Sample Category Title

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2808; (P) 1.2844; (R1) 1.2870; More....

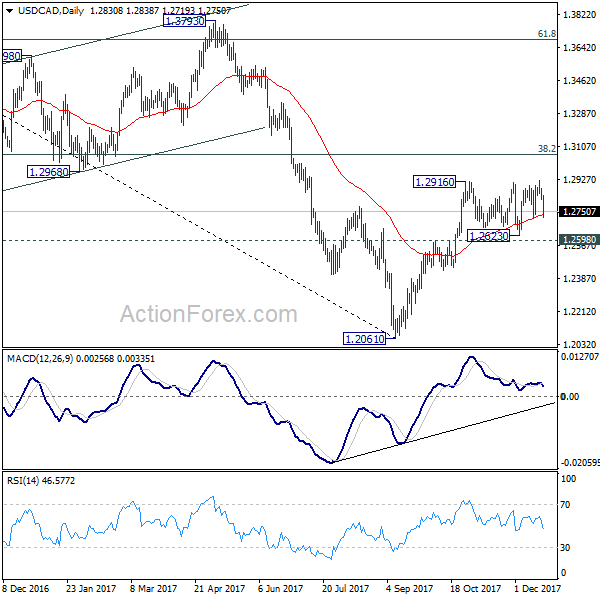

USD/CAD drops sharply to as low as 1.2719 in early US session. But it still staying in range between 1.2598/2919. Intraday bias stays neutral at this point. As noted before, as s long as 1.2598 resistance turned support holds, near term outlook remains bullish. On the upside, firm break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2885). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

CAD Surges on Strong Retail Sales and CPI, Dollar Trying to Recover

Canadian Dollar soars in early US session after impressive economic data. Head line retail sale rose 1.5% mom in October versus expectation of 0.3% mom. Ex-auto sales rose 0.8% mom versus expectation of 0.4% mom. Inflation data also came in generally stronger than expected. Headline CPI accelerated to 2.1% yoy, up from 1.4% yoy and beat expectation of 2.0% yoy. CPI core median rose to 1.9% yoy, up from 1.7% yoy and beat expectation of 1.7% yoy. CPI core trim rose to 1.8% yoy, up from 1.5% yoy, beat expectation of 1.5% yoy. Nonetheless, CPI core common slowed to 1.5% yoy, down from 1.6% yoy and missed expectation of 1.7% yoy. The set of data adds to the case for BoC to raise interest rate again in Q1. USD/CAD dipped to as low as 1.2719, comparing to this week's high at 1.2919.

US initial claims jumped 20k, Dollar trying to recover

US initial jobless claims rose 20k to 245k in the week ended December 15, well above expectation of 234k. Nevertheless, it should be noted that prior week's 225k was an ultra-low level." Four week moving average rose 1.25k to 236k. Continuing claims rose 43k to 1.93m in the week ended December 8. The set of jobless claims data did nothing to change the healthy outlook of the job market. Also from US, Philly Fed manufacturing index rose to 26.2 in December, up from 22.7 and beat expectation of 20.8. House price index rose 0.5% mom in October. Q3 GDP growth was finalized at 3.2% annualized, downwardly revised from 3.3%.

Dollar traders generally firmer today except versus Aussie and Loonie. Still, the greenback is in red against all except Yen and Swiss Franc for the week. There is little support from the passing of tax bill in the Congress.

Released elsewhere, UK public sector bet borrowing rose to GBP 8.1b in November. Gfk consumer confidence dropped to -13 in December. Swiss trade surplus widened to CHF 2.63b in November. New Zealand GDP grew 0.6% qoq in Q3.

BOJ Maintained Accommodative Policies, Kuroda Sent No Signal About Normalization.

As widely anticipated, BOJ again voted 8-1 to leave the monetary policies unchanged in October. The targets for short- and long-term interest rates stay at -0.1% and around 0%, respectively while the guideline for JGB purchases remains at an annual pace of about 80 trillion yen. The central bank has turned more upbeat on the economic outlook, especially on Capex and consumption. Goushi Kataoka was again the lone dissent as he supported bond purchases so as to facilitate the decline of 10-year (or over) bond yields. Governor Kuroda's speech at the press conference has not tilted towards less easing/ policy normalization in the near-term. More in BOJ Maintained Accommodative Policies, Kuroda Sent No Signal About Normalization.

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.2808; (P) 1.2844; (R1) 1.2870; More....

USD/CAD drops sharply to as low as 1.2719 in early US session. But it still staying in range between 1.2598/2919. Intraday bias stays neutral at this point. As noted before, as s long as 1.2598 resistance turned support holds, near term outlook remains bullish. On the upside, firm break of 1.2916 will resume the rise from 1.2061 and target 1.3065 medium term fibonacci level next. However, sustained break of 1.2598 will argue that rebound from 1.2061 has completed after hitting 55 week EMA (now at 1.2885). Near term outlook will be turned bearish in this case.

In the bigger picture, USD/CAD should have defended 50% retracement of 0.9406 (2011 low) to 1.4689 (2016 high) at 1.2048. And with 1.2048 intact, we'd favor the case that fall from 1.4689 is a correction. Rise from 1.2061 medium term bottom should now target 38.2% retracement of 1.4689 to 1.2061 at 1.3065. Firm break there will target 1.3793 key resistance next (61.8% retracement at 1.3685). We'll now hold on to this bullish view as long as 1.2450 support holds.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | GDP Q/Q Q3 | 0.60% | 0.60% | 0.80% | 1.00% |

| 00:01 | GBP | GfK Consumer Confidence Dec | -13 | -12 | -12 | |

| 02:00 | JPY | BOJ Rate Decision | -0.10% | -0.10% | -0.10% | |

| 07:00 | CHF | Trade Balance Nov | 2.63B | 2.84B | 2.33B | |

| 09:30 | GBP | Public Sector Net Borrowing Nov | 8.1B | 8.6B | 7.5B | |

| 13:30 | CAD | CPI M/M Nov | 0.30% | 0.20% | 0.10% | |

| 13:30 | CAD | CPI Y/Y Nov | 2.10% | 2.00% | 1.40% | |

| 13:30 | CAD | CPI Core - Common Y/Y Nov | 1.50% | 1.70% | 1.60% | |

| 13:30 | CAD | CPI Core - Trim Y/Y Nov | 1.80% | 1.50% | 1.50% | |

| 13:30 | CAD | CPI Core - Median Y/Y Nov | 1.90% | 1.70% | 1.70% | |

| 13:30 | CAD | Retail Sales M/M Oct | 1.50% | 0.30% | 0.10% | |

| 13:30 | CAD | Retail Sales Ex Auto M/M Oct | 0.80% | 0.40% | 0.30% | 0.20% |

| 13:30 | USD | Philly Fed Manufacturing Index Dec | 26.2 | 20.8 | 22.7 | |

| 13:30 | USD | Initial Jobless Claims (DEC 16) | 245K | 234K | 225K | |

| 13:30 | USD | GDP Annualized Q/Q Q3 T | 3.20% | 3.30% | 3.30% | |

| 13:30 | USD | GDP Price Index Q3 T | 2.10% | 2.10% | 2.10% | |

| 14:00 | USD | House Price Index M/M Oct | 0.50% | 0.40% | 0.30% | 0.50% |

| 15:00 | USD | Leading Index Nov | 0.40% | 1.20% | ||

| 15:00 | EUR | Eurozone Consumer Confidence Dec A | 0.2 | 0.1 | ||

| 15:30 | USD | Natural Gas Storage | -69B |

Canada: Inflation Bounces Back with Energy Prices in November

Consumer price inflation rose to 2.1% year-on-year in November (from 1.4% in October), a hair above expectations for 2.0%. Month-on-month seasonally-adjusted prices were up a strong 0.5%

Price gains were relatively widespread, with all major categories except health and personal care rising in the month and accelerating on a year-on-year basis.

Energy prices rebounded soundly after pulling back in October. Energy prices were up 7.6% year-on-year, led by gasoline prices (up 19.6%).

Food and beverage prices rose 0.2% month-on-month in November (seasonally adjusted) and accelerated to 1.6% year-on-year (from 1.3%).

Core price inflation accelerated nicely according to two of the Bank of Canada's three measures: CPI-trim rose to 1.8% (from 1.5%), while CPI-median rose to 1.9% (from 1.7%). The CPI-common measure was the hold out, edging down to 1.5% from 1.6% in October.

Key Implications

Inflation suddenly doesn't feel so soft in Canada. The broad-based gain in prices in November echoes the trends seen in the rest of the economy and suggests that the Phillip's curve relationship between inflation and economic slack (or lack thereof) still has some explanatory power.

With economic momentum appearing to hold up into the fourth quarter (reinforced in today's retail sales report), the case for the Bank of Canada to follow the Federal Reserve in hiking interest rates is building. Don't be surprised if it comes sooner rather than later.

Markets Flat as US Congress Passes Tax Reform

No Sign of "Buy the Rumour, Sell the Fact" Trading After Tax Reform Bill Passes

US equity markets are expected to open relatively unchanged on Thursday, a day after posting small losses despite tax reform successfully making its way through Congress in time for the holidays.

With tax reform having been priced in over the course of the year, including a late push in recent weeks as details of the bill became clear and progress through Congress was made, it's evident that it is already priced in. While we're not yet seeing signs of corrections following – in buy the rumour sell the fact fashion – markets may struggle for positive catalysts over the next week or so.

Catalan Looks to Elect New Parliament But Crisis May Go Unresolved

Catalonia will vote to elect a new parliament on Thursday, a couple of months after the previous administration was sacked, with some members jailed and others opting for self-imposed exile in Belgium. It is hoped that the election will resolve the issues of independence and show that the majority of Catalans do not in fact favour independence from Spain. Unfortunately, it's very unlikely to be so straightforward.

The topic of independence is a very divisive issue in Catalonia and it remains quite evenly split between those wanting it and those not. There's a good chance that this election will produce a hung parliament which will far from resolve the crisis and even a small majority for independence parties will be unlikely to see them get their wishes.

BoJ Warns Against Speculation of Monetary Tightening

The yen is trading a little lower today after the Bank of Japan left monetary policy changed at its final meeting of 2017 – a result that surprised no one – while re-emphasizing its commitment to its ultra-accommodative stance. There had been some speculation that the central bank may be tempted to take its foot off the gas soon as the economy is performing well and inflation is no longer in negative territory.

Governor Haruhiko Kuroda stoked this further at a speech in Zurich last month when discussing the potential for low interest rates to be contractionary, which some viewed as a signal that the central bank may consider tightening in fear of such a scenario. As it turns out, Kuroda was not implying such an action and claims the BoJ remains committed to achieving its 2% inflation target, which weighed a little on the yen.

CADJPY Struggles Beneath Significant Obstacles; Bias is Bullish

CADJPY printed two daily closes and added more than 1% to its performance, following the strong rebound on the medium-term ascending trend line which overlaps with the 87.25 support level. The diagonal line is has been holding for 13 months.

Zooming on the recent upward movement and on the short to medium timeframe, the price struggles beneath the 50 and 100 simple moving averages as well as below the short-term falling trend line which stands since mid-September. If the price successfully surpasses the aforementioned obstacles, it could drive the pair towards the next resistance levels at 89.20 and 89.80.

An alternative scenario is a penetration of the significant uptrend line to the downside, which could expose the pair towards the 85.40 support barrier. It is worth mentioning that the price will have to slip below the 200-day SMA as well.

The MACD and the RSI momentum indicators are endorsing the bullish near-term tendency on price as both are rising. The MACD oscillator is moving higher in the negative zone and posted a bullish crossover with its trigger line, whilst the RSI indicator entered the positive area and is pointing north.

USDJPY Further Bullish Above Key 113.40 Level

The U.S dollar has moved to a new weekly price-high against the Japanese yen, hitting 113.64, during the European trading session. The move higher in the USDJPY pair occurred, as bond yields across the globe continue to move into new trading ranges. The USDJPY pair currently trades around the 113.55 level, pulling back slightly, after buyers failed to pierce above the December price-high, set a 113.75. The markets attention now turns to the United States economy, with a raft of high-impacting data set to be released for the month of November.

The USDJPY pair remains strongly bullish while trading above the 113.40 level, intraday buyers will again target the 113.80 level, with extended resistance found at 114.10.

Should the USDJPY pair move below the 113.40 level, sellers may move to target the 113.10 and 112.70 support levels.

EURUSD Strongly Bullish Above 1.1860 Level

The euro continues to move higher against the U.S dollar, with price-action so far finding interim weekly resistance at the 1.1900 level. The recent fall in the Japanese yen currency on the back of falling bond prices, is helping to underpin overall euro sentiment, with the EURJPY pair benefitting the most. The EURUSD currently trades around the 1.1870 level, with buyers well in control above the 1.1860 support level. Traders now await the release of weekly jobs, wage inflation and third quarter Gross Domestic Product figures from the United States economy.

The EURUSD remains strongly bullish while trading above the 1.1860 support level, buyers may now target towards the 1.1900 and 1.1940 technical resistance levels.

Should the EURUSD pair start to decline below the 1.1860 technical level, sellers may push price-action towards the 1.1845 and 1.1813 support levels.

Canadian Dollar in Holding Pattern Ahead of CPI, Retail Sales

The Canadian dollar has shown little movement this week. Currently, USD/CAD is trading at 1.2831, down 0.03% on the day. On the release front, Canada releases CPI and Core Retail Sales. In the US, there are three key events – Final GDP, the Philly Manufacturing Index and unemployment claims. On Friday, Canada releases GDP, while the US will release Core Durable Goods, New Home Sales and UoM Consumer Sentiment.

Traders should be prepared for some movement from USD/CAD during Thursday's North American session, with a host of key indicators on both sides of the border. Canada will release consumer inflation and spending data, while the US publishes Final GDP. The markets are predicting another banner quarter, as the estimate stands at 3.3%, which would be unchanged from the Preliminary GDP release. US economic growth has looked sharp in 2017, prompting the Federal Reserve to raise rates three times this year, most recently in December. Another rate increase is widely expected in January, and a combination of strong US expansion and an accelerated pace of rate hikes could boost the US dollar.

President Donald Trump and Republican lawmakers are celebrating, after scoring a major legislative victory. On Wednesday, the House of Representatives voted for to pass Trump's tax reform bill, after it narrowly passed in the Senate, by a vote of 51-48. Trump is expected to sign the bill into law next week. The tax legislation marks the first major overhaul of the US tax code in 30 years, and reduces corporate taxes from 35% to 21%. After failing to overturn Obamacare, the Republicans finally scored a big win, and will now have to sell the tax plan to a skeptical public, with congressional elections slated for November 2018.

Euro Flat ahead of Catalonia’s Vote; European Stocks Weaker

Here are the latest developments in global markets:

FOREX: Major currencies were range-bound during the early European session, with the euro being not much stressed ahead of a regional election in Catalonia. Euro/dollar changed hands at 1.1880 around 1000 GMT (+0.09%), while euro/yen edged up to a two-year high of 134.86 (+0. 12%).The dollar was flat versus the yen and the loonie at 113.44 and 1.2829 respectively as the passage of the US tax legislation was already highly priced in the markets. The pound managed to erase most of its earlier losses, rebounding to $1.3380 after the UK government announced dates on the next parliamentary Brexit debates (January 16-17).

STOCKS: European stocks drifted lower despite the passage of the US tax legislation in Congress. The pan-European STOXX 600 was down by 0.18% at 1000 GMT as shares in Steinhoff International Holdings continued to weigh heavily on the index after they touched a fresh record low in early trades today. The Spanish IBEX 35 also lost 0.18% but was in a better position than the German DAX 30 and the French CAC 40 which retreated by 0.20%.

COMMODITIES: Oil prices pulled back on news that the British Forties, one of the largest pipelines operating in the North Sea, would start operations probably in early January. Brent fell by 0.20% to $64.43 per barrel and WTI crude slipped by 0.14% to $58.01. Gold was flat at $1,265.80 per ounce.

Day ahead: Catalonia back to polls; Canadian inflation eyes BOC target

The economic calendar will be pretty busy on Thursday, with the US, Canada and the Eurozone delivering reports ahead of the Christmas holiday. Regional elections in Catalonia will also be in focus today, where pro-independence parties will take the chance to echo their desire to leave Spain. However, in case they draw significant support, that would be another headache for the Spanish government and for the euro itself.

Out of the US, final GDP growth figures are due at 1330 GMT, with analysts predicting the gauge to match second estimates at 3.3% on an annualized basis in the third quarter. This is the highest expansion the economy has experienced in a year.

Meanwhile, final core PCE prices are expected to stand in line with previous estimates at 1.4% y/y in the third quarter.

US initial jobless claims are anticipated to climb by 6,000 in the week ending December 15, while the Philadelphia's Fed manufacturing index is forecasted to decline by 0.8 points to 21.5 in December.

The focus would also turn to Canada at 1330 GMT, where data on inflation and retail sales are expected to come higher. According to forecasts, the headline CPI Is anticipated to rise by 0.6 percentage points to 2.0% y/y in November, bringing good news to the BOC policymakers who are eagerly awaiting the index to hit this level before they decide to tighten monetary policy even further.

Monthly retail sales are said to expand by 0.3% in October compared to 0.1% seen in September. If true, this would be the highest mark posted since July. The core measure, which excludes volatile items is projected to inch up by 0.1 percentage points to 0.4%.

Elsewhere, flash readings on Eurozone's consumer confidence will be available at 1500 GMT. After reaching positive levels for the first time since 2001, the measure is now said to come lower at 0 in December.

CAC Almost Unchanged as Markets Eye Catalan Election

The CAC index is showing little movement in the Thursday session. Currently, the index is at 5355.50, up 0.06% on the day. There are no eurozone or French events on the schedule. On Friday, the US releases Final GDP.

President Donald Trump can finally hang his hat on a legislative victory, after a difficult first year in office. On Wednesday, the House of Representatives voted for to pass Trump's tax reform bill, after it narrowly passed in the Senate, by a vote of 51-48. Trump is expected to sign the bill into law next week. The tax legislation marks the first major overhaul of the US tax code in 30 years, and reduces corporate taxes from 35% to 21%. After failing to overturn Obamacare, the Republicans finally scored a big win, and will now have to sell the tax plan to a skeptical public, with congressional elections slated for November 2018.

Later on Thursday, the US releases one of the most important market-movers, US Final GDP. Investors expect another banner quarter, as the estimate stands at 3.3%, which would be unchanged from the Preliminary GDP release. We could see some movement in the stock markets following the GDP release. Investors are also keeping an eye on French consumer spending, which will be released on Friday. Consumer spending was dismal in October, with a sharp decline of 1.9%, compared to the forecast of 0.0%. However, the markets are expecting a strong rebound for November, with an estimate of a 1.4% gain. Christmas shopping will likely translate into strong consumer spending numbers for December, which could boost fourth quarter economic growth and send the CAC to higher levels early in the New Year.