Sample Category Title

IMF backs BoJ’s gradual rate hikes, sees policy rate moving toward neutral by 2027

Nada Choueiri, deputy director of IMF’s Asia-Pacific Department and mission chief for Japan, stated that IMF remains “supportive” of BoJ’s current monetary policy course. She emphasized that rate hikes should be implemented in a gradual and flexible manner to ensure that domestic demand continues to recover.

Choueiri projected that BoJ’s policy rate could rise “beyond 0.5%” by the end of this year, with a longer-term path toward the “neutral level” by the end of 2027.

IMF estimates Japan’s neutral rate to be within a band of 1% to 2%, with a midpoint of 1.5%.

Also, IMF maintains an optimistic outlook for Japan’s economy, forecasting 1.1% GDP growth in 2025, supported by increasing wages and stronger consumer spending.

Given these projections, IMF expects BoJ to continue its tightening cycle in a controlled manner.

BoC’s Macklem warns tariff threats already weighing on confidence

Speaking at a conference in Mexico City, BoC Governor Tiff Macklem raised concerns over the economic uncertainty stemming from U.S. President Donald Trump’s tariff threats. He noted that "threats of new tariffs are already affecting business and household confidence, particularly in Canada and Mexico."

"The longer this uncertainty persists, the more it will weigh on economic activity in our countries," he warned.

Macklem stressed that central banks face a challenging task in managing the economic fallout. He explained that policymakers cannot counteract both "weaker output" and "higher inflation" simultaneously.

The challenge will be to assess the downward pressure on inflation from reduced economic activity while balancing it against the upward pressure from higher input costs and supply chain disruptions caused by tariffs.

Fed’s Logan sees rates on hold “for quite some time” even if inflation drops

Dallas Fed President Lorie Logan suggested at a BIS conference overnight that interest rates may remain on hold for "quite some time," even if inflation continues to move closer to the 2% target. She emphasized that a decline in inflation alone would not be a sufficient trigger for policy easing, as long as labor market conditions remain strong.

She argued that such a scenario would "strongly suggest that" interest rate is

already pretty close to neutral, "without much near-term room for further cuts".

Instead, Logan highlighted that signs of a weakening labor market or a slowdown in demand would be more relevant factors in determining when easing should begin.

Keeping Your Head When Everyone Else is Losing Theirs

Market reaction to US tariff news has been intense, and volatile. It pays to keep your head in the face of such volatility, but some of the repricing could be helpful.

If you think your newsfeed is wild, check out an intra-day graph of the exchange rate.

It was always obvious that the Trump administration would impose tariffs: they were a major plank of his campaign. The details matter, though, so financial market pricing has been sensitive to any news about specific tariff plans. The early targeting of the US’s nearest neighbours was a bit of a surprise and shows that US trade policy cannot be shoehorned neatly into a framework emphasising US–China rivalry, the way it could under Biden.

As is usually the case, policy uncertainty produces a ‘risk off’ tone in markets, resulting in a sell-off in the Australian dollar and other currencies, as investors pile into USD-denominated assets. And of course much of this reversed when the measures against Canada and Mexico were subsequently delayed. The unceasing flow of headlines shows up in market pricing, and this is likely to remain the case.

It’s all too easy to catastrophise about the disruptions to trade and global growth from escalating tariffs. While they can be disruptive, it is also important to recognise that countries and companies can adapt, respond, and route around constraints. If one country imposes tariffs on your exports, there are always other places you can sell them, perhaps at a lower price. As Westpac Senior Economist Mantas Vanagas points out today in a separate note, the scope to redirect trade is greater for a country like Australia that mostly exports commodities.

Some historical perspective is useful here. During the Asian Financial Crisis of the late 1990s, many observers were concerned about the loss of demand for Australia’s exports from the region. It turned out that much of this production was able to be redirected to entirely new destinations such as the Middle East. More recently, when China stopped all coal imports from Australia, our exports were again rerouted elsewhere, to markets that had previously bought coal from the other producer nations that were now selling to China.

Redirecting trade in this way does become harder when a product is designed to cater to the specific consumer tastes or regulations of one market – think certain kinds of seafood or medications – or where one country dominates global demand, as would be the case for iron ore. It is also harder when the affected goods are upstream parts of complex supply chains criss-crossing borders multiple times. This is a big issue for Canada and Mexico (and the US-based companies they deal with), much less so for Australia. And while – as a post-Brexit United Kingdom found – these connections can take a while to unpick and reconfigure from what were previously friction-free trading relationships, it is nowhere near as disruptive as a global supply chain disruption of the kind seen during the pandemic.

Another way economies adapt and reroute around trade disruptions is via the exchange rate. If US tariffs make other countries’ exports more expensive in the US, exchange rate depreciation can undo a lot of that apparent loss of competitiveness. Market responses to fears over the hit to growth from tariffs can therefore at least partly unwind that hit to growth, albeit at the cost of a bit more inflation outside the US. But this does require markets to react, and the sensitivity of this reaction can add volatility in a market that affects many parties.

Keeping your head when the markets are this volatile is a good plan, but ironically at some level, the US’s trading partners are better off if people do lose their heads a little. Recall that day-to-day fluctuations in exchange rates do not affect overall economic outcomes, but sustained movements can.

Another wrinkle is that market reactions to tariff developments do tend to push the USD to appreciate against other currencies, but this comes at a time that the USD is already richly valued. Various measures of the USD real effective exchange rate – covering the currencies of many trading partners and adjusting for relative inflation rates – show it at the highest levels it has been since the mid-1980s. Back then, the high level of the exchange rate caused considerable difficulties for US exporters. To address this, the major economies agreed to the Plaza Accord on exchange rate intervention to wind back the degree of overvaluation of the US dollar.

A similar predicament for US exporters can be envisaged this time around. As well as contending with an over-valued exchange rate as in the 1980s, their domestic cost base will increase in line with the inflationary impact of tariffs. While goods exports are only around 9% of US GDP, sheltering behind a tariff wall will not improve exporting firms’ situation. Eventually, the USD will need to depreciate, but history shows that this can take some years to work through.

The competing forces of in-the-moment reactions to tariffs and risk on the one hand, and correction of overvaluation on the other, could drive swings in exchange rates through a much wider range than the Australian dollar has seen over the past decade (the pandemic period excepted). If that does play out, it will definitely pay to keep your head through the volatility.

Cliff Notes: Some Promising Signs for the Consumer

Key insights from the week that was.

In Australia, updates on the consumer were constructive overall. Nominal retail sales lifted 1.4% during Q4 and prices were up 0.4%. Retail sales volumes therefore managed a gain of 1.0% in Q4, building on Q3’s 0.5% increase to be up 1.1% over 2024. That all states and retail categories gathered momentum into year-end not only highlights the breadth of the current upturn but also points to a delayed tax cut response beginning to come through. These findings were corroborated by the ABS’ new experimental measure of household spending (covering two-thirds of total household consumption compared to one-third for retail) which lifted 0.4% (4.3%yr) in December on strength in discretionary spending, particularly goods.

While these developments point to upside risks to our current Q4 household consumption forecast of 0.7%qtr, we are mindful that the uncertainty surrounding our forecast are two-sided. Evidence from card activity data and our Westpac Consumer Panel suggests the overall response to Stage 3 tax cuts has been underwhelming, with consumers seeking to rebuild savings buffers eroded over 2023 and 2024. Looking forward, the durability of the upturn is yet to be tested beyond the year-end sales period, which reportedly saw aggressive discounting. The latest edition of the Westpac Red Book discusses these themes in depth.

On housing, the latest CoreLogic data pointed to a broadening slowdown in price growth across the major capitals. Sydney and Melbourne continued to record declines in January with buyers constrained by affordability and supply. Perth, Adelaide and Brisbane meanwhile are gradually seeing annual price growth decelerate to low double-digit rates as demand and supply come into better balance. On new construction, the modest increase in dwelling approvals – driven by a bounce in high-rise units – masked a third consecutive monthly decline in private detached house approvals, raising questions over the pipeline’s persistence and breadth.

Before moving offshore, it is worth highlighting the downside surprise in December’s goods trade data, the surplus narrowing from $6.8bn to $5.1bn. Greater-than-usual monthly volatility looks to be at play, trade flows shifting, at least in part, in anticipation of tariffs being imposed by the US. Australia is not immune from global trade tensions, but an assessment of our direct and indirect trade with the US makes clear we are well positioned to minimise the net cost. In this week’s essay, Chief Economist Luci Ellis reflects on global developments in trade policy and the implications for markets.

Offshore, the pulse of key data was favourable overall, though policy makers continued to emphasise greater-than-usual uncertainty over the outlook.

In the US, the manufacturing PMI increased by 1.7 points to 50.9 points in January, its first expansionary read since October 2022. The gain was supported by strength in new orders, prices, production and, most notably, employment, up 4.9 points. President Trump’s promise to support US manufacturing investment and production is likely a factor here despite any windfall being a future prospect not a present reality. Notably, the average reading through President Trump’s first term exceeded that of both the Obama and Biden administrations by around 2 points. The non-manufacturing index meanwhile declined 1.2 points, although at 52.8 still points to expansion. Activity, new orders, inventories and prices saw a substantial decline while other measures saw tepid increases, including a 1 point increase in employment. All components except prices remain below their 5-year pre-COVID average, indicative of modest growth in the sector. Still to come tonight is the January employment report and 2024 annual revision for nonfarm payrolls. Available labour market detail continues to broadly point to balance between demand and supply, limiting risks to demand and inflation over the period ahead.

Across the Atlantic, the Bank of England cut rates by 25bps to 4.5% in a 7 to 2 vote, the dissenters preferring a 50bp cut. Growth forecasts were marked down out to Q1 2026, the economy now expected to grow 1.2%yr through 2025, down from 1.7%yr in the November projections. Mild upward revisions were made to the out years, though with the passage of time comes risk. Projections for headline inflation were lifted, particularly for 2025. This was attributed to higher energy prices and the government policies announced in the Autumn Budget 2024, with underlying inflation still anticipated to ease. The Monetary Policy Report also highlighted tariff uncertainty, with analysis showing downside risks to growth, due to the UK’s close relationship with the EU and a potential rotation in production from the UK to the US, and uncertainty for inflation. Looking back, the Bank also reviewed its estimates of neutral, the primary findings being that neutral is higher post pandemic but that uncertainty around estimates is high. A rate cut per quarter this year seems most probable, but if growth continues to disappoint, the pace of easing could be accelerated.

US Dollar Index (DXY) and the NFP Jobs Report: What to Expect

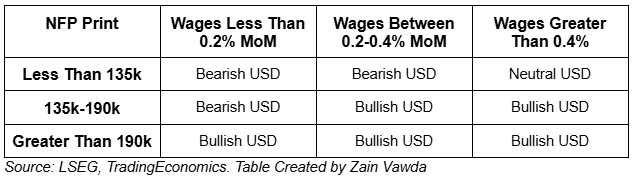

- Consensus forecasts predict an increase of 169,000 jobs, with the unemployment rate expected to remain at 4.1%.

- Strong numbers (over 190,000 jobs) could strengthen the dollar, while weak numbers (less than 135,000 jobs) could weaken it.

- (DXY) currently has support levels around 107.00, 106.13, and 105.76, and resistance levels at 108.00, 108.49, and 109.52.

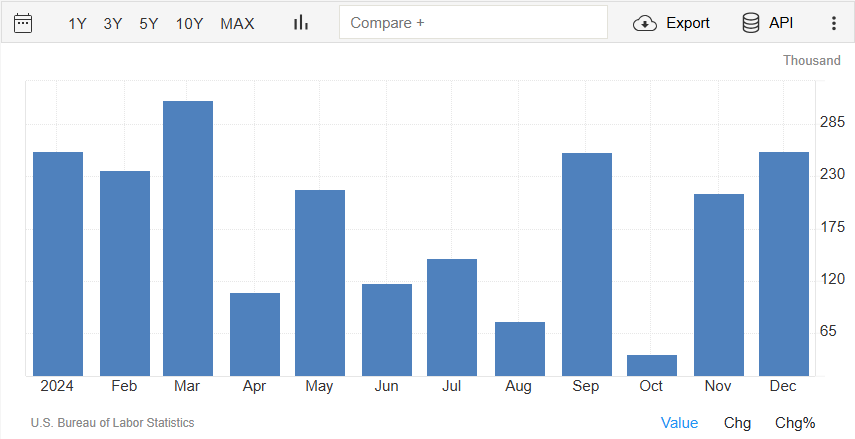

The US Bureau of Labor Statistics is set to release the non-farm payroll and jobs data for January 2025 on Friday, February 7th, 2025.

NFP Report Expectations

The consensus forecast for January’s non-farm payroll is an increase of 169,000 jobs, following a robust gain of 256,000 jobs in December 2024. Recent jobs data has been strong, with the US economy adding an average of 186,000 jobs per month in 2024. This suggests that the labor market remains healthy heading into 2025.

Source: TradingEconomics

The unemployment rate is expected to stay at 4.1%, and wages are predicted to grow by 0.3% this month (3.8% over the past year). However, job growth could be higher than expected, with estimates ranging from 175,000 to 225,000 new jobs.

As always the average hourly earnings measure will play a key role. Any significant deviation away from the 3.8-4% range here could see an uptick in inflation expectations. This would then have a knock on effect on Fed policy regarding rate cuts which could see the US Dollar experience some volatility.

There are challenges ahead with concerns that tariff uncertainty and growth worries may lead to a cautious approach toward hiring in the first part of 2025. It will be interesting to see if these concerns come to fruition and we see any cooling of the labor market and a drop in hiring.

The Current State of the US Labor Market

The US labor market is slowing down gradually. A December report showed over 500,000 fewer job openings, bringing the total to 7.6 million. Professional services and healthcare saw the biggest drops, while leisure and hospitality stayed strong.

Hiring has been slower, and layoffs are balancing out new hires in some industries. However, wages have stayed steady, with average pay growth at 3.9-4.0% over the past five months, showing that demand for workers is still solid.

There have been some mixed signs in recent data releases however, with metrics like the manufacturing and services PMI employment components, pointing to sustained hiring momentum. The ISM Manufacturing Employment Index recently climbed to 50.3, signaling expansion, while the ADP private payrolls report showed 183,000 jobs added in January.

Given the above and with the geopolitical and trade developments one may understand why tomorrow’s report is so crucial.

Potential Impact and Scenarios

The NFP report plays a big role in shaping the US Dollar Index (DXY) and overall market mood. If the report shows strong numbers, especially over 190,000 new jobs, the US dollar could strengthen, especially since it’s close to support levels around 107.50. But if the report is weak, with less than 135,000 jobs added or wage growth under 0.2%, markets may expect the Fed to cut rates more aggressively, which could weaken the dollar.

For stocks, strong job numbers might raise concerns about stubborn inflation moving forward, which could slow down market gains. On the other hand, weak job data could signal easier monetary policies ahead and more rate cuts thus stoking market optimism. .

Potential Impact on the US Dollar Based on the Data Released

Technical Analysis – US Dollar Index (DXY)

Looking at the US Dollar Index and bulls have failed to kick on this week as price action has now printed a lower high but no lower low has materialized yet. Will the jobs data help the DXY continue its recent malaise or will it give bulls renewed impetus to push on?

Immediate support rests at 107.00 before the 106.13 and 105.76 handles come into focus.

A move higher from here will need to break above the 108.00 handle before resistance at 108.49 and 109.52 come into focus.

US Dollar Index (DXY) Daily Chart, February 6, 2025

Source: TradingView (click to enlarge)

Support

- 107.00

- 106.13

- 105.76 (100-day MA)

Resistance

- 108.00

- 108.49

- 109.52

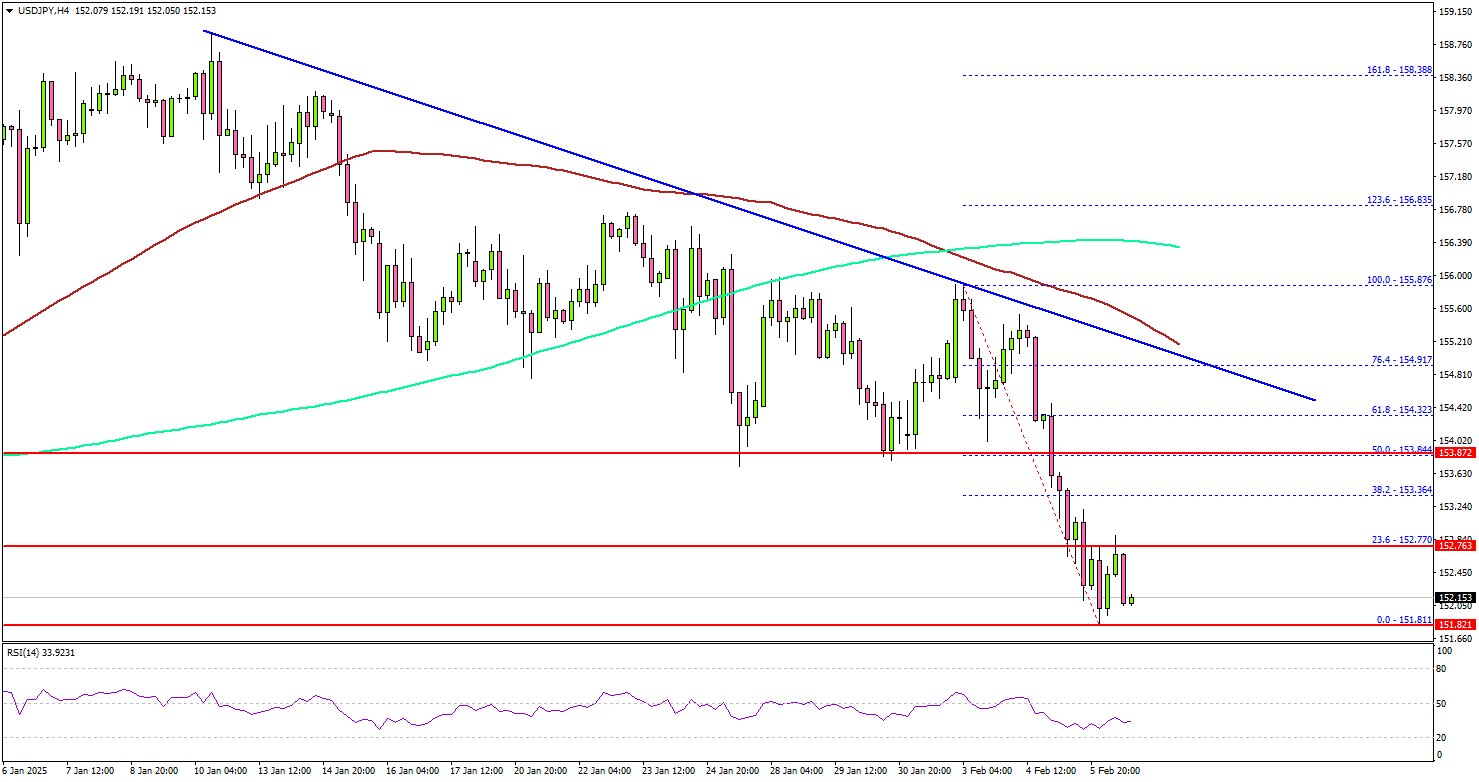

USD/JPY Extends Decline as Markets Brace for US NFP Data

Key Highlights

- USD/JPY started a fresh decline below the 155.50 support zone.

- A connecting bearish trend line is forming with resistance at 154.80 on the 4-hour chart.

- EUR/USD recovered above 1.0400 before the bears appeared again.

- The US nonfarm payrolls could change by 170K in Jan 2025, down from 256K.

USD/JPY Technical Analysis

The US Dollar started a fresh decline below 156.20 against the Japanese Yen. USD/JPY declined below 155.50 and 155.00 to enter a short-term bearish zone.

Looking at the 4-hour chart, the pair settled below the 154.20 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The bears seem to be in control and might aim for more losses.

On the downside, immediate support sits near the 151.80 level. The next key support sits near the 151.20 level. Any more losses could send the pair toward the 150.50 level.

On the upside, the pair seems to be facing hurdles near the 152.80 level. The next major resistance is near the 153.80 level. The main resistance is now forming near the 154.00 zone.

There is also a connecting bearish trend line forming with resistance at 154.80 and the 100 simple moving average (red, 4-hour). A close above the 154.80 level could set the tone for another increase. In the stated case, the pair could even clear the 155.50 resistance.

Looking at EUR/USD, the pair was able to recover above the 1.0400 resistance, but the bears are still active below 1.0450.

Upcoming Economic Events:

- US nonfarm payrolls for Jan 2025 – Forecast 170K, versus 256K previous.

- US Unemployment Rate for Jan 2025 - Forecast 4.1%, versus 4.1% previous.

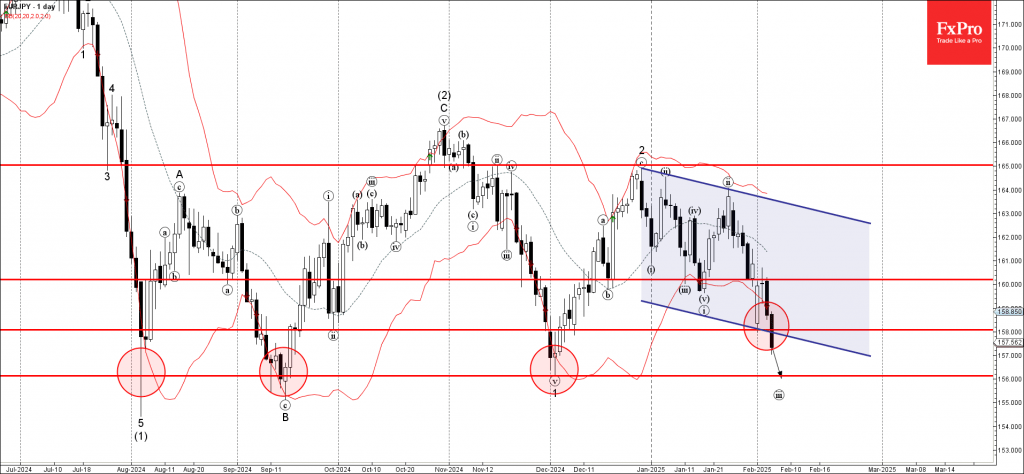

EURJPY Wave Analysis

- EURJPY broke support zone

- Likely to fall to support level 156.00

EURJPY currency pair today broke support zone between the support level 158.00 (which reversed the price at the start of this month) and the support trendline of the daily down channel from December.

The breakout of this support zone strengthened the bearish pressure on this currency pair, which accelerated the active impulse wave iii.

EURJPY currency pair can be expected to fall to the next support level 156.00 (which has been reversing the price from August).

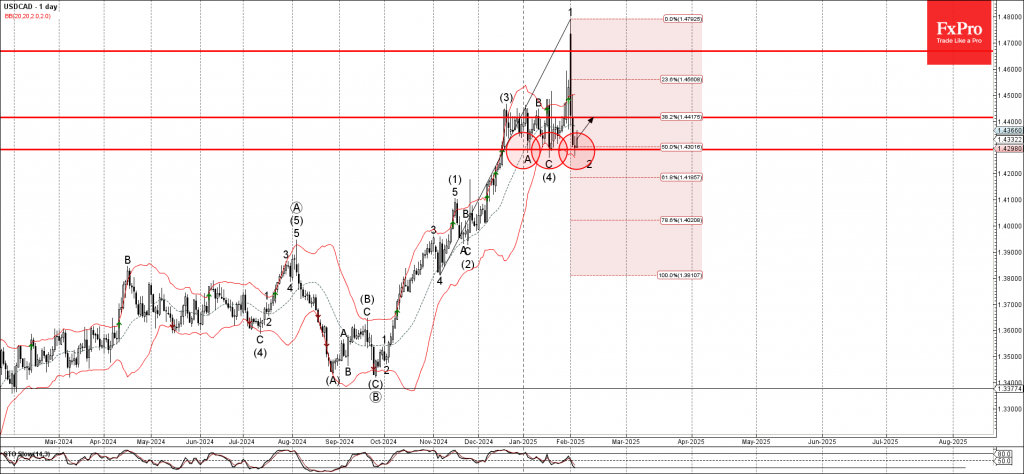

USDCAD Wave Analysis

- USDCAD reversed from the support zone

- Likely to rise to resistance level 1.4400

USDCAD currency pair recently reversed from the support zone between the pivotal support level 1.4290, which has stopped the previous corrections A, C , as can be seen below and the lower daily Bollinger Band.

The upward reversal from this support zone created the daily Japanese candlestick reversal pattern Doji, which stands near the 50% Fibonacci correction of the previous upward impulse from November.

Given the clear daily uptrend, USDCAD currency pair can be expected to rise to the next resistance level 1.4400.

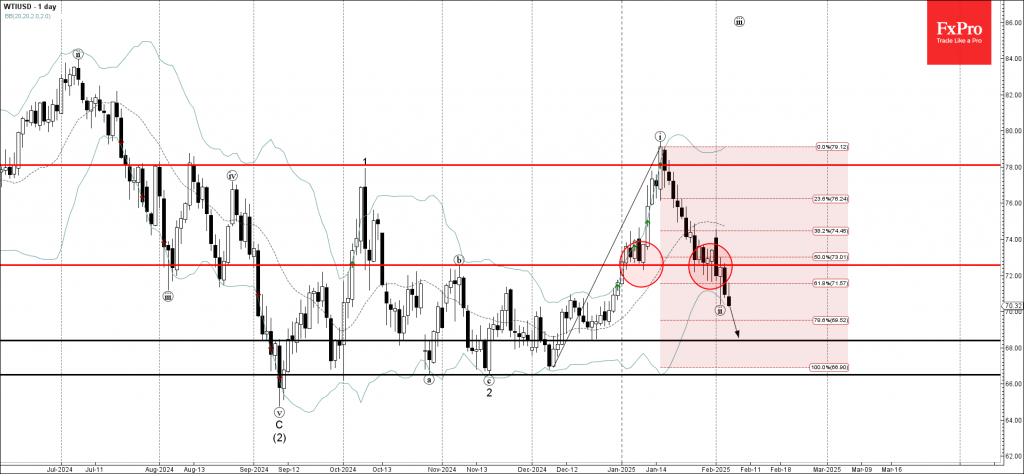

WTI Crude Oil Wave Analysis

- WTI Crude oil broke support zone

- Likely to fall to support level 68.00

WTI Crude oil recently broke the support zone between the support level 72.60 (which has been reversing the price from the start of January) and the 50% Fibonacci correction of the previous upward impulse from December.

The breakout of this support zone accelerated the active ABC correction ii from the middle of January.

WTI Crude oil can be expected to fall to the next support level 68.00 (former minor support from December.