Sample Category Title

Top Weighs On Euro

EUR/USD is in danger of forming a double top after the failure at 1.21. The New Zealand dollar was the top performer while the euro lagged. Japan returns from holiday Tuesday. There are currently 7 Premium trades in progress, 4 of which are in profit, 2 in a loss and 1 unchanged.

EUR/USD slid 60 pips to 1.1960 on Monday in a soggy start to the week. The record net long in CFTC positioning was the talk of the trade and surely made a few longs nervous.

The technicals are another reason to worry as a potential double top coincides with the completed inverted Head-&-Shoulder formation along the September high of 1.2092. The weakness emerges despite upbeat eurozone retail sales and business confidence data.

In the US, there was also a dovish hint from Atlanta Fed President Bostic who said he thinks the FOMC should hike 2-3 times this year rather than 3-4 but his comments didn't have an effect on the market.

In terms of economic data, the main headlines emerged from the Bank of Canada's business outlook survey. It showed increasing optimism from businesses and a line from the central bank saying that excess capacity has been absorbed, except in the resource sector.

The report solidified calls for a BOC hike next week, with the probability up to 86%. See Ashraf's detailed piece on the loonie & CAD here. What's also more likely is a hawkish statement and a return to the 'sunny' Stephen Poloz from early in his term. If so, the loonie could continue back down to its 2017 lows.

The S&P 500 rallied for a fifth day to another record at 2747.

Looking ahead, Japan returns from holidays and that will put a renewed focus on the yen. The November report on Japanese labor cash earnings is due at 0000 GMT and forecast to show just a 0.6% y/y rise.

Dollar Bears Got Too Far Over Their Skis

Dollar bears got too far over their skis

The USD dollar has a spring in its step to start the week. But with little to no evidence that the broader US dollar downtrend has run its course, the short-term correction is little more than the recent buildup on EURUSD longs has left dollar bears too far over their skis and vulnerable to a position squeeze given the lack of near-term bullish Euro catalysts.

With no imminent threat from a more aggressive policy shift from US Federal Reserve. Most traders will feel comfortable selling USD dollar rallies but are likely waiting for a more pronounced correction or a stronger signal to re-engage dollar shorts. In the meantime, they’re equally content to take to the sidelines keeping the powder dry but most of all avoiding any early year losses. There is nothing worse than digging oneself out of a hole at the beginning of the year so best to have your ducks in a row before testing the waters.

Oil prices

Protest in Iran, and decreasing US crude inventories are providing a stable floor on WTI. And while the frigid temperatures in the US North East are pressuring heating oil, travel chaos sparked by heavy snows is keeping driver off the roads adding to higher inventories of gasoline which could temper price action. And while speculative positioning is stretched in record territory increasing the potential for a position squeeze, there’s no arguing the trend is your friend in this move. And with geopolitical risk extending from Tehran to Venezuela’s economic demise, the market remains on a bullish tack.

Gold

Gold prices edged a bit lower overnight after the US dollar took back some lost ground from the EUR.But as the USD mini-correction ran out of steam, gold prices quickly retraced earlier loses. Given the very tight current correlation between Gold and USD coupled with relatively sparse news flow, bullion dealers will be keying on Fed speak to provide a catalyst for the dollar ahead of Friday key US CPI, but so far the Fed rhetoric as contributed few sparks.

Equity Markets

With absolutely no threat from the US Federal Reserve who is guiding the market to a well-telegraphed three rate hikes this year and the ECB ambling into an equally well-telegraphed temperate monetary policy for 2018, equity investors continue to enjoy the relative calm exuded by centeral banks.

And with earning season brings renewed optimism, but in the absence of any significant news flow overnight investors sat idle, but none the less the S&P managed to eke out a small gain despite US 10-year Treasury yield sticky around the 2.48% level.

G-10

The Euro

The latest IMM data suggests speculators increased their largest EUR long position since October 2013. And with the Euro falling to take out 2017 highs after the weaker NFP there been a bit of a clear out of weaker longs this week. But market positioning is still substantial, and the dollar bears are playing more of a tactical game early in the week and not showing a competitive bias to accumulate EURO. Also, the Euro rate curve is taking a pause this week after the EONIA curve steepened last week when the market started repricing ECB risk more aggressively.

The Japanese Yen

There’s a disconnect between USDJPY and broader US dollar trend that’s likely a result of EURJPY steering the JPY ship these days. And with the Euro in consolidation mode, it looks like we’re stuck in the range bound malaise.

Looking for a medium-term trade on USDJPY is like sitting on a razor’s edge. We know JPY could weaken given the favourable global risk conditions and rising global yields. But the vast unknown remains the hawkish tail risks to the speed of the BoJ’s “stealth taper”, which in turn could accelerate repatriation into Japan.

Australian Dollar

The broader commodity space continues to look medium term bullish especially oil and hard commodities on the back of the stronger global growth narrative. This period of consolidation should not be confused with anything other than just that. However, commodity block traders are pilling their risk into the Canadain Dollar in the wake of last week stupendous employment data and a probable Bank of Canada rate hike later this month.The speculative rotation is taking a bit of focus away from the Antipodeans early this week.

Via Reuters AUSTRALIA’S MINING INDEX HITS NEAR 5-YR HIGH AS IRON ORE PRICES RISE –

The Chinese Yaun

Despite the mini-dollar correction yesterday the overtones from the mainland suggest regulators are determined to accelerate Yuan exchange rate reform after a two-year hiatus. Given the probable inclusion of CGB’s in Global Bond Indexes later in 2018, the Yuan is likely to keep strengthening through the first part of the year.

Asia FX

While there’s tangible evidence that trends tend to reverse in January on their volition, however unofficial jawboning from an unnamed Korean official was enough to upset the $ Asia apple cart yesterday

The Korean Won

After breaking the critical USDKRW 1060 level driven exporter and foreign fast money flow, vague rumours of intervention chatter started to circulate sending the quick money types into a tizzy posting the USDKRW 1% higher. If recent history tells us anything about verbal intervention is that it’s entirely ineffective in reversing or slowing down domestic currency appreciation

None the less, it spooked the $Asia complex on the assumption that other regional central banks will be just as vigilant against currency appreciation, when in fact nothing could be further from the truth.

With diplomacy between North Korea and South Korea on tap today, the easing of regional tensions could play favourably into the Won and regional currency sentiment today.

The Malaysia Ringgit

The Ringgit held its ground overnight as unlike the BOK the BNM has indicated that they welcome a stronger currency to fend off inflationary pressure . Mind you the Ringgit remains relatively undervalued on a trade-weighted basis.

However, the broader picture remains favourable for further Ringgit appreciation in the lead up to the BNM policy decision later in the month especially in the backdrop of a soft dollar trend and surging Oil prices.

The Philippines Peso

The Philippines Peso suffered a LIFO event after most of the regional currency sentiment wilted on the intervention chatter. The PHP was in the process of playing catch up to region peers ( Last In) but took the biggest hit ( First Out) on the regional currency wobble.

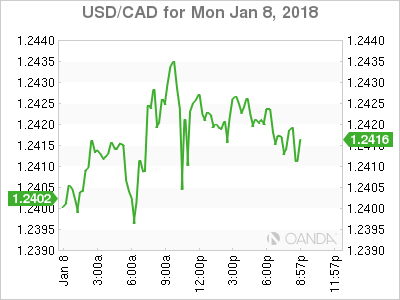

USD/CAD Canadian Dollar Flat As BoC Ponders January Rate Hike

The Canadian dollar was slightly lower agains the US dollar at the start of the week. The loonie is up 1.17 percent versus the greenback so far in 2018. The American currency has not had the best of starts this year. The tax reform and December interest rate hike by the Fed had already been priced in and investors are looking ahead to a highly political year for the USD. Canadian employment was a huge surprise to the upside with another massive job gain. The number of jobs added to the economy in December was 78,600 much higher than the forecasted 1,000. The monster gain has prompted Canadian financial institutions to update their forecasts for the January policy meeting of the BoC with the majority expecting a rate hike. The loonie continued rising after the slow start to the year of the US and the boost from higher oil prices.

The fate of NAFTA remains a possible threat to the CAD, but today’s release of the Bank of Canada (BoC) Business survey shows that companies are not suffering extra anxiety in their outlook. The BoC hiked twice in 2017 before a slowdown in the economy forced the central bank to adopt a more neutral tone. Governor Poloz ended the year with a speech focusing on the topics that kept him up at night but the solid December jobs report and the BoC Survey have all but convinced the market that a rate hike will be announced on the January 17 central bank meeting. Societe Generale is forecasting a price level of 1.2050 or lower if the Bank of Canada (BoC) goes ahead with life of the interest rate to 1.25 percent next week.

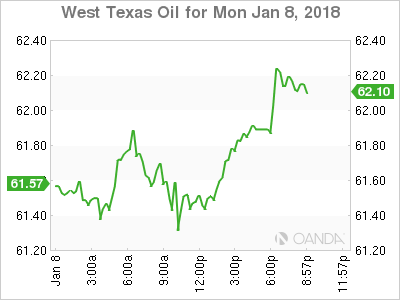

Oil is still near 2015 highs but as supply disruptions or geopolitical risks remain investors are looking at higher production from US producers starting to ramp up. The Organization of the Petroleum Exporting Countries (OPEC) deal to cut production enlisted major producers, but those not included could be the biggest winners if prices remain in current levels.

The USD/CAD rose 0.09 percent on Monday. The currency pair is trading at 1.2422 as the USD seeks to regain traction after a disappointing U.S. non farm payrolls (NFP) report on Friday, January 5 and a monster number of jobs gain in Canada on the same day. The near 80,000 added jobs convinced major institutions to change their forecast for the January 17 central bank meeting. A 25 basis points has been forecasted by most major banks with Royal Bank of Canada being one of the outliers who does expect higher rates, but later in the year. The BoC is expected to lift rates 2 or 3 times this year, the same as the U.S. Federal Reserve. The Canadian central bank has been aware of the high level of household debt but improving economic indicators could hasten the monetary policy decision.

West Texas Intermediate is trading at 61.87. The price of crude remains high as political tension in Iran and the North Sea pipeline maintenance work continues. Drilling has not been particularly strong in the US but that is expected to change soon as weather improves and shale operations could ramp up at a higher rate explaining the lack of new oil rigs.

Geopolitical risk in the oil market has been high as various members of the Organization of the Petroleum Exporting Countries (OPEC) are facing political headwinds. The big three: Saudi Arabia, Iraq and Iran have all experienced different forms of uncertainty as leadership has either changed or had to respond to different challenges. The relationship between them has also been frayed which could put into question how effective the OPEC’s production cut agreement will remain in place, or even the organization if there is a major disagreement between its biggest producers.

Market events to watch this week:

Wednesday, January 10

4:30am GBP Manufacturing Production m/m

10:30am USD Crude Oil Inventories

7:30pm AUD Retail Sales m/m

Thursday, January 11

8:30am USD PPI m/m

8:30am USD Unemployment Claims

Friday, January 12

8:30am USD CPI m/m

8:30am USD Core CPI m/m

8:30am USD Core Retail Sales m/m

8:30am USD Retail Sales m/m

Gold Rally Takes Pause As Investors Look For Cues

After another week of gains, gold is trading quietly in the Monday session. In North American trade, the spot price for an ounce of gold is $1319.03, down 0.07% on the day. On the release front, it’s a quiet start to the trading week, with no major US releases.

On Friday, the US posted mixed employment numbers. Nonfarm Payrolls dropped to 148 thousand, down from 228 thousand in the previous release. This was well below the estimate of 190 thousand. There was better news from wage growth, which edged up to 0.3%, matching the forecast. This marked a 3-month high. The unemployment rate remained unchanged, at a sizzling 4.1%.

Gold prices continue to head higher, as the metal rolled off a fourth straight winning week. Gold has jumped an impressive 5.5% since December 11, despite a strong US economy and a December rate hike from the Federal Reserve. On Friday, gold touched a high of $1326, its highest level since mid-September. Risk appetite on the part of investors remains high, but for now, this has not dampened enthusiasm for gold. With the US dollar showing broad losses in recent days, gold could continue to rally.

Another Quarter of Solid Sentiment from Canadian Firms

Sentiment among Canadian firms remained positive during the final quarter of 2018, according the Bank of Canada's quarterly Business Outlook Survey (BOS).

The 'headline' indicator of the balance of firm opinion on future sales ticked down a notch (to 19% on balance, from 31% previously), but remained in positive territory. The broader-based indicator of future sales, which summarizes order books, advance bookings, sales inquiries and similar information, also ticked down slightly, but at 55% still marked its third highest reading on record (last quarter saw the second highest reading). Firms cited increased competition, notably in the retail sector as dampening the sales outlook.

On the investment and hiring front, it was a positive story. The balance of opinion on investment intentions rose to 29% as the share of firms planning to reduce investment fell. It is important to remember that these questions are relative to the past 12 months, which have seen a healthy recovery of investment activity, making today's figures more impressive. A similar improvement was seen in hiring plans, where the balance of intentions ticked up to +40%. Hiring intentions were reportedly driven by the service sector, and by firms located in Central Canada. Firms also reported anticipating more difficulty meeting an unexpected increase in demand, with labour shortages more widely reported than in the previous survey.

On the price front, firms are now expecting an increase in the pace of input cost growth, on balance, but expect competition to limit their ability to pass these costs on (the balance of opinion on output prices was 0%). Inflation expectations remain well within the control range, but the share of firms expecting inflation over the next two years to fall into the 2% to 3% range climbed 14 percentage points.

Senior Loan Officer Survey

Released alongside the BOS, the Senior Loan Officer Survey indicated that lending conditions eased slightly as spreads on lending to corporate borrowers narrowed. This ended a five quarter run of effectively unchanged lending conditions. It was also reported that both price and non-price conditions eased in the Prairies as activity in the resource sector continued to increase. On the other side of the coin, demand for credit reportedly rose after a flat reading in the prior survey.

Key Implications

This was a solid report. Headline sales expectations may have ticked down a hair, but overall sentiment remains robust. This is best captured by the Bank of Canada's summary measure (The "BOS indicator"), which rose to within a hair of its 2017Q2 reading (which presaged last year's back-to-back rate hikes).

Reinforcing the strength, while the spectre of a poor outcome from NAFTA renegotiations continues to hang over business leaders, healthy US demand and a supportive loonie were also reported as supporting the business outlook.

Particularly interesting in the current context, additional focus was given to wage pressures. Pressure is now seen as positive in all regions, and while minimum wage changes may be driving the gain in some areas, so too are healthy labour markets that are leading to reported challenges in recruiting and retaining staff.

When the wage outlook and its underlying drivers are taken together with the tick-up in investment intentions and the healthy outlook for hiring (even more impressive in light of the recent string of strong jobs numbers), the picture that emerges is one of economic strength. Today's report should thus provide Bank of Canada Governor Stephen Poloz with further confidence that emergency level interest rates are no longer needed, with the next policy interest rate increase to come next week (January 17th)

BoC’s Business Outlook Survey Firms Up Expectations for a Rate Hike Next Week

Highlights:

- The BOS indicator, which summarizes the main survey questions, rebounded close to the peak seen in the summer survey—which was a major factor in the BoC raising rates last July.

- The balance of opinion on future sales moderated following "unsustainable" strength in the first half of 2017. Still, firms expect an acceleration in export growth.

- Investment intentions rebounded as firming capacity pressures helped offset "tax and regulatory hurdles" as well as uncertainty over US trade policy.

- The share of firms that would have difficulties meeting an unexpected increase in demand hit its highest level in a decade. Labour shortages also became more common.

- Inflation expectations were little changed with a slight majority of respondents still expecting inflation to be in the lower half of the BoC's 1-3% target range.

Our Take:

We think last Friday's impressive employment report tipped the scales in favour of a January rate hike, and today's release of the Business Outlook Survey gives further weight to that view. This survey has become a key input in the Bank of Canada's policy deliberations, and signs that "positive business sentiment is widespread" give the central bank the all clear to raise interest rates next Wednesday. Importantly, capacity pressures continued to firm and businesses are responding by boosting investment and hiring, even amid concerns about US trade policy. Not all indicators point to an urgent need to raise rates—wage pressures increased but still aren't widespread and upward pressure on output prices is being offset somewhat by structural factors like e-commerce—but overall it is increasingly clear that Canada's economy doesn't need the amount of monetary policy stimulus currently being provided.

Global Economic Themes for 2018

Although 2017 started on a more upbeat note than 2016, few forecasters expected the positive surprises that the year had in store. Economic momentum proved to be stronger and persistent, particularly within G7 countries. A typically weak (residual-seasonality distorted) first quarter in the U.S. quickly gave way to sustained, above-trend growth thereafter. A virtuous global cycle finally kicked in, feeding into trade volumes and many emerging market economies.

More of the same is on the docket for 2018. We anticipate the global economy to grow by 3.8%, slightly firmer than the 3.7% pace from last year. Indeed, many of the same themes will act to support global economic activity. Advanced economies will remain fairly hot, with emerging markets gaining speed. Although monetary stimulus should continue to wane, there is no question that conditions will still be highly accommodative by historical standards. Labor markets will tighten further, but a rapid uptick in wage and price pressures is unlikely. In fact, this is a key pillar supporting the view of many analysts that monetary stimulus will be removed at a gradual pace. Any shift in this market perception or actual data can quickly become a game changer for central bankers and bond yields in 2018.

The year has barely started and an "everything-is-awesome" sentiment dominates the outlook. The global financial crisis, the euro debt crisis and the commodity price shock are all now largely in the rear view mirror. However, the true test of global health will be how economies adjust to less central bank stimulus after nearly a decade of priming the pump in favor of asset prices. And, this year will also give analysts a good look at how much politics will run interference with the international movement of goods and people.

We've identified six themes that we believe will shape the economic narrative for 2018:

Theme #1: Global Reflation

In a note last fall, we highlighted a number of factors that may explain why inflation in G7 economies has been subdued despite strong economic growth and the rapid absorption of slack. Our empirical analysis showed that the link between economic slack and inflation still holds, but has weakened during the current cycle. However, weakened does not correspond to dead. It's just a matter of time before wage and price pressures respond to ever-tightening capacity conditions. Some signs are already evident in Canada and Europe, and various reports within the U.S. are reinforcing increasing wage pressures within the higher skilled segments of the labor force (Chart 1). With unemployment rates in advanced economies set to continue to plummet below historical norms, the laws of supply and demand favor increased wage-competition as labor becomes scarcer.

As with all economic forecasts, nothing is written in stone. But, a virtuous growth-cycle on a global scale does tilt the balance of risks more in favor to the upside for inflation, rather than downside. Certainly adding to this risk (and current reality) is that elevated geopolitical risks drive energy prices higher, pushing headline inflation up.

However, some aspects cannot yet be fully reconciled within forecast models, such as what's referred to as the "Amazonization" of prices, as well as the inherent imprecision that surrounds the calculation of output gaps and equilibrium interest rates across countries. We may find that inflation-targeting central banks will be more inclined to run their economies a little hotter than necessary, rather than risk tightening financial conditions too fast and ending the expansion prematurely.

Theme #2: Rising global interest rates

G7 central banks are on track to continue along the path of gradually removing stimulus. The Federal Reserve will have good company in raising its main policy rate by at least another 50bps, with both the Bank of England and the Bank of Canada each expected to follow suit with 25 bps and 50 bps hikes, respectively (Chart 2). Not to be left out, the European Central Bank has reduced its monthly asset purchases to €30 billion, and will likely cease altogether by year-end. This will leave Japan as the only G7 central bank continuing with a monthly asset purchase program through the end of 2018, and likely into 2019 as well.

With central bank demand for bond-related purchases set to shrink, this may have knock-on effects to asset prices more broadly. There is the general sense that a decade of low interest rates has instilled a sense of complacency in investors, evidenced by ultra-low volatility in global stock and bond markets despite elevated policy uncertainty and geopolitical risks (Charts 3 and 4). It would not be unusual to see rising interest rates trigger bouts of financial market volatility in the coming months.

Historically, higher borrowing costs have triggered a selloff in asset markets. This suggests that the pace of wealth creation from asset price appreciation could slow or cease altogether as interest rates rise further and central banks withdraw from adding assets to their balance sheet. A surgical skill will be required of central banks to maintain credible communication, ensuring that balance sheet normalization be a boring process.

Of course, rising borrowing costs implies that servicing debt becomes more burdensome for borrowers. As such, higher rates should cool demand for housing, while also making highly speculative assets, such as high-yield debt and cryptocurrencies, less attractive to investors. Overall, we anticipate that the gradual pace of policy normalization is likely to do what policymakers intend: temper house price growth, slow asset price growth, and keep consumer spending and debt in check.

Theme #3: Elevated debt levels

Given the forthcoming rise in debt service costs, there are concerns regarding the elevated levels of debt in G7 and emerging market economies. Within a global context, all sectors of the economy - households, firms, and government - have added leverage over the past decade. In its November update, the OECD provided an in-depth analysis of this rapid uptake in global debt. For businesses, the rise in debt is largely a consequence of the low cost of capital that resulted from monetary policy actions. However, increased leverage in household and government sectors is a little more difficult to unwind. Corporations have the option to switch to equity issuance and pay off debt. This amounts to reversing course of what has been years of financial engineering to minimize financing costs. This action poses relatively little economic risk, barring a sustained, adverse reaction by investors.

In contrast, although governments have the option of extracting more revenue from their tax base or cutting back expenditures, these are all options that tend to exert a drag on economic activity now, or in the future.

Conversely, households are most likely to have a difficult time adjusting to higher interest rates. Those economies that have high household leverage relative to incomes - like Canada and the UK - are now more interest-rate sensitive. Chart 5: Most Households Have Tough Time Recovering From Wealth Stocks In contrast, American households were one of the few to experience a true deleveraging cycle in the past decade. But, these same households have only recently been able to taste the fruit of their labor with a recovery in wealth across income categories (Chart 5). What's more, most of the wealth-gains have been captured by higher income individuals, which still leaves many American households price-sensitive to movements in interest rates and income. Let's also not gloss over the fact that this economic cycle is long-in-the-tooth, particularly in North America. This does leave economies more susceptible to debt fatigue, policy errors, and asset re-pricing risks that can suddenly exacerbate debt conditions within the various segments of the economy.

Looking ahead, it's extremely difficult to forecast how each sector will respond to higher interest rates in G7 economies. But, in the absence of an unanticipated shock, 2018 is unlikely to be the year that a major deleveraging episode occurs in Canada, the U.S., Europe or Japan. Persistent above-trend income growth is a positive sign and the baseline view is that a gradual rise in interest rates shouldn't see debt service costs become too onerous. Instead, this is probably the year when the appetite for corporate debt finally slows after a decade long feast. The response of governments and households remains to be seen.

Theme #4: Productivity growth ticking up

Strong economic growth over the last six quarters in G7 economies has partly reflected firming productivity gains (Chart 6). That is, the economy grew more than the amount of extra output resulting from the increased usage of labor and capital. Moreover, this recent uptick in productivity growth raises questions about existing trend estimates of its past and future path.

Labor productivity growth can be decomposed into the contribution from capital deepening (change in the additional investment in capital per unit of labor), and from total factor productivity. The post-crisis slump in productivity has been blamed on slower growth in both components. Indeed, slower business investment growth was puzzling especially in a historically low interest rate climate. Together with weak demand, the uncertain business climate after the Great Recession drove firms to prefer to return cash to shareholders instead of investing in their business. Less certain is why total factor productivity growth slumped. The most popular theory comes from Professor Robert Gordon, who theorizes that past waves of innovation have fully passed-through to the economy, leaving smaller influences stemming from the recent pace of innovation.1

Although it's still early days, the recent uptick in productivity growth, if it persists, may be a sign of a turning tide. Business investment globally has been ticking up in response to persistence of highly accommodative financial conditions and stronger demand. Although more difficult to assess, firmer productivity growth may also reflect a rebound in total factor productivity growth.

What's more, one of the greatest economic experiments is about to get underway. Will the massive, sudden drop in the U.S. corporate tax rate, combined with temporary full-expensing of capital investment, unleash the investment-beast in America? Economists say "no" to the beast, but "yes" to the jackrabbit. However, with investment momentum already accelerating last year, it will be difficult to fully untangle the sources of influences. Country comparisons will be useful in gauging impacts as we go forward.

Why does this matter? Trend estimates of productivity growth and its components feed directly into estimates of potential output. The estimated gap between actual and potential economic output helps policymakers assess how much slack exists within the economy, ultimately determining the speed and level of interest rate adjustments. So, if productivity growth is indeed heating up in G7 economies, central banks will have to reassess how much economic slack remains, potentially altering the pace of policy normalization.

Theme #5: Election outcomes

Elections and referendum results at times have become detached from polls in recent years. Markets were surprised by the UK vote to leave the EU, and the election of Donald Trump as President of the United States. With U.S. mid-term elections and general elections in parts of Europe this year, politics may once again shape market knee-jerk responses and economic outcomes.

Indeed, the U.S. economy performed very well last year, averaging just under 3.0% growth over the past three quarters. Moreover, the unemployment rate has plunged to a seventeen year low, with job gains likely to remain reasonably strong through at least the first half of 2018. Now that tax changes are a done deal, political focus will shift to NAFTA negotiations, immigration reform, repairing or replacing the Affordable Care Act, and maybe even an infrastructure plan. With mid-term elections this November, the Republican majority House would like to see progress in at least one of these areas before voters head to the polls. But, with a paper-thin Republican majority Senate at stake, posturing for mid-term elections and any shift in composition thereafter could deal a blow to the ability for the U.S. administration to implement other long-lasting economic reforms over the remainder of its term.

Similarly, European economies outperformed expectations last year, as economic activity in the Euro Area expanded at a pace almost double trend estimates. Moreover, the outlook for Europe remains largely positive. There are good indications that momentum is carrying into the first half of this year and unemployment rates should continue to plummet, even in the periphery which is still in recovery mode.

Simply put, all signs point to a region that has moved beyond past economic crises. However, the outlook is not all roses. Anti-establishment political movements are likely to continue to cast a long shadow this year, threatening the stability of the euro and the European Union. Although the populist threat to core economies largely fizzled following electoral victories last year by more centrist candidates in the Netherlands and France, the election of the young, anti-migrant Austrian Prime Minister Sebastian Kurz and the entrance into parliament of the nationalist AfD party in Germany prove that anti-establishment policies remain attractive to voters.

Italians are first to head to the polls this year, with parliamentary elections scheduled for March. Although the anti-euro/EU M5S party is favored to win, currently polling at 27% of the popular vote, they are still far short of a majority. Moreover, recent electoral changes in Italy and M5S's refusal to negotiate a coalition reduce the chance that M5S will be able to form a government. However, an outcome that proves otherwise could be disruptive to market sentiment.

Flying somewhat below the radar are forthcoming elections in Eastern Europe. Hungary, Czech Republic, and Poland have all been vocal about EU immigration policies, or the lack thereof, and the current brand of soft Eurosceptic leadership is likely to remain after elections later this year. Although Poland isn't going to the polls, its dispute with European authorities regarding judicial changes that violate European laws resulted in a ruling last month which opens the door for the EU to impose sanctions on Poland until it returns independence to its judiciary. Initial sanctions are likely to include suspending Poland's ability to vote on EU articles. How the EU handles Poland could have implications for upcoming elections.

Theme #6: Brexit, NAFTA, and geopolitical risks

Lastly, there are several overarching themes carrying over from last year that will intensify this year. The timeframe for Brexit negotiation and resolution will be shortening with each passing month. Although Phase 1 negotiations that largely dealt with Brexit costs wrapped up last month, Phase 2 is really where the rubber hits the road. Critically, negotiations this year will entail compromises by both the UK and the EU-27 in order to establish the necessary framework to avoid a hard Brexit in March 2019.

Other trade negotiations will also garner critical market attention. NAFTA renegotiations will continue behind closed doors probably (at least) through the first quarter of this year. Material changes could have substantial negative implications for the economies of Mexico and Canada. For example, if the U.S. were to pull out of NAFTA entirely, we estimate that a return to WTO trading rules could shave about 0.7% off of the level of our baseline view for economic activity in Canada within the first year. Although macroeconomic estimates of the impact on U.S. activity are much smaller, the indirect impacts both to the U.S. economy and global supply chains will be largely unobservable until after a complete withdrawal from NAFTA occurs. In addition, the U.S. would not be able to skirt a negative financial market reaction on a NAFTA withdrawal or changes that are materially unfavorable to the states/industries that have high growth-reliance on Canada and Mexico.

As U.S. interest in trade liberalization has waned, the rest of the world will continue to work to build closer relationships this year. The Trans Pacific Partnership (TPP) will remain in the headlines, as more countries, including Canada, seek to join New Zealand and Japan by having the agreement ratified by their parliaments. China will also drive harder on building inroads on more new free trade agreements (FTAs), seeking to add an additional eleven to its current roster of seventeen over the next few years.2

Outside of trade packs, North Korea will likely remain as the most pertinent geopolitical risk. Thus far, North Korea's leadership has been reluctant to negotiate terms to abandon its nuclear weapons research and stockpile. Moreover, there is little comfort that the situation can deescalate while North Korea continues to fire ballistic missiles near its neighbors and conducts nuclear tests. Financial markets are betting that a large political misstep doesn't occur that causes a stumble into conventional or nuclear war.

The Case for Higher Interest Rates in 2018: The Fundamentals

Day-to-day, countless factors drive gyrations in the Treasury market. The key fundamentals, however, drive the underlying trend, and we believe these factors are poised to drive U.S. Treasury yields higher in 2018.

Fundamental #1: Economic Growth and Inflation

The case for higher U.S. Treasury yields in the United States in 2018 starts with the most basic of fundamentals: economic growth and inflation. When the 10-year U.S. Treasury yield reached a cycle low of 1.36 percent in the summer of 2016, it occurred at a time of global tumult related to the Brexit vote, but the underlying fundamentals of both U.S. economic growth and inflation were also very soft (top chart). Real GDP growth was a paltry 1.5 percent in 2016, and the PCE deflator rose just 1.2 percent over the same period. In 2017, real GDP accelerated to roughly a 2.3 percent pace, while inflation as measured by the PCE deflator strengthened to 1.7 percent.

Faster economic growth/inflation has pushed nominal GDP growth back to a 4 percent year-over-year pace, and we expect the upward trend to continue in 2018. We expect real GDP growth of 2.7 percent this year and for inflation to drift closer to the Fed's 2 percent target. A continued acceleration in GDP and prices suggests these two key fundamentals will be supportive of higher yields on U.S. Treasuries this year.

Fundamental #2: Monetary Policy

With faster growth/inflation and a falling unemployment rate, the FOMC is positioned to hike the fed funds rates multiple times for the second year in a row. We expect three rates hikes this year, occurring in March, June and September. If realized, this would put the fed funds target range at 2.00-2.25 percent by year end. The FOMC dot plot suggests a neutral rate of 2.50-2.75 percent, signaling that another year of three rate hikes would put the Fed within spitting distance of a "normal" stance of monetary policy, at least in regard to the fed funds rate.

With regards to the Fed's balance sheet, monetary policy remains more accommodative, but here too the fundamentals suggest upward pressure on Treasury yields. The balance sheet reduction program initiated last October will see the run-off caps rise to $50 billion/month in Q4-2018 for Treasuries and MBS. If the Fed follows its stated plan, approximately $230 billion in Treasury debt would mature and not be reinvested in 2018 (middle chart). Steady increases in the fed funds rate and snowballing balance sheet reductions suggest an upward shift for the yield curve in 2018.

Fundamental #3: Treasury Supply

After steadily failing through FY 2015, the federal budget deficit has begun to rise again (bottom chart). As a result, the supply side of the Treasury market will see a surge of new issuance due to several factors: secular pressures related to the aging Baby Boom generation, additional spending from an expected budget deal and for hurricane/wildfire related emergencies and lower tax collections as a result of the tax overhaul bill passed in December. A jump in net issuance represents an additional catalyst for higher Treasury yields in 2018.

Yen Subdued After Dollar Gains

USD/JPY is showing little movement in the Monday session. In North American trade, USD/JPY is trading at 113.00, down 0.06% on the day. On the release front, there are no major US or Japanese events. On Tuesday, the US releases JOLTS Jobs Openings.

On Friday, the US posted mixed employment numbers. Nonfarm Payrolls dropped to 148 thousand, down from 228 thousand in the previous release. This was well below the estimate of 190 thousand. There was better news from wage growth, which edged up to 0.3%, matching the forecast. This marked a 3-month high. The unemployment rate remained unchanged, at a sizzling 4.1%.

As we begin the New Year, what can investors expect from the Bank of Japan? BoJ Governor Haruhiko Kuroda has generally stuck to his script that the Bank will maintain its massive stimulus program until inflation rises, but there have been subtle hints form Kuroda that he could change course, if the economic rebound which marked 2017 continues. The stimulus program has failed to lift inflation above 1%, well below the BoJ inflation target of around 2%. Some analysts expect a 'stealth tapering', whereby the BoJ would reduce asset purchases and tighten policy, but in small, incremental steps. In this way, the BoJ could change its monetary stance, while minimizing market volatility.

Bank of Japan Governor Haruhiko Kuroda is slated to end his 5-year term in April, but will he be staying on? The Japanese government hasn't made up its mind, and Prime Minister Shinzo Abe said as much on Sunday. Abe said that Kuroda has met his expectations, but admitted that he had not made up his mind about the reappointment. With Japan posting seven straight quarters of growth and inflation moving higher, there's a strong likelihood that Kuroda will be given the green light for another term at the helm of the central bank.

Slew of Fed Speakers Have the Capacity to Affect Dollar Positioning

The dollar is in recovery mode on Monday after falling on Friday, recording its lowest since January 2 versus a basket of currencies and coming close to hitting a fresh 3½-month low. Dollar selling took place in the aftermath of December's jobs report which showed the US economy adding notably fewer positions than analysts had expected.

Despite earlier declines, the dollar managed to recover, finishing Friday's trading higher, albeit only slightly so. Dollar bulls eventually taking control was attributed to the fact that last week's NFP report doesn't seem to be changing perceptions among Fed policymakers, with markets continuing to in large part – more than 60% at the moment according to CME futures – pricing in a rate hike during the Federal Reserve's March meeting. Remarks by Fed policymakers late last week also played their role, with positive momentum for the US currency carrying through Monday's trading, as comments by FOMC policymakers were broadly tilted towards the hawkish side. The dollar index is trading in the green during Monday's trading and at a distance to Friday's low, touching 92.36 at its highest, a level last experienced on December 29.

In a Reuters interview over the weekend, San Francisco Fed President John Williams said that the US central bank should raise interest rates three times this year – as projected in December's dot plot – making reference to an already strong economy that will receive a boost from lower taxes and leaving the door open for more hikes (but less tightening as well) depending on economic conditions. John Williams is a hawkish-perceived FOMC member that is holding voting rights in 2018. Later on Monday – at 1835 GMT – he is scheduled to participate in a panel discussion titled "The Options: Keep it, Tweak it, or Replace It" with "It" referring to the Fed's 2% inflation target. Williams' comments will be attracting attention.

Cleveland Fed President Loretta Mester, also an FOMC voting member in 2018, was typically hawkish in her comments late last week, saying she expected four rate hikes in 2018; markets are currently roughly pricing in two 25 bps interest rate hikes in 2018.

Another hawkish-perceived FOMC member, Boston Fed President Eric Rosengren, will be participating in a discussion (2125 GMT) at the same event as John Williams, the topic of which is "Next Steps: Learning from the Bank of Canada". Unlike Williams, Rosengren doesn't hold voting rights in the FOMC in 2018; he will be a voting member next year.

Earlier on Monday – at 1740 GMT – Atlanta Fed President Raphael Bostic will be speaking on the economic outlook and monetary policy before the Rotary Club of Atlanta. Given that Bostic is holding a voting status in 2018 and being viewed as falling neither on the hawkish nor the dovish side of the spectrum, forex market participants will likely be paying attention to his comments.

The dollar ended last week with a three-day advance versus the Japanese currency, its longest streak since the end of November. Should Fed-talk continue to be on the hawkish side, the pair is expected to head higher, especially if one takes into account that the Bank of Japan seems in no hurry to begin normalizing policy, even in light of stronger growth in the world's third largest economy. In such an event, a barrier to the upside is expected around December's 12's two-month high of 113.75. A successful break above it would shift focus to early November's ten-month high of 114.72, with the area around this level encapsulating a few other peaks from the relatively recent past.

On the downside and should the greenback fail to find support from comments by Fed officials, the range around the current level of the 50-day moving average at 112.86 might act as support. Price action is at the moment taking place close to this point, with a breach turning attention to the 112.00 handle, a potential psychological level and an area of congestion in recent weeks.

In a week packed with speeches by FOMC members, Minneapolis Fed President Neel Kashari is scheduled to participate in a Q&A session on Tuesday at 1500 GMT. Him and Chicago Fed President Charles Evans, with the latter participating in a discussion on current economic conditions and monetary policy on Wednesday at 1400 GMT, were the two FOMC members voting against an interest rate increase during the Fed's latest meeting in December. They're both thought of as chief doves by markets and they will importantly be losing their voting rights in 2018, a factor that renders some to speculate on a more hawkish-than-currently-priced-in direction by the Fed.

Other Fed speakers making talks this week are Dallas Fed President Robert Kaplan (centrist-viewed and non-FOMC voting member in 2018), St. Louis Fed President James Bullard (viewed as a dove and holding voting rights in 2019) and New York Fed President William Dudley (centrist-perceived with the New York Fed holding permanent voting rights within the FOMC). A few months ago, Dudley announced that he will be stepping down before his 10-year term at the NY Fed expires in January 2019. Speculation on who will replace him is well underway.

Beyond Fed officials, other catalysts could drive the US currency this week: perhaps most important in terms of releases are Friday's inflation and retail sales figures for the month of December, both due at 1330 GMT. Other data also have the capacity to drive positioning on the dollar, including tomorrow's JOLTS job openings report for the month of November to be made public at 1500 GMT.