Sample Category Title

New Zealand Growth Expected to Reflect a Slowdown; Kiwi Eyed

New Zealand's third quarter GDP growth figures are due on Wednesday at 2145 GMT, with forecasts projecting a slowdown in the pace of expansion during the quarter. The kiwi will be in focus as slower growth has, among others, the capacity to postpone policy normalization plans by the Reserve Bank of New Zealand.

Quarterly growth in Q3 is expected to stand at 0.5%. This compares to the preceding quarter's 0.8%. Year-on-year, GDP is forecast to expand by 2.3% during the quarter, with Q2's respective figure coming in at 2.5%.

Should expectations materialize, the softening in the growth rate is anticipated to have resulted from a weakening housing market and a lack of strength in dairy prices, coupled with softer production of dairy products due to weather factors – New Zealand is a major exporter of dairy products, while slowing growth in the housing market is seen as acting as a drag on consumer spending.

The GDP figures will be the first since Jacinda Ardern's Labour-led government took office in late October. Investors' fears on economic policy uncertainty from a resulting center-left government pushed kiwi/dollar significantly lower over the last few months. However, some analysts argue that similar to Justin Trudeau coming to power in Canada, the positioning that took place was more of an overreaction by markets.

Weaker growth though might cast doubt on whether next year's upbeat official projections are justified; in its half-year update, the Treasury said it anticipates growth of 3.3% in the year to June 2018. Economists are warning that Q3 GDP numbers might reflect more long-lasting effects that could be detrimental to growth further ahead. A slower pace of growth moving forward might put at risk the government's ambitious pro-growth spending plans.

Expectations for quarterly growth are also running below the RBNZ's latest forecast of 0.7%. A disappointment in terms of economic expansion might result in forex market participants pushing back their projections for rate normalization by the RBNZ. In such an event, kiwi/dollar is expected to head lower, with potential support for the pair coming around 0.6930, this being the current level of the 50-day moving average.

If, on the other hand, the data surprises to the upside, then kiwi/dollar would likely appreciate. In this case, a barrier to the upside could be met around last week's two-month high of 0.7033, a level which at the moment lies not far above the current price level. A break above it, would shift focus to the 200-day MA at 0.7103 for additional resistance.

The RBNZ has indicated that it will keep rates at their current record low of 1.75% until early 2020 while inflation stabilizes around 2%. The central bank's target for inflation is 2% plus/minus 1%.

Trade Idea: USD/CAD – Target met and stand aside

USD/CAD - 1.2857

Trend: Near term up

Original strategy :

Bought at 1.2765, met target at 1.2915

Position: - Long at 1.2765

Target: - 1.2915

Stop: -

New strategy :

Stand aside

Position: -

Target: -

Stop:-

Although the greenback rose to as high as 1.2920 (our long position entered at 1.2765 met target at 1.2915 with 150 points profit), lack of follow through buying on break of previous resistance at 1.2917 and the subsequent retreat suggest further consolidation would be seen, risk of a pullback to 1.2800 cannot be ruled out, however, reckon support at 1.2738 would limit downside and indicated key support at 1.2713 would remain intact.

As we have taken profit on our long position entered at 1.2765, would not chase this rise here and would be prudent to stand aside in the meantime. Above 1.2920 would revive bullishness and extend recent rise to 1.2975-80 (61.8% Fibonacci retracement of 1.3547-1.2061), then towards psychological resistance at 1.3000.

To recap, wave B from 1.3066 is unfolding as an a-b-c and is sub-divided as a: 1.2192, b: 1.2716 and wave c is a 5-waver with i: 1.1983, ii: 1.2506, extended wave iii with minor iii at 1.0206, wave iv ended at 1.0781 and wave v as well as wave iii has ended at 0.9931, hence the subsequent choppy trading is the wave iv which is unfolding as (a)-(b)-(c) with (a) leg of iv ended at 1.0854, followed by (b) leg at 1.0108 and (c) leg as well as the wave iv ended at 1.0674. The wave v is sub-divided by minor wave (i): 0.9980, (ii): 1.0374, (iii): 0.9446, (iv): 0.9913 and (v) as well as v has possibly ended at 0.9407, therefore, consolidation with upside bias is seen for major correction, indicated target at 1.3700 and 1.4000 had been met and further gain to 1.4700 would be seen later.

Brexit to Remain the Dominant Theme for Sterling in 2018

Sterling staged a modest recovery in 2017, on the back of a rate hike by the Bank of England and some noteworthy, albeit slow, progress in the Brexit talks. Even though monetary policy has been supporting the currency in recent months, it is an open question whether this will remain the case moving forward. Moreover, the Brexit negotiations have only just entered their second and perhaps most crucial phase, where the two sides will discuss the all-important trading relationship. Numerous political uncertainties persist, and until the smoke clears, one could argue that any rallies in the pound may remain relatively limited.

Despite a plethora of uncertainties emanating from both politics and economics, 2017 was a kind year for the British pound, with the currency outperforming most of its major peers, besides the almighty euro. Sterling's gains were particularly visible against the wounded US dollar, with sterling/dollar trading in an uptrend for practically the entire year. What was the catalyst behind the currency's rally, and is it likely to continue into 2018?

In terms of monetary policy, the Bank of England (BoE) raised its benchmark interest rate by 25 basis points for the first time in a decade, and provided signals of more to come, albeit at a gradual pace. At the time of writing, markets have fully priced in another quarter-point rate increase by year-end 2018, according to the UK overnight index swaps. Thus, the key question for sterling now is whether the BoE will deliver more, or fewer hikes than what is currently expected.

Looking at UK economic data, policymakers have little reason to raise rates aggressively. Inflation has accelerated, but wages have not, keeping real wage growth negative. This in turn, has been weighing on private consumption, something evident by the weakening trend in retail sales, resulting in a slowdown in broader economic growth. Rapid policy normalization could make a bad situation even worse, as it would likely depress wages further. Furthermore, the Bank also has the Brexit negotiations to consider, and the fact that the future EU-UK trading relationship remains largely an unknown. Unless both inflation and wages begin to surprise to the upside relative to the BoE's own forecasts, it is difficult to envisage a scenario where policymakers hike rates twice or more in 2018, as that would potentially entail more risks than benefits to the UK economy. Therefore, the risks surrounding sterling from monetary policy in 2018 may be tilted to the downside, with the BoE more likely to either meet market expectations for one quarter-point rate hike, or perhaps disappoint and not hike at all.

Turning to politics, 2017 was a bumpy year for the pound, with the snap election called by Theresa May resulting in a hung parliament, and the continued headlines around Brexit providing ample of volatility to keep GBP traders busy. After several delays in the Brexit talks, the two sides finally managed to reach a consensus on the first issue at hand; the divorce terms. Now, the negotiations can finally move on to phase two, which will deal with the future EU-UK relationship and the all-important subject of trade.

While the fact that the talks are moving forward is a positive development for sterling, one must highlight that this process has already been substantially delayed on what should have been a relatively simple matter to settle in the divorce terms. The inability of the two sides to agree on the terms in a timely manner suggests that when we do begin to discuss trade, we may encounter fresh setbacks and disappointments there, especially considering the more complex nature of the subject. The longer the overall process is delayed, the higher the likelihood that business uncertainties may begin to translate into weaker business investment and thus, slower economic growth. Moreover, it is paramount to note that the UK government is under pressure domestically as well, with the lack of a majority in Parliament and the constant "rebellions" within the Conservative Party undermining Theresa May's political capital and negotiating power.

Bearing all the above in mind, the outlook for sterling appears somewhat grim into 2018. One could argue that any rallies in the GBP may remain relatively limited, perhaps until the fog of political uncertainty lifts. The key risk to this view would be material progress in the Brexit process that tips the scale in favor of the pound, such as a breakthrough in trade talks, which appears rather unlikely judging from the lack of headway in the negotiations thus far. Although volatility is likely to remain high, sterling/dollar could finish the year close to the 1.3000 psychological territory, especially if the dollar was to regain some of its shine throughout the year. On the flipside, in the less-likely scenario of material progress being achieved in the Brexit talks, Cable could surge and target the 1.3850 territory, marked by the lows of February 2016.

CHFJPY is Ready to Extend its Gains above the Descending Triangle?

CHFJPY has been trading within a descending triangle, which is a continuation pattern, since June 2017. In a daily timeframe, the price posted the third consecutive green day. The pair tested several times the upper band of the triangle so a daily close above the descending triangle and the 115.10 strong barrier could drive the price towards the next immediate resistance level at 115.70 and 116.45, which coincides with the 200-week simple moving average (SMA). On the reverse side, in case of a bearish move, CHFJPY could hit again the significant lower band at 112.50.

Remaining in the short to medium-timeframe, the MACD oscillator entered the bullish area after a long time below zero but is moving with weakening momentum, while the RSI indicator is holding in the positive territory and is sloping to the upside. It is worth mentioning that the three simple moving averages (50, 100 and 200) are flattening below the current market price as they don't give a clear signal during the creation of a pattern.

The pair has been developing within an ascending trendline over the last 1½ years in a medium-term chart and the anticipation is to continue the upward tendency.

GBPUSD Only Bullish Above 1.3400 Level

The British pound has reversed its fortunes against the U.S dollar, with price-action now testing the 1.3400 level, after declining towards the 1.3330 region on Tuesday. Technically, the GBPUSD pair has created a bullish triple-bottom pattern, indicating that buying demand is still strong above the 1.3300 mark. Overall buying interest above 1.3400 is limited at present, with the pair still struggling to break the 1.3418 weekly price-high. Traders now look an upcoming speech from Bank of England Governor Mark Carney, and the release of U.S Existing Home Sale figures for November.

The GBPUSD pair will remains intraday bullish while trading above the 1.3400 level. Intraday upside price-targets are currently 1.3418 and 1.3450.

Should price-action on the GBPUSD pair move below the 1.3400 level, further intraday selling towards 1.3360 and 1.3330 seems likely.

USDJPY Further Bullish Above 113.10

The U.S dollar has moved to a new weekly price-high against the Japanese yen, hitting 113.18 during the European trading session. Price-action on the pair is now testing the key 113.10 level, with buyers firmly in control whilst price holds above this key technical region. Overall Japanese yen weakness across a broad spectrum of currencies appears to be underpinning USDJPY strength. Traders now look to the Bank of Japan monetary policy decision, with economists expecting no major changes to Japanese fiscal policy at this meeting.

The USDJPY pair is further bullish while trading above the 113.10 level, buyers are now expected to push price towards the 113.40 and 113.70 resistance levels.

Should price-action move below the 113.10 level, sellers may push the USDJPY pair back towards the 112.70 and 112.30 support regions.

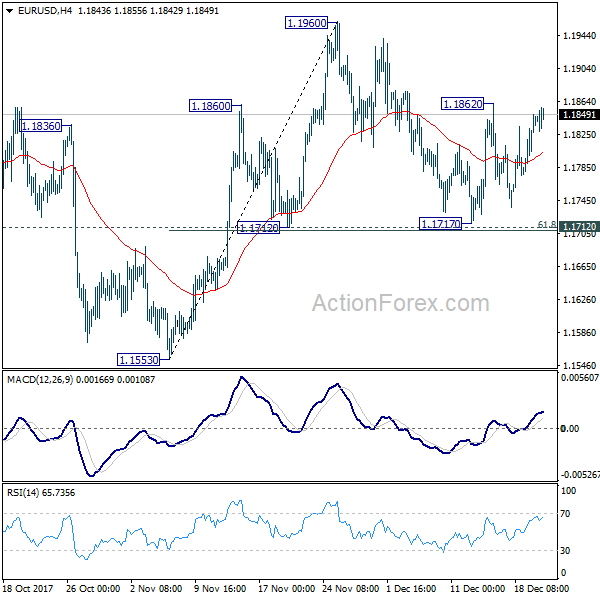

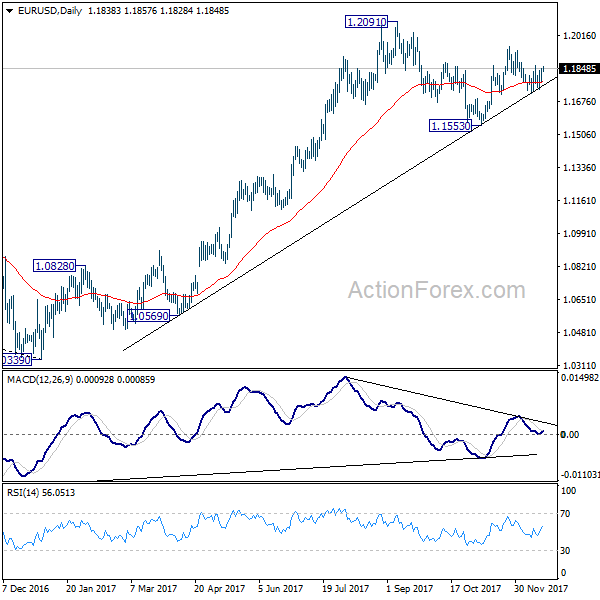

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1794; (P) 1.1821 (R1) 1.1866; More....

EUR/USD is stills staying below 1.1862 resistance and intraday bias remains neutral despite of the recovery. On the upside, above 1.1862 will revive near term bullishness. In such case, intraday bias will be turned back to the upside for 1.1960 resistance first. However, decisive break of 1.1712 cluster support (61.8% retracement of 1.1553 to 1.1960 at 1.1708) should confirm completion of rebound from 1.1553 at 1.1960. And in that case, deeper fall should be seen through 1.1553 to extend the medium term decline from 1.2091.

In the bigger picture, rise from 1.0339 medium term bottom is seen as a corrective move for the moment. Therefore, in case of another rally, we'd be expect 38.2% retracement of 1.6039 (2008 high) to 1.0339 (2017 low) at 1.2516 to limit upside and bring reversal. Meanwhile, sustained trading below 55 week EMA (now at 1.1435) will suggest that such medium term rebound is completed and could then bring retest of 1.0339 low.

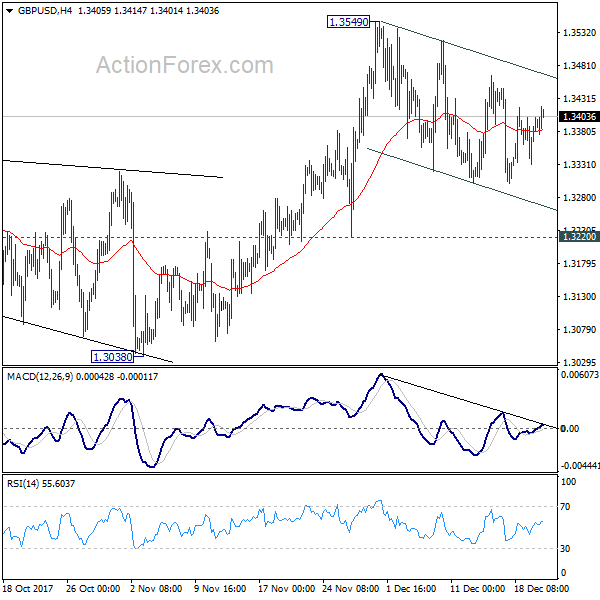

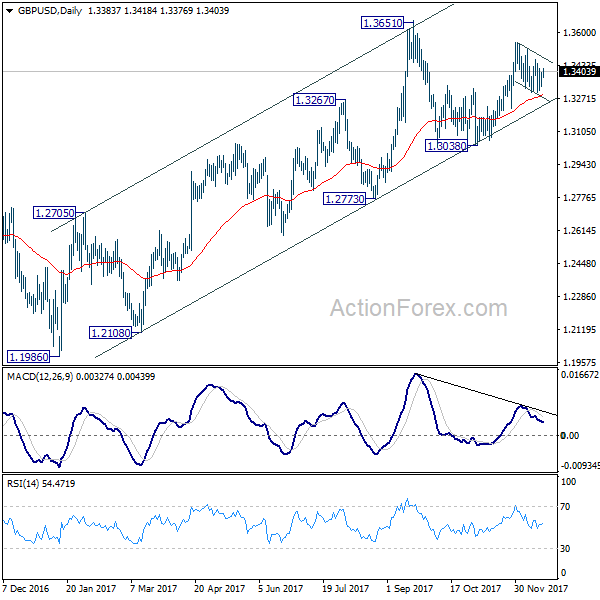

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3341; (P) 1.3372; (R1) 1.3414; More.....

GBP/USD is staying in the correction from 1.3549 and intraday bias stays neutral for the moment. As long as 1.3220 support holds, we'd favor another rise. Break of 1.3549 will target 1.3651 high next. Break there will resume medium term rally from 1.1946. However, firm break of 1.3220 will turn near term outlook bearish for 1.3038 key support level.

In the bigger picture, while the medium term rebound from 1.1946 low was strong, it's limited below 1.3835 key support turned resistance. As long as 1.3835 holds, we'd view such rebound as a correction. That is, we'd expect another leg in the long term down trend through 1.1946 low. However, sustained break of 1.3835 should at least send GBP/USD to 38.2% retracement of 2.1161 (2007 high) to 1.1946 (2016 low) at 1.5466.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9829; (P) 0.9853; (R1) 0.9873; More....

USD/CHF formed a temporary low at 0.9834 and intraday bias is turned neutral again. On the upside, above 0.9977 will resume the rebound from 0.9734 for 1.0037 resistance. On the downside, below 0.9834 will probably extend the correction from 1.0037 through 0.9734. But we'd expect strong support from 61.8% retracement of 0.9420 to 0.1.0037 at 0.9656 to complete the correction from 1.0037 and bring rebound.

In the bigger picture, range trading continues between 0.9420/1.0342. At this point, 0.9420 appears to be a strong support level. Therefore, in case of decline attempt, we don't expect a firm break of this level. Nonetheless, strong break of 1.0342 is also needed to confirm upside momentum. Otherwise, medium term outlook will stay neutral.

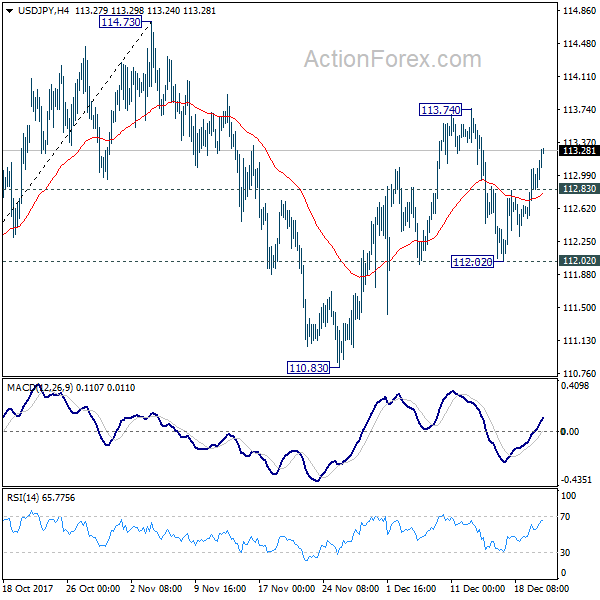

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.56; (P) 112.82; (R1) 113.13; More.....

Intraday bias in USD/JPY remains on the upside as rebound from 112.02 is on course to 113.74 resistance. Break will resume the rise fro 110.83 and target key resistance at 114.73 next. On the downside, below 112.83 minor support will turn intraday bias neutral first. But we'll continue to expect further rally ahead as long as 112.02 support holds.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.