Sample Category Title

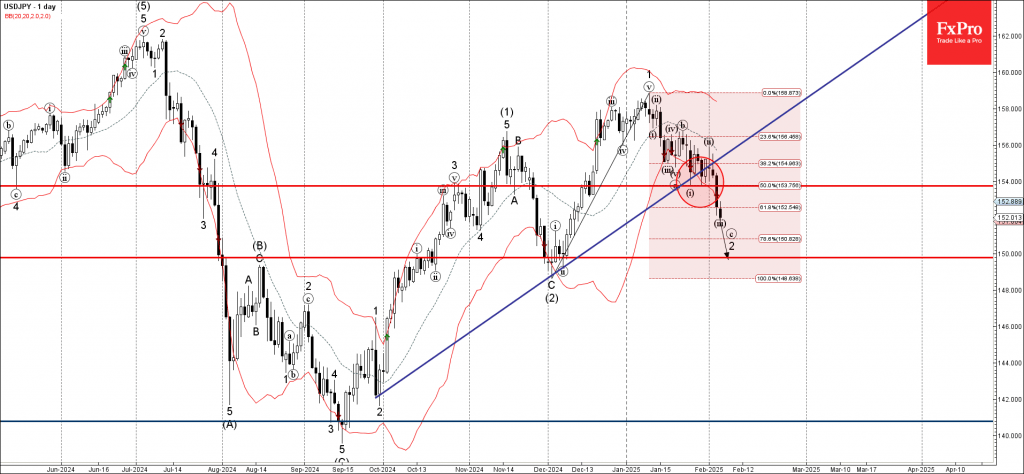

USDJPY Wave Analysis

- USDJPY under the bearish pressure

- Likely to fall to support level 150.00

USDJPY currency pair under the bearish pressure after the earlier break out of the support zone between the support level 154.00, support trendline from September and the 50% Fibonacci correction of the previous upward impulse from December.

The breakout of this support zone accelerated the c-wave of the active ABC correction 2 from the start of this year.

Given the strongly bullish yen sentiment seen across the currency markets today, USDJPY currency pair can be expected to fall to the next support level 150.00 (target for the completion of the active c-wave).

Bank of England Review – Gradual Quarterly Cuts Remain Our Base Case

- At today's monetary policy meeting the BoE cut the Bank Rate by 25bp to 4.50%, as was widely expected.

- In line with our view, the BoE delivered a dovish twist to its guidance with a dovish vote split, which triggered the immediate market reaction. Yet the statement and press conference revealed that BoE still favours a "gradual" and "careful" approach to easing monetary policy.

- Gilt yields tracked lower and EUR/GBP moved higher on the dovish vote split and communication.

As expected, the Bank of England (BoE) decided to cut the Bank Rate by 25bp to 4.50%. The vote split was 7-2 with the majority of members voting for a 25bp cut and Dhingra and Mann voting for a larger 50bp cut. This marks an important shift as Mann has been the most hawkish member of the MPC, voting for an unchanged decision the past many meetings. Mann stated that "a more activist approach at this meeting would give a clearer signal of financial conditions appropriate for the UK".

The BoE retained much of its previous guidance noting that "a gradual and careful approach to the further withdrawal of monetary policy restraint is appropriate" adding the word "careful" to reflect the higher degree of uncertainty. It likewise kept the wording that "monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further". In its updated projections, conditioned on a more hawkish implied Bank Rate path, the BoE revised growth significantly downwards while noting a high degree of uncertainty related to the trajectories of demand and supply in the economy. This will likely be key in determining the future path of interest rates for the MPC. Inflation was adjusted upwards in the near-term on the back of higher global energy costs and regulated price changes in the spring. Overall, we think the communication today supports our call of a continuous gradual approach to the cutting cycle. We expect the next 25bp cut in May with the Bank Rate ending the year at 3.75%. However, we highlight that the risk is skewed towards a swifter cutting cycle in 2025, given the clearly dovish bias within the MPC as evident from today's vote split and communication.

Rates. Gilt yields moved lower across the board on the dovish vote split. Markets price 7bp worth of cuts for March and 67bp by YE 2025. We highlight the potential for BoE to deliver more easing in 2025 than currently priced, expecting the next cut in May and a total of 100bp worth of easing in 2025.

FX. EUR/GBP moved higher on the announcement with the dovish vote split taking centre stage. The still cautious guidance delivered today highlights the more gradual approach of the BoE compared to European peers. More broadly, we expect EUR/GBP to move lower in the coming quarters driven by a relatively hawkish BoE, and a growth pickup in the UK relative to the euro area in 2025 and a USD-positive investment environment. The key risks are reignited debt concerns and a more forceful policy easing stance from the BoE.

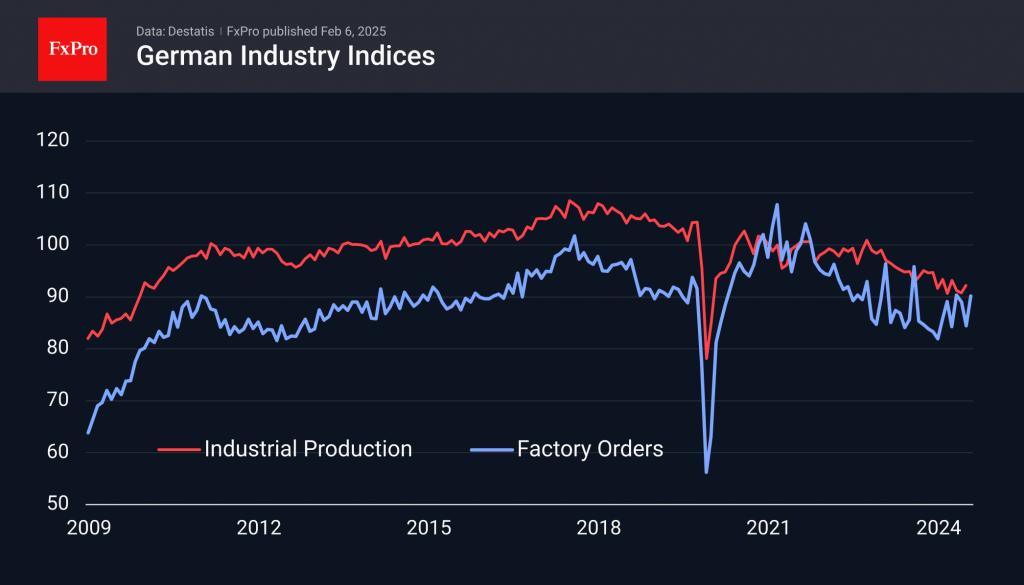

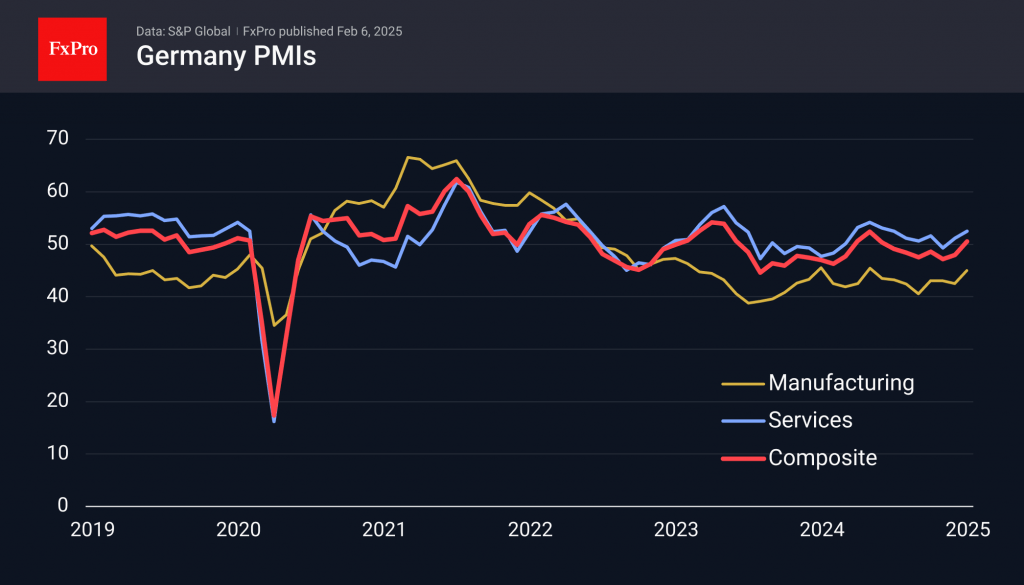

German Manufacturing: Growth is on the Way

German data is increasingly exceeding expectations, fuelling hopes for an improvement in the Eurozone economy.

The industrial orders index increased by 6.9% in December, offsetting November’s 5.2% decline. The year-on-year decline is 6.3% y/y. The low point of the current business cycle was reached in May last year, and since then, the orders index has risen by more than 10%, although it remains volatile.

Similarly, the industrial production index shows signs of reversal. It showed significant fluctuations at the end of last year but is now showing signs of stabilising.

Earlier in the week, the PMI index also showed positive revisions. The manufacturing index has remained below 50 for the past 31 months, but the composite index, thanks to the services sector, has entered growth after six months below the waterline.

The German economy is undergoing a transformation accompanied by an increase in the unemployment rate. Nevertheless, there are signs of improvement as companies are becoming more optimistic and the economy is showing signs of recovery. This could prove to be an important supportive factor for the euro in the coming weeks.

Sunset Market Commentary

Markets

The Bank of England today as expected cut its policy rate by 25 bps to 4.50%. The communication post the MPC decision contained some mixed signals, which we in the end see as tilting to the hawkish side. But first the dovish part of the narrative. The vote was 7-2. There was consensus on today’s rate cut. Two members (including Catherine Mann who was seen as being hawkish preferred to cut the policy rate to 4.25%. However, the underlying analyses from the monetary policy report was quite challenging from a monetary policy point of view. The BOE upwardly revised its inflation forecast while downgrading that for this year’s growth. Average 2025 growth was reduced to 0.75% from 1.5%. Growth for 2026 and 2027 was set marginally stronger at 1.5% (from 1.25%). Average inflation was upwardly revised to 3.5% from 2.75% for 2025 and is expected to decline gradually to 2.50% next year (from 2.25%) and 2.0% in 2027 (from 1.75%). Meeting the inflation target in 2027 is also seen conditional to a substantially higher implied policy rate path compared to the November forecast (+0.5 ppts for 2025 on an average of expected base rate of 4.2%, cycle low policy rate at 4.0%). To put it otherwise, potential growth that allows the economy to growth without creating inflation has declined in the wake of the government budget. In its policy assessment, the BOE states that ‘key indicators suggested progress on underlying disinflation in domestic prices and wages had generally continued. There had nevertheless been substantial upside news to the near-term outlook for headline CPI inflation, which was now expected to rise quite sharply in the near term, to 3.7% in 2025 Q3, owing in part to energy prices, before easing again’. The bank concludes that ‘a gradual and careful approach to the further withdrawal of monetary policy restraint was appropriate’. Despite the guarded BoE message, markets still slightly raised expectations on further easing throughout 2025 (two 25 bps steps fully discounted and about 75% of a third one). The message from higher 2025 inflation and lower actual and potential growth is an obvious negative for sterling. EUR/GBP already rose in the run-up to the meeting to test the 0.8375 area after the decision (currently 0.8365 from an open near 0.832). The established 0.822/0.8475 trading range for now remains firmly intact.

News & Views

Swedish January inflation smashed estimates, including those from the central bank. Headline CPI was flat compared to the -0.6%M/M forecasted, raising the yearly figure from 0.8% to 1%. The Riksbank’s preferred CPIF gauge accelerated 0.4% m/m, defying expectations for a 0.3% decline and picking up from December’s 0.3%. The y/y measure as a result jumped north of 2% again for the first time in eight months. The Riksbank had penciled in 1.8% in December. Prices ex. energy (0.2% m/m) soared to 2.7% from 2%. The Riksbank last month cut the policy rate from 2.5% to 2.25% and signaled it could be the final one. The meeting minutes released earlier this week revealed governor Thedeen was even surprisingly explicit about it, saying “the rate has probably been lowered sufficiently”. Previous cuts are now expected to usher in an economic recovery. Markets were not so certain and still expected one more reduction later this year. Today’s CPI numbers upended that thinking. Odds for another cut slumped from 100% to around 60% currently. The Swedish krone’s recent strong performance enters its fourth day. EUR/SEK currently trades around 11.32 compared to 11.5 at the beginning of the week..

The Czech Statistical Office for the first time released a flash CPI estimate for January. Inflation rose a faster-than-expected 1.3% m/m to be up 2.8% y/y (down from 3% in December). The upside surprise came on the account of food prices (5% m/m). Core gauges (ex. energy & food) increased by 0.6% m/m and topped the upper bound of the central bank’s 2% +/- 1ppt tolerance range. Services inflation (1% m/m) eased from 5% y/y to a still-elevated 4.7%. This is one of the key inflation risks for the central bank but that didn’t prevent it from cutting the policy rate from 4% to 3.75% shortly after. The move was widely expected. CNB policymakers including governor Michl flagged the move well in advance. KBC Economics expects one more additional cut, to a neutral level of around 3.5%, but sees risks tilted to the downside. These relate to the German economy (on which Czech exports heavily depend) as well as the (indirect) impact of potential US tariffs. The Czech crown appreciates against EUR today. EUR/CZK remains trapped in a tight sideways trading range from a broader perspective.

GBPCAD Technical Analysis

The USDCAD pair is seeing a slight increase on Thursday, trading around 1.4345 after bouncing from a two-week low of 1.4270. The US Dollar has regained some strength after three days of losses while falling oil prices are putting pressure on the Canadian Dollar. However, the US Dollar’s gains remain limited as traders expect the Federal Reserve to ease the policy further. On the technical side, the pair is facing key support near 1.4260, and a drop below this level could trigger further declines toward 1.4200. On the upside, resistance is near 1.4400, and a breakout above this level could push prices higher toward 1.4500.

GBPCAD – D1 Timeframe

The daily timeframe chart of GBPCAD shows the price already taking off from the supply zone at the tip of the SBR pattern and the 88% Fibonacci retracement level. However, the price created a large momentum candle, indicating the likelihood of a fair value gap within the impulse candle. Based on this, we will check the lower timeframe chart for details of the FVG, which should provide room for a bearish continuation entry.

GBPCAD – H4 Timeframe

The 4-hour timeframe chart of GBPCAD reveals the FVG area within the daily momentum candle and that the FVG region overlaps the 76% Fibonacci retracement level. The target for the bearish price action is the last low, as seen on the chart.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.74432

- Invalidation: 1.82096

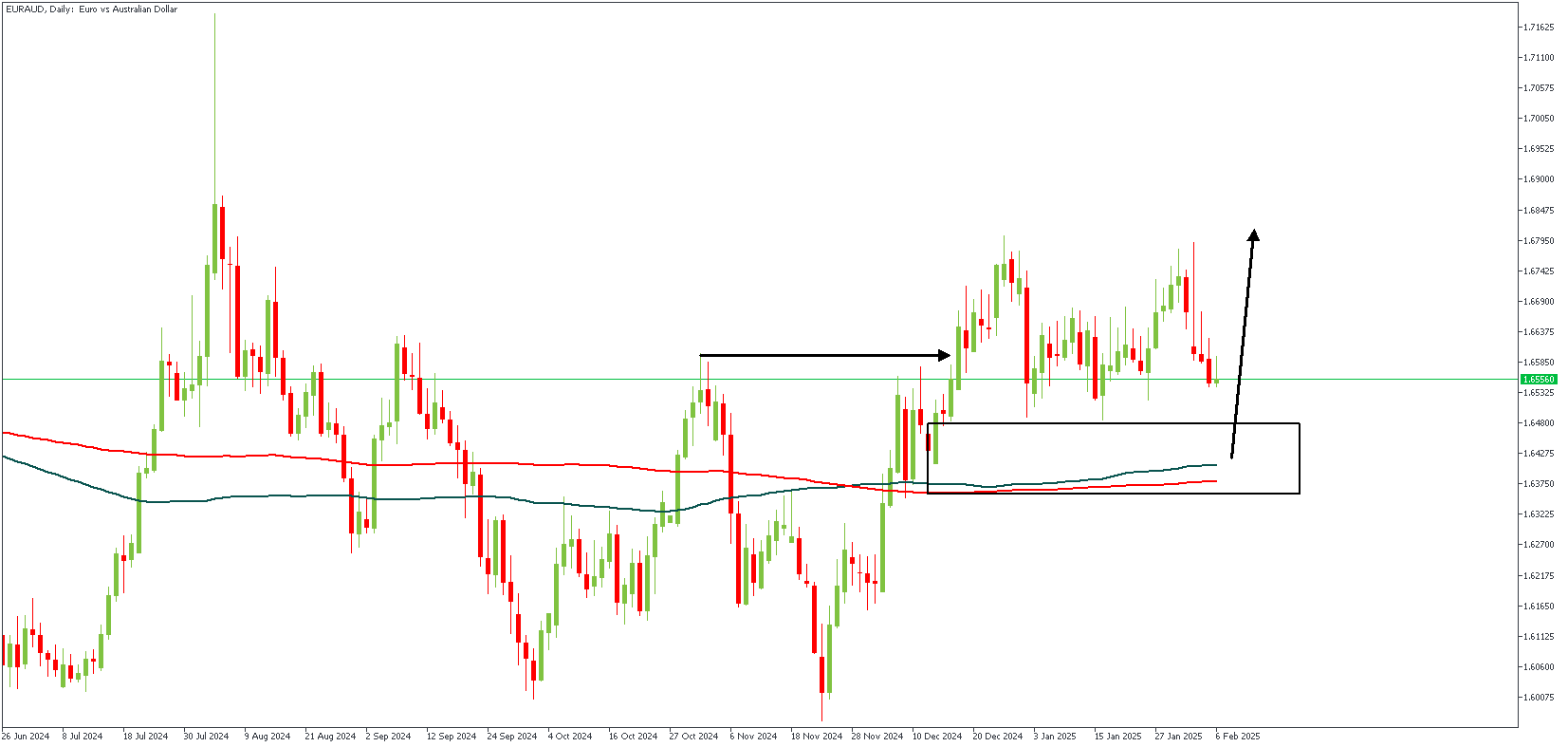

EURAUD Technical Analysis

EURUSD struggles to stay above 1.0400 on Thursday after gaining in the previous two days. The 4-hour chart shows the RSI falling below 50, signaling weakening bullish momentum, while the pair hovers around 1.0350-1.0360, where key technical levels meet. If EURUSD drops below this zone, further declines toward 1.0300 and 1.0250 could follow. On the other hand, resistance is seen at 1.0400, with potential gains extending to 1.0440 and 1.0500 if buyers regain control. Traders are closely watching US jobless claims and labor cost data for further direction, though market moves may remain limited ahead of Friday’s key Nonfarm Payrolls report.

EURAUD – D1 Timeframe

On the daily timeframe chart of EURAUD, the recent structure break is highlighted by the horizontal arrow, and the drop-base-rally demand zone is highlighted by the rectangle. The bullish array of the moving averages on the daily timeframe chart adds some confluence in favor of the bullish sentiment.

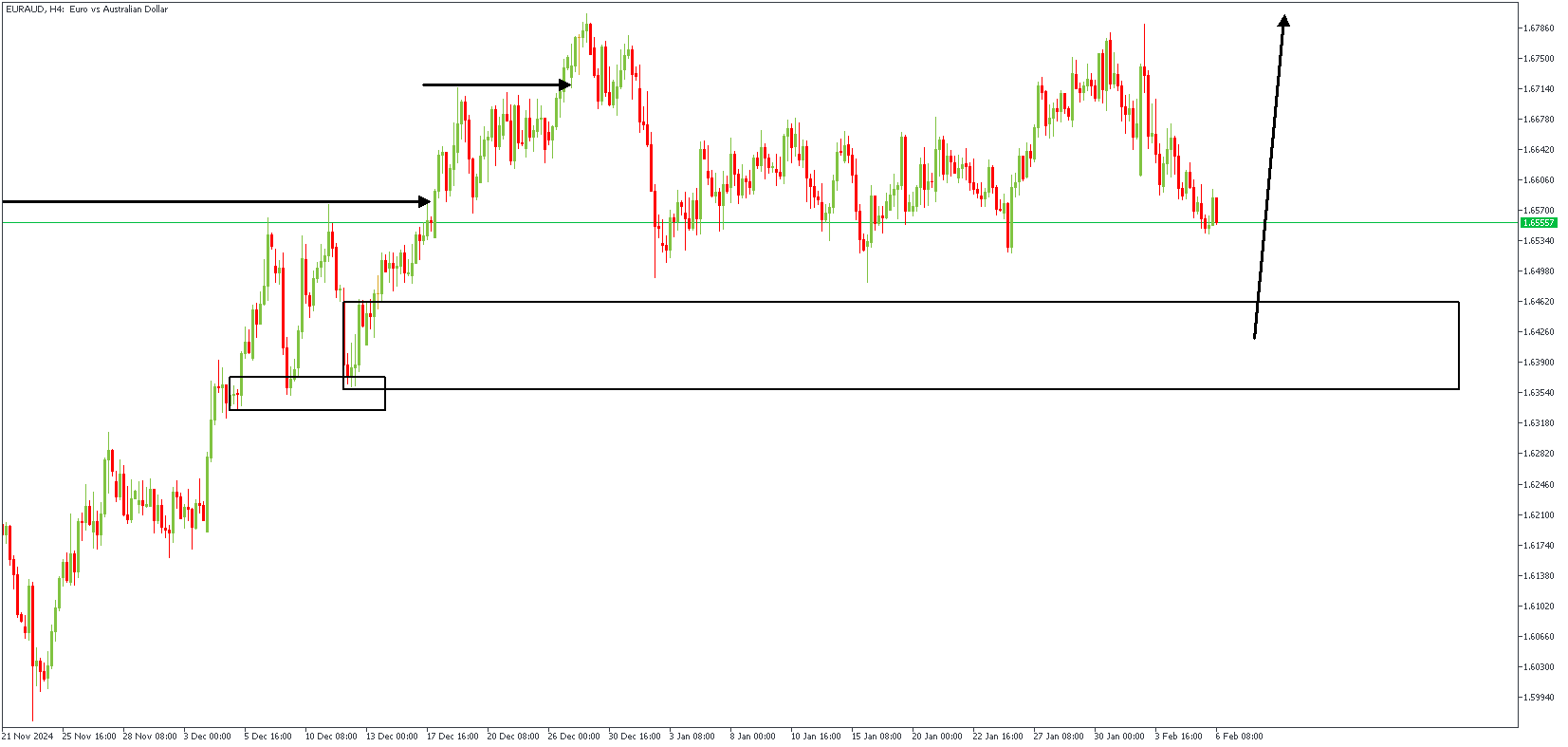

EURAUD – H4 Timeframe

On the EURAUD 4-hour timeframe chart, we see the SBR pattern currently playing out, with the demand zone just below the liquidity area. The conclusion mainly favors the bull by comparing this with the daily timeframe price action.

Analyst’s Expectations:

- Direction: Bullish

- Target: 1.67943

- Invalidation: 1.62855

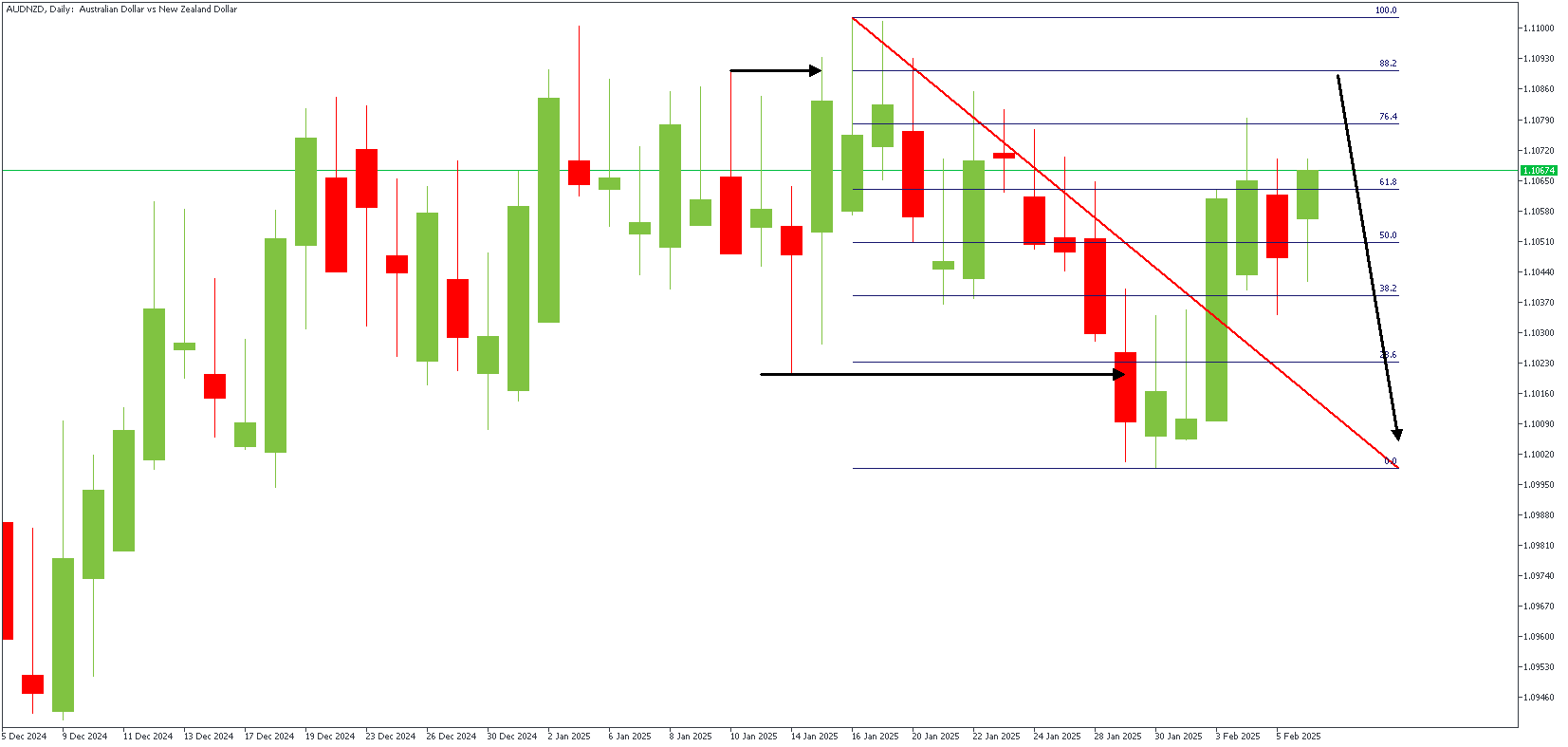

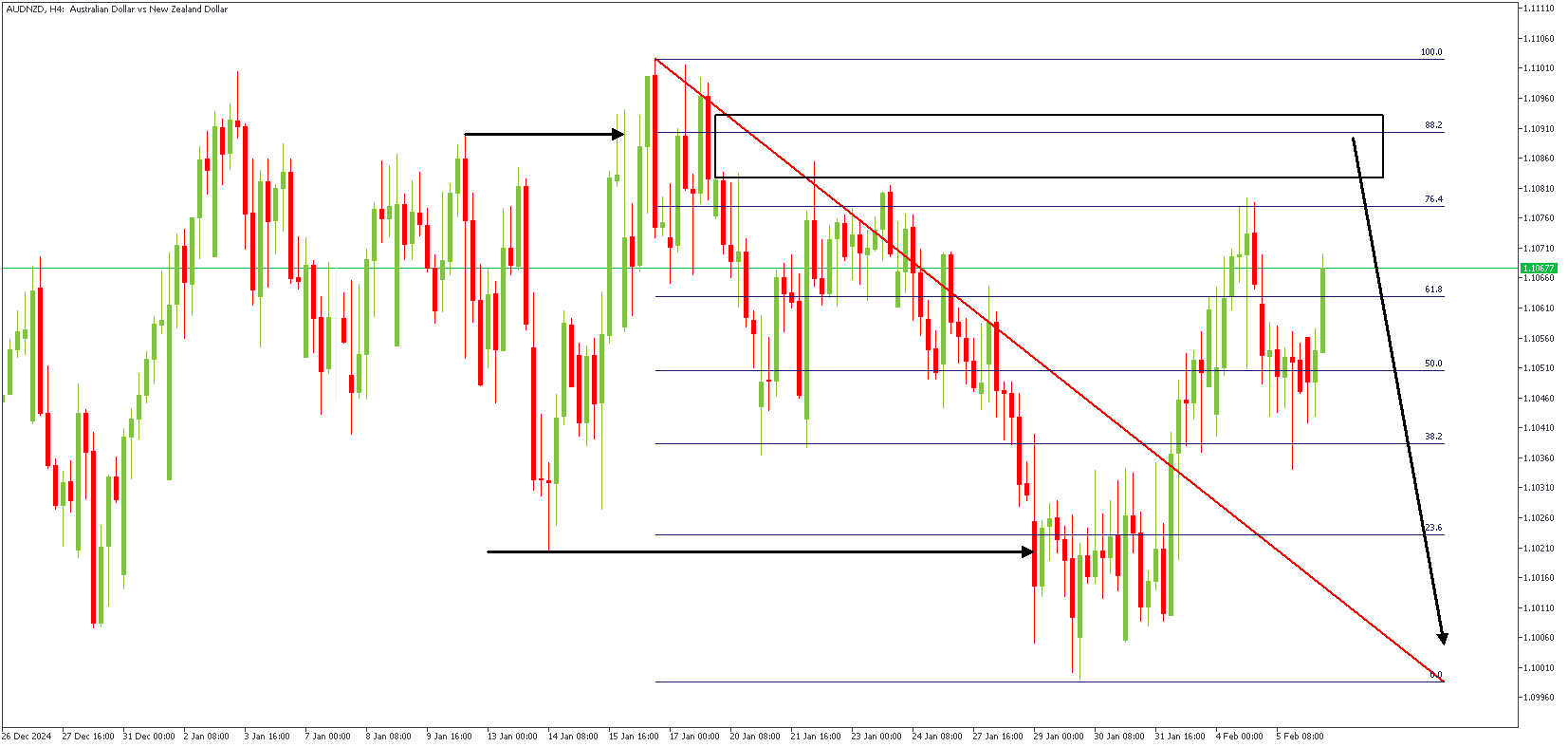

AUDNZD Technical Analysis

The Australian Dollar (AUD) is gaining strength against the US Dollar (USD), pushing AUDUSD higher after recently hitting its lowest level since April 2020. However, traders should be cautious, as key support sits at 0.6087, while resistance is near 0.6330. The US Dollar has weakened for three straight days, partly due to uncertainty around new tariffs proposed by President Trump. Meanwhile, Australia’s inflation data suggests the Reserve Bank of Australia (RBA) may cut interest rates soon, which could limit further AUD gains. Looking ahead, traders will watch economic data from both Australia and China to determine the Aussie’s next move.

AUDNZD – D1 Timeframe

Following the sweep above the previous high on the Daily timeframe chart of AUDNZD, we saw the price dip lower to break the previous low, resulting in an SBR pattern. The ongoing bullish retracement is approaching 76% of the Fibonacci retracement tool in preparation for bearish momentum.

AUDNZD – H4 Timeframe

On the 4-hour timeframe chart of AUDNZD, we see the drop-base-drop supply zone near the tip of the SBR pattern overlapping the 88% Fibonacci retracement level, with an area of liquidity sitting nearby. The expectation from all these confluences is a bearish outcome.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.10154

- Invalidation: 1.11046

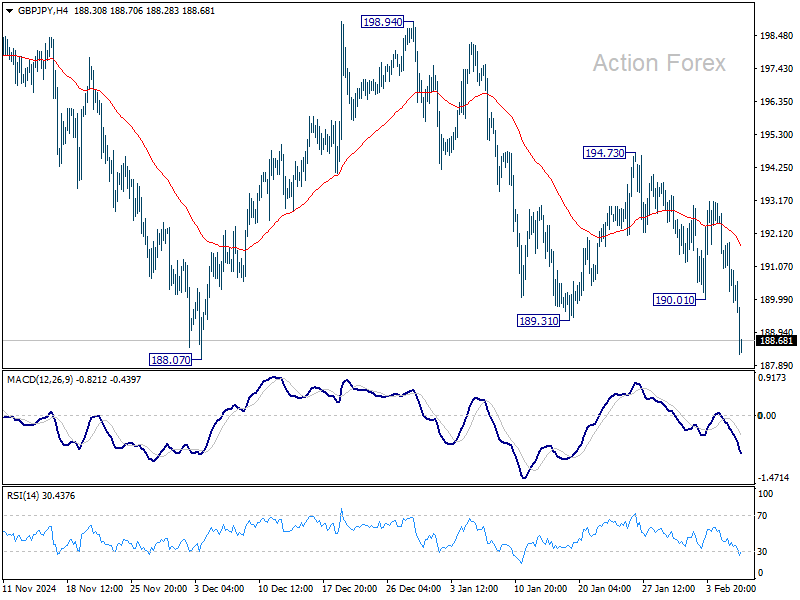

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 189.81; (P) 191.31; (R1) 192.31; More...

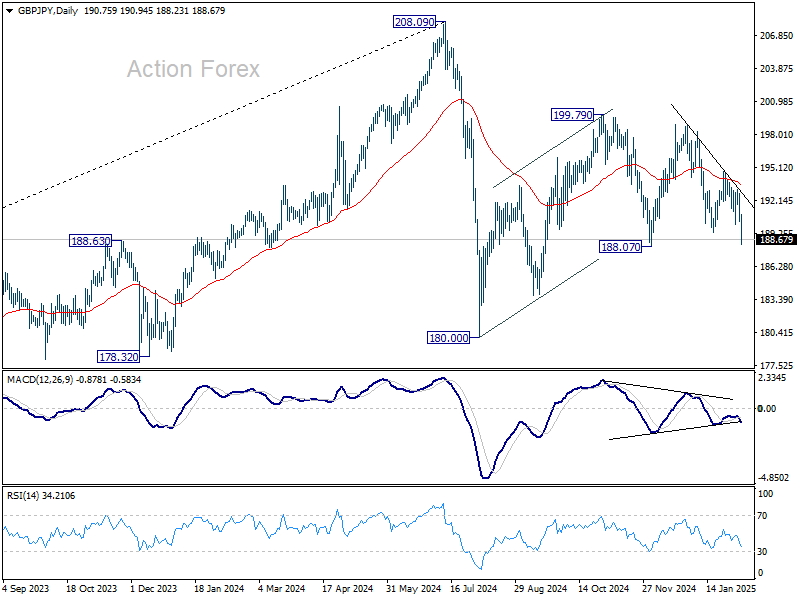

GBP/JPY's fall from 198.94 resumed by breaking through 189.31 support and intraday bias is back on the downside. Current development argues that corrective pattern from 180.00 might have completed. Break of 188.07 support will solidify this case and target a retest on 180.00. On the upside, though, above 190.01 support turned resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

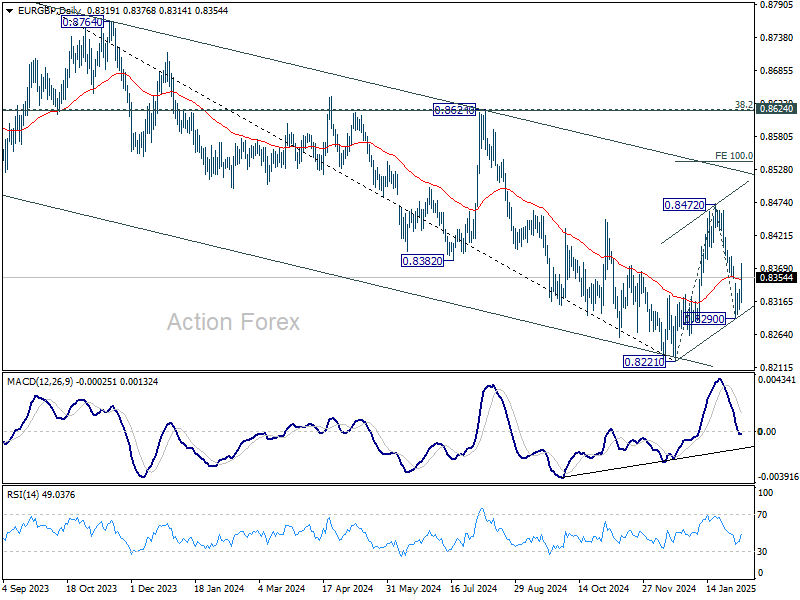

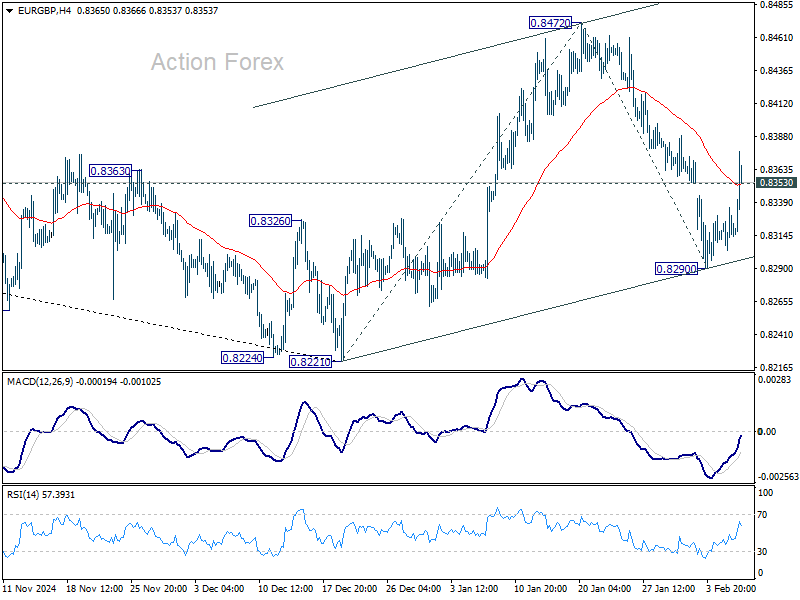

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8303; (P) 0.8320; (R1) 0.8335; More...

EUR/GBP's break of 0.8353 resistance argues that fall from 0.8472 has completed at 0.8290. Intraday bias is back on the upside for 0.8472 resistance. Firm break there will resume the rebound from 0.8221. On the downside, break of 0.8290 will target a retest on 0.8221 low.

In the bigger picture, a medium term bottom should be in place at 0.8221, just ahead of 0.8201 key support (2022 low). Sustained trading above 55 W EMA (now at 0.8442) will pave the way to 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621), even just as a correction to the down trend from 0.9267 (2022 high). But still, medium term outlook will be neutral at best as long as 0.8621/4 holds.