Sample Category Title

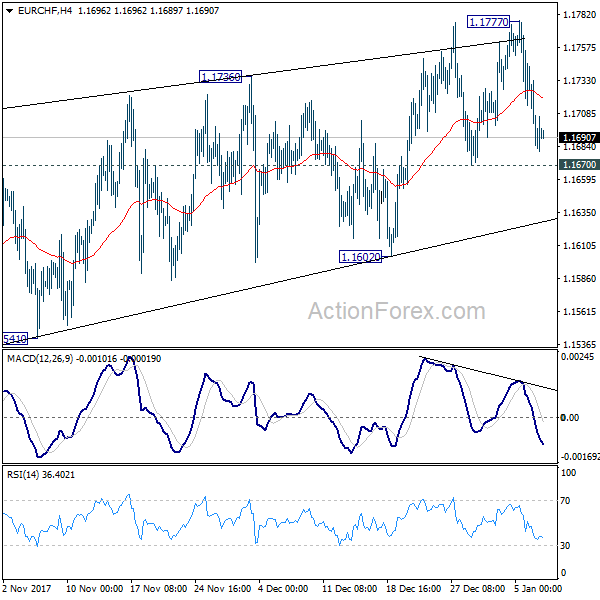

EUR/CHF Daily Outlook

Daily Pivots: (S1) 1.1670; (P) 1.1708; (R1) 1.1733; More...

Intraday bias in EUR/CHF remains neutral at this point. We're holding on to the view that it's close to topping, if not formed. And even in case of another rise, strong resistance should be seen well below 1.2 handle to bring medium term reversal. On the downside, below 1.1670 minor support will turn bias to the downside for 1.1602 support first. Further break of 1.1602 will indicate reversal and turn outlook bearish for 1.1387 and below.

In the bigger picture, while a medium term top could be around the corner, there is no change in the larger outlook. That is, long term rise from SNB spike low back in 2015 is still in progress and would extend. As long as 1.1198 resistance turned support holds, we'll hold on to this bullish view and expect another to prior SNB imposed floor at 1.2000. Though, we'll reassess the outlook if 1.1198 is firmly taken out.

Market Update – Asian Session: North And South Korea Hold First Talks Since 2015

Headlines/Economic Data

General Trend: Asian equities are generally higher as US indices ended mostly positive

Nikkei and USD/JPY pare gains amid BoJ reduction of purchases of longer dated JGBs in daily operation

Analysts ponder if BoJ move at daily operation has broader implications for monetary policy

Japan Nov inflation adjusted real wages see first rise in 11-months (*Note: Wages are seen as key to BoJ policy to help maintain the ‘virtuous’ cycle. On

Jan 5th, Japan PM Abe reiterated his call for companies to raise wages by 3% to put the economy on a ‘virtuous’ cycle)

Japan Finance Min Aso said equities are rising at fast pace on global economic recovery

Samsung Electronics declines as Q4 guidance below consensus

In talks, North Korea and South Korea said to reach agreement on Winter Olympics, but other areas less clear

Japan

Nikkei 225 opened +1% (closed during prior session): close +0.6%

TOPIX Real Estate Index +2.2%, Securities +0.8%

Sony +2.6% (released 2017 holiday sales for PS4)

Fast Retailing +1.4% (Dec SSS +18.1% y/y)

USD/JPY down over 0.4%, BOJ bond buying adjustment triggering the yen and hitting stops

(JP) JAPAN NOV LABOR CASH EARNINGS Y/Y: 0.9% V 0.6%E; REAL CASH EARNINGS Y/Y: +0.1% V -0.1%E (1st rise in 11-months)

(JP) Japan Fin Min Aso: Equities are rising at a fast pace

(JP) BOJ announcement related to daily bond buying operation: reduces planned daily purchases of 10-25 year and over 25-year JGBs each by ¥10B

(JP) Analysts look at tonight's announcement by the BOJ reducing bond buying and how it could be the first indication that tightening is on the way, despite its commitment to ultra easy monetary policy

6758.JP Reports 2017 holiday period PS4 sales of 5.9M units v 6.2M units in 2016

Korea

Kospi opened -0.1%

Samsung -2.8%: Reported prelim Q4 below expectations, 005930.KR Reports prelim Q4 (KRW) Op profit 15.1T v 15.9Te; Rev 66.0T v 66.8Te; opened slightly lower

Steelmakers track gains seen in the US: Hyundai Steel +1.7%, Posco +1.7%

LG Innotek: +10.5%: Apple said to be funding LG Innotek's 3D camera factory - Korean press

LG Electronics +2.3% (reported prelim Q4 results; declined over 5% on prior session)

Samsung C&T +3.5% (announced management changes)

(KR) South Korea trade officials see 4% growth in exports in 2018 - Korean press

(KR) North and South Korea hold first talks since 2015: North Korea expressed will to jointly enter winter Olympics

China/Hong Kong

Hang Seng opened +0.1%, Shanghai Composite -0.1%

Hang Seng Info Tech Index +0.9%, Services Index +1.1% (strength in gaming names)

Hang Seng Materials Index -1.8%: Aluminum Corp of China -4.5% (broker commentary)

(CN) China Ministry of Industry: To allow 1 tonne of new steel capacity to be built for each 1.25 tonnes closed in key regions – press

(CN) Commerzbank economist Zhou Hao: Possibility very low for China lending rate hike

(CN) China said to have stopped approving some kinds of consumer loan ABS, including micro loans - press

USD/CNY (CN) Yuan is likely to keep strengthening, China may accelerate yuan exchange rate reform - China Securities Journal

USD/CNY China's stable FX reserves will support yuan value in 2018 - Chinese press

(CN) China PBoC: Skips OMO for 12th straight session; Net drains CNY130B v CNY40B prior; Current bank liquidity is moderate (prior banking liquidity at relatively high level)

(CN) China PBoC sets yuan reference rate at 6.4968 v 6.4832 prior

(CN) China Dec Retail Auto Sales y/y: 0.6% v 3.2% prior; 2017 24.2M units, 1.5% y/y (record sales for 27th consecutive year) - PCA

Looking Ahead: China Dec CPI and PPI due for release on Wednesday

Australia/New Zealand

ASX 200 opens +0.1%; closed %

ASX 200 Resources Index +0.7%, Financials +0.2%; Consumer Discretionary -0.5%

(AU) AUSTRALIA NOV BUILDING APPROVALS M/M: 11.7% V -1.3%E; Y/Y: 17.1% V 4.6%E

(AU) Australia Dec ANZ Job Advertisements M/M: -2.3% v 1.1% prior

Looking Ahead: Australia Dec NAB Business Confidence due for release on Wednesday

Other Asia

(ID) Indonesia Fin Min Indrawati: 2017 GDP growth to fall short of target; ready to use all instruments to maintain growth momentum

(TW) Taiwan 2018 machinery exports seen up over 10% - Taiwanese Press

North America

US equity markets ended mostly higher: Dow -0.1%, S&P500 +0.2%, Nasdaq +0.3%, Russell 2000 +0.1%

S&P500 Sectors: Utilities +0.9%, Real Estate +0.7%; Health Care -0.4%, Financials -0.1%

(US) Fed's Bostic (2018 voter, dove): Fed may not need 3 or 4 rate hikes a year; policy is approaching a more neutral stance that could be close to 2%; Personal base case is for 2 or 3 rate hikes this year; Wants to see inflation higher to justify 3-4 rate hikes

(US) Fed's Williams (moderate, 2018 voter): central banks have less room to cut rates in the next crisis

(US) Fed's Rosengren (moderate, non-voter): Optimal rate of inflation may move around just as the natural rate of unemployment does

(US) White House reportedly near to a decision on Fed vice chair nomination - press

(US) Special Counsel Mueller reportedly likely to interview Pres Trump as part of Russia investigation in next few weeks - Wash Post

Looking Ahead: US Weekly API Crude Oil Inventories due for release

Europe

(UK) Brexit Min Davis: sees EU's no-deal Brexit planning as 'damaging' to the process - FT

(UK) DEC BRC SALES LFL Y/Y: 0.6% V 0.3%E

(IE) Ireland Dec Consumer Confidence Index: 103.2 v 103.6 prior

Looking Ahead: Germany Nov Trade Balance and Industrial production due to be released

Levels as of 01:00ET

Nikkei225 %, Hang Seng +0.3%; Shanghai Composite +0.0%; ASX200 +0.1%, Kospi -0.3%

Equity Futures: S&P500 +0.2%; Nasdaq100 +0.2%, Dax +0.2%; FTSE100 +0.1%

EUR 1.1975-1.1958; JPY 113.18-112.50; AUD 0.7865-0.7839;NZD 0.7197-0.7167

Feb Gold -0.0% at $1,320/oz; Feb Crude Oil +0.8% at $62.22/brl; Mar Copper +0.0% at $3.23/lb

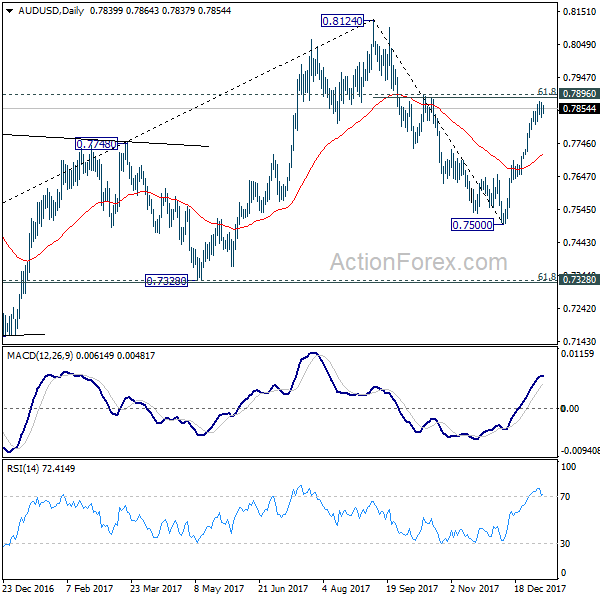

AUD/USD Daily Outlook

Daily Pivots: (S1) 0.7821; (P) 0.7846; (R1) 0.7866; More...

Intraday bias in AUD/USD remains neutral for the moment. Considering bearish divergence condition in 4 hour MACD, even in case of another rise, upside should be limited by 0.7896 cluster resistance (61.8% retracement of 0.8124 to 0.7500 at 0.7886) resistance zone to bring short term topping. Break of 0.7804 minor support will turn bias to the downside for 55 day EMA (now at 0.7711).

In the bigger picture, we're still slightly favoring the case that corrective rise from 0.6826 medium term bottom is completed at 0.8124, after hitting 55 month EMA (now at 0.8032). But stronger than expected rebound from 0.7500 is dampening this bearish view. On the downside, break of 0.7500 will target 0.7328 key cluster support (61.8% retracement 0.6826 to 0.8124 at 0.7322) to confirm this bearish case. But break of 0.8124 will extend the rise from 0.6826 to 38.2% retracement of 1.1079 (2011 high) to 0.6826 (2016 low) at 0.8451 before completion.

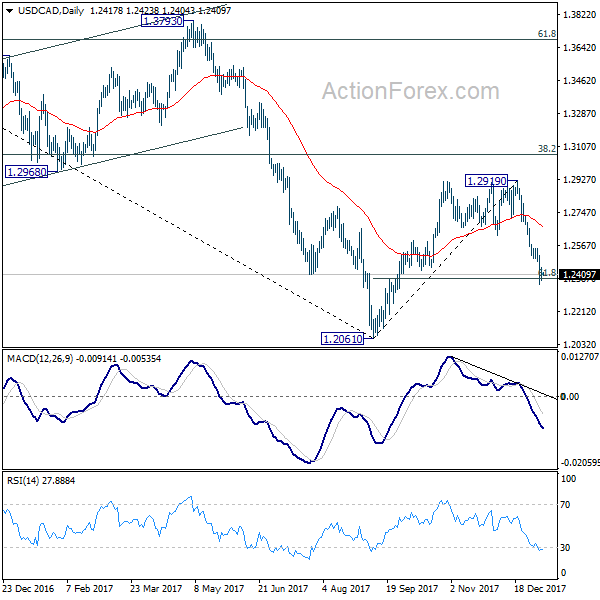

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.2381; (P) 1.2415; (R1) 1.2453; More....

With 1.2480 minor resistance intact, intraday bias in USD/CAD remains on the downside. Current momentum argues that larger down trend from 1.4689 might be resuming. Deeper fall should be seen back to retest 1.2061 low first. On the upside, above 1.2480 minor resistance will turn bias neutral and bring consolidation before staging another decline.

In the bigger picture, current development argues that rebound from 1.2061 has completed at 1.2919, rejected by 55 week EMA (now at 1.2850) and kept below 38.2% retracement of 1.4689 to 1.2061 at 1.3065. The development also suggests that long term fall from 1.4689 is not completed yet. Decisive break of 1.2061 low will target 61.8% retracement of 0.9406 to 1.4689 at 1.1424. This will now be the favored case as long as 1.2929 resistance holds.

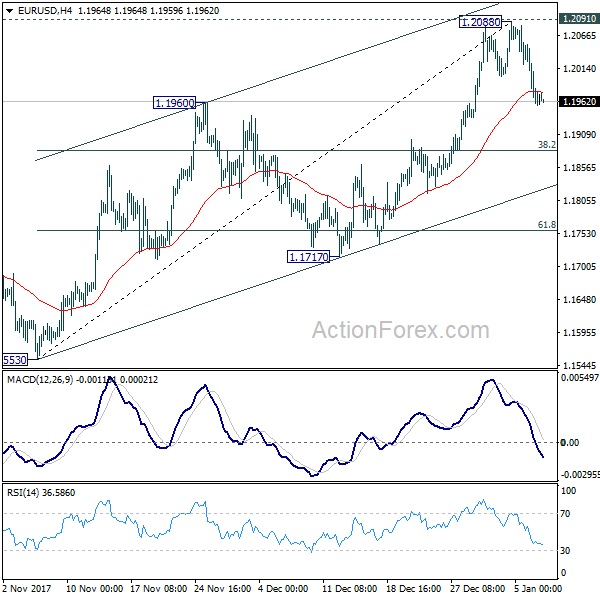

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1931; (P) 1.1991 (R1) 1.2028; More....

Intraday bias in EUR/USD remains mildly on the downside for the moment. The pair could have been rejected by 1.2091 key near term resistance. And, fall from 1.2088 might be the third leg of consolidation pattern from 1.2091. Further decline should be seen to 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break of 1.1884 will target 61.8% retracement at 1.1757 and below. On the upside, firm break of 1.2091 is needed to confirm up trend resumption. Otherwise, we'd expect more corrective trading in near term.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

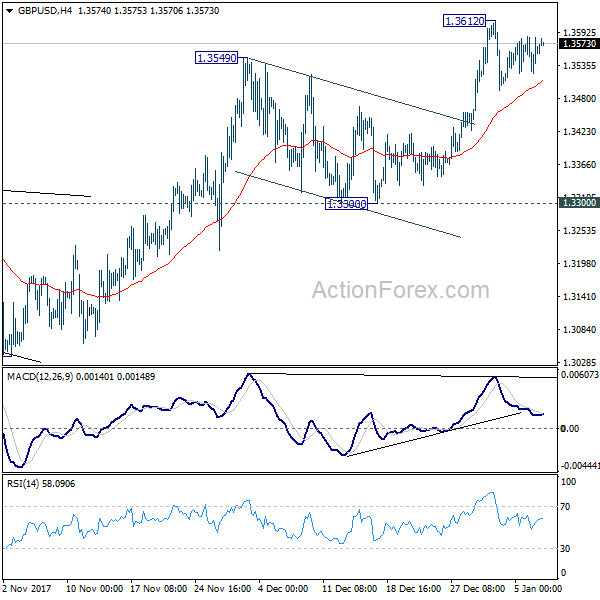

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3530; (P) 1.3558; (R1) 1.3593; More.....

GBP/USD is staying in consolidation from 1.3612 temporary top. Intraday bias remains neutral first. As long as 4 hour 55 EMA (now at 1.3508) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support instead.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

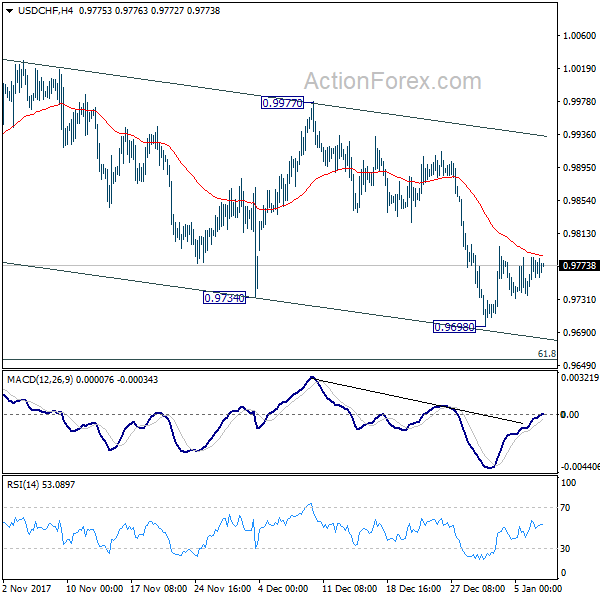

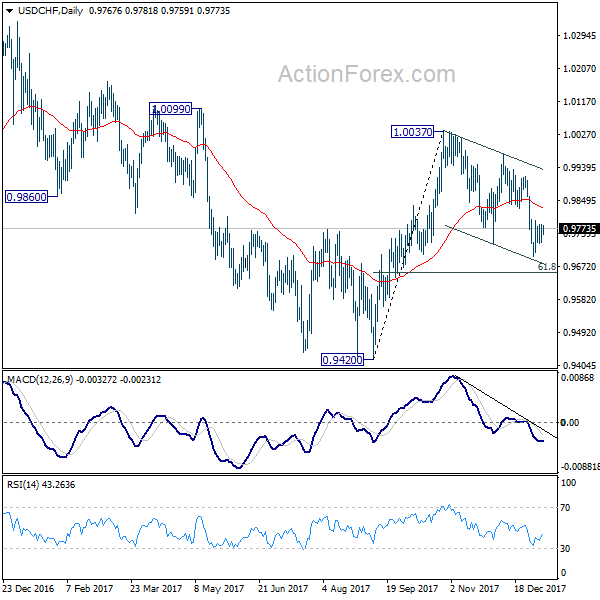

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.9745; (P) 0.9764; (R1) 0.9791; More....

USD/CHF is still staying in corrective trading above 0.9689 temporary low. Intraday bias remains neutral at this point. As long as 4 hour 55 EMA (now at 0.9785) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

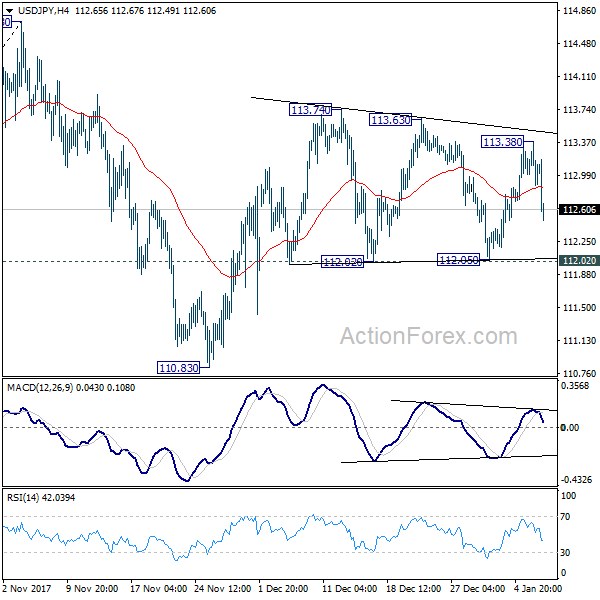

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.85; (P) 113.11; (R1) 113.35; More...

USD/JPY drops sharply after hitting 113.38. But after all, it's staying in range of 112.02/113.74. Intraday bias remains neutral at this point. Also, outlook remains cautiously bullish as long as 112.02 holds and further rise is in favor. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Yen Jumps as BoJ Lowers Long Dated JGB Purchase, Aussie Rebounds on Housing Data

Yen strengthens against all major currencies in Asian session on news that BoJ lowers its long-dated JGB purchases. Strength in Yen is followed by Aussie, which is lifted by strong housing data. On the other hand, Dollar and Euro are both trading weakly. Comments from Fed officials overnight gave no extra confidence to the markets that Fed would hike three more times this year, not to mention four. Meanwhile, Euro stays soft as recent rally lost steam.

BoJ cut 10-25 years JGB purchase by JPY 10b

Yen surges broadly today as data showed BoJ has cut its long-dated JGB purchases in market operations. That's seen as a sign by many of BoJ is finally moving towards stimulus exit. Today, BoJ offered to buy JPY 190b of JGBs with 10 to 25 years maturity. That's JPY 10b lower from the prior tender on December 28. Besides, BoJ also lower the offer on 25 to 40 years maturity JGBs by JPY 10b to JPY 90b. Nonetheless, it should be emphasized that it's far still early for BoJ to start stimulus exit as inflation remains way off target.

Also, it's still uncertain whether BoJ Governor Haruhiko Kuroda's term would be renewed this year. Prime Minister Shinzo Abe said during the weekend that "Gov. Kuroda has met my expectations with job availability at a 43-year high," and "I want him to keep up his efforts". But Abe also noted that "I haven't made up my mind" on who's going to lead BoJ after Kuroda's term expires in April.

Released from Japan, labor cash earnings rose 0.9% yoy in November, above expectation of 0.6% yoy.

Aussie rebounds on strong building approvals

Australian dollar rebounds notably today following strong housing data. Building approvals rose 11.7% mom in November, versus consensus of -1.0% mom fall. AUD/USD dipped briefly yesterday after the government forecasts iron ore price to drop 20% this year. While loss was very limited, it should be noted that upside momentum in AUD/USD has been diminishing for a while. Hence, we're not expecting a 0.7896 near term resistance on the next move. Aussie will look into retail sales and China data later in the week.

North and South Korea delegates meet in the "Peace House"

North and South Korea holds a rare high-level talks in the so-called Peace House in Panmunjom, a village in the Demilitarized Zone between the two countries. North Korea said that it would send athletes and a high-level delegation to the Winter Olympics in South Korea in February. The delegation will include athletes and supporters, amongst others. The North also expressed the willingness to resolve inter-Korea issues through dialogues. On the other hand, delegates from the South wants both nations to march together at the Games and proposed reunions of families during the upcoming Lunar New Year.

More bet on BoC hike this month

Hopes for a BOC rate hike, by 25 bps, at next week's meeting has surged to 85%, thanks to the Business Outlook and Senior Loan Office surveys for 4Q17 and the strong job market data which has already sent the loonie to a 3 months' higher last week. Canadian government bond prices generally weakened across the yield curve, sending 2-year yields lower 1.784% and 10-year yields down to 2.159%. The Business Outlook survey revealed that a net 56% of firms admitted "some" or "significant" difficulty in meeting additional demand. This marks the highest reading for a decade. Meanwhile, firms' capex and hiring intentions strengthened in 4Q17. However, inflation expectations remained subdued, a net 56% of respondents expecting inflation to stay at or below 2% over the next 2 years, compared with 59% in the previous survey.

Atlanta Fed Bostic: May not need three hikes per year

Atlanta Fed President Raphael Bostic said that he agrees to Fed's "slow removal" of monetary policy accommodations. But he emphasized "I would caution that that doesn't necessarily mean as many as three of four moves per year." He pointed to the surveys should that "individuals may not be completely convinced" on Fed's commitment or ability to reach the 2% inflation target. And "this possibility is one factor that might argue for being somewhat more patient in raising rates." Bedsides, he noted that the so called "neutral" rate could have dropped to "close to 2%". And Fed only needs to hike two or three more times before monetary policy is no longer considered "loose".

On the other hand, San Francisco Fed President John Williams said Fed should hike three times this year. He noted that "we're in a pretty good situation: the economy is doing great, everyone expects us to raise rates gradually ... and if the data change we can respond to that." He expressed that "I'm not worried about inflation suddenly taking off," and "something like three rate hikes makes sense to me".

Looking ahead

Swiss unemployment rate, foreign currency reserves and retail sales will be featured in European session. Eurozone will release unemployment rate, German industrial production and trade balance. Later in the data, Canada will release housing starts.

USD/JPY Daily Outlook

Daily Pivots: (S1) 112.85; (P) 113.11; (R1) 113.35; More...

USD/JPY drops sharply after hitting 113.38. But after all, it's staying in range of 112.02/113.74. Intraday bias remains neutral at this point. Also, outlook remains cautiously bullish as long as 112.02 holds and further rise is in favor. Break of 113.74 will resume the rebound from 110.83 and target 114.73 key resistance. Decisive break there will carry larger bullish implications. However, break of 112.02 will likely extend the corrective pattern from 114.73 with another leg through 110.83 support.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 0:00 | JPY | Labor Cash Earnings Y/Y Nov | 0.90% | 0.60% | 0.60% | 0.20% |

| 0:01 | GBP | BRC Retail Sales Monitor Y/Y Dec | 0.60% | 0.30% | 0.60% | |

| 0:30 | AUD | Building Approvals M/M Nov | 11.70% | -1.00% | 0.90% | -0.10% |

| 5:00 | JPY | Consumer Confidence Index Dec | 45 | 44.9 | ||

| 6:45 | CHF | Unemployment Rate Dec | 3.00% | 3.00% | ||

| 7:00 | EUR | German Industrial Production M/M Nov | 1.80% | -1.40% | ||

| 7:00 | EUR | German Trade Balance Nov | 20.7B | 19.9B | ||

| 8:00 | CHF | Foreign Currency Reserves Dec | 738B | |||

| 8:15 | CHF | Retail Sales Real Y/Y Nov | -2.50% | -3.00% | ||

| 10:00 | EUR | Eurozone Unemployment Rate Nov | 8.70% | 8.80% | ||

| 13:15 | CAD | Housing Starts Dec | 240K | 252K |

Market Morning Briefing: Dollar Index Has Moved Up

STOCKS

Dow (25283.00, -0.05%) was quiet yesterday with not much of movement. There is scope of further rise towards 25400-25600 before a corrective dip or sideways consolidation is seen. Overall the index looks bullish.

Dax (13367.78, +0.36%) closed just below resistance at 13400 and while that holds, the index could probably pause for sometime before attempting to move higher. Failure to pause just now could take it higher towards 13600-13800 in the next couple of weeks.

Nikkei (23843.70, +0.54%) saw a dip as the resistance near 113.50 produced a rejection on the Dollar Yen. Weekly resistance is visible near 24000 and that could be tested before a sharp correction sets in.

Shanghai (3412.37, +0.08%) is eventually moving up and could test 3450. Near term looks bullish.

Nifty (10623.60, +0.61%) could face rejection from levels near 10750-10800 which could push it back towards10400 while Sensex (34352.79, +0.58%) is likely to come off from 34500-34650 while above 34200 levels.

COMMODITIES

Gold (1319.11) is in a pause mode after rallying from levels near 1240 in Dec’17. A small pause is possible with a maximum extension towards 1300 on the downside before another leg of rally sets in. Medium term looks bullish.

Brent (68.22) and WTI (62.25) have both moved up quite a bit. As mentioned yesterday, Brent could test immediate resistance near 70 on the upside while WTI could test 63 in the next few sessions.

Copper (3.2330) has come off further and is likely to move down towards 3.20-3.15 in the coming sessions. Near term looks bearish.

FOREX

Dollar Index (92.267) has moved up and seems to be on course to test 92.5-92.75, seen as near term resistance on 3 day candles and 3 day line charts. Simultaneously, we saw Euro (1.1971) break below 1.20, which could now move down towards crucial support near 1.19-1.195 (seen on 3 day and weekly candles) as the Dollar Index moves towards 92.5-92.75.

Dollar-Yen (112.58) as per expectations has seen a dip from resistance level near 113-113.25 and might now test support at 112.50 on the daily candles. This could prove to be a crucial support, which would see a break if Dollar Index goes back to levels below 92.

The Pound (1.3579) is continuing its trade in the narrow range of 1.35-1.36 and we might have to wait for a couple of sessions to get further directional clarity.

Aussie (0.7858) is pausing in its uprise beyond the 200 day moving average on the weekly line charts and should be ranged between 0.78-0.786 for the next couple of sessions.

Dollar-Rupee (63.5050) rose yesterday on back of Dollar strength against the Euro and might see trade within 63.40-63.60 today, with 63.20 acting as a strong support.

INTEREST RATES

The US 10Yr (2.4836%), US 5 Yr (2.2886%) and US 30 Yr (2.8136%) haven’t seen much movement yet. We can expect minimal movement in US yields till the CPI data release on 12th Jan. In case, the data reflects higher inflation due to the recent rise in crude prices, we could see the 5 Yr move past resistance near 2.3 and the 30 Yr could move closer to resistance near 2.9%-3%.

The German-US 10 Yr Yield Spread (-2.0553%) has fallen since yesterday and instead of moving up towards -2%, it could first test support near -2.06%—2.07%.

Japanese 10 Yr Yield (0.068%) has been rising in the last few days, having broken resistance near 0.06% on the short term charts and is now around long term resistance near 0.07%. This has brought the US-Japan 10 Yr yield spread down to 2.4156% and we might see a test of support near 2.36%-2.37% in case the Japanese 10 Yr breaches long term resistance near 0.07%.