Sample Category Title

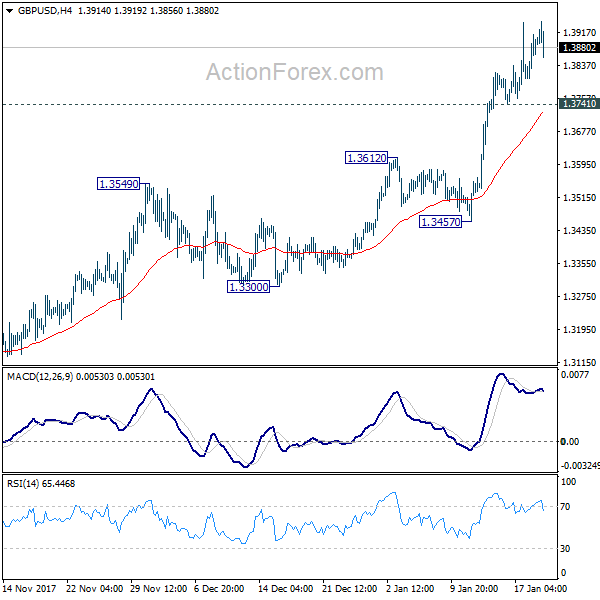

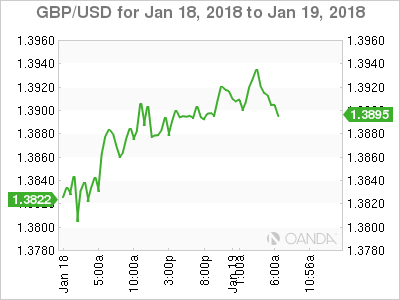

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3826; (P) 1.3869; (R1) 1.3936; More.....

Despite the mild retreat, intraday bias in GBP/USD remains on the upside at this point. And, sustained trading above 1.3835 will carry larger bullish implication and should target long term fibonacci level at 1.5466 next. On the downside, though, break of 1.3741 minor support will indicate rejection from 1.3835 and turn bias to the downside for 1.3457.

In the bigger picture, sustained break of 1.3835 key resistance level will indicate that rebound from 1.1946 is at least correcting the long term down from from 2007 high at 2.1161. In that case, further rise should be seen back to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466. Nonetheless, rejection from 1.3835 will maintain medium term bearishness and thus, the risk retesting 1.1946 ahead.

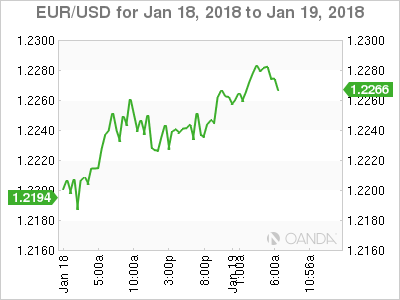

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2181; (P) 1.2222 (R1) 1.2281; More....

EUR/USD continues to be bounded in consolidative trading below 1.2322 and intraday bias remains neutral. More consolidations could be seen. But as long as 1.2088 resistance turned support holds, further rally is expected. Break of 1.2322 will resume medium term rise to 1.2494/2516 key resistance zone next. At this point, we'd expect strong resistance from there to limit upside and bring reversal. On the downside, break of 1.2088 will argue that EUR/USD has topped earlier than expected. In that case, intraday bias will be turned to the downside for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.

Yen Rebounds Strongly Before Weekly Close, Dollar Follows

Dollar is trying to recover again as markets are heading for weekly close. But the greenback is overwhelmed by the rebound in Yen. There was some concerns over US government shut down. But with the spending bill passed in the House already, vote in the Senate should be just procedural. Sterling is also paring some gains after weaker than expected retail sales. Meanwhile, in spite of solid data from Canada, the Loonie is also trading mildly softer. From Canada, manufacturing sales rose 3.4% mom in November, international securities transactions dropped to CAD 19.56b.

German SPD to vote on coalition on Sunday

In Germany, 600 Social Democrats (SPD) delegates will vote on Sunday on the proposal to start formal coalition talks with Chancellor Angela Merkel's CDU/CSU this Sunday. The vote will be the junction in German politics as either heading back to stability of grand coalition, or to another election. On the table is a 28-page policy framework, the production of the marathon preliminary talks between CDU/CSU and SPD.

Released from Europe, German PPI rose 0.2% mom, 2.3% yoy in December. Swiss PPI rose 0.2% mom, 1.8% yoy in December. Eurozone current account surplus widened to EUR 32.b in November. UK retail sales dropped sharply by -1.5% mom in December, below expectation of -0.9% mom.

Japan government upgraded economic assessment

The Japan Cabinet Office raised the economic assessment in the monthly economic report released today. The document noted that "Japan's economy is gradually recovering". Consumer spending is also seen as "recovering" too. Japan Economy Minister Toshimitsu Motegi said that "the difference between previous recoveries and the current recovery is that right now both the corporate sector and the household sector are steadily improving." Economists noted that global economic recovery will continue to help the export led Japanese economy. At the same time, there is little sign of a drag from domestic factors.

New Zealand manufacturing PMI tumbled sharply

New Zealand business NZ manufacturing PMI dropped sharply to 51.2 in December, down from 57.7. While it still stayed above 50 which signals expansions, the slowdown is notable. Looking in to the details, all five of the sub-indices declined with the biggest fall seen in new orders, from 57.3 to 50.2. BNZ noted that "anecdotal evidence, across the economy, suggests there was a post-election hiccup in activity as businesses put off major spending."

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2181; (P) 1.2222 (R1) 1.2281; More....

EUR/USD continues to be bounded in consolidative trading below 1.2322 and intraday bias remains neutral. More consolidations could be seen. But as long as 1.2088 resistance turned support holds, further rally is expected. Break of 1.2322 will resume medium term rise to 1.2494/2516 key resistance zone next. At this point, we'd expect strong resistance from there to limit upside and bring reversal. On the downside, break of 1.2088 will argue that EUR/USD has topped earlier than expected. In that case, intraday bias will be turned to the downside for 1.1915 support first.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494. Break of 1.1553 support will confirm completion of the rise. However, sustained break of 1.2516 will carry larger bullish implication and target 38.2% retracement of 1.6039 to 1.0339 at 1.3862.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:30 | NZD | Business NZ Manufacturing PMI Dec | 51.2 | 57.7 | ||

| 07:00 | EUR | German PPI M/M Dec | 0.20% | 0.20% | 0.10% | |

| 07:00 | EUR | German PPI Y/Y Dec | 2.30% | 2.30% | 2.50% | |

| 08:15 | CHF | Producer & Import Prices M/M Dec | 0.20% | 0.40% | 0.60% | |

| 08:15 | CHF | Producer & Import Prices Y/Y Dec | 1.80% | 2.10% | 1.80% | |

| 09:00 | EUR | Eurozone Current Account (EUR) Nov | 32.5B | 31.3B | 30.8B | 30.3B |

| 09:30 | GBP | Retail SalesM/M Dec | -1.50% | -0.90% | 1.10% | |

| 13:30 | CAD | Manufacturing Sales M/M Nov | 3.40% | 2.00% | -0.40% | -0.60% |

| 13:30 | CAD | International Securities Transactions (CAD) Nov | 19.56B | 15.76B | 20.81B | 20.77B |

| 15:00 | USD | U. of Mich. Sentiment (JAN P) | 97 | 95.9 |

US Investors Shrug Off Shutdown Fears

- US Futures Suggest Government Shutdown No Big Deal;

- GBPUSD Steady Despite Weaker UK Retail Sales;

- Bitcoin Finds its Feet But More Downside Possible.

US Futures Suggest Government Shutdown No Big Deal

US equity markets are seen reversing Thursday's losses at the open on Friday, even as investors prepare for the first government shutdown since 2013 if the Senate doesn't pass a temporary spending bill.

Investors don't appear particularly bothered about the prospect of a government shutdown, with the assumption being that one will eventually be signed and any economic impact will be minor or non-existent. While the US dollar has remained under significant pressure, there is little to suggest this is related to the budget talks while rising US yields is likely more a reflection of the general central bank tightening environment.

Equity investors seem unfazed, despite small losses being seen on Thursday. A temporary spending bill may have passed through the House but getting it through the Senate will be far more challenging making a shutdown likely. The question now is how long the shutdown will last as that will determine what, if anything, the economic impact could be. The last shutdown lasted a couple of weeks and the long-term impact was marginal which may explain the current relaxed attitude towards another.

GBPUSD Steady Despite Weaker UK Retail Sales

There isn't too much else on the agenda as we head into the end of the week with a small amount of companies releasing earnings and UoM consumer sentiment the only notable data point. The consumer is an extremely important part of the US economy and the data is expected to break with a couple of months of softer numbers, with the survey seen rising back to 97 in January.

The pressure on the US dollar has eased up a little as we approach the open but there is clearly substantial negative sentiment towards it, as clearly seen earlier in the European session when the UK released much weaker than expected retail sales data and yet cable rose shortly after. The dollar has since made a small recovery since and now trades down only a tenth of one percent on the day.

Bitcoin Finds its Feet But More Downside Possible

Bitcoin appears to have found its feet following another sharp sell-off earlier in the week. Having dipped below $10,000 on Wednesday, prices have recovered a little although there still doesn't appear to be much appetite at this stage, particularly compared to how aggressively dips were being bought towards the end of last year.

It's clear that we're seeing speculators being shaken out here which means any sustainable move higher this time around may be more gradual. While some are questioning whether this is the beginning of the end, I think it's more a case of the cryptocurrency – and others – heading back to where they should have been trading at this moment, rather than the frenzy-driven levels that they actually achieved. I think there could still be some more downside for bitcoin unless it quickly arrests the slump.

Dollar Index Holds Losses on Funding Bill Uncertainty; European Stocks Hit Fresh Highs

Here are the latest developments in global markets:

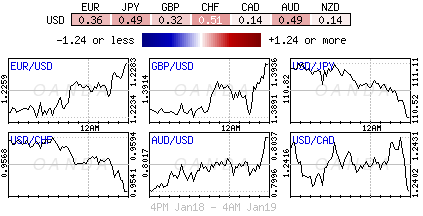

FOREX: The dollar index remained pressured near three-year lows, at 90.34 (-0.16%), as investors were waiting for US Senators to prevent a potential government shutdown today. Traders were also pricing that the dollar might lose steam versus its peers if other central banks follow the Fed by tightening monetary policy. Dollar/yen lost 0.38%, retreating to an intra-day low of 110.48. Pound/dollar reversed today's gains, edging down to 1.3873 after monthly retail sales in the UK declined more than expected in December, seeing the biggest fall since the beginning of 2017. Euro/dollar inched up to 1.2259 (+0.18%) and euro/pound rose to 0.8833 (+0.28%).

STOCKS: European stocks headed higher with mining sectors leading the gains and offsetting losses in energy shares after China reported a robust industrial data.The pan-European STOXX 600 jumped to fresh 2 ½-year highs and the blue-chip Euro STOXX 50 held onto gains, supported by optimism on global economic performance. The former rose by 0.45% and the latter by 0.40% at 1100 GMT. The German Dax 30 surged by 1.08%, the French CAC 40 gained 0.56%, while the British FTSE 100 rose by 0.31%. Concerns on profits from Dignity and Carpetright as well as a drop in last month's retail sales weighed on British stocks.

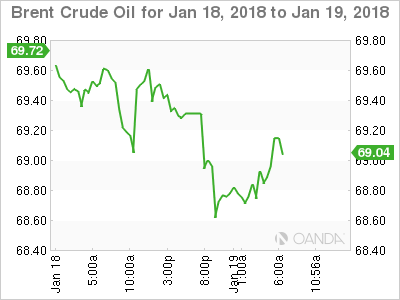

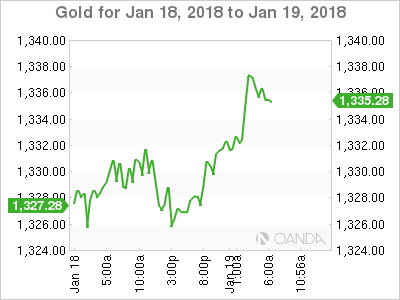

COMMODITIES: Oil prices managed to pare part of earlier losses after the International Energy Agency said on Friday that global oil markets are tightening faster due to falling supplies in Venezuela which are currently at 30-year lows and are projected to decline even further. WTI crude bounced to $63.64 per barrel (-0.83%) and Brent crawled up to $68.72 (-0.89%) but both remained relatively weak on the day. Gold consolidated around $1,335 per ounce, remaining 0.61% up on the day.

Day ahead: US Senate votes on government's spending bill

Economic releases will be limited during the rest of the day, with the US and Canada releasing data on consumer sentiment and manufacturing sales respectively.

At 1330 GMT, Canadian manufacturing sales for the month of November are expected to post a strong rebound, rising by 2.0% m/m after falling by 0.4% in October. This would be the highest growth seen in a year.

In the US, the University of Michigan will give preliminary estimates on US consumer sentiment for the month of January at 1500 GMT. Analysts anticipate the index, which gauges the relative level of current and future economic conditions, to take off from three-month lows and climb by 1.1 points towards 97.

A Senate vote on the government's funding bill, though, will be in main focus in the US as the bill which has been extended three-times so far expires today. Yesterday, the House of Representatives approved a spending bill through February 16 but the battle might be harder in the Senate as some Republicans and Democrats Senators recently expressed their opposition to the House bill. Now markets believe that the Senate might pass a shorter-time-period funding bill in order to avoid a potential government shutdown and gain more time to negotiate the plan.

In oil markets, Baker Hughes will issue readings on the US oil rig count at 1800 GMT. In other news, OPEC and non-OPEC members will gather in Oman over the next two days to review their strategy to cut global supply, with the Russian energy minister Alexander Novak saying that the meeting could include mechanisms to gradually exit supply cuts after the deal concludes in the end of the year.

Turning to public appearances, the Boston Fed President John Williams will participate in an informal discussion titled "Thoughts on the Economy" at 1345 GMT. The Fed Vice Chair for Supervision, Randal Quarles will follow later at 1800 GMT, speaking on Bank Regulation before the American Bar Association Banking Law Committee annual meeting, while the San Francisco Fed President John Williams will also be talking at a Bay Area forecasting conference at 1830 GMT. All three are FOMC voting members.

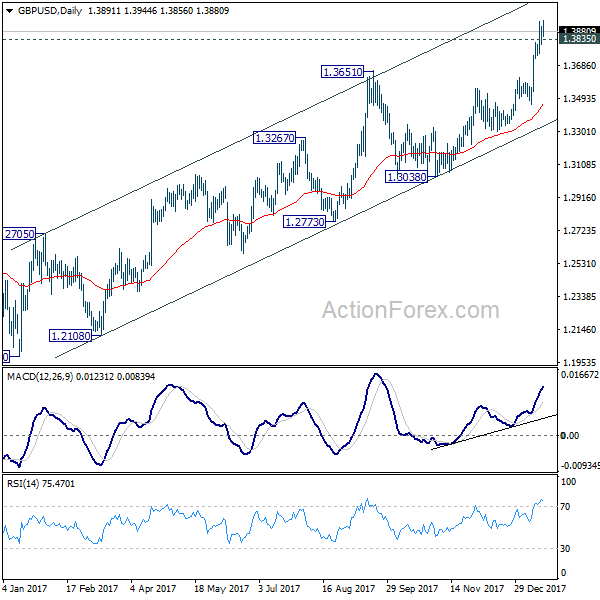

GBPUSD Likely to Push Higher While Above 1.3880

The British pound remains increasingly volatile against the U.S dollar, with the pair whipsawing to a new 2018 high, hitting 1.3944, during the European trading session. The GBPUSD pair initially spiked lower towards the 1.3900 level, after UK Retail Sales came in much weaker than forecasted, falling -1.5 percent during the month of December. Price-action currently trades around the 1.3910 level, as traders await the upcoming release of the Michigan Consumer Sentiment Index from the United States economy.

Intraday sentiment on the GBPUSD pair remains strongly bullish while price-action trades above the 1.3880 level. Further upside towards the 1.3944 and 1.4030 still seems possible.

Should price-action on the GBPUSD pair start to trade below the 1.3880 level, further downside towards the 1.3830 and 1.3758 support levels may occur.

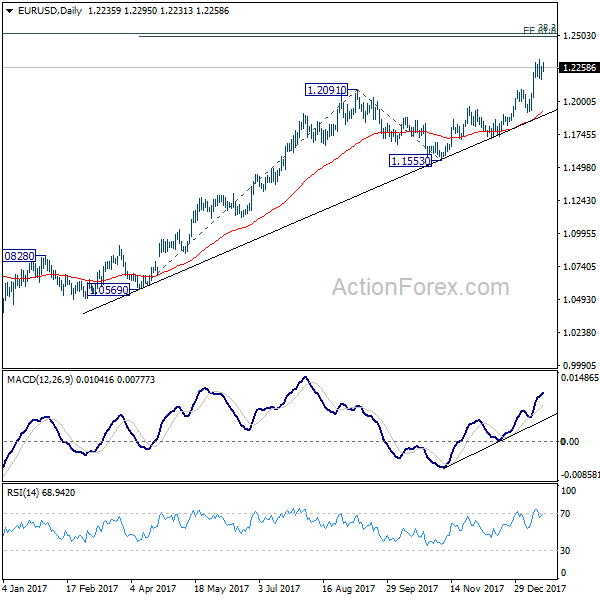

EURUSD Intraday Bullish Bias Intact Above 1.2258

The euro has move higher against the U.S dollar during the European session, hitting 1.2294, as the U.S dollar index declines to fresh 3-year trading lows. The EURUSD pair moved higher, amidst strong selling in the greenback, as U.S lawmakers work to avoid a U.S government shutdown next week. Price-action currently trades around the 1.2270 level, with the pairs weekly trading high still intact, at 1.2320. Traders now look to the release of high-impact U.S macro-economic data, whilst a host of Federal Reserve members are out delivering scheduled speeches.

The EURUSD remains strongly bullish while price-action traders above the 1.2258 level, further upside towards 1.2320 and 1.2350 seems possible.

Should the EURUSD move below the 1.2258 level, sellers may push price-action towards the 1.2200 and 1.2155 support levels.

Canadian Dollar Quiet Ahead of Key Manufacturing Report

USD/CAD is trading sideways in the Friday session. Currently, the pair is trading at 1.2426, up 0.07% on the day. On the release front, there are two key releases on the schedule. Canada will release Manufacturing Sales, which are expected to rebound with a strong gain of 1.9%. The US publishes UoM Consumer Sentiment, with an estimate of 97.0 points.

As was widely expected, the Bank of Canada pressed the rate trigger on Wednesday, raising interest rates by 25 basis points, from 1.00% to 1.25%. However, traders hoping for a stronger loonie were disappointed, as dovish comments from BoC Governor Stephen Poloz kept the currency from making headway against the US dollar. Poloz noted his concerns over NAFTA, the three-way free trade agreement which is crucial to the Canadian economy. US President Trump has threatened to cancel the pact unless Mexico and Canada make major concessions to the US. If the agreement is terminated, the Canadian dollar would likely take a tumble. Another round of negotiations is slated to be held in Montreal next week, and a lack of progress could weigh on the Canadian dollar.

Capitol Hill is in the headlines on Friday, as a Federal government shutdown will take effect at midnight Friday, if Congress does not vote on a short-term spending bill. The House of Representatives passed such a bill on Thursday, but Republicans face a tougher battle in the Senate. A 60-seat majority is needed for the measure to pass, which means that the Republicans, who have a 51-49 majority, will need substantial support from the Democrats. However, many Democrat lawmakers are incensed over President Trump's threat to deport young illegal immigrants and his recent inflammatory language against immigrants from poor countries. A government shutdown last occurred in 2013, and resulted in temporary layoffs for 800,000 non-essential Federal workers. With an election year in 2018, lawmakers from both parties will not want to anger voters, so we could see a last minute compromise which prevents a shutdown. However, if the shutdown takes place, risk appetite could dampen, and that could mean minor currencies like the Canadian dollar could be under pressure.

U.S Dollar Shutdown

The U.S dollar again trades atop of its three-year lows against G10 currency pairs while Treasuries yields trade steady after yesterday's bond selloff as capital markets weigh up the reality of potential U.S government shutdown and signs of domestic/global inflation picking up.

The once 'mighty' dollar is heading for a sixth week of losses before the federal spending authority is due to expire at midnight today Friday (12:01 am EDT).

European stocks are following their Asian counterparts higher while U.S futures point to small gains.

Global crude prices have extended their retreat from its three-year highs and gold has climbed for the first time in four-days to minimize its first weekly loss in six-weeks.

Beware: Germany's SDP are holding their convention on Sunday Jan 21 on whether to pursue formal talks with Chancellors Merkel's CDU-led bloc on forming a government. It could be a bumpy open in Asia for the EUR (€1.2266).

1. Stocks see the 'light'

Overnight in Japan, the Nikkei share average edged up on Friday with financial stocks leading the gains after U.S yields backed up to three-year high yields. The Nikkei rose +0.2%, while the broader Topix gained +0.7%.

Down-under, Aussie shares edge lower as miners slide. The S&P/ASX 200 index fell -0.2% at the close of trade. It fell -1.1% over the week, a second consecutive weekly fall. In S. Korea, the Kospi gained +0.1%.

In Hong Kong, the Hang Seng ends at a new peak, up for six-weeks in a row. At close of trade, the Hang Seng index was up +0.41%. For the week, the index rallied +2.7%, while the Hang Seng China Enterprises index rose +0.65%.

In China, stocks scaled a two-year high after a solid GDP print Thursday. The Shanghai Composite index was up +0.41%, while the blue-chip CSI300 index was up +0.35%.

In Europe, regional indices trade higher across the board, tracking higher futures in the U.S, which have reversed earlier declines as the threat of a U.S government shutdown looms.

U.S stocks are set to open in the black (+0.3%).

Indices: Stoxx600 +0.4% at 400.3, FTSE +0.1 at 7712, DAX +0.9% at 13399, CAC-40 +0.5% at 5520, IBEX-35 +0.4% at 10470, FTSE MIB +0.6% at 23785, SMI +0.4% at 9491, S&P 500 Futures +0.3%.

2. Oil prices fall as U.S. output rise outweighs crude stock falls, gold higher

Oil prices are on the back foot ahead of the U.S open, which puts them on course for the biggest weekly fall in three months, as a bounce-back in U.S production outweighs the ongoing declines in crude inventories.

Brent crude futures are at +$68.70 a barrel, down -61c from Thursday's close. On Monday, they hit their highest price in three-years at +$70.37. U.S. West Texas Intermediate (WTI) crude futures are at +$63.38 a barrel, down -57c from their last settlement. WTI marked a December-2014 peak of +$64.89 a barrel on Tuesday.

The IEA monthly report has maintained its 2018 global demand growth forecast, but has also seen a surge in non-OPEC supplies as prices rise – U.S and Canada.

Note: EIA data shows that U.S crude oil production stands at +9.75m bpd and expects this to soon exceed +10m bpd, overtaking OPEC's Saudi Arabia and rivalling Russia.

Ahead of the U.S open, gold prices are trading higher (+0.1% at +$1,328.98 an ounce), supported by a weaker dollar and worries about a possible U.S government shutdown, but the precious metal is still on track for its first weekly drop in six-weeks. Yesterday, the yellow metal touched its weakest level since Jan. 12 at +$1,323.70, having fallen from recent four-month highs. Spot gold has fallen -0.8% so far this week.

3. Sovereign yields back up

Market optimism about global growth is finally having an impact on the bond markets. With investors factoring in the prospect of accelerating price increases is backing up sovereign yield curves. Yesterday's sale of U.S bonds that offer a hedge against faster inflation attracted very strong demand.

Note: U.S Treasury +$13B 10-year TIPS drew +0.548% with a bid-to-cover of +2.69 – the strongest BTC since May 2014.

Better-than-expected growth numbers from China this week has also added to a slew of recent global data releases supporting the positive outlook. Next week two of the major G7 central banks will hog the limelight – Bank of Japan (BoJ) monetary policy decision and briefing on Jan. 23, while the European Central Bank (ECB) rate decision is on Jan. 25.

The yield on 10-year Treasuries increased +1 bps to +2.63%, the highest in more than three years. In Germany, the 10-year bund yield has gained +1 bps to +0.58%, while the U.K 10-year yield Gilt climbed less than +1 bps to +1.331%, the highest in a week.

4. Dollar Shutdown

The consensus is that the impact on the USD in case of a U.S government shut-down should be more pronounced this time compared with other times when the government stopped working, like in 2013 when the dollar's reaction was relatively muted.

The dollar is already on the back foot on the uncertainty over whether the short-term funding bill to prevent a shutdown will be passed today with the EUR/USD rising +0.3% to €1.2272 and USD/JPY falling -0.4% to ¥110.63.

Note: The bill still needs to go through the Senate and the Republicans need at least nine Democrats to back it up. So far only one Democrat has said he will vote yes.

Sterling remains volatile after data this mornings disappointing U.K retail sales number (see below). GBP/USD is last up +0.1% at £1.3910, compared with £1.3933 before the data. EUR/GBP is up +0.2% at €0.8828, roughly where it was beforehand.

5. U.K retail sales had steepest December drop in seven years

Data this morning showed that U.K retail sales fell sharply in December; with Britons paring back their spending after taking advantage of “Black Friday” in November.

Monthly retail sales fell by -1.5% compared with the previous month. This was nearly double the decline anticipated by the street and the steepest monthly drop since June 2016, the month of the Brexit referendum, and the biggest decline for that month in seven years.

Note: The fall followed a +1.0% monthly increase in November, driven by Black Friday discounts as well as by Britons' early Christmas purchases.

Compared with the same month a year earlier, sales grew by +1.4%

DAX Jumps On Eurozone Current Account, Surplus, U.S Gov. Shutdown Worries

The DAX has posted strong gains in the Friday session. Currently, the index is trading at 13,407.00, up 0.94% on the day. On the release front, it’s a quiet end to the trading week. The Eurozone Current Account Surplus widened to EUR improved to 32.5 billion, beating the estimate of EUR 31.3 billion.

A booming German economy is not without its problems. Case in point, the country’s large current account and budget surpluses. A strong demand for German products, record low unemployment and the ECB’s expansionary monetary policy have all contributed to the surpluses. What should be done with all these funds? This was a source of disagreement a recent conference in Frankfurt, hosted by the IMF and German Bundesbank. IMF Managing Director Christine Lagarde suggested that Germany should increase public spending. However, Bundesbank President Jens Weidmann acknowledged that the surpluses may be getting too large, but that increasing public expenditures was not the solution. With the German economy far outpacing its eurozone peers, most of them would likely envy Germany’s quandary over what to do with large surpluses. Weidmann made headlines earlier in the week, when he stated that he did not expect interest rates to rise until mid-2019, even if QE ends in late 2018. If Weidmann reiterates this stance on Thursday, investors may take note and the euro could backtrack on some of its recent gains.

The markets are glued to Washington, where a Federal government shutdown will take place on Saturday if Congress does not reach agreement on a short-term spending bill. The House of Representatives passed such a bill on Thursday, but Republicans face a tougher battle in the Senate. A 60-seat majority is needed for the measure to pass, which means that the Republicans, who have a 51-49 majority, will need substantial support from the Democrats. However, many Democrat lawmakers are incensed over President Trump’s threat to deport young illegal immigrants and his recent inflammatory language against immigrants from poor countries. A government shutdown last occurred in 2013, and resulted in temporary layoffs for 800,000 non-essential Federal workers. With an election year in 2018, lawmakers from both parties will not want to anger voters, so we could see a last minute compromise which prevents a shutdown.