Sample Category Title

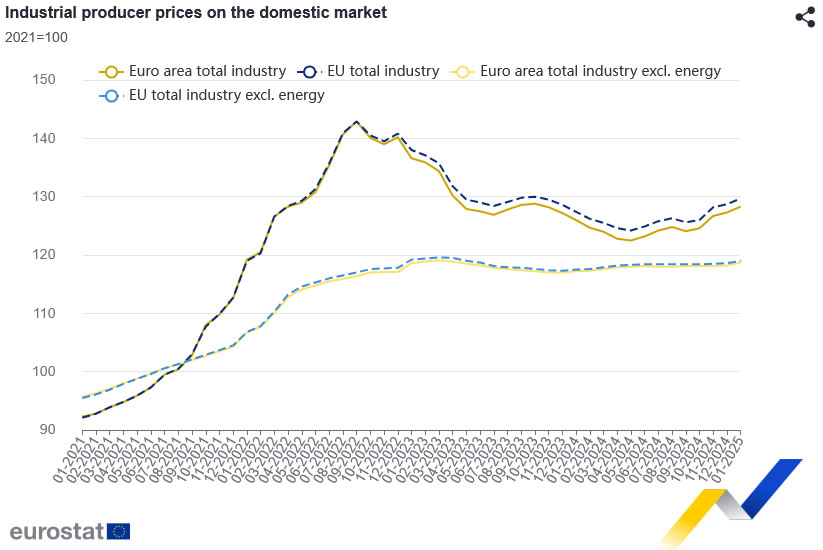

Eurozone PPI up 0.8% mom 1.8% yoy in Jan, above expectations.

Eurozone producer prices rose sharply by 0.8% mom and 1.8% yoy in January, exceeding expectations of 0.3% mom and 1.4% yoy, respectively.

The monthly increase in Eurozone PPI was primarily driven by a 1.7% mom jump in energy prices, while capital goods and durable consumer goods also saw notable gains of 0.7% mom and 0.6%, respectively. Intermediate goods prices edged up by 0.3% mom, while non-durable consumer goods saw a modest 0.2% mom rise.

The broader EU also recorded a 0.8% mom, 1.8% yoy in producer prices. Among individual member states, Ireland saw the largest monthly price jump at 6.2%, followed by Bulgaria (+5.4%) and Sweden (+2.3%).

However, not all countries experienced inflationary pressures, as Portugal (-2.2%), Austria (-0.6%), Slovenia (-0.5%), and Cyprus (-0.3%) registered price declines.

EUR/JPY Moves Swiftly Up Near Familiar Support

- EUR/JPY climbs higher after finding solid ground.

- Technical signals are promising.

- Bullish trend reversal remains uncertain.

EURJPY picked up steam on the back of news that Germany plans to inject hundreds of billions into defense and infrastructure investments, rapidly approaching the 160.00 mark after bouncing off the well-tested 155.50 support level.

Currently, the pair is setting its sights on the 50-day simple moving average (SMA) at 160.30 and the psychologically significant 161.00 level. A decisive close above this region could pave the way for a challenge of the resistance trendline at 162.70 and the 200-day SMA at 163.20. However, for a true bullish trend reversal to materialize, the rally would need to convincingly extend beyond 165.00.

Momentum indicators suggest further upside in the near term. The RSI is strengthening above the neutral 50 mark, and the MACD is widening its gap above the red signal line – both encouraging signs for buyers. That said, the stochastic oscillator’s entry into overbought territory hints at a possible consolidation phase before the next move.

On the downside, if the bears regain control, initial support may emerge near the 20-day SMA around 157.70, followed by the well-established 155.55 base. A break below the latter could put sellers back in the driver’s seat, with 154.37 – the area that has acted as a buffer multiple times in the past two years – standing as the next line of defense. A failure to hold there might clear the way towards the 151.00 level.

Overall, EURJPY appears poised to maintain its positive momentum in the short term, but whether this recovery can evolve into a sustained bullish breakout remains to be seen, as key obstacles continue to loom ahead.

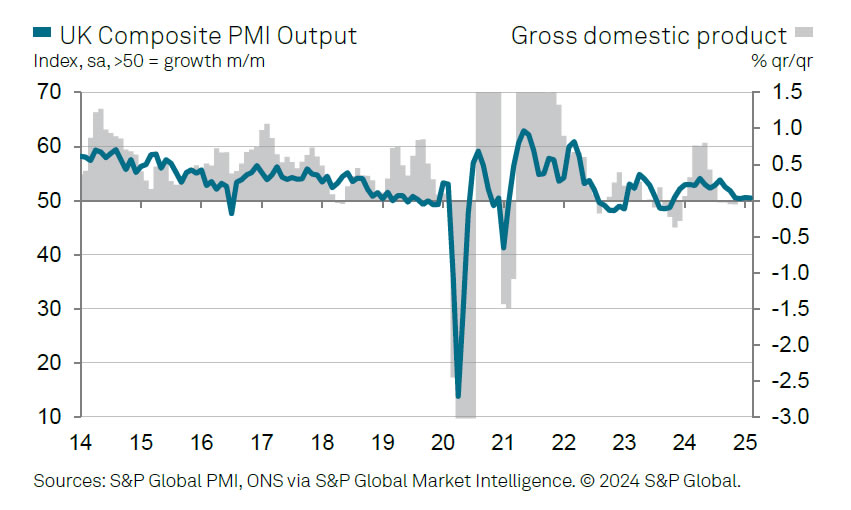

UK PMI services finalized at 51, stagflation risks grow

The UK services sector showed little improvement in February, with PMI Services finalized at 51.0, slightly up from January’s 50.8 but still well below its long-run average of 54.3. Meanwhile, PMI Composite edged lower from 50.6 to 50.5, signaling stagnant overall economic activity as demand conditions continue to weaken both domestically and in export markets.

Tim Moore, Economics Director at S&P Global Market Intelligence, warned of "elevated risk of stagflation on the horizon". New orders falling at their sharpest rate in over two years. Rising payroll costs and economic uncertainty have eroded business confidence, bringing sentiment to its lowest level since December 2022.

Concerns over slowing growth and persistent inflation pressures have also led to continued job losses, with employment in the services sector contracting for a fifth straight month—the longest period of decline outside of the pandemic since early 2011.

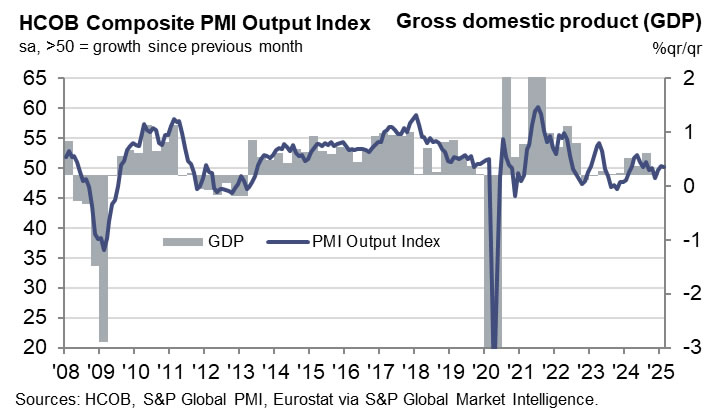

Eurozone PMI composite finalized at 50.2, barely grow for two months

Eurozone economy showed little momentum in February, with PMI Services finalizing at 50.6, down from 51.3 in January, while PMI Composite was unchanged at 50.2.

The picture was mixed across the region with Spain, Ireland, and Italy showing signs of expansion, while Germany’s services sector slowed and France’s continued its sharp contraction, posting its lowest reading in 13 months at 45.1.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that services growth is barely offsetting the prolonged slump in manufacturing. He pointed to rising input costs, particularly wage pressures, as a growing concern for ECB.

Political uncertainty in key economies is also weighing on sentiment. France’s services sector is deteriorating at a much faster pace, likely influenced by unresolved political instability. In contrast, Germany’s services sector, though slowing, remains in expansion, with hopes that post-election stability could support economic recovery.

However, with external risks from trade tensions and weak consumer spending, a decisive rebound in Eurozone remains uncertain.

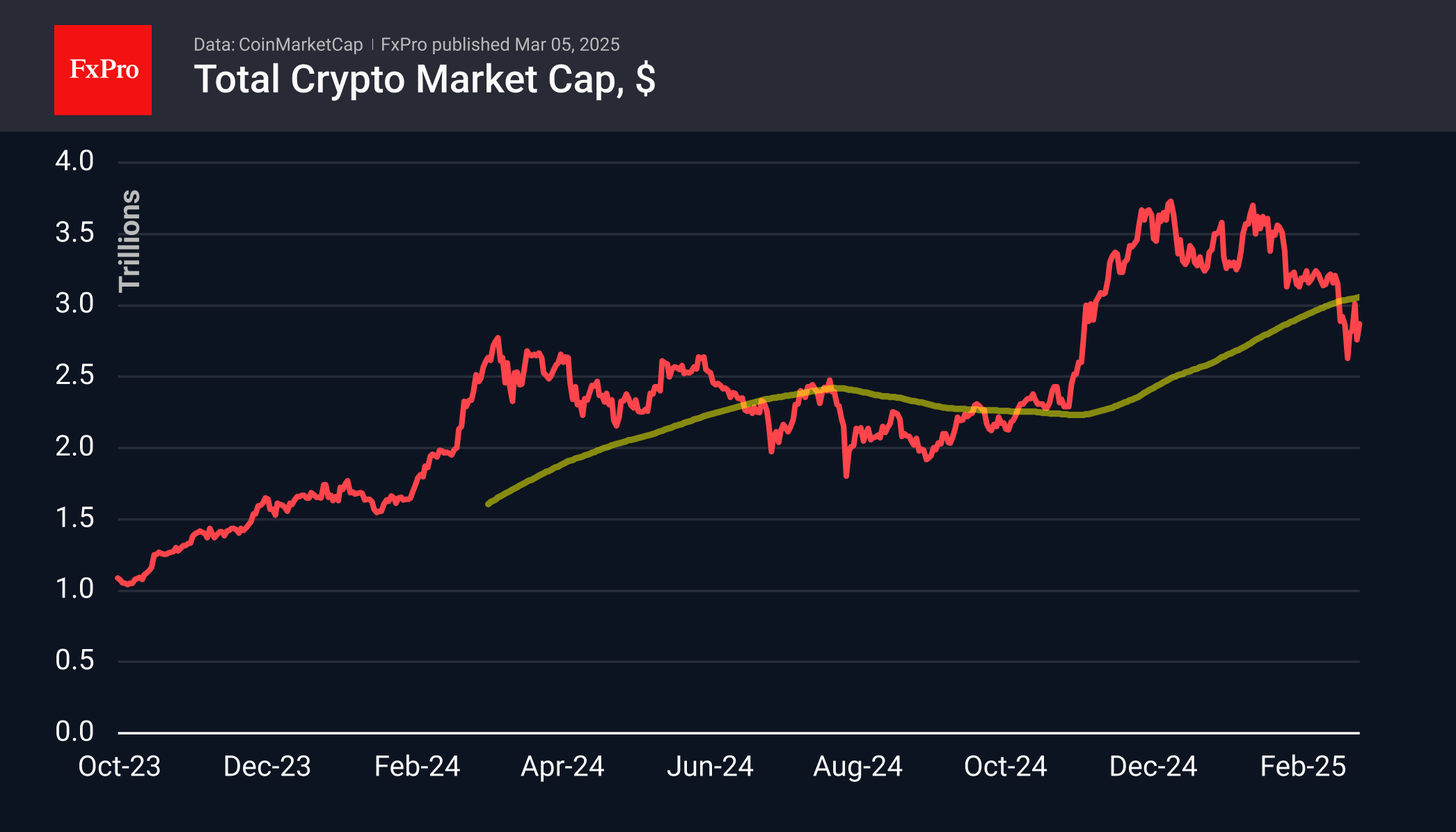

Crypto’s Unconvincing Rebound

Market Picture

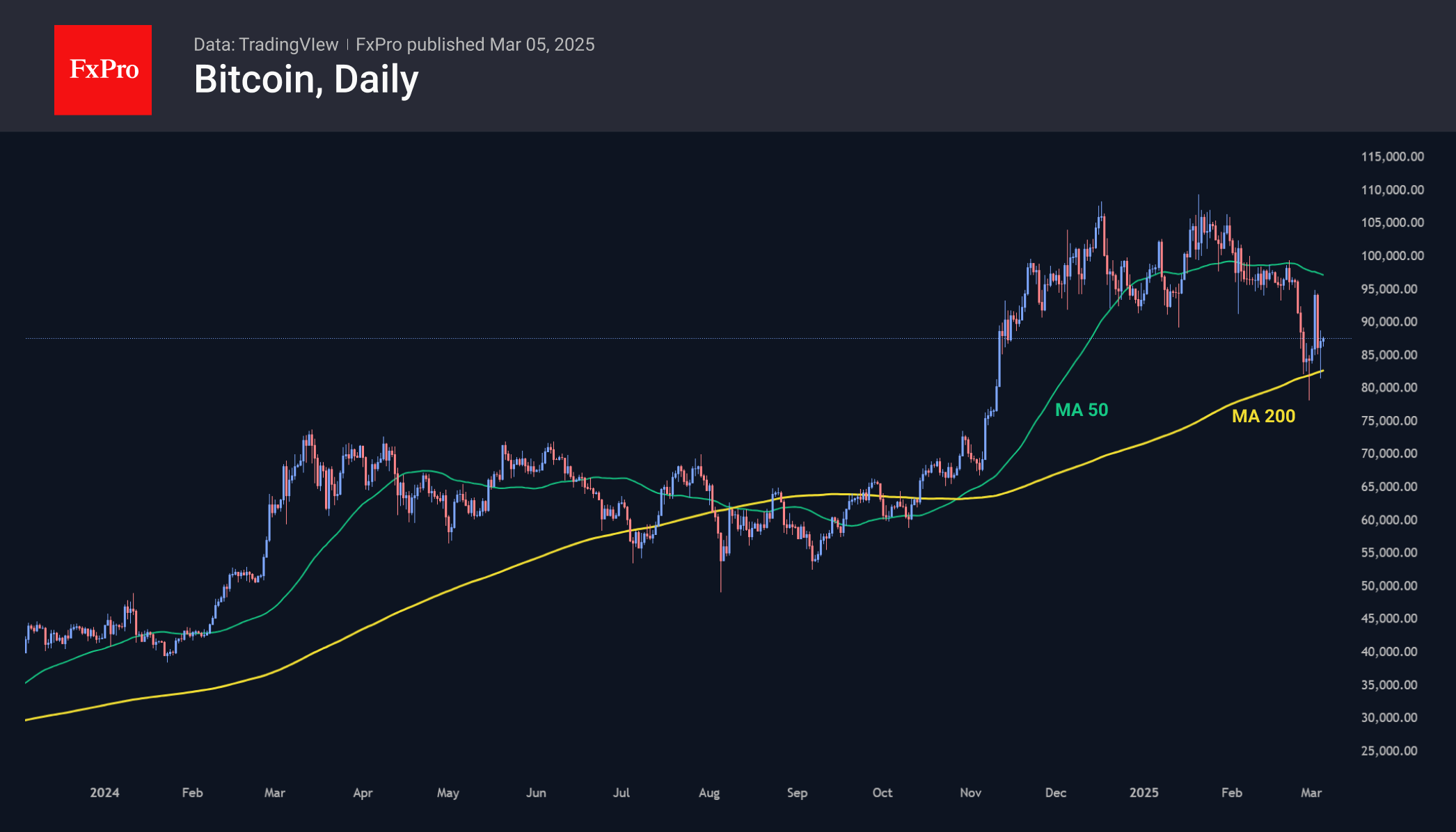

The crypto market has gained 4% in cap in 24 hours, but this looks more like a wild swing than the start of a recovery. The $2.87 trillion market remains below the long-term trend line of the 200-day moving average, near $3 trillion, and the initiative has shifted back to Bitcoin.

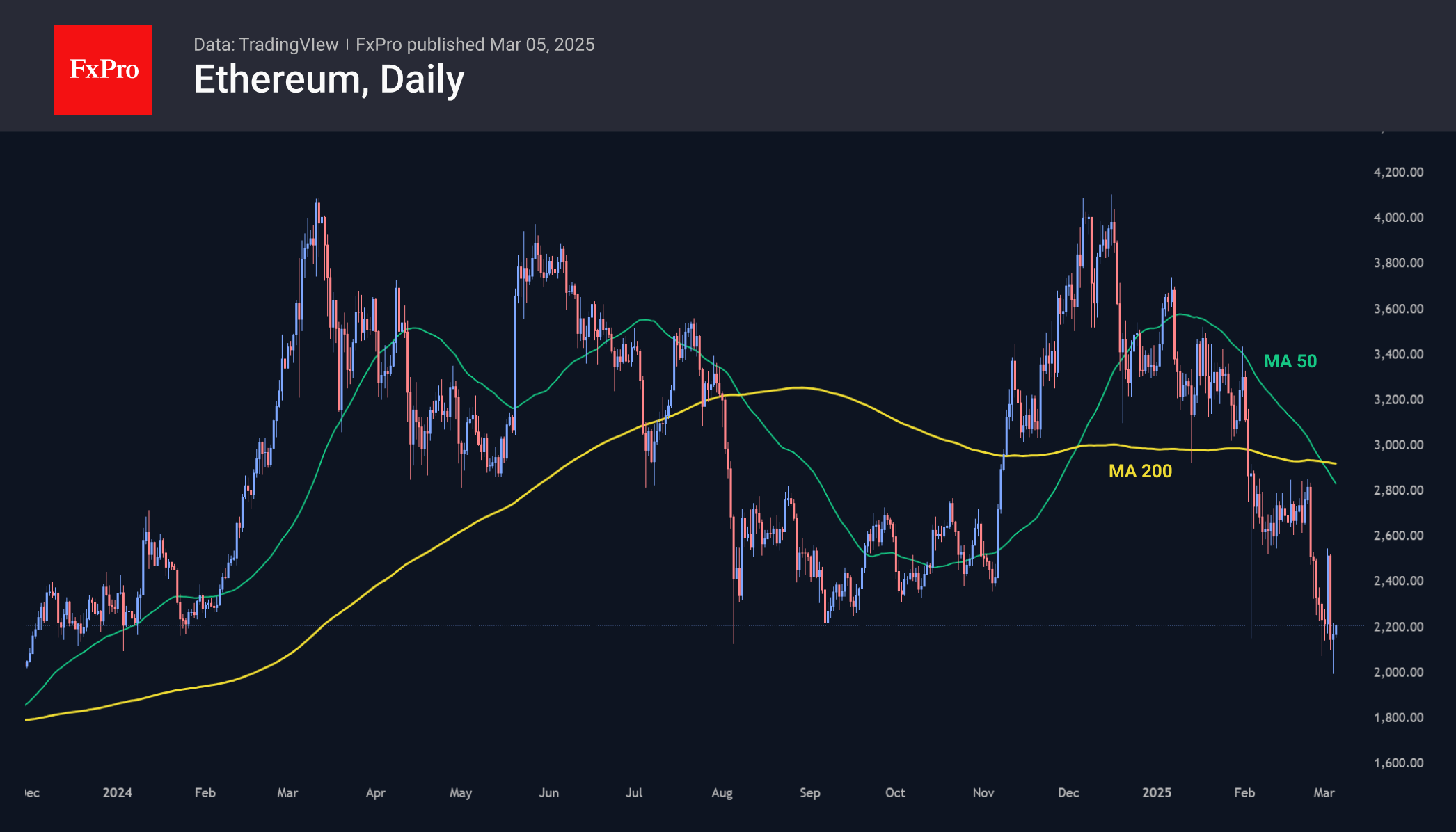

Bitcoin’s share of the crypto market exceeds 60%, which is typical in periods of fear. This time, we also note the decline in Ethereum’s share to 9%, a low in almost five years. This negative trend has been maintained for the last two years with brief spikes.

Bitcoin continues to flirt with the 200-day MA, popping out on Tuesday shortly after touching that level below $83,000. Wednesday morning’s market dynamics reflect cautious attempts to form a bottom. A return to the area above the 50-day at $97,000 is a marker of bullish success.

Ethereum is trading below $2200. Earlier in the week, it dipped below $2000 at the peak of the decline but stabilised near the support line in early 2024. This dangerous proximity to the lower end of the trading range keeps our focus on ETH as the market’s canary, which is having a tough time right now.

News Background

Net outflows from spot Ethereum-ETFs in the US fell to $12.1 million on 3 March, a negative trend for the eighth consecutive trading session. Total inflows since the product launch on 23 July fell to $2.81bn.

President of Euro Pacific Capital and bitcoin critic Peter Schiff called on Congress to launch an investigation into US President Donald Trump’s actions in the field of cryptocurrencies. He said the politician’s posts on the Truth Social platform, which led to a sharp rise in cryptocurrencies and then their fall, could have been part of a pump-and-dump scheme.

Affiliates of the collapsed FTX and Alameda addresses unlocked 3.03 million SOLs worth $431 million, Lookonchain said. This is the largest withdrawal since November 2023. Most of the tokens were sold through Binance and Coinbase at an average price of $125.8 per coin.

EUR/USD Rallies While USD/CHF Dips Further

EUR/USD started a fresh increase above the 1.0550 resistance. USD/CHF declined and now struggling below the 0.8950 resistance.

Important Takeaways for EUR/USD and USD/CHF Analysis Today

- The Euro started a decent recovery wave from the 1.0360 zone against the US Dollar.

- There is a connecting bullish trend line forming with support near 1.0570 on the hourly chart of EUR/USD at FXOpen.

- USD/CHF declined below the 0.8975 and 0.8950 support levels.

- There is a short-term contracting triangle forming with resistance near 0.8910 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair started a fresh increase from the 1.0360 zone. The Euro cleared the 1.0450 resistance to move into a bullish zone against the US Dollar, as mentioned in the last analysis.

The bulls pushed the pair above the 50-hour simple moving average and 1.0550. Finally, the pair tested the 1.0635 resistance. A high was formed near 1.0637 and the pair is now consolidating gains above the 23.6% Fib retracement level of the upward wave from the 1.0359 swing low to the 1.0637 high.

Immediate support on the downside is near a connecting bullish trend line at 1.0570. The next major support is the 1.0500 level and the 50% Fib retracement level of the upward wave from the 1.0359 swing low to the 1.0637 high.

A downside break below the 1.0500 support could send the pair toward the 1.0465 level. Any more losses might send the pair into a bearish zone toward 1.0425.

Immediate resistance on the EUR/USD chart is near the 1.0635 zone. The first major resistance is near the 1.0665 level. An upside break above the 1.0665 level might send the pair toward the 1.0720 resistance.

The next major resistance is near the 1.0750 level. Any more gains might open the doors for a move toward the 1.0800 level.

USD/CHF Technical Analysis

On the hourly chart of USD/CHF at FXOpen, the pair started a fresh decline from well above the 0.9000 zone. The US Dollar dropped below the 0.8975 support to move into a negative zone against the Swiss Franc.

The bears pushed the pair below the 50-hour simple moving average and 0.8920. Finally, the bulls appeared near the 0.8870 level. A low was formed near 0.8871 and the pair is now consolidating losses.

There was a minor increase and the pair tested the 23.6% Fib retracement level of the downward move from the 0.9036 swing high to the 0.8871 low. On the upside, the pair could face resistance near the 0.8910 level.

There is also a short-term contracting triangle forming with resistance near 0.8910. The next major resistance is near the 50% Fib retracement level of the downward move from the 0.9036 swing high to the 0.8871 low at 0.8950, above which the pair could test the 0.8975 level.

If there is a clear break above the 0.8975 resistance zone, the pair could start another increase. In the stated case, it could even surpass 0.9000.

On the downside, immediate support on the USD/CHF chart is 0.8900. The first major support is near the 0.8870 level. The next major support is near 0.8850. Any more losses may possibly open the doors for a move toward the 0.8820 level in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

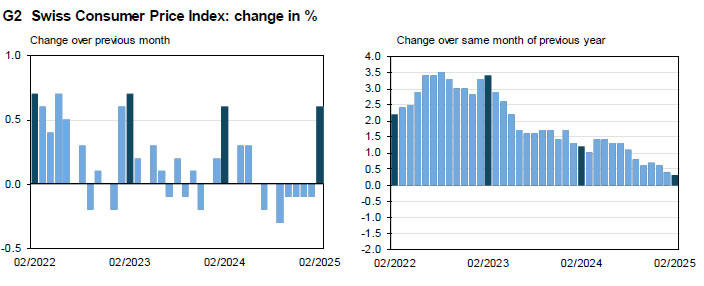

Swiss annual CPI ticks down to 0.3% yoy, remains weak

Swiss inflation accelerated on a monthly basis in February, with CPI rising 0.6% mom, slightly above the expected 0.5%. Core CPI, which excludes fresh and seasonal products, energy, and fuel, increased by 0.7% mom. The rise was driven by both domestic and imported product prices, which climbed 0.5% mom and 0.9% mom, respectively.

However, the broader inflation trend remains subdued. On a year-over-year basis, headline CPI slowed to 0.3% yoy from 0.4% yoy, though it was still slightly above expectations of 0.2% yoy. Core CPI remained steady at 0.9% yoy. While domestic product price inflation eased from 1.0% yoy to 0.9% yoy, imported prices continued to contract, staying at -1.5% yoy.

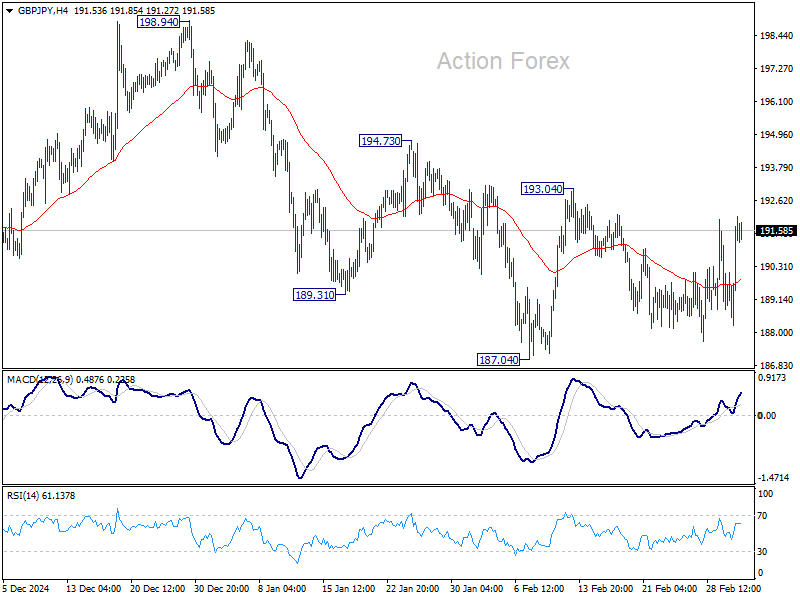

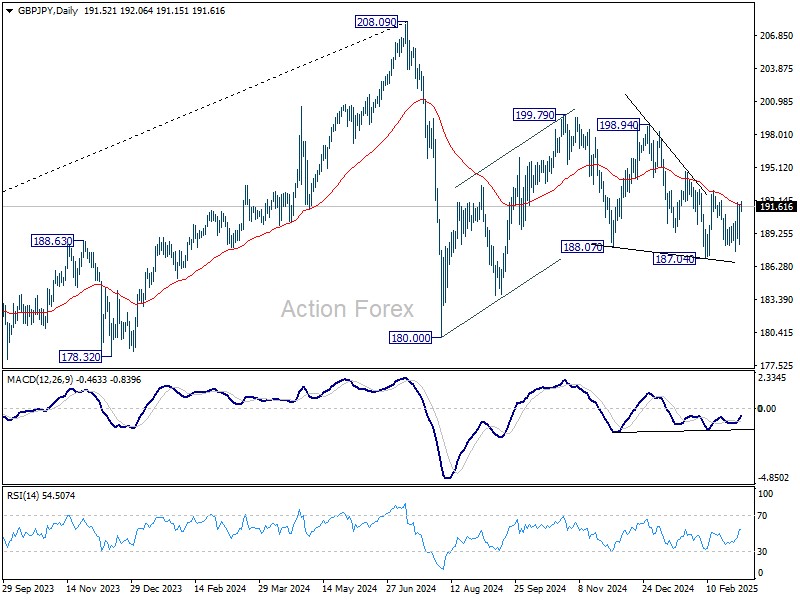

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.36; (P) 190.57; (R1) 192.89; More...

No change in GBP/JPY's outlook as range trading continues. O the upside, fir break of 193.04 will resume the rebound from 187.04 to 194.73 resistance, and then 198.94. On the downside, firm break of 187.04 will extend the fall from 199.79 towards 180.00 support. Overall, corrective pattern from 180.00 might still be extending.

In the bigger picture, price actions from 208.09 are seen as a correction to rally from 123.94 (2020 low). Strong support should be seen from 38.2% retracement of 123.94 to 208.09 at 175.94 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction.

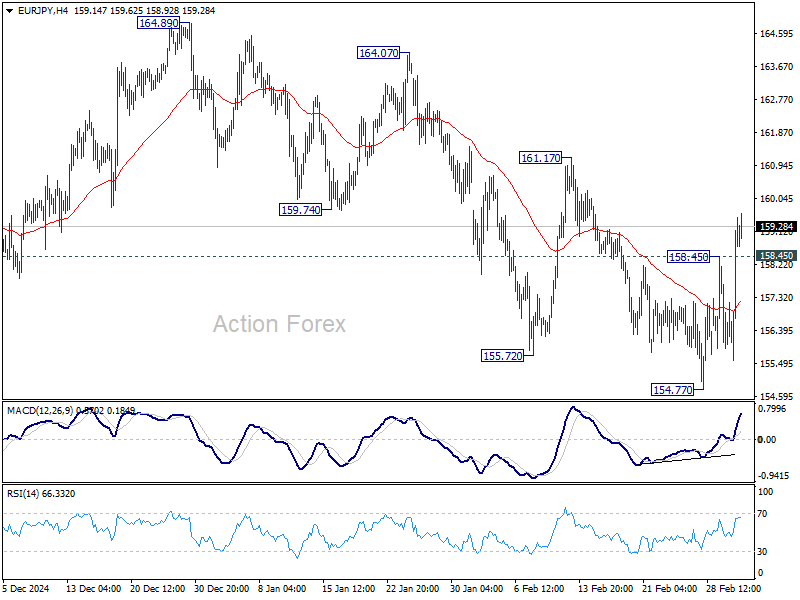

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.79; (P) 158.00; (R1) 160.41; More...

EUR/JPY's rebound from 154.77 resumed and break of 158.45 indicates short term bottoming. Intraday bias is back on the upside. Sustained break of 55 D EMA (now at 159.55) will argue that corrective pattern from 154.40 has started another rising leg, and target 161.17 resistance and above.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). Strong support should be seen from 38.2% retracement of 114.42 to 175.41 at 152.11 to contain downside. However, sustained break of 152.11 will bring deeper fall even still as a correction. Next target will be 100% projection of 175.41 to 154.40 from 166.67 at 145.66.

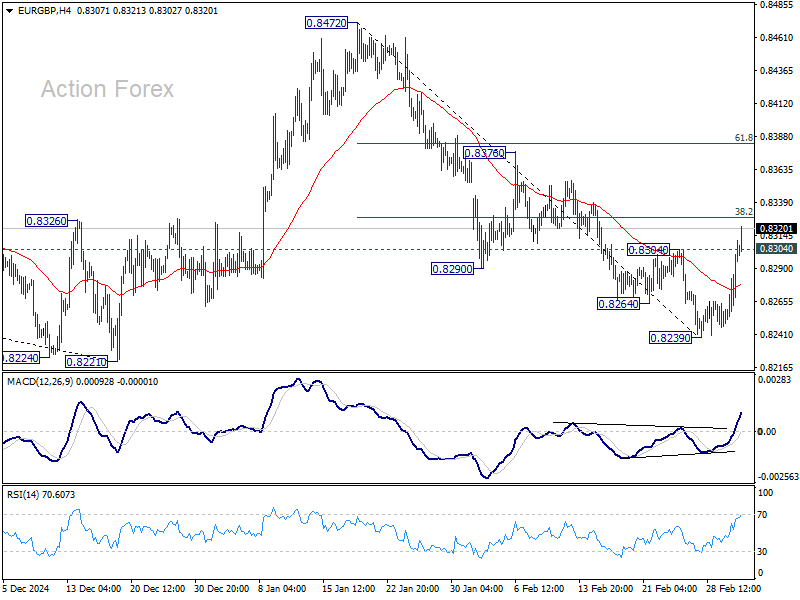

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8268; (P) 0.8287; (R1) 0.8323; More...

A short term bottom is in place in EUR/GBP with break of 0.8239 resistance. Intraday bias is back on the upside for 38.2% retracement of 0.8472 to 0.8239 at 0.8328. Sustained break there will argue that whole fall from 0.8472 has completed and target 61.8% retracement at 0.8383. However, rejection by 0.8328 will bring another decline through 0.8239 support.

In the bigger picture, the medium term down trend remains intact with EUR/GBP staying well inside the falling channel. Prior rejection by 55 W EMA (now at 0.8414) also affirm bearishness. Decisive break of 0.8201/8221 support zone will resume whole down trend from 0.9449 (2020 high) and carry larger bearish implications.