Sample Category Title

Daily Wave Analysis: EUR/USD Tests 38.2% Fibonacci Support At 1.2250

Currency pair EUR/USD

The EUR/USD continued to move lower within the bearish channel but price has now reached the 38.2% Fibonacci level of wave 4 (purple). This could be a potential bounce spot if price does complete the wave 4 correction. A break above resistance (red/orange) could see the start of a wave 5 (purple).

The EUR/USDfailed to break above resistance and in fact extended the bearish correction. The wave pattern however remains most likely an ABC (green) correction. Whether the wave C (green) is indeed completed depends if price can break above the potential bottom of wave 1 (orange), otherwise one more lower low as part of wave 4-5 (orange) could occur.

Currency pair GBP/USD

The GBP/USD could still be in a wave 4 (green) correction. A new bearish break would make this wave analysis unlikely and could indicate a potential larger bearish trend. A break above the previous top (red) could indicate a continuation rally.

The GBP/USD did not invalidate the bottom of wave 2 (blue) and be building a wave 1-2 (blue) pattern.A break above resistance (red/orange) could indicate the start of wave 3 (blue).

Currency pair USD/JPY

The USD/JPYis trapped in betweenstrong support (green/blue) and resistance (red/orange) but price still seems to be buildinga wave 1-2 (purple) pattern. A bearish break below the bottom and 100% Fib invalidates the wave 2 (purple).

The USD/JPYneeds to break above resistance (red) before an uptrend continuation is likely.

Market Update – Asian Session: Equities Remain Mixed, China Records Jan Trade Surplus, Encourages US To Deal Prudently With...

Headlines/Economic Data

General Trend: Asian equities trade mixed

Chinese equities decline amid weaker than expected trade surplus

China Jan imports jump as crude oil imports hit record high

Yuan (CNY) declines over 1% versus USD, despite stronger PBoC fix

Kiwi (NZD) under performs as RBNZ official commented on probability of rate cut

Aussie traders look ahead to Friday's release of the RBA quarterly policy statement and forecasts

RBA Gov Lowe expected to speak later today during the European morning

BoJ’s Suzuki comments on recent declines in markets and possibility of ‘tweak’ in policy easing

Japan

Nikkei 225 opened +0.4%; closed +1.1%

Nissan [7201.JP] gains ahead of earnings report

(JP) Japan Dec BoP AdjCurrent Account: ¥1.48T v ¥1.65Te; Current Account Balance: ¥797.2T v ¥1.06Te;Trade Balance BoP: ¥538.9B v ¥520.4Be; 2017 current account surplus¥21.874T, +7.5% y/y; largest since 2007

(JP) BoJ Suzuki: Reiterates important to 'patiently' maintain 'powerful' monetary easing; does not rule out a chance of 'tweak' under powerful easing; BoJ may fine-tine YCC in future but that won't be big turnaround in its monetary policy or exit from easy policy; Impact of 'market rout' on policy may be limited

(JP) Japan Chief Cabinet Sec Suga: No decision made on meeting between Abe and North Korea

(JP) Japan MoF sells ¥800B v ¥800B indicated in 0.8% (0.8% prior) 30-yr bonds; Avg yield: 0.820% v 0.832% prior; Bid to cover: 4.27x v 3.77x prior

Korea

Kospi opened +0.2%

Chip makers Samsung Electronics and Hynix gain over 1%

Daewoo Engineering & Construction [047040.KR]: Declines over 6%: Hoban said to be considering dropping its bid due to extra losses - Korean press

(KR) North Korea: Will not use Winter Olympics aspolitical venue – KCNA

(KR) South Korea Industry Ministry launchedproject to boost the country's semiconductor and display sectors through newtechnology development and localized production - Korean press

(KR) Bank of Korea (BoK): Reiterates monetary policy to remain accommodative; Sees strong exports of memory chips and oil products

(US) Vice President Pence: Will meet any use of nuclear weapons with rapidresponse; all options are on the table for North Korea - Speaking to troops inJapan

China/Hong Kong

Hang Seng opened +0.8%, Shanghai Composite -0.9%

Hang Seng Info Tech Index +1.6%, Services +1.5%, Financials +0.6%, Property/Construction+0.2%; Materials -1.8%, Energy -1.1%

(CN) CHINA JAN FOREIGN RESERVES: $3.162T V $3.170TE (released after Shanghai closeyesterday)

(CN) CHINA JAN TRADE BALANCE (CNY): 135.8B V 330.0BE; Exports YoY: 6.0% v 2.6%e, Imports YoY: 30.2% v 5.3%e

(CN) CHINA JAN TRADE BALANCE (USD): $20.3B V $54.7BE; Exports YoY: 11.1% v 10.7%e, Imports YoY: 36.9% (fastest growth since Feb 2017) v 10.6%e

ZTE Corp [763.HK] Senator's Tom Cotton and Marco Rubio introduce Defending US Govt Communications Act; legislation that would prohibit the United States government from purchasing or leasing telecommunications equipment and/or services from Huawei, ZTE, or any subsidiaries or affiliates

(CN) China Economic Daily Commentary: One-waymove of yuan is unlikely in 2018

(CN) China Jan excavator sales said to more than double - Chinese Press

(CN) China Central Depository & Clearing annual report: Interbank holdingsof wealth management products CNY3.25T v CNY6.65T y/y

(CN) Standard Chartered Economist Ding: Yuan could appreciate to 6.18/dollar bythe end of the year

USD/CNY (CN) PBOC SETS YUAN REFERENCERATE AT 6.2822 V 6.2882 PRIOR (strongest CNY fix since Aug 11, 2015)

(CN)PBOC Statement: To improve the framework of regulation underpinned by monetarypolicy and macro-prudential policy in 2018

(CN) China FX Regulator SAFE: Will support "capable and qualified"businesses to invest overseas this year to advance cross-border investment

(CN) China probe on US Sorghum imports is normal case; urges US to prudentlydeal with 301 probe

USD/CNY Onshore yuan falls 0.7% to 6.3268/dollar, biggest decline in 13-months

(CN) China has resumed an outbound investment scheme, under the Qualified Domestic Limited Partnership (QDLP) plan after a 2-yr break, granting licenses to ~12 global money managers - financial press

Looking Ahead: China Jan CPI and PPI expected to be released on Friday

Australia/New Zealand

ASX 200 opened -0.2%; closed %

ASX 200 Resources Index -1.2%, Energy -1.5%, Utilities -1.3%; Telecom +1.5%, Financial +0.8%

(NZ) NEW ZEALAND CENTRALBANK (RBNZ) LEAVES OFFICIAL CASH RATE (OCR) UNCHANGED AT 1.75%; AS EXPECTED

(NZ) RBNZ Gov Spencer: not concerned about the NZD, comfortable with where the currency is - post rate decision comments

(NZ) RBNZ Assistant Gov McDermott: Drop in inflation expectations could trigger rate cut; currently RBNZ has neutral stance on rates

(NZ) New Zealand Central Bank (RBNZ) Gov Spencer: Did not cut rates because inflation will come back – parliament

(AU) Australia Q4 NAB Business Confidence: 6 v 8 prior

Blackham Resources (+32%) BLK.AU Reports Jan gold production6.5K oz v 5.5K m/m

AGL Energy[AGL.AU]: Declines over 1% as H1 underlying EBIT missed expectations

Looking Ahead: RBA Gov Lowe expected to speak during European morning

RBA Quarterly Monetary Policy Statement due for release on Friday

Other Asia

(PH) Philippines Central Bank (BSP) due to hold policy meeting later today

Singapore bank DBS [DBS.SG] gains over 2% after reporting Q3 earnings

North America

US equity markets closed mostly lower: Dow -0.1%, S&P500 -0.5%, Nasdaq -0.9%, Russell 2000 +0.1%

S&P500 Energy Sector -1.7%, Technology -1.3%

Costco [COST] Reports Jan SSS (ex-gas) 2.9%;US SSS (ex-gas) 3.6% v 2.1%e

Victory Capital [VCTR ] Prices 11.7M share IPO at$13.00/shr v $17-19/shr range indicated

SPDR Gold Trust ETF daily holdings -0.3% at 826.9 metric tonnes

(US) White House aide: we have come to agreement on 2-year budget deal (agreement includes $300B boosts to defense and non-defense spending); Deal would extend reaching the debt ceiling until March 2019

(US) Fed's Williams(moderate, voter): No strong view between 3 or 4 Fed hikes in 2018

(US) Fed's Dudley (dove, FOMC voter): A sustained drop in stock market would impact my outlook; recent activity has no consequence for economic outlook

(US) Fed’s Evans (non-voter, dove): there's a hint inflation pressures may be in train today; his dissent on Dec rate hike was a close call; Under an alternate scenario where inflation picked up more assuredly, would support 3 or even 4 rate hikes in 2018 - comments in Iowa-

(US) TREASURY'S $24B 10-YEAR NOTE AUCTION DRAWS:2.811%; BID-TO-COVER RATIO: 2.34 V 2.48 PRIOR AND 2.33 OVER THE LAST 10 AUCTIONS (bid to cover lowest since Sept 2017)

(US) DOE CRUDE: +1.9M V +2.5ME

(CA) Canada Prime Min Trudeau: NAFTA needs to be updated and improved

Europe

(EU) ECB's Nowotny (Austria): US Treasury is deliberately putting pressure on the dollar and wants to keep it low - press interview

(DE) Germany SPD Leader Schulz: optimistic we can get SPD party members to agree to SPD-CDU coalition

(DE) Germany's SPD leader Schulz to step down asp arty leader; says party leader should not be part of the govt cabinet (Schulz will become Foreign Minister under the coalition deal)

(DE) Germany's SPD party to announce results of members ballot on supporting govt coalition deal on March 4th - press

(UK) Citing UK Govt economic analysis: a no-deal Brexit would cost £80B in public finances, with the leave-voting heartlands of north-east England and West Midlands worst affected - Guardian

Swiss Re [SREN.CH]: Softbank said to be in advanced talks to take as much as a 33% stake in Swiss Re - press

Looking Ahead: BoE rate decision and inflation report due later today

Levels as of 01:00ET

Nikkei225 +1.1%, Hang Seng +0.6%; Shanghai Composite -1.5%; ASX200 +0.2%, Kospi +0.8%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.3%,Dax +0.3%; FTSE100 -0.2%

EUR 1.2286-1.2252; JPY109.68-109.12; AUD 0.7832-0.7803;NZD 0.7238-0.7181

Apr Gold -0.1% at $1,313/oz; Mar Crude Oil -0.4%at $61.55/brl; Mar Copper +0.5% at $3.11/lb

S&P500 Closed 0.5% Lower Yesterday

The main focus continues to be overall market confidence and whether the worst is over with regard to the big equity sell-off earlier this week. Our market sentiment indicators have moved from very stretched positive sentiment two weeks ago to now neutral suggesting that markets are more in balance and sooner or later we expect the upward trend in equities to resume. However, the markets will likely stay fragile short term.

It is super Thursday in UK today with one of the 'big' Bank of England meetings, which includes the Inflation Report and a press conference. We expect an unanimous vote for unchanged rates and a 'wait -and-see' stance from BoE for now. Markets are pricing the probability of a rate hike already in May by 50/50, which is too hawkish in our view.

We will also get a series of ECB speeches and the ECB Monthly Bullet in is released. On the data front we have German trade balance and US init ial jobless claims.

In Scandi the SCB house prices for Sweden are released. We put more weight on the Valueguard prices, though.

Selected market news

Markets are still fragile and after a very volatile day, S&P500 closed 0.5% lower yesterday and the future is trading a bit lower this morning. Asian stocks are mixed. VIX declined to 22 yesterday but is back to nearly 28. US 10yr Treasury yield rose yesterday to as high as 2.85, as the increasing US deficit means Treasury needs to issue more debt . Brent oil is down at 65.3 dollars per barrel (versus peak of 70), as data showed US crude product ion jumped to a record 10.12 million barrels a day last week. This morning, USD/CNY has risen from 6.28 to 6.32 in the biggest increases since the FX regime shift in 2015, as the Chinese trade balance in January declined to USD20.3bn from USD54.59bn in December due to a big increase in imports (although it is likely just a seasonal blip due to the Chinese New Year, as we usually see dips in the trade balance every year).

US Senate leaders announced a bipartisan two-year spending bill yesterday, which increases spending caps both for defence and non-defence spending adding approximately USD150bn to the government deficit in both 2018 and 2019 (the same as the annual cost of tax reform), so deficit may exceed USD1,000bn next year although the output gap is more or less closed. The deal includes a suspension of the debt limit until March 2019, meaning Treasury can start rebuilding its cash buffer again, which will drain USD liquidity if passed. While House Speaker Paul Ryan and President Trump support the bill, it is opposed by the Republican fiscal hawks in the House and the House Democratic leader Nancy Pelosi, who will not support a spending bill due to the ongoing discussion about immigrat ion reform. The short -term funding bill expires today and risk is a government shutdown tomorrow if the bill is voted down.

Yesterday the deadline expired for nominating candidates to succeed Vítor Constâncio as Vice-president of the ECB. The position as VP is the first of a total of four seat in the ECB's board that is up for change until the end of next year (see diagram towards the end of this piece). The race is between the long-time named favourite Spanish Luis de Guindos and Ireland's Philip Lane.

RBNZ Downgraded Inflation Forecasts, First Rate Hike Unlikely Until 2019

As widely anticipated, RBNZ left the OCR unchanged at 1.75%. Owing to the downside surprise in 4Q17 inflation, policymakers revised lower their inflation forecast, mainly driven by tradeable inflation. Meanwhile, the central bank now sees currency appreciation a less concern, as NDZUSD has retreated to a one-month low, and indicates that the positive impacts of fiscal stimulus (including KiwiBuild and the increase in minimum wages) have diminished. The overall monetary stance remains neutral with the first hike unlikely coming before the 2Q19.

Headline CPI in New Zealand slowed to +0.1% q/q in 4Q17, from +0.5% a quarter ago. This came in even weaker than consensus of +0.1%. From a year ago, inflation eased to +1.6% from third quarter's +1.9%. The market had anticipated a steadied +1.9%. The downside surprise triggered RBNZ to revise lower its headline inflation projection to +1.5% in 2018 (financial year), from November's estimate to +2%, and to +1.8% for 2019, from November's +2%. Most of the downside would be driven by tradeables inflation which is expected 'to remain subdued through the forecast period'. Meanwhile the central bank expects a reacceleration in non-tradeables inflation 'in line with increasing capacity pressures'.

The central bank also adjusted its GDP growth forecasts. Growth is expected to reach +3.2% in 2018, down -0.6 percentage point from the previous estimate, followed by an upward revision on 2019 growth to +3.5%, from November's +3%. Note that growth over both periods should remain above the RBNZ's estimate of trend growth of +3%. As noted in the accompanying statement, the central bank suggested that 'the growth profile is weaker in the near term but stronger in the medium term', when compared to the November statement.

On the exchange rate, RBNZ acknowledged that it has 'firmed' since the last meeting. However, it suggested that the strength was mainly driven by 'a weak US dollar' and noted that the trade-weighted exchange rate would 'ease over the projection period'.

On the monetary policy outlook, RBNZ maintained the November reference that 'monetary policy will remain accommodative for a considerable period. Numerous uncertainties remain and policy may need to adjust accordingly'. The OCR projections stay the same as the previous meeting with any move unlikely until mid- to end-2019 while more material rate hikes not seen until 2020.

RBNZ made quite a number of changes in the policy statement. However, the overall tone remains neutral as the positives and negatives largely offset each other. All in all, the central bank should leave the policy rate unchanged at 1.75% for the rest of this year. any rate hike would unlikely come until 2Q19, quite a distant future.

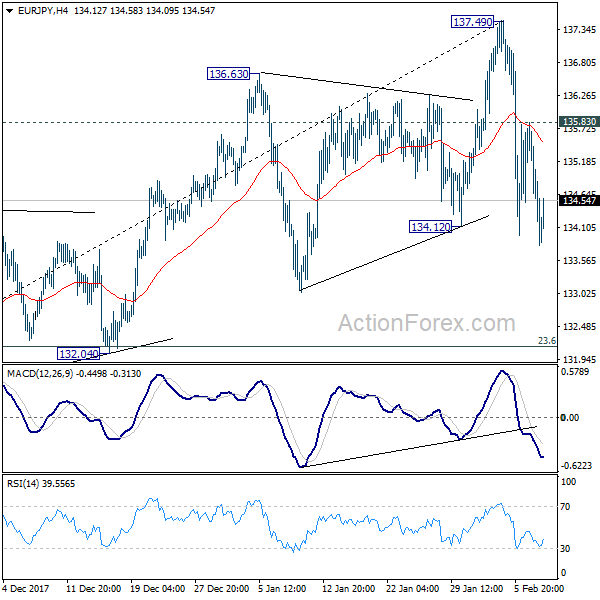

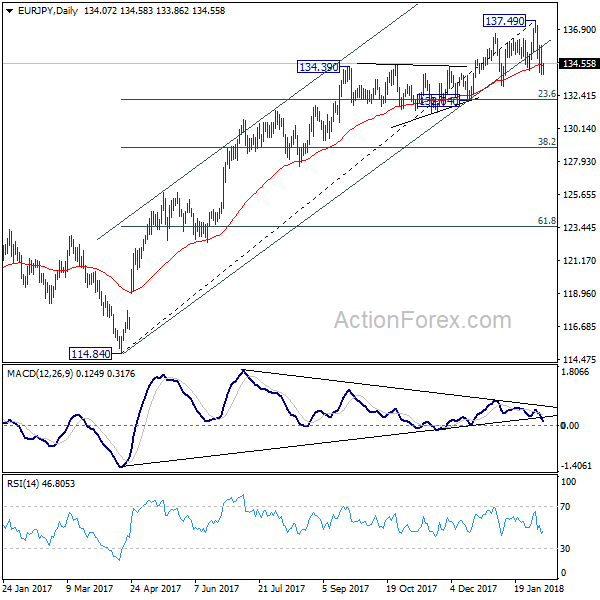

EUR/JPY Daily Outlook

Daily Pivots: (S1) 133.31; (P) 134.57; (R1) 135.33; More....

EUR/JPY's fall resumed after brief recovery and intraday bias is back on the downside. As noted before, near term trend is likely reversed considering bearish divergence condition in daily MACD. Deeper fall should be seen to 132.04 cluster support first (23.6% retracement of 114.84 to 137.49 at 132.14). Decisive break there will indicate larger reversal. However, above 135.83 minor resistance will turn focus back to 137.49 resistance instead.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support, however, will be an early sign of trend reversal and will bring deeper fall back to 124.08 key medium term support.

GBP/JPY Daily Outlook

Daily Pivots: (S1) 151.01; (P) 152.06; (R1) 152.79; More...

Intraday bias in GBP/JPY remains neutral for consolidation above 151.19 temporary low. Considering bearish divergence condition in daily MACD, the near term trend could have reversed. Hence, deeper fall is in favor. Below 151.19 will target 150.18 support first. Break of 150.18 will affirm this case and target 146.96 key support level.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. In that case, deeper fall would be seen to 38.2% retracement of 122.36 to 156.59 at 143.51 and then 61.8% retracement at 135.43.

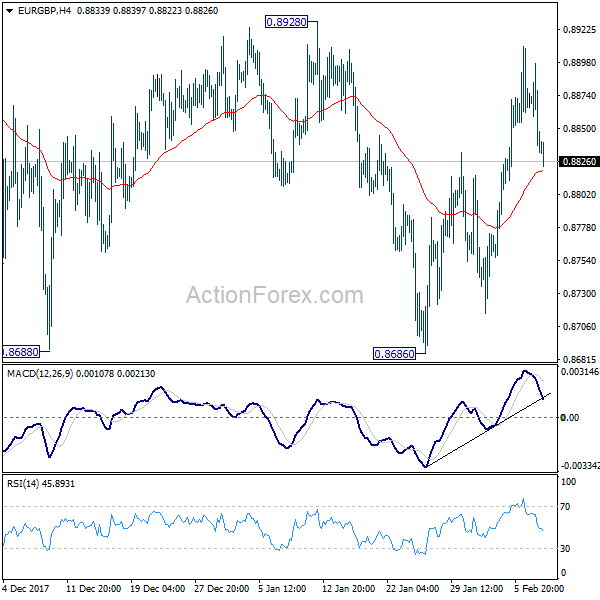

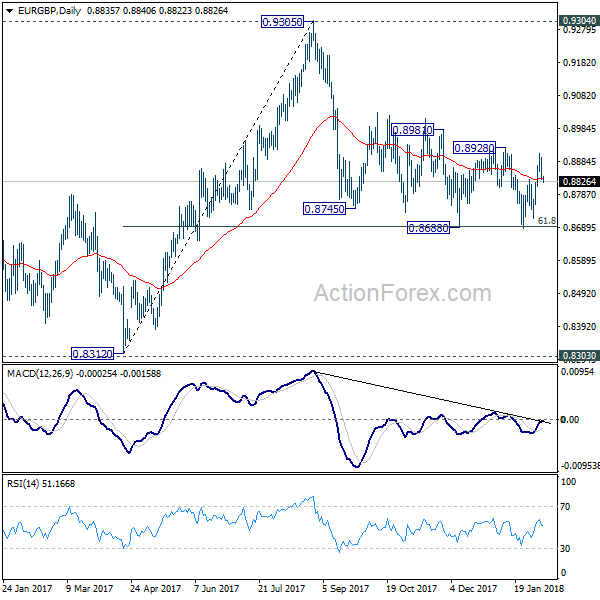

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8812; (P) 0.8855; (R1) 0.8876; More...

EUR/GBP's rebound was limited below 0.8928 resistance and weakens again. The cross is staying in range of 0.8686/8928 and intraday bias remains neutral first. And, near term outlook will remain mildly bearish as long as 0.8928 resistance holds. On the downside, firm break of 0.8686 will resume whole decline from 0.9305. As 61.8% retracement of 0.8312 to 0.9305 should then be taken out too. Deeper decline would be seen to retest 0.8303/8312 support zone. Nonetheless, on the upside, break of 0.8928 will indicate near term reversal and turn outlook bullish for 0.9304 resistance.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

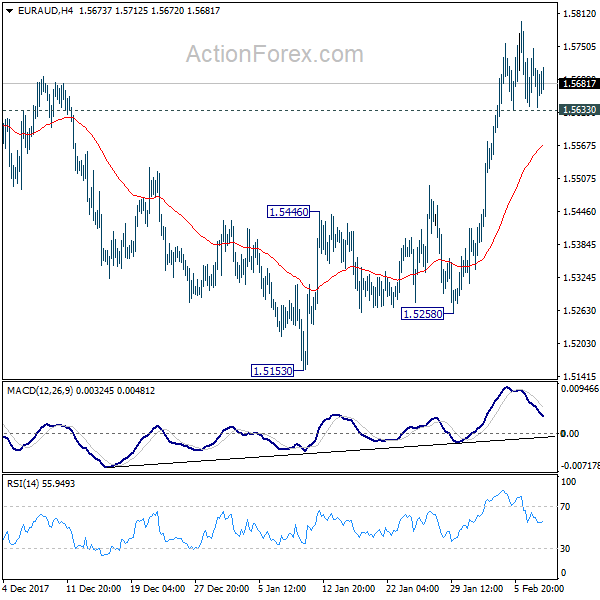

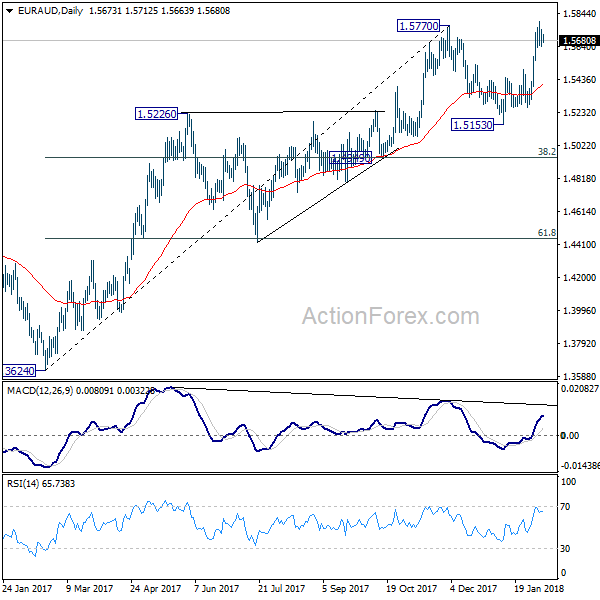

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.5629; (P) 1.5688; (R1) 1.5737; More....

As long as 1.5633 minor support holds, further rise is expected in EUR/AUD. The breach of 1.5770 resistance suggests that medium term rise from 1.3264 is resuming. Sustained trading above 1.5770 will pave the way to 1.6587 key long term support. Nonetheless, below 1.5633 minor support will dampen this bullish case and turn intraday bias neutral first.

In the bigger picture, medium term rise from 1.3624 is not completed yet. Break of 1.5770 will extend the rise to retest 1.6587 (2015 high). However, considering bearish divergence condition in daily MACD, sustained break of 1.4949 cluster support (38.2% retracement of 1.3624 to 1.5770 at 1.4950) will indicate medium term reversal. And there is prospect of retesting 1.3624 low in that bearish case.

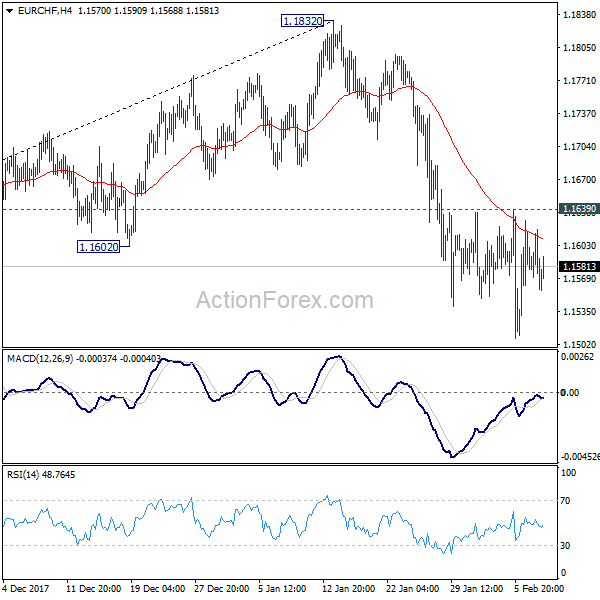

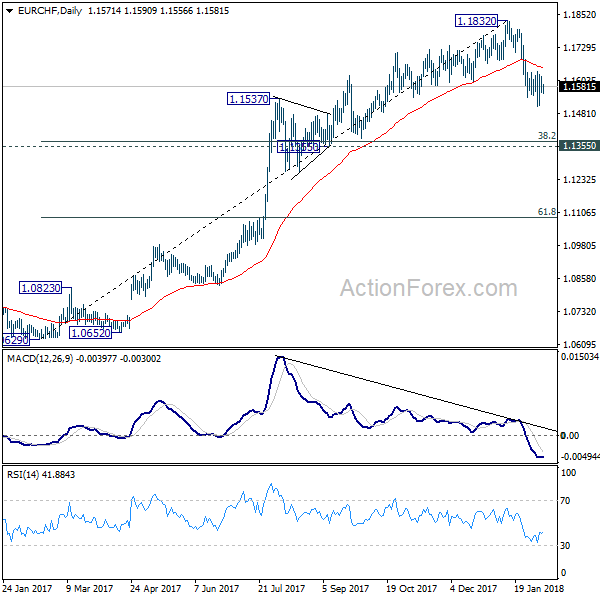

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1543; (P) 1.1581; (R1) 1.1604; More...

No change in EUR/CHF's outlook. As long as 1.1639 minor resistance holds, deeper decline is expected. Fall from 1.1832 is correcting medium term rise from 1.0629. Next target will be 1.1355 cluster support (38.2% retracement of 1.0629 to 1.1832 at 1.1372.) On the upside, though, above 1.1639 will indicate short term bottoming and bring stronger recovery first.

In the bigger picture, a medium term top should be in place at 1.1832 on bearish divergence condition in daily MACD. But there is no indication of long term reversal yet. As long as 1.1198 resistance turned support holds, we'd still expect another rise through prior SNB imposed floor at 1.2000.

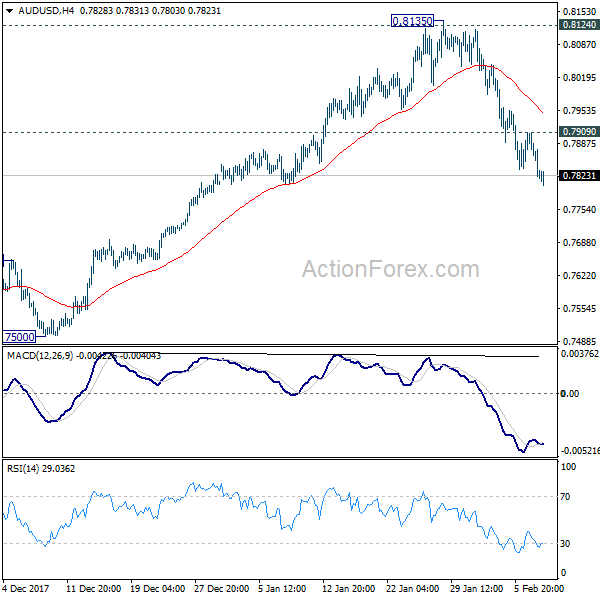

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7789; (P) 0.7848; (R1) 0.7881; More...

AUD/USD's decline from 0.8135 is still in progress and intraday bias remains on the downside. Sustained trading below 55 day EMA will argue that rise from 0.7500 has totally completed and will pave the way to retest this support level. Nonetheless, break of 0.7909 minor resistance will turn bias back to the upside for retesting 0.8135 high.

In the bigger picture, medium term rebound from 0.6826 is seen as a corrective move. It might still extend higher but we'd expect strong resistance from 38.2% retracement of 1.1079 to 0.6826 at 0.8451 to limit upside to bring long term down trend resumption. On the downside, break of 0.7500 support will now be an important signal that such corrective rebound is completed.