Sample Category Title

Aussie Higher after Retail Sales, Dollar Down But Not Out

Aussie trades broadly higher in Asian session as lifted by retail sales data. While AUD/UD is still limited below 0.7896 key near term resistance, EUR/AUD has dipped through 1.5226 support, which signals more Aussie strength ahead. Over the week, Yen remains the strongest one on speculations of BoJ stimulus exit. Dollar suffered steep selling of talks that China will slow purchases of US assets. But still, the greenback in trading mixed, in red against Yen Aussie and Kiwi only.

Australia retail sales grew 1.2% in November

Australian Dollar is lifted by stronger than expected retail sales data today. Retail sales grew 1.2% mom in November, triple of expectation of 0.4% mom. There are talks that RBA could finally join some other global central banks in tightening this year. And RBA could raise the official cash rate by 25bps in August. However, the key would possibly lie in wage growth, which has been sluggish in spite of healthy job market growth. Also, recent cooling of housing markets also lessen the pressure on RBA to hike. These will be the two key factors to watch ahead.

Chicago Fed Evans prefer pause in rate hike

Chicago Fed President Charles Evans said he'd prefer a pause in tightening and wait until mid-2018 before raising interest rate again. He said that "I'd feel a lot more confident if I saw those transitory reductions in the inflation rate go away." And, "if in fact things are worked out we could resume a nice gradual pace (of rate hikes) at that point, and still get the funds rate up to its natural level before too long."

St Louis Fed President James Bullard joined the debate on so far price level targeting. Bullard said Fed's inability to meet inflation target in the past five years resulted in a 4.6% gap in the economy. And that amounts to more than USD 820b in the USD 18T economy. And to compensate for that, Fed would have to allow inflation to hit 2.5% for a decade.

Trump may announce Nafta withdrawal

Reuters reported that Canadian government is increasing convinced that US President Donald Trump will announce withdraw from Nafta, giving six month notice. Officials declined to comment on the rumor. The next talk between the US, Canada and Mexico will start on January 23 in Quebec, Canada. There are talks that officials are already scheduling to meet again in Mexico the next month, but there is no formal announcement yet. Canadian Dollar is mildly lower after the news.

Meanwhile, the President of US Chamber of Commerce Thomas J. Donohue warned that withdrawing from Nafta would be a "grave mistake". He said that "the American economy has taken several big steps forward with regulatory relief and tax reform, and the administration deserves lots of credit. But a wrong move on NAFTA would send us five steps back." He supported the modernization of the 24 year old trade agreement. But he emphasized that the trade agreement "should not close markets, undermine investment protections, or limit trade with regulatory red tape." And, "the bottom line is that growth will be weakened, not strengthened or sustained, if we pull back from trade."

Looking ahead

ECB monetary policy meeting accounts will be a key focus today. Eurozone will also release industrial production. Canada will release new housing price index. US will release PPI and jobless claims.

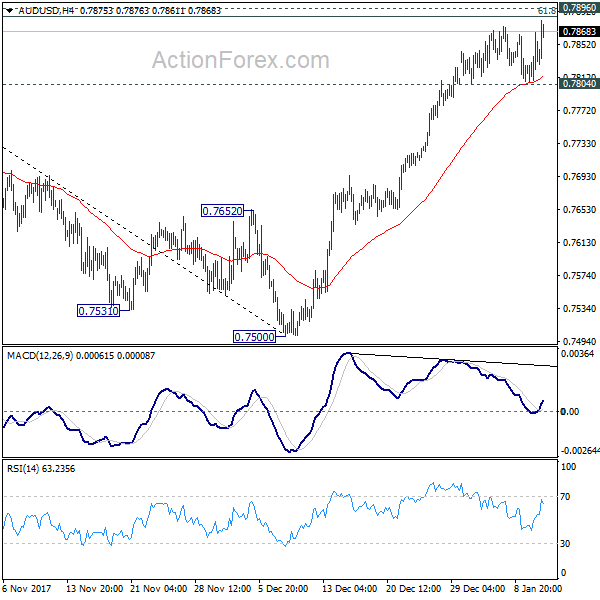

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7811; (P) 0.7838; (R1) 0.7869; More...

AUD/USD's rally resumed after drawing support from 4 hour 55 EMA. Outlook is unchanged. Considering bearish divergence condition in 4 hour MACD, upside should be limited by 0.7896 cluster resistance (61.8% retracement of 0.8124 to 0.7500 at 0.7886) resistance zone to bring short term topping. Break of 0.7804 minor support will turn bias to the downside for 55 day EMA (now at 0.7725). However, sustained break of 0.7886/96 will pave the way for retesting 0.8124 high.

In the bigger picture, we're still slightly favoring the case that corrective rise from 0.6826 medium term bottom is completed at 0.8124, after hitting 55 month EMA (now at 0.8032). But stronger than expected rebound from 0.7500 is dampening this bearish view. On the downside, break of 0.7500 will target 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) to confirm this bearish case. But break of 0.8124 will extend the rise from 0.6826 to 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451 before completion.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 00:30 | AUD | Retail Sales M/M Nov | 1.20% | 0.40% | 0.50% | |

| 05:00 | JPY | Leading Index Nov P | 108.6 | 106.5 | ||

| 10:00 | EUR | Eurozone Industrial Production M/M Nov | 0.80% | 0.20% | ||

| 12:30 | EUR | ECB Monetary Policy Meeting Accounts | ||||

| 13:30 | CAD | New Housing Price Index M/M Nov | 0.20% | 0.10% | ||

| 13:30 | USD | PPI M/M Dec | 0.20% | 0.40% | ||

| 13:30 | USD | PPI Y/Y Dec | 3.00% | 3.10% | ||

| 13:30 | USD | PPI Core M/M Dec | 0.20% | 0.30% | ||

| 13:30 | USD | PPI Core Y/Y Dec | 2.50% | 2.40% | ||

| 13:30 | USD | Initial Jobless Claims (JAN 06) | 248K | 250K | ||

| 15:30 | USD | Natural Gas Storage | -206B |

USDJPY – Risk Remains Lower, Sells Off

USDJPY - The pair closed further lower on sell off on Wednesday. On the downside, support lies at the 111.00 level where a break if seen will aim at the 110.50 level. A cut through here will turn focus to the 110.00 level and possibly lower towards the 109.50 level. On the upside, resistance resides at the 112.00 level. Further out, we envisage a possible move towards the 112.50 level. Further out, resistance resides at the 113.00 level with a turn above here aiming at the 113.50 level. On the whole, USDJPY faces further bearishness.

Caution: Enter At Your Own Risk

Caution enter at your own risk

It has been a very unsettling time in the macroeconomic world since we entered 2018, but the plethora of USD destabilising headlines overnight stretching from Beijing to Washington has thrown a spanner into the works letting the foxes run wild in the USD henhouse. It all kicked off with suspicious headlines from 'people familiar with the matter” that China officials are viewing US treasuries as less attractive. But the timing of the headline is what sent the market reeling trigging a frantic knee-jerk reaction on USD and Gold as it was thought China was retaliating ahead of potential trade announcements from the Trump Administration.

We have been down this road before, and US treasuries are often used during the political ping-pong match when trade tensions escalate. While it’s entirely possible that China could take measure to rebalance their reserve as they have done in the past, but the markets quickly dismissed the headline first viewing it as little more than political sabre rattling and then correctly determining its highly improbable China will stop buying US Treasuries.

Equity Markets

The US equity markets waned in very choppy trading overnight as US yields jumped higher on the China rumours but more significantly that NAFTA speculation was suggesting that President Trump would announce the US is pulling out of the trade agreement which sent the three major US stock indexes reeling given possible negative implication on corporate earnings. However, the selloff is likely a bit overblown, as political noise tends to exaggerate when there is a shortage of US economic data.

Oil Markets

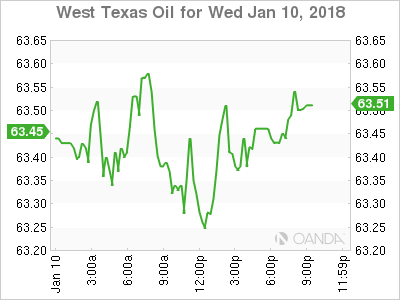

Oil prices were buoyant, and while showing no signs of buyers remorse, Traders did not substantially add to yesterday’s gains despite the Energy Information Administration reported a higher draw than expected. After touching price peaks not seen since 2014 on Wednesday, the lack of follow-through from the EIA data could mean markets are getting a bit fatigued, and a healthy correction could be on the cards.

Gold Markets

Gold markets were predictably reactive to the rumour roil overnight. Nevertheless, that aside, rising oil prices and strong global growth suggest gold will remain supported as investors look for inflation protection. Also, a highly anticipated stock market correction is providing support on dips which continues to support the bullish Gold narrative.

G-10

Canadian Dollar and Mexican Peso

Both currencies gapped lower on the NAFTA headlines. While we do not know the full extent of the US trade policy as of yet, there is some thought we are entering the year of US protectionism, and there is no better platform than World Economic Forum in Davos Jan 23-26 to unleash a torrent of protectionist America First policy. While uncertainty around the NAFTA agreement is swirling, the risk of its demise is elevated wilting any Bank of Canada rate hike momentum the Canadian dollar was riding.

Japanese Yen

Asia is very much in focus this morning after the USDJPY plummeted through significant support levels like a hot knife through butter. USDJPY is touched a low of 111.30 overnight of the China/Treasuries rumours triggered a wave of dollar selling, but unlike against other G-10 pairs, USDJPY has failed to recover suggesting the market remains on guard against a quicker pace of BoJ tapering. Also, while the latest move is screaming, 'correction ', surprisingly few are willing to take a pig and a poke at this juncture .

Asia FX

Good news is the market is not falling to pieces after the mini USDCNY squeeze. Moreover, whatever whispers have been circulating about the imminent demise of Asia FX, they indeed have not led to a dramatic transformation or a notable shift in attitude. Instead now is the time to be patient and let the rumour roiled markets settle.

Not to diminish the fact that rising US yields could present some significant headwinds for local currencies, but the USD is getting little support from higher US rates suggesting FX markets are less sensitive to that specific correlation near term.

China inflation data was a bit damp, and that too has given traders cause for thought.

The Malaysian Ringgit

The Ringgit remains entrenched around the 4.00 USDMYR level awaiting the next domestic catalyst. Industrial Production is due later today, but I suspect the market remains more focused on rate hike speculation. On a positive note, high-energy prices are most helpful to Malaysia adding a welcome boost to fiscal revenue.

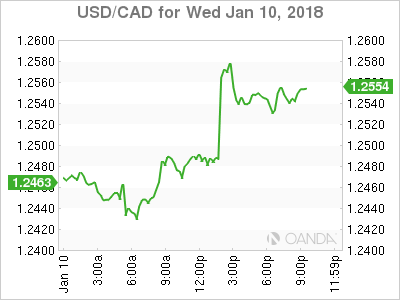

USD/CAD Canadian Dollar Drops On NAFTA Concerns

The Canadian dollar fell 0.62 percent on Wednesday after reports circulated about the Trump administration pulling the US out of NAFTA. The loonie had a positive return this year versus the greenback, but the NAFTA setback has it now at negative 0.11 percent YTD. Canadian officials anonymously agreed that there is a rising probability of the White House giving a six month notice on the trade agreement.

The White House made an official announcement that there hasn't been any change in the Trump's administration position on NAFTA, but given the lack of real progress on the talks between Canada, Mexico and the United States there was little hope of a successful renegotiation to begin with.

The CAD has been surging after a strong Canadian jobs report put the odds of a rate hike by the Bank of Canada (BoC) at 80 percent for the January monetary policy meeting. The outcome of the NAFTA renegotiations is one of the identified unknowns by Stephen Poloz which could keep the central bank from raising interest rates.

The USD/CAD gained 0.65 percent on Wednesday. The currency pair is trading at 1.2543 after the impact of the report by Reuters who cited two unknown sources within the Canadian government on the probability of the end of NAFTA. The trade agreement renegotiations will enter its sixth round of talks.

The process has been slow and painful as the United States opened negotiations with a very one sided demands that were met with shock from their counterparts in Canada and Mexico and they have not backed down. Mexico has said it would back out if tariffs were introduced and Canada has also questioned the higher US content rules on vehicles.

The Canadian dollar was on the rise with strong fundamentals and a higher oil price sustaining the move, but it all changed with the open secret that Canadian officials foresee its largest trading partner backing out of the two decade deal. The resulting uncertainty on the two partner NAFTA deal and bilateral trade with the US, outstanding disputes in mind, puts downward pressure on the prospects for the Canadian economy. The USD is having a terrible start of the year, but very swiftly the CAD could underperform optimistic expectations.

The Bank of Canada (BoC) Business survey released this week showed that Canadian companies are not suffering extra anxiety in their outlook due to their trade agreement, but as evidenced today the market does not share that optimism.

Governor Poloz ended the year with a speech focusing on the topics that kept him up at night but the solid December jobs report and the BoC Survey have all but convinced the market that a rate hike will be announced on the January 17 central bank meeting.

The price of oil rose to $63.380 after the release of the US crude inventory data by the Energy Information Administration (EIA). A bigger than expected crude drawdown of 4.9 million barrels was almost double the forecast of 2.5 million barrels. Gasoline and distillates showed a buildup of inventories with gasoline stocks rising 4.1 million barrels versus the 2.5 million estimate. Distillates rose 4.2 million barrels destroying the forecast of 1 million.

Market events to watch this week:

Thursday, January 11

8:30am USD PPI m/m

8:30am USD Unemployment Claims

Friday, January 12

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Gains As China Mulls Slowing US Bond Purchases

Gold has posted gains in the Wednesday session. In North American trade, the spot price for an ounce of gold is $1316.80, up 0.30% on the day. On the release front, it was a quiet day. Import Prices slowed to 0.1%, short of the estimate of 0.4%. On Thursday, the US releases PPI reports and unemployment claims.

The US dollar is under pressure on Wednesday, and gold has moved higher. The catalyst for this move was a report on Wednesday that China was considering slowing or halting the purchase of US government bonds. China boasts the largest currency reserves, estimated at $3 trillion. It is also the biggest holder of US government bonds, in the amount of $1.19 trillion. Why would China make this move? One reason is that it may consider US treasuries less attractive compared to other assets. As well, it could be part of China’s strategy to flex some muscle as a possible trade war looms between the US and China, which are the two largest economies in the world. The report has pushed US Treasury yields higher and sent the US dollar downwards.

Gold prices have shown strong gains since mid-December, leaving many investors scratching their heads. A robust US economy and a December rate hike from the Federal Reserve have increased the appetite for risk, and the stock markets have pushed higher since the New Year. This should translate into lower prices for safe-haven gold, but the base metal has jumped on the bandwagon and posted strong gains in early January. On Friday, gold touched a high of $1326, its highest level since mid-September. Will enthusiasm for gold continue? Much will depend on the strength of the US dollar – if the greenback runs into headwinds against the major currencies, gold could resume its rally.

British Pound Edges Lower As Manufacturing Production Slows

The British pound has posted slight losses in the Wednesday session. In North American trade, GBP/USD is trading at 1.3510, down 0.23% on the day. In economic news, British Manufacturing Production slowed to 0.4% in November, down from 0.7% a month earlier. Still, this beat the estimate of 0.3%. Over in the US, Import Prices slowed to 0.1%, short of the estimate of 0.4%. On Thursday, the US releases PPI reports and unemployment claims.

The US dollar is under pressure, after a report on Wednesday that China was considering slowing or halting the purchase of US government bonds. China boasts the largest currency reserves, estimated at $3 trillion. It is also the biggest holder of US government bonds, in the amount of $1.19 trillion. Why would China make this move? One reason is that it may consider US treasuries less attractive compared to other assets. As well, it could be part of China’s strategy to flex some muscle as a possible trade war looms between the US and China, which are the two largest economies in the world. The report has pushed US Treasury yields higher and sent the US dollar downwards.

Brexit negotiations have been slow and difficult, as Europe is not keen on rewarding Britain for departing the European Union. There are serious divisions within the government with regard to the talks. and May has to walk carefully, as she has a razor thin majority in parliament, Prime Minister May can ill afford any mistakes, and if her government runs into trouble, she may be forced to call elections, which could shake up the markets and send the pound downwards. The public is almost evenly split on whether Brexit is a good idea, and there are serious concerns that the British economy will take a hit, even if a deal is worked out before the March, 2019 deadline. The parties do not have a lot of time to hammer out a host of trade issues, and all indications are that the negotiations road will be bumpy and difficult.

EURJPY Extends Downtrend; Risk of More Downside

EURJPY extended its bearish phase by dropping another leg lower into the 133 handle. The downtrend since January 5 from the high of 136.63 has not shown signs of reversing. RSI on the 4-hour chart is well into bearish territory although close to oversold levels. This suggests some easing in downside pressure for now.

Short-term price action still looks soft and there is a high risk of another extension lower towards 133. This is considered to be a strong support level which saw several tests back in 2017.

Meanwhile, any rebound from current levels is expected to find resistance at 134. Only a move above resistance at 135 would indicate the end of the recent downtrend and would give scope for a test of 136, which was previously a strong support level. As such, it may be a challenge to breach but if successful, EURJPY would likely rise towards the 136.63 peak and beyond.

For now, EURJPY is clearly in a bearish phase with low odds for a rebound past 134 in the near term.

Sunset Market Commentary

Global core bonds trade mixed today with US Treasuries underperforming German Bunds. The main move of the day (sell-off US Treasuries) occurred after rumours that China is contemplating to slow or halt US Treasury purchases from its giant FX reserves. That would come at a time when the US Treasury needs to plug a bigger funding hole. The Bloomberg article triggered more selling and curve steepening in an already fragile US bond market. The US 10-yr yield broke above 2.5% (minor) resistance yesterday and is now definitively on its way to key 2.63%/2.64% resistance (2016/2017 highs). Tomorrow and Friday's inflation readings could be a trigger. US yields add 0.4 bps (2-yr) to 4.4 bps (30-yr) on a daily basis. Rising inflation (expectations), a tight labour market, strong growth and global policy normalization were already at play. The German bund whipsawed around opening levels amid an empty eco calendar. The €5bn German Bund auction drew only €4.56bn bids, but that's no recent phenomenon. Changes on the German yield curve are limited to 1 bp. Peripheral yield spreads widen marginally. The Italian debt agency successfully launched a new 20-yr BTP via syndication (€9bn 2.25% Sep2036). The Portuguese Treasury raised €4bn via a syndicated 10-yr PGB launch (Oct 2028).

This morning, it looked that the dollar would follow a similar pattern as it did yesterday. USD/JPY remained in the defensive as the yen held strong after yesterday's reduced BoJ bond purchases. EUR/USD didn't decline further and EUR/USD settled in the 1.1925/50 area. The headlines on the China reserve policy also unsettled USD trading. The dollar was hit quite hard even as interest rate differentials widened in favour of USD. Investors concluded that less Chinese appetite for US assets could also reduce the share of USD in Chinese FX reserves, triggering USD selling. USD/JPY trades near 111.50. EUR/USD hovers around the 1.20 pivot.

Sterling trading was again mainly driven by the broader price moves in the euro and the dollar. EUR/GBP traded with a positive intraday bias. The pair rebounded from the 0.8820 area to 0.8870, supported by the intraday rise of EUR/USD. Some sterling softness was also at work, probably as markets were disappointed by the UK government reshuffle. UK eco data (production, trade balance, GDP estimate) were mixed to OK, but didn't help sterling much. Cable trades in the 1.3535 area and hardly profits from the overall USD decline.

Stock markets got a snag from the bounce in volatility after the Chinese rumours. European indices lose up to 0.5% with Germany underperforming (-0.90%). Openings losses on US bourses amount to 0.3%.

News Headlines:

Officials in Beijing reviewing the nation's foreign-exchange holdings have recommended slowing or halting purchases of US Treasuries, according to people familiar with the matter. Markets reacted nervous (see above).

Scandinavian currencies were in good shape ahead of the Chinese news. The Norwegian krone profited from higher-than-forecast Norwegian inflation readings (1.6% Y/Y headline and 1.4% Y/Y core CPI) with EUR/NOK temporary hitting 9.60. The Swedish krona received a boost after the publication of slightly more hawkish than expected Riksbank Minutes. Governors Ingves suggested that the Swedish central bank could start its normalization process earlier than the ECB. EUR/SEK reached an intraday low around 9.75.

The Polish central bank kept its policy rate unchanged at 1.5% as widely anticipated. Governor Glapinski and the other central bankers will comment on the decision later this afternoon.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.28; (P) 112.72; (R1) 113.09; More...

USD/JPY drops sharply today with a strong break of 112.02 support. The development now suggests that decline from 114.73 is resuming. Intraday bias is back on the downside for 110.83 first. Break will target 61.8% retracement of 107.31 to 114.73 at 110.14. We'd look for bottoming signal again below 110.14. On the upside, above 112.05 minor resistance will turn intraday bias neutral first.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

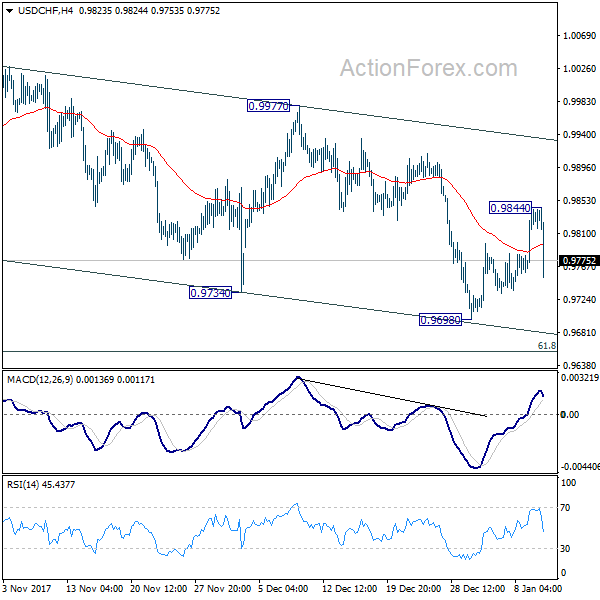

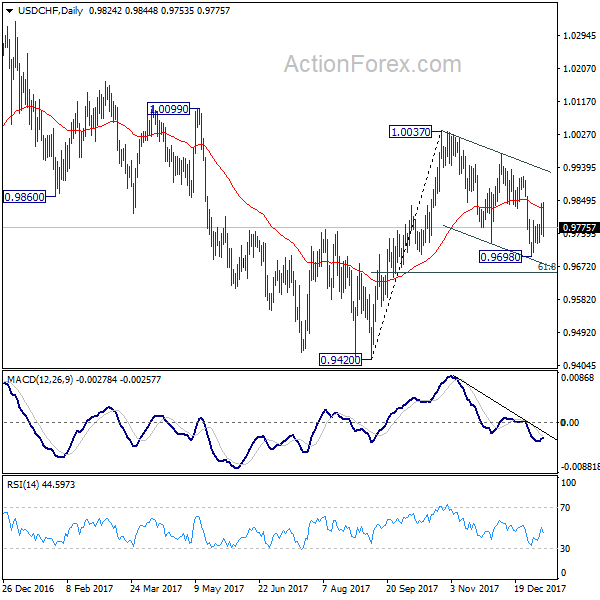

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9780; (P) 0.9811; (R1) 0.9863; More....

USD/CHF's rebound was limited at 0.9844 and drops sharply. Intraday bias is turned neutral first with mixed near term outlook. Nonetheless, we're still slightly favoring that correction from 1.0037 has completed with three waves down to 0.9698. Above 0.9844 will turn bias back to the upside for 0.9977 resistance for confirming this bullish view. However, break of 0.9698 will extend such correction to 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 before completion.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.