Sample Category Title

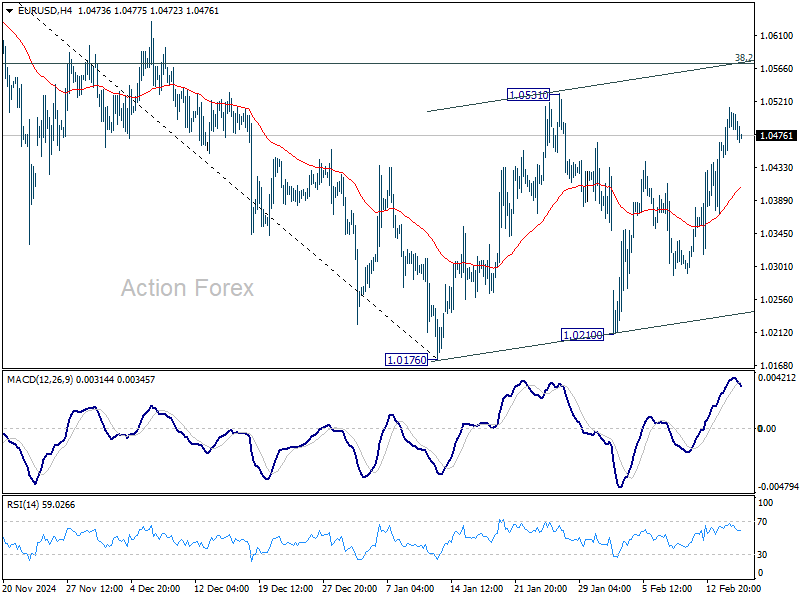

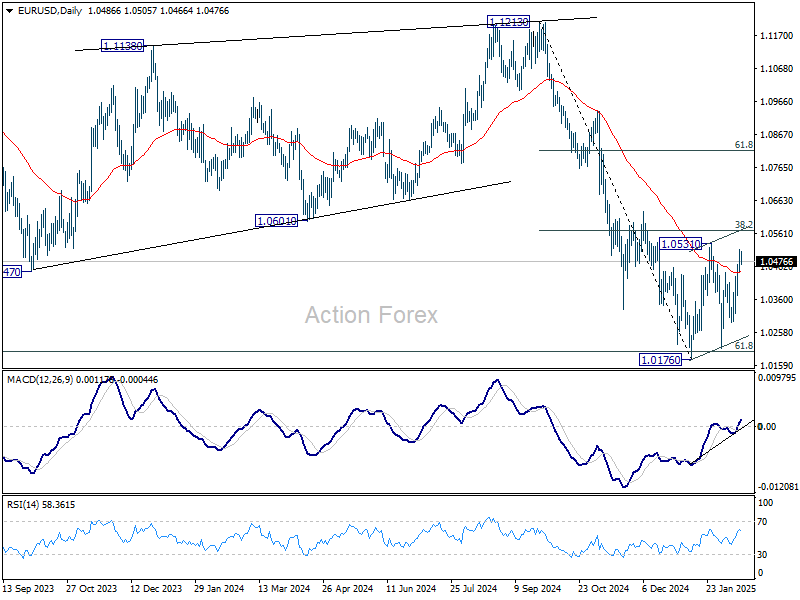

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0454; (P) 1.0484; (R1) 1.0521; More...

EUR/USD is staying in consolidation from 1.0176 and intraday bias remains neutral. Stronger rebound might be seen but outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

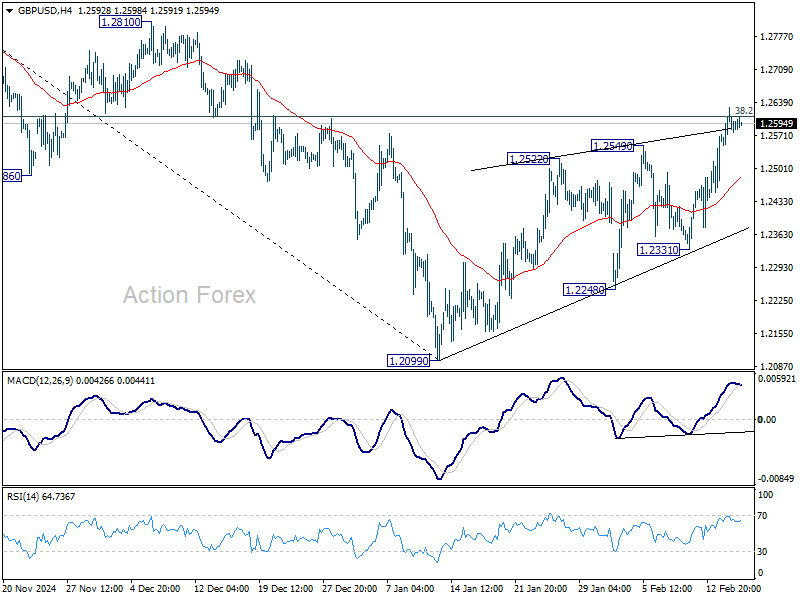

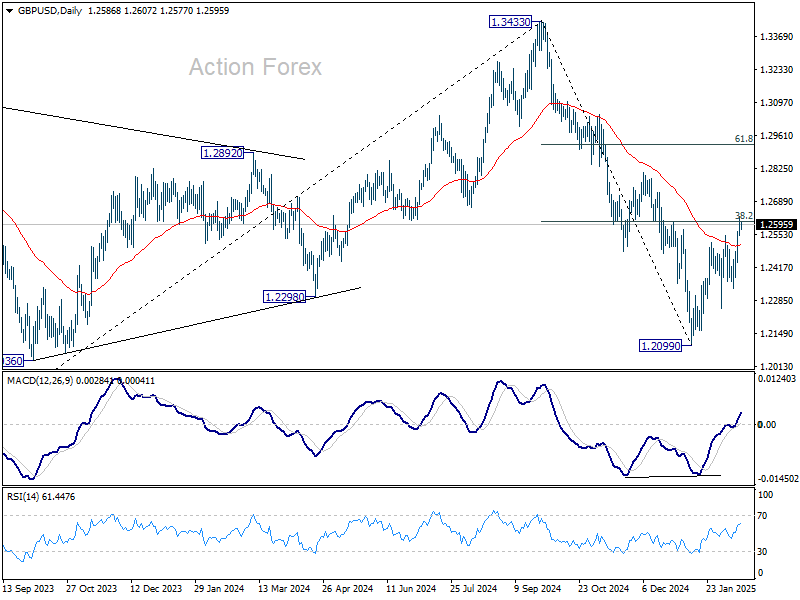

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2539; (P) 1.2585; (R1) 1.2630; More...

Intraday bias in GBP/USD remains neutral with focus on 38.2% retracement of 1.3433 to 1.2099 at 1.2609. Rejection by this level will keep near term outlook bearish. Break of 1.2331 support will suggest that the rebound from 1.2099 has completed as a correction, and bring retest of 1.2099 low. However, firm break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

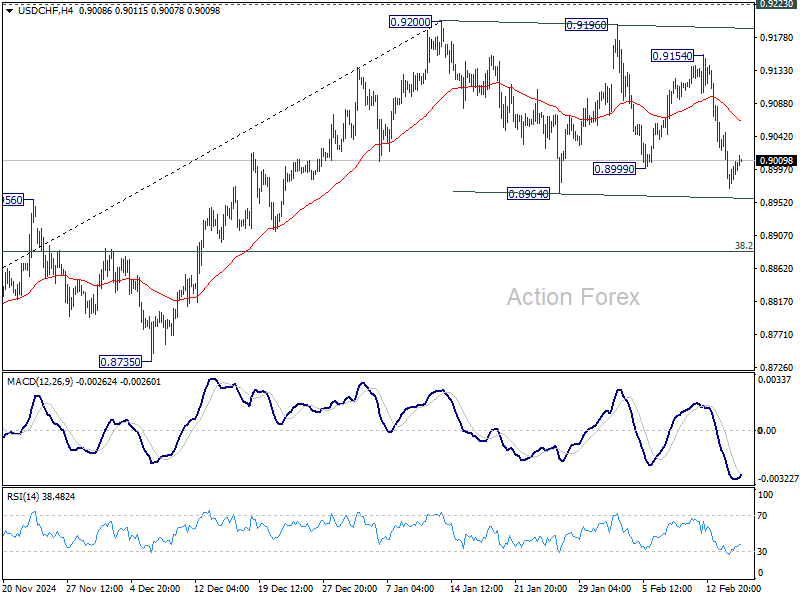

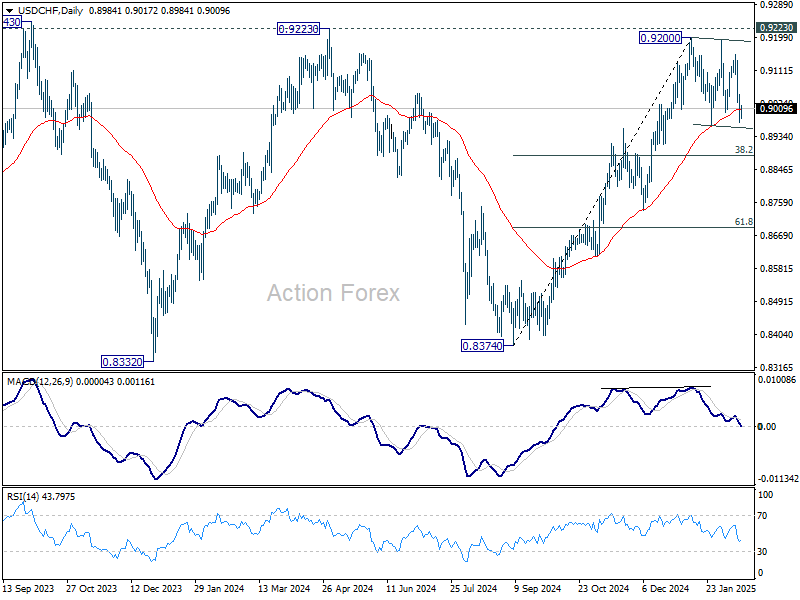

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8954; (P) 0.9017; (R1) 0.9061; More…

No change in USD/CHF's outlook as consolidation from 0.9200 is still extending. Intraday bias stays neutral at this point. While deeper pull back might be seen, outlook will stay mildly bullish as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, firm break of 0.9223 key resistance will carry larger bullish implication. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

Yen Extends Gains on Strong GDP

The Japanese yen continues to roll against the US dollar and has posted gains for a third straight trading day, gaining 1.9% during that time. In the European session, USD/JPY is trading at 151.43, down 0.53% on the day.

Japan’s Q4 GDP beats estimate

Japan’s GDP in the fourth quarter rose 0.7% q/q, blowing past the market estimate of 0.3% and above the upwardly revised 0.4% gain in the third quarter. This marked the third straight quarter of quarterly growth, pointing to stronger economic activity. On an annualized basis, GDP jumped 2.8%, well above the market estimate of 1% and beating the revised third-quarter GDP gain of 1.7%.

The strong GDP report was driven by an increase in exports. Private consumption gained just 0.1%, compared to a 0.7% gain in the third quarter and higher than the market estimate of -0.3%. The weakness in domestic demand, which was also reflected in a decline in imports, is weighing on economic growth.

Inflation continues to move higher, and December CPI hit 3% y/y, its highest annual level in 16 months. There are growing expectations that the Bank of Japan will again raise rates in the coming months, although the central bank isn’t signaling any particular dates. The BoJ raised rates by a quarter-point in January and the next meeting is on March 19.

The US wrapped up the week with a soft retail sales report. January retail sales slid 0.9%, much worse than the market estimate of -0.1% and following a solid gain of 0.7% in December. This was the sharpest decline since March 2023, as severe weather and the Los Angeles fires dampened consumer spending. Annually, retail sales eased to 4.2%, down from an upwardly revised 4.4% in December and above the forecast of 3.7%.

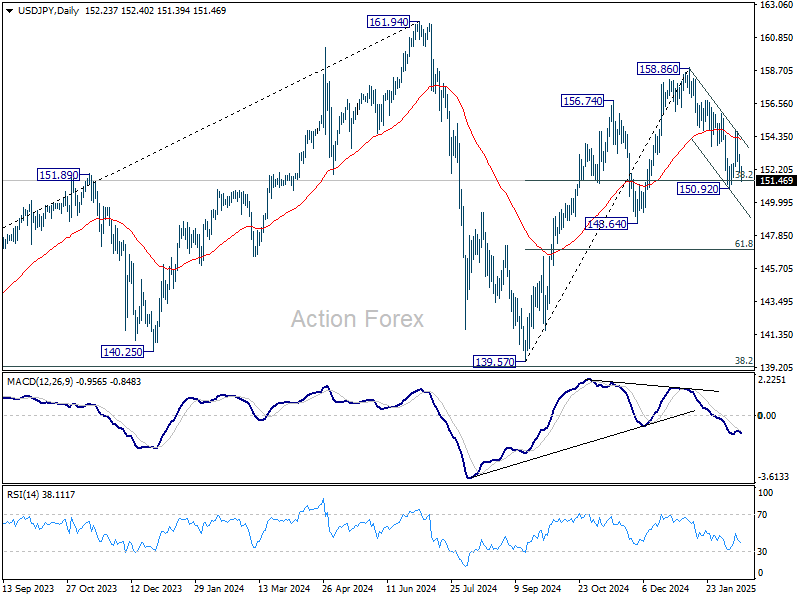

USD/JPY Technical

- USD/JPY has pushed below support at 151.86 and is putting pressure on support at 151.36

- 152.49 and 153.96 are the next resistance lines

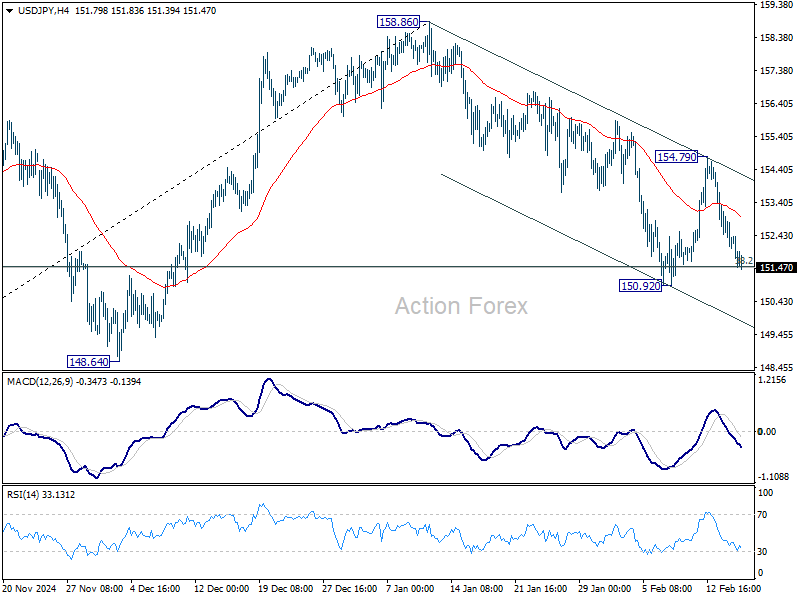

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.83; (P) 152.49; (R1) 152.96; More...

Intraday bias in USD/JPY remains neutral with focus on 38.2% retracement of 139.57 to 158.86 at 151.4. Strong rebound from there will maintain near term bullishness. On the upside, break of 154.79 will revive the case that correction from 158.86 has completed at 150.29. Further rise should be seen to retest 158.86 high. However, break of 150.92 and sustained trading below 151.49 will raise the chance of trend reversal, and target 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Strength Holds as Focus Turns to RBA Rate Cut

Yen remains the standout performer, even though momentum had moderated slightly. Discussions surrounding BoJ’s next move continue to dominate, particularly in a low-activity session with both US and Canadian markets closed for holidays.

After stronger than expected Japanese Q4 GDP report, market expectations for a July rate hike to 0.75% have strengthened to around 80%. However, the timeline could shift sooner if results from the upcoming Shunto wage negotiations indicate stronger-than-expected wage growth.

Looking further ahead, some analysts see BoJ’s policy rate reaching 1% by year-end, which would mark the lower bound of its own estimated neutral rate range of 1-2.5%. This shift in policy expectations has kept Yen well-supported against its peers for now.

In the upcoming Asian session, focus is turning toward RBA, which is widely anticipated to begin its easing cycle with a 25bps rate cut to 4.10%. A Reuters poll of economists showed that 31 out of 41 analysts expect another quarter-point cut in Q2, bringing rates down to 3.85%.

Among major Australian banks, ANZ, CBA, NAB, and Westpac all foresee a 25bps cut tomorrow, but their forecasts for cumulative cuts in 2025 vary between 50 and 100 basis points. Market participants will closely watch the RBA’s guidance and updated economic forecasts for further clues on the policy path ahead.

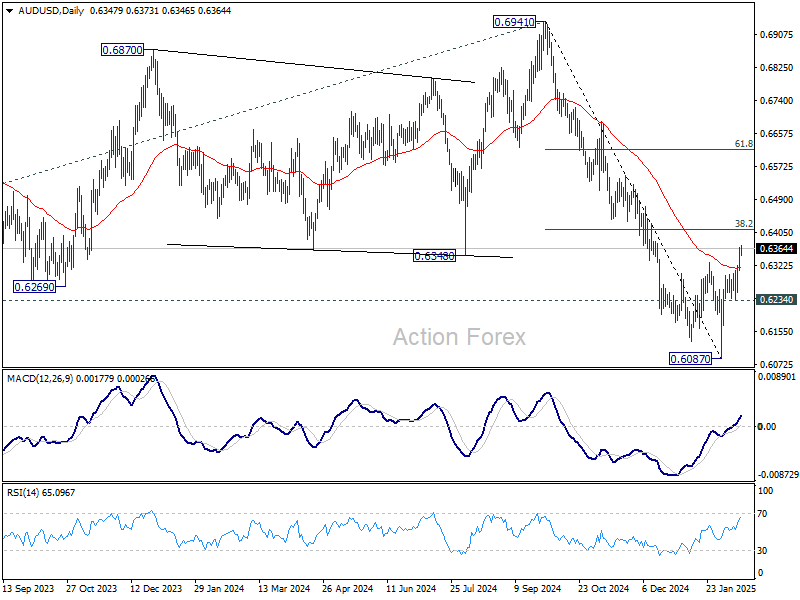

Technically, AUD/USD's rebound from 0.6087 is seen as a corrective move only, probably the first leg of a consolidation pattern to the decline from 0.6941. Strong resistance should be seen from 38.2% retracement of 0.6941 to 0.6087 at 0.6413 to limit upside. However, sustained break there could bring stronger rise to 61.8% retracement at 0.6615, even still as a correction.

In Europe, at the time of writing, FTSE is up 0.24%. DAX is up 0.93%. CAC is up 0.11%. UK 10-year yield is up 0.0414 at 4.551. Germany 10-year yield is up 0.056 at 2.490. Earlier in Asia, Nikkei rose 0.06%. Hong Kong HSI fell -0.02%. China Shanghai SSE rose 0.27%. Singapore Strait Times rose 0.71%. Japan 10-year JGB yield jumped 0.0362 to 1.393.

BoE’s Bailey sees ongoing gradual disinflation, warns of two-sided risks

BoE Governor Andrew Bailey reaffirmed today that the UK remains on "gradual disinflation" path, noting that the lingering effects of past economic shocks are slowly fading.

However, he emphasized that risks are “two-sided,” as highlighted in the BoE’s latest minutes, where differences within the committee surfaced.

On Q4 GDP data, which came in stronger than expected, Bailey downplayed its impact, stating that the economy has been “quite static” since late spring 2024.

Regarding the US government’s evolving stance on tariffs, Bailey expressed concerns about economic fragmentation, warning that such shifts could harm global growth.

However, he acknowledged that the inflationary impact from tariffs remains “ambiguous,” as it depends on factors such as “redirection of trade” and retaliatory measures.

He reiterated that risks exist on both sides, justifying the BoE’s use of “careful” alongside “gradual” in its policy guidance.

Eurozone goods exports rises 3.1% yoy in Dec, imports rises 3.8% yoy

Eurozone goods exports rose 3.1% yoy to EUR 226.5B in December. Goods imports rose 3.8% yoy to EUR 211.0B. Trade balance recorded EUR 15.5B surplus. Intra-Eurozone trade rose 1.7% yoy to EUR 191.5B.

In seasonally adjusted term, goods exports fell -0.2% mom to EUR 240.8B. Goods imports fell -0.8% mom to EUR 226.2B. Trade balance reported EUR 14.6B surplus, smaller than expectation of EUR 15.0B. Intra-Eurozone trade rose 0.6% mom to EUR 213.1B.

Japan’s Q4 GDP beats forecasts with 0.7% qoq growth

Japan’s economy expanded by 0.7% qoq in Q4 2024, surpassing market expectations of 0.3% qoq and improving from the previous quarter’s 0.4% qoq rise. On an annualized basis, GDP grew 2.8%, significantly above 1.0% forecast and accelerating from Q3’s 1.7% pace.

Private consumption, which accounts for over half of Japan’s economic output, edged up by 0.1% qoq, defying expectations of a -0.3% qoq contraction. However, it slowed sharply from the 0.7% qoq increase recorded in Q3, reflecting a cautious spending environment.

Capital spending improved by 0.5% qoq, reversing the -0.1% qoq decline in Q3, but fell short of the anticipated 1.0% qoq rise.

Price pressures continued climbing, with the GDP deflator inching up from 2.4% yoy to 2.8% yoy.

Despite the strong Q4 performance, full-year 2024 GDP growth slowed sharply to 0.1%, a steep decline from the 1.5% expansion in 2023.

NZ BNZ services rises to 50.4, stabilization rather than elevation

New Zealand BusinessNZ Performance of Services Index climbed from 48.1 to 50.4 in January, marking a return to expansion after four consecutive months of contraction. While this signals some improvement, the index remains below its long-term average of 53.1.

A closer look at the components reveals a mixed picture. Activity/sales saw a notable rebound, rising from 46.5 to 54.0, while new orders/business ticked up slightly from 49.4 to 50.0. Stocks/inventories also edged into expansion territory at 50.1, up from 48.9. However, employment continued to struggle, slipping from 47.4 to 47.1. Supplier deliveries showed minimal improvement, moving from 47.7 to 47.8.

Despite the headline figure turning positive, sentiment remains weak. The proportion of negative comments rose to 61.9% in January, up from 57.5% in December and 53.6% in November. Respondents cited economic uncertainty and broader downturn concerns as key issues.

BNZ’s Senior Economist Doug Steel noted that the PSI reflects “stabilization rather than elevation,” highlighting that while the upward move is a positive sign, the sector is far from robust growth.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.83; (P) 152.49; (R1) 152.96; More...

Intraday bias in USD/JPY remains neutral with focus on 38.2% retracement of 139.57 to 158.86 at 151.4. Strong rebound from there will maintain near term bullishness. On the upside, break of 154.79 will revive the case that correction from 158.86 has completed at 150.29. Further rise should be seen to retest 158.86 high. However, break of 150.92 and sustained trading below 151.49 will raise the chance of trend reversal, and target 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

RBA Poised to Cut Rates, Aussie Edges Higher

The Australian dollar is higher for a third consecutive trading day. In the European session, AUD/USD is trading at 0.6363, up 0.25% on the day. Earlier, AUD/USD climbed as high as 0.6373, its highest level this year.

RBA expected to cut rates to 4.1%

The Reserve Bank of Australia meets on Feb. 18 and is widely expected to lower the cash rate by a quarter-point to 4.1%. The money markets have priced in a rate cut at 90% and this would mark a milestone for the RBA, which has maintained rates since Nov. 2023. While most of the major central banks are well into an easing cycle, the RBA has remained an outlier.

Why has the RBA been reluctant to lower rates? Headline inflation has fallen back to the RBA’s target range of 2-3%, but underlying inflation has declined more slowly. Underlying inflation is a more accurate gauge of inflation trends and the most recent inflation report, which was released at the end of January, showed underlying inflation falling to 3.2%. This appears to have cemented a long-awaited rate cut.

The RBA meeting also has significant political implications. Prime Minister Anthony Albanese’s Labor government is trailing the opposition and an election must be held by May. If, as expected, the RBA cuts rates, Albanese will be quick to claim that the government’s economic policies enabled the RBA to lower rates for the first time since Nov. 2020.

The US wrapped up the week with a soft retail sales report. January retail sales slid 0.9%, much worse than the market estimate of -0.1% and following a solid gain of 0.7% in December. This was the sharpest decline since March 2023, as severe weather and the Los Angeles fires dampened consumer spending. Annually, retail sales eased to 4.2%, down from an upwardly revised 4.4% in December and above the forecast of 3.7%.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6376. Above, there is resistance at 0.6401

- There is support at 0.6344 and 0.6319

USDJPY – Weekly Inverted Hammer Suggests that Bears May Lose Traction at the Zone of Key Fibo Support

USDJPY remains in red for the third consecutive day and hits again pivotal Fibo support at 151.50 (38.2% of 137.57/158.87).

Recent attack was contained at this zone that validates support, setting scope for another rejection here that would add to scenario of healthy correction before broader bulls resume.

Although daily studies are negative (strengthening bearish momentum / formation of 10/200 DMA death cross) and favor further downside, inverted hammer candlestick on weekly chart warns of potential bounce.

In such scenario, bulls will face several strong obstacles, 200DMA (152.73) and more significant base of thick daily cloud (153.76) violation of which will be required to generate reversal signal and expose next key barriers at 154.80/90 (Feb 12 lower top / 50% retracement of 158.87/150.93 bear-leg).

Watch reaction at 151.00 zone for fresh direction signals.

Res: 152.37; 152.73; 153.12; 153.76

Sup: 151.50; 150.93; 150.00; 149.22

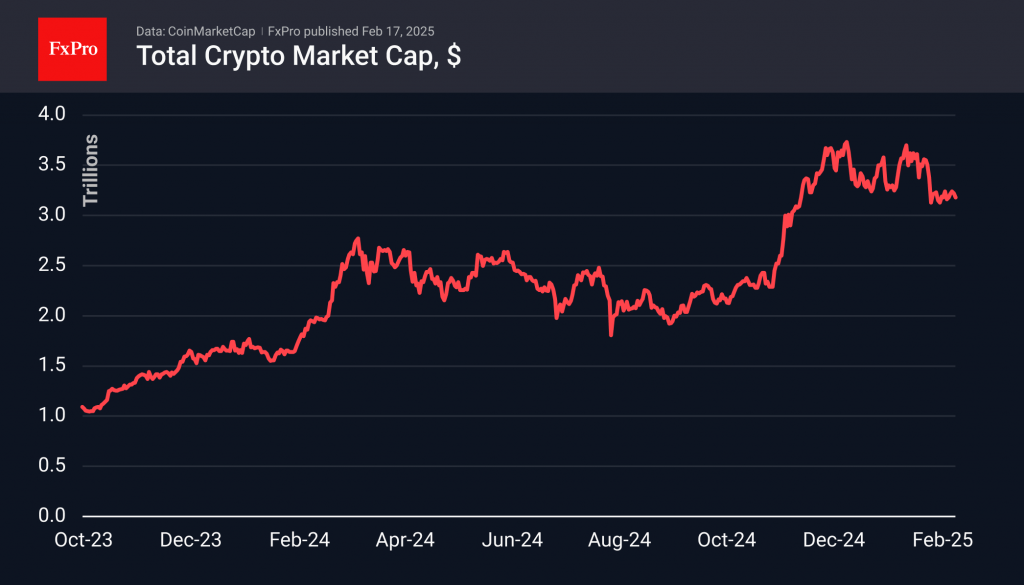

Sluggish Crypto Decline

Market Picture

The crypto market has been sluggishly declining since the end of last week, pulling back 0.8% in the last 24 hours to $3.19 trillion. This is marginally higher than levels a week earlier, but we see the market stabilising at a lower level compared to January. The $3.3 trillion capitalisation level is acting as resistance where sellers are taking the initiative.

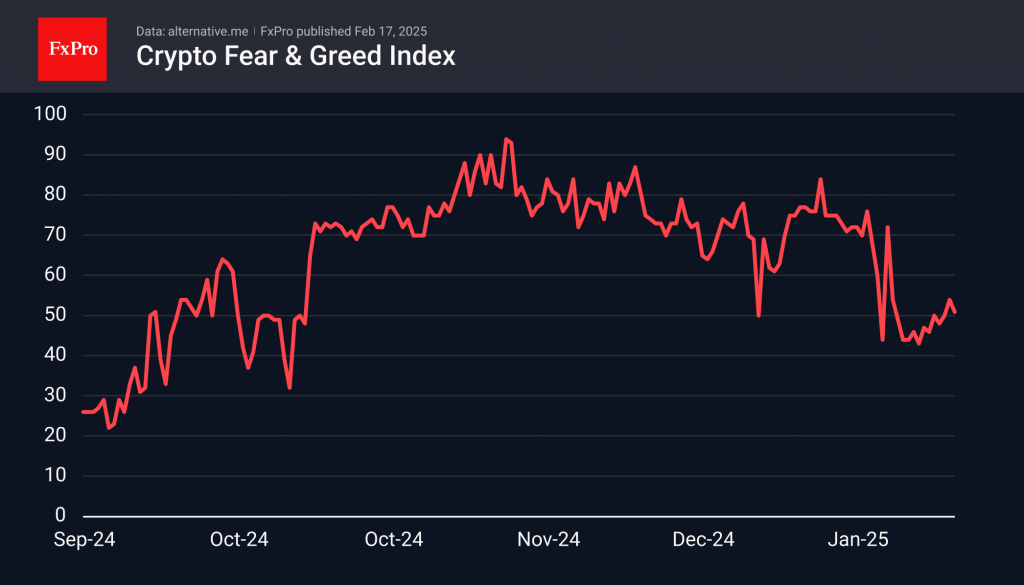

Trading volumes have pulled back to levels we saw prior to last November as the sentiment index drops from greed to the borderline territory between fear and neutral.

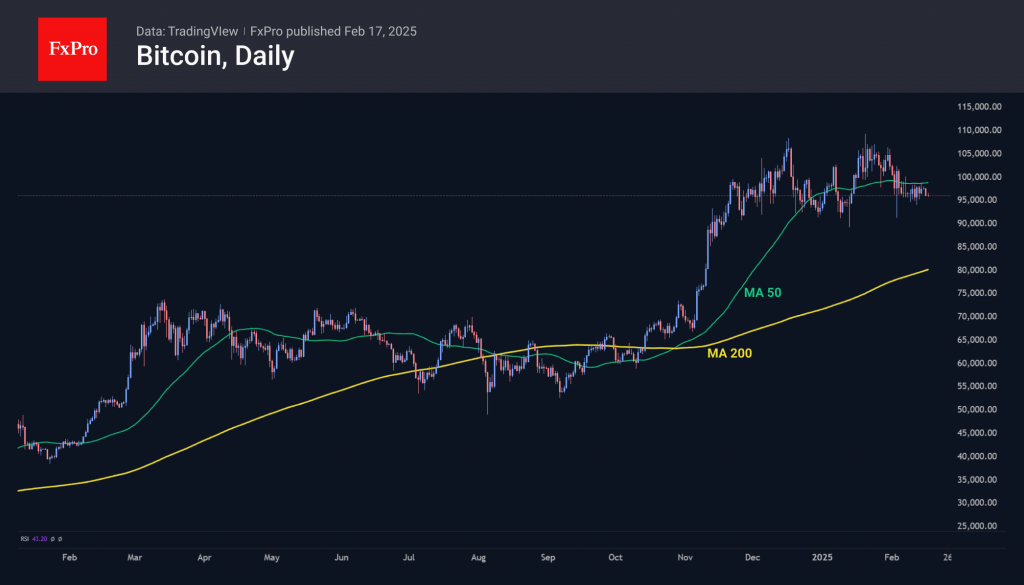

Bitcoin has been moving almost strictly horizontally since the 5th of February, hovering near $95,000 for most of the time. This is below the 50-day moving average, breaking the upward trend. The lack of a sell-off, however, suggests there is still interest in long-term buying on dips near current levels.

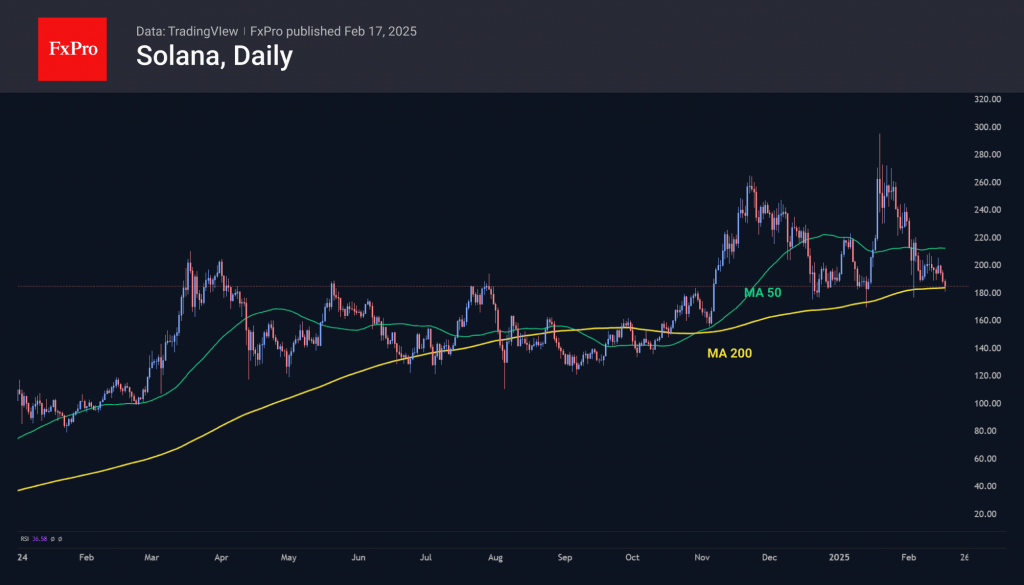

Solana pulled back to $180 on Monday morning, attempting to dip below the 200-day moving average. The coin reversed to gains near these levels in December and January. A sustainable move lower would be the second bearish signal for the broader crypto market, following a similar decline in Ethereum in early February.

News Background

The positive weekly trend in US spot bitcoin ETFs broke after six weeks of inflows. According to data from SoSoValue, net outflows from spot bitcoin-ETFs in the US totalled $581.2 million for the week, cumulatively totalling $40.12 billion. Net outflows from ETH-ETFs totalled a small $26.3 million, bringing cumulative all-time inflows to $3.15 billion.

Santiment calculated that the BTC had shed 277,240 active wallets over the past few weeks, which they attribute to fears of further price declines.

Abu Dhabi Sovereign Wealth Management disclosed a $436.9 million investment in BlackRock’s spot bitcoin-ETF (IBIT). Barclays Bank also disclosed a $131.2 million investment in IBIT. The largest institutional investor in IBIT, Goldman Sachs, has invested more than $1.6 billion in IBIT.

Cryptocurrency trading volume on crypto exchange Coinbase grew 137% in the fourth quarter of last year, while online broker Robinhood saw a 393% increase. The drivers were the hope for more sector-friendly regulation after Donald Trump’s victory.

Users of the Wallet custodial mini-app Wallet on Telegram have been given the option to buy Tether’s USDT stablecoin with zero fees. The option was implemented with the support of the Mercuryo payment network and in cooperation with The Open Platform infrastructure platform for developers in the TON ecosystem.

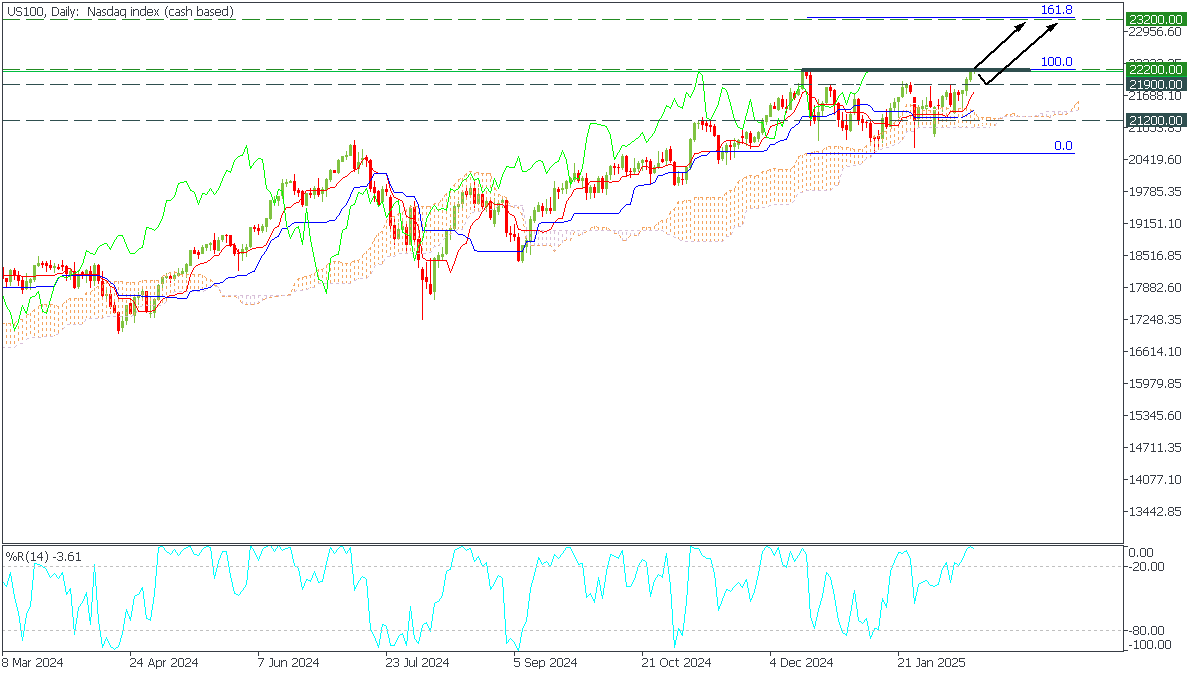

US100: ATH

US100, Daily

In the Daily timeframe, US100 made an all-time high after reaching our previous target. Tenkan has crossed upwards from the Kijun at Ichimoku. However, the %R indicates a significant overbought condition, making a minor correction possible before the 10000 pips rise.

- We consider buying US100 only on consolidation above 22200 with a target to 23200;