Sample Category Title

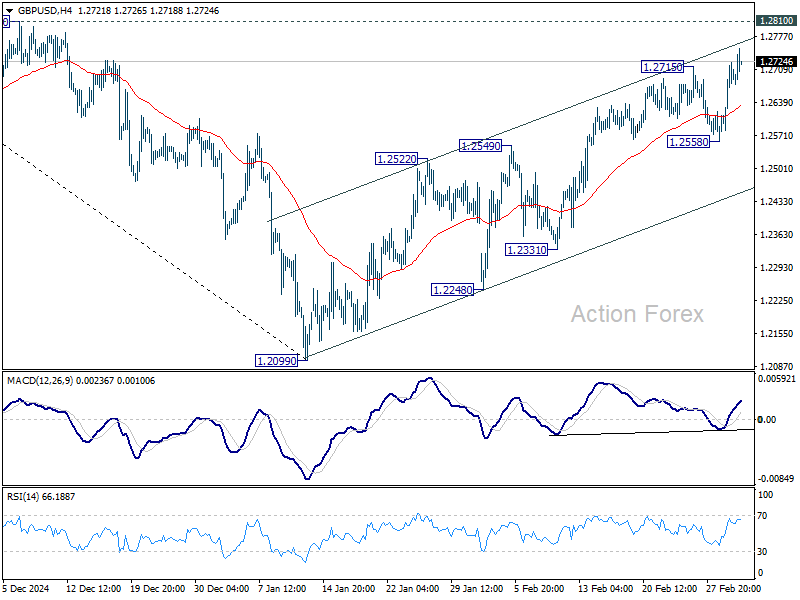

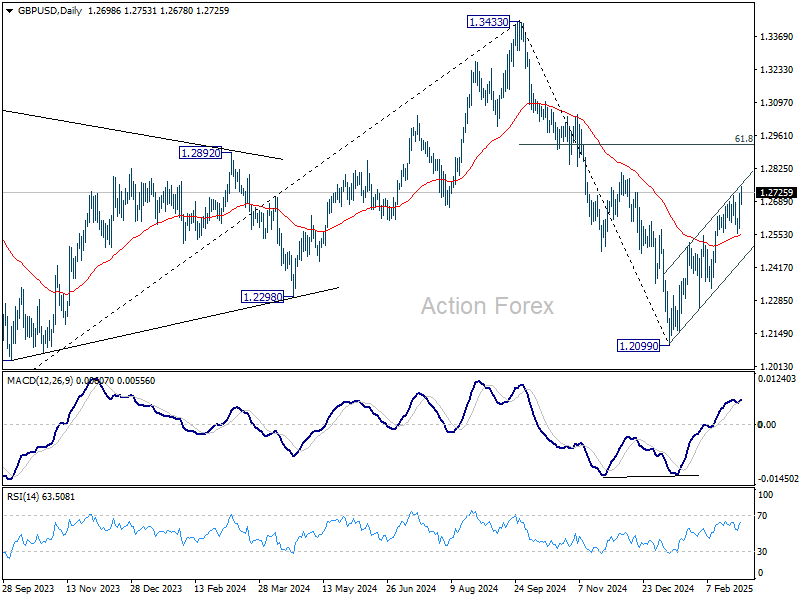

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2614; (P) 1.2669; (R1) 1.2757; More...

Intraday bias in GBP/USD remains on the upside as rise from 1.2099 is in progress for 1.2810 resistance. Firm break there will target 61.8% retracement of 1.3433 to 1.2099 at 1.2923. On the downside, break of 1.2558 will turn bias back to the downside for near term rising channel support (now at 1.2453).

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

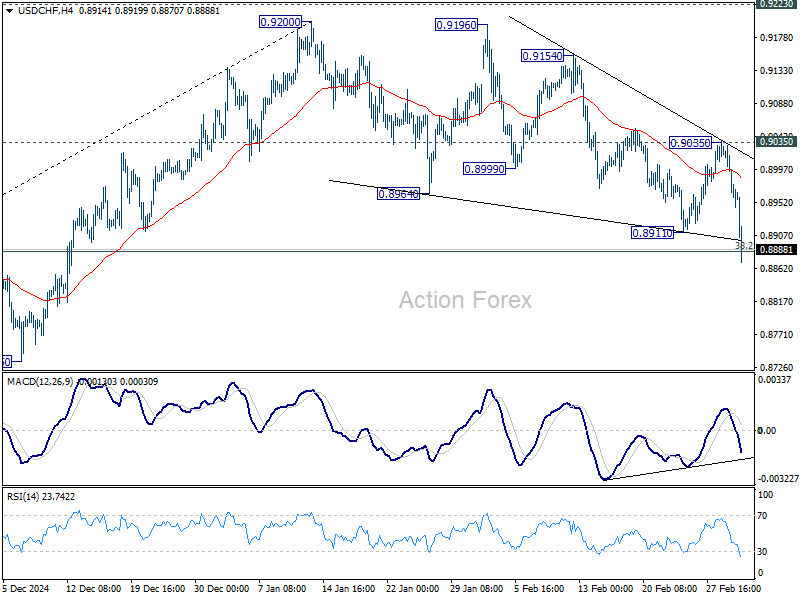

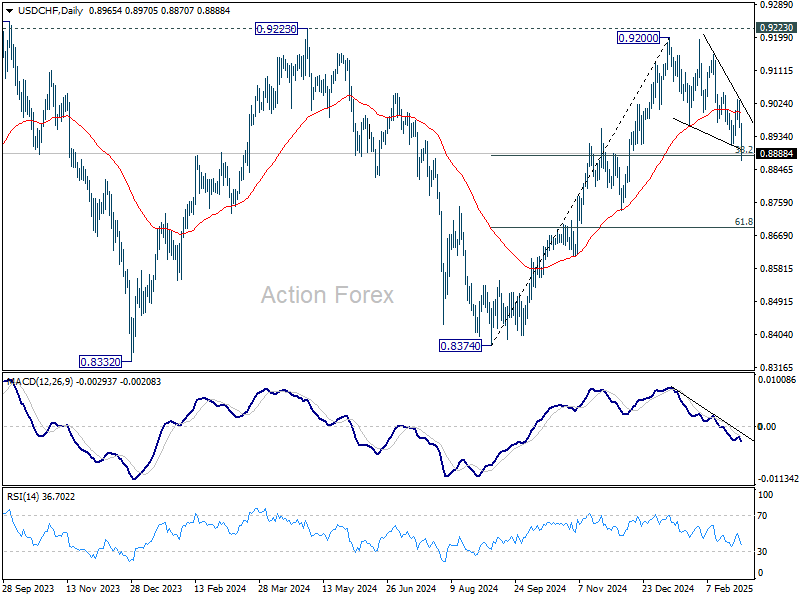

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8941; (P) 0.8987; (R1) 0.9013; More…

Intraday bias in USD/CHF is back on the downside as fall resumes through 0.8911 support. Immediate focus is now on 38.2% retracement of 0.8374 to 0.9200 at 0.8884 Strong rebound from current level, followed by break of 0.9035 resistance, will retain near term bullishness, and bring retest of 0.9200/23 resistance zone. However, firm break of 0.8444 will confirm rejection by 0.9223 resistance and turn near term outlook bearish.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

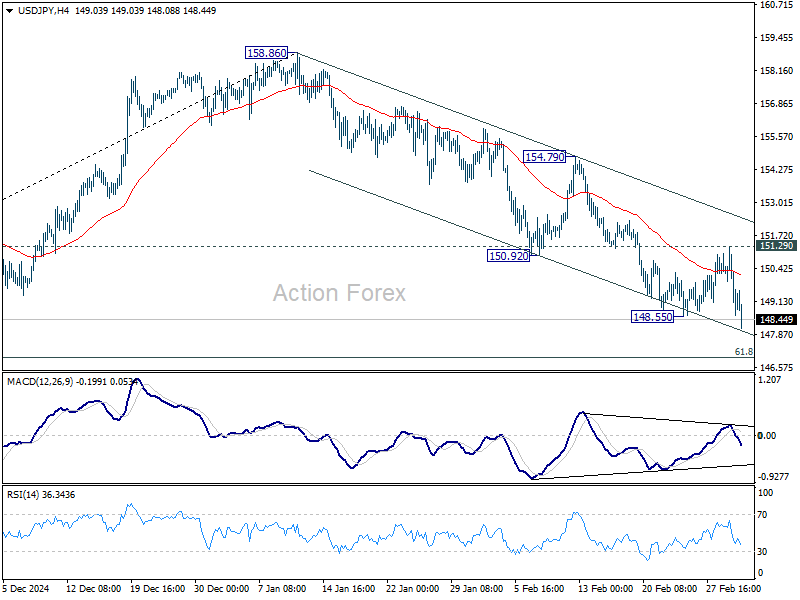

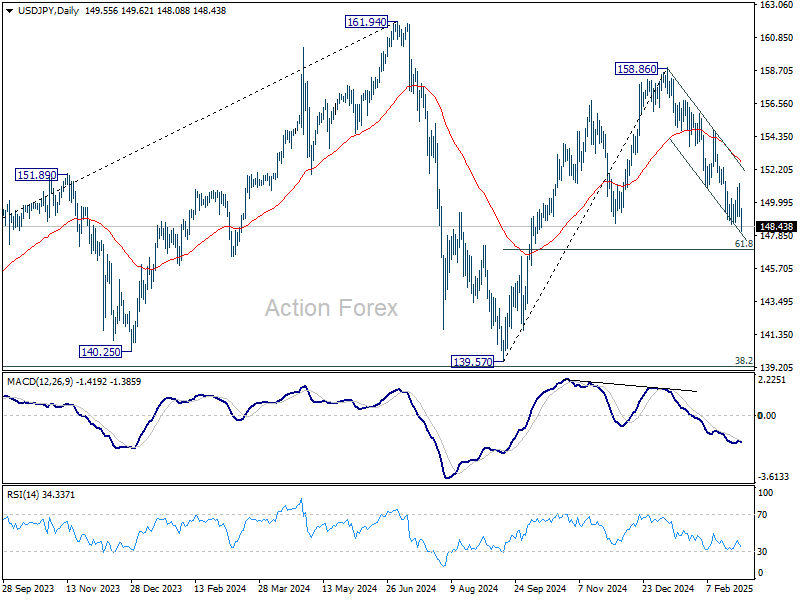

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.63; (P) 149.97; (R1) 150.83; More...

USD/JPY's fall from 158.86 resumed after brief consolidations and intraday bias is back on the downside. This decline is as the third leg of the corrective pattern from 161.94 high. Next target is 61.8% retracement of 139.57 to 158.86 at 146.32. Sustained break there will pave the way back to 139.57 low. For now, risk will remain on the downside as long as 151.29 resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

‘Trumpcession’ Concerns Drag Dollar Down, Fed Rate Cut Bets Surge

Dollar fell broadly today, an unusual development in contrast to recent rallies on escalating trade tensions and tariff announcements. Market sentiment soured as traders began to weigh the risks of a “Trumpcession,” a new term coined to describe the potential for US President Donald Trump’s policies to drive the economy into contraction or a full-blown recession.

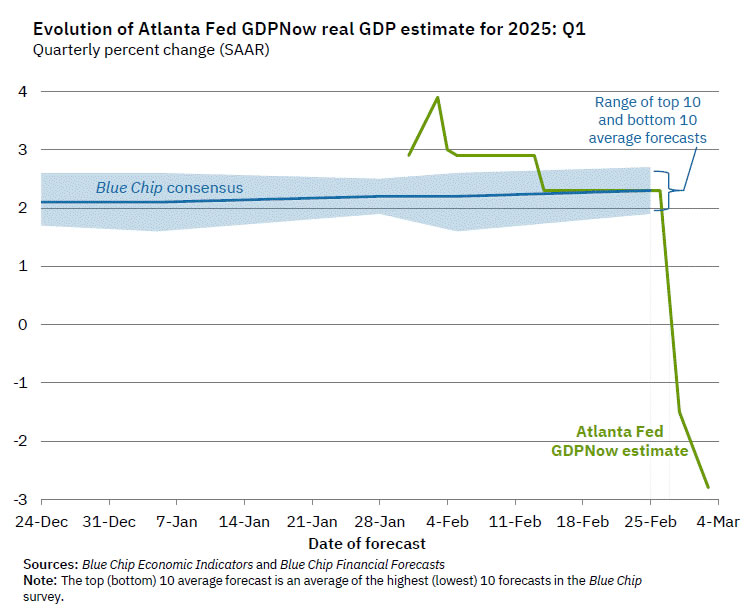

A major trigger for today’s shift in risk sentiment was the latest Atlanta Fed GDPNow estimate, which plummeted to -2.8% for Q1 2025, compared to -1.5% just days ago on February 28. This marks a dramatic deterioration in economic expectations, signaling that growth could already be already contracting at an alarming pace. Markets are increasingly recognizing that the tariff impact is not just theoretical—it is already weighing on consumption and business investment, and the effects could worsen in the coming months.

The first round of US tariffs officially took effect today, with a 25% levy imposed on Canada and Mexico, alongside a 20% additional tariff on Chinese imports. While this was expected, the concern now is the snowball effect. With more tariffs looming—including reciprocal tariffs set for April 2 and possible new levies on Japan and China for alleged currency devaluation.

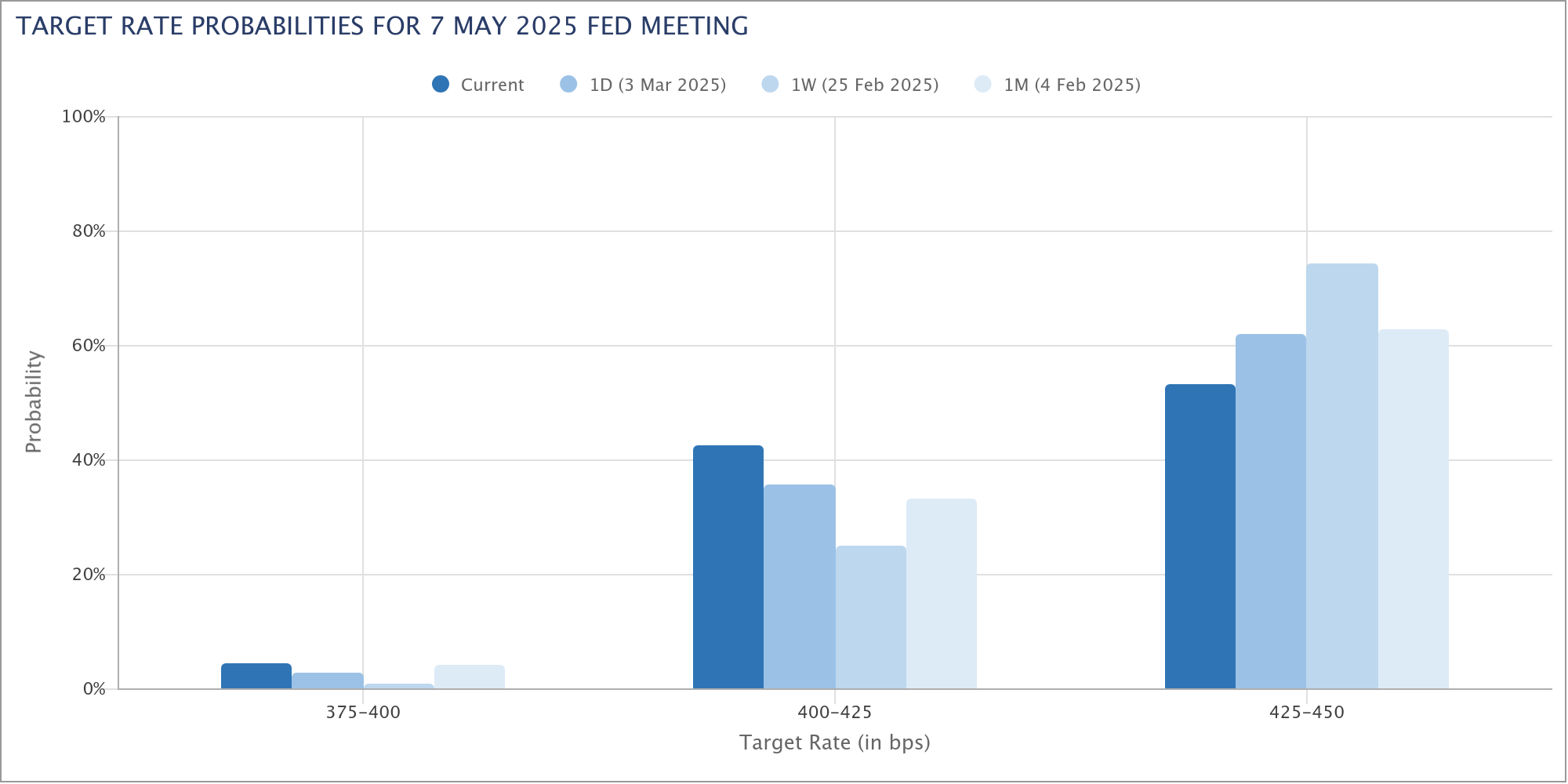

Market pricing for Fed rate cuts is accelerating too. Fed fund futures now assign a 47% probability of a rate cut in May, up from just 26% a week ago. If economic data continues to deteriorate, expectations could quickly rise above 50%, signaling that markets believe Fed will have little choice but to step in and resume monetary easing sooner than anticipated.

With overall sentiment on shakier ground, upcoming releases including tomorrow’s ISM services PMI and Friday’s non-farm payroll report have taken on added importance.

In the currency markets, Dollar is currently the worst performer of the day, followed by Aussie and Sterling. Meanwhile, Swiss Franc is leading gains, followed by Yen and Euro. Kiwi and Loonie are trading in the middle of the pack.

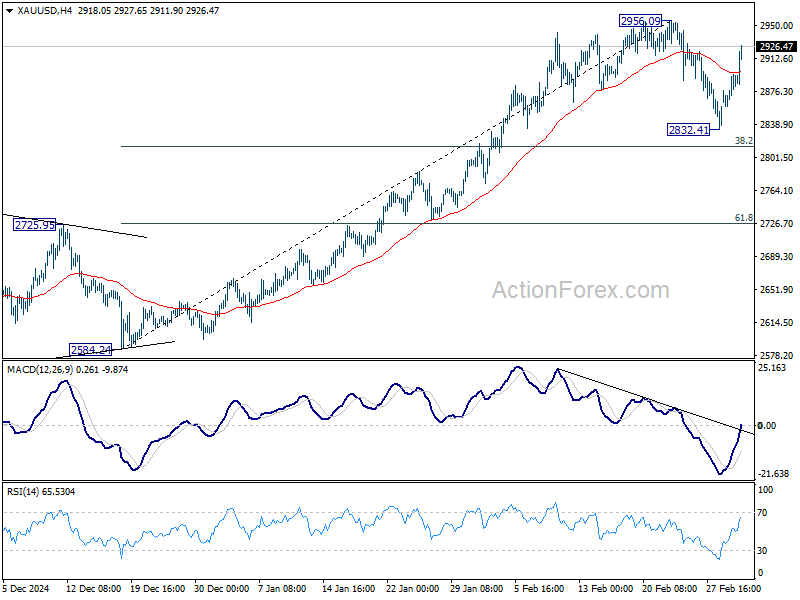

Technically, Gold reboounded strongly today following Dollar's selloff. The development suggests that pull back from 2956.09 is merely a near term correction, and has completed at 2832.41, ahead of 38.2% retracement of 2584.24 to 2956.09 at 2814.04. Retest of 2956.09 should be seen next and break there will resume larger up trend towards 3000 psychological level.

In Europe, at the time of writing, FTSE is down -0.75%. DAX is down -2.60%. CAC is down -1.68%. UK 10-year yield is down -0.068 at 4.444. Germanyu 10-year yield is down -0.027 at 2.466. Earlier in Asia, Nikkei fell -1.20%. Hong Kong HSI fell -0.20%. China Shanghai SSE rose 0.22%. Singapore Strait Times fell -0.28%. Japan 10-year JGB yield rose 0.018 to 1.428.

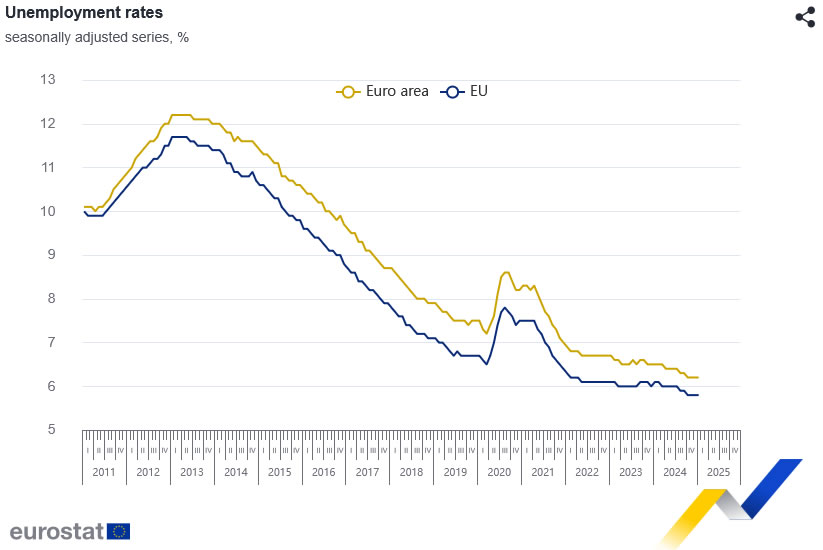

Eurozone unemployment rate unchanged at 6.2% in Jan

Eurozone unemployment rate was unchanged at 6.2% in January, coming in better than expectations of 6.3%. Across the broader EU, unemployment rate also held firm at 5.8%.

According to Eurostat, the number of unemployed individuals stood at 12.824 million in the EU, of which 10.655 million were in the Eurozone.

On a monthly basis, Eurozone unemployment fell by -42k, while the overall EU saw a more modest decline of -8k.

RBA minutes: No commitment to further rate cuts

The minutes from RBA’s February meeting reinforced the central bank’s cautious approach to monetary easing, making it clear that the recent 25bps rate cut to 4.10% does "not commit them to further reductions" in subsequent meetings.

Policymakers acknowledged that inflation has been falling at a “somewhat faster pace than expected,” which helped ease concerns over upside risks. However, they stressed that the path to returning inflation to target while maintaining labor market gains is “not yet assured.” The Board ultimately deemed that the stronger case was to ease policy, given the downside risks to the economy.

Despite the decision to cut, RBA members debated the risks of "easing policy too soon", recognizing that a premature policy shift could lead to resurgence in inflation.

They noted that if inflation proved “more persistent than expected,” holding the cash rate at 4.1% for an “extended period” or even tightening policy would be warranted.

Australia retail sales rises 0.3% mom, driving by food-related spending

Australia's retail sales turnover rose 0.3% mom to AUD 37.08B in January, matched expectations.

Robert Ewing, ABS head of business statistics, said: "While the pick-up in retail spending since mid-2024 has been boosted by more discretionary spending, this month’s rise is mostly driven by food-related spending."

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 148.63; (P) 149.97; (R1) 150.83; More...

USD/JPY's fall from 158.86 resumed after brief consolidations and intraday bias is back on the downside. This decline is as the third leg of the corrective pattern from 161.94 high. Next target is 61.8% retracement of 139.57 to 158.86 at 146.32. Sustained break there will pave the way back to 139.57 low. For now, risk will remain on the downside as long as 151.29 resistance holds, in case of recovery.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

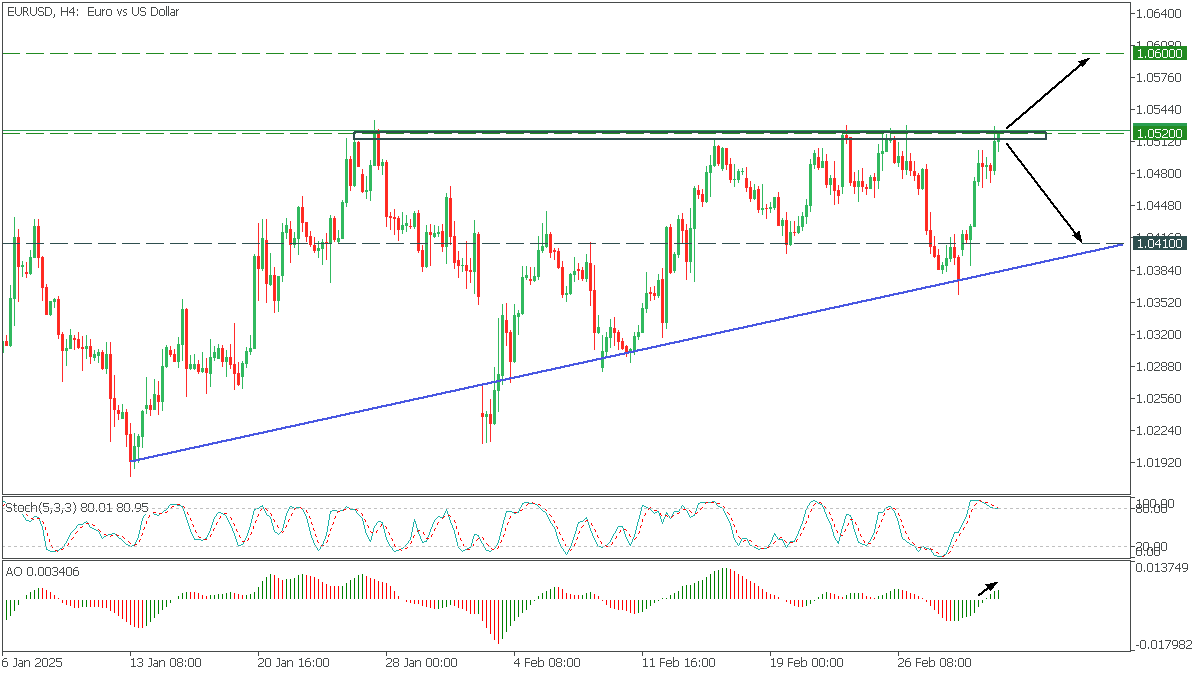

EURUSD: Rising triangle

EURUSD, H4

On the H4, EURUSD formed a rising triangle pattern, and the price reached the upper boundary. The AO confirms the growing bullish sentiment, but the Stochastic indicates the possibility of a decline.

- A break above 1.0520 will open the way to 1.0600;

- A rebound from the upper boundary will drop EURUSD to the lower trendline towards 1.0410;

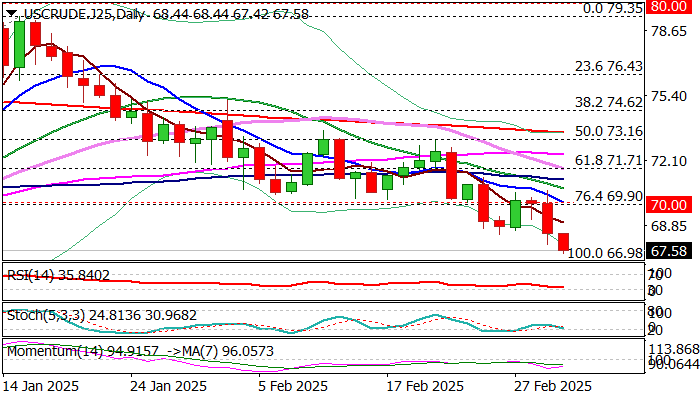

WTI: Crude Price Falls Further on Increased Output, Trade War Escalation

WTI Oil extends steep fall from Monday’s $70.58 lower top and hit the lowest in nearly three months on Tuesday.

A number of factors continue to weaken oil’s sentiment, with the latest decision of OPEC+ group to proceed with planned production increase, adding to growing uncertainty over escalation of trade war, as well as halt of US military aid to Ukraine.

Markets anticipate that economic slowdown in deepening trade conflict would significantly impact demand, while supply is expected to continue to rise and that would further weigh on oil prices.

Bearish technical picture on daily chart contribute to negative outlook, with recent break through significant supports at $70/$69.90 (psychological / Fibo 76.4% of $66.98/$79.35 rally) and multiple recovery rejections at this zone, before bears regained control, have generated strong bearish signal.

Upticks on partial profit-taking are likely to be limited and stay under $69.70/$70, now acting as solid resistances and reinforced by falling 10DMA, to keep larger bearish structure intact and offer better selling opportunities.

Res: 68.37; 69.00; 70.00; 70.58.

Sup: 67.42; 66.98; 66.54; 65.26.

RBA Minutes Hawkish, Aussie Edges Higher

The Australian dollar has edged higher on Tuesday. AUD/USD is trading at 0.6243 in the European session, up 0.28% on the day.

RBA minutes: Don’t count on more cuts

The Reserve Bank of Australia’s minutes from the February meeting reiterated the central bank’s cautious stance. The meeting marked a milestone as the RBA pressed the rate-cut trigger for the first time in four years, after maintaining the cash rate at 4.35% for over a year. The decision was a “hawkish cut” with a message for the markets not to expect a series of rate cuts.

In the minutes, members said the rate cut did not “commit them to further rate cuts”, a warning that the easing cycle could be short. The RBA remains concerned about inflation even though it has dropped to 2.4%, in the mid-range of the RBA’s target band of 2%-3%. Governor Bullock has said that the RBA is keeping a close eye on the labor market, which has been resilient and not supportive of further rate cuts.

Another headache for the RBA is the threat of US tariffs, in particular the specter of another US-China trade war. Both countries have imposed new tariffs on the other, and a damaging trade war would hurt Australia’s export industry, as China is Australia’s largest trading partner.

Australian retail sales rebound

Australia’s retail sales posted a turnaround in January, with a gain of 0.3% m/m. This matched the market estimate and followed the 0.1% decline in December. The driver of the gain was food-related spending and most sub-categories showed an increase in spending. The outlook for consumer spending has improved, with the RBA rate cut, the drop in inflation and cuts to income tax.

AUD/USD Technical

- AUD/USD is testing resistance at 0.6228. Above, there is resistance at 0.6251

- 0.6200 and 0.6177 are providing support

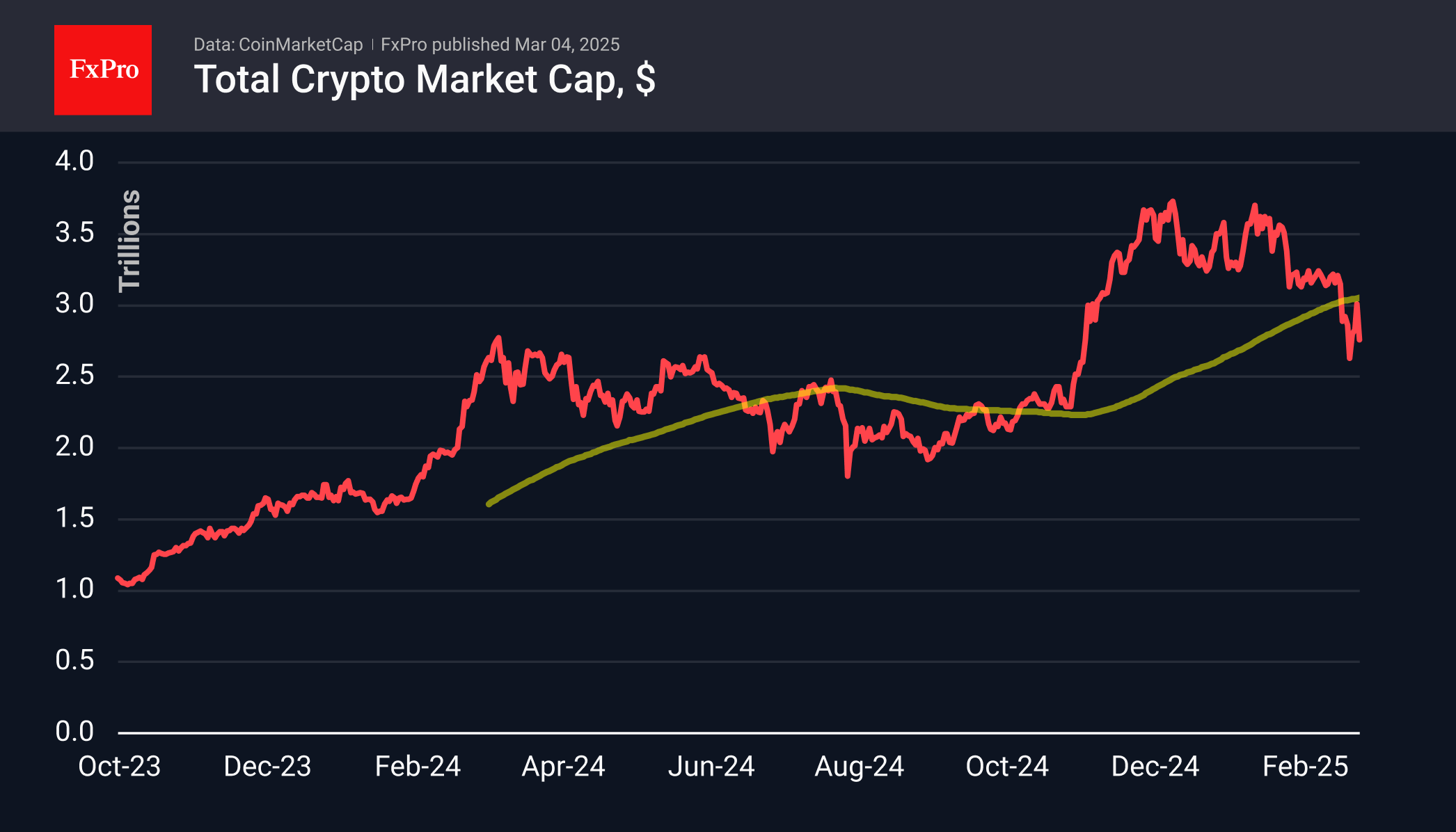

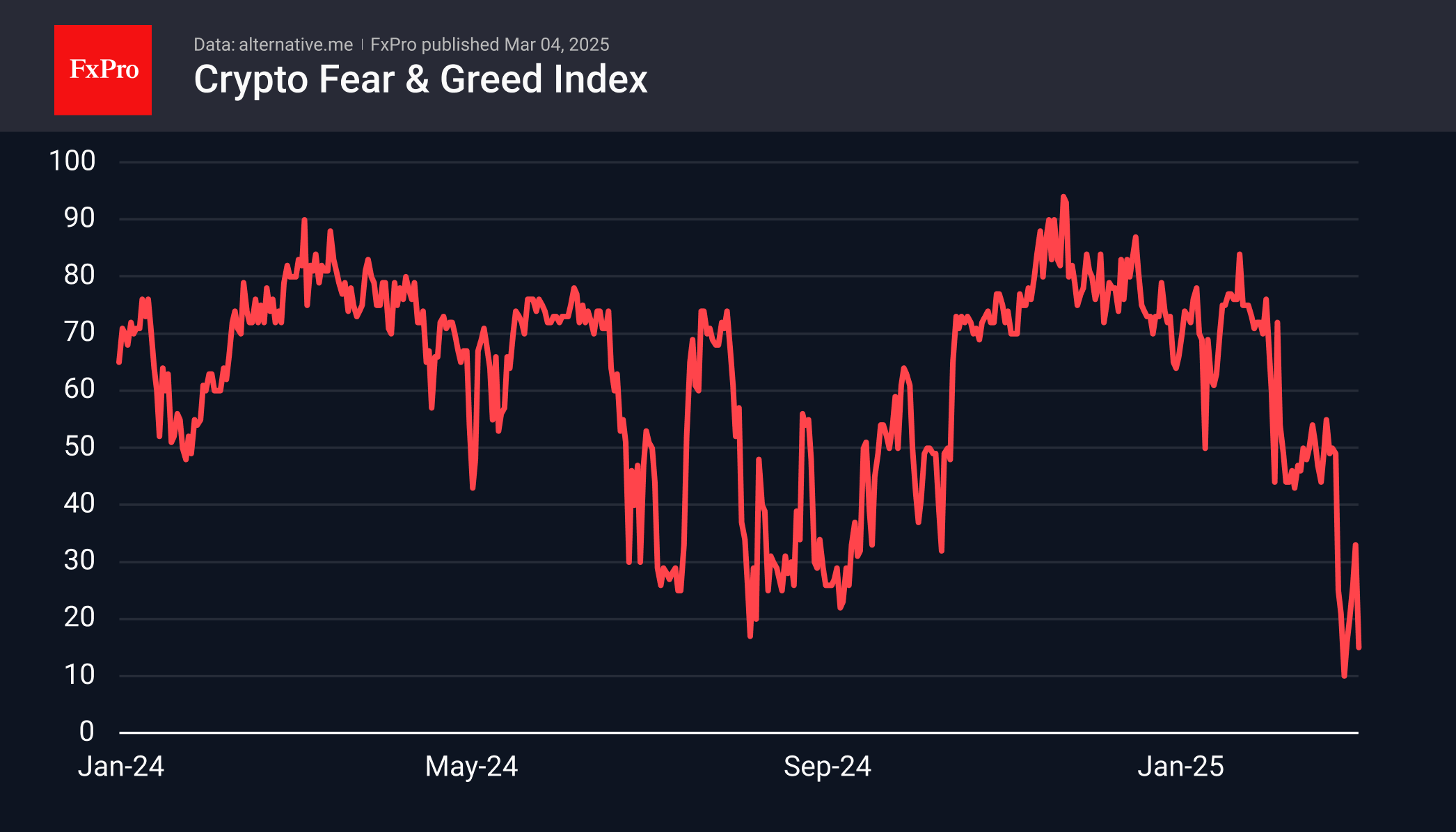

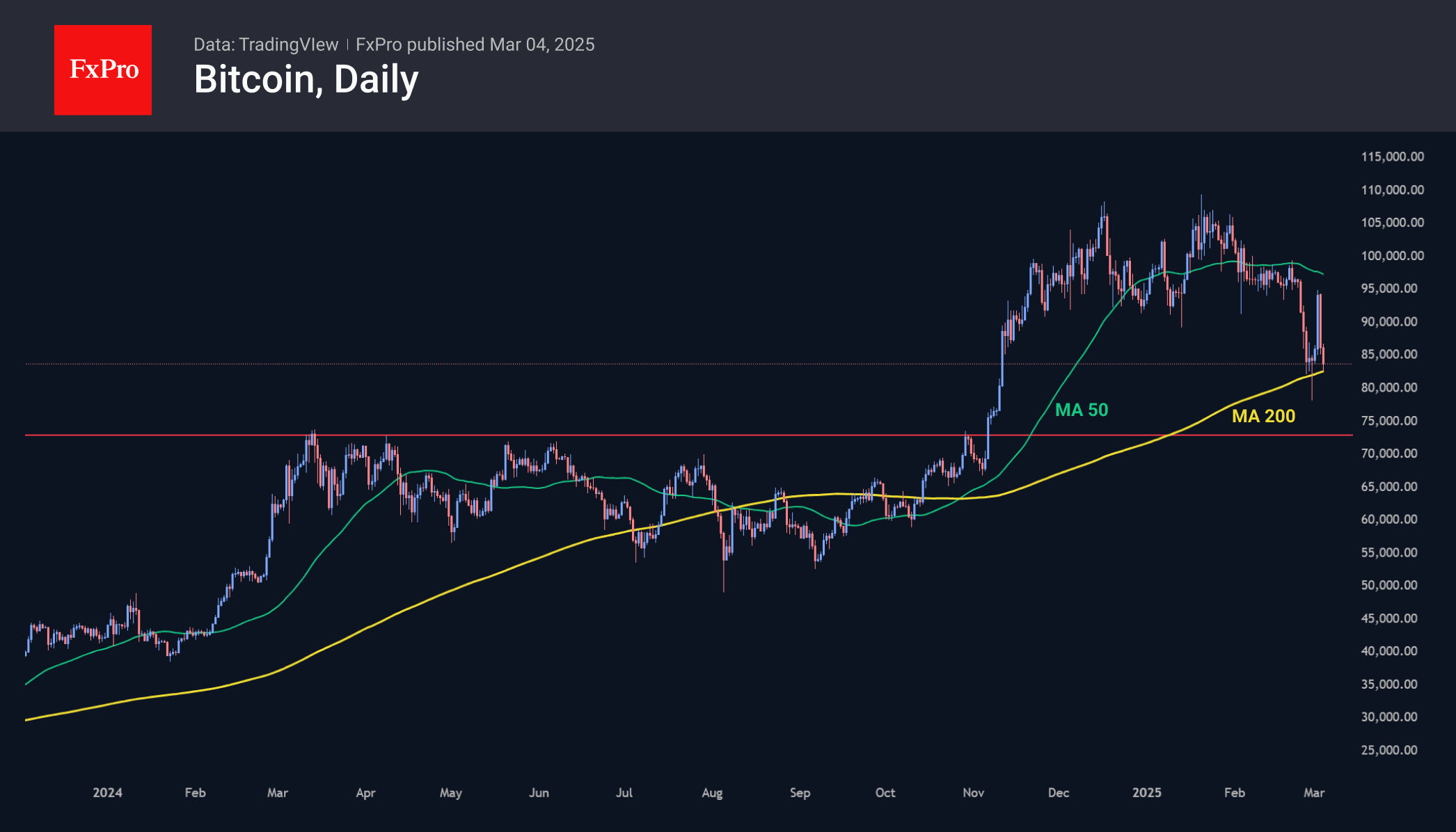

Crypto Could Not Hold Up

Market Picture

Pressure in traditional markets has clipped the wings of the crypto market, which is almost back to the point from which Sunday’s rally started. At the start of the day on Tuesday, it was capitalised at $2.76 trillion, having lost over 9% in the last 24 hours. The market fell under the 200-day average on increased momentum, and an attempt to rebound failed even with the help of cryptocurrency news.

Sentiment in the cryptocurrency market has returned to extreme fear territory, to the 15 level – the second lowest level after 27 February in more than two and a half years.

Bitcoin has lost 9.5% over the past 24 hours to levels below $83.3K. It continues to flounder between the 50- and 200-day moving averages but is dangerously assessing the latter this week. A failure below formally triggers a bearish scenario, with the potential next stop in the $70-72K area. That said, it is clear how uncomfortable this decline is for the current administration, and it may go for new industry proposals to support sentiment.

News Background

According to CoinShares, global crypto fund investments fell by a record $2.911 billion last week. Bitcoin investments were down by $2.598 billion, Ethereum by $300 million, and Solana by $7 million. Sui investments were up by $16 million, and XRP by $5 million.

CoinShares suggests that several factors, including the recent Bybit hack and the preceding 19-week streak of $29bn, influenced this trend. These factors have led to profit-taking and weakened sentiment towards this asset class.

Mint Ventures draws attention to the significant sponsorship that the companies behind XRP, SOL and ADA gave Trump before and after the election. However, this absurd approach could further reduce the likelihood of a relevant bill being passed at the federal level.

Bitcoin is not suitable for inclusion in government reserves because cryptocurrencies lack stability, liquidity and security, Swiss National Bank Governor Martin Schlegel said.

A US court dismissed the SEC’s lawsuit against Richard Hart, founder of HEX, PulseChain, and PulseX. The regulator accused Hart of raising more than $1bn through unregistered cryptocurrency offerings through the HEX, PulseChain, and PulseX projects.

Eurozone unemployment rate unchanged at 6.2% in Jan

Eurozone unemployment rate was unchanged at 6.2% in January, coming in better than expectations of 6.3%. Across the broader EU, unemployment rate also held firm at 5.8%.

According to Eurostat, the number of unemployed individuals stood at 12.824 million in the EU, of which 10.655 million were in the Eurozone.

On a monthly basis, Eurozone unemployment fell by -42k, while the overall EU saw a more modest decline of -8k.

Brent Crude Price Breaks Key Support Level

Today, Brent crude is sliding towards the psychological $70 per barrel mark, with the XBR/USD chart showing a break below a key support level (marked in blue) that had been holding since autumn last year.

Why Is Brent Crude Falling?

The bearish sentiment in the market is driven by OPEC+’s decision to increase oil production, contrary to analysts’ expectations that existing output cuts—designed to support prices—would remain in place.

According to the Wall Street Journal, analysts now predict:

→ Oil production will rise by 137,000 barrels per day from April 2025 to September 2026.

→ Brent crude may drop below $70 per barrel.

Technical Analysis of XBR/USD

From a long-term perspective, Brent crude is forming a descending channel (marked in red), connecting the April and July 2024 peaks. The break below this support level could signal a renewed downtrend following a prolonged period of consolidation.

If XBR/USD sees a short-term recovery from its yearly lows, key resistance levels to watch include:

→ The midline of the descending channel.

→ The former support level (marked in blue).

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.