Sample Category Title

Japanese Yen Surges as Weak US Dollar Fuels Momentum

The USD/JPY pair extended its decline on Wednesday, dropping to 142.36 amid sustained dollar weakness.

Key factors driving USD/JPY Movements

The Japanese yen’s appreciation is being propelled by broad-based US dollar softness. The greenback faced selling pressure as concerns grew over the economic fallout from proposed new US tariffs.

In a fresh escalation of trade tensions, US President Donald Trump has called for an investigation into imposing tariffs on critical mineral imports – many of which originate from China. This move has heightened investor anxiety, further weighing on the dollar.

Meanwhile, market attention is turning to the upcoming US-Japan trade talks, where Tokyo is expected to push for the complete removal of US tariffs.

On the domestic front, Japan’s latest economic data revealed an eight-month high in manufacturing sector optimism for April. However, the outlook remains cautious due to lingering risks surrounding US trade policy.

Technical Analysis: USD/JPY

The USD/JPY pair continues to consolidate around 143.20. A downside breakout could signal a further decline towards 141.70, marking the third wave of the downtrend. Conversely, an upside breakout may trigger a technical correction towards 145.00. This scenario is supported by the MACD indicator, with its signal line below zero but pointing firmly upwards.

The pair has formed a broader consolidation range between 142.46 and 144.07, with a triangle pattern emerging. A breakout above this range could initiate a corrective rally towards 145.00. The Stochastic oscillator reinforces this view, as its signal line – currently below 20 – is trending sharply upwards towards 80.

Conclusion

The yen’s rapid appreciation reflects both dollar weakness and cautious optimism in Japan’s manufacturing sector. However, trade policy uncertainties and technical patterns suggest continued volatility, with key levels at 141.70 (downside) and 145.00 (upside) in focus.

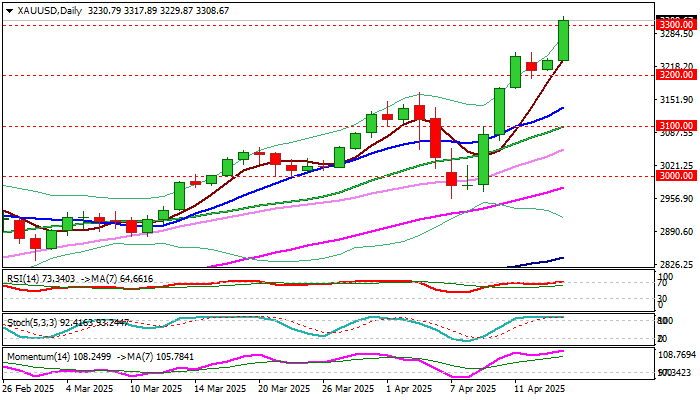

Gold Hits New Record High Above $3300

Gold broke above psychological $3300 barrier and hit new record high on Wednesday morning, as growing uncertainty over US-China trade war sparked fresh wave of migration into safety, with weaker dollar adding support to metal’s price.

Deteriorating fundamentals after China decided to stop any further deliveries from Boeing, warn of severe negative impact from escalation of conflict that keeps bullish outlook for the yellow metal.

The latest rally took just four days to rally from one to the other round-figure level, indicating that bulls hold grip despite the recent jumps from $3000 to $3100 and from $3100 to $3200 which took only two days each.

Subsequent dip below $3300 (correction low was $3288) is seen as positioning for fresh push higher, with daily close above $3300 level required to confirm break and shift focus on next targets at $3329, $3350 and $3378.

Caution on break below $3288 (reinforced by rising 10HMA) which would sideline bulls for deeper correction.

Res: 3317; 3329; 3350; 3378

Sup: 3300; 3288; 3277; 3264

UK Inflation Update March 2025: GBP/USD Market Analysis & BoE Rate Cut Predictions

- UK annual inflation dropped to 2.6% in March 2025, lower than expected, with notable decreases in recreation, culture, and transport prices.

- Markets are pricing in an 85% probability of a Bank of England rate cut at the May meeting.

- Analysts debate whether inflation has bottomed out, with concerns about rising energy and water bills potentially pushing inflation higher in the coming months.

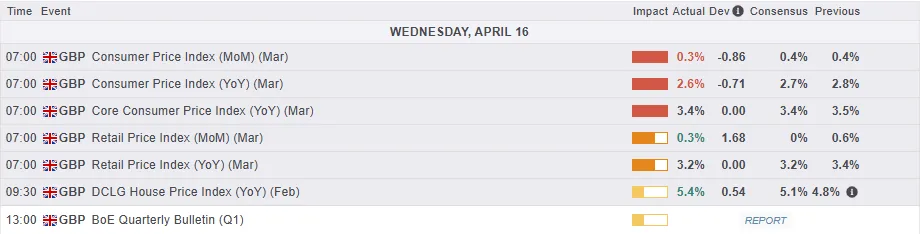

The Office for National Statistics (ONS) released UK inflation data for March this morning. The data revealed that the UK's annual inflation rate dropped to 2.6% in March 2025, down from 2.8% in February and below the expected 2.7%. The biggest price decreases came from recreation and culture, particularly games, toys, and hobbies (-4.2%) and data processing equipment (-5.1%). Transport also played a role, with motor fuel prices falling by 5.3%.

Price increases slowed for restaurants and hotels (3%, the lowest since July 2021), housing and utilities (1.8%), and food and non-alcoholic drinks (3%). On the other hand, clothing and footwear prices rose by 1.1%, reflecting typical increases as spring fashions hit stores.

Monthly inflation rose by 0.3%, slightly less than the previous month's rise and below predictions of 0.4%. Core inflation, which excludes volatile items, eased to 3.4% from 3.5%.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

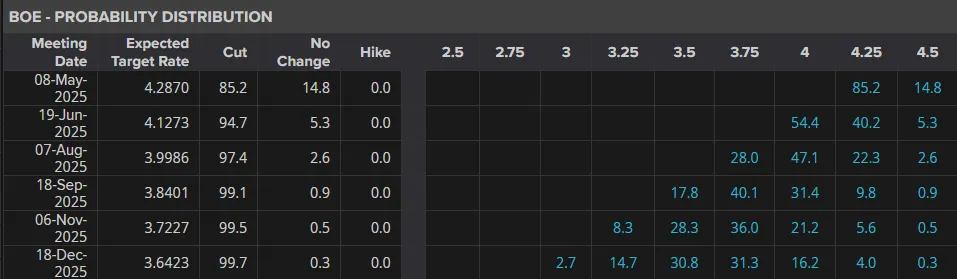

Inflation moving forward and implications for the Bank of England (BoE)

Following the inflation data, markets are pricing in around an 85% probability of a rate cut from the BoE at the Central Banks May meeting.

Source: LSEG

The bigger question for consumers at least is whether this is as good as it is going to get? There is a school of thought among analysts that inflation has likely bottomed and that markets and consumers need to prepare for higher inflation moving forward.

The reason is largely to do with energy prices as ING THINK put it well, stating energy bills have mostly helped lower inflation due to the big drop in natural gas prices after the 2022 spike. However, starting in April, energy bills will add 0.8 percentage points more to the annual CPI than they did in March. Water bills have also gone up significantly this month.

With this in mind ING forecasts put April’s CPI figure at 3.2%, rising to 3.5% or maybe even a tad higher towards the end of the third quarter.

Personally I do not see such a huge jump in April largely on the back of global uncertainty which I think is already impacting demand and spending habits. This could lead to consumers spending less and prioritizing savings due to an uncertain economic outlook and thus help keep Global inflation in check.

Of course this will also depend on how tariff negotiations shake out as this could in theory also lead to an increase in inflation thus negating my assessment of lower demand and steady inflation.

Services inflation also still remains uncomfortably high, but is on target to reach the BoEs forecast figure.

All in all, an interesting period ahead for the UK economy, something the rest of the world is likely to grapple with as well for the majority of 2025.

Technical Analysis - GBP/USD

Looking at GBP/USD from a technical standpoint, the rally to the upside has broken above the resistance level at 1.3261. However, GBP/USD needs to record a daily close above the 1.3261 for further gains to materialize.

The 14-period RSI is also approaching overbought territory which could hinder further upside.

As discussed in yesterday's article GBP/USD Analysis: labor data, inflation watch & key trading levels.

A modest recovery by the US Dollar is what kept GBP/USD from advancing yesterday and early session weakness today is allowing cable to move higher.

I stand by my analysis yesterday, this move is largely being driven by the weaker US dollar rather than GBP strength.

GBP/USD Daily Chart, April 16, 2025

Source: TradingView.com

Support

- 1.3261

- 1.3100

- 1.3000

Resistance

- 1.3322

- 1.3415

- 1.3500

Inflation in the UK Has Fallen

According to Forex Factory, the Consumer Price Index (CPI) reading came in below expectations: while analysts had forecast a decline to 2.7% year-on-year from the previous 2.8%, the actual CPI figure was 2.6%.

Following the release of this news, the GBP/USD exchange rate rose to 1.3280 – the highest level in seven months.

On the one hand, falling inflation is a sign of a healthy economy and a relief for the Bank of England, especially considering that CPI stood in double digits just two years ago. As a result, analysts may now predict that interest rates could be cut at the meeting scheduled for 8 May.

On the other hand, demand for the dollar remains volatile due to Trump’s tariff policies, fears of a US recession, and a wave of bond sell-offs.

Technical Analysis of the GBP/USD Chart

In just one week, the pound-to-dollar rate has risen by approximately 4.2%, with the RSI indicator now hovering near extreme overbought levels. Furthermore, the price is approaching the upper boundary of the ascending channel, which has been in play since the beginning of 2025.

In such conditions, a correction (with a bearish breakout of the ascending trendline, shown in blue) appears a logical development. However, a key factor in sustaining the current trend of dollar weakness could be the speech by Federal Reserve Chair Jerome Powell, scheduled for today at 20:30 GMT+3.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

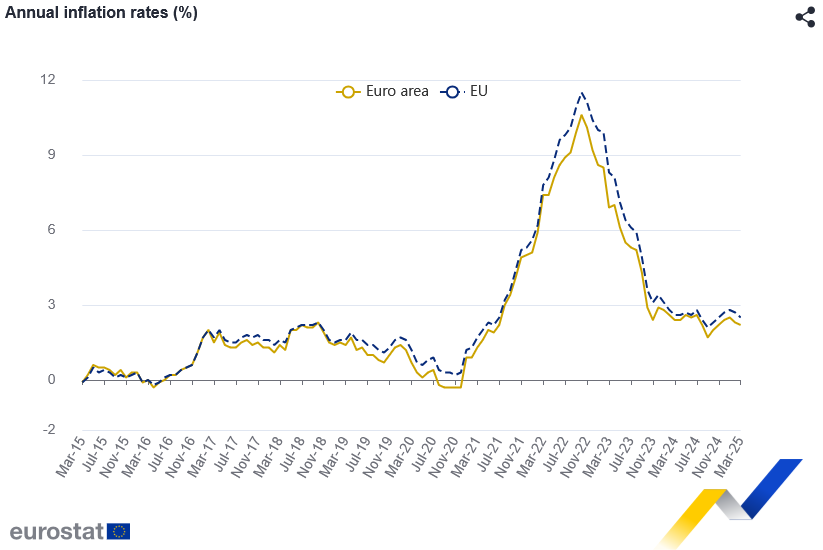

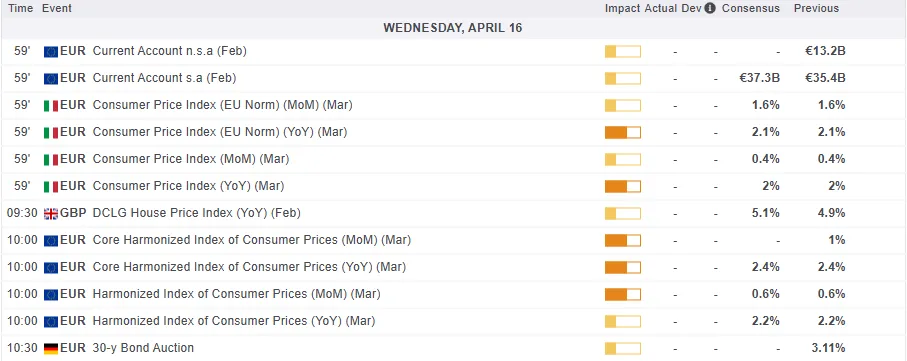

Eurozone CPI finalized at 2.2% in March, core at 2.4%

Final data confirmed that Eurozone headline inflation edged lower to 2.2% yoy in March, down from 2.3% in February. Core inflation (ex energy, food, alcohol & tobacco) also softened to 2.4% from 2.6%.

Services was the main contributor to price pressures in Eurozone, adding 1.56 percentage points to the annual rate, followed by food, alcohol and tobacco at 0.57 points. Energy contributed negatively, subtracting -0.10 points from the overall figure.

At the EU level, inflation was finalized at 2.5% yoy, an improvement from February's 2.7% yoy. France registered the lowest annual rate at just 0.9%, while Denmark and Luxembourg followed at 1.5% and 1.5% respectively. In contrast, inflation remains more persistent in Eastern Europe, with Romania (5.1%), Hungary (4.8%), and Poland (4.4%)recording the highest annual rates.

Europe’s Opening Bell: China Q1 GDP Beat, Gold Nears $3300/oz as Global Stock Surge Grinds to a Halt

The two-day global stock surge came to a halt this morning following further escalations in the US-China trade war. The Trump administration slapped fresh curbs on Nvidia chip exports to China which saw NVIDIA shares tumble post market.

The doom and gloom from the NVIDIA announcement has weighed on global stocks and indexes. Chinese technology companies drove Asian equities lower, while equity index futures in Europe and the US both struggled.

Japan’s 30-year bonds recovered as U.S. Treasury market volatility eased, and BoJ’s Ueda suggested a possible reaction to higher U.S. tariffs. However, a weak economy could threaten the BoJ's plans to slowly raise interest rates.

The only positive outcome during the Asian session appears to be around China. China's economy grew faster than expected in the first quarter, driven by strong consumer spending and industrial production.

Gold prices stole the show once again as the precious metal is trading within a whisker of $3300/oz, having risen around 1.82% to trade $3290/oz at the time of writing.

The DXY resumed its struggle following a brief reprieve yesterday which saw the greenback gain around 0.50%. The Euro and Swiss Franc appear to be the biggest gainers from the NVIDIA ban, both gaining in Asian trade.

Looking at the European session, the chances that European tech shares follow their Asian and US counterparts are high. We are already seeing weakness in index futures with the DAX trading 0.85% down at the time of writing.

Economic data releases

From a data perspective, we have Eurozone and Italian CPI (final) numbers being released this morning. Neither of these releases should have a major impact on market moves this morning with the overall tariff narrative still front and centre.

For all market-moving economic releases and events, see the MarketPulse Economic Calendar. (click to enlarge)

Chart of the day - DAX

From a technical standpoint, the DAX is at a key level and a critical junction for the index.

Bulls and bears are battling out for supremacy as the index hovers at the 100-day MA eyeing either a break or bounce.

Yesterday saw the DAX end the day in the green but failing to record a close above the 100-day MA.

The overnight announcement around NVIDIA and China weighed on the DAX as well with the Index opening lower today.

Currently the Index is down around 0.85% and faces significant hurdles if it is to reclaim the 22000 handle.

Keep an eye on the period-14 RSI with a break above the 50 level a potential sign that bullish momentum is in play.

A rejection of the RSI 50 level and the 100-day MA could bring support at 21000 and 20550 back into focus.

DAX 40 Index Chart, April 16, 2025

Source: TradingView.com (click to enlarge)

Support

- 21000

- 20550

- 20000

Resistance

- 21365

- 21803

- 22405

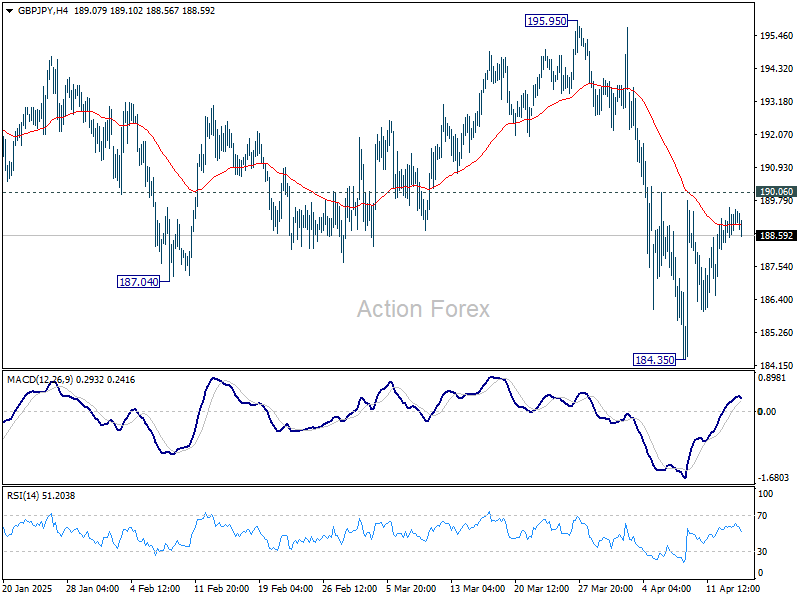

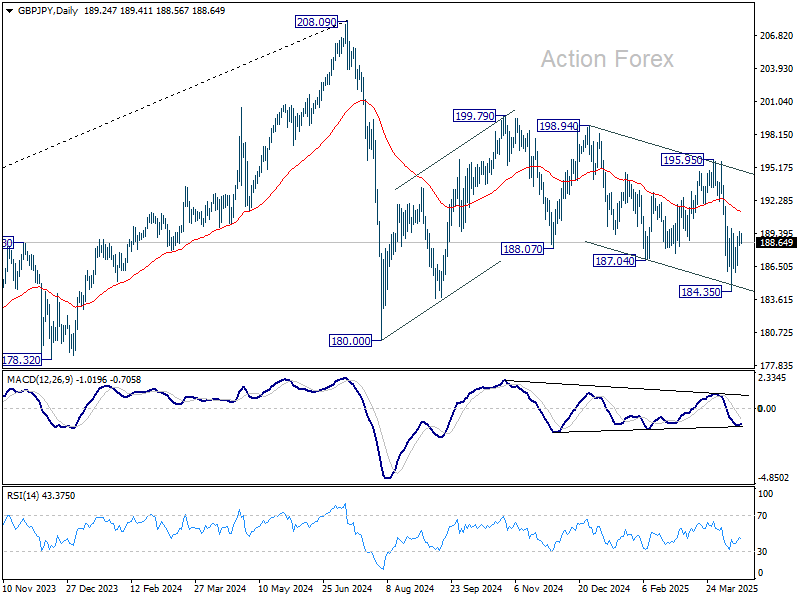

GBP/JPY Daily Outlook

Daily Pivots: (S1) 188.76; (P) 189.18; (R1) 189.96; More...

GBP/JPY is staying in consolidation above 184.35 and intraday bias stays neutral. Risk will remain on the downside as long as 190.06 resistance holds. Below 184.35 will target 180.00 low. Nevertheless, break of 190.06 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 175.94 will bring deeper fall even still as a correction.

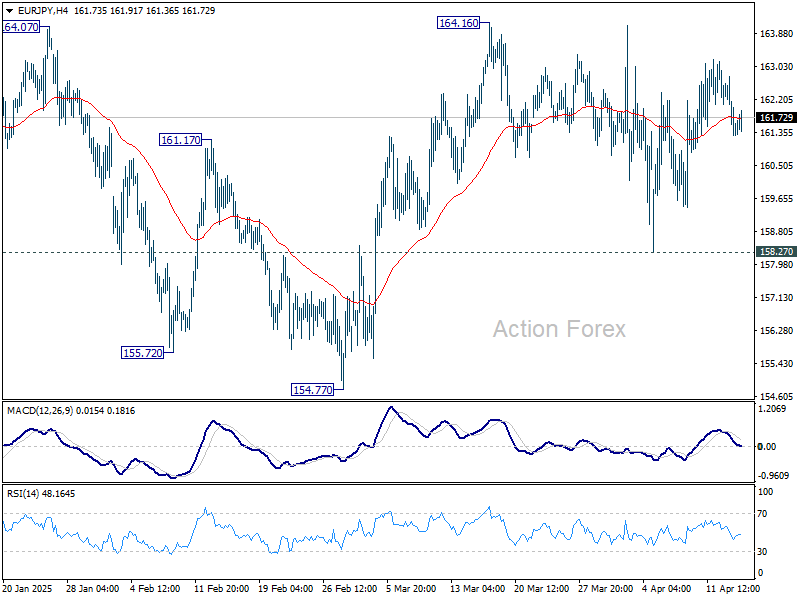

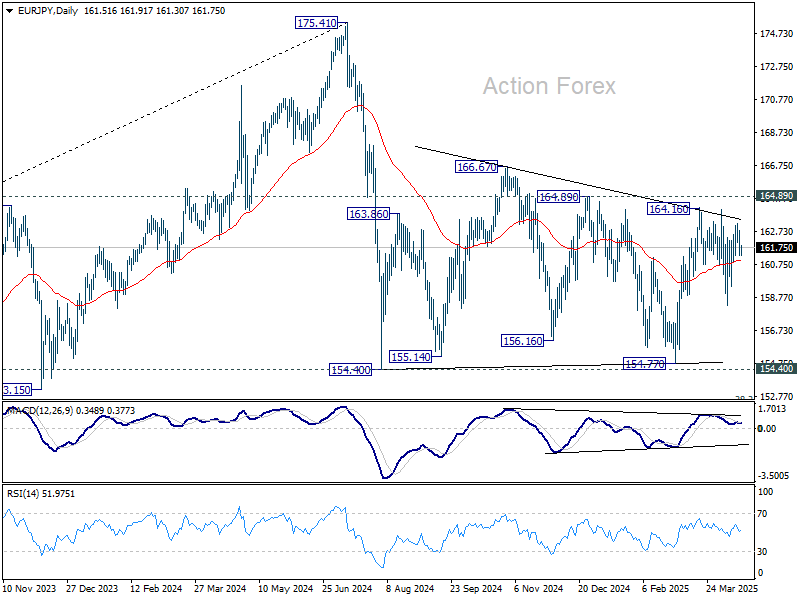

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.01; (P) 161.91; (R1) 162.52; More...

Range trading continues in EUR/JPY and intraday bias stays neutral. On the upside, above 164.16 will resume the rally from 154.77 to 164.89 resistance, and then 166.67. However, decisive break of 158.27 support will bring deeper decline back to 154.77 support. Overall, sideway consolidation pattern from 154.40 is still extending.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

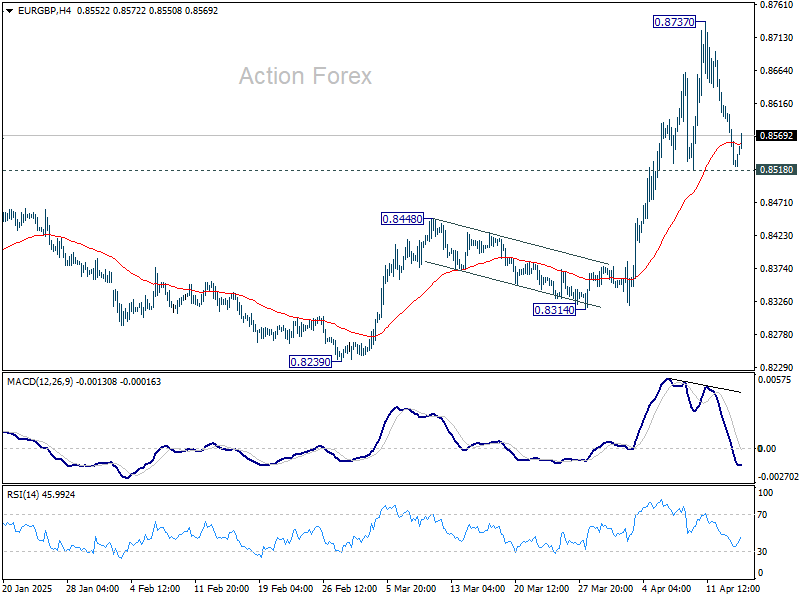

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8495; (P) 0.8556; (R1) 0.8587; More...

No change in EUR/GBP's outlook and intraday bias stays neutral. Consolidations from 0.8737 could extend but further rise is still expected as long as 0.8518 support holds. On the upside, break of 0.8737 will resume the larger rally from 0.8221.

In the bigger picture, down trend from 0.9267 (2022 high) should have completed at 0.8221, just ahead of 0.9201 key support (2024 low). Rise from 0.8221 is likely reversing the whole fall. Further rise should be seen to 61.8% retracement of 0.9267 to 0.8221 at 0.8867 next. This will now remain the favored case as long as 0.8472 resistance turned support holds.

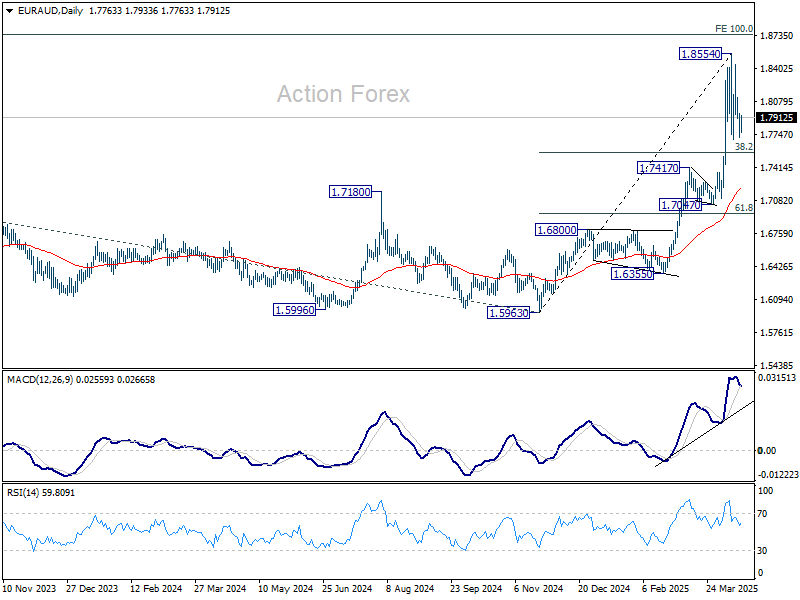

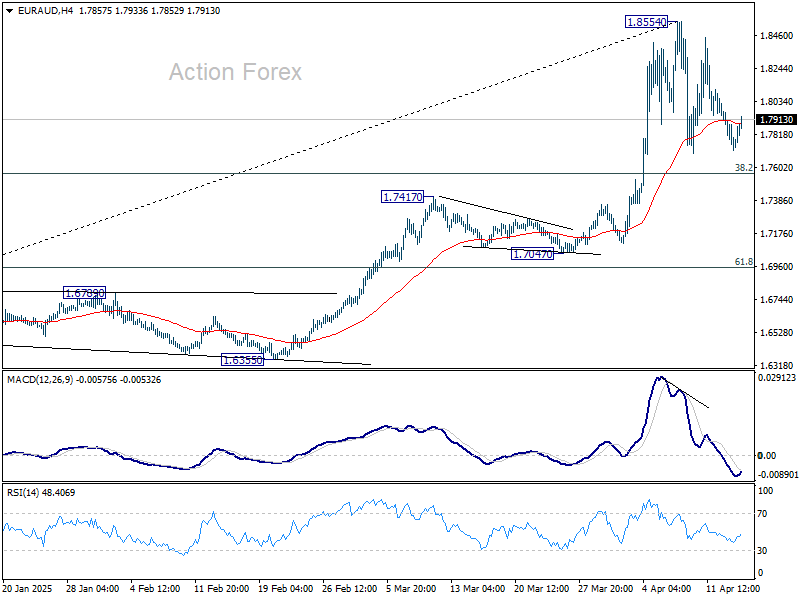

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.7673; (P) 1.7821; (R1) 1.7925; More...

Intraday bias in EUR/AUD remains neutral as consolidation from 1.8554 short term top is still extending. Downside of the pull back should be contained by 38.2% retracement of 1.5963 to 1.8854 at 1.7750. On the upside, firm break of 1.8554 will resume larger up trend.

In the bigger picture, up trend from 1.4281 (2022 low) is in progress, and in reacceleration phase as seen in W MACD. Next target is 100% projection of 1.4281 to 1.7062 from 1.5963 at 1.8744. Firm break there will pave the way to 138.2% projection at 1.9806, which is close to 1.9799 (2020 high). Outlook will remain bullish as long as 1.7417 resistance turned support holds even in case of deep pullback.