Sample Category Title

US Dollar Vulnerable to Political Drama

Central banks and growth indicators to feature alongside Washington Turmoil

The USD dollar remains weak versus most majors due to the downward pressure from the threat of a government shutdown. The House of representatives have passed a short term funding bill, but it faces an uphill battle in the Senate with the midnight deadline fast approaching.

- Bank of Japan expected to add clarity to bond purchases

- European Central Bank (ECB) unlikely to send end of QE signals

- US first GDP estimate for Q4 forecasted at 2.9 percent

US Government Shutdown Dragging Dollar Lower

The USD/JPY dropped 0.35 percent during the last five days. The currency pair is trading at 110.68 as the weakness in the US dollar has combined with strong economic indicators in Japan. The Bank of Japan (BOJ) is optimistic about the economy and the 2 percent inflation target is looking like less of an impossible dream. The BOJ will release its monetary rate statement on Monday, January 22 at midnight EST to be followed by a press conference with BOJ Governor Haruhiko Kuroda on Tuesday, January 23 at 1:30 am EST. Economists see little chance of a change in monetary policy announced at the January meeting, with odds rising slightly starting in the fall.

The BOJ could add some details on why it cut some of the long-dated bonds purchases last week and if not is sure to be part of press conference. G10 central banks are putting pressure on the Fed as the gap between easing and tightening is smaller. The US dollar enjoyed some support from the Fed reducing stimulus and eventually hiking rates, but now with political instability and the Bank of Canada (BoC), the European Central Bank (ECB) and even the BOJ moving closer to reducing stimulus the greenback is struggling.

The EUR/USD gained 0.27 percent in the last five trading days. The single currency is trading at 1.2236 ahead of the midnight deadline for the shutdown of the US government. The EUR has been gaining against the USD on the back of improved economic indicators in Europe. Rising inflation could help the European Central Bank (ECB) set an end to their massive quantitative easing program. The ECB has said that inflation is still too weak, with stimulus to continue for the time being, but stronger growth has the market increasing the odds of the end of European QE sooner rather than later.

The USD has failed to gain traction in 2018 and politics is very much a part of what is wrong with the greenback this year. US congress is having trouble finding a way got avoid a government shutdown with the clock ticking down and President Trump complicating matters. The primaries in the fall are not looking good for the Republican party, but they are finding it challenging to break away from the President and that could cost them control of the House and the Senate.

The US Bureau of Economic Analysis (BEA) will release the first estimate of the gross domestic product (GDP) for the fourth quarter of 2017. US growth has been strong and with the highly anticipated tax reform finally a reality it is expected to continue trending upwards. There are three releases for the GDP figures as more data refines the final indicator. The first release is the most impactful given its only 30 days after the end of the quarter. The 4Q GDP will be released on Friday, January 26 at 8:30 am EST. Forecasts are calling for a gain of of 2.9 percent. A reading above that first estimate could bring some relief for the USD based on the strength of US fundamentals and the expectations of strong growth in 2018. A lower than expected GDP indicator could put even more pressure on the US currency at a time when the Trump Administration is dealing with multiple fronts.

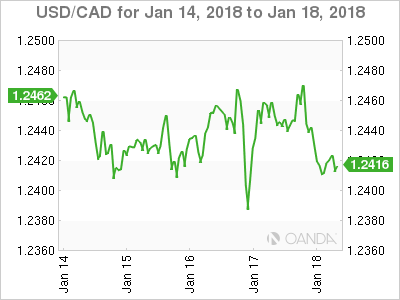

The USD/CAD rose 0.20 percent this week. The currency pair is trading at 1.2481 despite the Bank of Canada (BoC) rising rates 25 basis points. The monetary policy decision did not have the usual impact as the loonie remain subdued due to political risks. The growing risk the US pull out of the trade agreement has been already been voiced by anonymous Canadian officials and has put the loonie under pressure versus the US dollar. The three members of NAFTA originally wanted to avoid going into 2018 without the details of the deal hammered down. Mexican presidential elections in July and the US primaries in November could interfere with the already divisive topic and could politicize even further forcing it decision based on populism and not economics.

The sixth round of negotiations will kick off in Montreal on January 23 and will go until the 28. This round is of particular note given that the Foreign ministers will rejoin the talks after skipping the November and December talks.

The Bank of Canada (BoC) has now hiked three times since the summer of 2017. After two rate cuts in 2015 Governor Poloz had been cautious to remove the stimulus, but that suddenly changed in July in which various members of the monetary policy team dropped heavy hints that a hike was coming. The BoC followed that with a small surprise by hiking one month ahead of the expected date in September. The tone of the CB changed to one more neutral with no rate moves expected until the end of the first quarter.

The November and December job reports in Canada changed all that. Both had gains of 70,000 jobs and brought the unemployment rate to a 40 year low. Governor Poloz had a tough task, keep removing stimulus but at the same time warn about potential headwinds. His strategy was to focus on the actions of the Trump Administration. The tax cuts approved in December in the US could end up reducing investment in Canada, just as the negative impact of the end of NAFTA could derail the Canadian growth story.

Market events to watch this week:

Monday, January 22

- Midnight JPY Monetary Policy Statement

- Midnight JPY BOJ Outlook Report

Tuesday, January 23

- 1:30 am JPY BOJ Press Conference

Wednesday, January 24

- 4:30 am GBP Average Earnings Index 3m/y

- 10:30am USD Crude Oil Inventories

- 4:45 pm NZD CPI q/q

Thursday, January 25

- 7:45am EUR Minimum Bid Rate

- 8:30 am CAD Core Retail Sales m/m

- 8:30 am EUR ECB Press Conference

Friday, January 26

- 4:30 am GBP Prelim GDP q/q

- 8:30 am CAD CPI m/m

- 8:30 am USD Advance GDP q/q

- 8:30 am USD Core Durable Goods Orders m/m

*All times EST

Australia & New Zealand Weekly: Employment Robust in 2017 but December Unlikely the Tipping Point for Wages

Week beginning 22 January 2018

- Employment robust in 2017 but December unlikely the tipping point for wages.

- Australia: Westpac-MI Leading Index, Australia Day holiday.

- NZ: Q4 CPI.

- US: Q4 GDP.

- Central banks: ECB policy meeting and BoJ policy decision.

- Key economic & financial forecasts.

Information contained in this report was current as at 19 January 2018.

Employment robust in 2017 but December unlikely the tipping point for wages

December sealed a solid year for the labour market

Total employment rose by 34.7k in December, well above both the market's (+15k) and Westpac's (-10k) expectations with a small upward revision to November (to 63.6k from 61.6k). But most notably, despite the solid gains in employment, the unemployment rate rose to 5.5% as a 0.2ppt rise in participation boosted the labour force by 55.2k. In the year total employment gained 403k or 3.3%.

The surge in employment also saw further solid gains in full-time employment (+15.1k). In the year full-time employment gained 303.4k. Part-time employment rose 19.5k to be up 99.7k/2.61%yr. Total hours worked did ease back a touch (-0.2%mth) but they are still up a solid 3.2%yr. In the month the dip in hours worked was due to a decline in hours worked per full-time employee; hours worked per part-time employee was flat.

This was the 15th consecutive monthly gain in employment matching the longest period of consecutive employment which ended July 1994. There is every chance we could see a record 16th consecutive gain in January.

Females continue to be the dominate force for employment ...

Female employment continues to outpace male employment, not just in growth rates but also in absolute terms. In the year to December female employment has lifted 4.3%yr or 238.9k. Male employment lifted 164.1k/ 2.6%yr. As noted below we believe this reflects both structural and cyclical factors that are driving a surge in services employment particularly for heath and education.

... and participation

Female participation has risen 0.7ppt in the last six months, 1.3ppts in the year. So while male participation has also improved, 0.4ppt in six months and 0.5ppt in the year, and overall is still higher than female participation (71.0% vs. 60.6%) the robust gain in female employment is being more than matched by gains in female participation.

That is the supply of female labour is rising to match the rise in female employment. This is a key reason we believe to why the unemployment rate will hold around current levels through the first half of 2018 even with further robust gains in employment.

Female employment lifts on the back of strong growth in the services sectors

In the year to November (sector date is released in the mid-month of each quarter) health care & social services made the single largest contribution to the gain in employment of 134.7k. A bit further back was construction (102k) but then it was education & training (60.8k), accommodation & food services (38.7k), retail trade (35.8k) then transport, postal & warehousing (29.9k). So of the top five sectors for employment four were those that have a higher than average share of female employees. And this rising demand for labour has drawn both more females into the workforce and encouraged more females to extend their working life (female average retirement age is still lower than males but rising). That is the supply of labour is rising to meet demand and is part of the reason why unemployment has not fallen further and, more importantly, why we are yet to see any wage pressure even in the sectors with robust employment growth.

Mining states & NSW driving the recovery of employment

In December the main gains in employment came from NSW (+14.3k) and WA (6.1k). In the month NSW unemployment lifted to 4.8% from 4.6% in November, but it is still down from the 2017 high of 5.2%. Unemployment has been somewhat more volatile in Vic rising to 6.1% in December from 5.5% in November (the previous peak was 6.1% in August). Qld unemployment was 6.0% vs. 5.9% in November and a peak of 6.4% in June. WA has seen quite a bit of volatility printing 5.7% in December compared to 6.6% in November and an earlier peak of 6.4% in March.

By state, Vic continued to motor in 2017 but the pace of employment growth slowed from 4%yr at the start of the year to 2.9%yr by December. In the year to December Victorian employment grew by 87.7k compared to a 139.7k lift in NSW and a 100.6k gain in Qld. Even WA contributed a surprising 49.9k gain in 2017 (a 3.0%yr pace). So while the labour market is still quite robust in Victoria the recovery is being driven by the mining states and NSW.

This is also seen in the lift in state participation. While Victorian participation is still higher than what it is in NSW (66.4% vs. 64.6%) in the year participation lifted 0.97ppt in NSW and just 0.37ppt in Victoria. In Qld participation has lifted 1.53ppt in the year (to 65.8%) while in WA it rose 1.47ppt through to a national high of 68.5%.

A solid update on the labour market

December employment again exceeded expectations and continues to be underpinned by the robust leading indicator of the labour market. It confirms that we are in the midst of a better than expect expansion of the labour market so while we do note that the ABS reports some sample volatility issues, (the incoming rotation group had a higher employment to population ratio than both the group it replaced and the entire sample) we are cautious about looking for a January correction.

January is subject to a large positive seasonal adjustment associated with a usual significant dip in original employment over the Australian summer holidays. As such, we would rather stay on the sidelines for now than look for a near term correction.

However, we don't believe that December marks a tipping point for the outlook for wages. Ongoing strength in female participation will prevent a meaningful fall in the unemployment rate in the first half of 2018 before we see a moderation in employment growth through the second half of the year.

The week that was

It has been another very positive week for Australian economic data, with the labour force survey the highlight. A raft of China data has also come in, further emphasising the strength of their economy in 2017.

The best place to start our discussion is the labour force report. This edition received special attention because a positive employment outcome would mean that the past 15 months would stand as the (equal) longest period of consecutive employment gains in the history of the series. This indeed was the case, with 35k jobs reported in December following November's outsized 63k gain. For the year as a whole, 400k jobs were created; and, at 3.3%yr, the annual pace was more than twice the current estimate of population growth. Matching underlying growth, increases in employment have been concentrated in the southeast states and in the services sector (particularly health and education).

Intriguingly, despite the strong employment gain, the unemployment rate actually rose in December, from 5.4% to 5.5%; the cause was a 0.2ppt increase in the participation rate. Female participation has been in a strong uptrend since 2013 and stands in stark contrast to male participation, which is little changed over the period. It is logical to conclude that this rise in the supply of workers from outside the labour force has been a significant factor in restraining wage gains - along with industry rotation; soft domestic demand; and global factors such as greater competition and technology. Looking forward, we anticipate a slowing in the pace of employment growth. However, the leading indicators imply momentum will remain robust well into 2018.

Our Westpac-MI consumer sentiment survey was also released this week for January. Being the summer holiday period, confidence is typically overstated, hence we adjust both the headline measure and its components to compensate. After adjustment, January still reported a 1.8% increase in the headline index to 105.1, comfortably above both the series' long-run average and the 100 optimist/ pessimist divide. Expectations around the economy drove the monthly gain, the 'economic conditions, next 12 months' sub-index up 2.6% and 'economic outlook, next five years' sub-index surging 5.4%.

Expectations of family finances for the coming year also improved, rising 1.7% to 109.1 - the highest level in over four years. However, compared to a year ago, the majority of households actually felt worse off. Arguably this is why the 'time to buy a major household item' sub-index remained well below its longrun average. If consumption growth is to accelerate in 2018 as the RBA anticipate, then we will need to see the strength in employment growth pass through to both family finances (higher wages) and sentiment. We remain doubtful that this will occur in the foreseeable future.

Finally for the domestic economy, housing finance approvals also surprised to the upside in November, the number of approvals to owner occupiers rising 2.1% (2.4% and 9.2%yr excluding refinance) as the value of loans to investors lifted 1.5% (-8.3%yr). This result contrasts with a priori expectations that 2017's macroprudential policy changes would have a lasting impact on activity - as occurred in 2015. The detail showed that first-home buyers were a key support (4.5%; 36%yr), and unsurprisingly that this strength was concentrated in NSW and Vic - states where first-home buyer activity has been at low levels for a protracted period, and where state governments are offering considerable support. A possible conclusion to draw from this stronger momentum is that foreign buyers - who don't form part of this survey - may be a greater contributor to the broader housing slowdown than currently perceived.

Moving offshore, this really has been China's week. The first take home from the array of data released is that China's economy had a stellar year in 2017. The second is that a slowdown in growth is underway, a consequence of tighter policy. In Q4, annual GDP growth came in at 6.8%yr, unchanged from September and only a tick down from the first half's 6.9%yr pace. That said, the 1.6% quarterly gain was a step down from the near 1.9% experienced through mid-year. Driving this slowdown has been a material and broad-based deceleration in investment across the economy. Through 2017, growth in fixed asset investment has slowed from 9% to 7%. A base does look to be forming in a number of sectors, including housing construction, but the amplitude of the next upcycle is likely to be muted. This leaves the consumer as the key cyclical driver of growth. While momentum in consumer-related sectors remains robust, it has failed to accelerate further - likely owing to underwhelming gains for employment and incomes, a theme we have highlighted repeatedly as part of our PMI release.

Come 2018, with net exports not expected to contribute as they did in 2017, and given consumption growth is unlikely to accelerate further, we anticipate that growth will slow from 2017's year-average pace of 6.9% to around 6.2%. That should still be regarded as a robust and sustainable result, one that better fits authorities' desire for 'quality growth'. Crucial to the outlook for the consumer and the industrial sector will be credit supply. Authorities took a much tougher stance in this area in 2017, and these restrictions are set to remain in place. The purpose is to remove the risk that speculation and exuberance can create in a developing economy, particularly one that already has a high level of debt. It is for this reason that the central government is also unlikely to replenish its funding to local government authorities to allow stronger public investment in the provinces, and also why future house price and investment gains are likely to be modest compared to history, and skewed to tier 2 and beyond.

New Zealand: week ahead & data wrap

Unhappy new year

Firms have taken a dimmer view of the economy's prospects in the early part of this year. Some of that can be pinned down to the recent change of government, but not all - there are genuine signs that economic growth has slowed from its previous pace.

The NZIER Quarterly Survey of Business Opinion found that a net 11% of firms were pessimistic about the general business environment over the coming months, compared to a net 5% who were optimistic in the September quarter survey. Firms' own reported and expected trading activity, which tends to correspond more closely with GDP, saw more modest declines.

The fall in confidence wasn't a surprise in itself. Monthly business surveys had already shown a steep drop in confidence in November after the new Labour-led Government was formed, though with some rebound in December after the initial dummyspitting. The drop in confidence in the QSBO wasn't as dramatic, but it did reach its lowest levels in several years.

It may be tempting to write this off as just a protest vote against the new government, but we don't think that the results can be so easily dismissed. For one thing, impressions matter for how people act. One of the reasons that we downgraded our near-term growth forecasts last year is that we expect a hiatus in business investment, as firms get to grips with the new government's policies. The QSBO provides some support for that view: firms' intentions to invest in plant and machinery fell from 17 to 12, the lowest in two years. Slower investment would lead directly to lower GDP growth in the near term (but would add to concerns about capacity constraints in the longer run).

Another factor is the extent of the decline. We find that general sentiment in the QSBO tends to be around 10 points lower under Labour governments than under National governments, so a 16-point drop is within the range of plausible outcomes. However, there's no such bias evident in the firms' own-activity measures, which fell in the latest survey. We'd also point out that business confidence has been falling even since before the election; the cumulative fall has been much greater than we would normally see from a change of government.

So there does seem to be some genuine loss of optimism about the economy as well - at least, compared to the economy's strong run of growth in previous years. Revisions to the national accounts, published at the end of last year, showed that the economy powered ahead to 4% growth in 2016. But things were relatively more subdued in 2017, with annual growth slowing to around 3% by the September quarter. With population growth still running at around 2% a year, that amounts to a substantial slowing in per-capita terms. The latest QSBO results are in line with our view that growth will continue to slow in the near term. There was another important aspect to the QSBO: it highlighted how far the economy has progressed from the sharp downturn that followed the global financial crisis. Several years of strong GDP growth mean that the economy is now running closer to full capacity again. That is particularly evident in the labour market, with firms reporting that the difficulty of finding skilled workers and employee turnover are at their highest in 12 years.

Consequently, the survey's measures of average costs and prices have been gradually heading up over the last couple of years. At their current levels, they don't suggest a risk of inflation challenging the upper end of the Reserve Bank's inflation target. Rather, they suggest that we may now be past the era of surprisingly and persistently low inflation.

We expect next Thursday's CPI release to show the annual inflation rate holding at 1.9% in the December quarter, very close to the RBNZ's target midpoint of 2%. Some of the inflation comes from rises in food and fuel prices that we don't necessarily think will be sustained in coming years; excluding these items, we expect annual inflation to hold at a more modest 1.6%.

Of course, low interest rates have also been a major part of getting the inflation rate to this point. The OCR cuts in 2015 and 2016 were prompted by the persistent weakness of inflation in recent years, with concerns that this would flow through into people's perceptions over the longer term. While those interest rate cuts are now doing what they were meant to, we're not convinced that there is a case for withdrawing them yet. We continue to expect no changes to the cash rate until late 2019.

Data Previews

Aus Dec Westpac-MI Leading Index

Jan 24, Last: +0.69%

The six month annualised growth rate in the Leading Index lifted from +0.51% in October to +0.69% in November, a strong above trend reading indicating some of the headwinds evident earlier in the year have eased.

The Dec index looks set to record a further lift with several components posting strong gains, most notably dwelling approvals which jumped 10.4% in Nov due to a spike in high rise approvals in Vic. Other components recording improvements include: the ASX200, up 1.6%; the Westpac- MI Consumer Expectations Index, up 3.1%; US industrial production, up 0.9%; commodity prices, up 3.7% (in AUD terms); and the Westpac-MI Unemployment Expectations Index.

NZ Q4 CPI

Jan 25, Last: 0.5%, Westpac f/c: 0.4%, Mkt f/c: 0.4%

We estimate that consumer prices rose by 0.4% in the December quarter, led by higher fuel prices and other transport costs. This would keep the annual inflation rate at 1.9%, very near the 2% midpoint of the Reserve Bank's target range. Excluding the volatile food and fuel categories, we expect annual inflation to remain at a more modest 1.6%.

Our forecast is slightly higher than the Reserve Bank's pick of 0.3% for the quarter, although the difference is in the more persistent non-tradable categories where an upside surprise would be more significant.

The December quarter release will incorporate Stat NZ's three-yearly reweighting of the basket of goods and services that make up the CPI. However, the new weights have had very little impact on our inflation forecast.

Eur ECB policy meeting

Jan 25, deposit rate Last -0.40%, WBC -0.40%

The December meeting minutes heightened expectations of a coming shift in the Council's forward guidance.

Therein, the Council highlighted that growth in the region was "increasingly self-sustaining" and that the output gap was expected to close soon. The consequence for inflation is an erosion of remaining downside risks and greater belief that it will reach their 2.0%yr target in the 'medium term'.

We and the market do not expect a near-term change in the stance of policy. Instead, the debate is over whether the asset purchase program can end at September, or will need to be run down over the remainder of the year. From there, the key question is how far into 2019 it will be before a rate hike is delivered. A definitive view wont be available for months, but that wont stop the market from extrapolating any change in tone in the interim - however minor.

US Q4 GDP

Jan 26, Last 3.2% annualised, WBC 3.3% annualised

Following a slow start to 2017, activity growth accelerated to above 3% in Q2, a pace it has since sustained. Q4 is unlikely to challenge this 'trend', with a 3.3% gain anticipated.

Consumption growth will be a key support in Q4 thanks to strength in durables spending as well as robust momentum for services. After two negative quarters, residential investment should also aid GDP in Q4.

Business investment has certainly improved through 2017; but circa 5%, the annual pace is still modest versus history. A similar gain is expected in the final 3 months of 2017.

Inventories and net exports are wild cards quarter to quarter. In this instance, the risks are likely offsetting.

Weekly Focus: No Changes to ECB’s Forward Guidance

Market movers ahead

- We do not expect the ECB to change its forward guidance when it meets on Thursday next week but believe it will wait until the March meeting.

- In Norway, we do not expect new signals from Norges Bank but we think the likelihood of a rate hike in December has increased since the last meeting.

- The Bank of Japan meeting ends Tuesday morning and we expect no changes to monetary policy.

- Otherwise, we are due to get preliminary PMIs for January for the euro area and the US. Next week also sees the first estimate of GDP growth in the US and UK in Q4.

Global macro and market themes

- The 5Y point is the pivotal point on the EUR curve. This is right after the textbook and the normal pattern we see when monetary policy is about to change in either direction.

- While the 2Y5Y curve has steepened, the 5Y10Y curve has flattened. Also, the 10Y30Y curve has flattened, as long rates are already trading close to the 'neutral rate' in the eurozone – a curve dynamic close to the curve dynamics seen in the US since 2013.

- We expect to see an extension of the recent flattening of the EUR curve in 2018.

Canadian Manufacturing Sales Jumped Higher in November

Highlights:

- Manufacturing sales jumped 3.4% in November, and 2.5% controlling for the impact of price gains.

- Motor vehicle sales bounced back after transitory disruptions in earlier months and chemical sales increased sharply in November.

- The jump in manufacturing sale volumes suggests overall GDP may have bounced back 0.3% in November after an unexpectedly soft flat reading in October.

Our Take:

Nominal sales jumped 3.4% in November - the fastest one-month gain since March 2015 - after falling 0.6% in October. About a percent of that increase was due to higher prices, largely a 6% jump in petroleum prices. Volume sales were still up 2.5%, though, led by a 14.7% (12.9% in nominal terms) bounce-back in manufacturer motor vehicle sales following transitory production disruptions in earlier months. Chemical sale volumes also bounced back, rising 5.0% after a 3.7% drop in October. Machinery sale volumes dipped lower for a second straight month but were still up 14% from a year ago. NAFTA uncertainty remains a risk to the outlook, particularly for manufacturers, but the still-strong level of domestic manufacturer machinery sales coupled with an earlier-reported surge in equipment imports in November suggest that Canadian businesses continued to increase investment in Q4. The outsized pace of overall GDP growth from mid-2016 to mid-2017 was never likely to be sustained for a long period of time. Today's data adds to the list of indicators - not least of which is the solid labour market data - suggesting that although growth has slowed somewhat, the economy remains on a firm footing.

Sunset Market Commentary

Markets:

Global core bonds corrected slightly higher today in a news-thin trading session. US yields bounced into key resistance levels at the 5-yr (2.42%) and 10-yr (2.63%/2.64%) tenors with the US senate vote on a stopgap funding bill looming. Rejection would cause a partial government shutdown. US Treasuries tended to profit in such periods in 1995 and 2013. Some cautiousness was warranted in Europe as well ahead of this weekend's SPD party convention and next week's ECB meeting. The SPD vote will decide whether or not the party engages into formal coalition talks with CDU/CSU. Saxony-Anhalt, Berlin and the youth chapter of the party already showed their disapproval earlier this week. Regarding the ECB, we think it's too early to change the communication strategy about APP already and expect such turnaround at the March meeting. Changes on the US yield curve range between +0.5 bps (2-yr) and -1.1 bp (10-yr). The German yield curve steepens with yield changes varying between -1.5 bps (2-yr) and +0.6 bps (30-yr). On intra-EMU bond markets, 10-yr yield spreads versus Germany narrow up to 2 bps with Spain & Portugal outperforming (-4 bps) and Greece outperforming (+4 bps).

Trading in the major dollar cross rates was technical in nature. There were no data with market moving potential. Evidently, there were plenty of headlines on whether or not the US is heading to a partial government shutdown. For now, the impact on markets is limited. There is no indication of risk aversion. US yields stay within reach of the recent highs. The US/German interest rate differential also holds near the ST peak and (European) equities show good gains. The dollar trades mixed to slightly lower. EUR/USD trades little changed in the 1.2235/40 area. USD/JPY feels some more headwinds and returned below the 111 mark (currently 110.60). This might be dollar weakness, but investors maybe also want to reduce yen shorts ahead of next week's BOJ meeting. The Senate budget vote remains a wildcard for USD trading, but we don't expect it to be a real game-changer, whatever the outcome.

The focus for sterling trading turns to the December UK retail sales. Sales declined a bigger than expected 1.5% M/M. A fall of only 1.0% M/M was expected after strong November growth. Part of the unexpected big decline was maybe due to issues of seasonal adjustment on Black Friday sales. Even so, Q4 sales as a whole were disappointing. In line with the constructive sterling momentum earlier this week, EUR/GBP drifted to the low 0.88 area before the publication of the retail sales. The reaction to activity data was modest as was the case of late. Even so, the test of the 0.8805/10 intermediate support was rejected. EUR/GBP trades again near 0.8840. Cable jumped to the mid 1.39 area, but also reversed the intraday rebound and trades currently again in the 1.3865 area.

European stock markets gain around 0.5% today with the German Dax outperforming (+1%). US stock markets opened around 0.25% higher, ignoring the looming deadline.

News Headlines:

The Federal Reserve is said to be working to relax a key part of increased capital levels at the biggest banks, a move that could free up billions of dollars. It might bring the leverage-ratio rule more in line with a recent agreement among global regulators, according to sources familiar with the matter.

Racing against a midnight deadline, the US Congress will try to send President Donald Trump legislation to keep the government operating and avoid federal agency shutdowns that would otherwise begin tomorrow.

Canadian manufacturing sales jumped 3.4% in November, their biggest increase in 2-1/2 years, on strength in transportation equipment and petroleum and coal products. Sales set a record high of C$55.47 bn ($44.38 bn) on improved performances in 12 of 21 industries.

Spot Gold Rallies after Correction But Negative Signals Building on Weekly Chart

Spot Gold price jumped on Friday as dollar weakened on political uncertainty in the US. Reversal pattern was formed on daily chart following today's bounce to $1338, which marks over 61.8% retracement of $1344/$1324 pullback and suggests that corrective phase might be over. Underlying bulls look for further advance and retest of key short-term barrier at $1357 (08 Sep high), as the yellow metal maintains strong bullish sentiment on weak greenback. However, risk of deeper pullback after uninterrupted rally in past five weeks exists, as weekly chart shows gold price on track for weekly close in Doji. This could signal that steep five-week rally is showing signs of indecision ahead of key $1357 barrier, which could result in correction. Weekly slow stochastic turned sideways in deep overbought territory and supports scenario. Ascending 10SMA which contained corrective pullback from $1344, now acts as initial support at $1327 and marks pivotal support zone with $1324 (correction low), loss of which would generate stronger bearish signal.

Res: 1338; 1344; 1350; 1357

Sup: 1327; 1324; 1319; 1315

Sterling, Dollar and Gold in Focus

Sterling bears entered the scene on Friday after British retail sales tumbled sharply in December.

U.K. retail sales slumped -1.5% in December as the unsavoury combination of rising inflation and tepid wage growth sapped consumers' spending power. With wage growth consistently lagging behind inflation and putting the squeeze on household incomes, concerns are likely to heighten over the sustainability of Britain's consumer-driven economic growth. It is becoming clear that Sterling's appreciation this month had nothing to do with a change of sentiment towards the U.K. economy but rather ongoing Dollar weakness and market optimism over a soft Brexit. With political conflict at home still a recurrent theme, and weak economic fundamentals eroding investor appetite for Sterling, the GBPUSD's upside potential could be limited.

From a technical standpoint, the GBPUSD continues to follow a bullish trend on the daily charts. The breakout above 1.3850, could pave a way higher back towards 1.3920 and 1.4000, respectively. Alternatively, a breakdown below 1.3850, has the ability to trigger a decline back to 1.3700.

Dollar sulks near three year low

The Dollar was pummelled and pounded by investors on Friday thanks to growing fears of a possible U.S. government shutdown. Sentiment remains bearish towards the Dollar with further downside on the cards, as political uncertainty in the United States weighs heavily on the currency.

From a technical standpoint, the Dollar Index is heavily bearish on the daily charts. There have been consistently lower lows and lower highs while prices trade comfortably below the 50 Simple Moving Average. The 91.00 has acted as a minor resistance this week with some support found around 90.30. An intraday breakdown below 90.30 could invite a decline towards 90.00.

Commodity spotlight - Gold

Gold found support on Friday in the form of Dollar weakness and market anxiety over a potential U.S. government shutdown. With the Dollar struggling to gain ground and at the mercy of political uncertainty in Washington, the yellow metal is likely to remain buoyed.

Taking a look at the technical picture, Gold continues to fulfil the prerequisites of a bullish trend as there have been consistently higher highs and higher lows. There is a possibility that a new higher low has been created at $1324.15 and as such could provide a foundation for bulls to elevate prices back towards $1340. A decisive breakout and weekly close above $1340 could pave a path towards $1360.

Canada: Manufacturing Sales Rebound Strongly in November

Following a pullback in October, Canadian manufacturing sales rebounded a robust 3.4% in November. In real terms, sales volumes were up 2.5% during the month.

The bulk of the gain stemmed from the motor vehicle assembly (+14.2%) and motor vehicle parts (+11.3%). In real terms motor-vehicle assembly volumes were up 14.7% in the month.

A rebound in chemical industry sales also contributed to the strength of November's report. Sales were up 5.9% (5.0% in volumes terms), following a 2.7% decline (3.7% real) in October.

Regionally, sales were up in all provinces except Manitoba (-1.0%). Ontario recorded a 5.8% gain due in large part to the auto industry. Growth was positive, but slowed in Western provinces following a strong performance the month prior.

The inventory-to-sales ratio fell to 1.36 (from 1.39 previously) as the robust sales growth outpaced a more modest inventory build-up. The forward-looking components of the report were somewhat soft, with both unfilled and new orders declining on the month (-0.9% and -1.8% respectively). The declines were largely the result of the aerospace industry.

Key Implications

The strength in manufacturing sales and the rebound in the auto sector is encouraging following the setback in October. Economic growth in the fourth quarter is likely to come in relatively close to the Bank of Canada's expectation for 2.5% with some upside possible given this morning's strong number.

With November's strength largely reflecting a reversal of earlier production interruptions, the path forward remains somewhat unclear. Healthy job gains, rising incomes, and a strong outlook south of the border all bode well for manufacturers, but NAFTA uncertainty continues to hang over the outlook.

Indeed, economy watchers remain attuned to ongoing NAFTA negotiations, which continue next week in Montreal. President Trump has continued to talk tough, threatening to pull out of the agreement. The Bank of Canada has cited uncertainty around the outcome as a key downside risk to the outlook and we second this view.

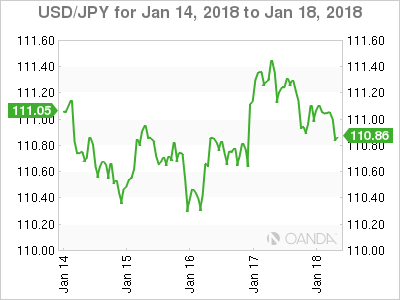

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 110.69; (P) 111.09; (R1) 111.49; More...

Intraday bias in USD/JPY remains neutral for the moment. Correction from 114.73 could have completed with three waves down to 110.18, ahead of 61.8% retracement of 107.31 to 114.73 at 110.14. Above 111.47 will target 113.38 resistance first. Break of 113.38 should confirm this bullish case. However, below 110.18 will extend the correction lower. But we'd again look for bottoming signal in next fall.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

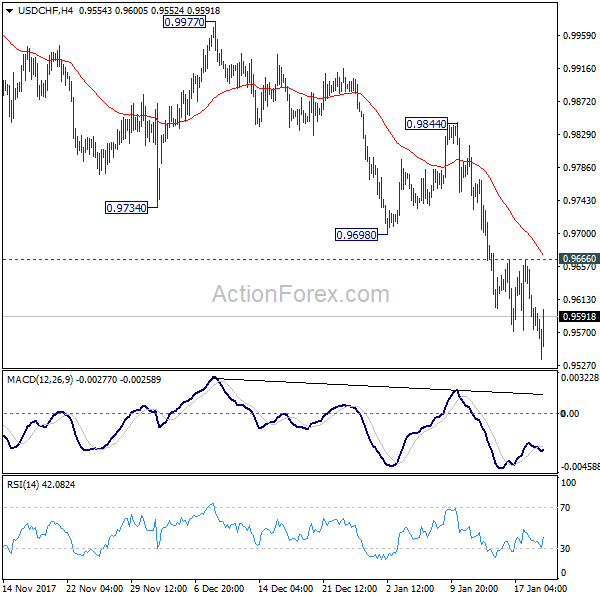

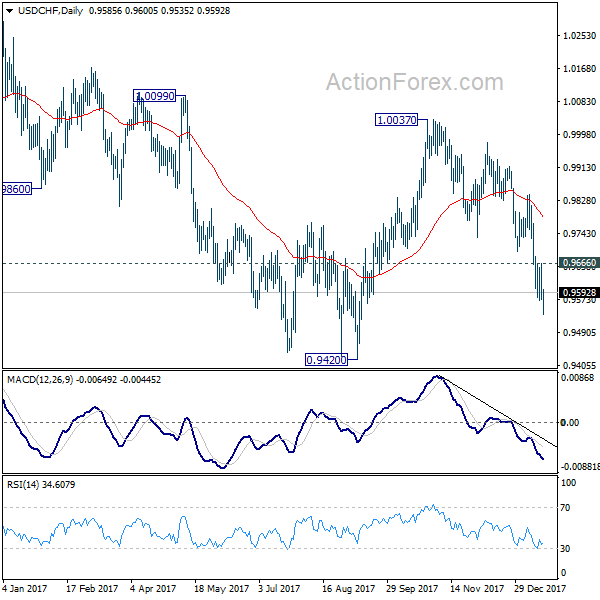

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9553; (P) 0.9609; (R1) 0.9644; More....

Intraday bias in USD/CHF remains on the downside for the moment. Current fall from 1.0037 would target a test on 0.9420 key support level. On the upside, break of 0.9666 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.