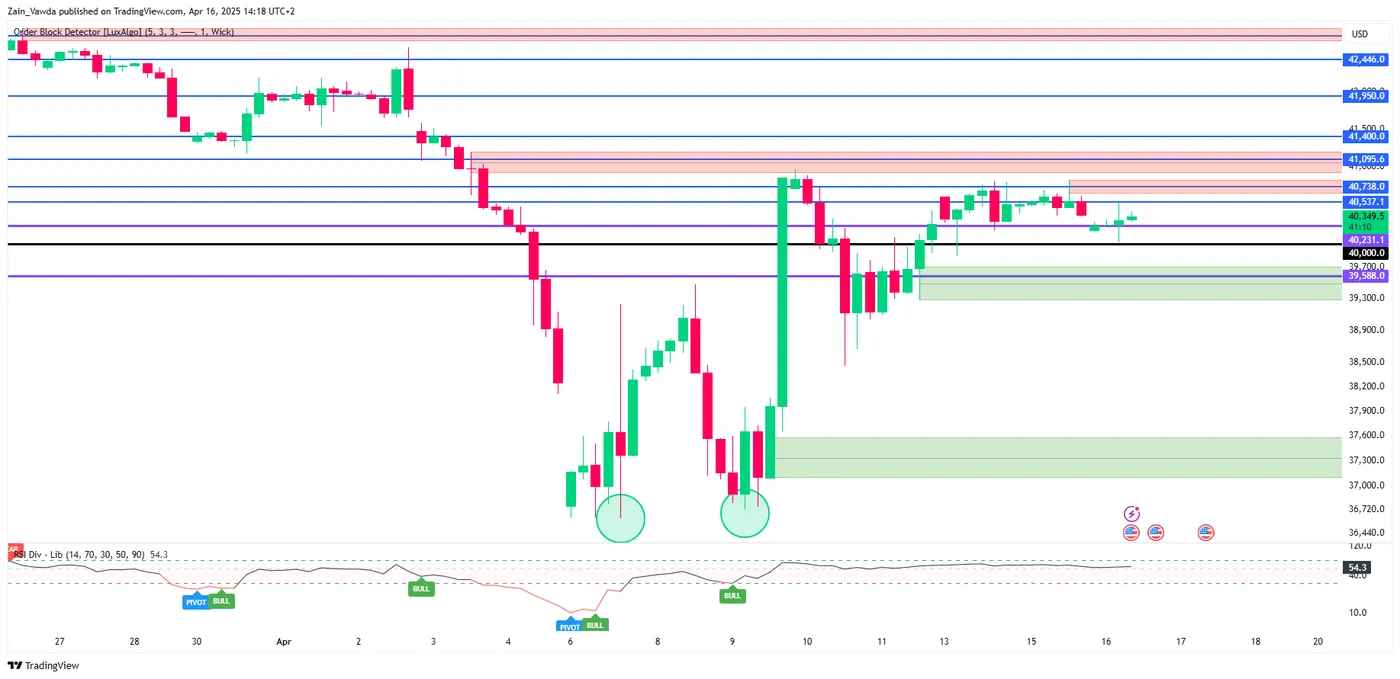

Chart of the day - Dow Jones

The Dow Jones continues to hold the high ground despite the trade tensions in play.

The index has held above the 40000 psychological level since reclaiming it on April 9. A retest in the European session occurred once more before the index pushed higher but downside pressure does remain a concern.

Immediate resistance rests at 40537 before the 40738 and 41095 handles come into focus.

Support at 40000 has held firm but a break of this key level could open up a run toward 39588, 38500 and potentially recent lows around the 36720 mark.

Dow Jones Index (DXY) Chart, April 16, 2025

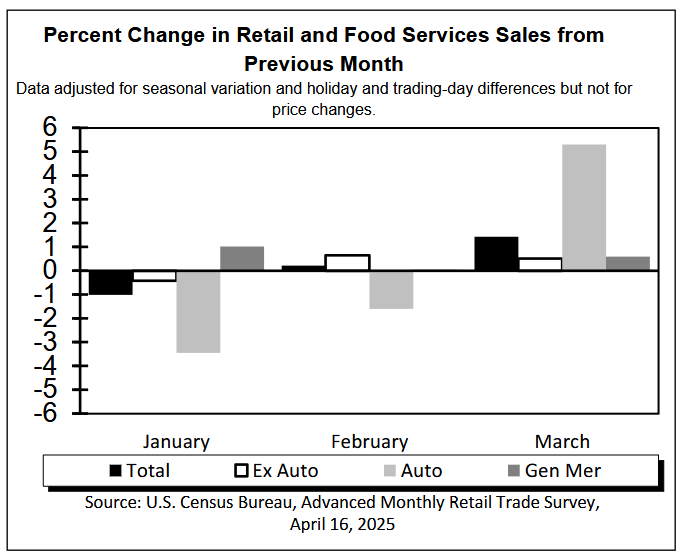

US: Retail Sales Surged in March as Consumers Stocked Up Ahead of Tariffs

Retail and food services sales jumped 1.4% month-on-month (m/m), in line with market expectations.

Sales of vehicles and parts played a big role in driving last month's gain, surging by 5.3% m/m as consumers rushed to purchase new cars ahead of the auto tariffs. Building materials and equipment stores' also posted a large increase, rising by 3.3% m/m – the largest monthly gain since March 2021. Meanwhile, sales at gasoline stations declined by 2.5% m/m, weighed down by lower gas prices.

Sales in the "control group", which excludes volatile components above (i.e., gasoline, autos and building supplies) also rose in-line with expectations, increasing by 0.4% on the month.

Sales increased across most of the remaining categories. The largest gains were in sporting goods & hobby stores (+2.4% m/m), electronics & appliance stores (+0.8% m/m), and health & personal care stores (+0.7% m/m). Furniture and home furnishings stores were the only category to post a decline. Online sales were little changed (+0.1%), but that came after a surge of 3.5% m/m in February.

Spending at bars and restaurants also rebounded last month (+1.8%), following an uneven performance in the last three months.

Key Implications

There were no major surprises in today’s report. The sharp increase in retail sales was widely anticipated, given the surge in vehicle purchases that had already been signaled earlier this month. However, cars were not the only thing selling like hot cakes in March, with consumers were stocking up on a range of goods ahead of the reciprocal tariff announcement set for April 2nd. Even sales at bars and restaurants saw an improvement last month following unsteady performance in the prior three months, with eating out perhaps complementing the shopping experience. While some of this behavior may carry over into April, it’s likely to mark a final burst of spending before consumers begin tightening their purse strings.

Consumer sentiment indicators suggest growing concern. Confidence has dropped sharply, with households increasingly worried about inflation and job security. Household wealth has also taken a hit, as the financial market selloff has eroded savings and reduced the safety cushion. Prices are expected to rise further, with inflation likely to accelerate as early as Q2. At the same time, economic growth is expected to stall through the first half of the year, accompanied by a rising unemployment rate. Today's retail reading suggests consumer spending is likely to expand by just 1% (annualized) in Q1 – a sharp slowdown from Q4-2024's 4.0% – with a further softening in Q2 spending looking increasingly likely.

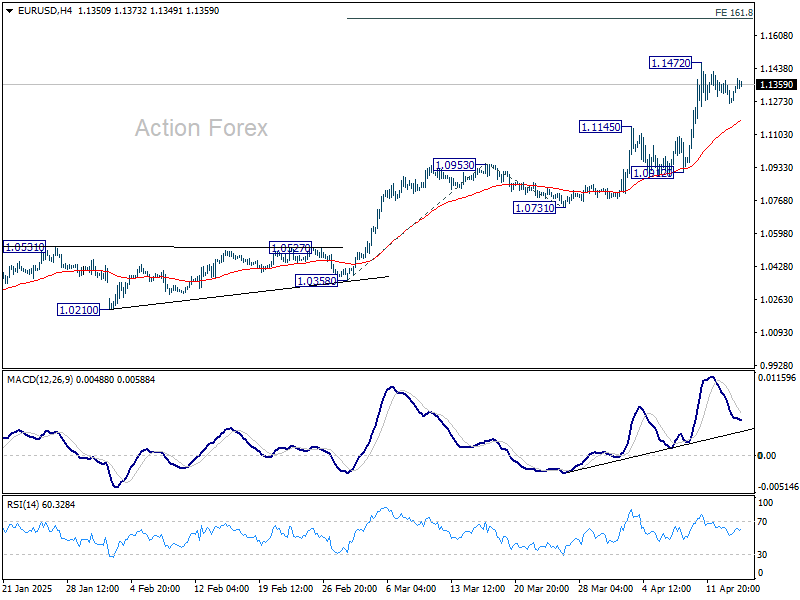

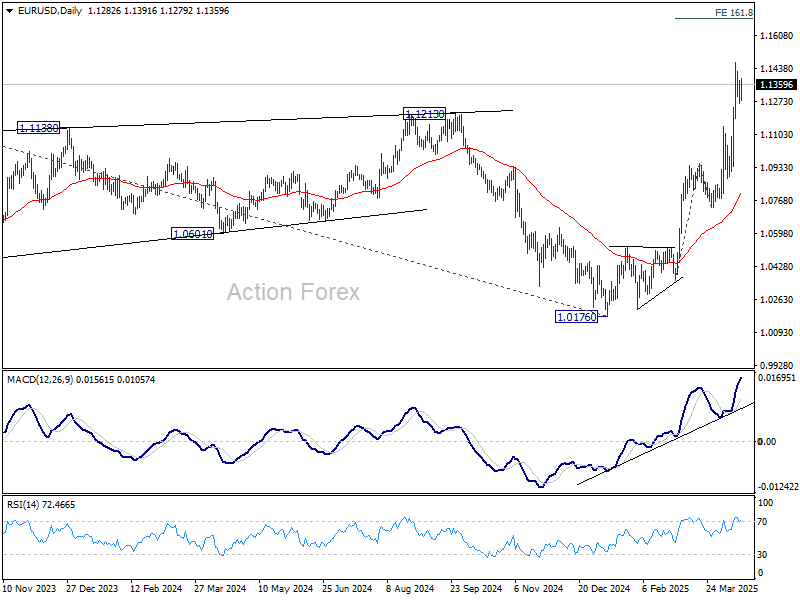

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1238; (P) 1.1308; (R1) 1.1353; More...

EUR/USD is extending consolidations below 1.1472 and intraday bias remains neutral. Deeper pullback cannot be ruled out. But downside should be contained by 1.1145 resistance turned support to bring another rally. On the upside, break of 1.1472 will target 161.8% projection of 1.0358 to 1.0953 from 1.0731 at 1.1694.

In the bigger picture, rise from 0.9534 long term bottom could be correcting the multi-decade downtrend or the start of a long term up trend. In either case, further rise should be seen to 100% projection of 0.9534 to 1.1274 from 1.0176 at 1.1916. This will now remain the favored case as long as 55 W EMA (now at 1.0745) holds.

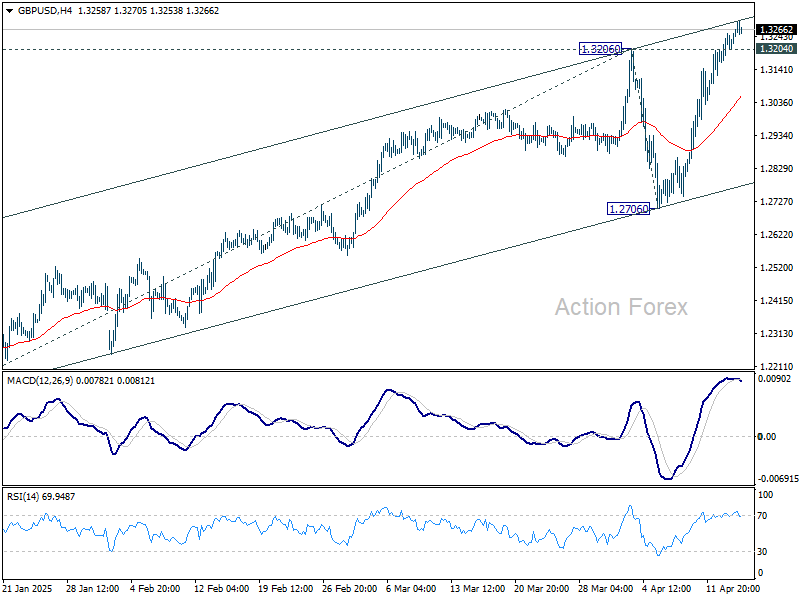

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3180; (P) 1.3216; (R1) 1.3268; More...

Intraday bias in GBP/USD stays on the upside at this point. Current rise from 1.2099 should target 61.8% projection of 1.2099 to 1.3206 from 1.2706 at 1.3390, and possibly further to 1.3433 high. On the downside, below 1.3204 minor support will turn intraday bias neutral first. But overall near term outlook will stay bullish as long as 1.2706 support holds.

In the bigger picture, price actions from 1.3433 are seen as a corrective pattern to the up trend from 1.3051 (2022 low). Rise from 1.2099 could be the second leg. Overall, GBP/USD should target 1.4248 key resistance (2021 high) on break of 1.3433 at a later stage.

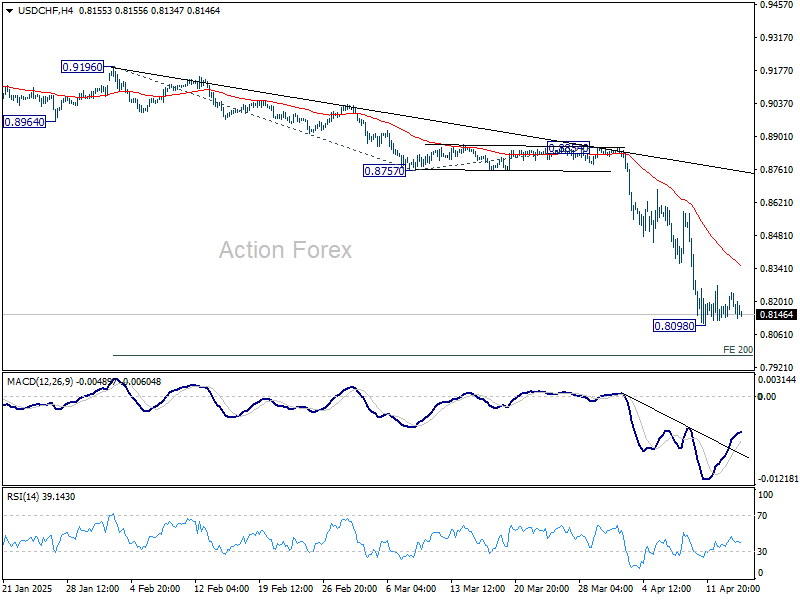

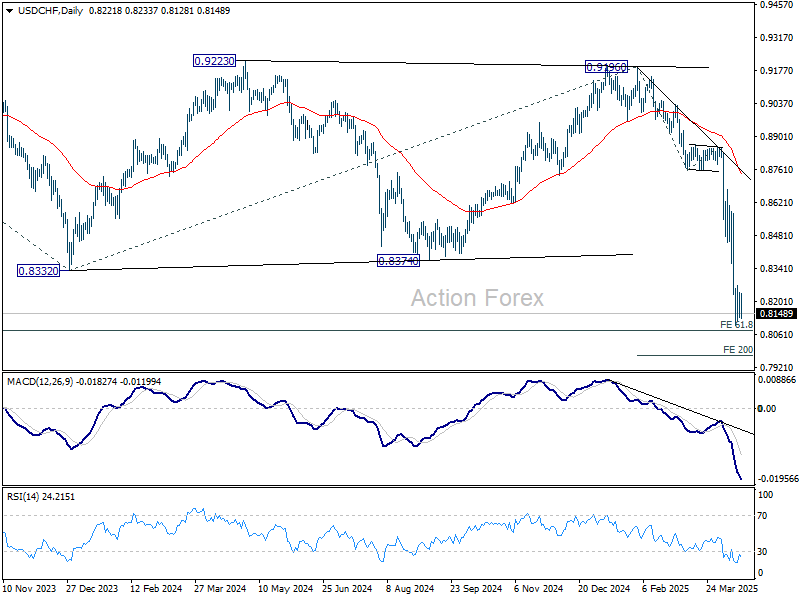

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8163; (P) 0.8201; (R1) 0.8273; More…

No change in USD/CHF's outlook as consolidations continue above 0.8098. Intraday bias stays neutral for the moment. While stronger recovery might be seen, upside should be limited by 55 4H EMA (now at 0.8357) to bring another fall. On the downside, break of 0.8098 will resume recent down trend to 200% projection of 0.9196 to 0.8757 from 0.8854 at 0.7976 next.

In the bigger picture, the break of 0.8332 (2023 low) confirms resumption of long term down trend from 1.0342 (2017 high). Next target is 61.8% projection of 1.0146 (2022 high) to 0.8332 from 0.9196 at 0.8075. Firm break there will target 100% projection at 0.7382.

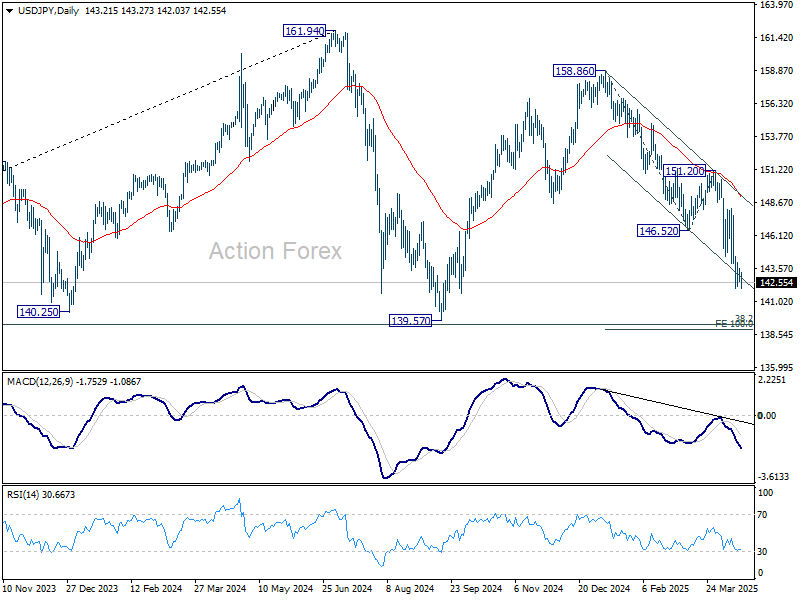

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.71; (P) 143.15; (R1) 143.70; More...

USD/JPY is still bounded in consolidations from 142.05 temporary low and intraday bias remains neutral. Another recovery cannot be ruled out, but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Risk Appetite Eases; Markets Await Clarity from US-Japan Negotiations

Global markets are trading with a mildly risk-off tone today, with losses spanning from Asia through to Europe, and US futures following suit. Technology stocks are under pressure, led by AI-chip giant Nvidia, which warned of significant charges stemming from new US restrictions on semiconductor exports to China. The announcement marks the latest escalation in trade tensions between Washington and Beijing, particularly in high-tech sectors where geopolitical and economic interests are increasingly colliding.

Despite the drag from tech, the broader equity pullback remains relatively contained. Some support is being drawn from slightly stronger-than-expected US retail sales data, which helped ease fears of a sharp consumer slowdown. Still, sentiment remains cautious ahead of potential headlines from US-Japan negotiations later today. The discussion is expected to touch on key topics including tariffs, defense cost-sharing, energy policy, and exchange rate management. The results of these talks could offer a clearer view of US President Donald Trump's broader trade strategy and whether current tariff policies are a prelude to further escalation.

Meanwhile, pressure is mounting on BoJ, with reports suggesting it is preparing to downgrade its economic growth outlook at the April 30–May 1 policy meeting. BoJ’s current forecast of 1.1% GDP growth for fiscal 2025 is likely to be revised downward in response to the mounting impact of US tariffs. While inflation in Japan has been trending upward gradually, central bank officials are now questioning whether the external drag from trade tensions could offset domestic momentum.

In the currency markets, the Swiss Franc is leading gains for the day, followed by Euro and Yen, as investors rotate back into safer assets. Dollar, by contrast, is the day’s weakest performer, followed by Kiwi and Pound. Loonie and Aussie are positioning in he middle.

Technically, Sterling has shown some resilience this week, but signs of fatigue are emerging near key resistance levels. EUR/GBP has found support at 0.8518, while GBP/USD is struggling to break above its near-term channel ceiling. Pullback in the Pound from current levels is plausible, though any downside is likely to remain limited unless EUR/GBP breaks back above 0.8737. Conversely, a decisive upside break against both Euro and Dollar could reignite a broader rally in Sterling.

In Europe, at the time of writing, FTSE is down -0.34%. DAX is down -0.54%. CAC is down -0.66%. UK 10-year yield is down -0.0037 at 4.622. Germany 10-year yield is down -0.034 at 2.502. Earlier in Asia, Nikkei fell -1.01%. Hong Kong HSI fell -1.91%. China Shanghai SSE rose 0.26%. Singapore Strait Times rose 1.04%. Japan 10-year JGB yield fell -0.078 to 1.298.

US retail sales rise 1.4% mom in March, above exp 1.3%

US retail sales rose 1.4% mom to USD 734.9B in March, slightly above expectation of 1.3% mom. Ex-auto sales rose 0.5% mom to USD 590.9B, above expectation of 0.4% mom. Ex-gasoline sales rose 1.7% mom to USD 683.4B. Ex-auto & gasoline sales rose 0.8% mom to USD 539.5B.

Total sales for the January through March period were up 4.1% from the same period a year ago.

Eurozone CPI finalized at 2.2% in March, core at 2.4%

Final data confirmed that Eurozone headline inflation edged lower to 2.2% yoy in March, down from 2.3% in February. Core inflation (ex energy, food, alcohol & tobacco) also softened to 2.4% from 2.6%.

Services was the main contributor to price pressures in Eurozone, adding 1.56 percentage points to the annual rate, followed by food, alcohol and tobacco at 0.57 points. Energy contributed negatively, subtracting -0.10 points from the overall figure.

At the EU level, inflation was finalized at 2.5% yoy, an improvement from February's 2.7% yoy. France registered the lowest annual rate at just 0.9%, while Denmark and Luxembourg followed at 1.5% and 1.5% respectively. In contrast, inflation remains more persistent in Eastern Europe, with Romania (5.1%), Hungary (4.8%), and Poland (4.4%)recording the highest annual rates.

UK CPI falls to 2.6%, both goods and services inflation ease

UK consumer inflation continued to ease in March, with headline CPI slowing to 2.6% yoy, slightly below the expected 2.7% and down from 2.8% yoy in February. On a monthly basis, prices rose 0.3%, also under consensus 0.4% mom forecast.

The decline was broad-based, with annual goods inflation falling to 0.6% yoy from 0.8% yoy and services inflation easing to 4.7% yoy from 5.0% yoy.

Core CPI (excluding energy, food, alcohol and tobacco) edged down to 3.4% as expected, from 3.5% previously.

BoJ’s Ueda: US tariffs nearing bad scenario, policy response may be needed

BoJ Governor Kazuo Ueda warned that US President Donald Trump’s escalating tariff policies have "moved closer towards the bad scenario” anticipated by the central bank.

“We will scrutinise without pre-conception the extent to which US tariffs could hurt the economy,” he said in an interview with Sankei newspaper.

"A policy response may become necessary. We will make an appropriate decision in accordance with changes in developments," he added.

Nevertheless, Ueda reiterated that BoJ will continue to raise interest rates “at an appropriate pace” as long as economic and price conditions align with its projections.

On inflation, Ueda said domestic food price pressures are expected to ease. He sees real wages turning positive and continuing to rise into the second half of the year, supporting consumption and price stability.

Still, he warned of dual risks: persistent inflation driven by global supply shocks, or a consumption drag caused by the rising cost of living.

Australia Westpac leading index falls as tariff shock starting to weigh

Australia’s Westpac Leading Index slipped from 0.9% to 0.6% in March. Westpac noted that the index has only just begun to reflect the escalating disruptions caused by US President Donald Trump's reciprocal tariff announcement on April 2.

While the immediate impact on Australia is seen as limited and manageable for now, "some further softening in the growth pulse looks likely in the months ahead".

Westpac has revised down its growth forecast for Australia in 2025 to 1.9% from 2.2%, citing the accumulating downside risks.

Looking ahead to RBA's May 19–20 meeting, Westpac expects the deteriorating global backdrop and clearer signs of inflation cooling will prompt a 25bps rate cut.

Moreover, the tone of the meeting is likely to pivot more decisively "away from lingering questions about inflation to downside risks to growth." Such a shift would lay the groundwork for additional policy easing in the second half of the year.

China Q1 GDP tops forecasts with 5.4% growth

China’s economy started the year on a stronger footing, with GDP expanding by 5.4% yoy in Q1, surpassing market expectations of 5.1%. On a quarterly basis, growth slowed to 1.2% from 1.6% in Q4.

March’s activity indicators were broadly upbeat. Industrial production surged by 7.7% yoy, well above the 5.6% yoy forecast. Retail sales climbed 5.9%, also ahead of expectations of 5.1% yoy.

Fixed asset investment increased 4.2% year-to-date, modestly exceeding projections. However, persistent weakness in the property sector continues to weigh on the recovery narrative. Property investment fell -9.9% in Q1, slightly worse than the -9.8% decline recorded over the first two months of the year. Private sector investment—a key gauge of business confidence—rose only 0.4%.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 142.71; (P) 143.15; (R1) 143.70; More...

USD/JPY is still bounded in consolidations from 142.05 temporary low and intraday bias remains neutral. Another recovery cannot be ruled out, but outlook will stay bearish as long as 151.20 resistance holds. Below 142.05 will resume the fall from 158.86 to 139.57 support.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low), with fall from 158.86 as the third leg. Strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

US retail sales rise 1.4% mom in March, above exp 1.3%

US retail sales rose 1.4% mom to USD 734.9B in March, slightly above expectation of 1.3% mom. Ex-auto sales rose 0.5% mom to USD 590.9B, above expectation of 0.4% mom. Ex-gasoline sales rose 1.7% mom to USD 683.4B. Ex-auto & gasoline sales rose 0.8% mom to USD 539.5B.

Total sales for the January through March period were up 4.1% from the same period a year ago.

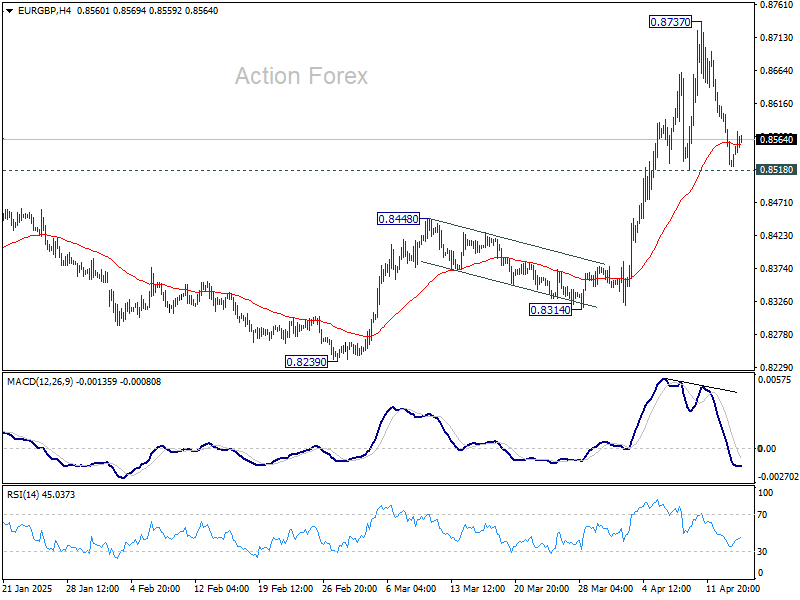

GBP/USD Rockets Higher While EUR/GBP Slips

GBP/USD is gaining pace above the 1.3220 resistance. EUR/GBP declined and is now consolidating losses above the 0.8500 region.

Important Takeaways for GBP/USD and EUR/GBP Analysis Today

- The British Pound is attempting a fresh increase above 1.3220.

- There is a key bullish trend line forming with support near 1.3245 on the hourly chart of GBP/USD at FXOpen.

- EUR/GBP is trading in a bearish zone below the 0.8630 pivot level.

- There is a connecting bearish trend line forming with resistance near 0.8570 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair remained well-bid above the 1.2850 level. The British Pound started a decent increase above the 1.3000 zone against the US Dollar.

The bulls were able to push the pair above the 50-hour simple moving average and 1.3150. The pair even climbed above 1.3200 and traded as high as 1.3263. It is now consolidating gains and trading well above the 23.6% Fib retracement level of the upward move from the 1.3030 swing low to the 1.3263 high.

On the upside, the GBP/USD chart indicates that the pair is facing resistance near 1.3260. The next major resistance is near 1.3320. A close above the 1.3320 resistance zone could open the doors for a move toward 1.3450.

Any more gains might send GBP/USD toward 1.3500. On the downside, there is a key support forming near a bullish trend line at 1.3245.

If there is a downside break below 1.3245, the pair could accelerate lower. The next major support is at 1.3145. It is close to the 50% Fib retracement level of the upward move from the 1.3030 swing low to the 1.3263 high.

The next key support is seen near 1.3030, below which the pair could test 1.2860. Any more losses could lead the pair toward the 1.2745 support.

EUR/GBP Technical Analysis

On the hourly chart of EUR/GBP at FXOpen, the pair started a steady decline from well above 0.8700. The Euro traded below the 0.8630 support level against the British Pound.

The EUR/GBP chart suggests that the pair even declined below the 0.8600 level and tested 0.8520. It is now consolidating losses and trading below the 50-hour simple moving average. Recently, there was a minor increase above the 0.8540 level.

The pair is now facing resistance near the 23.6% Fib retracement level of the downward move from the 0.8738 swing high to the 0.8518 low. There is also a connecting bearish trend line forming with resistance near 0.8570.

The next major resistance could be 0.8630 and the 50% Fib retracement level of the downward move from the 0.8738 swing high to the 0.8518 low.

A close above the 0.8630 level might accelerate gains. In the stated case, the bulls may perhaps aim for a test of 0.8685. Any more gains might send the pair toward the 0.8740 level.

Immediate support sits near 0.8520. The next major support is near 0.8500. A downside break below the 0.8500 support might call for more downsides. In the stated case, the pair could drop toward the 0.8360 support level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.