Sample Category Title

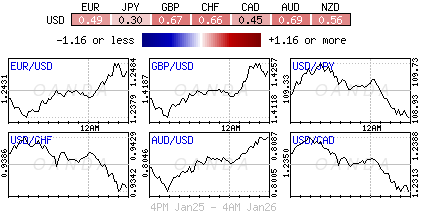

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4031; (P) 1.4188; (R1) 1.4294; More.....

Intraday bias in GBP/USD remains neutral for consolidation below 1.4345 temporary top. More sideway trading could be seen with risk of another fall. But downside of retreat should be contained above 1.3651 resistance turned support and bring another rise. Above 1.4345 will extend medium term rally to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Dollar Remains Range Bound Despite GDP Miss, But Lacks Momentum for More Rebound

Dollar stays steadily in range in early US session after mixed economic data. Q4 GDP showed only 2.6% qoq growth, missing expectation of 3.0% qoq. Though, GDP price index rose 2.4%, above expectation of 1.3%. Headline durable goods orders rose 2.9% in December, well above expectation of 0.9%. Ex-transport orders rose 0.6%, inline with consensus. Trade deficit widened to USD -71.6b in December. Wholesale inventories rose 0.2% mom in December.

Selloff in the greenback accelerated earlier this week after Treasury Secretary Steven Mnuchin said a weak Dollar is good for trade and opportunities. That was taken by the markets as an endorsement of a weak dollar policy. But the greenback gained some footing after President Donald Trump said he wants to see a strong Dollar. For the moment, there is no sign of reversal yet. Today's recovery could just be consolidations after selling momentum got exhausted.

Also released in US session. Canada CPI slowed to 1.9% yoy in December, in line with expectation. CPI core-trimmed rose to 1.9% yoy. CPI core-common rose to 1.6% yoy. CPI core median was unchanged at 1.9% yoy. USD/CAD is range bound after the release.

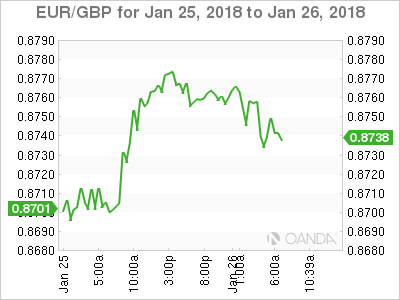

UK GDP rose 0.5% qoq in Q4, accelerated from prior quarter's 0.4% qoq and beat expectation of 0.4% qoq. Index of services rose 0.4% 3mo3m in November. Sterling is the second strongest currency for the week, just next to Swiss Franc. And it also looks like Sterling's rally is getting exhausted for now. Also fro Europe, Eurozone M3 rose 4.6% mom yoy in December.

Released earlier today, Japan national CPI core was unchanged at 0.9% yoy in December. Tokyo CPI core slowed to 0.7% yoy in January. Corporate services price rose 0.8% yoy in December.

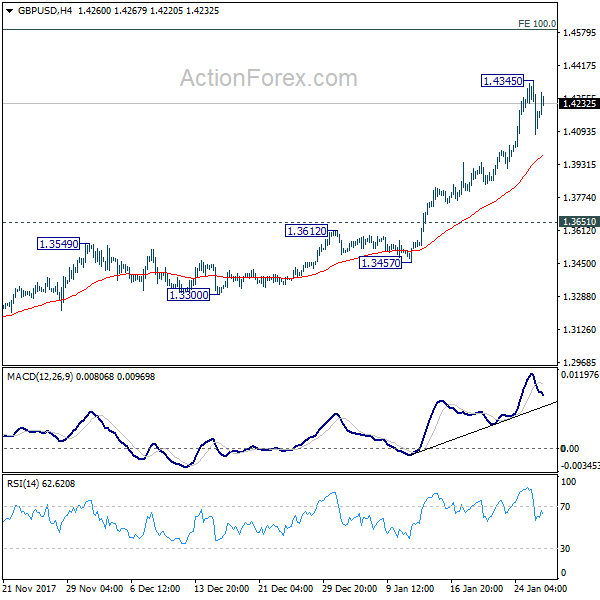

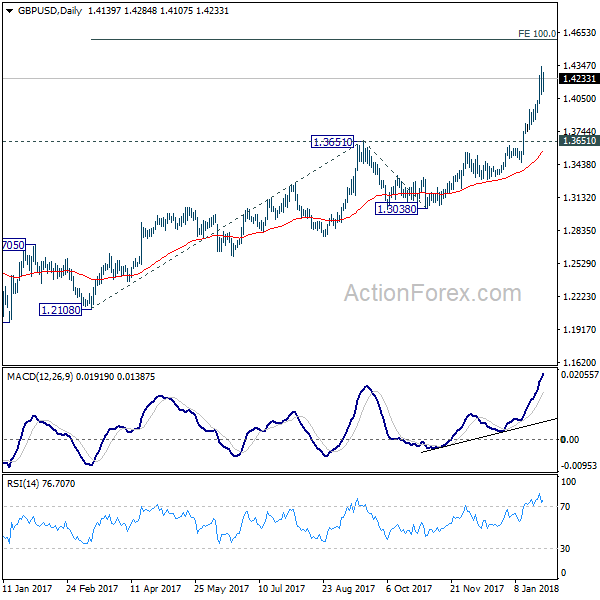

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.4031; (P) 1.4188; (R1) 1.4294; More.....

Intraday bias in GBP/USD remains neutral for consolidation below 1.4345 temporary top. More sideway trading could be seen with risk of another fall. But downside of retreat should be contained above 1.3651 resistance turned support and bring another rise. Above 1.4345 will extend medium term rally to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next.

In the bigger picture, sustained break of 1.3835 key resistance level indicates that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. Further rise should now be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Medium term outlook will stay bullish as long as 1.3038 support holds, in case of pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | National CPI Core Y/Y Dec | 0.90% | 0.90% | 0.90% | |

| 23:30 | JPY | Tokyo CPI Core Y/Y Jan | 0.70% | 0.80% | 0.80% | |

| 23:50 | JPY | Corporate Service Price Y/Y Dec | 0.80% | 0.80% | 0.80% | |

| 23:50 | JPY | BOJ Minutes | ||||

| 09:00 | EUR | Eurozone M3 Money Supply Y/Y Dec | 4.60% | 4.90% | 4.90% | |

| 09:30 | GBP | Index of Services 3M/3M Nov | 0.40% | 0.40% | 0.30% | |

| 09:30 | GBP | GDP Q/Q Q4 A | 0.50% | 0.40% | 0.40% | |

| 13:30 | CAD | CPI M/M Dec | -0.40% | -0.30% | 0.30% | |

| 13:30 | CAD | CPI Y/Y Dec | 1.90% | 1.90% | 2.10% | |

| 13:30 | CAD | CPI Core - Trimmed Y/Y Dec | 1.90% | 1.80% | ||

| 13:30 | CAD | CPI Core - Common Y/Y Dec | 1.60% | 1.50% | ||

| 13:30 | CAD | CPI Core - Median Y/Y Dec | 1.90% | 1.90% | ||

| 13:30 | USD | GDP Annualized Q/Q Q4 A | 2.60% | 3.00% | 3.20% | |

| 13:30 | USD | GDP Price Index Q4 A | 2.40% | 2.30% | 2.10% | |

| 13:30 | USD | Durable Goods Orders Dec P | 2.90% | 0.90% | 1.30% | |

| 13:30 | USD | Durables Ex Transportation Dec P | 0.60% | 0.60% | -0.10% | |

| 13:30 | USD | Advance Goods Trade Balance Dec | -71.6B | -68.6B | -70.0B | |

| 13:30 | USD | Wholesale Inventories M/M Dec P | 0.20% | 0.30% | 0.80% |

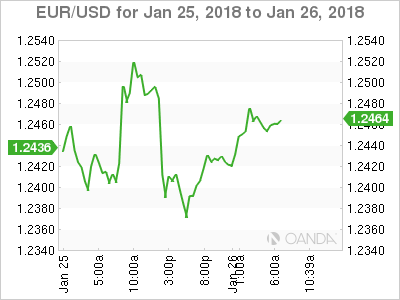

EURUSD Traders Still Focused on 1.2432 Level

The euro has remained consistent with the recent strong uptrend against the greenback, with price-action climbing back towards the 1.2500 level, following a weakening of the U.S dollar index back below the 89.00 mark. The EURUSD has so far found intraday resistance at the 1.2493 level, with pair now trading around the 1.2460 level. Moving into the U.S session, traders will look to U.S GDP and Trade Balance figures, and U.S President Donald Trump's scheduled speech at the World Economic Forum.

The EURUSD pair remains intraday bullish while trading above the 1.2432 level, key resistance is set at the 1.2493 and 1.2537 levels.

If the EURUSD pair starts to trade under the 1.2432 level for a sustained period, sellers may push price towards the 1.2400 and 1.2364 levels.

GBPUSD Intraday Bullish Above 1.4190 Level

The GBPUSD pair remains intraday bullish while trading above the 1.4190 level, further upside towards 1.4286 and 1.4345 seems possible.

Should price-action on the GBPUSD pair decline below the 1.4190 level, sellers may test towards the 1.4160 and 1.4100 support regions.

Dollar Surrenders Trump-Related Gains ahead of Key Data and Speeches

Here are the latest developments in global markets:

FOREX: The dollar has remained on the back foot, with the dollar index being almost 0.6% lower, giving back nearly all the gains it posted yesterday following President Trump's comments. The biggest beneficiaries of the greenback's weakness were the Swiss franc and the British pound, both trading 0.8% higher against the USD. The Australian dollar followed closely, with aussie/dollar up 0.7%. Dollar/loonie was down more than 0.5%, weighed on by a weaker greenback and elevated oil prices.

STOCKS: European stocks were a sea of green at 1130 GMT. The blue-chip Euro STOXX 50 was up 0.4%, while the pan-European STOXX 600 was nearly 0.5% higher. The charge was led by the French CAC 40, up almost 0.9% in the day, while the British FTSE 100 was 0.5% higher. Meanwhile, the German DAX 30 was practically flat.

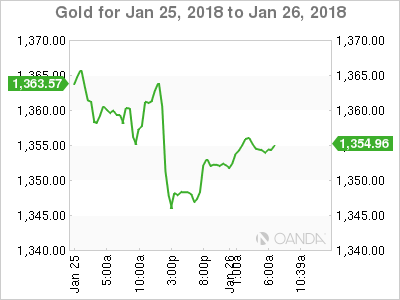

COMMODITIES: Oil prices erased their earlier losses and rebounded, with WTI and Brent crude both up by 0.2%. Later today at 1800 GMT, the Baker Hughes US oil rig count could provide markets with some clues as to whether US production has started to rise again in the face of higher prices. Elsewhere, gold was more than 0.4% higher, as the pullback in the USD helped to make the dollar-denominated precious metal appear more attractive.

Day ahead: US GDP and Canadian inflation prints due out; Davos speeches eyed

Economic releases will be in the spotlight during the European afternoon on Friday, with markets likely to focus predominantly on US GDP growth and Canadian inflation data. After that, attention will shift to Davos, where US President Donald Trump, BoE Governor Mark Carney, and BoJ Governor Haruhiko Kuroda, will all deliver remarks.

In the US, the preliminary estimate of GDP for the final quarter of 2017 is due at 1330 GMT, and expectations are for economic growth to have slowed to 3.0% on an annualized basis, from 3.2% in the previous quarter. Interestingly enough though, both the Atlanta Fed GDPNow and the New York Fed Nowcast models project an acceleration in growth, to 3.4% and 3.9% respectively. In case of a positive surprise in the official figures, the dollar could recoup some of its latest losses. The US will also see the release of durable goods orders for December at exactly the same time as the GDP numbers, implying that any market reaction at the release may be influenced by those figures as well.

Over in Canada, CPI data for December are due for release at 1330 GMT as well. Expectations are for the headline inflation rate to decline to 1.9% in yearly terms from 2.1% previously, while no forecast is available for the core CPI print. These data could play a major role in determining how many more times the Bank of Canada will raise rates this year and thus, they are likely to have a sizeable impact on the CAD.

In terms of public appearances, investors will turn their eyes to the World Economic Forum in Davos, where US President Trump will speak at 1300 GMT. Then at 1600 GMT, the Governors of the Bank of England and the Bank of Japan will participate in a panel discussion with the head of the International Monetary Fund, Christine Lagarde.

Later during the day at 1800 GMT, oil traders will turn their attention to the US Baker Hughes oil rig count. The number of active US oil rigs has remained more or less flat in recent weeks even despite the surge in oil prices. It will be interesting to see whether US producers have begun to react to the higher prices, with any increase in the number of active rigs likely to dent some of the optimism currently surrounding the energy market.

In stock markets, Honeywell International Inc. and Gentex Corporation are among companies to report quarterly earnings before the US markets open today.

USDJPY: Sets Up To Strengthen Further Higher

USDJPY: The pair closed higher on price rejection on Thursday leaving risk of more strength. On the downside, support lies at the 109.00 level where a break if seen will aim at the 108.50 level. A cut through here will turn focus to the 108.00 level and possibly lower towards the 107.50 level. On the upside, resistance resides at the 110.00 level. Further out, we envisage a possible move towards the 110.50 level. Further out, resistance resides at the 111.00 level with a turn above here aiming at the 111.50 level. On the whole, USDJPY faces further upside pressure

Canadian Dollar Higher, CPI Next

The Canadian dollar has posted slight gains in the Thursday session. Currently, the pair is trading at 1.2310, down 0.53% on the day. On the release front, there are two key indicators, either of which could impact on USD/CAD. Canada releases CPI,which is expected to decline 0.3%. The US will publish Advance GDP, which is forecast to post a strong gain of 3.0%.

On Thursday, both Canadian and US data was mixed, and the Canadian dollar didn't show much movement. Canadian Core Retail Sales jumped 1.6% in November, crushing the estimate of 0.8%. This marked the strongest gain since January. Retail Sales couldn't keep pace, as the small gain of 0.2% missed the estimate of 0.7%. In the US, unemployment claims rose to 233 thousand, but still beat the estimate of 239 thousand. Housing numbers continue to soften, as New Home Sales fell to 625 thousand, well off the estimate of 679 thousand. This follows the trend we saw earlier in the week, when Existing Home Sales slowed to 5.57 million, short of the estimate of 5.72 million.

The Canadian economy has been performing fairly well, and recent employment numbers have been much stronger than expected. However, there is a dark cloud on the horizon regarding NAFTA. The free trade agreement is critical for the Canadian economy, so threats by US President Trump to blow up the agreement are causing genuine concern for the government and the Bank of Canada. Negotiations between Canada, Mexico and the US, which are slated to end in March, have not yielded much progress, with the US side reportedly showing little flexibility. Trump has repeatedly said he is unhappy with the deal, and may prefer a new bilateral agreement between the US and Canada. At the same time, there are also many US companies that benefit from the current deal and are opposed to the US pulling the plug. If NAFTA is terminated, it's a good bet that the Canadian dollar will take a tumble.

DAX Dips as ECB Dovish on Stimulus

The DAX is almost unchanged in the Friday session. Currently, the index is trading at 13,293.50, down 0.04% on the day. On the release front, there are no major eurozone events. Investors will be keeping a close eye on US Advance GDP, which is expected to post a strong gain of 3.0%.

There were no surprises on Thursday, as the ECB maintained interest rates at a flat 0.00%. ECB President Mario Draghi was dovish in his follow-up remarks. Draghi said that interest rates would not rise until well after the ECB's asset-purchase program (QE) was over. The QE program will not end until September at the earliest, so Draghi essentially ruled out any rate hikes before early 2019. Draghi added that the ECB was prepared to increase QE in "size or duration", a reminder to the markets that it is premature to expect normalization anytime soon. A new headache for Draghi is the streaking euro, which has hit 3-year highs against the US dollar. Will this have a negative impact on the stock markets? Investors are worried that a stronger euro could hurt exports and company earnings. EUR/USD has jumped 3.6% in January, as the dollar continues to struggle.

The German economy is firing on all cylinders, and confidence levels improved in January. Consumer confidence improved to 11.0, pointing to an optimistic consumer early in 2018. Business confidence also moved higher, as Ifo Business Climate improved to 117.6, up from 117.1 in the previous release. The German Office of Statistics recently released preliminary data for GDP, and the reading of 2.2% for 2017 improved on the 2016 figure of 1.9%.

It's a busy time for the Federal Reserve, which will set the benchmark rate on January 31 and bid adieu to Janet Yellen, who will be replace by Jerome Powell in February. Earlier in the week, the Senate confirmed Jerome Powell in a decisive vote of 84-13, reflecting strong bipartisan support for Powell. The new chair is expected to continue Yellen's monetary stance, which was marked by small, incremental rate hikes during a period of economic expansion. The Fed has started to trim its massive balance sheet, another vote of confidence in the strength of the economy. At the same time, Fed policymakers are divided over how to approach inflation, which remains below the Fed target of 2 percent, despite a strong economy and a red-hot labor market. The markets will be watching to see how Powell & Co. respond to President Trump's tax reform legislation, which is sure to have a significant impact on the US economy.

Trump Davos Speech Headlines Lively Session

- Trump to Promote America First at WEF;

- Carney and Kuroda to Speak on Panel in Davos;

- US GDP Release Follows Modest UK Report.

Trump to Promote America First at WEF

It's been another interesting week in financial markets and as it draws to a close, there are still a few more headline events to squeeze in that could shake things up.

The most obvious of these will be Donald Trump's speech at Davos which always promises to be eventful. Trump is widely expected to push his America first agenda while making the argument for fair and reciprocal trade and claiming the country is now open for business. The visit is clearly an attempt to pitch the country to business leaders following the recent tax overhaul while at the same time reaffirming the US' position in the world and even perhaps clearing up some of the damage caused by recent unsavoury leaks.

Carney and Kuroda to Speak on Panel in Davos

Another notable event at the World Economic Forum today will be the panel discussion on the Global Economic Outlook, which will include the heads of the Bank of England and the Bank of Japan on the panel. Mark Carney and Haruhiko Kuroda will both be part of the discussion at a time when both central banks continue to pursue very loose unconventional monetary policy measures.

The BoE may have raised interest rates last year but this only took them back to pre-Brexit levels and with inflation seen easing from the highs and growth slowing, the central bank may hold off on more. It will be interesting to hear the views of both central banks and whether they allude to their exit strategies from both these unconventional policy measures and, arguably more importantly, the timing of it.

US GDP Release Follows Modest UK Report

Outside of Davos, there'll also be a focus on the economic data on Friday. The UK has already released growth figures for the fourth quarter which slightly surpassed expectations but still highlighted the gradual slowdown the country is experiencing. The pound was slightly buoyed by the higher than expected reading, adding to gains already seen earlier in the session and returning close to yesterday's highs against the dollar. The pound is now trading above the lows seen in the run up to the EU referendum against the dollar although this is also largely due to the greenback depreciation.

The US will release GDP data for the fourth quarter today and it is expected to show the economy grew by 3% on an annualised basis, slightly down from 3.2% in Q3 but still representing another strong quarter. This will be accompanied by durable goods orders for December and retail sales data from Canada which should ensure it's another lively session for markets.

U.S Dollar Shackled To Trumps Trade And Twitter Rants

President Trump's self-proclaimed 'gift of gab' temporarily gave aid to the struggling U.S dollar Thursday, just a day after his Treasury secretary endorsed a 'weak' dollar.

His Davos 'strong dollar' comments managed to temporarily jolt capital markets reserve currency of choice out of a three-day tailspin.

The forex market has been jarred first by U.S Treasury secretary's Mnuchin's unusual favouring Wednesday of a 'weaker' greenback that's good for trade and also by ECB's President Draghi comments post ECB's rate announcement Thursday, that the eurozone's regional growth justified gains in the common currency.

Elsewhere, stocks are little changed after erasing earlier gains as investors assess the impact of the greenback's gyrations. Corporate results had set the tone on most regional bourses.

Note: The dollar's decline in recent months has partially been driven by brightening prospects for growth outside the U.S, which have bolstered investors' expectations for 'tighter' monetary policy elsewhere.

With President Trump expected to deliver a keynote closing speech at Davos' World Economic Forum later this morning, investors should be expecting further dollar volatility.

Note: President Trump is expected to address the Worlds Economic Forum at 8 am EDT.

1. Stocks under pressure from currency strength

In Japan, the Nikkei has closed out the week lower in choppy trade on Friday as investors locked in profits ahead of the weekend, while mining shares and financial firms underperformed the market. The Nikkei closed -0.2% down, wile the broader Topix slid -0.3%. For the week, the Nikkei declined 0.7 percent.

Note: Australia was closed for a bank holiday.

In Hong, the Hang Seng ended the week at a record high, capping its seventh consecutive week of gains, amid optimism toward global economic recovery and accelerated money inflows from China. At close of trade, the Hang Seng index was up +1.53%, while the Hang Seng China Enterprises index rose +2.51%.

In China, equities closed out at a high, but are off their two-year highs with the Shanghai index up for the sixth-week in a row, supported by gains in real estate and transport firms. The Shanghai Composite index was up +0.3%, while the blue-chip CSI300 index was up +0.39%.

In Europe, regional indices trade higher across the board, rebounding from yesterday's losses as positive earnings in Europe and the U.S has helped lift markets.

U.S stocks are set to open in the 'black' (+0.2%).

Indices: Stoxx600 +0.5% at 400.4, FTSE +0.4% at 7642, DAX +0.2% at 13322, CAC-40 +0.9% at 5531, IBEX-35 flat at 10595, FTSE MIB +0.3% at 23787, SMI +0.7% at 9551, S&P 500 Futures +0.2%.

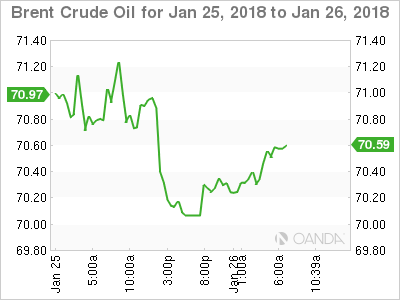

2. Oil firms as dollar falls further, gold higher

Ahead of the U.S open, oil prices have reversed its earlier fall as ongoing weakness in the U.S dollar is seen as supporting fuel consumption.

Brent crude futures are at +$70.40 per barrel, down -3c from their last close, after dropping as low as +$70.07 in the Asian session. U.S West Texas Intermediate (WTI) crude futures are at +$65.52 a barrel, up +1c from their previous close, recovering from an overnight session-low of +$64.91 a barrel.

Casting a shadow over this weeks oil rally is the presence of growing output of U.S shale oil, as higher prices encourage more investment in expanding supplies.

Note: U.S crude oil production is expected to surpass +10m bpd next month, and on the way to a record ahead of previous forecasts according to the U.S government's EIA.

Gold prices have rallied to an 18-month high this week, buoyed as the U.S dollar hit three-year lows after 'weaker currency' comments from U.S Treasury secretary Mnuchin. Spot gold has rallied +0.3$ to +$1,350.86 per ounce. The 'yellow' metal has gained +1.5% so far this week.

3. German Bund yields close out on a high

This morning, German bund yields have managed to gravitate away from their six-month lows and remain set for their sixth consecutive week of rises, a day after the ECB surprised markets by its modestly 'dovish' tone in the face of a robust EUR.

President Draghi yesterday failed to live up to the market's dovish expectations with his communication on the exchange rate falling short of expectations for a stronger stance ahead of the ECB meeting.

Germany's 10-year Bund yield has fallen -2 bps to +0.54%, after having hit a six-month high at +0.579% on Thursday after Draghi said eurozone inflation should rise in the medium term.

Note: Germany – a new round of negotiations for a coalition government has begun, which could contribute to added demand for safe haven assets.

Elsewhere, the yield on U.S 10-year Treasuries has fallen -3 bps to +2.62%, while in the U.K the 10-year Gilt yield has climbed +1 bps to +1.41%.

4. Dollar direction dictated by Trumps trade rants

FX volatility is back in a big way, with verbal rhetoric and 'clarifications' playing havoc with intraday ranges.

Currently, Trump's induced dollar lift has only been temporary, as markets look beyond rhetoric to raw fundamentals.

Today, G7 currency pairs are expected to engage in wide intraday ranges with President Trump's expected 'protectionist' speech in Davos.

The EUR/USD (€1.2458) is again encroaching on its three-year high just above the psychological €1.25 barrier. A level many felt overbought, especially after Presidents Draghi's 'dovish' remarks.

GBP/USD (£1.42390 has received a lift following this morning's better U.K Q4 GDP data (see below). The pair tested £1.4270 after the release as expectations were skewed towards an under-shoot to the downside, rather than today's upside surprise.

The BoJ's Minutes release overnight of last month's monetary policy meeting reiterated their stance that it was appropriate to continue 'powerful' monetary easing. Some members noted that they must 'continue to look at both positive and negative effects of current policy, including effects on financial system.' Other data released, Japan's December inflation data showed improvement towards beating deflation remains ongoing. USD/JPY remains below the ¥109 level as investor's mull over the possibility of an announcement by the Bank of Japan (BoJ) in mid-2018.

5. U.K's Q4 GDP beats expectations, but the annual pace is at a five-year low

Data this morning showed that the U.K economy grew at the slowest pace in in five-years, highlighting how uncertainty linked to its looming departure from the E.U would suggest that the economy is benefitting from the recent upsurge in global growth.

The U.K. economy expanded +0.5% in Q3 of 2017, which translates to an annualized rate of +2.0%.

Note: It's fastest quarterly rate of expansion in 2017, and beat market expectations – U.K economy grew by +1.8% last year, the slowest rate of expansion in seven years.