Sample Category Title

Sunset Market Commentary

Markets:

The German Bund and US Note future traded volatile today, but are currently near opening levels. The short squeeze triggered by yesterday's huge sell-off on (US) stock markets didn't gain traction. Both markets are trying to reach a new short term equilibrium. European equities opened significantly lower, but didn't suffer additional losses. US stock markets opened with small losses. The eco calendar was empty apart from a bigger-than-expected US trade deficit which didn't impact trading. US yields add 4.5 bps (2-yr) to 6.7 bps (10-yr) at the time of writing. The US 10-yr yield retested the previous range top at 2.63%/2.64%, but rebounded higher. The German yield curve bull flattens with yields 0.2 bps (2-yr) to 3.1 bps (30-yr) lower. 10-yr yield spread changes versus Germany are nearly unchanged with Greece and Portugal underperforming (+7 bps). Greece held off launching a new 7-yr deal, probably because of increased market volatility.

The dollar still showed a diffuse picture this morning. EUR/USD tried to rebound after yesterday's correction during the equity sell-off. Strong German order data were a minor positive. More important, European equities opened with substantial losses, but the decline (about 2.5%/3.0% soon after the open) was not excessive given the price moves yesterday evening. This was also slightly euro supportive. EUR/USD filled offers in the 1.2430 area. At the same time, USD/JPY remained well bid. The pair held a tight range close to most slightly north of 109. The yen again didn't profit from the rise in global volatility as Japanese official reiterated their commitment to keep an easy monetary policy. Around noon, the dollar received a better bid across the board. Interest rate differentials widened slightly in favour of the dollar. Technical considerations were also in play. The US trade deficit was bigger than expected, but largely ignored. EUR/USD tested first intermediate support at 1.2323/35, but no break occurred (yet). A break would ease the upside pressure. USD/JPY is trending cautiously higher in the 109 big figure.

In nervous trade, EUR/GBP jumped up and down in the upper half of the 0.88 big figure and currently tries to clear the 0.89 mark. There was little 'new' news for sterling traders. With the Brexit procedure, one never knows, but recent comments from UK politicians suggest that a soft Brexit is becoming unlikely. This factor remains a negative for the UK currency. The 0.8928 intermediate resistance is coming with reach. The decline in cable is reinforced by a cautious comeback of the dollar. The pair dropped well below the 1.39 big figure. There are only second tier eco data in the UK tomorrow. Markets are counting down to Thursday's BoE meeting. Will Carney and Co keep the door open for the rate hike later this year even as chances on a hard Brexit are growing? This week's PMIs weren't really reassuring on the prospects for the UK economy in the short-to-medium term.

News Headlines:

German industrial orders surged a stronger than expected 3.8% in January, supporting expectations that Europe's largest economy is on track for a good start of 2018 after expanding by 2.2% in 2017. Export orders, especially orders from the rest to the euro zone were an important factor behind to strong order data.

The US trade deficit widened more than expected in December to $53.1bn, hitting its highest level since 2008. Robust domestic demand pushed imports to a record high. Part of the rise in the trade gap reflected commodity price increases. The deficit surged to $566.0 bn in 2017, the highest since 2008. The politically sensitive US-China trade deficit increased 8.1% to a record $375.2 billion last year.

A Scottish court rejected a legal attempt to ask the European Court of Justice (ECJ) to clarify whether Britain could unilaterally stop the Brexit process

Dollar Higher as Global Stock Market Rout Extends

Quick update: DOW seems to be finally getting some support around 24000 handle. It's recovering after dipping to 23778.74 and is up 1.2% at the time of writing. Let's see how it goes.

Global stock markets selloff continues today. At the time of writing, all major European indices are trading in red. FTSE 100 is down -1.9%, DAX down -2.4% and CAC 40 down -2.7%. DOW just had the biggest single day point drop yesterday. US futures suggest the selloff is going to continue, at least in the early part of today's US session. In the currency markets, Dollar is trading broadly higher today, but overwhelmed by New Zealand Dollar. Yen follows closely as the third strongest today, but the strongest for the week. Notable weakness is seen in European majors.

Economic data are talking a back seat today. US trade deficit widened to USD -50.4b in December. Canada trade deficit widened to CAD -3.19b in December. Eurozone retail PMI dropped from 53.0 to 50.8 in January. German factory orders rose 3.8% mom in December. Australia retail sales dropped -0.5% mom in December, trade balance indicated AUD -1.36b deficit in December.

German Merkel to make painful comprises in turbulent times

German Chancellor Angela Merkel is still in overtime coalition negotiation with SPD today. Merkel said that "each of us will have to make painful compromises and I am ready for that." Specifically, she pointed to the "the movements on the stock markets over the last hours" and said "we live in turbulent times". Andreas Scheuer, secretary general of CSU said "we have to come to an agreement tonight. Anything else would be unreasonable for our citizens." SPD negotiator Carsten Schneider said a deal was close and "we have 90-95 percent".

BoJ Kuroda: Inappropriate to hike or even lift yield target

BoJ Governor Haruhiko Kuroda ruled out the possibility of an early hike today. He said that "Japanese inflation hasn't even reached 1 percent. As such, it's inappropriate to prematurely shift monetary policy just to create future policy space." He further added that "it's inappropriate to raise our 10-year government bond yield target now, even by a small margin." Also Kuroda downplayed recent stock market routs and said the recovery in Japan, US and Europe is "broadening across sectors and the outlook remains good as a trend."

RBA stands pat, upbeat over economic outlook

RBA maintained cash rate unchanged at 1.50%. The decision had been widely anticipated. As suggested in the accompanying statement, the central bank continued to see positive economic developments both globally and at home. Policymakers have turned slightly more upbeat over the domestic growth outlook, projecting GDP to expand 'a bit above 3% over the next couple of years'. Meanwhile, RBA revealed that the central forecast for CPI is 'a bit above 2% in 2018. This marks a more hawkish tone when compared with December's language. While the job market has improved a lot, with the unemployment rate falling to the lowest level in 4.5 years, wage growth has remained lackluster. This has raised concerns over household expenditure. More in RBA Left Policy Rate At 1.5%, More Upbeat Over Growth And Inflation Outlook

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3890; (P) 1.4020; (R1) 1.4088; More.....

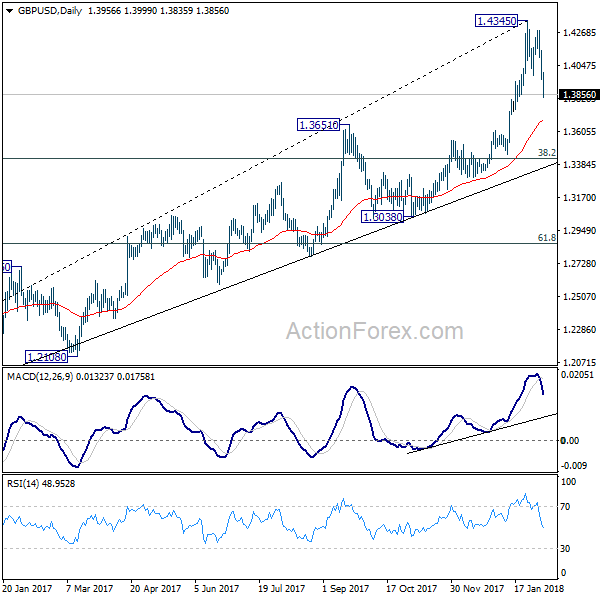

GBP/USD's decline accelerates to as low as 1.3835 today and breaks 1.3915 support. The development suggests that a short term top is at least formed at 1.4345 and deeper decline should be seen. Intraday bias is now on the downside for 1.3651 resistance turned support. For the moment, it's unsure where the decline is corrective rise from 1.3038, or that from 1.1946, or it's reversing the trend. Break of 1.3651 will turn to key fibonacci level at 1.3429. On the upside, above 1.3999 minor resistance will turn intraday bias neutral first.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish 38.2% retracement of 1.1946 to 1.4345 at 1.3429, in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:01 | GBP | BRC Sales Monitor Y/Y Jan | 0.60% | 0.70% | 0.60% | |

| 00:30 | AUD | Trade Balance Dec | -1.36B | 0.25B | -0.63B | 0.04B |

| 00:30 | AUD | Retail Sales M/M Dec | -0.50% | -0.20% | 1.20% | 1.30% |

| 03:30 | AUD | RBA Rate Decision | 1.50% | 1.50% | 1.50% | |

| 07:00 | EUR | German Factory Orders M/M Dec | 3.80% | 0.70% | -0.40% | -0.10% |

| 09:10 | EUR | Eurozone Retail PMI Jan | 50.8 | 53 | ||

| 13:30 | CAD | International Merchandise Trade (CAD) Dec | -3.19B | -2.3B | -2.5B | -2.71B |

| 13:30 | USD | Trade Balance Dec | -53.1B | -52.1B | -50.5B | -50.4B |

| 15:00 | CAD | Ivey PMI Jan | 55.2 | 60.7 | 60.4 |

US 30 Index Posts Steep Losses; Near 3-Month Low

The US 30 index has plunged sharply lower since Friday losing more than 3000 points from the last all-time high on January 29. The price posted a new more than 3-month low of 23116.40 earlier today, however, it later reversed some of its losses during the European session.

Prices broke below the 23.6% Fibonacci retracement level near 24000 of the up-leg with the low of 15250 and the high of 26700. The bullish picture in the medium-term weakened and a bearish correction is in progress.

Short-term indicators are also pointing to a continuation of the bearish bias. The RSI indicator entered the oversold area following the pullback from the overbought zone. Also, the MACD oscillator dropped below the zero line with an aggressive move.

Should prices reverse lower, immediate support could come again at 23220, which it hit earlier in the day. A drop below this area could take the index closer to the 38.2% Fibonacci mark slightly above the 22200 strong support level. A breach of this level would shift the outlook from positive to negative.

On the flip side, if prices reverse and jump above the 23.6% Fibonacci could open the way towards the next key resistance at 24500. Rising above the aforementioned obstacle could see prices re-test the all-time high at 26700.

Canada’s Trade Deficit Widened in December

Canada's trade deficit widened to $3.2B in December (previously $2.7B), as the 1.5% rise in imports outpaced the 0.6% gain in exports. In real terms, imports were up 1% while exports were flat during the month.

The rise in imports was fairly widespread, but led by a 17% increase in energy products. Industrial machinery and equipment imports (+6%) also posted a solid gain, while aircraft and other transportation equipment (-23%) provided some offset.

Exports rose for a third straight month, led by a bounce back in energy products (+6.2%) which were restrained in November by pipeline disruptions. Metal ores and non-metallic minerals (+8%) were also up in December, while exports of consumer goods (-8%) and industrial machinery and equipment (-4%) recorded the largest declines.

Canada's trade surplus with the US widened to $3.4B in December (previously $3.3B), as imports (-1.3%) fell more than exports (-0.8%). Canada's trade deficit with the rest of the world widened to $6.6B (previously $6.0B) as the 4.9% increase in exports trailed the 6.8% gain in imports.

Key Implications

For the fourth quarter as a whole, import volumes were up 1.2% while export volumes edged up by a mere 0.3%. As such, net trade will be a drag on growth during the quarter. Still, overall growth in Q4 is on track to come in at a healthy pace of about 2.2%.

Going forward, stronger export demand – propped up by robust US growth and a still-low Canadian dollar (expected to hover around 80 US cents) should enable trade to contribute favourably to growth. However, the NAFTA renegotiations pose some risk, with another round of talks set for February and March. Having said that, there is unlikely to be any impact on trade between the signatory countries in the near term.

The Bank of Canada will be disappointed by Canada's trade performance at the end of 2017. While other indicators have been more supportive of growth, the Bank is likely to remain on the sidelines until the summer as it assesses the impacts of shocks to the economy, including the implementation of updated B20 measures and provincial minimum wage hikes.

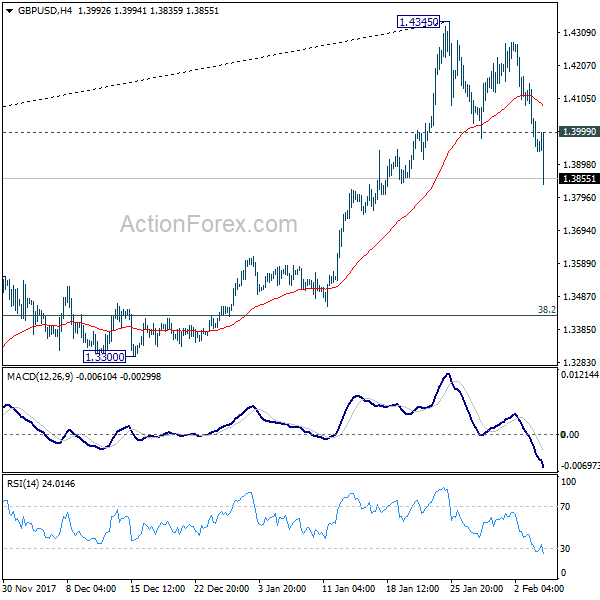

GBPUSD Strongly Bearish Below 1.3985 Level

The British pound has fallen sharply lower against the U.S dollar, hitting 1.3940 in early Tuesday trading, with price-action dropping over two-hundred pips since the Monday. The move lower has been sparked by extreme risk-off sentiment in financial markets, with traders moving into the perceived safety of the U.S dollar. Selling momentum in the GBPUSD is continuing to accelerate as sentiment worsens, volatility in the pair is expected to pick-up as we move into the U.S trading session.

The GBPUSD pair remains strongly bearish while trading below the 1.3985 level, further losses towards 1.3915 and 1.3870 are expected.

Should price-action on the GBPUSD pair start to move above the 1.3985 level, the 1.4058 and 1.4100 levels become the most relevant intraday resistance area.

EURUSD Under Heavy Selling Below 1.2350 Level

The euro has continued to sink lower against the greenback during the European trading session, after being swiftly rejected for the 1.2432 resistance level. The EURUSD is currently trading around the 1.2360 region, with the pair now approaching key downside technical support. Further heavy selling in European stock bourses has accelerated the sell-off in the euro, as traders move into safe-haven currencies such as the United States dollar, Swiss franc and Japanese yen.

The EURUSD pair is likely to see further intraday selling below the 1.2350 support level, downside targets remain 1.2322 and 1.2275.

If EURUSD price-action can hold above the 1.2350 level, we may see a further upside attempt at the pivotal 1.2400 level.

Canadian Dollar Under Pressure as Global Stock Markets Slide

The Canadian dollar is steady in the Tuesday session, after considerable losses in the past two sessions. Currently, the pair is trading at 1.2556, up 0.16% on the day. On the release front, Canada's trade deficit widened to C$2.3 billion, missing the estimate of C$2.3 billion. The US trade deficit also widened, climbing to $53.1 billion and missing the forecast of $52.1 billion. Later in the day, Canada releases Ivey PMI, which is forecast to improve to 60.7 points. In the US, the key event of the day is JOLTS Job Openings, which is expected to climb to 5.95 million. On Wednesday, Canada releases Building Permits.

The US dollar continues to post broad gains this week, and the Canadian dollar has declined 1.0% and is at its lowest level since mid-January. The greenback has pushed higher as global stock markets are in red territory. US stock markets started the week with strong losses, and the Dow Jones posted its biggest loss in one day on Monday, losing 1,500 points at one stage. The index ended the day down 4.6%, and the downward trend has continued in the Asian and European markets on Tuesday. As investors head for the hills, analysts are scrambling to find the reasons behind the massive sell-off in the stock markets. Some experts are pointing to the changing of the guard at the Federal Reserve, with Jerome Powell replacing outgoing chair Janet Yellen on Saturday. However, Powell is not expected to change current monetary policy, so it's unclear how Powell would have rubbed the markets the wrong way after just one day at his new job.

A more likely explanation for the sell-off can be attributed to strong US nonfarm payrolls and wage growth reports, which were released on Friday. Investors fear that the sharp data could lead to higher inflation, which in turn would result in more rate hikes this year. Higher interest rates make the dollar more attractive for investors, at the expense of the stock markets. Adding to investors' concerns, there are expectations that the ECB and possibly the Bank of Japan could raise rates late in 2018, which would push up the euro and yen and weigh on the stock markets.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 108.65; (P) 109.46; (R1) 109.94; More...

USD/JPY is supported above 108.27 and rebounded. Intraday bias is turned neutral first. Current development argues that larger fall from 114.73 is not completed. Break of 108.27 will resume the medium term correction from 118.65. That will send USD/JPY through 107.31 to 106.48 fibonacci level. Nonetheless, above 110.47 will turn intraday bias back to the upside and bring stronger rebound.

In the bigger picture, current development argues that the corrective pattern from 118.65 is extending. There is risk of dropping further to 61.8% retracement of 98.97 to 118.65 at 106.48. But this level should provide strong support to contain downside and bring resumption of rise from 98.97. However, sustained break of 106.48 will now likely send USD/JPY through 98.97 to resume the corrective fall from 125.85 (2015 high).

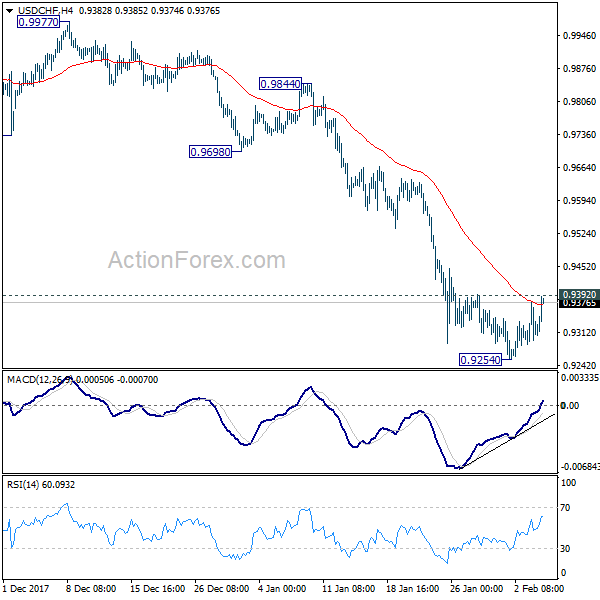

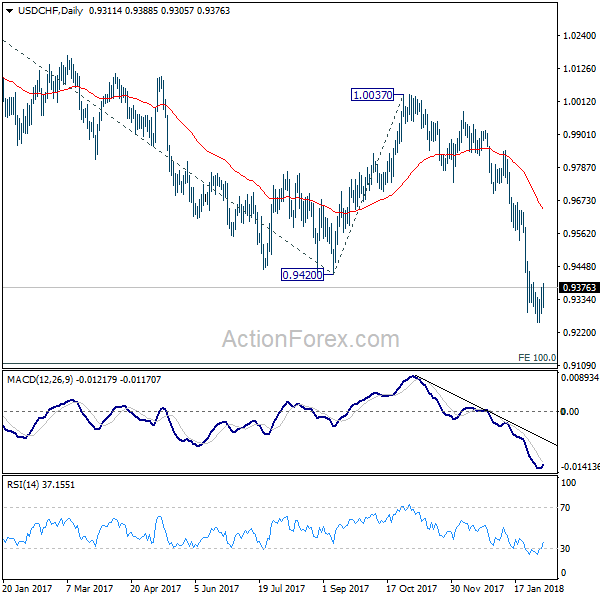

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9259; (P) 0.9298; (R1) 0.9345; More...

At this point, USD/CHF is staying below 0.9392 minor resistance and intraday bias remains neutral. On the downside, break of 0.9254 will extend recent fall from 1.0037 to next fibonacci projection level at 0.9115. On the upside, break of 0.9392 minor resistance, however, will indicate short term bottoming on bullish convergence condition in 4 hour MACD. That will bring stronger rebound back to 0.9420 support turned resistance and above.

In the bigger picture, the strong break of 0.9420 support suggests that fall from 1.0342 is developing into a medium term down trend. Deeper fall should be seen to 100% projection of 1.0342 to 0.9420 from 1.0037 at 0.9115. Break will target 161.8% projection at 0.8545. In any case, break of 0.9640 resistance is needed to be the first sign of medium term bottoming. Otherwise, outlook will stay bearish even in case of strong rebound.

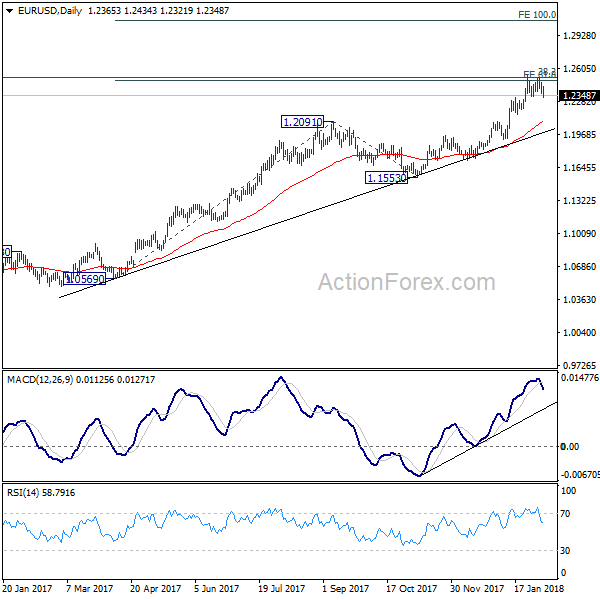

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2327; (P) 1.2401 (R1) 1.2439; More....

EUR/USD is still staying in consolidation below 1.2537 and intraday bias remains neutral. As long as 1.2222 support holds, further rise is in favor. Sustained break of 1.2494/2516 will target 100% projection of 1.0569 to 1.2091 from 1.1553 at 1.3075 next. However, break of 1.2222 will indicate rejection from 1.2494/2516, on bearish divergence condition in 4 hour MACD, and turn near term outlook bearish for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. But key fibonacci level at 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 is looking vulnerable. Sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862. Nonetheless, rejection from 1.2516 will maintain long term bearish outlook and keep the case for retesting 1.0039 alive.