Sample Category Title

Has Bitcoin Found A Floor?

On Wednesday, the price of bitcoin gained by almost 10% towards the end the day above $8,000. This marked a more than $2,000 gain from when the currency touched a low of under $6,000 early this week.

Traders attributed the sudden rise in bitcoin and other cryptocurrencies, to a meeting by the United States’ Senate Banking Committee. During the meeting, officials from the Securities and Exchange Commission (SEC) and Commodities and Futures Trading Commission emphasized the need to regulate the industry without calling for a blanket ban.

During the meeting, the officials said that the treasury was in the process of bringing together several agencies to coordinate the industry.

To traders, this was a positive move because it went against other countries like China, which have moved to ban ICOs and other blockchain related products entirely.

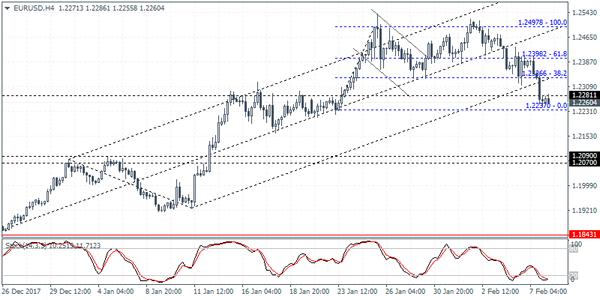

As shown below, at the current price, bitcoin has retraced to the 61.8% Fibonacci level. Unless there is any major negative news, the price of bitcoin could try to test the $8720 level, which is an important Fibonacci level.

Bank Of England Policy Meeting Takes Center Stage

A high-profile meeting of the Bank of England (BOE) will dominate the headlines on Thursday, giving stock and currency traders the latest reading on monetary policy. Although the central bank is not expected to raise interest rates, the official statement could shed light on the future path of monetary policy.

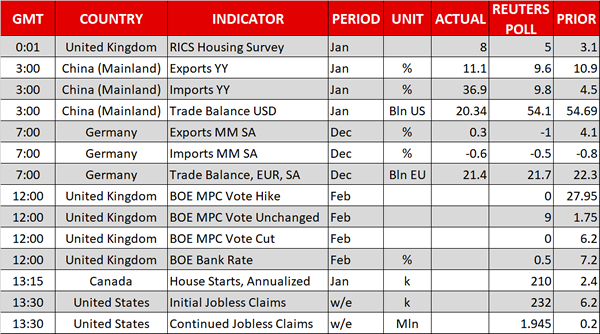

The European calendar picks up at 07:00 GMT with a report on German trade. Europe’s largest economy is expected to post a trade surplus of €21.7 billion in December, down from €22.3 billion. Exports are forecast to fall 1% month-on-month, following a 4.1% increase in November. Meanwhile, imports are expected to decline 0.5% from November.

Later in the morning, the European Central Bank (ECB) will unveil the latest Economic Bulletin, which provides a broad overview of the major trends impacting the currency region.

The BOE policy meeting will end in a rate statement at 12:00 GMT. The benchmark interest rate is forecast to hold steady at 0.5%, with the asset purchase facility also unchanged at £435 billion. Bank of England policymakers voted to raise interest rates in November for the first time in more than a decade in an attempt to cool surging inflation.

Elsewhere on the policy docket, US Federal Reserve Bank of Dallas President Steven Kaplan will deliver a speech at 09:50 GMT. Federal Open Market Committee (FOMC) member Patrick Harker is also scheduled to speak later in the day, as is Neel Kashkari of the Minneapolis Fed.

In terms of US data releases, the Department of Labor will issue its weekly jobless claims report for the period ended 2 February. The number of Americans filing for first time unemployment benefits is projected to rise by 2,000 to a seasonally adjusted 232,000.

EUR/USD

Europe’s common currency sunk to fresh two-week lows on Wednesday, as the US dollar rose across the board. The EUR/USD exchange rate recovered somewhat overnight, climbing 0.1% to 1.2272. The pair faces immediate resistance at 1.2310, followed by 1.2360. On the opposite side of the ledger, key support is located at 1.2255.

GBP/USD

Cable is coming off a volatile session, as prices fell sharply below the 1.3900 handle. The GBP/USD exchange rate was last seen trading at 1.3888, where it was up 0.1% from the previous close. The pair faces immediate resistance at 1.4000, a key psychological threshold.

USD/JPY

The dollar failed to extend its broad rally to the yen on Wednesday, with the USD/JPY fluctuating within a narrow range. The pair was little changed in Asian trading, as it held around 109.28. Immediate resistance is located at 109.75, followed by 110.05. On the opposite side of the spectrum, support is located at the 109.50 level, followed by 108.85.

Kiwi Records Losses As RBNZ Appears Cautious All Eyes On The Bank Of England

Here are the latest developments in global markets:

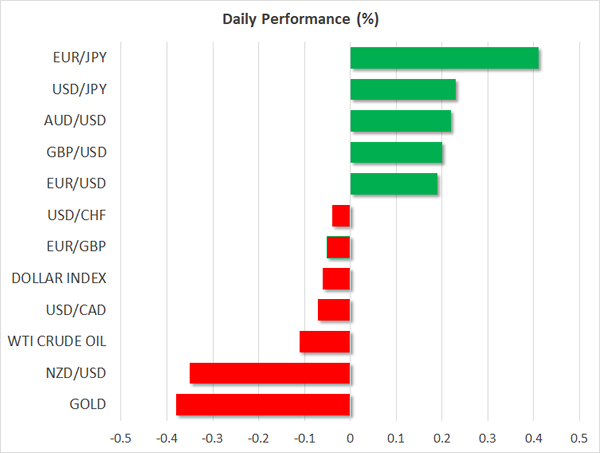

FOREX: The dollar index was marginally lower on Thursday, after previously posting notable gains on Wednesday, as yields on longer-dated US Treasuries moved higher. Meanwhile, sterling was a little higher ahead of the Bank of England's “Super Thursday” policy meeting. The kiwi dollar slipped, as the RBNZ disappointed those looking for an upbeat assessment.

STOCKS: US equity indices experienced another volatile session on Wednesday, and finished lower overall. The Nasdaq Composite fell by 0.9%, the S&P 500 closed 0.5% lower, while the Dow Jones declined by 0.1%. The shaky performance of these indices indicates that investors still appear skeptical of reentering long-equity positions, following the recent turmoil. Futures tracking the Dow, S&P, and Nasdaq 100 are all in positive territory, albeit marginally. In Asia, most markets were in the green. Japan's Nikkei 225 and Topix finished higher by 1.1% and 0.9% respectively, while Hong Kong's Hang Seng was up by 0.4%. In Europe though, futures tracking all of the major stock indices were in the red.

COMMODITIES: Oil prices were lower on Thursday, with WTI and Brent crude being down 0.1% and 0.3% respectively, both extending the notable losses they posted yesterday. The sharp plunge in prices came after the weekly EIA inventory data. Even though crude stockpiles rose by less than expected, the energy market finally took notice of the soaring US production, which surged to a record high of 10.25 million bpd. Should tomorrow's Baker Hughes oil rig count reveal a further increase in active US rigs, prices could remain under pressure, on speculation that US output may increase further. In precious metals, gold was lower by almost 0.4%, last trading near the $1,312 mark.

Major movers: RBNZ appears cautious; German leaders strike a deal; US deficit set to expand further

The Reserve Bank of New Zealand (RBNZ) kept its policy unchanged yesterday, while the tone of the accompanying statement was somewhat more cautious than previously. The Bank noted that the nation's growth profile is now weaker in the near-term, but stronger in the medium-term, while it also acknowledged the softness in the latest set of inflation data.

As for the kiwi, officials said that it has firmed recently, mostly due to the weak US currency. Importantly, they now assume that the trade-weighted exchange rate will ease over time. Moreover, in the press conference following the decision, assistant Governor McDermott indicated that if the trade-weighted index moves up, then investors should expect more aggressive language on the NZD. The two key takeaways from this meeting were that any rate hike in New Zealand is still a long way off, and that any further strengthening of the NZD would probably see the Bank threaten FX intervention, as it did multiple times in the past. Kiwi/dollar fell on the decision and continued lower in the following hours.

German political leaders finally managed to strike a coalition deal yesterday, after several months of negotiations. The deal must now be approved by the members of the SPD. Even though Germany will now most likely have a stable and pro-EU government, the euro remained on the back foot yesterday, before rebounding somewhat today. The weakness is being attributed to disappointment that SPD leader Martin Schulz will not be taking over the finance ministry, given his anti-austerity views.

In the US, Congressional leaders struck a two-year budget deal that will raise federal spending by $300 billion. If approved by Congress, this plan would add further to the rising US deficit, that has been a major concern for investors lately as the nation's long-term debt sustainability appears to be in jeopardy. Bond markets took notice of this, with the yields on longer-term US Treasuries rising notably. Interestingly enough, the dollar managed to rise alongside yields, reviving a relationship that had largely broken down in recent months.

In terms of economic data, Chinese exports and imports beat expectations, with the latter surging by an impressive 36.9%, almost four times the amount analysts projected. This resulted in a mush narrower trade surplus (exports minus imports) than expected and led to a considerable decline in the yuan relative to the US currency. Dollar/yuan was up by more than 0.4%. On Wednesday, the pair touched 6.2548, its lowest since August 2015. It should be mentioned that the release was likely distorted by seasonal effects owed to the Lunar New Year festivities.

Day ahead: BoE meeting the day's highlight; US jobless claims due

The European Central Bank's Economic Bulletin will be released at 0900 GMT. The report contains statistical data that policymakers use when deciding on interest rates, while it also offers an analysis on current and future economic conditions from the central bank's perspective.

Without a doubt the highlight of the day will be the Bank of England meeting on monetary policy. The Bank's decision on rates will be made public at 1200 GMT. No change in rates is expected, with attention falling to the central bank's quarterly inflation report which will include updated forecasts on economic growth and inflation; this will also be released at 1200 GMT. The vote count could also attract attention. While forecasts point to a unanimous 9-0 vote to hold rates unchanged, investors may look at whether notorious policy hawks such as Ian McCafferty and Michael Saunders will choose to dissent and vote for a hike instead, potentially increasing expectations that such an action may occur in the near future. Shortly after (at 1230 GMT), Governor Mark Carney will be holding a press conference. His comments have the capacity to spur volatility in sterling pairs, with market participants placing bets on the timing of the next interest rate hike by the BoE.

An appreciating British currency in 2018 is supportive of inflation moving lower towards the BoE's target for annual inflation of 2% and allowing the central bank to proceed more aggressively with its policy normalization plans. This is an issue that Carney might comment on during today's press conference.

Canadian housing starts for the month of January are scheduled for release at 1315 GMT.

US weekly data on initial and continued jobless claims are due at 1330 GMT. First-time unemployment benefit claimants are anticipated to increase by 2k relative to the week ending January 27 when they stood at 230k. A number below 300k is linked to a healthy jobs market. Should claimants stand below this level as expected, it would mark the 153rd such week, this being the longest streak since 1970.

Beyond the BoE press conference, other policymakers' appearances include: ECB chief economist Peter Praet and Dallas Fed President Robert Kaplan – a non-voting FOMC member in 2018 – will be speaking at a conference in Frankfurt at 0950 GMT. ECB executive board member Yves Mersch will be giving a lecture touching, among others, on central banks and digital currencies, at 1000 GMT. Other FOMC policymakers talking today are Philadelphia Fed President Patrick Harker (1300 GMT) and Minneapolis Fed President Neel Kashkari (1400 GMT) – neither holds voting rights within the FOMC during the current year. Lastly, Bank of Canada Senior Deputy Governor Carolyn Wilkins will be giving a speech at 1800 GMT.

In equities, the earnings season continues with Twitter and Philip Morris getting in line to release quarterly results.

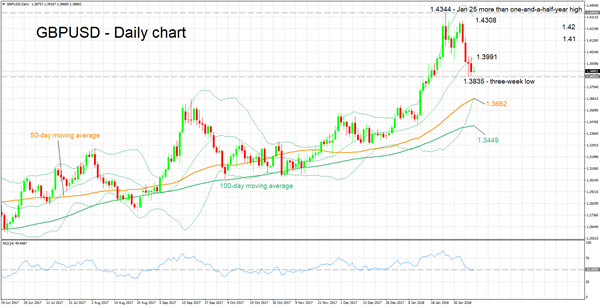

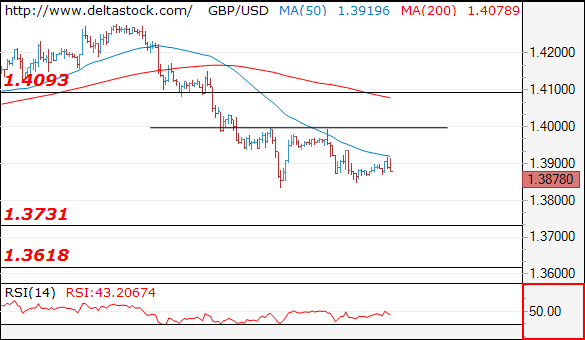

Technical Analysis: GBPUSD in wait-and-see mode ahead of BoE

GBPUSD has lost ground after posting a more than one-and-a-half-year high of 1.4344 on January 25. The RSI has been falling in previous days, pointing to negative short-term momentum. However, at the moment it is hovering around the 50 neutral level. This could be an indication that markets are in a wait-and-see mode ahead of the Bank of England meeting and subsequent press conference by the Bank's Governor.

Any signs that the BoE will tighten policy sooner than earlier thought, are anticipated to lead the pair higher. In this case, resistance could come around the middle Bollinger line – a 20-day moving average line – at 1.3991. The area around this level also encapsulates the 1.40 handle, a level of potential psychological importance. An upside break would turn the attention to 1.41, this being another level that may be of psychological significance.

On the other hand, a dovish message by the BoE is expected to lead to weakness in the pair. Immediate support might come around Tuesday's three-week low of 1.3835. Price action is currently taking place not far above this level, with a violation bringing into view the 50-day MA and lower Bollinger band, both at 1.3662.

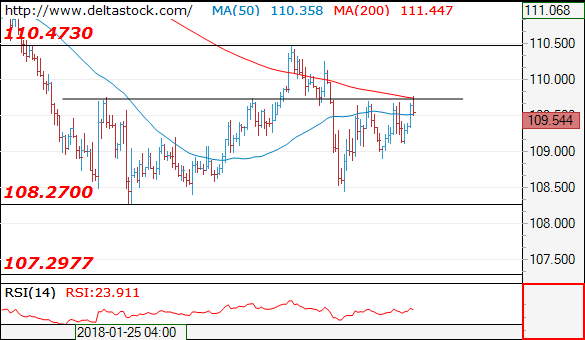

USDJPY Maintains Weak Bias, Broader Trend Still Neutral

USDJPY has been trading within a sideways channel in the daily timeframe since April 2017 with upper boundary the 114.50 significant and multi-tested resistance level, and with lower boundary the 108.20 support level, which has been penetrated once in September.

Currently, prices are developing below the 110.50 barrier and the 20-day simple moving average. The pair tested several times the 20-SMA, which is acting as a strong resistance level. However, the short-term technical indicators are slightly bullish and point for more upside movement in the market. The RSI indicator is pointing up in the negative zone, while the MACD oscillator is rising and jumped above its trigger line, creating a bullish crossover.

Upsides moves are likely to find resistance at 110.50. Rising above this area could help shift the focus to the upside towards the next immediate critical level at 111.50, which coincides with the upper Bollinger Band at the time of writing.

On the flip side, if dollar/yen reverse lower, the next level to have in mind is the 108.20 (lower boundary of trading range), which overlaps with the lower Bollinger Band. A drop below this area could take the pair below the sideways channel, challenging the 107.30 support level, taken from the low on September 8.

It is worth mentioning that USDJPY has been developing within a symmetrical triangle in the medium-term timeframe since May 2015. The symmetrical triangle is a continuation pattern, indicating further gains in case of a penetration to the upside on a weekly basis.

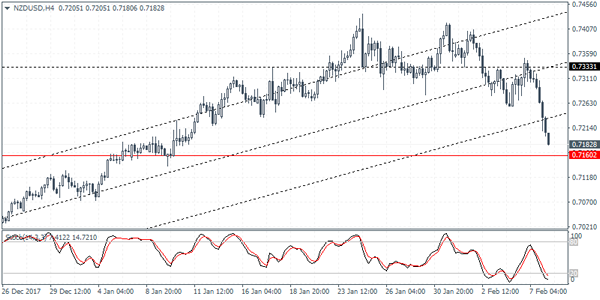

NZDUSD Posts Steep Losses, Finds Support At 38.2% Fibonacci Level

NZDUSD has been tumbling over Wednesday's and today's Asian sessions, while it recorded a fresh one-month low of 0.7175. The aggressive sell-off pushed the price below several key levels such as the 23.6% Fibonacci retracement level at 0.7280 from 0.6780 to 0.7436, 0.7255 and 0.7230.

In the 4-hour chart, short-term indicators are signaling a bearish movement. The Relative Strength Index (RSI) is holding near the 30 level, while the MACD oscillator is weakening in the oversold territory. Also, the latter oscillator recorded a bearish crossover with its trigger line in the previous sessions, indicating further losses.

If prices extend the downward pressure, immediate support could come at 0.7140. Below that, the price could hit the 50.0% Fibonacci retracement level at 0.7436. As a side note, the price needs to go through the 38.2% Fibonacci mark slightly above the one-month low.

In the event of an upside reversal, the next level to watch is the 0.7230 resistance obstacle as well as the 0.7255 level and the 23.6% Fibonacci at 0.7280.

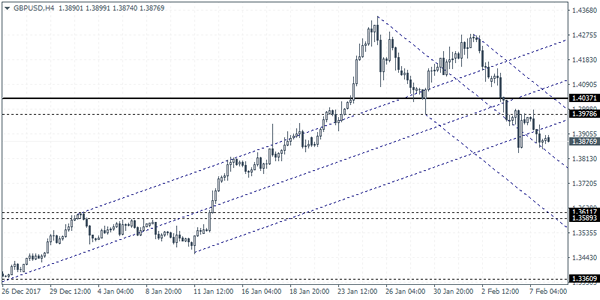

Technical Outlook: GBPUSD – BoE In Focus, Hawkish Stance Could Inflate Pound For Retest Of 1.40 While Softer Tone...

Cable was slightly higher during Asian trading on Thursday, but gains were so far unable to clearly break above 1.3900 barrier (broken 50% of 1.3457/1.4344/daily Kijun-sen).

Wednesday close in red and below 1.39 handle was negative signal, however, dips remain for now limited by pivotal support at 1.3841 (Fibo 38.2% of 1.3026/1.4344, Oct-Jan rally, reinforced by rising 30SMA).

Another strong support lies just below, at 1.3796 (Fibo 61.8% of 1.3457/1.4344 rally) and sustained break below 1.3841/1.3796 pivots will generate strong bearish signal.

Bearishly aligned daily studies weigh, but oversold slow stochastic signals that bears may hesitate ahead of renewed attempts lower.

Falling thick hourly cloud (spanned between 1.3936/93) marks strong barrier above initial 1.3900 hurdle and continues to weigh on near-term action.

BoE's interest rate decision and release of inflation report are key events for sterling today. The central bank is expected to keep interest rates unchanged at 0.50% on today's meeting, but hawkish tone could be expected. Traders expect the BoE to signal another interest rate increase in coming months and will look for voting results from the previous meeting, which could generate positive signal if any of nine MPC members voted for rate hike.

Positive signals would increase likelihood of rate hike in BoE's next policy meeting in May.

Hawkish stance from BoE could inflate the pound for retest of important 1.40 barrier (psychological resistance / broken Fibo 38.2% of 1.3457/1.4344) and could generate stronger bullish signal on firm break higher.

Conversely, softer tone from the central bank would increase pressure on pound for extension of pullback from 1.4344 (25 Jan peak/the highest level since Brexit vote).

Res: 1.3900, 1.3936, 1.4000, 1.4056

Sup: 1.3841, 1.3796, 1.3741, 1.3724

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

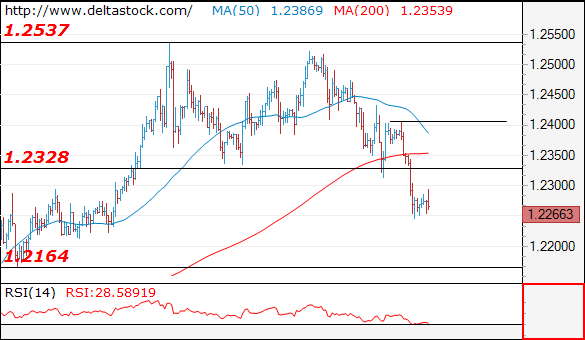

Current level - 1.2266

The outlook is bearish below 1.2330, for a slide towards 1.2160 area. Crucial on the upside is 1.2405 high.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2330 | 1.2540 | 1.2220 | 1.2160 |

| 1.2405 | 1.2870 | 1.2160 | 1.2090 |

USD/JPY

Current level - 109.54

Expect a violation of 109.70 resistance to initiate a rise towards 110.50. Crucial on the downside is 109.10.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.70 | 111.90 | 109.10 | 108.30 |

| 111.50 | 113.40 | 108.30 | 107.30 |

GBP/USD

Current level - 1.3878

The bias is bearish for a break through 1.3835 low, towards 1.3730, en route to 1.3620 area. Crucial on the upside is 1.4000.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4000 | 1.4090 | 1.3800 | 1.3730 |

| 1.4090 | 1.4174 | 1.3730 | 1.3620 |

NZDUSD Intraday Analysis

NZDUSD (0.7182): The New Zealand dollar was seen weakening since the RBNZ's decision. Price action briefly tested the breached support level at 0.7333 where resistance has been established. The reversal off this level has seen price declining with the first support level at 0.7160 within reach. Expect to see NZDUSD potentially rebounding at this level but the gains could be limited within the resistance level of 0.7333 and the current support. We expect the longer term trend to point to the downside with NZDUSD likely to see further declines that could test the lower support at 0.6950.

GBPUSD Intraday Analysis

GBPUSD (1.3876): The British pound has been extending declines over the past few daily sessions. Price action closed with an inside bar yesterday but further downside is expected. Following the breakdown below the support level at 1.4037, we expect to see a retracement to this level in the short term. If price action can establish resistance at this level, we could expect to see further declines pushing the GBPUSD down to the support at 1.3617 which is pending retest. To the upside, in the event that GBPUSD breaks past 1.4037, the downside bias is invalidated.

EURUSD Intraday Analysis

EURUSD (1.2260): The euro currency extended declines against the USD yesterday as price was seen falling to a fresh monthly low. The declines come following the doji pattern that was formed. With price closing below the doji's low, we expect to see further continuation in declines. Support is seen at 1.2091 on the daily chart which could be the first level of support. On the 4-hour chart the declines have invalidated the bullish flag pattern. Any near term retracements could be seen stalling near 1.2336 or up to 1.2398 level. A retest of this level could suggest further declines with the eventual target seen at 1.2090.