Sample Category Title

USD/CAD Might Make A U-Turn If 1.2560 Holds

The USD/CAD has been in a retracement mode but without an additional momentum to break recent highs. The pair is making a lower high now and if 1.2560 holds we might see a u-turn on the price. Targets are W H3 and W L3 levels - 1.2468 and 1.2376, but in the case you are trading intraday pay attention to W H1 - W L1 levels 1.2437 and 1.2405 respectively. A spike above 1.2560 could turn the price bullish again targeting 1.2606 and 1.2653.

W H1 -. Weekly Camarilla Pivot (Interim resistance - Weak)

W H2 - Weekly Camarilla Pivot (Weekly resistance)

W H3 - Weekly Camarilla Pivot (Weekly resistance - main)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

W L4 - Weekly Camarilla Pivot (Interim support - Strong)

W L3 – Weekly Camarilla Pivot (Interim support - Main)

W L2 – Weekly Camarilla Pivot (Interim support)

W L1 - Weekly Camarilla Pivot (Interim support - Weak)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Technical Outlook: WTI Oil Eases Further Following Brief Consolidation On Tuesday, EIA Report In Focus Today

WTI oil price fell to new three-week low at $63.03 on Wednesday, signaling continuation of steep decline from $66.28 on Fri/Mon, which was interrupted by consolidation phase on Tuesday. Fresh weakness probes again below cracked daily Kijun-sen ($63.46), looking for fresh bearish signal on close below. Pivotal support at $62.50 (Fibo 38.2% of $55.81/$66.64 upleg) is coming in focus and break here is needed to signal deeper correction. Scenario is supported by daily 10/20SMA's in bearish setup and momentum entering negative territory. API report on Tuesday showed a 1.05 million barrels drop in crude inventories, against expected build of 2.5 million barrels. Focus turns towards today's release of EIA crude stocks report which is forecasted for 3.18 million barrels build, the second increase in crude inventories (after last week's 6.77 million barrels build) following ten straight weeks of draws in crude stocks. Negative numbers today (further increase in oil stocks) would add on persisting pressure on oil prices due to recent strong fall in global stocks and rising fears on steady increase in US oil production which increased nearly 20% since mid-2016 and threatening to further distract efforts from major oil producers to stabilize oil market by reducing output.

Res: 63.46, 64.16, 64.46, 64.72

Sup: 63.03, 62.83, 62.50, 61.79

Euro, Pound Down As European Stocks Recover, Kiwi Slips Ahead Of RBNZ Rate Decision

Here are the latest developments in global markets:

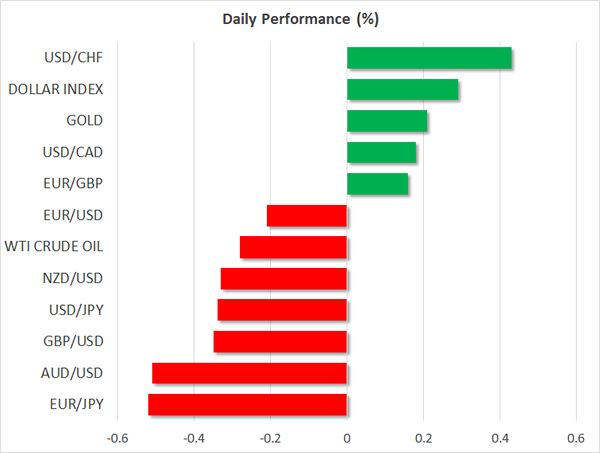

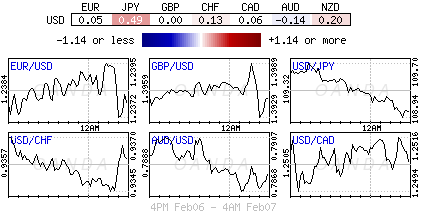

FOREX: The yen extended its uptrend against the dollar, sending dollar/yen lower to 109.10 as investors maintained their risk-averse behavior after the recent sell-off in stock markets. The dollar index, though, was building positive momentum on the back of a weaker euro and pound, climbing to 89.87 (+0.33%). Euro/dollar slipped to 1.2342 (-0.30%) and pound/dollar weakened to 1.3872 (-0.44%) after the ECB board member, Sabine Lautenschlaeger questioned whether the transitional period after Brexit will “really happen”, arguing that Britain-based banks have not yet submitted their license application to reallocate to the Euro area and the deadline was already ticking down. The antipodean currencies were on the backfoot as well. Aussie/dollar fell down to 0.7860 (-0.54%) and kiwi/dollar dropped to 0.7311 (-0.33%) ahead of the RBNZ policy meeting, unable to sustain gains from yesterday’s better-than-expected dairy prices and employment data. Dollar/swissie and dollar/loonie changed hands at 0.9398 (+0.43%) and 1.2513 (+0.20%) respectively.

STOCKS: European stocks managed to rebound after recent losses, following their US and Asian counterparts. The pan-European STOXX 600 and the blue-chip Euro STOXX 50 were almost 1.0% up at 1130 GMT, with every single sector comprising the indices being in the green. The German DAX 30 and the French CAC 40 were higher by 0.77%, the Italian FTSE MIB jumped by 1.05% and the British FTSE 100 increased by 0.75%. US stock futures were pointing to a positive open.

COMMODITIES: Oil prices pared earlier gains as concerns of a rising US output continued to weigh on the markets. WTI crude was last seen at $63.27/barrel (-0.20%) and Brent was lower at $66.80 (-0.09%). In precious metals, gold consolidated gains at $1328.43/ounce (+0.27%).

The aussie is viewed as a liquid proxy for China’s economy due to the two nations’ close economic ties – China is Australia’s largest export and import partner – and thus will also be gathering attention as the figures hit the markets.

Upbeat data could incentivize forex market participants to place long aussie/dollar positions. In this scenario, the pair might meet resistance around 0.7893, this being the 38.2% Fibonacci retracement level of the December 8 to January 26 upleg (0.7893 failed to provide support on the way down during Wednesday’s trading and could instead act as a barrier to the upside). This area also includes the 0.79 handle, a level of potential psychological significance. Further above, the focus would shift to the range around the 23.6% Fibonacci mark at 0.7986.

In case of weaker-than-anticipated figures however, aussie/dollar might head lower. Support in this case might come around the 50% Fibonacci mark at 0.7818 (including the 0.78 handle and the current level of the 50-day moving average). Steeper declines would shift the focus to the 61.8% Fibonacci level at 0.7743. Notice that the current level of the 200-day MA roughly coincides with this point. It should be pointed out that there is negative momentum at the moment for AUDUSD, with the pair looking set to finish the day lower on Wednesday after declining in all but one of the preceding seven trading days.

EURUSD Looking For Buyers Above 1.2400 Level

The euro has slipped lower during the European trading session, following its second technical rejection from the 1.2400 level. The EURUSD pair is currently trading around the 1.2370 region, as a marginal rebound in the value of the U.S dollar index and continued market jitters keep the pair's upside contained. Moving in to the U.S session, traders will look to the 1.2350 to 1.2400 price-range for confirmation of the EURUSD pairs next directional move.

The EURUSD pair will likely encounter further downside pressures below the 1.2350 level, intraday support is found at the 1.2313 and 1.2275 levels.

If the EURUSD pair can move above the 1.2400 technical level, upside objectives remain 1.2432, 1.2474 and 1.2500.

USDJPY Testing Pivotal 108.98 Level

The U.S dollar has lost ground against the Japanese yen in early Wednesday trading, falling back towards the pivotal 108.98 technical level. After seeing a strong relief rally towards the 109.71 level following a recovery in global equity prices, USDJPY price-action is now testing demand around the 109.00 zone. Going forward, risk-sentiment remains the key driver of the pair, as the Japanese yen currency is considered a major safe-haven asset in times of extreme market volatility.

The USDJPY pair remains bullish while price-action trades above the key 108.98 pivot, further upside towards the 109.44 level is still possible.

If the USDJPY pair falls below the 108.98 level, we may see a deeper correction back towards the 108.70 and 108.27 support levels.

Chinese Trade & Inflation Numbers On The Horizon, Attention On Aussie As Well

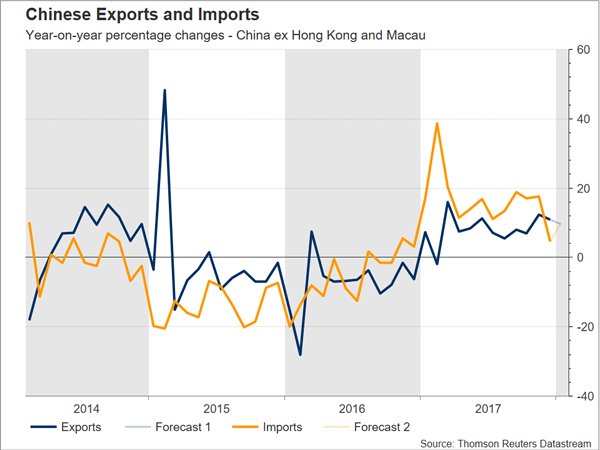

China will see the release of trade data for the month of January on Thursday, with analysts projecting both exports and imports to grow at a solid pace; the release is tentative, lacking a fixed time of release. Figures on January producer and consumer prices out of the world’s second largest economy will also be attracting attention on Friday. Both PPI and CPI are expected to soften on an annual basis.

Before delving into the analysis, it is worthy of mention that the long Lunar New Year celebrations taking place in China have the capacity to distort the various readings, thus one might be justified not to read so much into the trade data before and after the holiday. The Chinese New Year will be celebrated on February 16.

Exports and imports are anticipated to expand by 9.6% and 9.8% year-on-year in January respectively. These compare to a 10.9% export growth rate and a 4.5% import growth rate in December. The trade balance is forecast to narrow, reaching $54.10 billion from $54.69bn in December.

Despite the projected slowdown in export growth, a 9.6% pace of expansion – should it materialize – still translates into a strong reading and lends support to analysts making reference to improving global growth, which translates into rising demand for Chinese products. A factor potentially clouding the outlook for Chinese exports are rising trade disputes leading to the imposition of barriers to trade between the US and China. The Trump administration’s decision to impose tariffs on imported solar panels and washing machines in late January could be the prelude of what is to follow, while a tit-for-tat approach by China could see things escalating out of control. However, an escalating trade row between the world’s two largest economies doesn’t appear likely at the moment.

Turning to imports, those fell short of expectations in December by a relatively large margin, spurring concerns for a slowdown, something which would be troubling given the government’s efforts to rebalance the Chinese economy from the export-driven model of growth of the past to the one where domestically-driven consumption makes up a significant portion of the economic pie. If the actual reading comes as expected, January’s imports would grow at more than double December’s pace. This would be welcome news, though the increase is most likely to be attributed to inventory buildup ahead of New Year festivities, rather than reflect a rise in underlying demand. Moving forward, should the government’s attempts to curb risks in the financial system (in the form of excessive debt) intensify, this could pose downside risks on imports. However, such a move would likely contribute to the long-term sustainability of economic growth and subsequently imports by reducing the risk of a sharp slowdown due to a credit crisis getting out of hand.

The aussie is viewed as a liquid proxy for China’s economy due to the two nations’ close economic ties – China is Australia’s largest export and import partner – and thus will also be gathering attention as the figures hit the markets.

Upbeat data could incentivize forex market participants to place long aussie/dollar positions. In this scenario, the pair might meet resistance around 0.7893, this being the 38.2% Fibonacci retracement level of the December 8 to January 26 upleg (0.7893 failed to provide support on the way down during Wednesday’s trading and could instead act as a barrier to the upside). This area also includes the 0.79 handle, a level of potential psychological significance. Further above, the focus would shift to the range around the 23.6% Fibonacci mark at 0.7986.

In case of weaker-than-anticipated figures however, aussie/dollar might head lower. Support in this case might come around the 50% Fibonacci mark at 0.7818 (including the 0.78 handle and the current level of the 50-day moving average). Steeper declines would shift the focus to the 61.8% Fibonacci level at 0.7743. Notice that the current level of the 200-day MA roughly coincides with this point. It should be pointed out that there is negative momentum at the moment for AUDUSD, with the pair looking set to finish the day lower on Wednesday after declining in all but one of the preceding seven trading days.

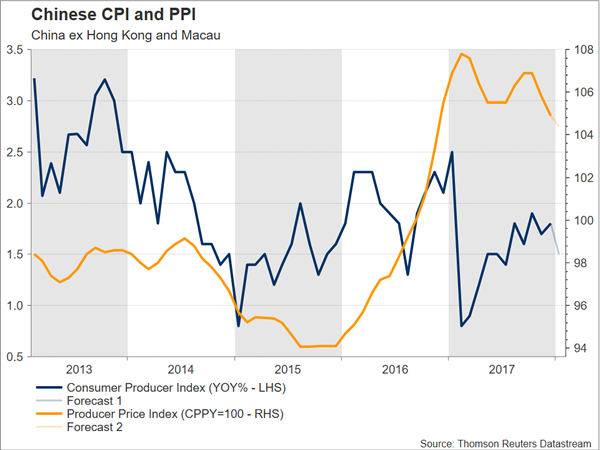

January produce and consumer figures out of China will be made public on Friday at 0130 GMT. CPI growth is projected to moderate to 1.5% y/y (versus 1.8% in December) and PPI growth is forecast to ease to 4.4% y/y (versus 4.9% in December). A slowdown in PPI would constitute the third straight month of declines, with the measure growing at its lowest since late 2016 if the reading is released in line with projections. Should annual CPI come in as expected, then it would stand at its lowest since July. Beyond yuan pairs, aussie pairs would again be eyed ahead of and in the aftermath of Chinese inflation data.

One hour before Chinese PPI and CPI numbers (at 0030 GMT), Australia will see the release of housing finance data for the month of December.

Forex Technical Analysis: EUR/USD, USD/JPY, GBP/USD

EUR/USD

Current level - 1.2396

The general bias is still bearish, for a dip to 1.2220 and 1.2160, but there is a minor risk of a break through 1.2435 crucial high, which will provoke another corrective leg to 1.2480 before drowning towards the mentioned projections.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.2440 | 1.2540 | 1.2330 | 1.2330 |

| 1.2475 | 1.2870 | 1.2220 | 1.2220 |

USD/JPY

Current level - 109.06

The recent climb was capped at 109.70 and current slide should be considered corrective, preceding another leg upwards, to 110.50 zone. Crucial on the downside is 108.30 low.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 109.70 | 111.90 | 108.30 | 108.30 |

| 111.50 | 113.40 | 108.30 | 107.30 |

GBP/USD

Current level - 1.3955

The overall bias remains bearish, for a slide towards 1.3730 and 1.3620 major static support. Key intraday resistance lies at 1.4000 and a violation of the latter will signal another corrective rebound to 1.4175 before drowning towards the mentioned targets.

| Resistance | Support | ||

| intraday | intraweek | intraday | intraweek |

| 1.4000 | 1.4090 | 1.3800 | 1.3730 |

| 1.4090 | 1.4174 | 1.3730 | 1.3620 |

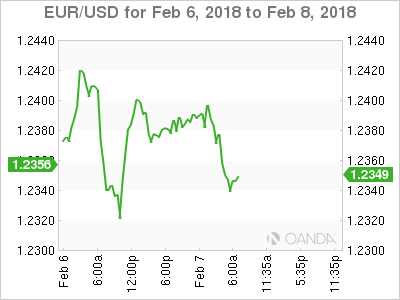

Euro Edges Lower As German Industrial Production Contracts

The euro has edged downwards on Wednesday. Currently, the pair is trading at 1.2343, down 0.27% on the day. On the release front, German Industrial Production declined 0.6%, close to the estimate of -0.7%. This marked the third decline in four months. There are no key releases out of the US. On Thursday, Germany releases Trade Balance and the US publishes unemployment claims.

It’s been a volatile week on the stock markets, with the Dow Jones posting its biggest 0ne-day loss on Monday. The markets were back in green territory on Tuesday. A key factor in the stock market slide was strong employment numbers on Friday, as nonfarm payrolls and wage growth reports beat their estimates. Investors shied away from the stock markets, concerned that the sharp data could lead to higher inflation, which in turn would result in more rate hikes this year. Higher interest rates make the dollar more attractive for investors, at the expense of the stock markets.

The Janet Yellen era is over at the Federal Reserve. On the weekend, Jerome Powell took over as chair, replacing Yellen. On Friday, Yellen waxed optimistic about the economy, saying that strong growth, a red-hot labor market and increased wage growth would require the Fed to gradually raise interest rates. Powell is expected to continue to Yellen’s policies, so the markets are not expecting any dramatic shifts. However, the massive US tax cut will have a strong impact on the US economy, and the markets will be looking to the Fed for guidance. If the Fed sounds optimistic about the tax reform package, the US dollar could move higher.

Beware: FX Space Is Calm, But Appearances Can Be Deceiving

Wednesday February 7: Five things the markets are talking about

Risk-averse sentiment seems to have cooled for the time being as a number of the major indexes rebound in the overnight session.

Note: From a volatility standpoint, the forex market space appears tranquil when compared to other asset classes like equities or bonds.

The rebound in equity prices has spread to Europe, but capital markets remain on edge as Asian bourses pared their advance while U.S futures retreated.

Elsewhere, U.S Treasuries have rebounded after yesterday's slump along with gold and crude prices. The dollar has edged a tad lower as the FX market showed limited reaction to the sharp drop in equities earlier this week.

In Germany, the CDU/CSU, SPD political parties are said to have agreed on a grand coalition treaty.

Up next: Monetary policy decisions are due this week in New Zealand (Today 03:00 pm EDT) and tomorrow in the U.K (07:00 am EDT).

1. Some stocks record small gains

In Japan, equities pared early gains to end a tad higher overnight in a volatile trading session, as investors remained wary of further losses as U.S futures slipped from their highs. The Nikkei 225 share average ended +0.2% higher, while the broader Topix gained +0.4%.

Down-under, Aussie shares rebounded after Tuesday's biggest one-day drubbing in roughly 24-months. Broad-based buying helped the S&P/ASX 200 index end up +0.8%. The benchmark slumped -3.2% in the previous session. In S. Korea, the Kospi index dropped more than -2%.

In Hong Kong, equities reversed their earlier gains and closed at a five-week low overnight, led lower by material and real estate firms. At close of trade, the Hang Seng index was down -0.89%, while the Hang Seng China Enterprises index fell -2%.

In China, stocks slumped as developers and consumers fall. At the close, the Shanghai Composite index was down -1.81%, while the blue-chip CSI300 index was down -2.38%.

In Europe, regional bourses have rebounded from Monday's sharp sell off, mirroring Wall Streets moves. However, U.S stock futures (-0.8%) are pointing lower once again as volatility continues.

Indices: Stoxx600 +0.8% at 375.9, FTSE +0.6% at 7187, DAX +0.7% at 12474, CAC-40 +0.6% at 5191, IBEX-35 +0.6% at 9869, FTSE MIB +0.8% at 22518, SMI +1.0% at 8926, S&P 500 Futures -0.8

2. Oil steadies, as lower inventories offset by higher U.S output, gold higher

Oil prices are holding steady, as the boost from a report showing a drop in U.S crude inventories last week was offset by evidence of soaring U.S output.

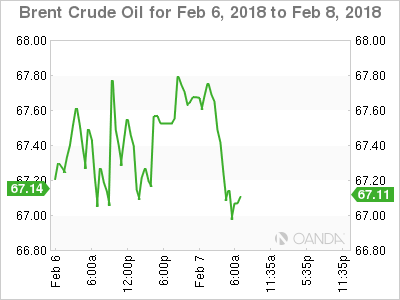

Brent crude futures are down -11c to +$66.75 a barrel, while U.S West Texas Intermediate (WTI) crude futures have eased -12c to +$63.27 a barrel.

Data yesterday showed that U.S. crude inventories fell by -1.1m barrels in the week to Feb. 2 to +418.4m barrels, helping support the commodity.

However, rising U.S oil production continues to hang over the market. EIA data shows that U.S output has risen by +1m bpd in the last year to about +10m bpd.

Investors will take their cue from todays EIA crude stock report (10:30 am EDT).

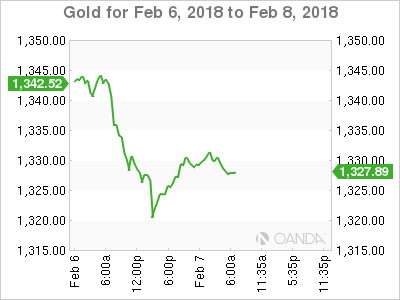

Ahead of the U.S open, gold prices have rallied from their three-week low on bargain hunting. Spot gold is up +0.5% to +$1,331.23 per ounce. Prices fell over -1% yesterday to hit its lowest since Jan. 11 at +$1,319.96.

3. Sovereign yields fall

In the Euro session, southern European government bond yields have fallen sharply and have extended their recent outperformance on news of a coalition agreement in Germany viewed as positive for Euro integration.

Germany's Chancellor Merkel's conservatives and the Social Democrats (SPD) have agreed “in principle” on a coalition deal. This will take Europe's economic powerhouse a step closer to a new government. Germany's 10-year Bund yield has climbed +1 bps to +0.70%.

Italian, Spanish and Portuguese 10-year government bond yields are -5 to -8 bps lower, and spreads over benchmark German Bunds have tightened.

Elsewhere, the yield on 10-year U.S Treasuries has dipped -4 bps to +2.76%, while in the U.K, the 10-year Gilt yield has advanced less than +1 bps to +1.523%.

Overnight, in India the Reserve Bank of India (RBI) statement noted that the decision to keep policy steady (+6%) was not unanimous (5-1) with a dissenter calling for +25 bps hike. It maintained its neutral monetary policy stance and reiterated to keep headline inflation close to +4% target on a durable basis.

4. Dollar has 'little traction'

From a volatility standpoint, the forex market space appears tranquil when compared to other asset classes like equities or bonds. The U.S dollar continues to be confined to its recent ranges against G10 currency pairs.

The EUR/USD (€1.2346) is a tad lower despite market reports of a grand coalition agreement in Germany. The pair continued to find headwinds above the psychological €1.24 level.

GBP/USD (£1.3884) continues to face headwinds as various press outlets noted that the E.U is prepared to harden its stance during the transition phase of negotiations.

USD/JPY (¥109.07) remains the liveliest of currency pairs, as risk-on and risk-off continues to find capital market leverage.

Note: The Nikkei 225 index did see its initial +2% gain disappear in the final hour of trading.

5. German industrial output slips

Data from Europe this morning revels that Germany's industrial output slipped at the end of 2017.

Industrial production in December fell -0.6% m/m, led by construction output. Market consensus was looking for a -0.5% decline.

Germany's economics ministry said manufacturers' order books signal vigorous production in the coming months. The trend is “clearly pointing up” after reporting a +3.8% monthly gain in manufacturing orders in December on Tuesday.

Global Equity Bulls Fight Back, Dollar Steady

Investors experienced a renewed sense of confidence on Wednesday morning following Wall Street's rebound overnight.

Asian stocks closed mostly mixed during early trading, while European shares ventured higher, as markets attempted to shake off the volatility and jitters witnessed in recent trading sessions. With the shocking levels of volatility limited to stock markets and not materially impacting currencies or commodities, the aggressive global equity sell-off could just be a steep correction. However, repeated weakness across stock markets may leave investors on high alert and on guard for something greater than a steep correction.

Dollar Index little changed

The Dollar remained steady against a basket of major currencies on Wednesday, as investors diverted most of their focus towards the development happening across stock markets. Sentiment towards the Dollar received a boost last week, after the stronger-than-expected growth in U.S. wages fueled speculations of higher U.S. interest rates. The Greenback has scope to appreciate further if economic data from the United States continues to beat market expectations. Taking a look at the technical picture, the Dollar Index has breached above the 89.50 lower high. The breakout above this level may encourage a further incline towards 90.00 and 90.55. Alternatively, a failure for prices to break above 90.00 could encourage a decline back to 89.50 and 89.00, respectively.

Commodity spotlight – WTI

WTI Crude found itself under noticeable selling pressure during Wednesday's trading session, amid ongoing concerns over soaring U.S. production weighing heavily on oil prices.

Although oil markets were initially supported on Tuesday after the American Petroleum Institute (API) reported an unexpected weekly decline in U.S. Crude stocks, gains were later relinquished by the oversupply fears. While price action continues to suggest that oil still has some upside momentum, gains could be capped by rising U.S. output. Focusing on the technical picture, WTI Crude is at risk of depreciating towards $62.20 if bears are able to conquer the $63.00 support level. In an alternative scenario, a breakout above $64.00 may re-open a path back towards $65 and $65.60.

Currency spotlight – EURUSD

The EURUSD edged lower during Wednesday's trading session with prices sinking towards 1.2350 as of writing.

With the bullish sentiment towards the European economy stimulating appetite for the Euro, the EURUSD remains heavily supported. From a technical standpoint, the EURUSD is in the process of a technical correction on the daily charts with 1.2300 acting as a level of interest. Price remains above the 50 Simple Moving Average, while the MACD trades to the upside. A creation of a new higher low around the 1.2300 region could be in play,which may provide a foundation for bulls to elevate prices higher. A breakdown and daily close below the 1.2300 level may inspire a decline towards 1.2180. Alternatively, if 1.2300 defends then the EURUSD could venture back to 1.2440.