Sample Category Title

European Leaders Gather in Paris to Discuss the Future of European Security

In focus this week

Today, European leaders gather in Paris for crisis talks about the future of European security regardless of US engagement, how to support Ukraine and strengthen Europe's position to negotiate. This comes as a response to President Donald Trump opening peace talks with Russia while limiting European involvement in the negotiations.

Markets are continuing to observe the recent movements in politics around the world, with the highlights being the potential ceasefire in Ukraine, the German federal election on Sunday and any signs of Xi-Trump talks related to the recent tariff increases.

The main data print of the week is anticipated to be the release of the PMIs from most major countries on Friday, apart from China, and with US regional surveys coming in the days before. Focus will be on the euro area release as to whether it continues to move in a positive direction supporting the view that the European economy is slowly being supported by rising real incomes and lower interest rates.

Today in Sweden, the monthly labour force survey is due at 08.00 CET where we expect to see a stabilisation of the current weak labour market, but without any marked improvement in the unemployment figure. Such an outcome would be in line with last week's PES report that showed an unchanged unemployment rate and a return of layoffs to their historical average after being at elevated levels in early autumn.

Economic and market news

What happened overnight

In the US, Secretary of State Marco Rubio said that Ukraine and Europe would be part of any real negotiations to end the war in Ukraine. The peace talks will kick off this week in Saudi Arabia between negotiating teams from the US and Russia. Ukraine's representatives apparently will not attend and their role in the process remains unclear. Read more on an alternative 'dirty deal' scenario and the expected market impacts in Research Global - What would a dirty deal in Ukraine mean for markets? 16 February.

In Japan, Q4 GDP came in above expectations at 2.8 % (cons: 1.0 %) and consumption growth for the same period slowed by less than expected, staying in the positives at 0.1% (cons: -0.3%). The strong prints caused the yen to rise and potentially pave the way for additional BoJ hikes down the road.

What happened over the weekend

The Security Conference in Munich, dominated headlines over the weekend, with a primary focus on the US-EU relationship. EU leaders are set to meet in Paris to continue discussions on the future of the EU across several topics.

In the US, January retail sales surprised to the downside across both headline sales at -0.9% m/m (cons: -0.2% m/m) and control group sales (-0.8% m/m SA). Overall, the print was weak, but less than the headline figures would suggest. The modest downtick in US yields is justified, but this should not have dramatic market impact.

In the euro area, employment increased 0.1% q/q in the fourth quarter of 2024, showing that the labour market remains resilient despite weak growth. The picture seen last year appears to be repeating itself, with Spain recording strong employment growth at 1.0 % q/q and Germany stagnating at 0.0 % q/q. We forecast a small increase in the unemployment rate as employment growth stagnates and the labour force grows.

In Norway, the Norwegian Technical Calculation Committee for Wage Settlements released their report ahead of this year's central wage negotiations. Notably, annual wage growth in 2024 came in at 5.3 % and the committee expects inflation to drop to 2.5 % in 2025, which could limit the upside risk to Norges Bank's wage growth estimate for this year of 4.2 %. All in all, the expected rate cut in March is not at risk. We maintain our call for four cuts in 2025, as growth has been weaker than expected, oil investments are about to turn, and domestic inflation keeps falling.

Equities: US and European equities were little changed on Friday and sector performance tightly bunched. This was a well-deserved break for markets, after rallying >1.5% for the week. Risk on was visible on Friday too: Europe outperformed the US (9% ytd vs 4% in the US). Vix dropped below 15, which is the lowest since late January. Investors found financing in defensives, with health care and consumer staples the worst performing sector on Friday. All in all, risk-on continued in markets last week despite the higher inflation print, hawkish Fed speeches and dirty dealmaking in Ukraine. This goes in line with our view that as long as demand stays strong, equity investors will be happy. Futures are higher this morning but note that US markets are closed for holiday.

FI: The direction for global bond yields still seems very uncertain even though we have been pricing out rate cuts from the Federal Reserve since the autumn last year. However, if we look at the movement in 10Y US Treasury yields since the inauguration of Donald Trump there has been no clear direction with 10Y Treasuries trading with a yield between 4.4% to 4.6% based on signals from the Federal Reserve as well as key economic data such as last week's US inflation. However, there has been a clear path for the US 10Y swap spread, which has widened some 10bp since late January.

FX: The broad USD declined last week as markets unwound some of the stretched USD-bullish positioning tied to Trump's policy agenda, particularly on tariffs, where there has been plenty of rhetoric but little immediate implementation. The weaker USD, combined with progress in Ukraine peace talks, supported EUR/USD to just below 1.05. USD/JPY fell back into the 152-153 range amid declining US yields. Both AUD and NZD ended the week on a strong footing, supported by broadly positive risk sentiment. In the Scandies, SEK outperformed, pushing EUR/SEK below 11.25, while EUR/NOK held around 11.65.

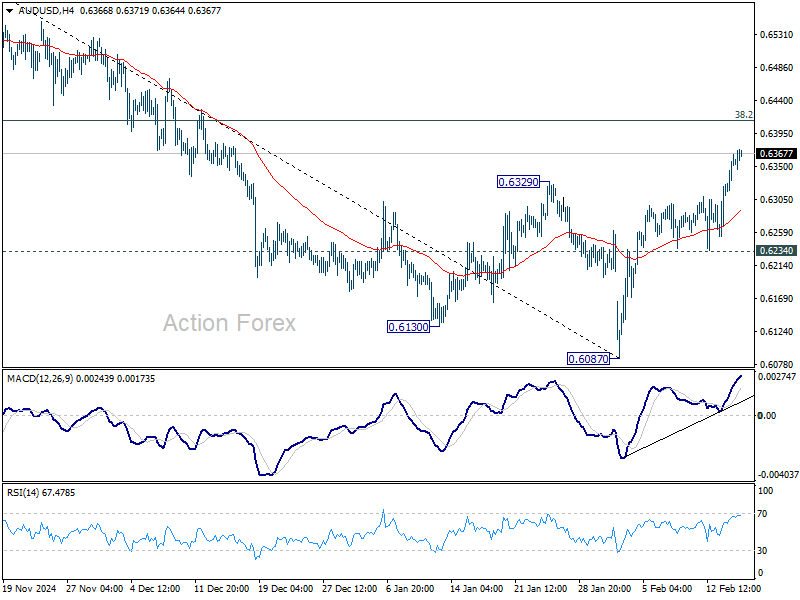

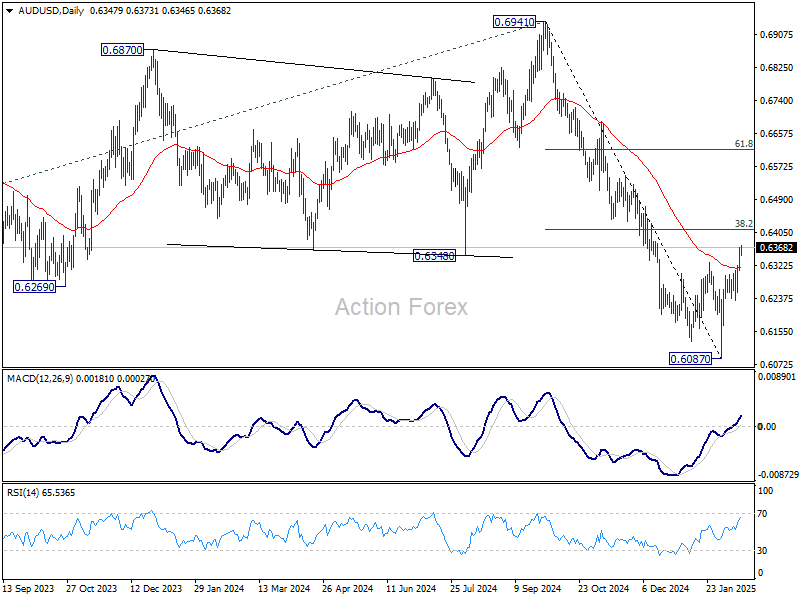

AUD/USD Daily Report

Daily Pivots: (S1) 0.6319; (P) 0.6344; (R1) 0.6376; More...

Intraday bias in AUD/USD remains on the upside for 38.2% retracement of 0.6941 to 0.6087 at 0.6413, as a correction to fall from 0.6941. On the downside, however, break of 0.6234 support will suggest that the rebound has completed and bring retest of 0.6087 low.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6516) holds.

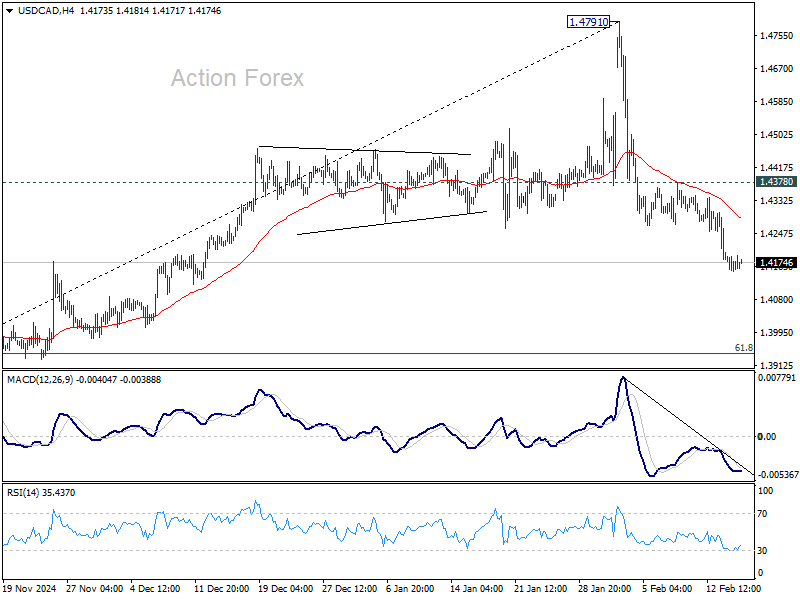

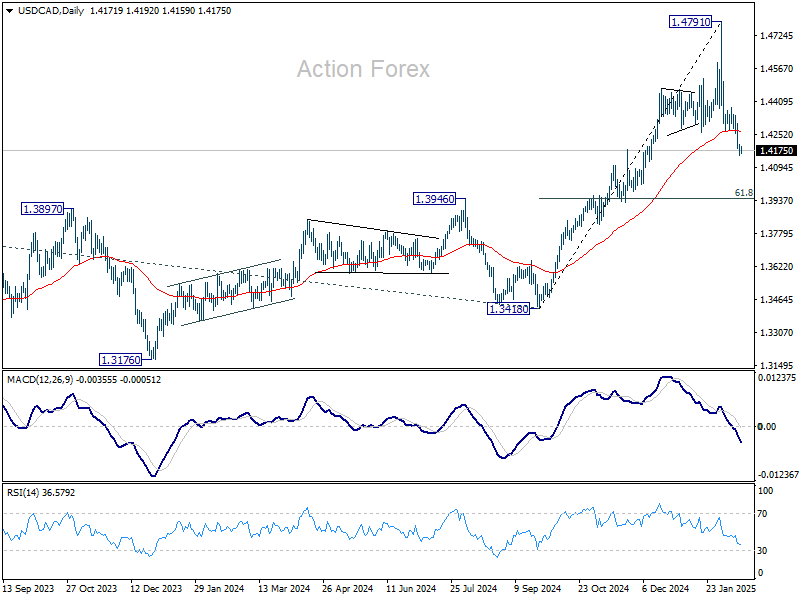

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4153; (P) 1.4178; (R1) 1.4204; More...

Intraday bias in USD/CAD stays on the downside for the moment. Fall from 1.4791 should target 1.3946 cluster support (61.8% retracement of 1.3418 to 1.4791 at 1.3942), as a correction to rise from 1.3418. For now, risk will stay on the downside as long as 1.4378 resistance holds, in case of recovery.

In the bigger picture, long term up trend is tentatively seen as resuming with prior breach of 1.4667/89 key resistance zone (2020/2015 highs). Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. This will remain the favored case as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

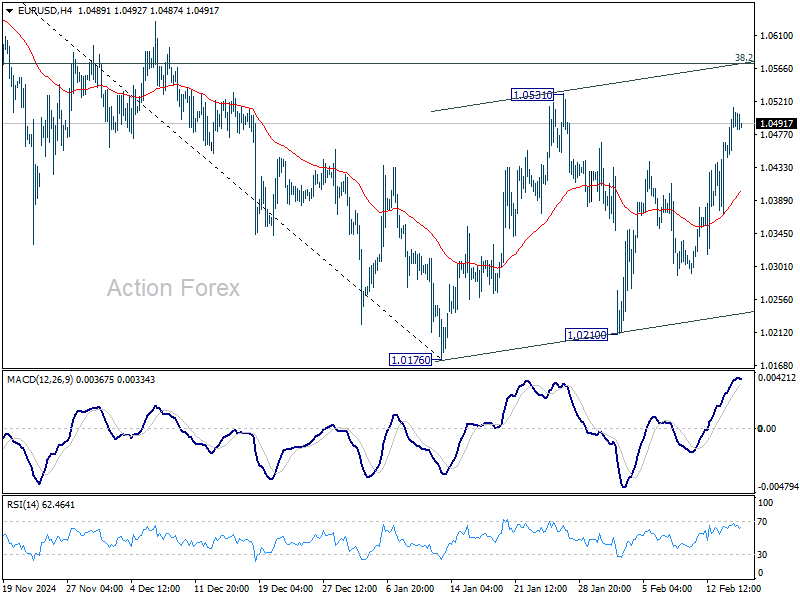

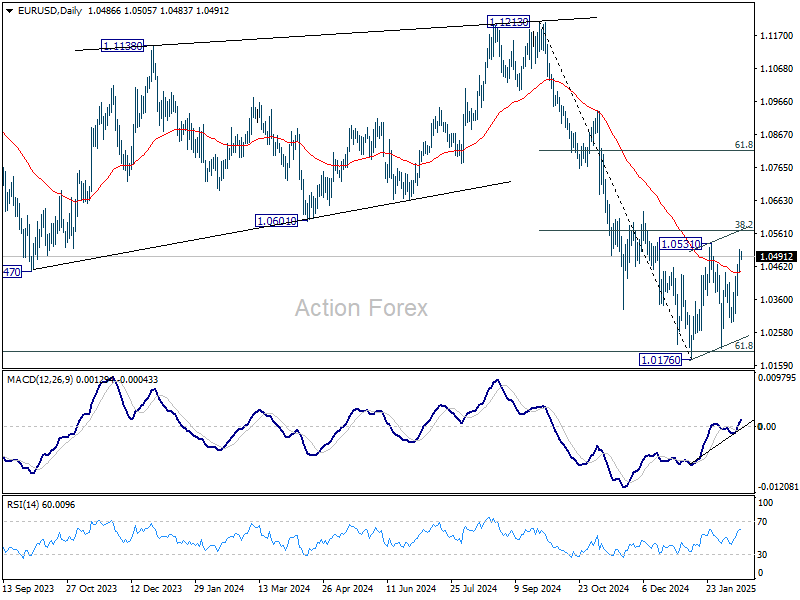

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0454; (P) 1.0484; (R1) 1.0521; More...

Intraday bias in EUR/USD stays neutral as consolidation from 1.0176 is still extending. Stronger rebound might be seen but outlook will remain bearish as long as 38.2% retracement of 1.1213 to 1.0176 at 1.0572 holds. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, decisive break of 1.0572 will raise the chance of reversal, and target 61.8% retracement at 1.0817.

In the bigger picture, immediate focus is on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, reversal from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

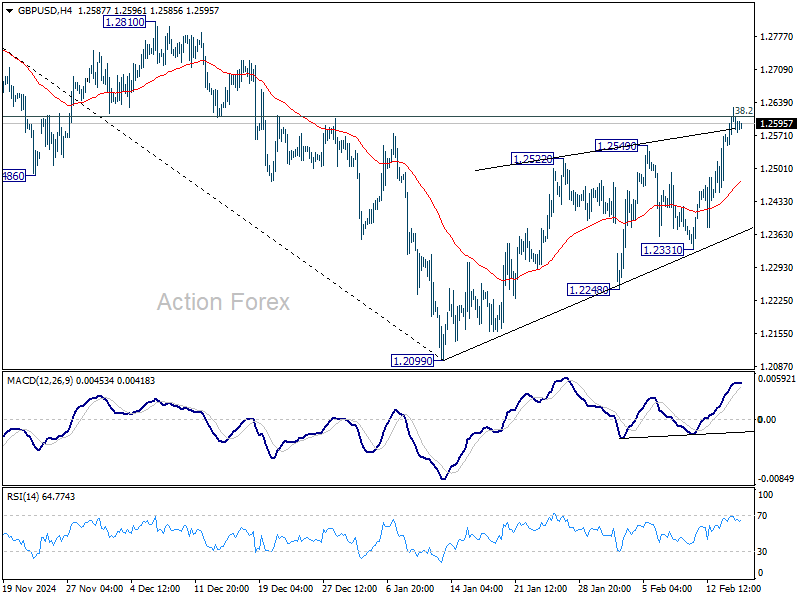

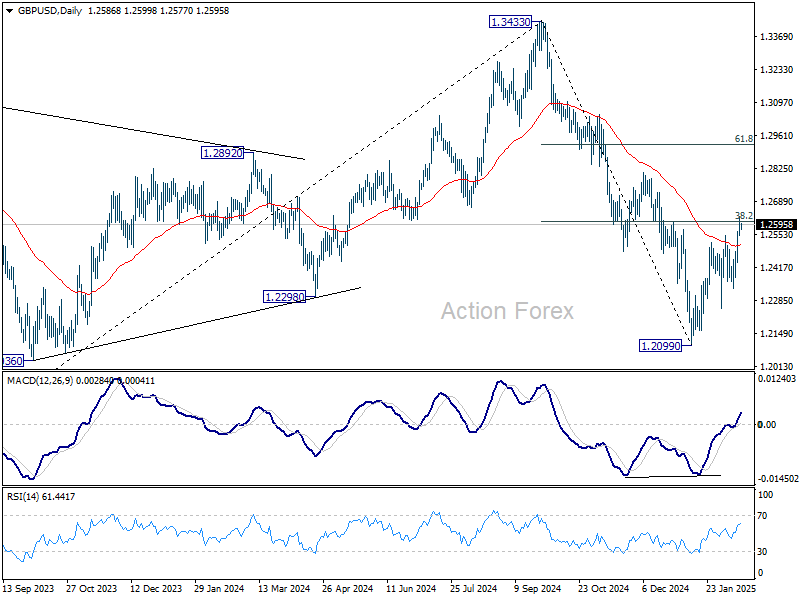

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2539; (P) 1.2585; (R1) 1.2630; More...

Intraday bias in GBP/USD stays neutral for the moment. Rejection by 38.2% retracement of 1.3433 to 1.2099 at 1.2609 will keep near term outlook bearish. Break of 1.2331 support will suggest that the rebound from 1.2099 has completed as a correction, and bring retest of 1.2099 low. However, firm break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

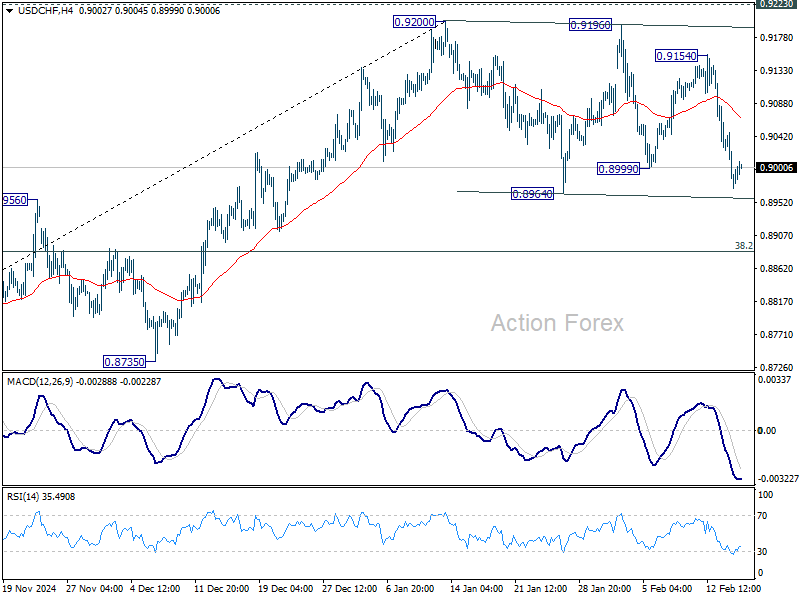

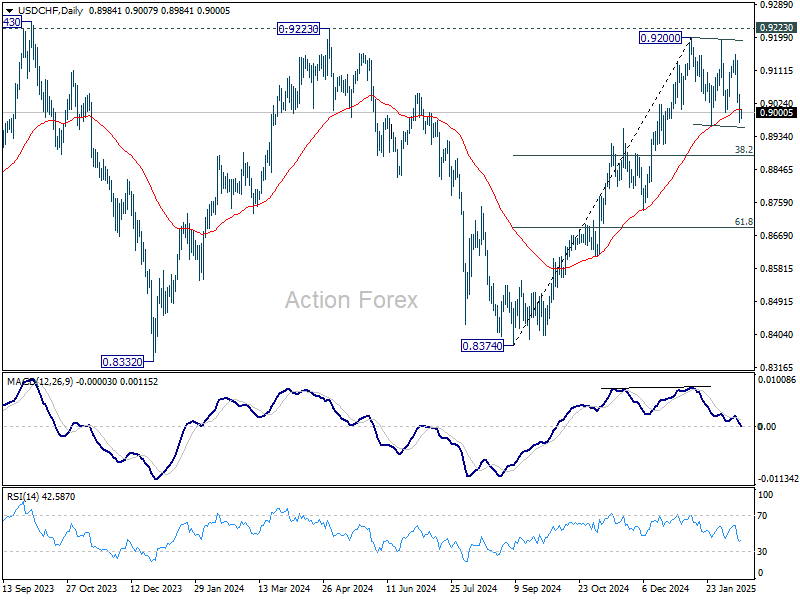

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8954; (P) 0.9017; (R1) 0.9061; More…

Intraday bias in USD/CHF stays neutral first as consolidation from 0.9200 is still extending. While deeper pull back might be seen, outlook will stay mildly bullish as long as 38.2% retracement of 0.8374 to 0.9200 at 0.8884 holds. On the upside, firm break of 0.9223 key resistance will carry larger bullish implication. However, sustained break of 0.8884 will indicate bearish reversal, and target 61.8% retracement at 0.8690 instead.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

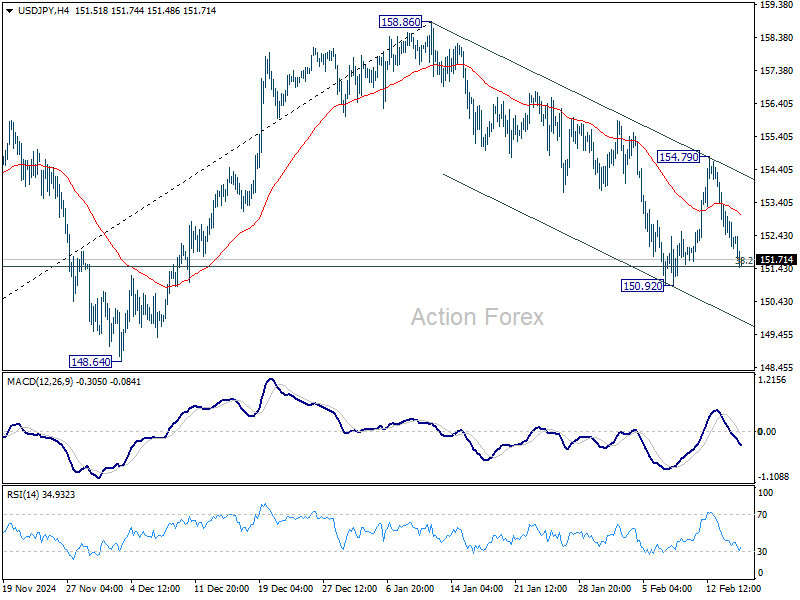

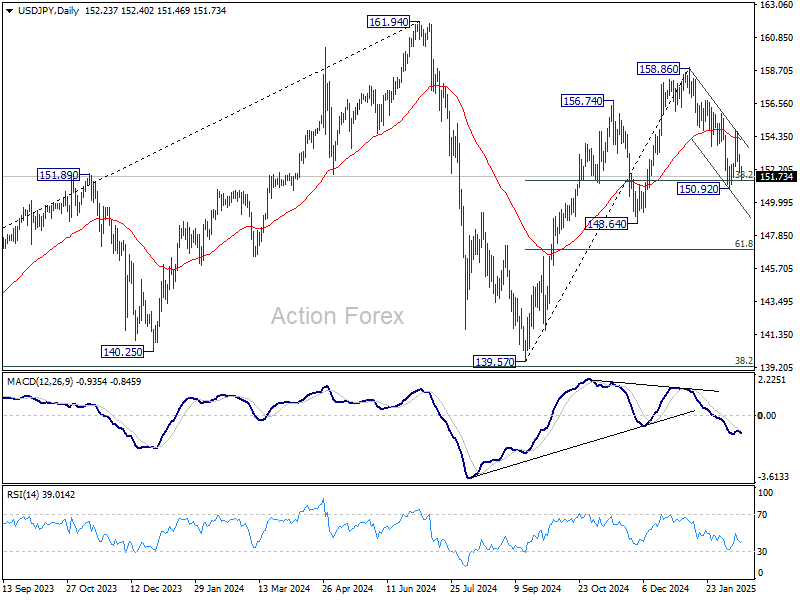

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.83; (P) 152.49; (R1) 152.96; More...

Intraday bias in USD/JPY stays neutral first. Strong support from 38.2% retracement of 139.57 to 158.86 at 151.49 would maintain near term bullishness. On the upside, break of 154.79 will revive the case that correction from 158.86 has completed at 150.29. Further rise should be seen to retest 158.86 high. However, break of 150.92 and sustained trading below 151.49 will raise the chance of trend reversal, and target 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Rallies as Strong GDP Fuels BoJ Rate Hike Speculation

Yen gained strength across the board after Japan’s Q4 GDP growth exceeded expectations, with both private consumption and capital investment rebounding. This development supports BoJ’s decision to hike in January and has fueled speculation that another rate increase could arrive sooner than expected.

It's now seen by some economists that the timing of the next BoJ move will largely hinge on the outcome of the Shunto wage negotiations, with markets eyeing a hike as early as May if wage growth matches 2024 levels.

Beyond Japan, Aussie and Kiwi have maintained their footing, benefitting from a mildly positive risk-on sentiment, even as both the RBA and RBNZ are expected to cut interest rates this week. Meanwhile, Dollar continues to struggle, extending its losses from last week. Euro and Swiss Franc are also on the softer side, while Loonie and Sterling trade mixed.

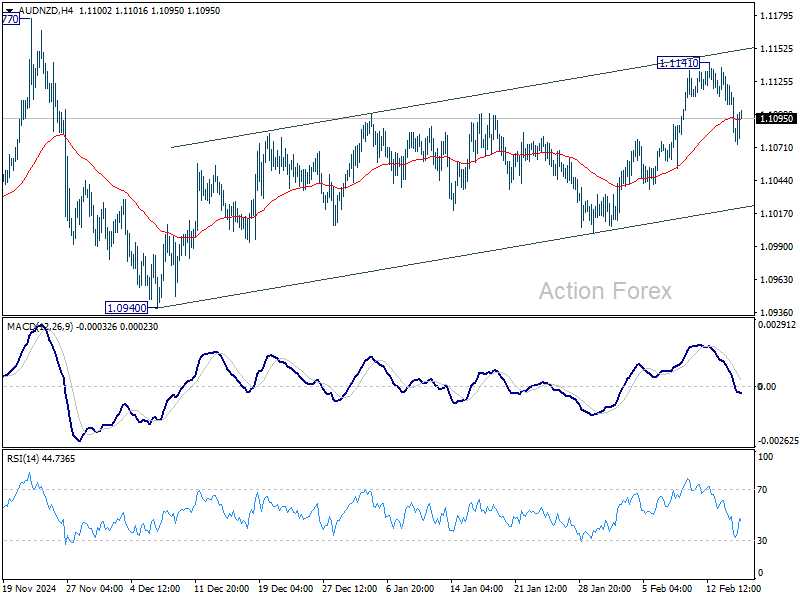

AUD/NZD would be a pair to watch this week with some bearish risks. Technically, choppy recovery from 1.0940 is likely just a corrective move. Hence, in case of another upside, upside should be limited by 1.1177 resistance. On the downside, firm break of the near term rising channel support (now at 1.1023) will argue that the recovery has already complete at 1.1141. Deeper decline should be seen back towards 1.0940 support as the third leg of the pattern from 1.1177.

In Asia, at the time of writing, Nikkei is down -0.01%. Hong Kong HSI is down -0.45%. China Shanghai SSE is down -0.44%. Singapore Strait Times is up 0.49%. Japan 10-year JGB yield is up 0.0114 at 1.368.

Japan’s Q4 GDP beats forecasts with 0.7% qoq growth

Japan’s economy expanded by 0.7% qoq in Q4 2024, surpassing market expectations of 0.3% qoq and improving from the previous quarter’s 0.4% qoq rise. On an annualized basis, GDP grew 2.8%, significantly above 1.0% forecast and accelerating from Q3’s 1.7% pace.

Private consumption, which accounts for over half of Japan’s economic output, edged up by 0.1% qoq, defying expectations of a -0.3% qoq contraction. However, it slowed sharply from the 0.7% qoq increase recorded in Q3, reflecting a cautious spending environment.

Capital spending improved by 0.5% qoq, reversing the -0.1% qoq decline in Q3, but fell short of the anticipated 1.0% qoq rise.

Price pressures continued climbing, with the GDP deflator inching up from 2.4% yoy to 2.8% yoy.

Despite the strong Q4 performance, full-year 2024 GDP growth slowed sharply to 0.1%, a steep decline from the 1.5% expansion in 2023.

NZ BNZ services rises to 50.4, stabilization rather than elevation

New Zealand BusinessNZ Performance of Services Index climbed from 48.1 to 50.4 in January, marking a return to expansion after four consecutive months of contraction. While this signals some improvement, the index remains below its long-term average of 53.1.

A closer look at the components reveals a mixed picture. Activity/sales saw a notable rebound, rising from 46.5 to 54.0, while new orders/business ticked up slightly from 49.4 to 50.0. Stocks/inventories also edged into expansion territory at 50.1, up from 48.9. However, employment continued to struggle, slipping from 47.4 to 47.1. Supplier deliveries showed minimal improvement, moving from 47.7 to 47.8.

Despite the headline figure turning positive, sentiment remains weak. The proportion of negative comments rose to 61.9% in January, up from 57.5% in December and 53.6% in November. Respondents cited economic uncertainty and broader downturn concerns as key issues.

BNZ’s Senior Economist Doug Steel noted that the PSI reflects “stabilization rather than elevation,” highlighting that while the upward move is a positive sign, the sector is far from robust growth.

RBA, RBNZ rate cuts, FOMC minutes, and more

The upcoming week is set to be highly eventful for global markets, with two major central bank meetings and a packed economic calendar. RBA and RBNZ are both expected to lower interest rates. Additionally, investors will scrutinize Fed’s January FOMC minutes to gauge the timing and conditions for policy shifts. Meanwhile, key economic indicators from the UK, Eurozone, Canada, and Japan will provide further insights into their economic trends.

RBA is widely expected to cut interest rates by 25 bps to 4.10%, marking its first rate reduction in this cycle. The decision follows the latest Q4 trimmed mean CPI, which revealed stronger-than-expected disinflation. Market participants will closely analyze the accompanying Statement on Monetary Policy for clues on the outlook. Some analysts anticipate a steady quarterly pace of 25 bps cuts, which could bring the cash rate to a neutral level of 3.35% by the end of the year.

RBNZ is expected to move more aggressively, with a 50 bps cut to 3.75%, as it seeks to transition its policy stance toward a neutral level of 2.50%-3.50%. However, with the rate approaching this estimated range, the central bank may soon opt for smaller rate cuts moving forward. Investors will carefully assess the updated Monetary Policy Statement to determine whether RBNZ signals a slowdown in its pace of easing and to gauge expectations for the terminal rate of this cycle.

Fed’s January FOMC meeting minutes will provide additional insights into policymakers’ discussions on the policy outlook. It is well understood that Fed is in no rush to resume policy easing, given persistent inflation and other risks. However, investors will be looking for answers to key questions: What conditions would trigger a resumption of rate cuts? When does the Fed expect this to happen? Is a rate hike completely off the table?

BoE's rate path has been relatively uncertain in recent weeks. The stronger-than-expected Q4 UK GDP data has significantly reduced the likelihood of a back-to-back rate cut in March. However, this week’s UK employment, wage growth, CPI, retail sales, and PMI reports will be critical in shaping market expectations. If these indicators show resilience in the economy and inflation remains sticky, markets will likely fully revert to pricing in a gradual, one-cut-per-quarter approach.

For Euro and DAX, German ZEW Economic Sentiment and Eurozone PMIs will be particularly important. If these data points confirm that Germany’s sluggish economy is finally starting to turnaround, it would provide a significant boost to investor sentiment and strengthen the case for continued DAX and Euro gains. Apart from central bank decisions, inflation data from Canada and Japan will also be closely watched.

Here are some highlights for the week:

- Monday: New Zealand BNZ services; Japan GDP; Eurozone trade balance.

- Tuesday: RBA rate decision; UK employment; German ZEW economic sentiment; Canada CPI; US Empire state manufacturing, NAHB housing index.

- Wednesday: New Zealand PPI; Japan trade balance, machine orders; Australia wage price index; RBNZ rate decision; UK CPI, PPI; Eurozone current account; US building permits and housing starts, FOMC minutes.

- Thursday: Australia employment; Swiss trade balance; Germany PPI; Canada IPPI and RMPI; US jobless claims, Philly Fed survey.

- Friday: New Zealand trade balance; Australia PMIs; Japan CP, PMIs; UK Gfk consumer confidence, retail sales; PMIs; Eurozone PMIs; Canada retail sales; US PMIs, existing home sales.

USD/JPY Daily Outlook

Daily Pivots: (S1) 151.83; (P) 152.49; (R1) 152.96; More...

Intraday bias in USD/JPY stays neutral first. Strong support from 38.2% retracement of 139.57 to 158.86 at 151.49 would maintain near term bullishness. On the upside, break of 154.79 will revive the case that correction from 158.86 has completed at 150.29. Further rise should be seen to retest 158.86 high. However, break of 150.92 and sustained trading below 151.49 will raise the chance of trend reversal, and target 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). In case of another fall, strong support should be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to bring rebound. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

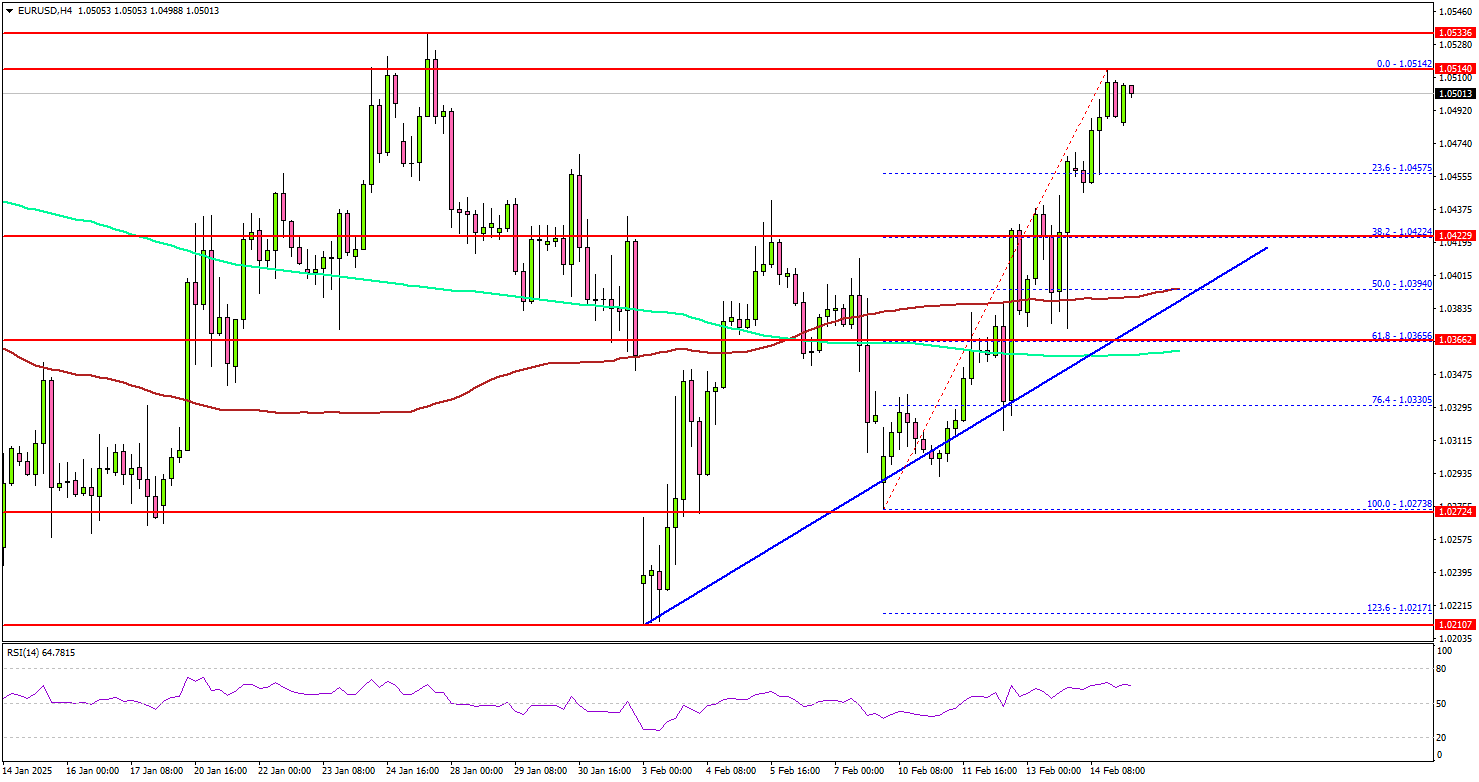

EUR/USD Picks Up Steam—Will It Break Key Resistance?

Key Highlights

- EUR/USD started a fresh increase above the 1.0400 resistance.

- A key bullish trend line is forming with support at 1.0380 on the 4-hour chart.

- GBP/USD climbed higher above the 1.2450 and 1.2500 resistance levels.

- Gold prices started a downside correction from the $2,940 resistance zone.

EUR/USD Technical Analysis

The Euro formed a base and started a fresh increase against the US Dollar. EUR/USD surpassed the 1.0400 and 1.0420 resistance levels.

Looking at the 4-hour chart, the pair settled above the 1.0420 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). However, the bears are still active below the 1.0520 and 1.0535 resistance levels.

On the downside, immediate support sits near the 1.0420 level. It is near the 38.2% Fib retracement level of the upward move from the 1.0273 swing low to the 1.0514 high.

The next key support sits near the 1.0400 level. There is also a key bullish trend line forming with support at 1.0380 on the same chart. It is close to the 50% Fib retracement level of the upward move from the 1.0273 swing low to the 1.0514 high.

Any more losses could send the pair toward the 1.0340 level. On the upside, the pair seems to be facing hurdles near the 1.0520 level. The next major resistance is near the 1.0535 level. The main resistance is now forming near the 1.0550 zone.

A close above the 1.0550 level could set the tone for another increase. In the stated case, the pair could even clear the 1.0620 resistance.

Looking at GBP/USD, the pair started a strong increase above the 1.2450 resistance and might aim for more gains above the 1.2620 level in the near term.

Upcoming Economic Events:

- Fed's Harker speech.

- Fed's Bowman speech.

- Fed's Waller speech.

Japan’s Q4 GDP beats forecasts with 0.7% qoq growth

Japan’s economy expanded by 0.7% qoq in Q4 2024, surpassing market expectations of 0.3% qoq and improving from the previous quarter’s 0.4% qoq rise. On an annualized basis, GDP grew 2.8%, significantly above 1.0% forecast and accelerating from Q3’s 1.7% pace.

Private consumption, which accounts for over half of Japan’s economic output, edged up by 0.1% qoq, defying expectations of a -0.3% qoq contraction. However, it slowed sharply from the 0.7% qoq increase recorded in Q3, reflecting a cautious spending environment.

Capital spending improved by 0.5% qoq, reversing the -0.1% qoq decline in Q3, but fell short of the anticipated 1.0% qoq rise.

Price pressures continued climbing, with the GDP deflator inching up from 2.4% yoy to 2.8% yoy.

Despite the strong Q4 performance, full-year 2024 GDP growth slowed sharply to 0.1%, a steep decline from the 1.5% expansion in 2023.