Sample Category Title

CADJPY Plunges But Stochastic Indicates Bullish Correction

CADJPY has been plunging in the past three weeks, breaking below the 85.45 key level during the previous sessions. The aggressive sell-off drove the pair below the 20 and 40 simple moving averages in the daily timeframe, while the short-term indicators seem in confusion. It is worth mentioning that the pair recorded a fresh 8-month low of 83.82 last Thursday.

Turning our attention to the technical structure, the stochastic oscillator is creating a positive divergence with the price. The oscillator is moving higher at the same time where the price is moving lower, suggesting that a bullish correction is possible in the near-term. Moreover, the MACD oscillator is flattening in the negative territory, near its trigger line, signaling a neutral trend.

Further losses should see the June low of 83.20 acting as a major support. A drop below the aforementioned level would reinforce the bearish structure in the medium-term and open the way towards the next key support of 80.85.

In the event of an upside reversal, the 85.45 could act as a resistance barrier. A break above this level could shift the short-term outlook to neutral one as it could take the pair above the 20-day SMA. Further gains would lead the way towards the 86.70 level.

Fed Powell at His First Testimony, Markets Yawn

Dollar strengthens on Fed chair Jerome Powell's prepared remarks for his first Congressional testimony. But the movements in the markets are slight. The markets are generally staying in consolidation mode. Indeed, Powell offered nothing new comparing to the Fed's Monetary Policy Report released last week. Elsewhere, the Swiss Franc is trading as the strongest today while commodity currencies and Sterling are soft. Overall, the currency markets are quiet.

Fed Powell: To strike a balance in gauging monetary policy path

In his prepared speech to Congress, Powell said that "in gauging the appropriate path for monetary policy over the next few years, the FOMC will continue to strike a balance between avoiding an overheated economy and bringing PCE price inflation to 2% on a sustained basis." He added that "the FOMC views the near-term risks to the economic outlook as roughly balanced but will continue to monitor inflation developments closely,"

Regarding the economy, "while many factors shape the economic outlook, some of the headwinds the U.S. economy faced in previous years have turned into tailwinds." Also, "the robust job market should continue to support growth in household incomes and consumer spending, solid economic growth among our trading partners should lead to further gains in U.S. exports, and upbeat business sentiment and strong sales growth will likely continue to boost business investment."

Powell also down played recent financial market volatility and said "we do not see these developments as weighing heavily on the outlook for economic activity, the labor market and inflation,"

Released from US, trade deficit widened to USD -74.4b in January. Durable goods orders dropped sharply by -3.7% in January, ex-transport orders dropped -0.3%. Wholesale inventories rose 0.7% mom in January.

Bundesbank Weidmann: Asset purchase could end this year

Bundesbank President Jens Weidmann, a known hawk, said today that ECB "gradually and dependably reduce the degree of monetary policy accommodation when the outlook for price developments in the euro area permits us to do so." He added that "if the upswing continues and prices rise accordingly, in my view, there is no reason why the Governing Council should not end the net purchases of securities this year." He emphasized that policy normalization will "take a long time", and policy will "remain very expansive even after the end of net bond purchases." Weidmann's comments were very different from ECB President Mario Draghi's.

Draghi sounded cautious again in his comments yesterday. He warned that "given the uncertainty surrounding the measurement of economic slack, the true amount may be larger than estimated, which could slow down the emergence of price pressures." And therefore, the "right blend" of stimulus measures is still needed. Nonetheless, he said "these factors should wane as the economic expansion continues and unemployment further declines." "The relationship between growth and inflation remains largely intact, even if it has temporarily weakened in recent years to the extent that the speed of adjustment in inflation towards our aim has been affected." But he remained confident that " headline inflation will resume its gradual upward adjustment, supported by our monetary policy measures."

Eurozone business climate dropped to 1.48 in February, down from 1.54 but beat expectation of 1.47. Economic confidence dropped to 114.1, down from 114.7 and beat expectation of 114.0. Industrial confidence dropped to 8.0, down from 8.8, met expectations. Services confidence rose to 17.5, up from 16.7, beat expectation of 16.3. Consumer confidence was finalized at 0.1, unrevised. The confidence indicators remain at historically high level, despite a dip. Also from Eurozone, M3 rose 4.6% yoy in January. German CPI slowed to 1.4% yoy in February, down from 1.6% yoy, missed expected of 1.5% yoy.

EU to publish draft Brexit treaty

EU will publish their own draft of Brexit withdrawal treaty tomorrow. The 100-page document is set to ignore UK Prime Minister Theresa May's request to extend the transition period. That also comes just two days before May's scheduled high-profile speech on future trade relationship with EU. It's believed the EU's document will be solely from EU's perspective for the negotiation ahead. Meanwhile, it draws criticism from UK that EU is only trying to push its agenda, rather than producing something that reflects the positions of both sides.

Separately, French President Emmanuel Macron said that a customs union is "a possible option" for post Brexit relationship. But he emphasized that it's "not full access to the the single market". That's seen as a response to UK Labour leader Jeremy Corbyn's push for the customs union.

BoE Deputy Governor Sam Woods said today that the central bank was putting a "huge premium" on the government agreeing a Brexit transition deal with EU. And he urged that avoiding chaos in insurance markets due to Brexit is a "top priority" for the BoE. Also, he added that BoE will not "go soft" on enforcing EU capital rules for insurers. Woods also said that there was "no convincing evidence" to show that EU rules hurt profitability nor growth of the sector.

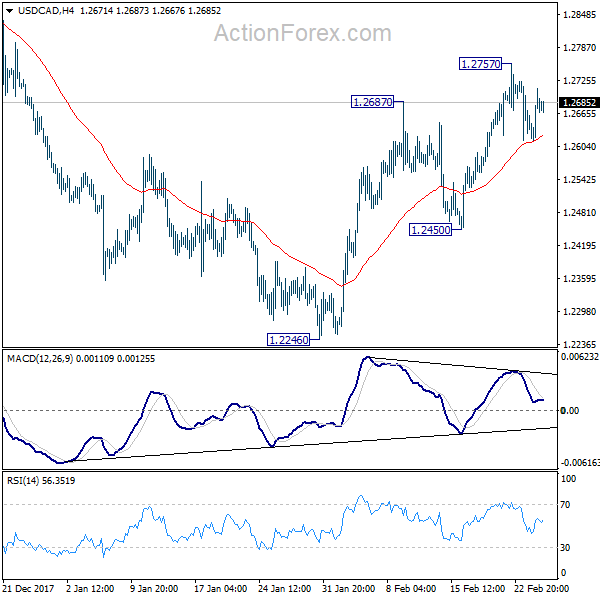

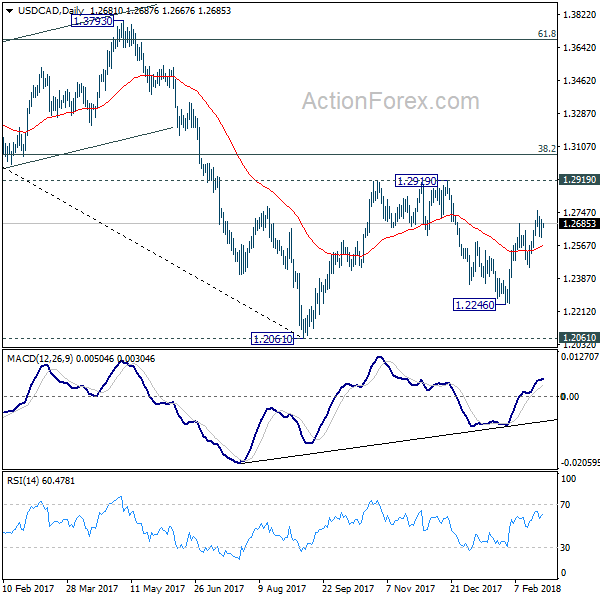

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2628; (P) 1.2670; (R1) 1.2725; More....

USD/CAD is staying in tight range below 1.2757 and intraday bias remains neutral first. On the upside, above 1.2757 will resume the rebound from 1.2246 and target a test on 1.2919 key resistance. We'd be cautious on strong resistance from there to limit upside. On the downside, below 1.2450 will turn bias back to the downside for 1.2246 support.

In the bigger picture, the rebound from 1.2246 is mixing up the medium term outlook. Nonetheless, USD/CAD is staying below falling 55 week EMA (now at 1.2771), hence, the bearish case is in favor. That is, fall from 1.4689 is not completed yet. Sustained break of 1.2061 key support will carry larger bearish implication and target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. However, firm break of 1.2919 will revive the case of medium term reversal and turn outlook bullish.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Jan | -566M | -2710M | 640M | 596M |

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Jan | 4.60% | 4.60% | 4.60% | |

| 10:00 | EUR | Eurozone Business Climate Indicator Feb | 1.48 | 1.47 | 1.54 | 1.56 |

| 10:00 | EUR | Eurozone Economic Confidence Feb | 114.1 | 114 | 114.7 | 114.9 |

| 10:00 | EUR | Eurozone Industrial Confidence Feb | 8 | 8 | 8.8 | 9 |

| 10:00 | EUR | Eurozone Services Confidence Feb | 17.5 | 16.3 | 16.7 | 16.8 |

| 10:00 | EUR | Eurozone Consumer Confidence Feb F | 0.1 | 0.1 | 0.1 | 1.4 |

| 13:00 | EUR | German CPI M/M Feb P | 0.50% | 0.50% | -0.70% | |

| 13:00 | EUR | German CPI Y/Y Feb P | 1.40% | 1.50% | 1.60% | |

| 13:30 | USD | Fed Powell's Congressional Testimony | ||||

| 13:30 | USD | Advance Goods Trade Balance Jan | -74.40B | -72.3B | -72.3B | |

| 13:30 | USD | Wholesale Inventories M/M Jan P | 0.70% | 0.30% | 0.40% | 0.60% |

| 13:30 | USD | Durable Goods Orders Jan P | -3.70% | -2.50% | 2.80% | |

| 13:30 | USD | Durable Goods Ex-Transport Jan P | -0.30% | 0.40% | 0.70% | |

| 14:00 | USD | House Price Index M/M Dec | 0.30% | 0.40% | 0.40% | 0.50% |

| 14:00 | USD | S&P/Case-Shiller Composite-20 Y/Y Dec | 6.30% | 6.30% | 6.40% | |

| 15:00 | USD | Consumer Confidence Index Feb | 126 | 125.4 |

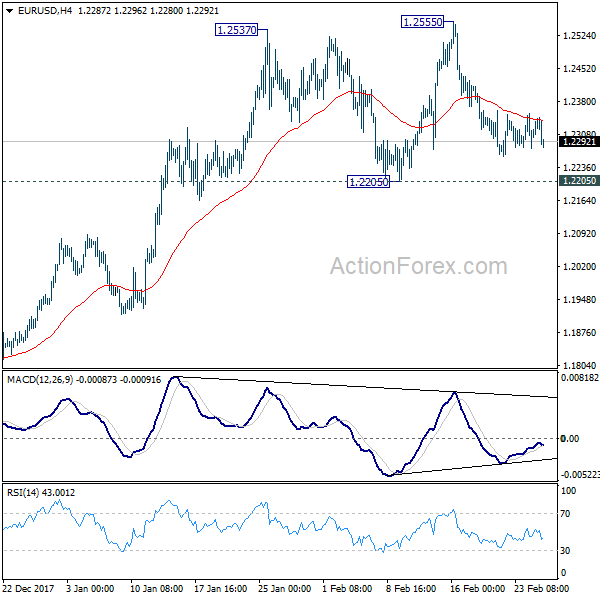

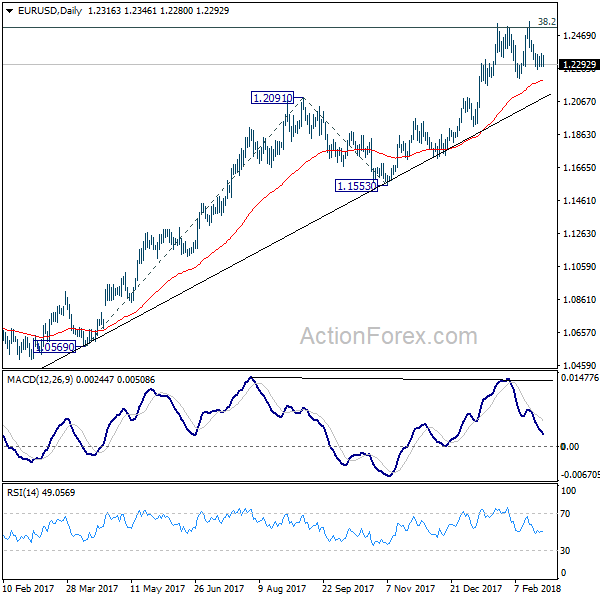

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2277; (P) 1.2316 (R1) 1.2355; More....

Intraday bias in EUR/USD remains neutral as it's still bounded in range of 1.2205/2555. On the upside, break of 1.2555 will revive the bullish case of up trend resumption and target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075. However, break of 1.2205 will confirm rejection by 1.2516 key fibonacci level and trend reversal.

In the bigger picture, key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 remains intact despite attempts to break. Hence, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

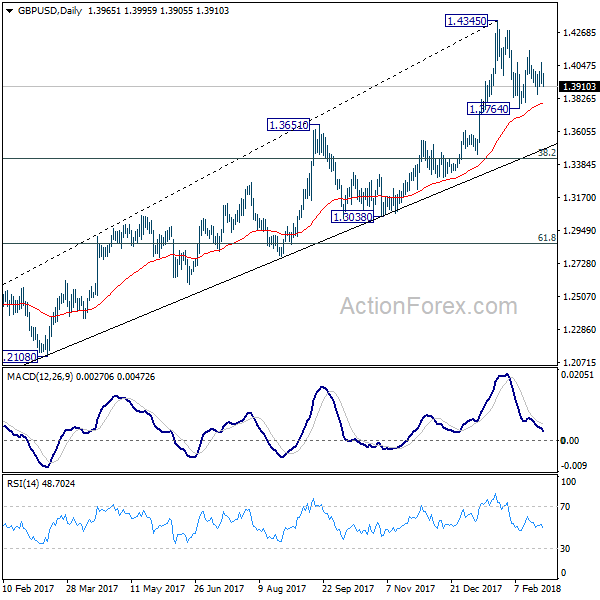

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3905; (P) 1.3988; (R1) 1.4048; More....

Intraday bias in GBP/USD remains neutral as it's bounded in range of 1.3764/4144. On the upside, break of 1.4144 will extend the rise from 1.3764 and target a test on 1.4345 resistance. Break there will resume larger up trend and target long term trend line resistance (now at 1.5056). On the downside, below 1.3764 will extend the correction from 1.4345 to 1.3651 resistance turned support instead.

In the bigger picture, as long as 1.3038 support holds, medium term outlook in GBP/USD will remains bullish. Rise from 1.1946 is at least correcting the long term down from 2007 high at 2.1161. Further rally would be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. However, GBP/USD fails to sustain above 55 month EMA (now at 1.4279) so far. Break of 1.3038 support, will suggests that rise from 1.1946 has completed and will turn outlook bearish for retesting this low.

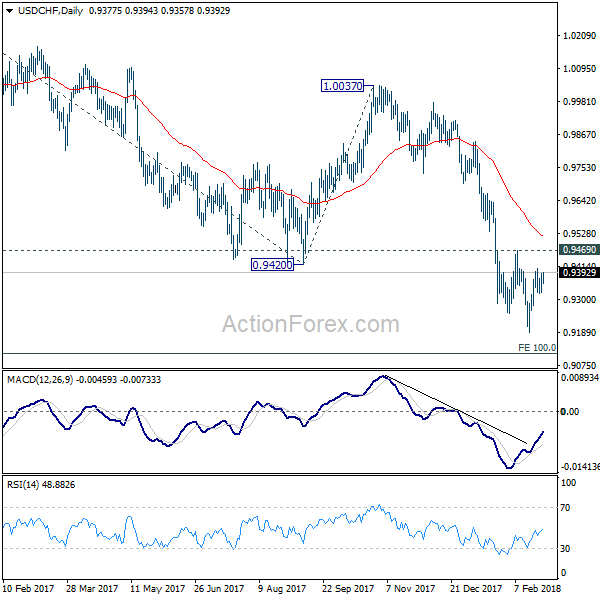

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9339; (P) 0.9365; (R1) 0.9405; More...

Intraday bias in USD/CHF remains neutral as consolidation from 0.9186 is extending. Also, outlook stays mildly bearish with 0.9469 resistance intact and another decline is in favor. On the downside, break of 0.9186 will extend the larger down trend to 0.9115 medium term projection level next. However, considering bullish convergence condition in 4 hour MACD, break of 0.9469 will indicate near term reversal and turn outlook bullish for 55 day EMA (now at 0.9517) and above.

In the bigger picture, fall from 1.0342 is seen as a medium term down trend. Deeper decline should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, sustained trading above 55 day EMA is needed to be the first sign of medium term reversal. Otherwise, outlook will stay bearish even in case of strong rebound.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 106.48; (P) 106.83; (R1) 107.28; More...

USD/JPY is still bounded in consolidation from 105.54 and intraday bias remains neutral for the moment. Also, with 108.27 resistance intact, outlook remains mildly bearish and deeper fall is expected. On the downside, break of 105.54 will extend the larger decline from 118.65 and target 100% projection of 118.65 to 108.12 from 114.73 at 104.20 next. However, break of 108.27 will be the first sign of near term reversal and will target 110.47 resistance for confirmation.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. The solid break of 61.8% retracement of 98.97 to 118.65 at 106.48 now suggests that the pattern from 125.85 high is possibly extending. Deeper fall could be seen through 98.97 key support (2016 low). This bearish case will now be favored as long as 110.47 resistance holds.

(FED) Chairman Jerome H. Powell – Semiannual Monetary Policy Report to the Congress

Chairman Hensarling, Ranking Member Waters, and members of the Committee, I am pleased to present the Federal Reserve's semiannual Monetary Policy Report to the Congress.

On the occasion of my first appearance before this Committee as Chairman of the Federal Reserve, I want to express my appreciation for my predecessor, Chair Janet Yellen, and her important contributions. During her term as Chair, the economy continued to strengthen and Federal Reserve policymakers began to normalize both the level of interest rates and the size of the balance sheet. Together, Chair Yellen and I have worked to ensure a smooth leadership transition and provide for continuity in monetary policy. I also want to express my appreciation for my colleagues on the Federal Open Market Committee (FOMC). Finally, I want to affirm my continued support for the objectives assigned to us by the Congress--maximum employment and price stability--and for transparency about the Federal Reserve's policies and programs. Transparency is the foundation for our accountability, and I am committed to clearly explaining what we are doing and why we are doing it. Today I will briefly discuss the current economic situation and outlook before turning to monetary policy.

Current Economic Situation and Outlook

The U.S. economy grew at a solid pace over the second half of 2017 and into this year. Monthly job gains averaged 179,000 from July through December, and payrolls rose an additional 200,000 in January. This pace of job growth was sufficient to push the unemployment rate down to 4.1 percent, about 3/4 percentage point lower than a year earlier and the lowest level since December 2000. In addition, the labor force participation rate remained roughly unchanged, on net, as it has for the past several years--that is a sign of job market strength, given that retiring baby boomers are putting downward pressure on the participation rate. Strong job gains in recent years have led to widespread reductions in unemployment across the income spectrum and for all major demographic groups. For example, the unemployment rate for adults without a high school education has fallen from about 15 percent in 2009 to 5-1/2 percent in January of this year, while the jobless rate for those with a college degree has moved down from 5 percent to 2 percent over the same period. In addition, unemployment rates for African Americans and Hispanics are now at or below rates seen before the recession, although they are still significantly above the rate for whites. Wages have continued to grow moderately, with a modest acceleration in some measures, although the extent of the pickup likely has been damped in part by the weak pace of productivity growth in recent years.

Turning from the labor market to production, inflation-adjusted gross domestic product rose at an annual rate of about 3 percent in the second half of 2017, 1 percentage point faster than its pace in the first half of the year. Economic growth in the second half was led by solid gains in consumer spending, supported by rising household incomes and wealth, and upbeat sentiment. In addition, growth in business investment stepped up sharply last year, which should support higher productivity growth in time. The housing market has continued to improve slowly. Economic activity abroad also has been solid in recent quarters, and the associated strengthening in the demand for U.S. exports has provided considerable support to our manufacturing industry.

Against this backdrop of solid growth and a strong labor market, inflation has been low and stable. In fact, inflation has continued to run below the 2 percent rate that the FOMC judges to be most consistent over the longer run with our congressional mandate. Overall consumer prices, as measured by the price index for personal consumption expenditures (PCE), increased 1.7 percent in the 12 months ending in December, about the same as in 2016. The core PCE price index, which excludes the prices of energy and food items and is a better indicator of future inflation, rose 1.5 percent over the same period, somewhat less than in the previous year. We continue to view some of the shortfall in inflation last year as likely reflecting transitory influences that we do not expect will repeat; consistent with this view, the monthly readings were a little higher toward the end of the year than in earlier months.

After easing substantially during 2017, financial conditions in the United States have reversed some of that easing. At this point, we do not see these developments as weighing heavily on the outlook for economic activity, the labor market, and inflation. Indeed, the economic outlook remains strong. The robust job market should continue to support growth in household incomes and consumer spending, solid economic growth among our trading partners should lead to further gains in U.S. exports, and upbeat business sentiment and strong sales growth will likely continue to boost business investment. Moreover, fiscal policy is becoming more stimulative. In this environment, we anticipate that inflation on a 12-month basis will move up this year and stabilize around the FOMC's 2 percent objective over the medium term. Wages should increase at a faster pace as well. The Committee views the near-term risks to the economic outlook as roughly balanced but will continue to monitor inflation developments closely.

Monetary Policy

I will now turn to monetary policy. The Congress has assigned us the goals of promoting maximum employment and stable prices. Over the second half of 2017, the FOMC continued to gradually reduce monetary policy accommodation. Specifically, we raised the target range for the federal funds rate by 1/4 percentage point at our December meeting, bringing the target to a range of 1-1/4 to 1-1/2 percent. In addition, in October we initiated a balance sheet normalization program to gradually reduce the Federal Reserve's securities holdings. That program has been proceeding smoothly. These interest rate and balance sheet actions reflect the Committee's view that gradually reducing monetary policy accommodation will sustain a strong labor market while fostering a return of inflation to 2 percent.

In gauging the appropriate path for monetary policy over the next few years, the FOMC will continue to strike a balance between avoiding an overheated economy and bringing PCE price inflation to 2 percent on a sustained basis. While many factors shape the economic outlook, some of the headwinds the U.S. economy faced in previous years have turned into tailwinds: In particular, fiscal policy has become more stimulative and foreign demand for U.S. exports is on a firmer trajectory. Despite the recent volatility, financial conditions remain accommodative. At the same time, inflation remains below our 2 percent longer-run objective. In the FOMC's view, further gradual increases in the federal funds rate will best promote attainment of both of our objectives. As always, the path of monetary policy will depend on the economic outlook as informed by incoming data.

In evaluating the stance of monetary policy, the FOMC routinely consults monetary policy rules that connect prescriptions for the policy rate with variables associated with our mandated objectives. Personally, I find these rule prescriptions helpful. Careful judgments are required about the measurement of the variables used, as well as about the implications of the many issues these rules do not take into account. I would like to note that this Monetary Policy Report provides further discussion of monetary policy rules and their role in the Federal Reserve's policy process, extending the analysis we introduced in July.

Thank you. I would be pleased to take your questions.

Canadian Dollar Steady Ahead of Canadian Budget and Powell Testimony

The Canadian dollar has recorded small gains in the Tuesday session. Currently, USD/CAD is trading at 1.2703, up 0.13% on the day. On the release front, the sole Canadian event is the annual budget. In the US, it's a busy day. Core Durable Goods Orders are forecast to dip to 0.4%, and Durable Goods Orders are expected to decline 2.4%. Another key release is CB Consumer Confidence, which is expected to climb to 126.2 points. As well, Jerome Powell will testify before a congressional committee.

It's budget day for Ottawa, and the markets are not expecting any bombshells from finance minister Bill Morneau. In October, the Trudeau government revised downwards the deficit for the 2017-2018 fiscal year to C$19.9 billion. The Canadian economy was steady in the fourth quarter, so the deficit could be even lower. The budget is not expected to show any major spending, so it's likely that the release will not shake up the Canadian dollar. The Canadian currency lost ground last week, and touched its lowest level since late December.

All eyes are on Federal Reserve Chair Jerome Powell, who took over from Janet Yellen earlier this month. Powell will testify before the House Financial Services Committee, his first major appearance as head of the central bank. Powell received a rude welcome from the markets just after moving into his new office, as the global stock market correction erased some $4 trillion in valuations. The volatility forced Powell to make a public statement, reassuring the markets that the Fed was closely monitoring the situation.

How will the US dollar react to Powell's testimony before the House Finance Services Committee? After the recent turmoil in the stock markets, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.

Major Pairs Cautious ahead of Powell’s Key Testimony; European Equities Head Lowe

Here are the latest developments in global markets:

FOREX: Major currencies were trading flat during early European afternoon as investors were waiting for the new Fed chair, Jerome Powell, to make his first major appearance before the US Congress later today. Market watchers were cautious as any language twinkles could spur noise not only in forex markets but also in bond and stock markets as well. The dollar index which gauges the dollar's strength against a basket of major currencies was last seen at 89.81 (-0.04%), while dollar/yen stood a shy below 107 key level (+0.04%). Euro/dollar gave up some gains despite Eurozone's consumer and business composite survey delivering slightly better results in February than forecasted as concerns linked to political conditions in Italy and Germany loomed in the background. Pound/dollar changed hands at 1.3961( -0.02%), pressured by uncertainties around the future EU-UK trade relations, while trade issues were also weighing on the Canadian dollar as NAFTA talks which hold the seventh round of negotiations this week have so far led nowhere. Aussie/dollar was trading weak at 0.7840 (-0.18%), while kiwi/dollar was the worst performer, extending losses towards 0.7277 (-0.33%). The Swedish krona tumbled versus the greenback after the Swedish central bank said that weak inflation developments are a concern and any adjustments in inflation readings the upcoming months would be crucial to determine any change in the central bank's plans to start raising interest rates. Note that forecasts are for the first rate hikes to come in the second half of the year. Dollar/ Swedish krona surged to a fresh one-month high of 8.1895 (+0.48%).

STOCKS: European stocks were heading lower in early European trading. The pan-European STOXX 600 was down by 0.14% at 1100 GMT as gains in financials and consumer cyclicals were unable to offset losses in telecommunications. The blue-chip Euro STOXX retreated by 0.29%. The Spanish IBEX 35 and the French CAC 40 fell by 0.10%, while the German DAX 30 was down by 0.18%. The British FTSE 100 and the Italian FTSE MIB were steady. US future stocks were in the green, pointing to a positive open.

COMMODITIES: Oil prices stretched lower on fears that the US production could hamper OPEC's efforts to curb global supply. On Tuesday, the International Energy Agency Executive director Fatih Birol said that the US would likely overtake Russia as the world's biggest crude oil producer "definitely next year". WTI crude lost 0.41% on the day to drop to $63.65/barrel, while Brent declined by 0.19% to $67.37/barrel. Gold was steady at $1332.60/ounce.

Day Ahead: Fed new Chief Jerome Powell testimony takes the stage; durable goods & consumer confidence pending in US

The calendar will be busy in terms of economic data for the remainder of the day, however, the focus would turn to Jerome Powell and his first major speech before the House Financial Market Committee as a head of the Federal Reserve where he will address the Fed's semi-annual monetary report.

In times of stock market volatility, Powell who will testify on behalf of the FOMC committee at 1500 GMT (the prepared statements will be published at 1330 GMT) is expected to emphasize the bullish outlook of the economy as expressed at January's FOMC meeting minutes, but probably he will avoid any reference on how fast should interest rates rise in order to keep markets calm, deterring another round of turbulence in equity markets.

Meanwhile, the former Fed Governor, Janet Yellen, will be interviewed by her predecessor, Ben Bernanke at the Brookings institution, discussing her career, the current state of the economy and the challenges the US economy faces.

Data on durable goods for the month of January will also attract attention at 1330 GMT, with analysts expecting the headline and the core measures to slow down on a monthly basis. At 1400 GMT, the CaseShiller indices gauging house prices during the month of December will be made public, while data on consumer confidence for the month of February will be released at 1500 GMT. The consumer confidence index is expected to rise to 126.6, coming closer to November's 18-year high of 128.6.

In Eurozone, Germany will deliver flash estimates on consumer prices for the month of February at 1300 GMT. Forecasts are for the headline CPI to inch down to 1.5% y/y, however, in monthly terms, the index is projected to jump by 0.5% after experiencing the biggest drop of 0.7% in almost two years. In Sweden, Fellow Riksbank Deputy Governor Henry Ohlsson will be discussing the Swedish central bank's tasks and his view of Swedish and international economic developments at 1700 GMT.

Oil traders will be paying attention to the API's weekly data on crude stocks due at 2130 GMT.

In equities, corporations continue to release quarterly earnings reports, though the markets' focus is expected to be on what Powell has to say later on Tuesday.

Brexit developments are also gathering attention as UK PM Theresa May prepares to deliver a speech on the nation's relationship with the EU after Brexit later in the week. In politics, NAFTA negotiations, which have entered their seventh and final round, will also be attracting interest.

DAX Under Pressure, Investors Eye German CPI

The DAX index is down considerably in the Tuesday session. Currently, the index is trading at 12,478.50 down 0.38% since the Monday close. On the release front, German Preliminary CPI is expected to rebound with a gain of 0.5%. In the US, Jerome Powell will testify before a congressional committee.

German president Angela Merkel received an overwhelming vote of confidence from her conservative CDU party on Monday. Delegates voted to in favor of the coalition with the socialist SPD party. Merkel's party did poorly in the September election, and has paid the price, as the SPD will receive the financial and foreign affairs posts in the new government. This will allow the SPD to set a more liberal policy regarding Germany's role in the eurozone, and that could mean a shift away from its conservative and rigorous stance towards budgetary issues, such as support for weaker members of the eurozone. The coalition agreement must still be approved by SPD members, who will vote on the measure on March 4.

All eyes are on Federal Reserve Chair Jerome Powell, who took over from Janet Yellen earlier this month. Powell will testify before the House Financial Services Committee, his first major appearance as head of the central bank. Powell received a rude welcome from the markets just after moving into his new office, as the global stock market correction erased some $4 trillion in valuations. The volatility forced Powell to make a public statement, reassuring the markets that the Fed was closely monitoring the situation.

How will the dollar react to Powell's testimony before the House Banking Committee? After the recent turmoil in the stock markets, Powell may opt to play it safe and keep away from any splashy headlines, which could lead to more fluctuation in the markets. Powell could choose to focus on the strong US economy and the Fed trimming its balance sheet, and steer away from a discussion of accelerating rate policy in order to head off higher inflation.