Sample Category Title

Yen Weakens as German Yield Surges again, NZD/JPY to Watch as NZ GDP and BoJ Loom

Yen continues to trade as the weakest one as German yield rises for another day. At the time of writing, 10 year bund yield rose another 3 pts to 0.41%. USD/JPY rises on that and and breaks 113 handle. But the greenback is seen soft elsewhere. Developments regarding the tax plan were positive. Senate finally voted 51-48 to pass the bill. House passed the bill yesterday with 227-203 votes. But due to technical glitches, House will have to re-do it again today. But that should just be procedural. Elsewhere, Sterling is trading rather firm today despite growth forecast downgrade by IMF.

IMF downgrades UK growth forecasts

The International Monetary Fund downgrades UK growth forecasts, citing Brexit uncertainty. Growth for 2017 was lowered by 0.1% to 1.6% and it's expected to slow to 1.5% in 2018. IMF managing director Christine Lagarde said that UK is losing out to the rest of the world in terms of growth. And that's a result of "higher inflation, pressure on wages and incomes and delayed investment". She pointed to investment as a example as she noted, "if you look at investment alone, with 2.1% of GDP in investment, with the global economy as it is, and the space the UK economy has in that global economy, it should be rolling at 6%."

And she emphasized that a new trade deal with EU will help restore productivity in the UK and helps improve living standard. She said that "the shape of the new agreement with the EU will affect productivity performance through its implications for trade, investment and migration." And, "the higher are any new barriers to the cross-border flow of services, goods and workers, the more negative the impact would be." Also, "Brexit has the potential to reshape the structure of the UK economy. The impact will depend on the nature of the final agreement and may take many years to fully materialise."

EU: Brexit transition to end on December 31, 2020

EU just published its guidelines for the next phase of Brexit negotiation. In the guidelines, the so called "transitional period" will last until December 31, 2020. EU emphasized that during the negotiation for the implementation phase will still have to follow the rules, and UK cannot adopt an "a la carte" approach. And, "the transition period needs to be clearly defined and precisely limited in time." During the period, EU would expect UK to continue to follow EU law while European Court of Justice rulings will still apply.

NZD/JPY to look into NZ GDP and BoJ

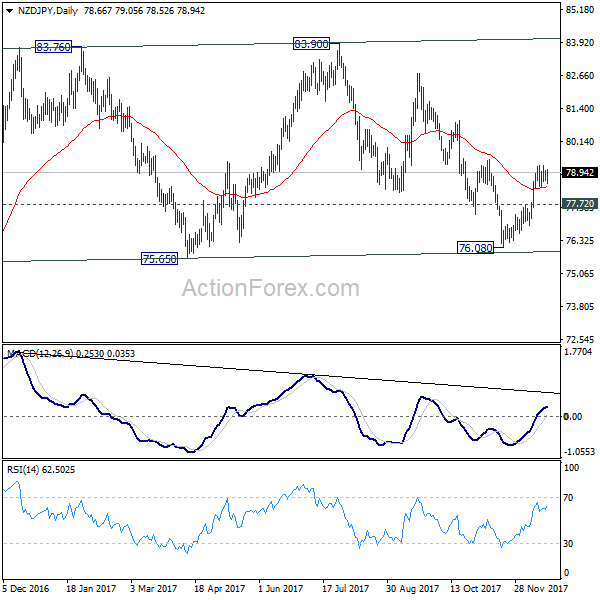

New Zealand Dollar has been under much pressure today after trade balance data. But comparing to the Japanese Yen while gives on global yield surge, it's rather steady. New Zealand GDP and BoJ rate decision will be the focuses in the upcoming Asian session. And some volatility could be seen in NZDJPY. The pair has been bounded in medium term range trading since hitting 83.76 back in January. With the strong rebound from 76.08, the fall from 83.90 should have completed. The sideway pattern could have completed with three waves down to 76.08. Near term outlook will stay cautiously bullish for a test on 83.90 resistance. Upside acceleration in the next move will raise the chance of range breakout. Nonetheless, break of 77.72 support will turn focus back to 75.65/76.08 support zone instead.

On the data front

Canada retail wholesale sales rose 1.5% mom in October. UK CBI reported sales rose to 20 in December. Eurozone current account surplus narrowed to EUR 30.8b in October. German PPI slowed to 2.5% yoy in November. Japan all industry index rose 0.3% mom in October. New Zealand trade deficit widened to NZD -1193m in November. New Zealand current account deficit narrowed to NZD -4.68b in Q3. From Australia, Westpac leading index rose 0.1% mom in November.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 112.56; (P) 112.82; (R1) 113.13; More.....

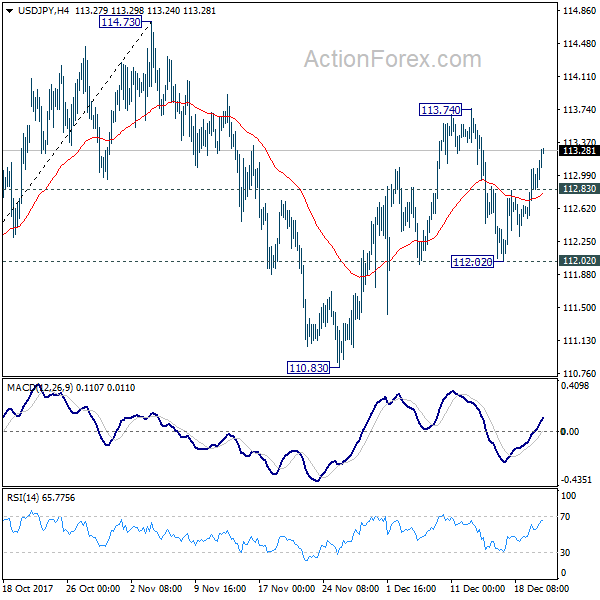

Intraday bias in USD/JPY remains on the upside as rebound from 112.02 is on course to 113.74 resistance. Break will resume the rise fro 110.83 and target key resistance at 114.73 next. On the downside, below 112.83 minor support will turn intraday bias neutral first. But we'll continue to expect further rally ahead as long as 112.02 support holds.

In the bigger picture, we're holding on to the view that correction from 118.65 is completed at 107.31. And medium term rise from 98.97 (2016 low) is going to resume soon. Sustained break of 114.73 should affirm our view and send USD/JPY through 118.65. However, break of 107.31 will dampen this view and extend the medium term fall back to 98.97 low.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 21:45 | NZD | Trade Balance Nov | -1193M | -550M | -871M | -843M |

| 21:45 | NZD | Current Account Balance Q3 | -4.68B | -4.22B | -0.62B | -0.51B |

| 23:30 | AUD | Westpac Leading Index M/M Nov | 0.10% | 0.13% | ||

| 04:30 | JPY | All Industry Activity Index M/M Oct | 0.30% | 0.30% | -0.50% | |

| 07:00 | EUR | German PPI M/M Nov | 0.10% | 0.20% | 0.30% | |

| 07:00 | EUR | German PPI Y/Y Nov | 2.50% | 2.60% | 2.70% | |

| 09:00 | EUR | Eurozone Current Account (EUR) Oct | 30.8B | 33.4B | 37.8B | 39.2B |

| 11:00 | GBP | CBI Reported Sales Dec | 20 | 20 | 26 | |

| 13:30 | CAD | Wholesale Sales M/M Oct | 1.50% | 0.50% | -1.20% | -1.10% |

| 15:00 | USD | Existing Home Sales Nov | 5.54M | 5.48M | ||

| 15:30 | USD | Crude Oil Inventories | -5.1M |

Swedish Krona Gains Following Central Bank Meeting; Kiwi Eyed ahead of GDP Data

Here are the latest developments in global markets:

FOREX: The dollar was not much changed versus other major currencies as trading is getting thinner ahead of the Christmas holidays and as the House of Representatives is anticipated to cast a final vote in favor of tax reforms later in the day.

STOCKS: European equities were heading lower, though losses were limited for the most part. At 1120 GMT, the pan-European Stoxx 600 was down by 0.2% and the blue-chip Euro Stoxx 50 traded lower by 0.4%. The UK's FTSE 100, German DAX and French CAC 40 were down by 0.2%, 0.25% and 0.3% respectively. Eurozone's exporter-heavy benchmarks, such as the DAX, were likely under pressure due to a rising euro as a result of rising German bond yields. Dow and S&P futures were up by 0.3%, while Nasdaq 100 equivalents traded higher by 0.35%.

COMMODITIES: Ahead of the weekly EIA report on US crude stocks, WTI was up by 0.3% at $57.73 a barrel and Brent crude was 0.05% down at $63.77. Gold gained 35% to trade at $1,266.08 per ounce, only marginally below its highest in two-weeks hit earlier in the day.

Day ahead: New Zealand GDP in focus while Swedish currency rises

The Swedish central bank maintained its benchmark rate at -0.50% and said it would reinvest coupons and cash from maturing bonds as it completed its meeting on monetary policy earlier today. The Riksbank left its projections on the timing of monetary policy normalization unchanged, expecting the repo rate to slowly begin rising in mid-2018, while adding that the outlook for inflation and economic activity was unchanged for the most part relative to the last time it met to set interest rates in October.

The Swedish currency surged within the first few minutes of the policy announcement with euro/stocky falling to a two-week low of 9.8592, and dollar/stocky touching 8.3158, this being a three-week low. The euro and the dollar later recovered somewhat, though they were still last down by 0.5% and 0.6% respectively versus the Swedish krona.

The Confederation of British Industry distributive trades survey's retail sales balance slid to +20 in December as expected. This compares to +26 in November. The survey projected robust expansion in UK retail sales as we're getting closer to Christmas, though retailers continue facing challenges in underlying trading conditions as consumers are seeing their purchasing power decline. Sterling experienced volatility following the release, initially gaining versus the dollar and the euro but soon after it gave up part of the gains.

On a relatively light day in terms of releases, the US will see the release of figures on November existing home sales at 1500 GMT. The pace of growth in sales is expected to ease relative to the preceding month. The greenback will be eyed for any surprise in the numbers that have the capacity to spur positioning on the currency.

Before that, loonie traders will be keeping an eye on Canada's October wholesale trade data due at 1330 GMT.

New Zealand third quarter GDP growth figures are scheduled for release at 2145 GMT. Analysts are projecting a slowdown in the pace of expansion during the quarter. The kiwi will be in focus as slowing economic activity has the capacity to delay the RBNZ's policy normalization plans.

A hearing on the November Financial Stability Report will be taking place at 1315 GMT and will among others feature BoE Governor Mark Carney and Deputy Governor Sam Woods.

Back in the US, the House of Representatives is widely expected to revote in favor of the tax reform bill – a second vote is needed due to procedural issues. The passage of the bill is already priced in by markets with limited, if any, movement expected to take place in relation to this.

In oil markets, the EIA's weekly report on, among others, US crude stockpiles, is due at 1530 GMT. The release has the capacity to move oil prices.

Global Stocks Mixed as Holiday Mood Kicks in

Global equity markets struggled for direction during Wednesday's trading session, with investors on the fence as activity continued to decelerate ahead of the upcoming Christmas holiday break.

Asian shares concluded on a mixed note on Wednesday as anticipation mounted ahead of a final vote on the US tax bill. In Europe, shares were lacklustre amid the limited appetite for risk and this could trickle back into Wall Street this afternoon. With global equity bulls and bears likely to be missing in action as the holiday mood kicks in, stock markets could remain subdued this week.

Sterling steady ahead of Carney testimony

Sterling nudged higher against the Dollar on Wednesday morning as market players awaited Bank of England Governor Mark Carney's appearance before Parliament.

Carney and Co. are scheduled to testify in front of Parliament's Treasury Select Committee this afternoon on the latest Financial Stability Report (FSR). With UK inflation rising to its highest level in almost six years and the uncertainty surrounding Brexit still weighing on sentiment, we could see some action in today's Parliamentary hearing. A heated discussion between Carney and the treasury committee over Brexit-related risks could punish the British Pound.

Taking a look at the technical picture, the GBPUSD edged higher on the daily charts with prices trading around 1.3380 as of writing. An intraday breakdown below 1.3350 could encourage a further decline towards 1.3300 and 1.3230, respectively. Alternatively, a breakout above 1.3440 may trigger a further incline towards 1.3520.

Commodity spotlight – Gold

Gold ventured higher during Wednesday's trading session with prices challenging $1267 amid a softer US Dollar.

With the recent market excitement from US tax reforms dwindling away and economic calendar relatively light, Gold could be driven by price action today. From a technical standpoint, the yellow metal remains somewhat bearish on the daily charts despite the impressive appreciation witnessed this week. The yellow metal is currently in the process of a technical bounce with firm resistance found at $1267. If prices fail to secure a daily close above $1267, then Gold may decline back towards $1250. Alternatively, a breakout above $1267 opens the gates back towards $1280.

USDJPY: Bullish, Eyes Further Upside Pressure

USDJPY: The pair closed higher on Tuesday following through higher on Wednesday. On the downside, support lies at the 113.00 level where a break if seen will aim at the 112.50 level. A cut through here will turn focus to the 112.00 level and possibly lower towards the 111.50 level. On the upside, resistance resides at the 113.50 level. Further out, we envisage a possible move towards the 114.00 level. Further out, resistance resides at the 114.50 level with a turn above here aiming at the 115.00 level. Its daily RSI is bullish and pointing higher suggesting more strength. On the whole, USDJPY faces further upside threats.

Canadian Dollar Remains Subdued, US GDP Looms

The Canadian dollar has shown little movement this week. Currently, USD/CAD is trading at 1.2852, down 0.22% on the day. On the release front, the US publishes Existing Home Sales and Canada releases Wholesale Sales. There are a host of key events on Thursday. Canada releases CPI and Core Retail Sales, and the US publishes Final GDP, the Philly Manufacturing Index and unemployment claims.

President Trump's gift-wrapped Christmas present is ready – almost. The Trump tax reform bill was passed in the House of Representatives and the Senate on Tuesday, but the bill is being sent back to the House for another vote on Wednesday due to a procedural requirement. The bill is expected to be ratified by the House and will then be sent to Trump to be signed into law. As expected, the congressional votes went along party lines, with the Senate narrowly approving the bill by a count of 51-48. This marks the first major overhaul of the US tax code in 30 years, and reduces corporate taxes from 35% to 21%. After failing to overturn Obamacare, the Republicans can finally chalk up their first legislative victory in the Trump administration, ahead of Congressional elections in 2018.

The US economy has performed well in 2017, and this has boosted Canada's economy as well. The US is expected to wrap up the year with a strong report card, with the release of Final GDP for Q3. Preliminary GDP posted an impressive 3.3% gain, and the markets expect Final GDP to be revised downwards to 3.1%, which still indicates strong economic expansion. The Federal Reserve wrapped up 2017 with a quarter-point hike, and another increase is widely expected at the January meeting. Strong economic numbers and this accelerated pace of rate increases bodes well for the US dollar.

CAC Dips on Soft Eurozone Current Surplus

The CAC index has recorded slight losses in the Wednesday session. Currently, the index is at 5370.30, down 0.23% on the day. On the release front, eurozone current account surplus dropped sharply to EUR 30.8 billion, well short of the estimate of EUR 33.4 billion. This was the smallest surplus since July. On Thursday, the US releases third quarter Final GDP.

President Trump will end 2017 on a high note, as his election pledge to implement major tax reform is on the verge of becoming law. The tax bill was passed in the House of Representatives and the Senate on Tuesday, but the bill is being sent back to the House for another vote on Wednesday due to a procedural requirement. The legislation is expected to be ratified by the House and will then be sent to Trump to be signed into law. As expected, the congressional votes went along party lines, with the Senate narrowly approving the bill by a count of 51-48. This marks the first major overhaul of the US tax code in 30 years, and reduces corporate taxes from 35% to 21%. After failing to overturn Obamacare, the Republicans can finally chalk up their first legislative victory in the Trump administration, ahead of Congressional elections in 2018.

It's a quiet week for economic indicators, and currency markets are generally quiet in the period ahead of Christmas. Still, investors should keep a close eye on French consumer spending, which will be released on Friday. Consumer spending was dismal in October, with a sharp decline of 1.9%, compared to the forecast of 0.0%. However, the markets are expecting a strong rebound for November, with an estimate of a 1.4% gain. Christmas shopping will likely translate into strong consumer spending numbers for December, which could boost fourth quarter economic growth and send the CAC to higher levels early in the New Year.

A strong US economy in 2017 has been good news for global stock markets, and the markets expect a thumbs-up report card on Thursday, with the release of Final GDP for Q3. Preliminary GDP posted an impressive 3.3% gain, and although Final GDP is forecast to be revised downwards to 3.1%, this would still indicate strong economic expansion. The Federal Reserve wrapped up 2018 with a quarter-point hike, and another increase is widely expected at the January meeting. Strong economic numbers and this accelerated pace of rate increases could send stock markets higher.

Will The Santa Rally Grind To A Premature Halt?

- Trump Set to Deliver Tax Reform Before Christmas;

- Sterling Higher as IMF Lowers UK Growth Forecasts;

- Bitcoin Dips Bought Again as Traders Eye $20,000.

US equity markets are poised to open a little higher on Friday, as we await the passage of tax reform through the House of Representatives giving Donald Trump his first major legislative victory since coming to office.

While it's debatable who the real beneficiaries of the bill will be, stock markets have clearly benefited in anticipation of it, with major corporations being among the big winners of the bill. With equity markets having risen more than 25% since Trump's election victory, at least in part due to his tax reform plans, it's likely that this is almost entirely priced in at this point so it will be interesting to see whether the rally can now be maintained until the end of the year, or whether the Santa rally will instead grind to a premature halt as investors lock in some profits.

It may be a while until we find out for certain who stands to really benefit from tax reform but it's interesting to see that the moves in the US dollar don't really reflect what we've seen in equities. I wonder whether this is a reflection of the perceived economic benefit of the bill and the impact, or lack of, it will have on inflation. If investors truly thought that there'll be a strong economic benefit – which has been strongly debated – I would expect the dollar to be reflecting this more.

The pound continues to trade a little higher on the day this morning, despite the fact that the IMF downgraded the country's growth forecast for this year and predicted slower growth again next. The downward revision comes as little surprise to anyone that's seen the data this year and the ongoing impact that a combination of slow wage growth and high inflation will have on the consumer.

It's no surprise that the IMF cited Brexit as being behind the UK's disappointing growth, claiming the data has justified its “gloomy” forecasts prior to the vote, with the body having been among those lambasted for their dire predictions. While forecasts of recessions now appear to have been over the top, it seems clear that over the next couple of years, low levels of growth are to be expected until more clarity on the future relationship is known and the inflationary impact of the pound's depreciation passes.

Bitcoin has rebounded from its earlier losses, with the crypto crowd seemingly undeterred by the 20% drop seen over the last few days. Once again traders are jumping at the opportunity to buy dips and Bitcoin on both the CME and CBOE is now trading in the green on the day, having been 5-10% lower earlier in the session. Traders clearly have their eye on $20,000, having stumbled at this level at the first time of asking and coming only a few weeks after $10,000 was surpassed for the first time.

DAX Dips Lower On Weak Eurozone, German Data

The DAX has inched lower on Wednesday, after losses in the Tuesday session. Currently, the index is at 13,177.50, down 0.28% on the day. On the release front, European indicators missed their estimates. German PPI slowed to 0.1%, shy of the estimate of 0.2%. This marked a 5-month low. As well, Eurozone Current Account Surplus dropped sharply to EUR 30.8 billion, well short of the estimate of EUR 33.4 billion. This was the smallest surplus since July. On Thursday, the US releases third quarter Final GDP.

President Trump's gift-wrapped Christmas present is ready – almost. The Trump tax reform bill was passed in the House of Representatives and the Senate on Tuesday, but the bill is being sent back to the House for another vote on Wednesday due to a procedural requirement. The bill is expected to be ratified by the House and will then be sent to Trump to be signed into law. As expected, the congressional votes went along party lines, with the Senate narrowly approving the bill by a count of 51-48. This marks the first major overhaul of the US tax code in 30 years, and reduces corporate taxes from 35% to 21%. After failing to overturn Obamacare, the Republicans can finally chalk up their first legislative victory in the Trump administration, ahead of Congressional elections in 2018.

The US economy has looked sharp in 2017, and is expected to wrap up the year with a strong report card, with the release of Final GDP for Q3. Preliminary GDP posted an impressive 3.3% gain, and the markets expect Final GDP to be revised downwards to 3.1%, which still indicates strong economic expansion. The Federal Reserve wrapped up 2017 with a quarter-point hike, and another increase is widely expected at the January meeting. Strong economic numbers and this accelerated pace of rate increases bodes well for the US dollar against the euro and other major rivals.

Coalition talks took a shift in Germany, as politicians struggle to form a new government. President Angela Merkel's conservative bloc suffered losses in the September election, and talks with smaller parties failed to break the political deadlock. Merkel has now shifted her efforts towards her previous junior coalition party, the Social Democrats (SDP). On Friday, the SDP voted to begin exploratory talks with Merkel, with a view to discussing substantive issues in January. Many SDP lawmakers want a more senior role for the SDP in any coalition, and the SDP will likely demand key portfolios in a new government. Despite the political uncertainty, the German economy continues to look very strong.

WTI Possible Double Top Breakout

The WTI has formed a bullish SHS pattern, and the price is struggling to break a double top that has been created by the pattern itself. A pullback within the POC zone 57.30-46 could reject the price again, and if we see a clear move above 57.76, then next target could be W H3 - 57.95 and 58.15 - D H5. If the price makes a 4h close above 58.00, then we could see the W H4 as the final target - 58.63. The full ATR projection also makes a confluence with the W H4 target should the price remain bullish

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

Technical Outlook: SPOT GOLD Extends Recovery But Risk Of Recovery Rally Stall Exists

Spot Gold remains supported and extends recovery on Wednesday, heading towards strong resistance at $1267 (200SMA/50% retracement of $1299/$1236 descend).

The yellow metal moved higher after Tuesday's action ended in Doji candle as the dollar remained soft after initial optimism over US tax overhaul faded.

Break above $1267 would trigger further retracement of $1299/$1236 descend and unmask key barriers at $1275 (Fibo 61.8%) and $1280 (base of thick daily cloud).

On the other side, 20/200SMA death-cross weighs and overbought slow stochastic warns of recovery stall.

Broken Fibo 38.2% level, former pivotal barrier, now acts as initial support, ahead of lower pivot at $1253 (sideways-moving 10SMA) which is expected to contain extended dips. The pace of recent rally would slow as volumes are expected to thin ahead of Christmas holidays.

Res: 1267, 1275, 1280, 1284

Sup: 1260, 1253, 1250, 1244