Sample Category Title

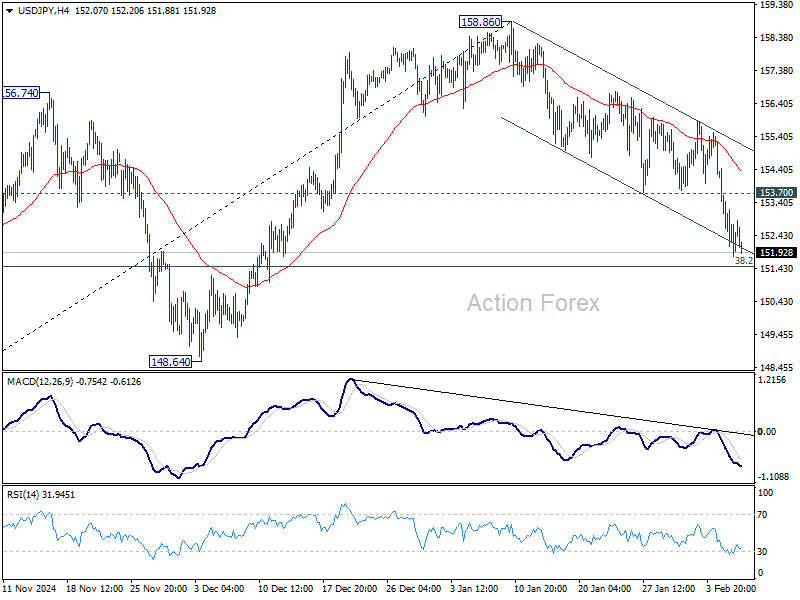

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 151.66; (P) 153.06; (R1) 154.00; More...

Intraday bias in USD/JPY remains on the downside as fall from 158.86 is in progress. Strong support is still expected from 38.2% retracement of 139.57 to 158.86 at 151.49 to contain downside. On the upside, firm break of 153.70 minor resistance will turn intraday bias back to the upside for rebound. However, sustained break of 151.49 will raise the chance of bearish reversal.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

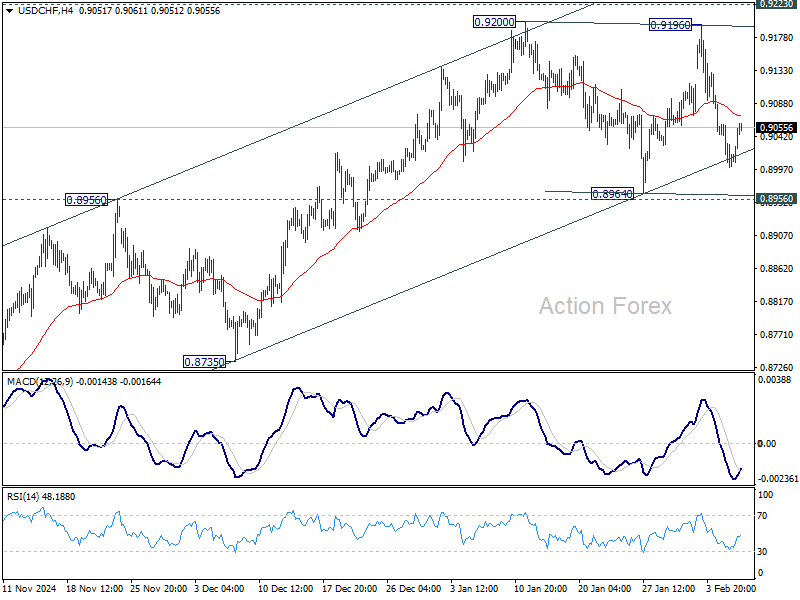

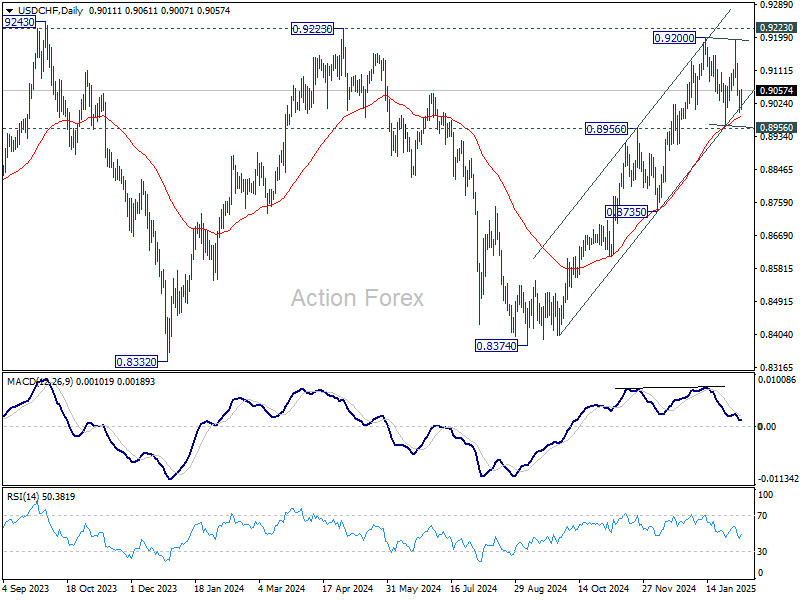

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8992; (P) 0.9028; (R1) 0.9054; More…

USD/CHF is staying in consolidation from 0.9200 and intraday bias stays neutral. Outlook will remain bullish as long as 0.8956/64 support holds. Firm break of 0.9200/9223 will resume the whole rally from 0.8374 and carry larger bullish implication. However, sustained break of 0.8964 will complete a double top reversal pattern, and turn bias to the downside for deeper decline.

In the bigger picture, decisive break of 0.9223 resistance will argue that whole down trend from 1.0342 (2017 high) has completed with three waves down to 0.8332 (2023 low). Outlook will be turned bullish for 1.0146 resistance next. Nevertheless, rejection by 0.9223 will retain medium term bearishness for another decline through 0.8332 at a later stage.

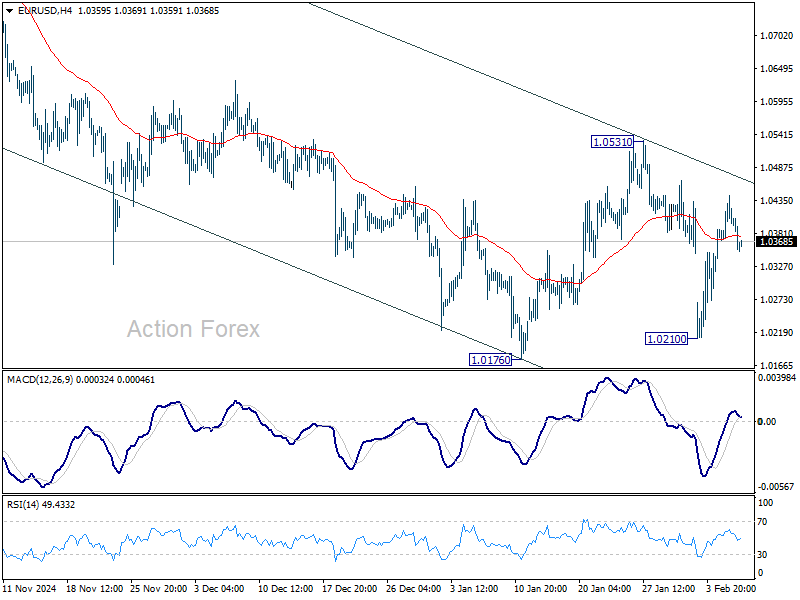

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0368; (P) 1.0405; (R1) 1.0440; More...

Intraday bias in EUR/USD stays neutral as consolidation from 1.0176 continues. Strong resistance is expected from 1.0531 to limit upside. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, sustained break of 1.0531 will rise the chance of bullish reversal and turn bias back to the upside for stronger rally.

In the bigger picture, immediate focus is back on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, strong support from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

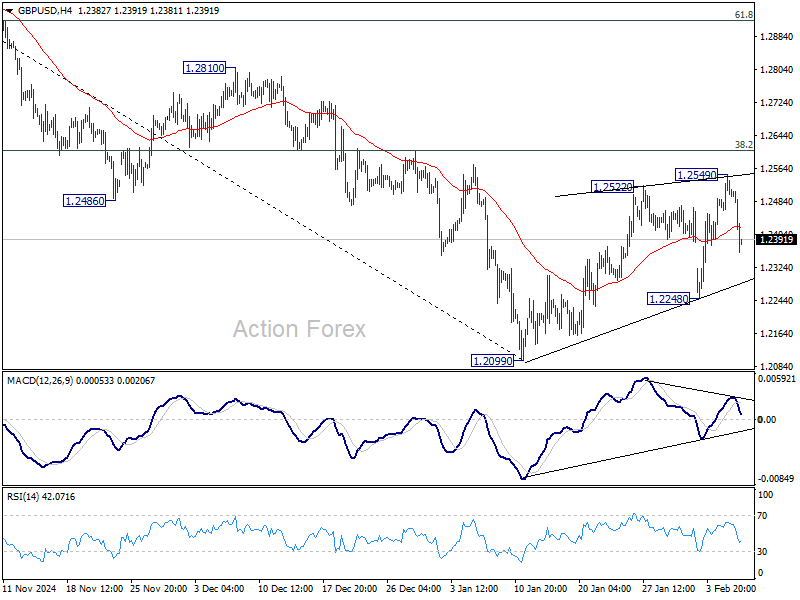

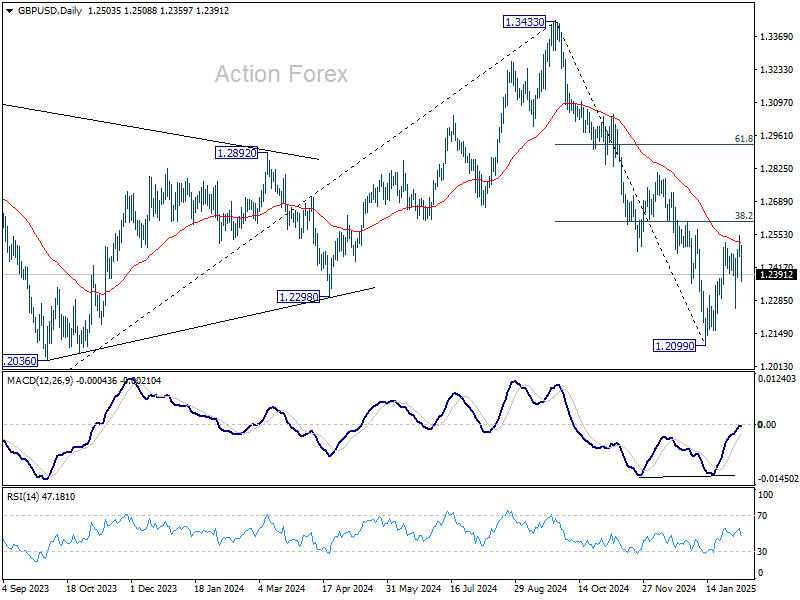

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2462; (P) 1.2506; (R1) 1.2548; More...

GBP/USD dips notably today but stays above 1.2248 support and intraday bias remains neutral. While corrective rebound from 1.2099 could still extend, upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 first. Firm break there will resume whole decline from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

Sterling Tumbles on BoE’s Dovish Rate Cut

The British Pound weakened significantly after BoE delivered a 25bps rate cut. The policy decision was more dovish than anticipated, primarily due to the unexpected shift in the MPC voting split. Catherine Mann, previously one of the most hawkish members of the committee, reversed course and joined Swati Dhingra in voting for a more aggressive 50bps cut.

Adding to the bearish sentiment on Sterling, BoE’s updated economic projections painted a complicated macroeconomic outlook. The central bank sharply downgraded its 2025 GDP growth forecast. At the same time, inflation forecasts were revised higher. Facing the increased uncertainty, BoE emphasized its commitment to a "gradual and careful" approach to policy easing.

Overall with today's announcement, risk is clearly tilted toward a more dovish policy stance. The base case remains as one 25bps cut per quarter throughout 2025,. But today’s decision raises the probability of a faster easing cycle, in particular if growth conditions worsen further.

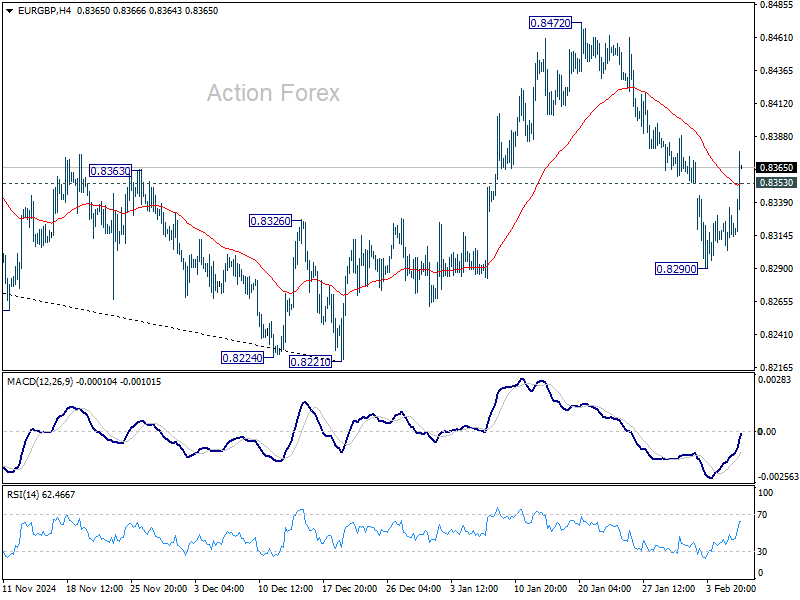

Technically, EUR/GBP's strong break of 0.8353 minor resistance argue that the pullback from 0.8472 might have completed at 0.8290 already. This also revives that case that rebound from 0.8221 is not totally completed. Further rise is now in favor back to 0.8472 resistance next.

Overall in the currency markets, Yen is currently the strongest one, followed by Canadian, and then Dollar. Sterling is the worst, followed by Kiwi, and then Swiss Franc. Euro and Aussie are positioning in the middle. The picture is rather mixed with the exception of clear strength in Yen and weakness in Sterling. Other parts of the markets might need tomorrow's US NFP data to provide more clarity.

In Europe at the time of writing, FTSE is up 1.53%. DAX is up 0.82%. CAC is up 0.97%, UK 10-year yield is down -0.0249 at 4.416. Germany 10-year yield is up 0.004 at 2.369. Earlier in Asia, Nikkei rose 0.61%. Hong Kong HSI rose 1.43%. China Shanghai SSE rose 1.27%. Singapore Strait Times rose 0.39%. Japan 10-year JGB yield fell -0.0166 to 1.267.

US initial jobless claims rises to 219k vs exp 214k

US initial jobless claims rose 11k to 219k in the week ending February 1, above expectation of 214k. Four-week moving average of initial claims rose 4k to 217k.

Continuing claims rose 36k to 1886k in the week ending January 25. Four-week moving average of continuing claims rose 2k to 1872k.

BoE cuts rates to 4.50% in surprisingly dovish vote

BoE lowered its policy rate by 25 basis points to 4.50%, as widely expected, but the tone of the decision was unexpectedly dovish.

The Monetary Policy Committee vote split at 7-2, with Swati Dhingra advocating for a more aggressive 50bps cut—as expected—but hawkish member Catherine Mann surprisingly joining her, marking a significant shift in her stance.

BoE emphasized a “gradual and careful” approach to easing, a slight adjustment from December’s messaging, which only referenced "gradual" reductions. This shift highlights policymakers' growing concerns over inflation persistence and economic fragility. Governor Andrew Bailey reaffirmed that rate adjustments would be assessed on a "meeting-by-meeting" basis, with no pre-determined path for cuts.

In its updated economic projections, BoE raised its inflation outlook, now expecting headline CPI to peak at 3.7% in Q3 2025, up from a prior forecast of 2.8%. The revision reflects higher energy costs and expected increases in regulated utility and transport prices. Inflation is not anticipated to return to the 2% target until Q4 2027, six months later than previously projected.

Growth forecasts were also downgraded sharply for 2025, with expected GDP expansion halved to 0.75%, citing weak business sentiment, sluggish consumer activity, and poor productivity growth. However, projections for 2026 and 2027 were revised slightly upward to 1.5% from 1.25%, suggesting policymakers see a slow but eventual economic recovery.

ECB’s Cipollone open to March cut, flags risks of full US-China trade war

ECB Executive Board member Piero Cipollone indicating that while "there is still room for adjusting rates downwards", the March decision remains uncertain. He stated that ECB must be "extremely careful" in its assessment, and he will enter the meeting "with an open mind".

Discussing the concept of the neutral rate in a Reuters interview, Cipollone downplayed its practical significance in policy setting. He pointed out that when estimates for the neutral rate vary widely—such as between 1.75% and 2.25%—it becomes "not terribly useful for setting monetary policy." If ECB operates near either end of the range, it could risk either undershooting or overshooting its inflation target.

Cipollone also raised concerns about the evolving global trade situation. The immediate impact of US tariffs depends on European retaliation and specific product categories affected, He warned that a "full trade war" between the US and China poses a more significant threat.

With China accounting for 35% of global manufacturing capacity, broad trade restrictions could flood European markets with Chinese goods. This would create a dual challenge— "deflationary" pressures from lower-priced imports and a "contractionary" effect as European producers struggle to compete.

Eurozone retail sales falls -0.2% mom in Dec, EU down -0.3% mom

Eurozone retail sales slipped by -0.2% mom in December, missing market expectations of -0.1% decline and pointing to continued weakness in consumer demand. The drop was largely driven by -0.7% contraction in food, drinks, and tobacco sales, while non-food products saw a modest 0.3% increase. Automotive fuel sales in specialized stores also ticked up 0.2%, providing some offset to the broader decline.

At the EU-wide level, retail sales fell even further, down 0.3% mom. The country-level breakdown highlights stark contrasts in retail activity. Slovenia (-2.2%), Germany (-1.6%), and Poland (-1.5%) saw the sharpest contractions, while Slovakia (+8.2%), Finland (+2.1%), and Spain (+1.4%) registered solid gains.

BoJ's Tamura advocates rate hike to 1% by late fiscal 2025

BoJ board member Naoki Tamura, a known hawk, reinforced his stance on the need for tighter monetary policy, stating that Japan’s short-term interest rates should rise to at least 1% by the second half of fiscal 2025 to mitigate inflation risks.

Tamura explained that inflationary pressures are mounting, necessitating a shift away toward a more neutral rate. He highlighted that by late fiscal 2025, the Japanese economy is expected to reach a point where the 2% inflation target can be considered sustainably achieved, supported by broad-based wage increases, including among smaller firms.

"Bearing in mind that short-term interest rates should be at 1% by the second half of fiscal 2025, I think the Bank needs to raise rates in a timely and gradual manner, in response to the increasing likelihood of achieving its price target," he said.

Australia’s NAB business confidence improves, but profitability weakens

Australia’s NAB Business Confidence rose from -7 to -4 in Q4, reflecting a slight improvement in sentiment. However, Business Conditions remained unchanged at 3, as trading conditions slipped from 6 to 5, and profitability turned negative from 0 to -1. Employment conditions as steady at 3.

Forward-looking indicators showed a mixed picture. Expected business conditions for the next three months edged lower, but sentiment for the 12-month horizon improved by five points, aligning with a three-point increase in capital expenditure plans, suggesting firms are cautiously optimistic about long-term prospects.

Cost pressures moderated, with labor cost growth slowing to 0.9% qoq from 1.2%, and purchase costs easing to 0.7% qoq from 1.0%. Retail price growth also softened to 0.5% qoq from 0.7%, though overall product price growth remained stable at 0.4% qoq, indicating ongoing margin pressure despite easing input costs. Wage costs remained the top concern for businesses, while demand constraints and labor shortages persisted as key challenges.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2462; (P) 1.2506; (R1) 1.2548; More...

GBP/USD dips notably today but stays above 1.2248 support and intraday bias remains neutral. While corrective rebound from 1.2099 could still extend, upside should be limited by 38.2% retracement of 1.3433 to 1.2099 at 1.2609. On the downside, break of 1.2248 support will bring retest of 1.2099 first. Firm break there will resume whole decline from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.

US initial jobless claims rises to 219k vs exp 214k

US initial jobless claims rose 11k to 219k in the week ending February 1, above expectation of 214k. Four-week moving average of initial claims rose 4k to 217k.

Continuing claims rose 36k to 1886k in the week ending January 25. Four-week moving average of continuing claims rose 2k to 1872k.

BoE cuts rates to 4.50% in surprisingly dovish vote

BoE lowered its policy rate by 25 basis points to 4.50%, as widely expected, but the tone of the decision was unexpectedly dovish.

The Monetary Policy Committee vote split at 7-2, with Swati Dhingra advocating for a more aggressive 50bps cut—as expected—but hawkish member Catherine Mann surprisingly joining her, marking a significant shift in her stance.

BoE emphasized a “gradual and careful” approach to easing, a slight adjustment from December’s messaging, which only referenced "gradual" reductions. This shift highlights policymakers' growing concerns over inflation persistence and economic fragility. Governor Andrew Bailey reaffirmed that rate adjustments would be assessed on a "meeting-by-meeting" basis, with no pre-determined path for cuts.

In its updated economic projections, BoE raised its inflation outlook, now expecting headline CPI to peak at 3.7% in Q3 2025, up from a prior forecast of 2.8%. The revision reflects higher energy costs and expected increases in regulated utility and transport prices. Inflation is not anticipated to return to the 2% target until Q4 2027, six months later than previously projected.

Growth forecasts were also downgraded sharply for 2025, with expected GDP expansion halved to 0.75%, citing weak business sentiment, sluggish consumer activity, and poor productivity growth. However, projections for 2026 and 2027 were revised slightly upward to 1.5% from 1.25%, suggesting policymakers see a slow but eventual economic recovery.

(BOE) Bank Rate reduced to 4.5%

Monetary Policy Summary, February 2025

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 5 February 2025, the MPC voted by a majority of 7–2 to reduce Bank Rate by 0.25 percentage points, to 4.5%. Two members preferred to reduce Bank Rate by 0.5 percentage points, to 4.25%.

There has been substantial progress on disinflation over the past two years, as previous external shocks have receded, and as the restrictive stance of monetary policy has curbed second-round effects and stabilised longer-term inflation expectations. That progress has allowed the MPC to withdraw gradually some degree of policy restraint, while maintaining Bank Rate in restrictive territory so as to continue to squeeze out persistent inflationary pressures.

CPI inflation was 2.5% in 2024 Q4. Domestic inflationary pressures are moderating, but they remain somewhat elevated, and some indicators have eased more slowly than expected. Higher global energy costs and regulated price changes are expected to push up headline CPI inflation to 3.7% in 2025 Q3, even as underlying domestic inflationary pressures are expected to wane further. While CPI inflation is expected to fall back to around the 2% target thereafter, the Committee will pay close attention to any consequent signs of more lasting inflationary pressures.

GDP growth has been weaker than expected at the time of the November Monetary Policy Report, and indicators of business and consumer confidence have declined. GDP growth is expected to pick up from the middle of this year. The labour market has continued to ease and is judged to be broadly in balance. Productivity growth has been weaker than previously estimated, and the Committee judges that growth in the supply capacity of the economy has weakened. As a result, the recent slowdown in demand is judged to have led to only a small margin of slack opening up.

In support of returning inflation sustainably to the 2% target, the Committee judges that there has been sufficient progress on disinflation in domestic prices and wages to reduce Bank Rate to 4.5% at this meeting.

Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint is appropriate.

In addition to the risks around inflation persistence, there are also uncertainties around the trajectories of both demand and supply in the economy that could have implications for monetary policy. Should there be greater or longer-lasting weakness in demand relative to supply, this could push down on inflationary pressures, warranting a less restrictive path of Bank Rate. If there were to be more constrained supply relative to demand, this could sustain domestic price and wage pressures, consistent with a relatively tighter monetary policy path.

The Committee will continue to monitor closely the risks of inflation persistence and what the evolving evidence may reveal about the balance between aggregate supply and demand in the economy. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 5 February 2025

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices. The latest data on these topics were set out in the accompanying February 2025 Monetary Policy Report.

2: The Committee discussed recent global economic developments, and in particular the extent to which these had been reflected in yield curves across advanced economies. During the current monetary policy cycle, the level of US and UK three-year forward rates, had been closer to each other than to the equivalent euro-area rates. The gap between the US and UK curves relative to the euro-area curve had widened materially over the previous six months or so, as US and UK rates had increased. Market intelligence suggested that the upward movement in US yields over this period had in part reflected expectations of a more inflationary policy mix, with the possible implementation of tariffs, looser fiscal policy and tighter controls on migration by the new US administration.

3: In the days leading up to the MPC’s policy decision, the US administration had made various announcements on trade tariffs, to which some other governments had responded. The Committee noted that this was a rapidly evolving situation, which it would be monitoring closely, and that the ultimate impact would depend on the final composition of policies, as discussed in Box C of the February Report. Nevertheless, there had already been an increase in economic uncertainty globally and a pickup in financial market volatility.

4: Market intelligence suggested that developments in the United States had influenced recent movements in UK government bond yields, alongside domestic factors. Since the MPC’s previous meeting, the market-implied path for Bank Rate in the United Kingdom had first risen and then fallen back, ending the period somewhat lower in aggregate. Almost all respondents to the Bank’s latest Market Participants Survey (MaPS) were expecting a 25 basis point reduction in Bank Rate at this MPC meeting, in line with market pricing. The median MaPS respondent expected 100 basis points of Bank Rate cuts this year, albeit with the overall distribution skewed towards fewer cuts, consistent with the market-implied path declining by around 85 basis points over the year. In addition to international factors, there had been UK-specific considerations, including data news that had been taken by market participants to suggest risks of a weaker outlook for activity, which had also been partly reflected in a small depreciation in the sterling effective exchange rate.

5: Bank staff expected that GDP had fallen by 0.1% in 2024 Q4 and projected that it would rise by 0.1% in 2025 Q1. The Committee discussed the extent to which recent developments reflected underlying demand and supply drivers, acknowledging significant uncertainties around the current and prospective balance between them. The recent slowdown in demand was assumed to have led to only a small margin of slack opening up, as growth in the supply capacity of the economy appeared to have been weakening for some time. Within potential supply, potential productivity appeared to have been very weak while labour supply growth had been strong. Business survey indicators of output growth had deteriorated over recent months, as had broader metrics of business and consumer confidence, which would be consistent with a slowdown in demand, and the household savings rate had continued to be high. The ratio of broad money to nominal GDP had returned to close to its pre-Covid trend, suggesting an erosion of the money overhang that had emerged during the pandemic.

6: Twelve-month CPI inflation had fallen slightly, to 2.5% in December. The latest evidence from key indicators suggested progress on underlying disinflation in domestic prices and wages had generally continued. There had nevertheless been substantial upside news to the near-term outlook for headline CPI inflation, which was now expected to rise quite sharply in the near term, to 3.7% in 2025 Q3, owing in part to energy prices, before easing again. Measures of households’ short-term inflation expectations had increased somewhat over the previous few months, while businesses’ short-term inflation expectations had picked up slightly but had remained well below recent peaks.

The immediate policy decision

7: The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

8: The Committee’s latest projection for CPI inflation was set out in the accompanying February Monetary Policy Report. In support of returning inflation sustainably to the 2% target, the Committee was maintaining its focus on the persistence of inflationary pressures in the medium term. Progress on disinflation in domestic prices and wages had generally continued.

9: Since the MPC’s previous meeting, CPI inflation had fallen slightly, while services inflation had moderated. Annual private sector regular AWE growth had increased, although the news from other pay indicators had been mixed. Pay growth was expected to slow to around 3¾% by year-end, broadly consistent with estimates from the Agents’ annual pay survey, as well as the Decision Maker Panel. GDP growth had been weaker than expected at the time of the November Report, and indicators of business and consumer confidence had declined. GDP growth was expected to pick up from the middle of this year. The labour market had continued to ease and was judged to be broadly in balance. Productivity growth had been weaker than previously estimated, and the Committee judged that growth in the supply capacity of the economy had weakened.

10: Reflecting recent developments in global energy costs and regulated prices, CPI inflation was expected to rise quite sharply in the near term, to 3.7%. The MPC judged that this would not lead to additional second-round effects on underlying domestic inflationary pressures. Compared with economic conditions during the succession of large external cost shocks in 2021-22, the labour market was now looser and therefore some of the dynamics observed previously were unlikely to reoccur. Nevertheless, given the recent extended period over which inflation had remained above the 2% target, the threshold for second-round effects might now be somewhat lower.

11: In the medium term, and conditioned on the market path for interest rates, inflation was expected to return to around the 2% target. The MPC’s February forecast remained consistent with the second case for the evolution of persistent inflationary pressures that the Committee had identified previously. That is, the emerging margin of slack in the economy was projected to act against some continuing second-round effects in domestic prices and wages, allowing CPI inflation to fall back to target sustainably.

12: Taking recent developments together, the Committee was now placing greater weight on the second and third cases that it had been considering. Nevertheless, there were considerable risks around the path of spare capacity in the economy and inflationary pressures over the medium term, to which monetary policy might need to respond.

13: In terms of upside risks, the continued elevated rate of wage growth, and the upside news in the near-term outlook for headline CPI, could present a risk to inflation persistence, particularly if it were to affect firms’ and households’ inflation expectations.

14: In terms of downside risks, domestic inflationary pressures could be weaker than projected in the forecast. In addition, recent developments in activity could reflect greater weakness in demand relative to supply, and UK and global uncertainties could weigh further on demand and the labour market. This could lower wage pressures and dampen companies’ pricing power going forward.

15: The MPC judged that monetary policy still remained clearly in restrictive territory, following recent reductions in Bank Rate. However, there was a range of views among members on the remaining degree of restrictiveness.

16: While cyclical developments in the economy played a significant role in determining the monetary stance at policy-relevant horizons, the long-term real equilibrium interest rate, R*, could also play a role in that assessment as a long-term anchor for the policy rate, albeit not as a direct guide for setting policy. As set out in Box A in the February Report, there was evidence that R* had risen modestly since the MPC's previous assessment in 2018, but there was significant uncertainty around the range of estimates at any point and the extent of any increase.

17: The Committee turned to the immediate policy decision.

18: Seven members preferred to reduce Bank Rate to 4.5% at this meeting, on the basis that there had continued to be sufficient progress on disinflation in domestic prices and wages. There was a range of views underlying these members’ outlooks for the economy, with various risks around both the domestic and global environment.

19: On one view, looking through the expected near-term pickup in CPI inflation, the disinflation process had remained on track, and weakening activity and a looser labour market could weigh further on inflation. There was increased uncertainty around both the UK and global economic outlooks, with potentially countervailing forces acting on the prospects for domestic inflation. This warranted an approach to policymaking which was both gradual in continuing to lean against the persistence in inflation and careful in recognising increased uncertainty and that there were two-sided risks to inflation.

20: On another view, the upside news in indicators of pay growth and inflation over recent quarters, in parallel with continued weakness in activity, was symptomatic of constrained supply relative to demand. In large part, this reflected tepid productivity growth, which was unlikely to recover significantly over the forecast period. On this basis, weakness in observed activity and employment going forward could continue to reflect constrained supply rather than an accumulation of economic slack. This view continued to warrant a cautious and gradual removal of monetary policy restriction.

21: Two members preferred a 0.5 percentage point reduction in Bank Rate, to 4.25%, although they had different views on inflation dynamics, the structural factors underpinning them, and future monetary policy. Disaggregated data pointed to inflation continuing to decline through both wage and price-setting channels. The prospect of weak activity and lower labour demand was likely to reduce wage pressures as well as moderate firms’ pricing power. For one member, a more activist approach at this meeting would give a clearer signal of financial conditions appropriate for the United Kingdom, even as monetary policy would need to remain restrictive for some time to anchor inflation expectations, and Bank Rate would likely stay high given structural persistence and macroeconomic volatility. For the other member, the subdued outlook for demand remained consistent with CPI inflation staying sustainably at the target in the medium term despite the expected near-term uptick in regulated prices, and Bank Rate needed to account for policy transmission and supply capacity over the medium term.

22: Based on the Committee’s evolving view of the medium-term outlook for inflation, a gradual and careful approach to the further withdrawal of monetary policy restraint was appropriate.

23: In addition to the risks around inflation persistence, there were also uncertainties around the trajectories of both demand and supply in the economy that could have implications for monetary policy. Should there be greater or longer-lasting weakness in demand relative to supply, this could push down on inflationary pressures, warranting a less restrictive path of Bank Rate. If there were to be more constrained supply relative to demand, this could sustain domestic price and wage pressures, consistent with a relatively tighter monetary policy path.

24: The Committee would continue to monitor closely the risks of inflation persistence and what the evolving evidence might reveal about the balance between aggregate supply and demand in the economy. Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee would decide the appropriate degree of monetary policy restrictiveness at each meeting.

25: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be reduced by 0.25 percentage points, to 4.5%.

26: Seven members (Andrew Bailey, Sarah Breeden, Megan Greene, Clare Lombardelli, Huw Pill, Dave Ramsden and Alan Taylor) voted in favour of the proposition. Two members (Swati Dhingra and Catherine L Mann) voted against the proposition, preferring to reduce Bank Rate by 0.5 percentage points, to 4.25%.

Operational considerations

27: On 5 February, the stock of UK government bonds held for monetary policy purposes was £646 billion.

28: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

David Roberts was also present on 27 January and 3 February, as an observer for the purpose of exercising oversight functions in his role as a member of the Bank’s Court of Directors.

Are Gold Bulls Exhausted?

- Gold bulls take a rest after record rally to $2,882.

- A potential decline could be contained above $2,843.

Gold bulls are taking a breather after a powerful rally to a new all-time high of $2,882. Although sellers tried to push the price lower earlier today, the upper band of the broken bullish channel added a footing under the price near $2,855.

With the RSI peaking in the overbought zone and the stochastic oscillator sailing southwards, a cooldown is likely but it could be temporary if the 20-period simple moving average (SMA) at $2,843 comes to the rescue once again. A break lower, however, could motivate some profit taking toward $2,810, with further declines to $2,790 or even $2,735 if bearish momentum accelerates.

On the upside, if gold reclaims $2,870, the next key test is the $2,900 psychological level, followed by $2,945.

Overall, the bottom line is that gold’s record rally has hit a hurdle at $2,870, but the bulls remain in control unless $2,840 gives way.

Australian Dollar Dips, Services PMI Beats Estimate

The Australian dollar has snapped a three-day rally on Thursday. In the European session, AUD/USD is trading at 0.6266, down 0.27% on the day. After sliding to a 5-year low on Monday, the Aussie has recovered and gain 0.9% this week.

Australia’s PMI stronger than expected

It’s been a good week for Australian PMIs. On Monday, Manufacturing PMI climbed back into positive territory in January and rose to a revised 50.2, up from a preliminary estimate of 49.8 and above the December reading of 47.8. This marked the first expansion in a year, as the manufacturing sector has been hit hard by the weak global economy and the slowdown in China, Austaralia’s number one trading partner.

This was followed by an acceleration in Services PMI on Wednesday, with a reading of 51.2 in January, up from the preliminary reading of 50.4 and above the December read of 50.8. The services sector has shown sustained growth for twelve straight months. This was the strongest expansion since August with an increase in customer demand and new orders.

Earlier in the week, Australia’s retail sales declined for the first time in nine months. Although the drop was a modest 0.1%, much better than the market estimate of -0.7%, it is raising concerns about the strength of the economy and has fueled expectations that the Reserve Bank of Australia will cut rates at the Feb. 18 meeting. The money markets are currently pricing a quarter-point cut at 80%.

The central bank has been an outlier amongst major central banks as it has not joined the easing cycle and a rate cut would be hugely significant. The RBA has held the cash rate at 4.35% since Nov. 2023 and with underlying inflation falling and a weak economy, conditions seem ripe for a rate cut.

AUD/USD Technical

- AUD/USD is testing support at 0.6274. Below, there is support at 0.6251

- There is resistance at 0.6308 and 0.6331