Sample Category Title

EUR/JPY Daily Outlook

Daily Pivots: (S1) 135.01; (P) 135.53; (R1) 135.87; More....

Intraday bias in EUR/JPY remains neutral at this point. More consolidation would be seen in range of 133.03/136.63. But after all, outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

Muted Reactions to US Government Shut Down, Big Week for Yen and Euro

Market reactions to the US government shutdown is rather muted. Dollar is trading generally lower today but is held within Friday's range. Asian markets are pretty steady with Nikkei trading down just -0.14% at the time of writing. The Senate was in session yesterday but failed to deliver any breakthrough. The shutdown is extending into its third day and there is no sign of a resolution in the Senate yet. A procedural vote is expected at noon today. But there are unlikely enough votes to pass the bill to keep government running through February 8. For forex traders there are so many key events ahead in the week that they couldn't care less regarding the government shut down.

Big week for Yen with BoJ and CPI

The week ahead is full of key events and is particularly important for Yen and Euro. BoJ meeting and announcement is a major focus. There has been talk that BoJ is starting to consider policy normalization, given the improvements in the economy. Also, the summary of opinions in the December meeting showed there was a slight change in the board members' thinking. One member noted that "when it is expected that economic activity and prices will continue to improve going forward, the situation may occur where the Bank will need to consider whether adjustments in the level of interest rates will be necessary."

For the moment, markets would like to get clear indications from BoJ that the massive stimulus is here to stay for some more time. There were unnamed sources quoted by Bloomberg saying that BoJ officials perceive markets expectation of stimulus withdrawal have well moved ahead of their own. And inflation is staying well off the 2% target without sign of any upthrust. In addition, the tweak in bond purchases this year carries no policy implications. That is, BoJ is still sticking to the yield curve control framework.

In addition to BoJ meeting, consumer inflation data to be released on Friday could also be a Yen mover.

Similarly important for Euro with ECB and data

Some ECB officials have recently talked about ending the EUR 30b a month asset purchase after September this year. The monetary policy account of December meeting also showed discussions on changing the central bank's communications. These factors prompted speculations that ECB could drop the pledge to extend the asset purchase program if necessary. However, Reuters quoted an unnamed source saying that "market reaction to the minutes was excessive". Euro would likely be very sensitive to any change, or lack of change, in ECB's forward guidance.

Besides, key economic data including German ZEW, Ifo, Eurozone PMIs will be released.

More in the calendar

Elsewhere, the week is also full of important economic data. Q4 GDP from UK and US, Canada retial sales and CPI, New Zealand CPI, UK employment will also be closely watched.

Here are some highlights for the week ahead:

- Monday: Canada wholesale sales

- Tuesday: BoJ rate decisions, all industry index; UK public sector net borrowing; German ZEW; Eurozone consumer confidence

- Wednesday: Japan trade balance; Eurozone PMIs; UK employment; US house price index, existing home sales, PMIs

- Thursday: New Zealand CPI; German Gfk consumer sentiment, Ifo business climate, ECB rate decision; Canada retail sales; US trade balance, jobless claims, wholesale inventories, new home sales

- Friday: Japan CPI; UK GDP; Canada CPI; US GDP, durable goods

EUR/JPY Daily Outlook

Daily Pivots: (S1) 135.01; (P) 135.53; (R1) 135.87; More....

Intraday bias in EUR/JPY remains neutral at this point. More consolidation would be seen in range of 133.03/136.63. But after all, outlook stays bullish with 133.03 support intact. Break of 136.63 will resume medium term up trend. However, on the downside, break of 133.03 will have 55 day EMA and medium term channel support firmly taken out. Also, considering bearish divergence condition in daily MACD too, that will suggest medium term reversal. Deeper fall should then be seen to 132.04 support for confirmation.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 13:30 | CAD | Wholesale Trade Sales M/M Nov | 1.00% | 1.50% |

Market Morning Briefing: Dollar Index Is Continuing To Stay Below 91

STOCKS

Global stock indices have all moved up quite well in the last few weeks and are likely to test resistance levels above current levels which if holds could push the prices to lower levels soon.

Dow (26071.72, +0.21%) is almost stable near current levels and seems to have paused for a while. While below 26250, there could be some sideways movement in the 25750-26250 region before the index resumes its rally upwards. We would have to see if the news of government shutdown would have any impact on the indices.

Dax (13434.45, +1.15%) rose up sharply last week to close above immediate resistance near 13400. While the rise sustains, the index could continue to rise towards 13500 and higher in the coming sessions.

Nikkei (23772.02, -0.15%) is expected to trade below 24200-24000 levels and come off sharply in the medium term.

Shanghai (3490.78, +0.08%) has tested resistance of 3500. As mentioned in our earlier edition, 3500-3510 is an immediate resistance on the upside and is likely to hold in the medium term pushing off the index to lower levels. Failure to come off from 3510 could take it higher towards 3530-3550 in the longer run.

It would be crucial to see if Sensex (35511.58, +0.71%) come off from levels near 35750-35800 and Nifty (10894.70, +0.72%) from 10950-11000 levels. Although we have been expecting a rejection soon, the prices are yet to indicate any confirmation on that.

COMMODITIES

Brent (68.88) and WTI (63.54) have moved up a bit but are overall steady near previous levels. There could be some consolidation in the coming sessions before deciding on further direction.

Gold (1331.36) may trade within 1345-1320 region for the coming sessions. Thereafter a possible rise towards 1350 r higher could be expected.

Copper (3.1985) has been gradually coming down as expected towards 3.15 and could pause there for a few sessions. Downside scope is open towards 3.10-3.00 in the near term.

FOREX

Dollar Index (90.573) is continuing to stay below 91 as new political developments (the US government shutdown) prevent any strengthening of the dollar. US yields (see Interest Rates below), contrary to our expectations for some consolidation have only risen further from highs seen on Friday. While Friday’s rise might have been due to a shift from US debt to equity, the further rise in yields might just indicate lesser appetite for US debt in general, which might not be too positive for the Dollar. Currently, we maintain that the Index should respect support near 90.4-90.5 as seen on daily line charts and try moving up towards resistance near 91.5-92 on the 3 day line chart.

Euro (1.2230) has stayed above 1.22, seeing a high of 1.2295 on Friday. We can expect Euro to range between 1.21 to 1.2330 (seen as immediate resistance on daily candles) for few more sessions before attempting further upmove.

Against our expectations, Dollar-Yen (110.79) has come down below 111 instead of continuing its rise towards 112. We can however expect Dollar Yen to respect support near 110.5 on the 3 day candles and make another attempt at a rise towards 112 while it stays above this support, and, also while the Dollar Index stays above 90.4-90.5.

Euro-Yen (135.51) has come down from a high near 136.05 (seen on Friday) along with the drop in Dollar Yen, signifying some interim Yen strength. We still expect a week of slow upmove before it tests resistance near 137 on the daily candles.

Pound (1.3867) saw a low of 1.3839 on Friday which might suggest that it is struggling a bit to see a definitive breach past resistance near 1.385 on the daily candles. However, it is currently trading above 1.385 again and while it stays above this level, it will attempt to move towards resistance near 1.41 on the weekly candles in this week.

As mentioned on Friday, we might have to wait for couple of sessions before the breach of important resistance at 0.80 on the weekly line charts is confirmed for the Aussie (0.7993). It had gone past 0.80 on Friday but is again trading below it. A confirmation of breach of 0.80 would lead the Aussie to its next target of 0.82 (seen as higher resistance on the 3 day line chart).

Dollar-Rupee (63.895) could move up towards 63.90-64.00 this week with the downside limited to 63.60.

INTEREST RATES

US yields have continued their uprise in wake of the recent govt shutdown with US 10 Yr (2.6611%), 30 Yr (2.9323%), 5 Yr (2.4559%) & 2 Yr (2.0689%) all moving further up. Being a politically sensitive week, we could see some more volatility in yields on the upside till the shutdown ends.

The rise in yields is however providing some marginal pause to yield flattening as the US 10 Yr – 5 Yr (0.2052%) & US 30Yr – 10Yr (0.2712%) stay above supports near 0.19% and 0.24-0.25% respectively, indicating that we can expect them to hold for the time being.

Japanese 10 Yr yield (0.079%) as per our expectations has continued its ranging between 0.07% and 0.088% on short term charts, which might continue in this week.

EURUSD – Vulnerable, Loses Upside Momentum

EURUSD - The pair backed off higher prices to close on a rejection candle the past week. On the upside, resistance comes in at 1.2250 level with a cut through here opening the door for more upside towards the 1.2300 level. Further up, resistance lies at the 1.2350 level where a break will expose the 1.2400 level. Conversely, support lies at the 1.2200 level where a violation will aim at the 1.2150 level. A break of here will aim at the 1.2100 level. Below here will open the door for more weakness towards the 1.2050. Its daily RSI is bullish and pointing higher. All in all, EURUSD faces further upside move on bullish offensive

EURGBP – Vulnerable, Looks To Weaken Further

EURGBP - The pair continues to face downside pressure closing lower the past week. Support lies at the 0.8800 level where a violation will turn focus to the 0.8750 level. A break will expose the 0.8700 level. Its daily RSI is bearish and pointing lower suggesting further weakness. Conversely, resistance resides at the 0.8850 level where a violation if seen will turn risk towards the 0.8900 level. Further up, resistance resides at 0.8950 level followed by the 0.9000 level. All in all, EURGBP remains biased to the downside on further weakness.

GOLD – Remains Vulnerable To The Downside Nearer Term

GOLD - The commodity faces further downside pressure after it failed to close higher the past week. On the downside, support comes in at the 1,320.00 level where a break will turn attention to the 1,310.00 level. Further down, a cut through here will open the door for a move lower towards the 1,300.00 level. Below here if seen could trigger further downside pressure towards the 1,290.00 level. Conversely, resistance resides at the 1,340.00 level where a break will aim at the 1,350.00 level. A turn above there will expose the 1,360.00 level. Further out, resistance stands at the 1,370.00 level All in all, GOLD looks to weaken further.

It’s Never Sunny In Washington D.C.

It's Never Sunny in Washington D.C.

Last week the US dollar was trying to perform it's best Lazarus impersonation but fell well short on all accounts not only hampered by dwindling long-term sentiment but also feeling the weight from the latest political fracas in Washington. However, the dollar has not weakened off to dramatically this morning after Shutdown headlines with USDJPY off about 20 pips to 110.60 at the Wellington Open. Sure the government shutdown remains in focus, but it's not a significant USD driver as it presents only a minuscule shock to risk appetite

Not unexpectedly SPD agreed to start formal coalition talks with Merkel; a decision which moves Germany closer to form a new government.By accepting to pursue further discussions and thereby dramatically improving the chances for another grand coalition, a temporary calm should engulf the EU political landscape. However, German political developments were not thought to be a significant disruptor, so the market focus now pivots to this weeks ECB.

A bit of everything for everyone this week with, politics, central banks earnings and Trump in Davos could be this weeks marquee event.

The focus will be on Davos and the World Economic Forum that will take place from Tuesday to Friday with President Trump due to deliver a keynote address on the final day. Anytime Trump takes the podium, especially when he's the headline event, the chance for market turmoil elevates two-fold. This time around, there are lots of gossips that he could use this platform to up the protectionist ante, but so far other than pulling out of TPP the risk of protectionism under President Trump has mostly proved a red herring. Stay tuned!

However, the big currency mover this morning was the Turkish Lira as USDTRY moved +1.5 %after Turkey launched airstrikes in Syria against US-backed Kurdish fighters ( My TRY view is covered at the bottom )

Oil Markets Overview

Trading oil markets these days can be a challenge as the past few session the inter day moves are position related rather than fundamentally driven. But after rallying at breakneck speed the past four weeks, it was finally time for investors to come up for air and book some profits but the correction has remained rather shallow relative to the recent rally.

Fridays Baker Hughes reports indicated US drillers cut oil rigs for the second in three weeks despite soaring crude prices. It begs the question where are the Shale producers ??

AS for weekend geopolitical risk, rising conflict between Kurds and Turkey usually implies that oil prices would move higher due to the (region‘s) strategic position in oil supply routes.

Gold Market Overview

The Escalation of Middle East tensions and the reemergence of US dollar weakness has Gold market opening firmer today. Indeed, an escalation of geopolitical tension in the Middle East hot pot of unrest bodes well for Gold markets.But gold will likely track the dollar momentum so as the Greenback turns so does Gold appeal

G-10

The Euro

Despite heightened EU political noise, USD weakness and a likely shift in ECB language are to remain the dominant drivers as long-term investors continue to move into at a Euro. Long-term Real Money inflow tends to be a good indicator of Euro future price movements. And if we consider historical correlations that a 50 bp rise in EU 5 years yield could mean 3-5% ( 1.27 Mid ) Euro appreciation while a 100 bp could lead to 7-9 % appreciation ( 1.3175 mid). It's no wonder Real Money investors a pilling into the EUR supporting the narrative for a possible shift in ECB policy. Its ECB policy, not EU politics that is steering the ship

With that in mind, this weeks ECB meeting will draw the most attention with Draghi's follow up presser taking the most significant slice of the cake.

But is so often the case pre ECB meeting, we may see some EUR position temporarily trimmed even more so given the markets extended views on the ECB policy shift

The Japanese Yen

So much for tradition correlation as with Stocks up, yields up USDJPY is still down. But it's been trading this way for a while, and traders are getting no joy from long dollar bets. However, given that a shift in BoJ rhetoric would boost the Yen well below 110, especially with the USD showing little correlation to higher US yields, the BoJ will most likely stay the policy course. In fact, the pushback could be strong catching some investors off guard even if the BoJ real intentions are to move forward with a more aggressive taper. There is little chance Kuroda will take that leap of faith as the market would hammer USDJPY mercilessly lower

The Australian Dollar

The market has chewed through 5 significant big figures with nary a care. And bullish sentiment remains high after assuredly conquering the .80 level.Commodity prices continue to pave the way and given the weaker USD dollar narrative which should continue to play out in 2018 we could expect more investor rotation in the AUD to ride the unabated regional risk rally that the Australian dollar will feed off.

But with only twenty-five bp's of rate hikes priced in STIRT for 2018 and a measly five bp's baked into May, I think the next significant piece of the puzzle will reveal after next weeks' CPI ( Jan 31) which could see rapid repricing on RBA risks.The long Aussie trade continues to resonate with investors as US dollar continues to weaken in the absence of the Greenbacks sensitivity to rising US bond yields.

The Chinese Yuan

It was evident at Friday's open traders were under-positioned for the long-term bullish view, so price sensitivity took a back seat to acquiring position size

The US dollar plunged below 6.40 on Friday reaching its weakest point in more than two years against amidst US dollar broad-based weakness. But that only offers up one side of the calculus.

Toward the end of 2017, what became abundantly clear is that Pboc policy in 2018 would be vastly different from practices of yesteryear as president Xi Jinping was laying the groundwork and seeding ambitious plans to have the Yuan used more openly for international trade.

Also, pre-eminence of the dollar in 2018 as a pricing channel for oil and other critical industrial commodities could come under threat. At the end of the day, China's trade channels are dominating the supply chain.

The aclivity of the Petro -Yuan could spell impending doom for the Greenback given that Russia, China's most significant exporter of Oil would be more than happy to be a receiver of Yuan for oil exchange.

Also with the lack of Pboc meddling interventions of late and the removal of countercyclical mechanisms, its possible investors will not have to stomach increased capital controls, nor the Pboc's affinity for interventions, thereby removing the most significant barrier for entering China's capital markets. Currency manipulation!

In fact, it could be time to get rid of the notion that policymakers are prioritising stability versus internationalisation as China has deep enough pockets to take on both issues and come out smelling like plum blossoms.

Asia FX

The Malaysian Ringgit

With absolutely no protest from BNM about the stronger Ringgit, the door is wide open to continued appreciation.

The MYR remains undervalued versus regional peers as expressed through a trade-weighted average which suggests the fair value of the Ringgit should be closer to 3.50-3.70. And with strong exports, Belt and Road initiative increasing Foreign Direct investment, improving oil prices and a weaker US dollar complimented by a hawkish BNM, markets could pivot to that direction.

Taking its cue from the surging Yuan on Friday, the Malaysian Ringgit dove through the 3.95 USDMYR and quickly moved sub 3.94 as investor piled into Ringgit positions ahead of Thursday's MPC.

But the move was as much about the BNM's impending shift to policy normalisation as it was about regional risk sentient that remains off the charts with Asian equities continuing the stellar start to 2018.

Also, global demand suggests Malaysian exports will remain firm and therefore support GDP. With rising oil prices adding to the positive domestic narrative, but also posing an upside threat of inflation, this suggests the market may be underestimating the potential of at least one additional rate hikes in 2018 and lending support to the Ringgit.

However in the build-up to the BNM policy decision, the market will continue to trade sensitivity to the USD dollar, but the bias will most likely be to cover risk on dips

Making a case for Bank Negara Malaysia Rate hike and stronger Ringgit

It's hard not remain firmly entrenched in the rate hike camp. After last policy meeting, it became clear as day that Bank Negara Malaysia (BNM ) was preparing to start normalising interest rates policy where during the November meeting there was a shift to a hawkish bias based broadly on the back of an optimistic outlook for both domestic and external environments.

Last November BNM left interest rates unchanged not advocating to reverse a surprise reduction by 25bps to 3% in July 2016. So it should come as no surprise that the BNM will remove the monetary accommodation driven by financial markets uncertainties around Brexit. Since Brexit risks have receded, global growth is surging, and the Malaysian economy is firing on all cylinders, it makes sense to get in front of inflation by gradually raising rate while allowing an undervalued Ringgit to appreciate. The recent rally in crude oil prices will drive up headline inflation while core inflation is expected to follow through with domestic demand accelerating. In fact, the BNM could deliver a hawkish rate hike which would assuredly strengthen the Ringgit, and by extension, the stronger MYR efficiently tightens monetary conditions while buttressing inflationary pressures

With a January rate hike all but certain, the focus now shifts to forward guidance as a more hawkish retort from BNM will increase expectations for a follow-up rate hike(s) in 2018 and the Ringgit will soar.

Bond markets have been consolidating with some investors pairing back short-dated tenors in case the BNM delivers a hawkish surprise, as yields will increase correspondingly.

But given that short-dated local currency denominated Malaysian government bonds are the ideal investment for foreign investors to express a bullish bias on the MYR, we could expect demand to surge post policy decision and lend further support to the Ringgit

EM FX

Turkish Lira

The market was fearfully focusing on developments on Syria border, and those fears came to fruiting over the weekend. Turkey launched Airstrikes into Northern Syria targeting US-backed Kurdish fighters while defying US appeals. Turkey is now tumbling down the US political frenemy index which has caused USDTRY to gap higher towards 3.83 ( +1.60) at the open. However, Unlike a war of word type scenario which tends to have a little lasting effect, dropping bombs is a different kettle of fish, so I doubt traders will be too eager to reverse this move too quickly until coolers political temperament emerges.

South African Rand

Reports are circulating that ANC will Jacob Zuma out of office, given the superabundance of Zuma generated political headwinds, his removal will clear the political path for much need reforms and could be the signal for market to by the ZAR

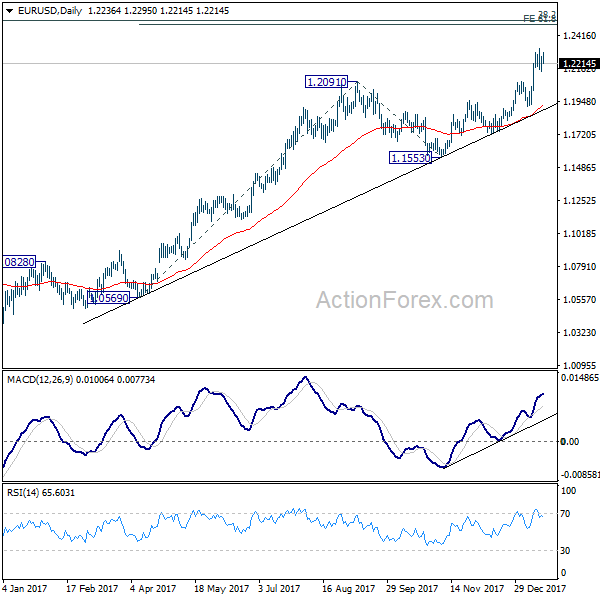

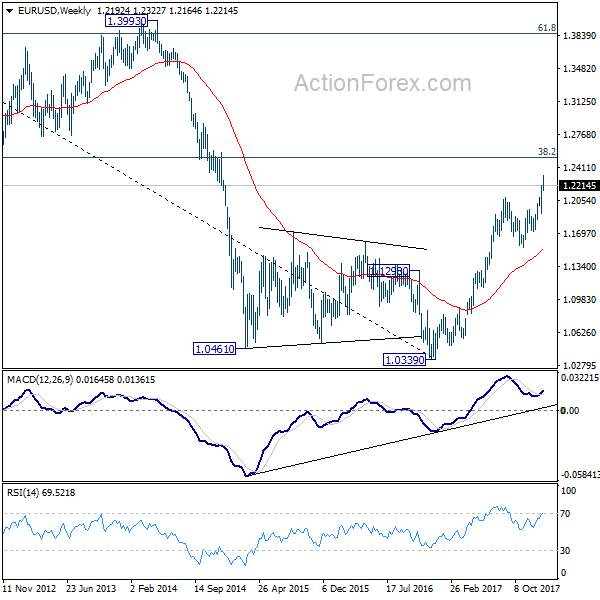

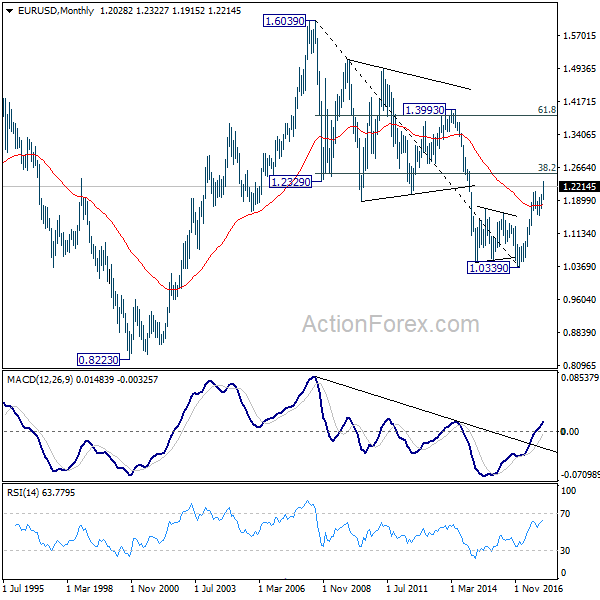

EUR/USD Weekly Outlook

EUR/USD rose to 1.2322 last week but turned into consolidation since then. Initial bias is neutral this week first. As long as 1.2088 resistance turned support holds, near term outlook remains bullish and another rise is expected. Above 1.2322 will extend the medium term rise to next key fibonacci level at 1.2494/2516. We'd expect strong resistance from there to bring reversal. Meanwhile, break of 1.2088 will argue that EUR/USD has topped earlier than expected. In that case, intraday bias will be turned to the downside for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of further rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 61.8% retracement of 1.6039 to 1.0339 at 1.3862.

In the long term picture, 1.0339 is seen as an important bottom as the down trend from 1.6039 (2008 high) could have completed. It's still early to decide whether price action form 1.0339 is developing into a corrective or impulsive pattern. On the upside, strong resistance could be seen from 38.2% retracement of 1.6039 to 1.0339 at 1.2516. On the downside, we're not anticipating a break of 1.0339 in medium term.

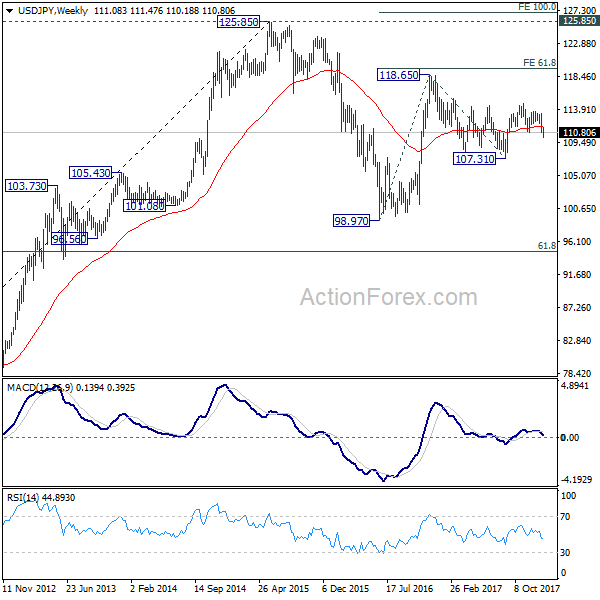

USD/JPY Weekly Outlook

USD/JPY rebounded after hitting 110.18 last week, ahead of 61.8% retracement of 107.31 to 114.73 at 110.14. But such rebound faced strong resistance from 4 hour 55 EMA and retreated. Initial bias is neutral this week first. On the upside, break of 111.47 will affirm the case that correction from 114.73 could have completed with three waves down to 110.18. Intraday bias should then be turned back to the upside for 113.38 resistance for confirmation. However, below 110.18 will extend the correction lower. But we'd again look for bottoming signal in next fall.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

In the long term picture, the rise from 75.56 (2011 low) long term bottom to 125.85 top is viewed as an impulsive move, no change in this view. Price actions from 125.85 are seen as a corrective move which could still extend. In case of deeper fall, downside should be contained by 61.8% retracement of 75.56 to 125.85 at 94.77. Up trend from 75.56 is expected to resume at a later stage for above 135.20/147.68 resistance zone.

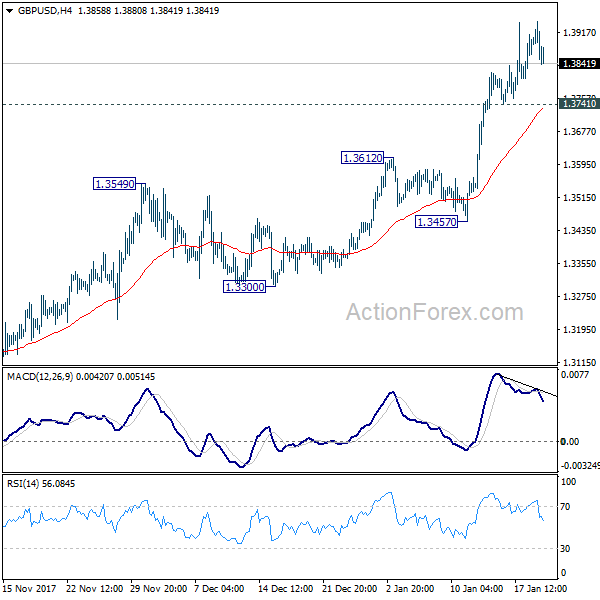

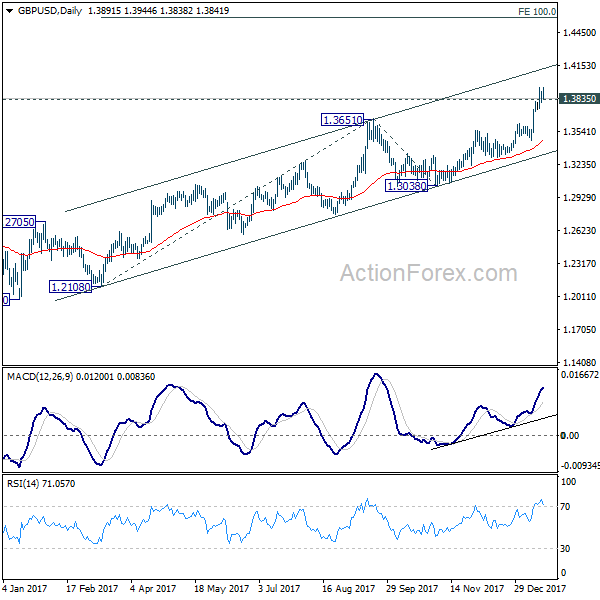

GBP/USD Weekly Outlook

GBP/USD surged to as high as 1.3944 last week and broken 1.3835 key resistance. At this point, the pair seems to be struggling to find follow through buying this level. But still, as long 1.3741 minor support holds, further rally is expected. Sustained trading above 1.3835 could trigger upside acceleration to 100% projection of 1.2108 to 1.3651 from 1.3038 at 1.4581 next. However, on the downside, break of 1.3741 minor support will indicate rejection from 1.3835 and turn bias to the downside for 1.3457.

In the bigger picture, sustained break of 1.3835 key resistance level will indicate that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. In that case, further rise should be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Nonetheless, rejection from 1.3835 will maintain medium term bearishness and thus, the risk retesting 1.1946 ahead.

In the longer term picture, long term bullish outlook is starting to get more conviction now. Still, sustained break of 1.3835 resistance is needed to confirm. And in that case, rise from 1.1946 should at least be correction whole long term down trend form 2.1161 and should target 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.