Sample Category Title

UK Retail Sales, US Sentiment Data To Drive Markets Friday

The global financial markets will be clued in to the economic calendar on Friday, with investors anticipating high profile reports from both sides of the Atlantic.

Action begins at 07:00 GMT with a report on German producer inflation. The producer price index (PPI) is forecast to rise 0.2% in December, following a 0.1% increase the month before. In annualized terms, this would translate into a gain of 2.3%.

Later in the morning, the Swiss government will also report on wholesale inflation via the producer price index. Producer prices are projected to climb 0.4% month-on-month after climbing 0.6% the month before. That would translate into a year-over-year gain of 2.1%.

The European Commission’s statistical agency will release the November currency account balance at 09:00 GMT. The region’s current account surplus is forecast to rise to €31.3 billion in November from €30.8 billion the month before.

At 09:30 GMT, the UK’s Office for National Statistics will report on retail sales for the month of December. Receipts at retail stores are expected to decline 0.6% in December despite the holiday season. Excluding fuel, sales are also expected to fall 0.8%.

In North America, the Canadian government will report on manufacturing shipments at 13:30 GMT. Shipments are expected to rise 2% month-on-month in November following a 0.4% drop the month before.

In the United States, the University of Michigan will issue its preliminary consumer sentiment index at 15:00 GMT. The report is expected to show a reading of 97.0 for January for an increase of 1.1 points.

In terms of monetary policy, Federal Reserve official Randal Quarles will deliver a speech at 18:00 GMT. The Fed will hold its first policy meeting of 2018 later this month, where no change in interest rates is expected.

EUR/USD

Europe’s common currency edged higher at the start of Asian trading, but continues to trade below 1.2300 US. The EUR/USD exchange rate was last seen hovering at 1.2262 for a gain of 0.2%. The pair is eyeing immediate resistance at the 16 January high of 1.2309.

USD/CAD

The Canadian dollar traded within a narrow range against the dollar Thursday as investors assessed the Bank of Canada’s recent decision to raise interest rates. The USD/CAD exchange rate is currently trading in the low 1.2400 region, having declined sharply from last week’s highs near 1.2600. The outlook seems to favour the loonie over the mid-term as the US dollar continues to struggle.

GBP/USD

Cable extended its bullish upside on Thursday, climbing above 1.3900 for the first time since the Brexit crisis. The GBP/USD exchange rate was trading in the low 1.3900 region in the Asian session, having gained 0.1% from the previous close. The pair now has its sights set on the 1.4000 resistance.

Forex Analysis: WTI Crude Weaker After Inventories, USD Index Retesting Significant Lows, GBP Firm Ahead Of Retail Sales Data

The Economic calendar for today is very light, with main events in focus for the European trading session concentrating around German PPI and UK Retail Sales data. Asian equity markets were positive, pointing to a sixth week of gains. The U.S. Dollar Index declined overnight, trading very close to the psychologically important 90.00 level, which represents a four-monthly low. Precious metals rebounded, with Gold trading close to $1330 and Silver close to $17.00. WTI Crude dipped lower after the inventories data published yesterday, which showed larger than expected drawdown but a rise in U.S. production. WTI Crude is trading close to $63.00 after retesting the highest level in more than three years prior to the data release. Apart from the economic data, market participants are looking forward to the 48th World Economic Forum Annual Meeting, which is scheduled for next week and will take place in Davos, Switzerland from 23rd until 26th January.

US Building Permits (MoM) (Dec) was released to show 1.302M v the consensus of 1.290M, from 1.298M previously. Housing Starts Change (Dec) was also released at the same time, coming in at -8.2% v an expected 1.7%, from 3.3% prior. Housing Starts (MoM) (Dec) showed 1.192M v an expected 1.275M, from a prior of 1.299M. Building Permits Change (Dec) showed-0.1% v an expected -1.0%, from -1.0% previously. Initial Jobless Claims (Jan 12) showed 220K v an expected 250K, from 261K previously. Continuing Jobless claims (Jan 5) showed 1.952M v an expected 1.900M, from 1.876M previously. Philadelphia Fed Manufacturing Survey (Jan) showed 22.2 v an expected 25.0, from a prior of 27.9. USD crosses and US Equity markets both reacted in a very limited way after the announcements.

ECB’s Executive Board member, Benoit Coeure, spoke at the conclusion of a panel on ‘A post-crisis agenda for the euro area and Germany: which way forward?’, at a joint conference of the IMF and Deutsche Bundesbank “Germany – Current Economic Policy Debates” in Frankfurt, Germany. During the speech, he mentioned that “Eurozone is in expansion, no longer in recovery”. Also, that “Most countries in Euro area need to rebuild fiscal buffers”. The German DAX equity index initially spiked higher, to the closely watched 13300 level.

US Weekly Crude Oil Inventories were released yesterday at 16.00 BST, a day later than normal due to the market trading holiday in the U.S. on Monday 15th January for Martin Luther King Jr. Day. Weekly inventories came in at -6.861M, which was a much larger drawdown than the expected -3.588M, from a previous value of -4.948M. Other data released at the same time showed inventories for Gasoline were at +3.620M, Distillate at -3.887M, Cushing at -4.184M and Production at +258K bpd. The EIA Crude Oil Stockpiles report is a weekly measure of the change in the number of barrels in stock of crude oil and its derivates and is released by the Energy Information Administration. This report tends to generate large price volatility, as oil prices impact worldwide economies, with the most affected being WTI and Brent Crude futures and commodity-related currencies such as the Canadian dollar. Both WTI and Brent crude futures reacted positively to the published figure, initially rallying from the pre-release intraday lows of $63.50 for WTI and $68.87 for Brent Crude futures. The Canadian dollar also showed some strength, which was clearly visible in USDCAD currency pair which pulled back from the pre-release high of 1.2485.

New Zealand Business NZ PMI (Dec) came in at 51.2. The previous release indicated a PMI of 57.7. The NZDUSD currency pair subsequently traded in a tight range with a 0.7309 high and 0.7282 low.

EURUSD is up overnight, trading around 1.2250.

USDJPY is down in early session trading at around 110.80.

GBPUSD is up to trade around 1.3900.

USDCAD is down, trading around 1.2420.

Gold is up in early morning trading at around $1,332.65.

WTI is down this morning, trading around $63.00

Major data releases for today:

At 07.00 GMT, German Producer Price Index is scheduled for release by the Statistisches Bundesamt Deutschland. It measures the average changes in prices in the German primary markets. Changes in the PPI are widely followed as an indicator of commodity inflation. The consensus is for 2.3% from 2.5% previously. Markets that could be impacted by this number are Euro currency crosses and German Equities.

At 09.30 GMT, UK Retail Sales are scheduled for release by the Office for National Statistics. It measures the total receipts of retail stores. Monthly percent changes reflect the rate of change of such sales. Changes in Retail Sales are widely followed as an indicator of consumer spending. The consensus for Retail Sales (YoY) (Dec) figure is 3.0%, from 1.6% previously. Markets that could be impacted by this number are GBP currency crosses and UK Equities. Generally speaking, a high reading is seen as positive, or bullish for the GBP, while a low reading is seen as negative or bearish.

At 18.00 GMT, The Baker Hughes Rig Count is scheduled for release. This is an important business barometer for the drilling industry and its suppliers. When drilling rigs are active, they consume products and services produced by the oil service industry. The active rig count acts as a leading indicator of demand for products used in drilling, completing, producing and processing hydrocarbons. This particular case represents the number of rigs drilling exclusively for oil. The previously published number was 752.

Currencies: US Government Shutdown And Consumer Confidence To Drive The Dollar

Sunrise Market Commentary

- Rates: US yields hit important resistance levels

The US Note future's underperformance against the German Bund continued yesterday. The move was mainly an extension of Wednesday's sell off. US 5-yr and 10-yr yields tested key resistance, respectively at 2.42% (2011 top) and 2.63%/2.64% (2016/2017 top), but a break didn't occur. The US Senate's vote on a stopgap funding bill could be key. - Currencies: US Government shutdown and consumer confidence to drive the dollar

The price action of the dollar remained unconvincing yesterday. The US currency reversed part of Wednesdays rebound as uncertainty on a US government shutdown weighed. The US Senate votes on a spending bill today. If approved, the dollar might receive additional interest rate support. However, of late this was no guarantee for sustained USD gains

The Sunrise Headlines

- US stock markets ended slightly lower yesterday with the Dow underperforming (-0.4%). Most Asian equity indices eke out gains overnight with Korea underperforming.

- The threat of a partial US government shutdown intensified as senators signaled opposition to a short-term spending bill that the House passed yesterday evening.

- The White House is considering SF Fed governor Williams as a candidate to serve as the vice chairman of the Federal Reserve Board in Washington, according to people familiar with the matter.

- The Fed should review its inflation target as part of an assessment of its tools for fighting the next recession NY Fed Dudley said, adding new impetus to an issue that is among the most important questions facing monetary policy.

- Leaders Silvio Berlusconi of Forza Italia, Matteo Salvini of Northern League and Giorgia Meloni of Brothers of Italy signed a joint election program ahead of Italy's March 4 general elections.

- The expected reduction of the ECB's monetary stimulus programme this year is unlikely to have a major adverse impact on Portugal, whose public debt should keep declining, a senior Fitch Ratings analyst said.

- Today's eco calendar contains University of Michigan consumer confidence and UK retail sales. Fed Bostic and Quarles are scheduled to speak, respectively on the economy and on bank regulation

Currencies: US Government Shutdown And Consumer Confidence To Drive The Dollar

Senate vote spending bill key for USD short-term ?

The dollar couldn't sustain early-day gains yesterday. Especially USD/EUR showed signs of weakness. The interest rate differentials widened again slightly in favor of the dollar. It was not enough to help the US currency, as was often the case of late. US data were mixed. Uncertainty on a US government shutdown capped further US equity gains and weighed on the dollar. USD/JPY finished the day at 111.11. EUR/USD closed the session at 1.2238.

Asian equities remain in good shape, but the positive risk sentiment doesn't help the dollar. The trade-weighted dollar (DXY) trades at 90.38 (near the cycle low). USD/JPY dropped back below 111 and AUD/USD surpassed the 0.80 mark. EUR/USD also regained a few more ticks even as US yields are at recent highs/key resistance levels.

The debate on the US spending bill and US consumer confidence (University of Michigan) are the main topics today with potential to move FX markets. Consumer confidence is expected to rebound after a setback in the previous two months. Recent US business sentiment indicators didn't profit much from the tax reform. So we are a bit cautious. A US government shutdown would weigh on the dollar. If a shutdown is avoided, US yields might break key resistances (see fixed income part). Will this be enough to improve USD sentiment? This weekend's SPD decision whether or not to start formal talks to form a German government are also important for European markets.

Global Picture: The dollar remains in the defensive as markets prepare for a change in policy from central banks outside the US. This propelled EUR/USD despite a huge interest rate differential in favour of the dollar. The USD decline slowed this week, but the 'rebound' remained unconvincing from now. A return below previous resistance at 1.2092 is needed to call off the ST alert for the dollar. EUR/USD 1.2598 (62% Retracement) is next important resistance on the charts.

The December UK retail sales are expected to decline 1.0% M/M after a strong November figure. A positive surprise (smaller decline) is possible. Activity data are not the most important issue for (FX) trading. Even so, sterling showed some underlying resilience recently. A break of EUR/GBP below 0.8810 would open the way to the 0.87 range bottom, which we consider solid support. Some further correction within the established range is possible.

DXY (USD trade-weighted): USD fails to rebound off recent lows

Market Update – Asian Session: Asian Equities Trade Mixed After Mostly Lower US Session

Headlines/Economic Data

Bank of Japan (BoJ) again leaves daily bond purchases unchanged ahead of next week’s policy meeting (Monday Jan 22- Tuesday Jan 23rd)

Fate of US stopgap funding bill is now in the hands of US Senate (**Note: The deadline for a government shutdown is midnight on Friday, Jan 19th)

Asian currencies trade firmer vs US dollar: Taiwan Dollar (TWD) trades at highest level vs US dollar (USD) since Nov 2013; Korean Won (KRW) gains over 0.4% on session; Yuan (CNY) fixed stronger on session

Asia bond yields track earlier rise in US Treasury yields: Australia 3-year yield 2.240% (highest since late 2014)

WTI Crude Oil declines by over 1%

Australia/New Zealand

ASX 200 opened +0.2%; closed -0.1%

ASX 200 REIT Index -0.7%, Telecom -0.6%, Financials -0.1%

(AU) Australia Government plans review of energy efficiency legislation

(NZ) NZ PM Ardern says she is expecting first child in June; Winston Peters to be acting PM for 6 weeks after baby is born

(NZ) New Zealand Dec Business Manufacturing PMI: 51.2 v 57.7 prior (5-year low)

China/Hong Kong

Hang Seng opened +0.1%, Shanghai Composite +0.2%

Hang Seng Property/Construction Index +1.5%, Industrial Goods +1.3%, Materials +1.2%, Information Tech +0.7%; Financials flat

Shanghai Pharmaceuticals [2607.HK]: -4.5% (To raise HK$3.13B by selling 153.2M H-shares at HK$20.43/share)

Tencent [700.HK]: Announced patent cross-licensing agreement with Google

Leshi Internet [300104.CN]: Terminates asset restructuring and name change plan; to hold investor meeting on Tuesday Jan 23rd

Huawei: Said to guide 2018 Rev at $102.2B - Chinese Press [**Note: The company guided its FY17 Rev at CNY600B (~$93.4B) v CNY522B y/y (+14.9% y/y)]

HNA unit Suparna Airlines said to miss yuan denominated lease payment - US financial press

(CN) US government panel may not approve any deals by China conglomerate HNA Group until there is clarify on the company's owners - financial press

(CN) PBOC SETS YUAN REFERENCE RATE AT 6.4169 V 6.4401 PRIOR (strongest yuan fix since Dec 9, 2015)

(CN) China PBOC OMO: Injects CNY230B v CNY160B injected in 7,14 and 63-day reverse repos prior: Net injection CNY80B v CNY90B injected prior; For the week, net injection at CNY590B v CNY40B net injection w/w

(CN) Shanghai International Energy Exchange Exec: China crude oil futures won't be used to challenge WTI futures

(CN) China issues sector components of Q4 GDP: Finance Sector GDP +4.0% y/y, IT/Software sector +33.8% y/y; Property sector +4.8% y/y (**Reminder from Thursday's session: CHINA Q4 GDP Q/Q: 1.6% V 1.7%E; Y/Y: 6.8% V 6.7%E)

(CN) China govt plans further restrictions on private bond offerings - Chinese press

Korea

Kospi opened +0.2%

Weakness in chipmakers: Samsung Electronics -1.5%, Hynix -2.4%

Japan

Nikkei 225 opened +0.4%; closed: +0.2%

Financials trade generally higher: TOPIX Securities Index +0.8%, Mitsubishi UFJ +0.8%, Sumitomo Mitsui +1.3%

TOPIX Real Estate Index +0.9%

Fast Retailing [9983.JP]: -0.3%

(JP) Japan Government Pension Fund (GPIF) may report 3-month investment profit of ¥6.3T – Japanese Press

Other Asia

(ID) Indonesia proposes reduction in income tax rate for small business

(PH) Philippines Central Bank (BSP) Gov Espenilla: domestic tax reform may 'temporarily' stroke inflation; To update CPI forecast to account for Peso (PHP), oil prices and domestic tax reform; Can wait for risks related to CPI to wane before cutting the reserve ratio requirement (RRR)

Taiwan Semi [2330.TW] +2.5% (Reports Q4 (NT$) Net 99.3B v 97.2Be; Op 108.9B v 107.5Be

North America

US equity markets ended mostly lower: Dow -0.4%, S&P500 -0.2%, Nasdaq flat, Russell 2000 -0.6%

S&P500 Real Estate Sector -1%, Energy -0.8%

American Express [AXP] Down over 2% afterhours: Reports Q4 $1.58 v $1.54e, Rev $8.84B v $8.72Be; suspends buyback in H1 to rebuild capital after tax reform; Guides initial FY18 $6.90-7.30 v $6.83e

IBM: Shares down over 3% in afterhours: Reported Q4 results, FY18 guidance

Metlife [MET]: Confirms it and Financial Stability Oversight Council (FSOC) file motion to dismiss appeal in SIFI* litigation; motions to bring litigation proceedings to an end

(US) NPD: US Dec Total Video Game Spending $3.3B, +10% y/y; 2017 US video game industry Rev $36.0B (record), +18% y/y (Hardware +19%, software +18%)

(US) White House said to consider San Francisco Fed President Williams for number 2 job at Fed (Vice Chair) - US financial press

(US) Fed's Mester (voter, hawk): Favors three to four rate hikes in 2018, 2019

US Government Funding: (US) House passes procedural vote to advance stopgap continuing resolution for debate – press

(US) Majority of House Freedom Caucus will back stopgap spending bill

(US) Pres Trump reportedly has called into a House Freedom Caucus meeting to negotiate to pass stopgap bill - press

(US) Senate Democrats say they have the votes to block govt funding bill – Politico

(US) Sen Paul (R-KY): will vote no on stopgap spending bill in Senate

Sen Graham (R-SC), Sen Rounds (R-SD) have indicated they will also be 'no' votes

(US) Sen Maj Leader McConnell (R-KY) reportedly is planning for a govt shutdown; Could stage various votes to embarrass the Democrats over the weekend if govt shuts down - Politico

(US) Sen Flake (R-AZ): a five-day stopgap bill is now under discussion (in case month long funding bill fails to get enough votes) – press

(US) US Senate Democrats said to plan to permit procedural vote on stopgap spending bill – US financial press

(US) US Senate plans first procedural vote on stopgap US government funding bill later tonight

(US) US Senator Schumer (D): Democrats will support procedural vote on stopgap; Senate should move 'very short-term' stopgap bill

(US) US Senate passes procedural motion to start debate on stopgap bill

(US) Treasury $13B 10-year TIPS draw 0.548%, BTC 2.69 (strongest BTC since May 2014)

(US) US-- 10-year Treasury yield hits highest level since 2016 (during Asian session)

(US) DOE CRUDE: -6.9M V -2.5ME

Europe

(UK) Prime Min May: reiterates there will not be second referendum on Brexit; declines to comment on how she would vote in a theoretical second referendum

(EU) ECB's Coeure (France): Euro Zone is in expansion and is no longer in recovery

(FR) ECB's Villeroy (France): prepared to trigger a counter cyclical cushion if needed; French banks should be cautious about creating excess credit growth; Already took some measures in December to curb lending in France

(FR) France Pres Macron: would never link Brexit and bilateral issues with the UK

(FR) France Fin Min Le Maire: completion of bank and capital markets EU union is priority; Plans to make joint Germany-France proposal on bitcoin regulation to G20

BASF: Reports prelim FY17 EBIT €8.3B v €7.9Be, +32% y/y, Rev €64.5B v €57.6B y/y; As forecast by BASF, sales, income from operations (EBIT) before special items and EBIT are considerably above the level of the previous year. The earnings figures exceed analyst estimates significantly; The reduction in the U.S. corporate tax rate from 35% to 21% results in one-time noncash, deferred tax income of almost EUR400 million in the fourth quarter of 2017.

Levels as of 01:00ET

Hang Seng +0.2%; Shanghai Composite +0.5%; Kospi +0.1%

Equity Futures: S&P500 flat; Nasdaq100 flat, Dax -0.1%; FTSE100 -0.2%

EUR 1.2232-1.2270 ; JPY 110.79-111.13; AUD 0.7997-0.8021 ;NZD 0.7288-0.7312

Feb Gold +0.3% at $1,331/oz; Feb Crude Oil -1.2% at $63.20/brl; Mar Copper +0.3% at $3,209/lb

US University Of Michigan Survey On The Agenda

US University Of Michigan Survey On The Agenda

Market movers today

The global data calendar is somewhat thin, albeit with eurozone current account data and the US University of Michigan survey on the agenda.

In the UK, we are due to get the retail sales number for December, which has historically moved GBP in the case of surprises, although it is a poor indicator for actual private consumption growth.

Markets will also monitor developments regarding a potential US government shutdown today, as Senate Republicans are now struggling to come up with a bill to keep the government open past the funding deadline today at midnight .

No major Scandi events are scheduled.

Selected market news

Sentiment was dampened overnight by the threat of a US government shutdown still lingering. The House of Representative managed to pass a spending bill to stop the funding gap until mid-February, which would provide more time to settle longer term issues such as domestic and defence spending. However, the bill st ill needs the backing of the Senate and Democrats have suggested they have the votes to block it in this process, unless they get concessions in terms of protect ion for young immigrants. Should the government shut down, it would be likely to lead to the closure of a range of less vital government institutions, possibly including the release of economic statistics. Note that the stopgap funding requirement near term is separate from the debt ceiling issue; in any case, the government should have the funds to avoid a default if an increase in the debt ceiling is simply agreed on before late February.

US equities ended Thursday lower following a notable decline in the Philly Fed index to 22.2 (from 27.9), thus providing another hint that the US manufacturing cycle is maturing. The market mood improved a bit in the Asian session, with stock indices generally posting small gains. EUR/USD has been relatively steady around the 1.2250 mark after the ECB’s Benoit Coeuré failed to deliver much new ECB insight when speaking yesterday. Oil prices remain under pressure, with Brent falling below USD68.5/bl. The 10Y US Treasury yield rose briefly into the 2.63% area; thus notably breaking the March 2017 high.

Separately, in an interview with the FT yesterday the Fed’s William C. Dudley shared his thoughts on what policy tools would be appropriate to fight the next recession. Notably, Dudley’s comment s echoed t he suggest ion of t he minutes from t he past two Fed meetings that alternative frameworks for monetary policy such as price-level targeting or an inflation target range may be useful to consider. In Research US - The subtle push for price level targeting continues, 3 January, we discussed how introducing a price level target would help the Federal Reserve return inflation to 2% but that it does face some operational hurdles and that a shift in target would be possible no earlier than in 2019.

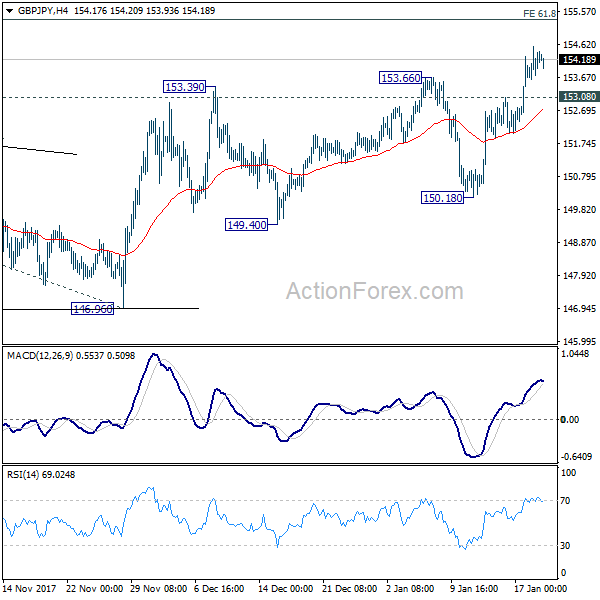

GBP/JPY Daily Outlook

Daily Pivots: (S1) 153.78; (P) 154.17; (R1) 154.74; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current rally should target 61.8% projection of 139.29 to 152.82 from 146.96 at 155.32. Break will target 100% projection at 160.49. On the downside, below 153.08 minor support will turn intraday bias neutral again. But outlook will stay bullish as long as 150.18 support holds.

In the bigger picture, as long as 146.96 key support holds, medium term outlook remains bullish. Rise from 122.36 is in favor to extend to 61.8% retracement of 195.86 to 122.36 at 167.78. However, break of 146.96 support will indicate trend reversal. And there would be prospect of retesting 122.36 in that case.

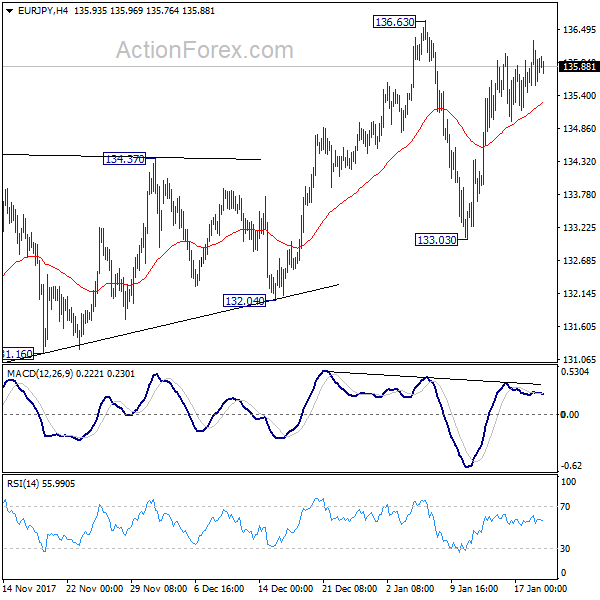

EUR/JPY Daily Outlook

Daily Pivots: (S1) 135.51; (P) 135.90; (R1) 136.37; More....

Intraday bias in EUR/JPY remains neutral as it's staying in range of 133.03/136.63. Near term outlook stays mildly bullish with 133.03 support intact and further rally is in favor. Break of 136.63 will resume medium term up trend. However, below 133.03 will turn focus to 132.04. Firm break there will indicate medium term reversal.

In the bigger picture, medium term rise from 109.03 (2016 low) is seen as at the same degree as the down trend from 149.76 (2014 high) to 109.03 (2016 low). It should be targeting 141.04/149.76 resistance zone. On the downside, break of 132.04 support is needed to indicate medium term reversal. Otherwise, outlook will stay bullish in case of deep pull back.

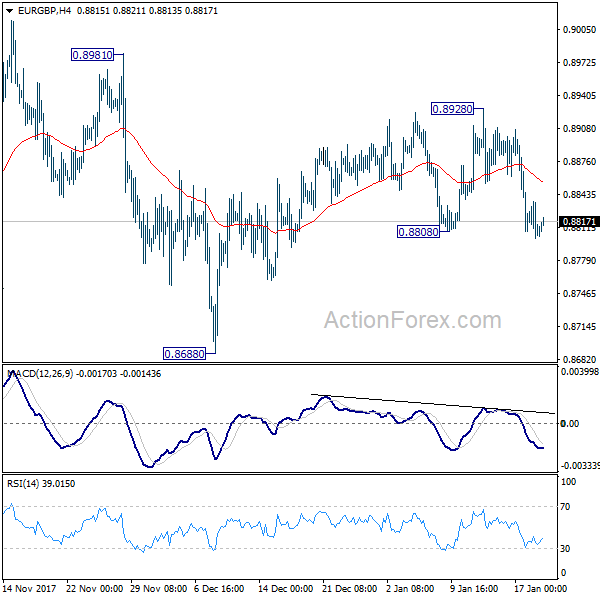

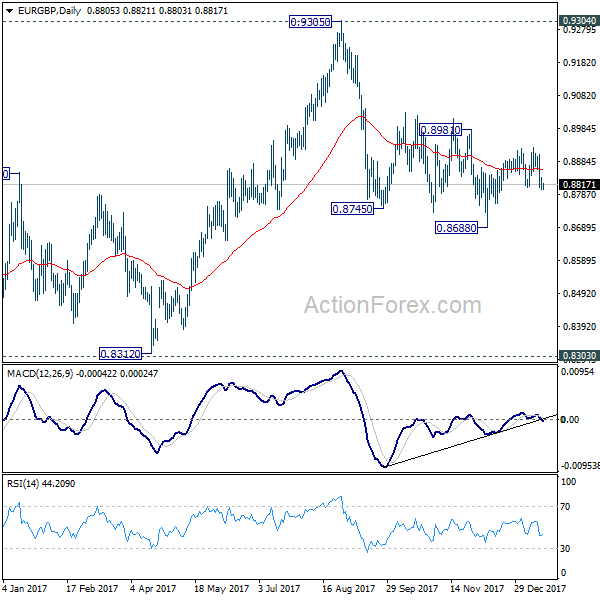

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8794; (P) 0.8815; (R1) 0.8830; More...

Intraday bias in EUR/GBP is turned to the downside with breach of 0.8808 minor support. Deeper fall would be seen to 0.8688 low first. Break there will resume whole decline from 0.9305. This will be favored as long as 0.8928 resistance holds, in case of recovery.

In the bigger picture, there are various ways to interpret price actions from 0.9304 high. But after all, firm break of 0.9304/5 is needed to confirm up trend resumption. Otherwise, range trading will continue with risk of deeper fall. And in that case, EUR/GBP could have a retest on 0.8303. But we'd expect strong support from 0.8116 cluster support (50% retracement of 0.6935 to 0.9304 at 0.8120) to contain downside.

Aussie Trading Higher In The Asian Session

For the 24 hours to 23:00 GMT, the AUD rose 0.6% against the USD and closed at 0.8006.

LME Copper prices traded flat to close at $7047.0/MT. Aluminium prices rose 1.7% or $38.0/MT to $2225.0/MT.

Yesterday, data showed that in China, Australia’s largest trading partner, gross domestic product (GDP) climbed more-than-anticipated by 6.8% on an annual basis in the fourth quarter of 2017, compared to market expectations for a rise of 6.7%. GDP had registered a similar rise in the prior quarter.

Other data revealed that the nation’s industrial production climbed 6.2% YoY in December, topping market expectations for a rise of 6.1%. In the prior month, industrial production had risen 6.1%. Meanwhile, the nation’s retail sales rose less-than-anticipated by 9.4% on a yearly basis in December, after recording a rise of 10.2% in the previous month, while investors were anticipating for a gain of 10.2%.

In the Asian session, at GMT0400, the pair is trading at 0.8015, with the AUD trading 0.11% higher against the USD from yesterday’s close.

The pair is expected to find support at 0.7969, and a fall through could take it to the next support level of 0.7923. The pair is expected to find its first resistance at 0.8041, and a rise through could take it to the next resistance level of 0.8067.

Amid no major macroeconomic releases in Australia today, investor sentiment would be governed by global macroeconomic news.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.

Euro Trading On A Stronger Footing This Morning

For the 24 hours to 23:00 GMT, the EUR rose 0.61% against the USD and closed at 1.2244.

The greenback nursed losses against its key counterparts, as investors were grappled with concerns of a possible US government shutdown as lawmakers struggled to forge a federal budget deal.

However, the US Dollar recouped some of its losses, after data showed that first time claims for the US unemployment benefits plunged more-than-expected to a level of 220.0K in the week ended 13 January, hitting its lowest level since February 1973, thus painting a rosier picture of the nation's jobs market. Markets had expected initial jobless claims to fall to a level of 249.0K, after recording a reading of 261.0K in the prior week.

On the other hand, the nation's housing starts fell more-than-anticipated by 8.2% on a monthly basis to an annual rate of 1192.0K in December, posting its biggest drop in just over a year, amid a steep decline in the construction of single-family housing units. Housing starts had registered a revised reading of 1299.0K in the previous month, while investors had envisaged for a fall to a level of 1275.0K. Further, the nation's building permits eased less-than-expected by 0.1% MoM to an annual rate of 1302.0K in December, compared to a revised level of 1303.0K in the prior month. Markets were expecting building permits to drop to a level of 1295.0K.

Other data indicated that the US Philadelphia Fed manufacturing index declined to a 5-month low level of 22.2 in January, more than market consensus for a drop to a level of 25.0. In the previous month, the index had registered a level of 26.2.

In the Asian session, at GMT0400, the pair is trading at 1.2262, with the EUR trading 0.15% higher against the USD from yesterday's close.

The pair is expected to find support at 1.2201, and a fall through could take it to the next support level of 1.2139. The pair is expected to find its first resistance at 1.2297, and a rise through could take it to the next resistance level of 1.2331.

Going ahead, traders would look forward to the Euro-zone's current account data for November and Germany's producer price index for December, scheduled to release in a few hours. Moreover, the US flash Michigan consumer sentiment index for January, slated to release later in the day, will attract a lot of market attention.

The currency pair is trading above its 20 Hr and 50 Hr moving averages.