Sample Category Title

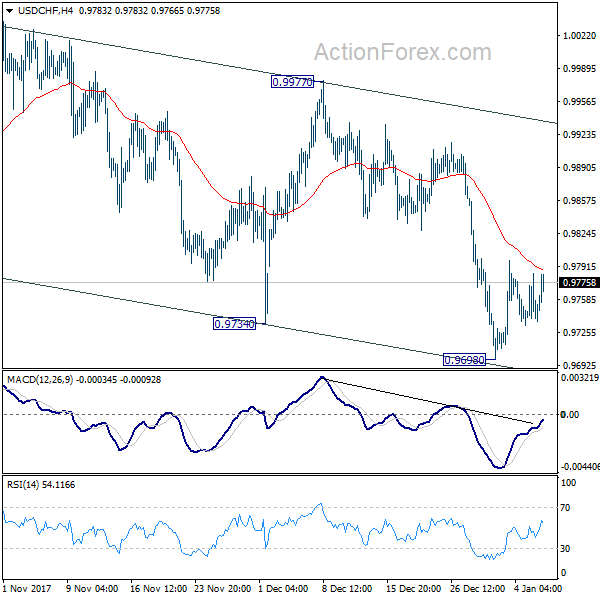

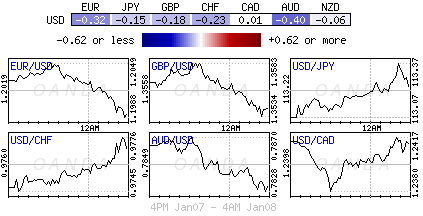

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9723; (P) 0.9753; (R1) 0.9771; More....

Intraday bias in USD/CHF stays neutral first. As long as 4 hour 55 EMA (now at 0.9788) holds, deeper fall is mildly in favor. But we'd expect 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to contain downside and bring rebound. Sustained break of 4 hour 55 EMA will argue that the correction from 1.0037 has completed and turn focus to 0.9977 resistance for confirmation.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

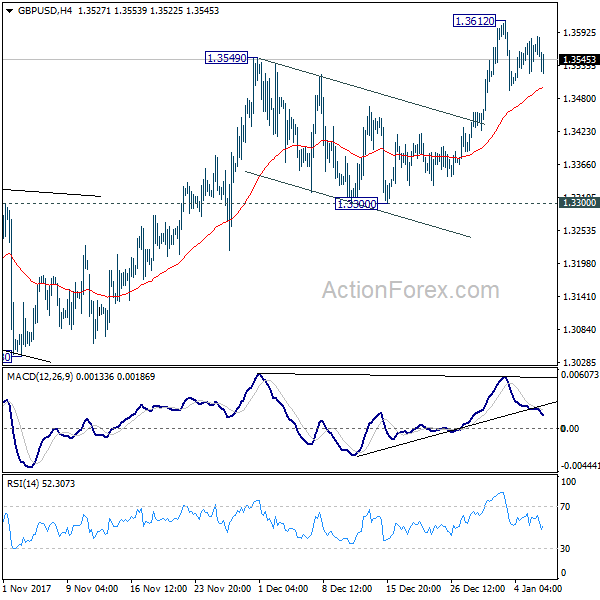

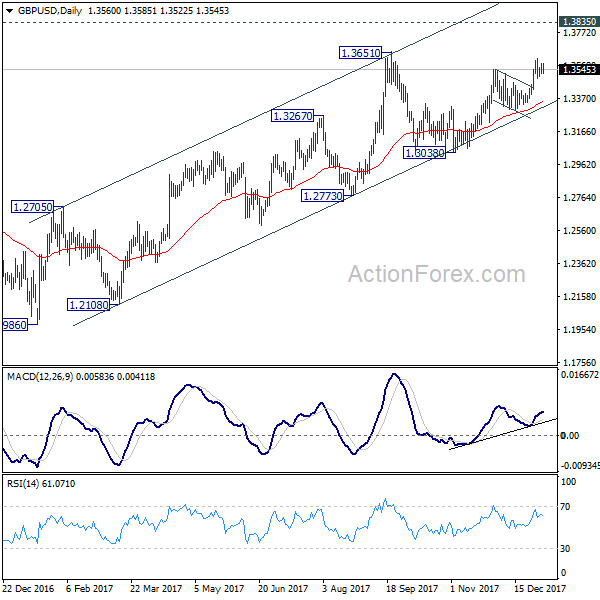

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3528; (P) 1.3555; (R1) 1.3587; More.....

Intraday bias in GBP/USD remains neutral at this point and consolidation from 1.3612 temporary top could extend. But as long as 4 hour 55 EMA (now at 1.3498) holds, further rally is expected. Above 1.3612 will target 1.3651 key resistance first. Break will resume medium term rise from 1.1946 and target key resistance level at 1.3835. However, sustained break of 4 hour 55 EMA will turn focus back to 1.3300 support.

In the bigger picture, the break of long term trend line resistance from 1.7190 (2014 high) is seen as a sign of long term reversal. However, rise from 1.1946 (2016 low) is not impulsive looking. And the pair is limited below 1.3835 key resistance. Hence, we won't turn bullish yet and would continue to monitor the development. On the downside, break of 1.3038 support will now indicate that rebound from 1.1946 has completed and turn outlook bearish. Meanwhile, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

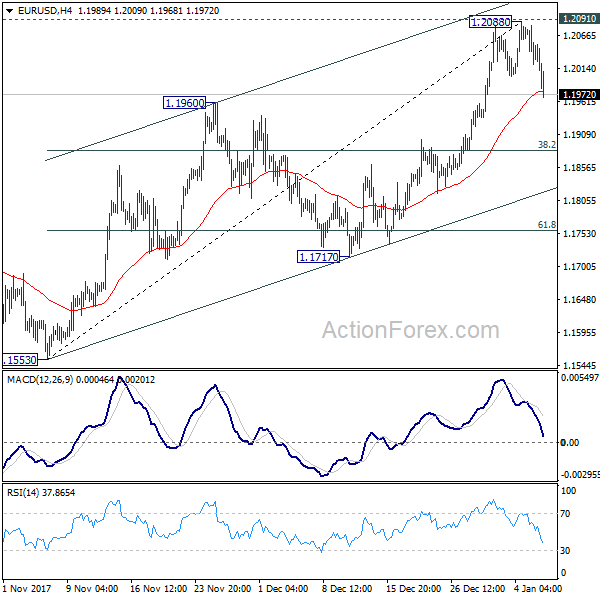

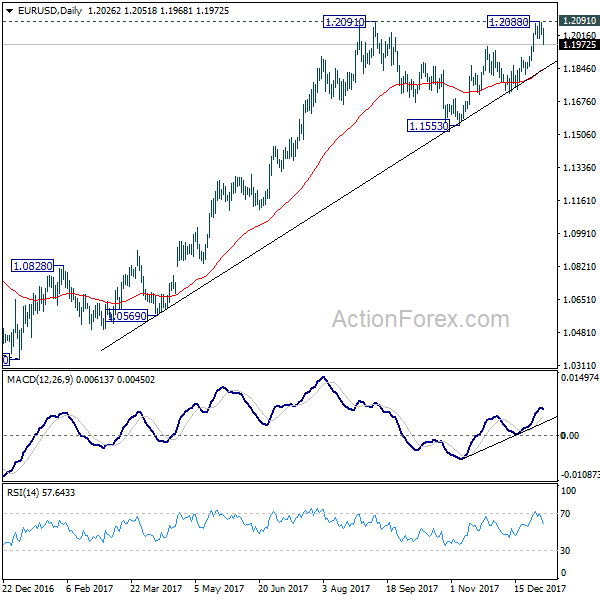

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2006; (P) 1.2044 (R1) 1.2068; More....

EUR/USD's fall from 1.2088 extends lower today. Break of 4 hour 55 EMA argues that it's rejected by 1.2091 key near term resistance. And, such decline could be the third leg of consolidation pattern from 1.2091. Intraday bias is turned to the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break of 1.1884 will target 61.8% retracement at 1.1757 and below. On the upside, firm break of 1.2091 is needed to confirm up trend resumption. Otherwise, we'd expect more corrective trading in near term.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Euro Shrugs off Upbeat Confidence Data, EUR/USD Risks Deeper Pull Back

Despite a string of upbeat confidence data from Eurozone, Euro tumbles broadly today. Weaker than expected German retail sales could be a factor. Some also point to the risks of upcoming election in Italy. But it's seen that the decline in Euro is due to recent loss in momentum, and the failure of EUR/USD to break through 1.2091 key resistance. On the other hand, the greenback is trying to regain some ground, together with the Japanese Yen. BoC business outlook survey is the only economic release in US session. Focus will be on speeches of Fed officials including Atlanta Fed Raphael Bostic and San Francisco Fed John Williams.

Eurozone Sentix had "astonishing" rise

Eurozone Sentix investor confidence rose to 32.9 in January, up from 31.1 and beat expectation of 31.3. Current situation index also hit the highest level in nearly a decade at 48. Sentix said that the rise is in confidence is "astonishing". However, it also warned of "danger of overheating" due to strong global momentum. It noted in the release that "particularly noteworthy is the USA, where investors are noticeably raising expectations. But latecomers such as Eastern Europe and Latin America can also improve considerably. The upswing is strong and increasingly synchronized." For Germany, the current situation index jumped to record high of 72.3, showing that "the economy has not yet missed a new government".

European Commission's economic confidence rose to 116 in December, up from 114.6 and beat expectation of 114.8. That's also the highest level since 2000. Industrial confidence rose to 9.1, up from 8.2, above expectation of 8.4. Services confidence rose to 18.4, up from 16.4, beat expectation of 16.5 Consumer confidence was finalized at 0.5. Business climate rose to 1.66, up from 1.49, beat expectation of 1.50.

Also from Europe, German retail sales dropped -0.4% mom in November. Swiss CPI was unchanged at 0.8% yoy in December.

UK PM May having third cabinet reshuffle

In UK, Prime Minister Theresa May is having her third cabinet reshuffle since becoming PMI back in 2016. This time, it's triggered by sacking of Damian Green as first secretary of state due to sexual harassment. Some key figures are expected to stay, including Brexit Secretary David Davis, Chancellor of Exchequer Philip Hammond and Secretary of State for Foreign Affairs Boris Johnson. Also, it's generally expected May would maintain the balance of anti- and pro-Brexit voices.

Aussie lower as government forecast 20% drop in iron ore price

Australian dollar tumbles today after Department of Industry, Innovation and Science said in the latest commodities outlook paper that iron ore price would drop 20% from 2017. The paper noted that "the iron ore price is expected to experience some ongoing volatility in early 2018, as the market responds to uncertainty regarding the impact of winter production restrictions on iron ore demand." But over the course course, there would be increase in global supply and moderation in demand from China. Iron ore is priced at around USD 75 a ton currently. Price averaged at around USD 64 in 2017. And Australia government expected it to drop to average USD 51.5 in 2018.

North and South Korea to meet tomorrow

In the upcoming Asian session, North Korea and South Korea will be holding their first high-level meeting in more than two years. The main topic of the meeting will be on participation of North Koreans in the Winter Olympic games to be held from February 9 in South Korean city of Pyeongchang. Talks were intiated after North Korea leader Kim Jong-un signaled his "earnestly wish" to participate. There is hope from the South that discussions could extend to topics on improve South-North tie.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2006; (P) 1.2044 (R1) 1.2068; More....

EUR/USD's fall from 1.2088 extends lower today. Break of 4 hour 55 EMA argues that it's rejected by 1.2091 key near term resistance. And, such decline could be the third leg of consolidation pattern from 1.2091. Intraday bias is turned to the downside for 38.2% retracement of 1.1553 to 1.2088 at 1.1884. Break of 1.1884 will target 61.8% retracement at 1.1757 and below. On the upside, firm break of 1.2091 is needed to confirm up trend resumption. Otherwise, we'd expect more corrective trading in near term.

In the bigger picture, rise from 1.0339 medium term bottom is still seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. That is also close to 61.8% projection of 1.0569 to 1.2091 from 1.1553 at 1.2494.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 7:00 | EUR | German Factory Orders M/M Nov | -0.40% | 0.00% | 0.50% | |

| 8:15 | CHF | CPI M/M Dec | 0.00% | -0.10% | -0.10% | |

| 8:15 | CHF | CPI Y/Y Dec | 0.80% | 0.80% | 0.80% | |

| 9:30 | EUR | Eurozone Sentix Investor Confidence Jan | 32.9 | 31.3 | 31.1 | |

| 10:00 | EUR | Eurozone Retail Sales M/M Nov | 1.50% | 1.30% | -1.10% | |

| 10:00 | EUR | Eurozone Consumer Confidence Dec F | 0.5 | 0.5 | 0.5 | |

| 10:00 | EUR | Eurozone Economic Confidence Dec | 116 | 114.8 | 114.6 | |

| 10:00 | EUR | Eurozone Business Climate Indicator Dec | 1.66 | 1.5 | 1.49 | |

| 10:00 | EUR | Eurozone Industrial Confidence Dec | 9.1 | 8.4 | 8.2 | |

| 10:00 | EUR | Eurozone Services Confidence Dec | 18.4 | 16.5 | 16.3 | 16.4 |

| 15:30 | CAD | BOC Business Outlook Survey |

Euro Shrugs off Data; European Stocks Hit Fresh Highs

Here are the latest developments in global markets:

FOREX: Encouraging data out of the Eurozone including on retail sales and economic sentiment did little for the euro which pared a small part of earlier losses in the wake of the figures. Euro/dollar continued to trade weaker, slightly below the 1.20 handle (-0.32%) as traders engaged in profit-taking. This compares to last week's four-month peak of 1.2089. On the other hand, the UK's disappointing housing figures kept the pound under pressure, with pound/dollar remaining close to intraday lows at 1.3459 (-0.18%). The dollar index inched below the 92-key level (+0.26%) against a basket of six currencies but maintained its upside momentum as markets continued to bet that the Fed would proceed with further monetary tightening this year. Dollar/yen stood flat at 113.13 after retreating from three-week highs reached early today, while aussie/dollar was on the backfoot, slipping to 0.7836 (-0.33%).

STOCKS: European shares followed their Asian counterparts and hit new highs on Monday as confidence in the Eurozone's economic performance continued to feed investor's appetite for riskier assets ahead of corporate earnings releases. The pan-European STOXX 600 jumped to a more-than-two-year high, lifted by rising auto shares, being 0.20% up on the day at 1000 GMT. The blue-chip Euro STOXX 50 gained 0.30% with all sectors being in the green. The German DAX 30 and the French CAC 40 increased by 0.36% and 0.32% respectively. The British FTSE 100 was steady around Friday's record peak. US futures on major Wall Street indices were all up.

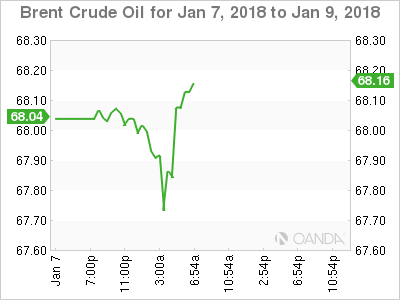

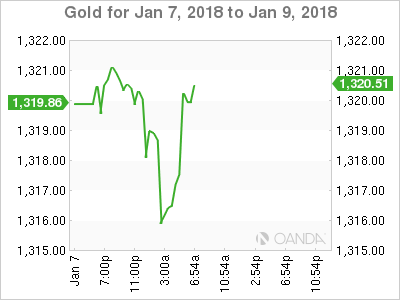

COMMODITIES: Oil prices held onto gains, with WTI crude climbing by 0.60% to $61.81 per barrel and Brent rising by 0.28% to $67.81. A Reuters survey showed that OPEC compliance to supply cuts strengthened in December due to output cuts in Venezuela and other production drops in other OPEC countries. Gold steadied at $1,320.40 per ounce, trading near three-week highs it first hit on Thursday.

Day ahead: FOMC members in focus; May initiates Cabinet reshuffle

Looking forward to the day, the economic calendar will gather little attention as data releases will be relatively light. Instead, the focus will turn to speeches made by FOMC members as investors seek for new clues on the path of US interest rates which federal fund futures suggest rising twice - by 25 bps each - this year. Moreover, a cabinet reshuffle is anticipated to take place today in the UK.

At 1740 GMT, the Atlanta's Fed President Raphael Bostic will speak on the economic outlook and monetary policy before the Rotary Club of Atlanta, while John Williams (1835 GMT) and Eric Rosengren (2125 GMT), the San Francisco and the Boston Fed Presidents, will follow up, participating in a panel discussion before the Brookings Institution event titled "Should the Fed stick with the 2-percent inflation target or rethink it?".

Meanwhile in the UK, the British Prime Minister is expected to hold the third cabinet reshuffle later on Monday since her appointment in July 2016. The reshuffle, triggered by the forced resignation of Damian Green as the first secretary of state due to sexual harassment, is expected to continue into Tuesday, and be an opportunity for May to unify the already divided-over-Brexit Conservatives and refresh the government. However, Philip Hammond (Chancellor of the Exchequer), Boris Johnson (Foreign Secretary) and David Davis (Brexit Secretary) are among ministers anticipated to remain in place.

In other political news, North and South Korea officials will meet early on Tuesday at 0300 GMT - this being the first high-level meeting since 2015 - to primarily discuss North Korea's participation in next month's Winter Olympics in Pyeongchang. Yet, markets see the talks as a great chance for the sides to express what they can offer beyond cooperation on the Olympics. According to South Korea's government officials, the South Korean President Moon Jae-in and the North Korean leader Kim Jong-Un will be able to listen to the discussions and if needed to intervene.

Market Update – European Session: Euro Zone Dec Business Climate Hits A Record High, UK PM Expected To Reshuffle...

Notes/Observations

Euro Zone Dec Business Climate Indicator hits a fresh record high (1.66 v 1.50e)

UK Halifax House Prices registers its 1st decline in 6 months (-0.6% v +0.2%e)

UK PM May expected to announce a Cabinet reshuffle but not expected to affect Foreign, Finance, Interior or Brexit Ministers

Merkel faces complex coalition building in Germany

Asia:

China Dec Foreign Reserves: $3.140T v $3.127Te (highest since Sept 2016, 11th consecutive gain, biggest gain since July). 2017 FX reserves rose $129.5B to $3.1405 for its first annual rise since 2014)

China FX Regulator SAFE: Too keep the nation's foreign exchange reserves and international balance of payments "balanced and stable" in 2018.

China PBOC deputy head of research Ji Min: Room for an increase in interest rates in the short term as industrial product prices and enterprises' profitability have improved since last year (does not specify which interest rate)

PBoC Adviser reiterated that saw CNY currency (yuan) as basically stable. Currently no pressure to depreciate the yuan; not necessary to increase deposit and lending rates in the real economy. Yuan will likely stabilize around 6.6 vs USD in longer term

China PBoC: Skips OMO for 11th straight session

Europe:

ECB's Weidmann (Germany) reiterated view that General Council should set a concrete date for ending its QE program; signs for inflation to return to a level that was sufficient to maintain price stability

German acting Chancellor Merkel: Optimistic that her conservatives and the Social Democrats (SPD) could form a government

German SPD leader Schulz: Party was entering the talks constructively. Won't draw any red lines - rather we want to push through as much red politics as possible

Italy Fin Min Padoan: Coalition between the outgoing centre-left Democratic Party (PD) and billionaire Silvio Berlusconi's Forza Italia (FI) could be on the cards. Could be political stalemate after general elections (**Reminder: Italy to hold elections on Mar 4th)

UK PM May said to plan cabinet changes, which are expected to include a cabinet minister for 'no deal' just in case the Brexit talks are unsuccessful and as negotiating tactic. Around 6 Cabinet changes could be made but not expected to affect Foreign, Finance, Interior or Brexit Ministers. Expected to announce new First Sec of State after Damien Green was forced resignation

UK Visa Dec Consumer Spending Y/Y: -1.0% v -0.9% prior (first Dec decline since 2012)

Americas:

Fed's Williams (2018 voter): Reiterates three rates hike in 2018 makes sense

Fed's Mester (voter, hawk): three or four rate hikes would be fine this year; today's jobs report was pretty strong. Basically at maximum employment but doesn't necessarily trigger policy action

White House chief economist Hassett: Fed would not need to tighten policy at a faster rate in response to recently passed tax cuts

Energy:

Weekly Baker Hughes US Rig Count: 924 v 929 w/w (-0.5%) (second consecutive weekly drop)

Economic Data:

(ZA) South Africa Dec Gross Reserves: $50.7B v $50.3B prior; Net Reserves: 42.9B v $42.7B prior

(DE) Germany Nov Factory Orders M/M: -0.4% v 0.0%e; Y/Y: 8.7% v 7.8%e

(NO) Norway Nov Industrial Production M/M: +0.6 v -1.4% prior; Y/Y: -1.3% v -2.0% prior

(NO) Norway Nov Manufacturing Production M/M: 0.3% v 0.5%e; Y/Y: 2.3% v 1.9% prior

(TR) Turkey Nov Industrial Production M/M: 0.3% v 0.3%e; Y/Y: 7.0% v 7.0%e

(TW) Taiwan Dec Trade Balance: $6.1B v $5.8Be; Exports Y/Y: 14.8% v 10.9%e prior; Imports Y/Y: 12.2% v 8.3%e

(CZ) Czech Nov Industrial Output Y/Y: 8.5% v 5.7%e

(CZ) Czech Nov National Trade Balance (CZK): 11.7B v 5.3Be

(HU) Hungary Nov Industrial Production M/M: -2.1% v +1.1% prior; Y/Y: 3.4% v 7.2%e

(HU) Hungary Nov Retail Sales Y/Y: 6.4% v 5.6%e

(CH) Swiss Dec CPI M/M: 0.0% v -0.1%e; Y/Y: 0.8% v 0.8%e

(CH) Swiss Dec CPI EU Harmonized M/M: +0.2% v -0.3% prior; Y/Y: 1.1% v 0.8% prior

(UK) Dec Halifax House Prices M/M: -0.6% v +0.2%e; 3M/3M: 2.7% v 3.3%e

(EU) Euro Zone Jan Sentix Investor Confidence: 32.9 v 31.3e

(EU) Euro Zone Dec Business Climate Indicator: 1.66 v 1.50e (record high); Consumer Confidence (Final): 0.5 v 0.5e, Economic Confidence: 116.0 v 114.8e, Industrial Confidence: 9.1 v 8.4e, Services Confidence: 18.4 v 16.5e

(EU) Euro Zone Nov Retail Sales M/M: 1.5% v 1.3%e; Y/Y: 2.8% v 2.4%e

Fixed Income Issuance:

None seen

SPEAKERS/FIXED INCOME/FX/COMMODITIES/ERRATUM

Equities

Indices [Stoxx600 ++0.3% at 398.3 , FTSE flat at 7727 , DAX +0.4% at 13374, CAC-40 +0.4% at 5491 , IBEX-35 +0.2% at 10434, FTSE MIB 0.1% at 22786 , SMI +0.1% at 9561, S&P 500 Futures flat]

Market Focal Points/Key Themes:

European Indices trade higher across the board being led by the Dax and Cac as the positive momentum in 2018 continues following on the heels of further record closes in US Indices despite weaker US Jobs data.

In the UK shares of Mothercare, Microfocus and McBride trade sharply lower following their trading updates, whilst Dialog Semi trades over 2% higher after prelim Q4 Rev was above prior forecasts. Ablynx will be in focus after rejecting a €30.50/shr offer from Novo Nordisk; Curetis trades over 30% higher after an FDA update.

In the US Mazor Robotics reported record Q4 Rev, and guides FY18 modestly higher, and Celgene confirms to acquire Impact Biomedicines for $1.1B upfront and up to $1.25B in contingent payments.

Movers

Consumer Discretionary [ Mothercare [MTC.UK} -26% (Christmas trading update), Givaudan [GIVN.CH] -2.3% (Analyst downgrade), Mcbride [MCB.UK] -18% (Trading update, profit warnings), H&T [HAT.UK] +3.3% (Trading update)]

Technology [ Dialog Semi [DLG.DE] +3.2% (Prelim Q4), Microfocus [MCRO.UK] -11% (Earnings) ]

Materials [ Gem Diamonds [GEMD.UK] +7% (Recovery of 2 high quality diamonds) ]

Industrials [Astaldi [AST.IT] +6% (Contract award)]

Healthcare [Curetis [CURE.NL] +25% (Expecting an early decision by the FDA via the De Novo application)]

Speakers

German conservatives and SPD said to seek raising threshold for high income earners to 42% on income above €60K (**Note: Threshold is currently at earnings of €53.7K)

German German SPD leader Schulz: Optimistic as coalition talks address Europe

Greece PM Tsipras: 3rd bailout review to be completed in coming days

Philippines Econ Planning Sec Pernia: Q4 GDP growth likely exceeded Q3 pace

Indonesia Fin Min Indrawati: 2017 GDP growth to fall short of target

Currencies

EUR/USD continued to move off 3-month highs as German economic data missed its mark. Merkel faces complex coalition building in Germany

GBP was softer in the session on that back of weaker economic data. UK Visa Dec Consumer Spending saw its 1st Dec decline since 2012 and the overall 2017 Consumer Spending enduring its first annual decline since 2012. GBP also weighed upon be renewed speculation that UK PM would announce a Cabinet reshuffle and perhaps name a minister for a “No Brexit” position

Looking Ahead

(UK) House of Commons reconvenes following its Christmas recess

(IT) Italy Debt Agency (Tesoro) announcement on upcoming BTP auction for Thurs, Jan 11th

(RO) Romania Central Bank (NBR) Interest Rate Decision: Expected to leave Interest Rate unchanged at 1.75%

(MX) Mexico Dec Vehicle Production: No est v 332.4K prior; Vehicle Exports: No est v 274.5K prior

05:25 (BR) Brazil Central Bank Weekly Economists Survey)

05:30 (NL) Netherlands Debt Agency (DSTA) to sell €1.0-2.0B in 6-month Bills

06:00 (CL) Chile Dec CPI M/M: 0.2%e v 0.1% prior; Y/Y: 2.3%e v 1.9% prior

06:00 (CL) Chile Dec CPI (Ex-food/energy) M/M: No est v -0.1% prior; Y/Y: No est v 1.8% prior

06:30 (CL) Chile Dec Trade Balance: $0.9Be v $0.5B prior; Total Exports: $6.7Be v $6.0B prior; Total Imports: $5.8Be v $5.5B prior; Copper Exports: No est v $3.3B prior

06:45 (US) Daily Libor Fixing

08:00 (UK) Baltic Dry Bulk Index

08:00 (RO) Romania Central Bank gov Isarescu post rate decision press conference

08:00 (ES) Spain Debt Agency (Tesoro) announces size of upcoming actions in week

08:00 (IN) India announces details of upcoming bond sale (held on Fridays)

08:55 (FR) France Debt Agency (AFT) to sell combined €4.7-5.9B in 3-month, 6-month and 12-month BTF Bills

To sell €3.4B in 3-month Bills

To sell €1.2B in 6-month Bills

To sell €1.3B in 12-month Bills

09:30 (EU) ECB announces Covered-Bond Purchases

09:35 (EU) ECB calls for bids in 7-Day Main Refinancing Tender

10:30 (CA) Bank of Canada Q4 Senior Loan Survey: No est v -0.5 prior; Business Outlook: No est v -0.5e

11:30 (US) Treasuries to sell to 3-month and 6-month bills

12:40 (US) Fed's Bostic (voter, dove) speaks on Economic Outlook in Atlanta

13:35 (US) Fed’s Williams (voter, moderate) at conference

15:00 (US) Nov Consumer Credit: $18.0Be v $20.5B prior

15:00 (MX) Mexico Citibanamex Survey of Economists

16:00 (US) Fed’s Rosengren (non-voter, hawk) at conference

EUR/USD Dips Below 1.20 As German Factory Orders Fall

The euro has started with slight losses in the Monday session. Currently, EUR/USD is trading at 1.1999, down 0.25% on the day. On the release front, German Factory Orders disappointed, with a decline of 0.4%. This was well short of the estimate of a 0.1% gain. In the Eurozone, Sentix Investor Confidence improved to 32.9, above the estimate of 31.5 points. Retail Sales rebounded with a strong gain of 1.5%, beating the estimate of 1.4%. There are no major events out of the US. On Tuesday, Germany releases Industrial Production and Trade Balance. The US will publish JOLTS Job Openings.

The German economy continues to look strong, despite a soft Factory Orders report for December. Retail Sales soared 2.3%, its fastest pace since October 2016. Services and Manufacturing PMIs improved and continue to point to strong expansion. The labor market remains robust, as unemployment rolls dropped sharply. However, the political landscape in the eurozone’s largest economy remains cloudy. President Angela Merkel is now looking at the Social Democrats to help her make a new government, and preliminary talks are scheduled to begin on Sunday. The negotiations are likely to be lengthy, and the current caretaker government could remain in office for several more months.

The euro lost ground on Friday, after mixed US employment numbers. Nonfarm Payrolls dropped to 148 thousand, down from 228 thousand in the previous release. This was well below the estimate of 190 thousand. There was better news from wage growth, which edged up to 0.3%, matching the forecast. This marked a 3-month high. The unemployment rate remained unchanged, at a sizzling 4.1%.

Technical Outlook: WTI Oil – Downside Rejection At $61.00 Keeps Bias With Bulls But Upside Attempts Could Be Limited...

WTI oil price is regaining traction and moved higher in mid-European session trading on Monday after shallow correction on Friday was contained just above psychological $61.00 support. Strong downside rejection last Friday sidelined signals of reversal, turning immediate focus to the upside. Technical studies remain in bullish setup on daily chart, favoring further advance, however, overbought conditions and concerns about rising US production, which offset positive signals from decline in US oil rigs, suggests limited upside action for now. The price may hold in extended consolidation before firmly breaking barrier at $62.00 per barrel, with extended dips not ruled out. Rising daily 10SMA continues to underpin and offers solid support (currently at $60.52) which is expected to contain downticks and limit risk of deeper pullback.

Res: 62.02, 62.19, 62.71, 63.00

Sup: 61.37, 61.08, 60.52, 60.17

Dollar Bulls Still Not That Confident

Monday January 8: Five things the markets are talking about

With risk assets enjoying a strong start to the New Year, the beginning of corporate earnings season is expected to dictate the next move for the stock markets.

In overnight trade, the EUR (€1.1989) and the pound (£1.3529) have retreated against the dollar, while U.S Treasury yields have little changed in light trading, while oil trades above +$61 a barrel.

Economic data in the coming week focuses mostly on merchandise trade balances and industrial production for November and prices in the U.S.

On Tuesday, Germany releases its important manufacturing orders and industrial production data along with its merchandise trade surplus. Wednesday sees China beginning to release its monthly data with December consumer and producer prices and merchandise trade balance. While down-under, Australia reports retail sales for December late Wednesday.

Stateside this week, U.S inflation data Thursday and Friday tops the agenda and will probably show price pressures remain muted, giving dollar ‘hawks' no ammo to argue for a faster Fed tightening.

Also, a couple of Fed speakers should be of interest for capital markets – SF Fed President Williams and head of the NY Fed Dudley are among policy makers scheduled to speak.

1. Stocks are given the green light

Both Asian and European markets have traded generally higher after Friday's gains in the U.S

Note: The Nikkei 225 was closed for holiday.

Down-under, Australian shares marked a ten-year peak overnight and rallied to end their fourth session higher on Monday, helped higher by financials and a positive cue from Wall Street. The S&P/ASX 200 index ended the session +0.1% higher. In Korea, the Kospi edged higher in light trade, up +0.11%.

Note: South Korea has stepped up its currency warning – Korean Won (KRW) has weakened ahead of Tomorrow's expected talks with North Korea.

In Hong Kong, the benchmark stock indexes rallied for a 10th consecutive session overnight, aided by bullish sentiment in global equity markets, and inbound investment from the mainland. At close, the Hang Seng index was up +0.28%, while the Hang Seng China Enterprises index rose +0.19%.

In China, stocks end at a six-week high with property developers lending support. At the close, the Shanghai Composite index was up +0.54%, while the blue-chip CSI300 index was up +0.52%.

In Europe, regional indices are trading higher across the board, led by the DAX and the CAC – this follows the record closes in U.S Indices despite last Friday's weaker non-farm payroll (NFP) report.

U.S stocks are set to open unchanged.

Indices: Stoxx600 ++0.3% at 398.3, FTSE flat at 7727, DAX +0.4% at 13374, CAC-40 +0.4% at 5491, IBEX-35 +0.2% at 10434, FTSE MIB 0.1% at 22786, SMI +0.1% at 9561, S&P 500 Futures flat

2. Oil stable on lower U.S. rig count, gold little changed

Oil prices are stable, supported by a slight decline in the number of U.S rigs drilling for new production. Prices are holding just below the commodities three-year highs reached last week.

Brent crude futures are at +$67.66 a barrel, up +4c above Friday's close, while U.S West Texas Intermediate (WTI) crude futures are at +$61.50 a barrel.

Note: Brent hit +$68.27 high last week, the highest since May 2015, while WTI futures reached +$62.21, the most since May 2015.

The slight gains are mostly due to a slight decline in the number of U.S rigs drilling for new production, which has eased by five in the week to Jan. 5 to +742, according to data from oil services firm Baker Hughes.

U.S crude prices have now entered a price range that is anticipated to attract increased shale oil production, which is expected to put a temporary cap on future higher prices.

Note: Rising U.S production is the main factor countering production cuts led by OPEC and by Russia, which began in January last year and are set to last through this year.

Ahead of the U.S open, gold prices have dipped as the U.S dollar firms a tad on rate hike views. Spot gold trades below its 3-1/2-month highs hit last week at +$1,322.73 an ounce – last week, prices touched their highest since Sept. 15 at +$1,325.86.

3. Euro yields face a busy issuance

Euro borrowing costs are set to back up with this week's new bond supply.

Germany, Austria, the Netherlands and Italy are expected to sell almost +€12B of bonds this week.

Note: January is one of the busiest months for new bond supply and fixed income traders need to cheapen their sovereign curves to take down supply.

For the bond ‘bull,' benign Euro inflation environment would suggest that the markets should be capable of absorbing the new supply with few problems.

Note: Euro inflation data last Friday showed a +1.4% year-on-year in December, well below the ECB's near +2% target. The core-measure (ex-food and energy) was +1.1%.

The yield on U.S 10-year Treasuries decreased less than -1 bps to +2.47%, while in Germany, the 10-year Bund yield has decreased -1 bps to +0.43%, the lowest in a week.

4. Dollar finds some much needed traction

EUR/USD (€1.2006) has continued to back away from its three-month highs as some German economic data missed its mark and while Chancellor Merkel faces a complex coalition-building task in Germany. Nevertheless, the Chancellor remains optimistic that her conservatives and the Social Democrats (SPD) could form a government.

Sterling (£1.3545) starts the weak a tad softer on that back of weaker economic data. U.K Visa December Consumer Spending saw its first end of year decline in five-years and the overall 2017 consumer spending enduring its first annual decline since 2012. The pound is also weighed upon be renewed speculation that U.K PM Theresa May will announce a Cabinet reshuffle and perhaps name a minister for a “No Brexit” position.

Bank of Canada (BoC) business survey at 10 am EDT could support a possible rate hike next week. Last Friday, Canada's unemployment rate dropped to a four-decade low in December and job creation exceeded expectations for a second consecutive month. The Canadian economy added a whopping net +78.6k jobs in December vs. market expectations of +2k. The loonie is trading flat C$1.2400.

5. Eurozone confidence stronger than expected in December

Data this morning showed that the surge in eurozone regional confidence continued as last year drew to a close, with the ESI (Sentix) rising more sharply than expected to hit its highest level in 17-years.

The aggregate measure of business and consumer confidence jumped to 116.0 in December from 114.6, as against a consensus forecast of 114.8.

The headline was driven in part by a rise in industrial confidence. It would suggest that the regions accelerated expansion would continue into the early months of the New Year.

Be aware, any drop in consumer inflation expectations will only worry ECB policy makers as that could feed into more modest wage demands.

Fed Speakers Eyed After Strong Start To 2018

After an impressive opening week to the year, US futures are pointing to a flat open on Wall Street on Monday, with investors eyeing a few key data points and the start of fourth quarter earnings season.

Heading into another earnings season, there is a strong sense of optimism in the markets, with the Dow having blown past 25,000 with relative ease before ending the week with a record close. While we're currently looking at a flat start, the US may take some direction from Asia and Europe as we approach the open with both regions having posted/posting moderate gains at the start of the week.

The US dollar is taking another stab higher this morning after its false start last week but it's clearly struggling for any upward momentum. Sentiment towards the greenback has softened considerably despite the passing of tax reform in the US, something many thought may have been a positive for the currency. Given the downside we've seen in the dollar over the last month, we could see a small correction although as of yet, there doesn't appear too much appetite for upside.

Perhaps today's Federal Reserve speakers will provide the catalyst for a move higher in the dollar, with John Williams, Raphael Rostic and Eric Rosengren all making appearances. Williams and Rostic will both be voters on the FOMC this year and so their views will be very closely monitored and could have an impact, although with Jerome Powell set to succeed Janet Yellen as Chair next month and a number of roles still to be filled, there remains an element of uncertainty when it comes to Fed policy going forward.

While there is a number of key data releases that will be closely monitored this week, the bulk of these will come later on, most notably US retail sales and CPI inflation on Friday. Friday will also mark the start of earnings season which will be a key focus for investors over the coming weeks now that tax reform is over the line.