Sample Category Title

Fed’s Waller downplays tariff impact, warns against policy paralysis

Fed Governor Christopher Waller downplayed concerns that tariffs would have a significant, lasting impact on inflation, stating that their effect is likely to be “modest” and “non-persistent.” As a result, he favors “looking through” these effects when setting policy.

In a speech overnight, he emphasized that while economic uncertainty remains, Fed cannot afford to fall into a “recipe for policy paralysis” by waiting for absolute clarity regarding the administration's policies.

However, he conceded that tariffs could have a larger impact than expected, depending on their size and implementation. At the same time, he pointed out that other policies under discussion could have positive supply-side effects, helping to ease inflationary pressures.

Waller defended Fed’s decision to hold rates steady in January, arguing that the current economic data “are not supporting a reduction in the policy rate at this time.”

He left the door open for future rate cuts, stating that “if 2025 plays out like 2024, rate cuts would be appropriate at some point this year.”

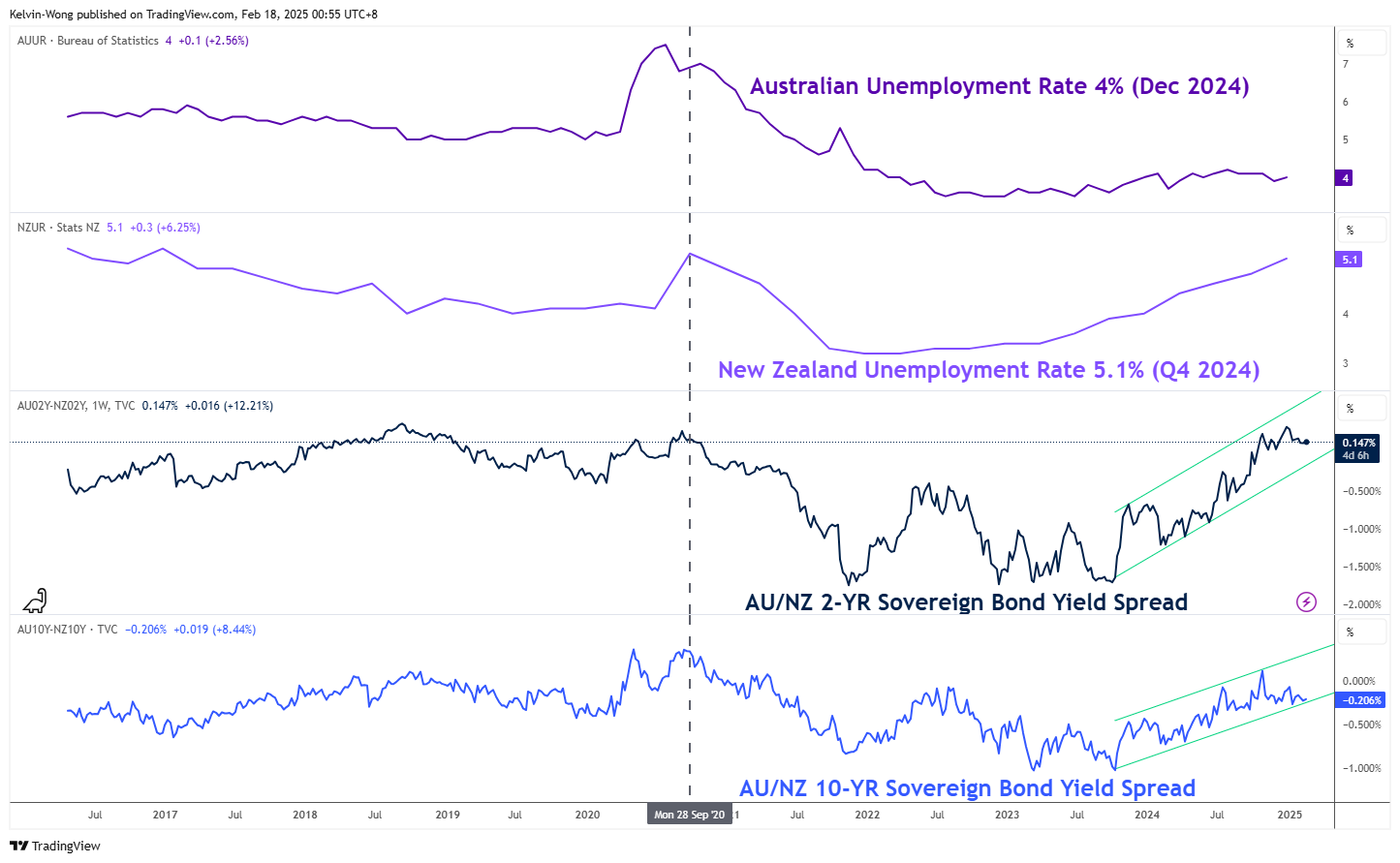

AUD/NZD: Further Aussie Outperformance Over Kiwi Supported by a Weaker New Zealand Labour Market

- New Zealand’s unemployment rate has accelerated to 5.1% in Q4 2024, a whisker below its Covid peak of 5.2% while Australia’s unemployment rate remained stable at 4%.

- A further steepening of yield spreads between Australian and New Zealand sovereign bonds may trigger further upside in the AUD/NZD cross rate.

- Watch the 1.0980 key medium-term support on AUD/NZD.

This week, the Antipodean countries’ central banks will decide their respective monetary policy; Australia’s RBA on Tuesday, 18 February, and New Zealand’s RBNZ on the following day on 19 February.

The Aussie and Kiwi have strengthened against the US dollar since 3 February when US President Trump “fired” his trade tariffs salvo against Canada, Mexico, and China. The AUD/USD and NZD/USD rallied by 4.6% and 4% in the past two weeks from their respective 3 February lows to 17 February at this time of writing.

Market participants have started to price in 25 basis points (bps) cut by RBA, its first cut in four years after being “late” to the global interest rate cut cycle (excluding Bank of Japan) to reduce its policy cash rate to 4.1%. A slowdown in the Australian inflation trend came in faster than the RBA anticipated where the trimmed mean gauge of consumer rose 3.2% y/y in Q4 2024 versus a higher consensus expectation of 3.3%.

Meanwhile, New Zealand’s RBNZ is expected to deliver another “jumbo size rate cut” of 50 bps after three consecutive rate cuts conducted in 2024 to reduce its official cash rate to 3.75% due to a deceleration in inflation trend and a rapid slowdown in growth conditions. Business confidence has declined for three consecutive months coupled with a 22-month streak of contraction in manufacturing PMI data.

A weaker New Zealand labour market is supporting a further steepening of AU/NZ sovereign bonds’ yield spread

Fig 1: AU & NZ unemployment rate with 2-year & 10-year yield spreads of AU/NZ government bonds as of 18 Feb 2025 (Source: TradingView, click to enlarge chart)

New Zealand’s unemployment rate has accelerated to 5.1% in the three months through December 2024 which is almost its Covid peak of 5.2% recorded in Q3 of 2020 (see Fig 1).

Meanwhile, the unemployment rate for Australia remained stable at 4% for its latest reading of December 2024, within the range of 4.1% to 3.7% recorded in 2024.

The bleaker labour market condition in New Zealand increases the odds that RBNZ is likely to adopt a relatively more dovish monetary policy in 2025 over RBA.

Therefore, the 2-year and 10-year yield spreads between Australia and New Zealand sovereign bonds are likely to steepen further and, in turn, may ignite upside pressure on the AUD/NZD cross rate.

Potential bullish change of trend for AUD/NZD

Fig 2: AUD/NZD major and medium-term trends as of 18 Feb 2025 (Source: TradingView, click to enlarge chart)

Since 17 July 2024, the price actions of AUD/NZD have not been above to break above a “stubborn” range resistance of 1.1165/1190 as it continued to consolidate above a rising 200-day moving average.

Several positive technical elements have emerged that support a potential impending bullish breakout above 1.1165/1190 for the AUD/NZD.

Firstly, its price actions have started to trade above its 50-day moving average since 4 February.

Secondly, the daily MACD trend indicator has just staged a bullish breakout from its descending trendline resistance, and its centreline on 10 February suggests a potential start of a medium-term bullish momentum condition that may lead to higher price actions on the AUD/NZD (see Fig 2).

Watch the 1.0980 key medium-term pivotal support and clearance above 1.1190 may see the next medium-term resistances coming in at 1.1245 and 1.1430/1460 (also the upper boundary of a major ascending channel from 22 February 2024)

However, failure to hold above 1.0980 invalidates the bullish scenario for a corrective decline to expose the next medium-term supports at 1.0850 and 1.0735.

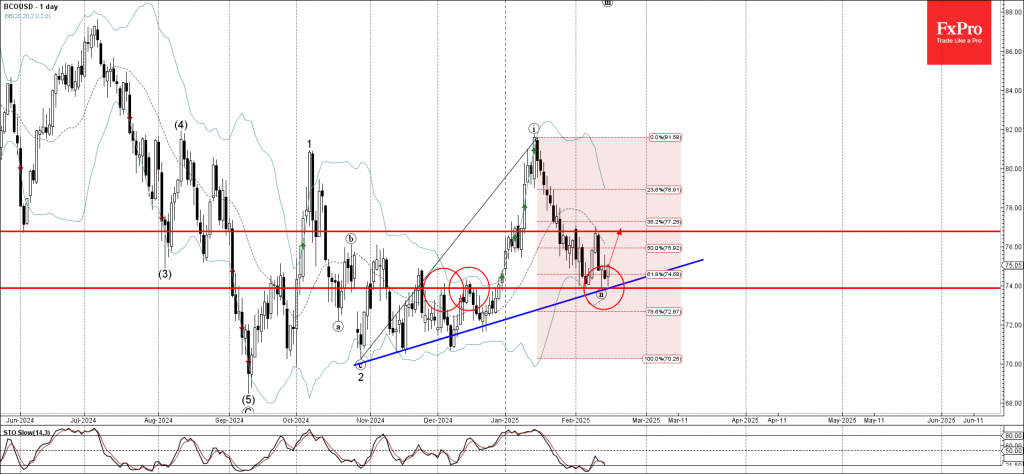

Brent Crude Oil Wave Analysis

- Brent Crude Oil reversed from support zone

- Likely to rise to resistance level 76.75

Brent Crude Oil recently reversed up from the support zone between the key support level 74.00 (former strong resistance from December), lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from October.

The upward reversal from this support zone stopped the previous short-term ABC correction ii from the middle of January.

Given the bullish divergence on the daily Stochastic, Brent Crude Oil can be expected to rise to the next resistance level 76.75.

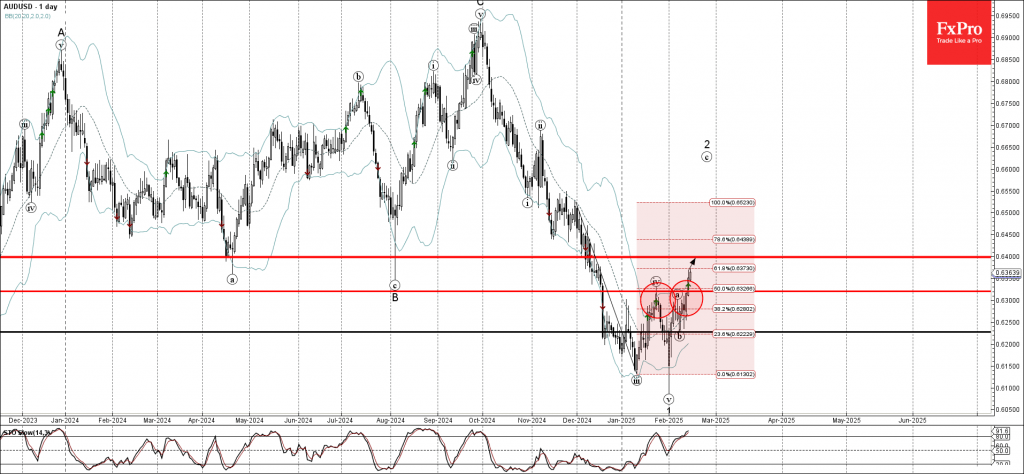

AUDUSD Wave Analysis

- AUDUSD broke the resistance zone

- Likely to rise to resistance level 0.6400

AUDUSD currency pair recently broke the resistance zone between the key resistance level 0.6320 (which stopped the previous minor correction iv) and the 50% Fibonacci correction of the downward impulse from December.

The breakout of this resistance zone accelerated the c-wave of the active ABC correction 2.

AUDUSD currency pair can be expected to rise to the next resistance level 0.6400 (former strong support from April and August of 2024).

Fed’s Bowman calls for patience, cites inflation risks and policy uncertainty

Fed Governor Michelle Bowman explained in a speech her support for keeping interest rates unchanged last month, citing the need for a patient approach while monitoring inflation developments.

She noted that after a 100 basis point rate adjustment through December, policy is now in a "good place," allowing the Fed to "pay closer attention to the inflation data as it evolves."

Bowman also highlighted the importance of assessing the impact of the administration’s policies on the broader economy, stressing the need for a "better sense of these policies" and their implementation.

On inflation, Bowman maintained a cautious outlook, expecting further moderation this year but warning that disinflation progress could remain "bumpy and uneven." Bowman noted her concerns about “greater risks to price stability”, particularly with a still-strong labor market.

Fed’s Harker signals no rush for rate cuts amid economic resilience

Philadelphia Fed President Patrick Harker said in a speech today that the US economy continues to operate from a “position of strength”. While inflation remains above target, Harker expressed confidence that it is on track to ease over time, supported by resilient economic growth and a balanced labor market.

These factors, in his view, are "reasons enough for holding the policy rate steady."

Harker avoided committing to a specific timeline for policy easing but stated that he remains “optimistic” about inflation’s continued decline, which would eventually allow Fed to lower rates “over the long run”.

However, he acknowledged uncertainty surrounding new economic policies, particularly regarding tariffs and immigration policies under President Trump’s administration.

Many economists warn that a combination of higher import taxes and stricter immigration measures could fuel inflation, complicating the Fed’s job of maintaining price stability. Harker admitted that the full impact of these policies remains unknown.

AUD/USD: Holds Near New 2025 High Ahead of RBA Rate Decision

AUDUSD hit new 2025 high on Monday (the highest since mid-December) in extension of broader rally in past two weeks (up nearly 5% on bounce from the lowest level in almost four years).

Weaker US dollar continue to fuel Aussie dollar’s advance, which turned the picture on daily chart positive and generating initial reversal signal.

Near-term action is moving within thick daily Ichimoku cloud and underpinned by formation of daily Tenkan/Kijun-sen) bull-cross, focusing key resistances at 0.6410/14 (daily cloud top / Fibo 38.2% of 0.6942/0.6087 downtrend).

Break of these levels to confirm reversal signal, though increased headwinds should be expected at this zone on overbought conditions and RBA’s rate decision in early Tuesday.

The Australia’ central bank is widely expected to cut interest rates by 25 basis points on Tuesday’s policy meeting, in the first rate cut in more than four years that will mark the beginning of monetary policy easing cycle.

Former top of Jan 24 (0.6330) offers immediate support, with near term bias to remain biased higher as long as the price action stays above strong 0.6300/0.6290 support zone.

Res: 0.6414; 0.6441; 0.6500; 0.6515.

Sup: 0.6330; 0.6290; 0.6235; 0.6194.

British Pound Eye Jobs Report

The British pound is showing little movement on Monday. In the North American session, GBP/USD is trading at 1.2592, up 0.06% on the day.

UK job growth expected to plunge

The markets are bracing for a sharp decline in employment in the three months to December, with a forecast of -130 thousand. This follows an increase of 36 thousand in the three months to November. Job growth has posted eight consecutive three-month periods of growth and the resilient labor market has eased pressure on the Bank of England to lower interest rates.

The unemployment rate is projected to creep up to 4.5% from 4.4%, and wage growth (including bonuses) is expected to rise to 5.9% in the three months to December, up from the previous release of 5.6%. Wage growth has been moving higher and is fueling inflation.

The Bank of England doesn’t meet till March 20 and after cutting rates earlier this month, back-to-back rate cuts remain unlikely. On Monday, Governor Andrew Bailey poured some cold water over last week’s better-than-expected GDP release, saying that the UK economy remained “quite static”. GDP for the fourth quarter eked out a gain of 0.1%, better than the BoE forecast of a contraction. The BoE remains concerned about sticky inflation and growing global political uncertainty.

The US ended the week with a disappointing retail sales report. January retail sales slid 0.9%, much worse than the market estimate of -0.1% and following a solid gain of 0.7% in December. This was the sharpest decline since March 2023, as severe weather and the Los Angeles fires dampened consumer spending. Annually, retail sales eased to 4.2%, down from an upwardly revised 4.4% in December and above the forecast of 3.7%.

GBP/USD Technical

- GBP/USD tested support at 1.2585 earlier. Below, there is support at 1.2539

- 1.2630 and 1.2676 are the next resistance lines

Sunset Market Commentary

Markets

The hastily arranged summit in Paris by French president Macron stood in the center of attention today. Last week’s string of events, involving US president Trump, his Defense Secretary Hegseth and VP Vance, created a sense of urgency. Both the EU and Ukraine want a say in the talks for a ceasefire and as such in the post-war security architecture on the old continent at a time when the US is effectively folding the NATO-umbrella. The European buy-in at that negotiation table is to invest massively in its own defense capacity after not having done so for decades. That’s what is being discussed at the Paris summit today by a handful of European leaders, accompanied by NATO secretary-general Rutte and EC president Von der Leyen. Outgoing German minister for Foreign Affairs Baerbock at the sidelines of the sobering Munich Conference flagged an upcoming “large package that has never been seen in this dimension before. Similar to the euro or the corona crisis, there is now a financial package for security in Europe.” Details of such a package won’t be released (officially, that is) until after the German elections on Sunday though. Either way, it’s yet another existential moment where Europe risks being marginalized, economically, militarily and politically by the other great powers that be, if it does not rise to the occasion. Member States in the past have shown they are ready and willing to overcome their differences whenever circumstances were at their direst: from the GFC over the migration crisis to the pandemic and the war-related energy crunch. We can only assume they will again. That should lead to a significant boost in defense expenditures, on a national level first before moving to the European level. The Next Generation EU framework that was created in the Covid aftermath serves as the perfect blueprint. The French minister for European Affairs said such joint European bonds should be discussed in the coming days. Speculation for such increased spending is flaring up today, especially for countries that have the most room to do so, i.e. Germany. Yields rise 1.7-6.4 bps in a bear steepening move. Bunds vs swap also underperform compared to other European nations. UK yields rise 0.5-3.4 bps on a net daily basis. Prime Minister Starmer, who joined the summit, said his country needed to lift defense spending as part of the new reality they are in now. US financial markets are closed for President’s Day. The Japanese yen outperforms on currency markets after Q4 GDP numbers exceeded expectations. USD/JPY eases to 151.51. Other dollar pairs trade muted in absence of the US. EUR/USD hovers near Friday’s closing levels just south of 1.05. DXY treads water at 106.85. Sterling strengthens to EUR/GBP 0.831 ahead of tomorrow’s labour market report, Wednesday’s CPI figures and Friday’s retail sales and PMIs.

News & Views

OPEC+ is considering delaying planned monthly oil supply increases (+120k barrels/day) set to begin in April. This would be the fourth postponement of production increases since 2022. The coalition, led by Saudi Arabia and Russia, aims to restore 2.2mn b/d by late 2026. Trump has urged OPEC to cut oil prices, but at currently $74.5/b (broadly unchanged on a daily basis), prices are still too low for many OPEC members to cover government spending. OPEC's decisions will prioritize long-term impacts with the group also concerned about the volatility caused by US trade tariffs. Even if OPEC+ maintains current output levels, global oil supplies are expected to exceed demand by 450,000 b/d this year according to the International Energy Agency.

The International Monetary Fund (IMF) has recommended that South Africa take bold steps to reduce its debt burden and boost economic growth. The IMF suggests a fiscal adjustment of 1% of GDP per year for three years, which would help lower public debt to more prudent levels of 60% to 70% of GDP within five to ten years from a projected 74.7% at the end of FY 2025. South Africa's debt-to-GDP ratio has risen significantly, and the country faces pressure to balance fiscal discipline with demands for increased spending. Key proposed measures include wage discipline, reforms at state-owned enterprises (SOEs), and tighter control of government procurement. The South African rand trades a tad softer today, bouncing off first technical support at USD/ZAR 18.30.