Sample Category Title

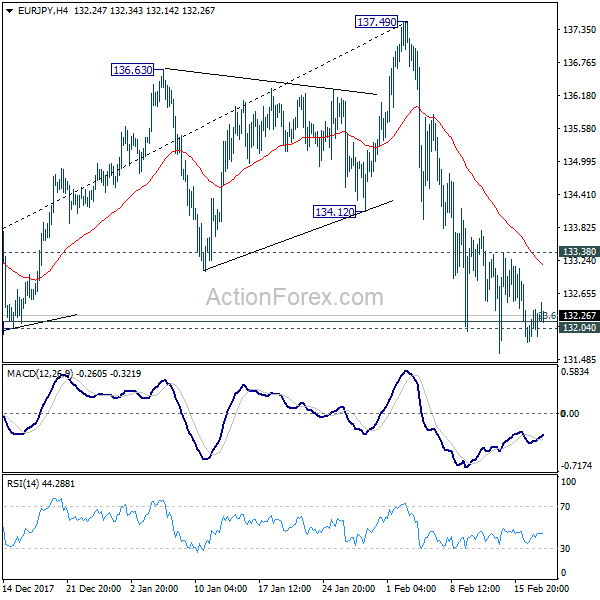

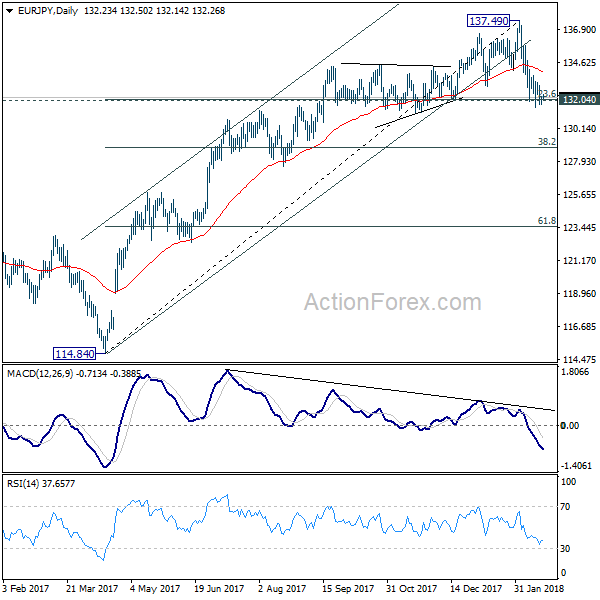

EUR/JPY Daily Outlook

Daily Pivots: (S1) 131.89; (P) 132.13; (R1) 132.46; More....

Near term outlook remains bearish with 133.38 resistance intact. Sustained trading below 132.04 cluster support (23.6% retracement of 114.84 to 137.49 at 132.14) will indicate larger trend reversal on bearish divergence condition in daily MACD. In such case, deeper decline would be seen for 38.2% retracement at 128.38 first. However, rebound from 132.04 will retain near term bullishness. Break of 133.38 minor resistance will turn bias back to the upside for 137.49 again.

In the bigger picture, bearish divergence condition in weekly MACD indicates loss of medium term upside momentum. Sustained break of 132.04 will be the early sign of long term reversal and should bring deeper fall back to retest 124.08 key support level. Meanwhile, break of 137.49 will resume the up trend from 109.03 to 141.04/149.76 resistance zone.

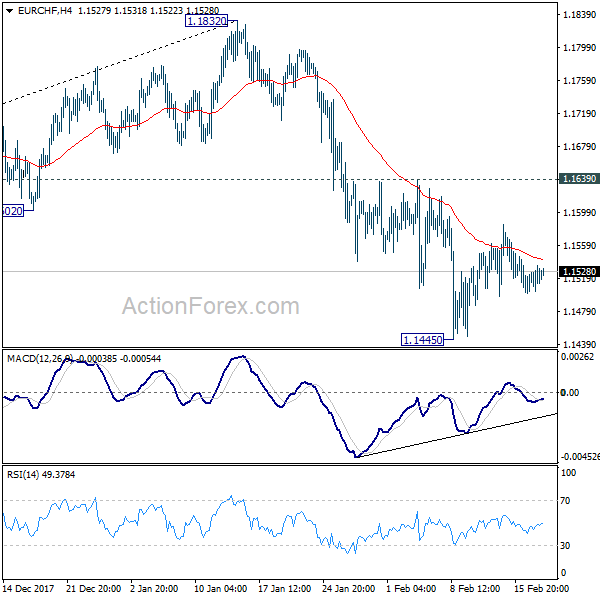

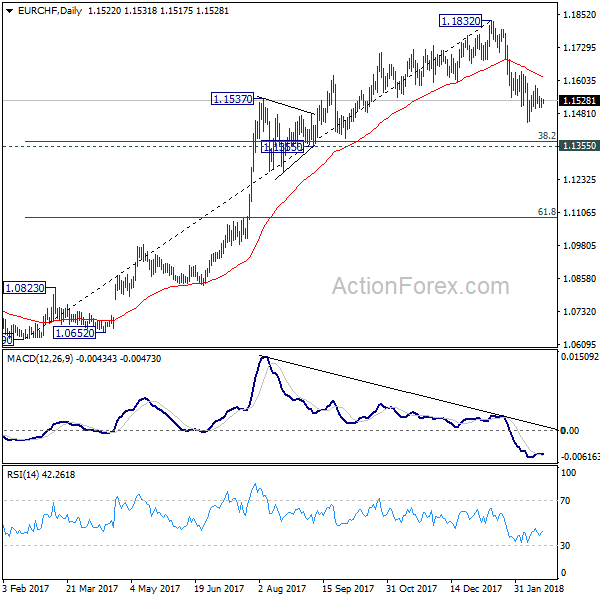

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1506; (P) 1.1520; (R1) 1.1538; More...

Consolidation from 1.1445 is still in progress and intraday bias remains neutral. Also, with 1.1639 resistance intact, near term outlook remains bearish. Break of 1.1445 will resume the corrective fall from 1.1832 and target 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) At this point, we'd expect strong support from there to contain downside and bring rebound.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

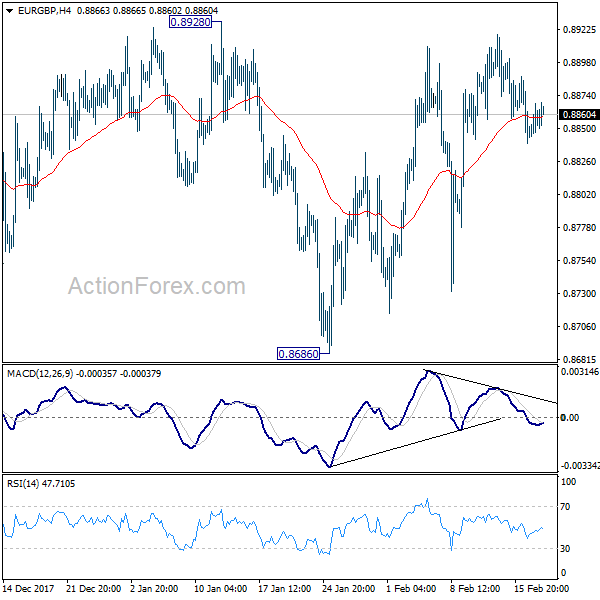

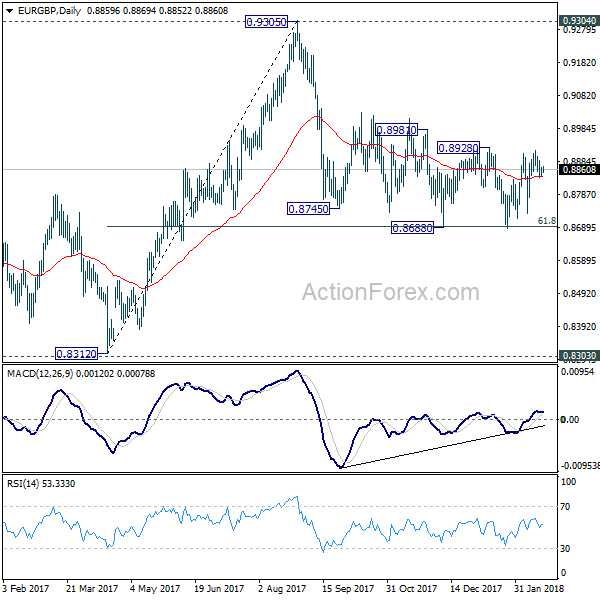

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8847; (P) 0.8858; (R1) 0.8872; More...

No change in EUR/GBP's outlook as range trading continues inside 0.8686/8928. Intraday bias remains neutral and deeper fall is mildly in favor with 0.8928 resistance intact. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too, deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

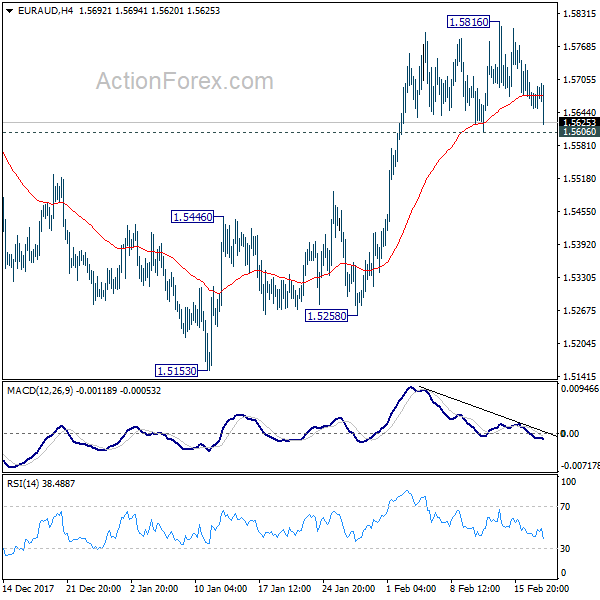

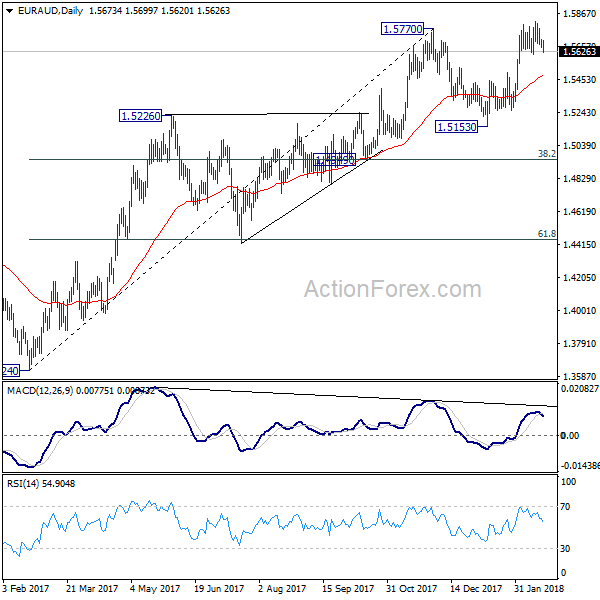

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5653; (P) 1.5675; (R1) 1.5700; More....

EUR/AUD weakens notably today but stays above 1.5606 so far. Intraday bias stays neutral first with focus back on 1.5606. Firm break of 1.5606 will argue that a short term top is formed. Intraday bias will be turned back to the downside for 55 day EMA (now at 1.5476) and below. Nonetheless, break of 1.5816 should now confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Sustained break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

Aussie Showing Some Strength after Neutral RBA Minutes, Dollar Mildly Higher

Dollar trades mildly higher today as risk markets are back on the defensive side. Yen is trading as the weakest one so far even though Nikkei is down -0.9% at the time of writing. Swiss Franc and Kiwi follows closely. Notable strength is seen in Aussie after RBA minutes showed neutral stance. Major forex pairs are crosses are generally stuck in range. Nonetheless, the dip in EUR/AUD is seen as a early sign of near term reversal and will be closely watched.

RBA cautiously neutral

RBA minutes showed that policymakers are maintaining the cautiously neutral stance. The low interest rate is helping to bring down unemployment rate and keep inflation inside target band. But it echoed recent comments from officials that "further progress on these goals was expected over the period ahead but the increase in inflation was likely to occur only gradually as the economy strengthened." The minutes also warned that "there was still a risk that growth in consumption might turn out to be weaker than forecast if household income growth were to increase by less than expected." It's generally expected that RBA will be on hold throughout 2018. But views on whether it will hike in early 2019 are divided.

BoJ to continue virtual normalization

Former BoJ board member Takahide Kiuchi said a "de-facto normalization" of monetary is already taking place with the central bank. And, the reappointment of Haruhiko Kuroda as Governor, and Executive Director Masayoshi Amamiya as the next deputy, showed the governments wants "continuity". Therefore, under the new board, BoJ will continue with such "virtual normalization". Meanwhile, Kiuchi said the reappointment of Kuroda shows Prime Minister Shinzo Abe is more focused on maintaining market stability and sustaining growth, rather than achieving the inflation target.

SPD members to vote on grand coalition

In Germany, over 450k members of the Social Democratic party will start voting on reforming the grand coalition with Chancellor Angela Merkel's Christian Democratic Union. They will have until March 2 to submit their votes. Result is expected to be announced on March 4. SPD leader Andrea Nahles said in an interview that there will be an "intense debate". She also said earlier that there is no "Plan B" if the notion is voted down by SPD members. And a new election could be the ultimate outcome should that happens. Newspaper Bild am Sonntag polled the mayors of the 35 biggest towns and cities ruled by the SPD. 26 of them said they back the notion. So far, the vote is wide open.

Elsewhere

New Zealand PPI input rose 0.9% qoq in Q4, PPI output rose 1.0% qoq. German PPI, ZEW will be the main focus in European session. Swiss will release trade balance while UK will release CBI trends total orders. Eurozone will also release consumer confidence. Canada wholesale sales will be featured.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5653; (P) 1.5675; (R1) 1.5700; More....

EUR/AUD weakens notably today but stays above 1.5606 so far. Intraday bias stays neutral first with focus back on 1.5606. Firm break of 1.5606 will argue that a short term top is formed. Intraday bias will be turned back to the downside for 55 day EMA (now at 1.5476) and below. Nonetheless, break of 1.5816 should now confirm resumption of medium term rise from 1.3264. In that case, EUR/AUD should target 1.6587 key long term resistance.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Sustained break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | PPI Input Q/Q Q4 | 0.90% | 0.30% | 1.00% | 1.10% |

| 21:45 | NZD | PPI Output Q/Q Q4 | 1.00% | 0.40% | 1.00% | |

| 0:30 | AUD | RBA February Meeting Minutes | ||||

| 7:00 | EUR | German PPI M/M Jan | 0.50% | 0.20% | ||

| 7:00 | EUR | German PPI Y/Y Jan | 1.80% | 2.30% | ||

| 7:00 | CHF | Trade Balance (CHF) Jan | 2.78B | 2.63B | ||

| 10:00 | EUR | German ZEW Economic Sentiment Feb | 16 | 20.4 | ||

| 10:00 | EUR | German ZEW Current Situation Feb | 94 | 95.2 | ||

| 10:00 | EUR | Eurozone ZEW Economic Sentiment Feb | 28.4 | 31.8 | ||

| 11:00 | GBP | CBI Trends Total Orders Feb | 11 | 14 | ||

| 13:30 | CAD | Wholesale Trade Sales M/M Dec | 0.40% | 0.70% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Feb A | 1 | 1.3 |

EUR/JPY Decline Looks Real, Can 131.50 Hold Losses?

Key Highlights

- The Euro traded lower recently and declined below 133.00 against the US Japanese Yen.

- There is a significant declining channel forming with resistance at 132.60 on the 4-hours chart of EUR/JPY.

- The Euro Area Construction Output increased 0.1% (seasonally adjusted) in Dec 2017, better than the forecast of -0.7% (MoM).

- Today, the German PPI report for Jan 2018 will be released, which is forecasted to increase by 0.3% (MoM), more than the last 0.2%.

EURJPY Technical Analysis

The Euro remained in a bearish bias during the past few days against the Japanese Yen. The EUR/JPY pair declined and it remains at a risk or more losses, with resistances on the upside at 132.60 and 133.00.

Looking at the 4-hours chart of EUR/JPY, there is a clear bearish trend in place. There was a break below a major support at 134.15, which opened the doors for more declines and the pair fell by more than 200 pips.

The recent low formed was 131.60 from where the pair started an upward correction. However, the upside wave faced sellers near 133.20-40. The pair is currently under pressure and is trading well below 133.00.

The pair remains in a downtrend as long as it is following a significant declining channel forming with resistance at 132.60. On the downside, supports are at 131.80 and 131.60. Below the stated 131.60, the pair could decline sharply towards 131.00.

Euro Area Construction Output

Recently in the Euro Area, the Construction Output figures for Dec 2017 were released by the Eurostat. The market was looking for a decline in the output by 0.7% compared with the previous month.

However, the actual result was better as there was a rise of 0.1% in the Construction Output (seasonally adjusted). Looking at the yearly change, there was a growth of 0.5% in the production, which was less than the forecast of +2.7%. The report added:

The average production in construction for the year 2017, compared with 2016, increased by 2.4% in the euro area and by 3.5% in the EU28. The increase of 0.1% in production in construction in the euro area in December 2017, compared with November 2017, is due to building construction rising by 0.5%, while civil engineering fell by 1.1%.

Overall, the Euro remains at a risk of more declines versus the Japanese Yen as long as it is below 133.00. On the other hand, EUR/USD may correct higher above 1.2450 in the near term.

Market Morning Briefing: The Dollar-Yen Saw A Low Of 105.55

STOCKS

Dow (25219.38,+0.08%) could move up towards 26000-26500 on a break above interim resistance near 25500. Medium term looks bullish.

Dax (12385.60, -0.53%) has resistance near 12600 and while the index trades below 12600, near to medium term looks bearish. Trade within 12600-12300 region looks likely in the near term.

Nikkei (21884.21, -1.20%) is down slightly after trying to move up yesterday. A break above 22200-22400 could take it higher towards 22800 levels else a fall back to 21400 or lower is possible in the coming sessions.

The resistance near 10680 on Nifty (10378.40, -1.58%) seems to be holding well. Currently trading near the 10260-10320 support region, if the index fails to bounce back immediately, it could be vulnerable to a further fall towards 10080 in the next few sessions. Else a bounce, if seen could take it higher towards 10680 levels again.

It would be important to see if Sensex (33774.66, -1.52%) breaks below 33500 in the coming sessions or attempts a bounce back towards 35000 or higher.

COMMODITIES

Overall the metals are trading lower today while the crude prices have inched up a bit.

WTI (62.17) may test decent resistance near current levels and could possible again come off towards 62-61 in the next few sessions, A break above 63 if seen would turn bullish for the medium term.

Brent (65.38) on the other hand needs to move above 66 to rise further in the near term. Else a pause near current levels could keep prices stable for now.

Gold (1343.50) saw a rejection from 1365-1367 levels and while that holds, a test of lower levels of 1340-1330 looks likely. Near term looks bearish.

Copper (3.1950) has come off from just below important resistance near 3.30 as seen on the 3-day charts. The price may head towards 3.15- 3.10 in the near term. Near term looks bearish.

FOREX

Support near 88.5 on daily candles has held well for the Dollar Index (89.33) and it is now seeing a bounce towards 90. It should test important resistance just above 90 on the weekly candles this week (daily candles also show resistance near 90).

As per expectations, Euro (1.2385) didn’t rise beyond 1.2556 (close to its previous high at 1.2537) and is now coming off towards support near 1.235 on the daily candles, which it might test in the next couple of sessions. Lower support is seen near 1.23 on the weekly candles, which could be tested later this week.

The Dollar-Yen (106.72) saw a low of 105.55 (support on daily candles – earlier mentioned as 106) from where it is now bouncing. Its next target could be 107.0-107.5 which is seen as resistance on the daily and 3 day candles.

The Euro-Yen (132.17) is again testing crucial support near 132 on the 3 day candles. For the Euro Yen to break this crucial support, the Euro should test 1.23 later this week while the Dollar Yen stays below 107.5, which is a possibility.

Pound (1.3975), as per our expectation, is dipping from resistance on 3 day candles and 3 day line chart near 1.42-1.43 and might now test immediate support near 1.39 on the daily candles soon. Test of lower support near 1.38 on daily and 3 day candles is also likely this week.

Dollar-Rupee (64.215) may see 64.30-35 this week and maybe higher by the end of the month.

INTEREST RATES

US 10 Year Yield (2.8968), US 30 year Yield (3.1431), US 5 year yield (2.6582), US 2 year yield (2.222) : The 2 Year Yield is slightly above our earlier mentioned long term resistance level near 2.2%. It will be important to see if it goes up further since a further upmove could pull up the other yields beyond their long term resistances as well. However, our preference still remains for a dip in the 2 year yield in the next couple of days below 2.2%.

(Long term resistance levels for the 4 yields earlier mentioned are as follows: 2.85-2.90, 3.20, 2.7 and 2.2 respectively - we have been expecting these levels to hold in this month.)

The 10-5 Year Spread (0.25) is testing the 21 day moving average on the short term chart and should move up in the next few sessions, indicating a likely dip for the 5 year yield from 2.65%.

USDJPY – Bullish, Triggers Further Correction

USDJPY - The pair closed higher on the back of its Friday gain on Monday. On the downside, support lies at the 106.00 level where a break if seen will aim at the 105.50 level. A cut through here will turn focus to the 105.00 level and possibly lower towards the 104.50 level. On the upside, resistance resides at the 107.00 level. Further out, we envisage a possible move towards the 107.50 level. Further out, resistance resides at the 108.00 level with a turn above here aiming at the 108.50 level. On the whole, USDJPY faces further downside pressure but with caution

Intermezzo

Intermezzo

It was a predictable snoozefest in FX overnight as global holiday sessions crimped activity. And adding to the void, there was scant data during European hours which severely nipped action as traders had few if any fundamental guideposts.

But the markets interlude included the usual holiday- liquidity induced mystery move as the dollar went bid at the NY open. But the step was humble and little more than an attempt to trigger some stops in low liquidity market conditions. But all near-term support levels held and the move and quickly retracted as there was no news to support the quickstep sell-off. Chalk it up to the ghosts of presidents past.

Currency markets have remained relatively muted with few if any headlines to sink one’s teeth into but as the markets pivot to Fed speak and the FOMC minutes this week, “deficit mania” is sounding a few decibels lower this morning.But none the less, ongoing concerns about swelling deficit’s and the Feds sequence of interest rate normalisation should be the markets key focus this week and the primary drivers of near-term volatility.

Oil Markets

Oil prices have started the week on a positive note.With risk aversion abating, equity markets have remained guardedly positive. Also, an escalation of middle east tensions on the back of Israeli Prime Minister Benjamin Netanyahu beating the war drums by suggesting that Isreal could act against Iran alone has nudged prices higher. Predictably this warmongering has put the region on a state of readiness fearing a head to head incident and boosted oil prices due to the fear of sizable supply disruptions. Of course, when Isreal comes into the equation it could spark contagion across a region

Also, convincing signals from OPEC and their partners to extend production cuts continues to resonate with investors.

Gold Markets

Gold prices slid lower overnight on a drop in volatility and a slightly stronger dollar. Selling pressure emerged after USD speculative buyers emerged along with some position short covering ahead of the plethora of critical Fed speak and of course the FOMC minutes. But given the late-January Fed meeting was primarily interpreted as Hawkish; the bar is high for the minutes to sound an even more Hawkish note, but they will still attract the lions share of attention.

Given that the sun seldom shines on a capital hill along with escalating middle east tension, on the first sign of a dollar downdraft gold with ratchet higher.

G-10

The Japanese Yen

Markets are focusing on Friday’s crucial Japan CPI print, and with all the recent chatter about the BoJ extending YCC in perpetuity given the stronger Yen, short-term traders are paring back bearish dollar bets. And with a relative sense of calm in overall volatility, dollar bears are taking an interlude in holiday thinned-trading conditions

The Euro

Very little buying interest yesterday after Friday’s sell-off so given the lack of demand the Euro could fall to low 1.23 on even minor unexpected hic-up on news flow given thin liquidity conditions. But dips should look attractive for long-term players.

The Malaysian Ringgit

Very quiet trading session to start the week with local trader biding time until the FOMC minutes release. In the meantime, the broader USD sentiment will dictate the pace of play for regional currencies and imparticular the USDJPY which is moving towards 107 which is mildly negative for the MYR

On a favourable note, Oil prices remain robust on the escalation of middle east tension and production cut compliance among OPEC members which should provide support for the MYR.

Gold Trading Sideways In Thin Holiday Trade

Gold prices are trading sideways in the Monday session. Currently, the spot price for an ounce of gold is 1347.25, down 0.02% on the day. There are no US releases on Monday, as bank and stock markets are closed for Presidents Day.

Volatility in the stock markets last week translated into gains for safe-haven assets such as gold. The base metal gained 2.3%, as nervous investors lost their appetite for risk. On Friday, gold lost ground but managed to briefly push above $1360, for the first time since late January. US fundamentals have been generally strong, pointing to a robust US economy. This has raised speculation of a quicker pace of rate hikes from the Fed, but gold has managed to hold its own against the US dollar, largely due to the recent stock market correction.

The US posted sharp housing and consumer confidence reports on Friday, but the dollar failed to make headway against the surging Japanese yen. Building Permits jumped to 1.40 million in January, up from 1.30 million in December. This easily beat the estimate of 1.29 million. Housing Starts followed suit and improved to 1.33 million in January, up from 1.19 million a month earlier. This was well above the forecast of 1.28 million. There was more positive news from consumer confidence, as UoM Consumer Confidence climbed to 99.9, well above the estimate of 95.4 points.