Sample Category Title

BoE Meeting Takes Centre Stage Today

In focus today

Today, we expect the Bank of England to cut the Bank Rate by 25bp to 4.50% in line with consensus and market pricing. We anticipate the vote split to be 8-1 with the majority voting for a cut and hawk Catherine Mann voting for an unchanged decision. We expect the BoE to stick to its previous guidance noting that "a gradual approach to removing monetary policy restraint remains appropriate". On balance, we tilt towards a dovish twist during the press conference with downside risks to growth tentatively materialising. See more in our preview Research UK - Budget skies are clearing for GBP; BoE to cut, 3 February.

From the US, preliminary US Q4 productivity data is released. Solid productivity gains have helped moderate growth in firms' unit labour costs despite relatively large increases in nominal wages. SF Fed's Daly is scheduled to give a speech in the evening.

In the euro area, retail sales data for December is released. This print has been rising during the past six months showing signs of recovering private consumption.

The focus in Sweden today will be on the January flash inflation print. We expect CPIF at 1.54% (Riksbank: 1.79%, cons: 1.6%) and CPIF excluding energy at 1.94% (Riksbank: 2.41%, cons: 2.1%). We see a clear downside risk to the Riksbank's forecast, and this print will be important for future policy considerations from the Riksbank. The flash estimate today will not provide any information about the components or the weights.

Economic and market news

What happened yesterday

In the euro area, the final composite PMI for January confirmed the initial reading of 50.2, with services PMI almost unchanged at 51.3. There were some revisions beneath the aggregate data, as German PMIs were revised upwards due to improvement in the manufacturing sector. In contrast, Spain and France showed lower figures in the final release. As Spain has been the main growth driver of the euro area, the weakening PMIs are noteworthy. Yet, Spain remains comfortably in growth territory, with a composite PMI of 54.0, a level it has maintained for the past six months, whereas French PMIs are lower signalling weaker activity.

In France, French Prime Minister survived the no-confidence vote and pushed through a delayed 2025 budget aimed at reducing France's deficits. Bayrou succeeded by negotiating budget compromise with the Socialist party.

In the US, the ISM non-manufacturing figure was lower than expected at 52.8 (prior: 54.1, cons: 54.3). The weak ISM pushed EUR/USD higher and confirmed earlier signals of weakness from PMI. Indices for business activity, new orders, and prices all declined. Leading data for January showed an unusual pattern, with manufacturing growth improving while the services sector lost stream. Meanwhile, ADP employment exceeded expectations with 183K jobs created in January (prior: 176K, cons: 150K), highlighting a surge in private sector employment and strengthening the case for a stable labour market.

In Norway, housing data showed great strength with seasonally adjusted housing prices increasing by 1.4% m/m in January, significantly surpassing Norges Bank's estimate of 0.5% from the December MPR. This may lead the market to question the necessity or possibility of rate cuts in Norway. However, at the press conference following the January monetary policy meeting, Governor Bache conveyed that there are no concerns in the housing economy that would impact rate cut decisions soon.

Equities: Global equities rose yesterday due to a variety of factors. Firstly, earnings on both sides of the Atlantic from some of the mega-cap companies impacted sector performance, resulting in a noticeably different outcome in Europe and the US. Secondly, defensive sectors outperformed on both sides of the Atlantic. While this aligns badly with the strong markets and with indices ending at daily highs, some of this can also be attributed to earnings and partly to the fact that yields took a nosedive. Adding complexity, despite what we might call mixed macroeconomic conditions and a significant drop in yields with a flatter curve, banks performed well yesterday.

This can also be ascribed to earnings from banks, especially on our side of the Atlantic. Finally, positive sentiment combined with lower yields aligns well with support for small caps, which outperformed large caps by 0.4% yesterday. In the US yesterday, the Dow rose by 0.7%, the S&P 500 by 0.4%, the Nasdaq by 0.2%, and the Russell 2000 by 1.1%. Markets in Asia are mostly positive this morning. Futures in Europe and the US are higher across the board this morning.

FI: European yield curves bear flattened yesterday as the short end went higher in yields following cautious comments from Lane on the speed of rate cuts while at the same time the 30y was supported by soft ISM services as well as the QRA being in line with their previous communications and expectations, thus the US Treasury saying that they expect to keep auction sizes steady for a least next several quarters. As for the front end, Lane said that it might take longer than expected to get inflation to the target amid he also said that the miss ground, where one is not to overweighing the upside risks nor the downside risks.

FX: EUR/USD has fully erased the tariff-induced losses earlier this week with the cross at 1.04. USD/JPY continues to slide, now just above 152. GBP/USD scale back some of yesterday's gains ahead of the BOE meeting where a cut is expected. The SEK has had a good run this week. EUR/SEK pauses at 11.35 and NOK/SEK at 0.97 ahead of the Swedish set of inflation data at 08:00 CET, where we and the market expect core and headline prints below the Riksbank's forecast. The zloty has re-found its groove with EUR/PLN back at the 4.20 support area.

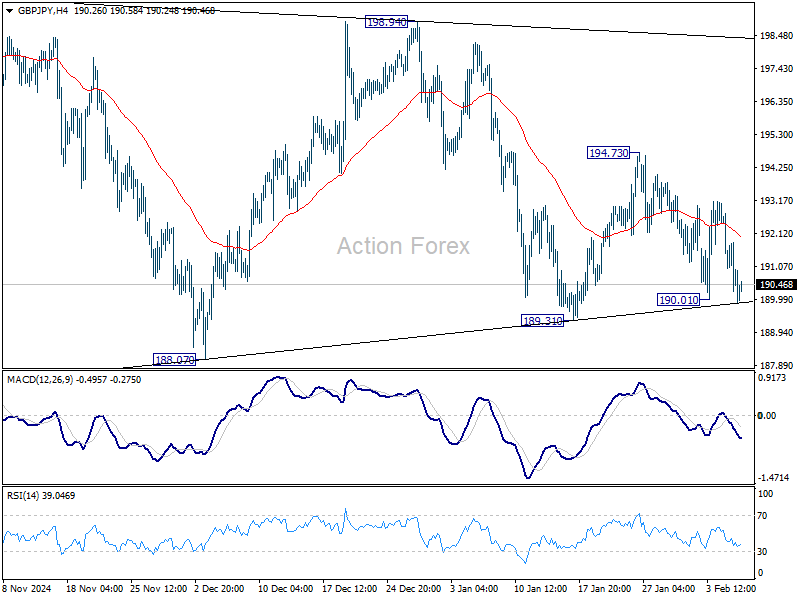

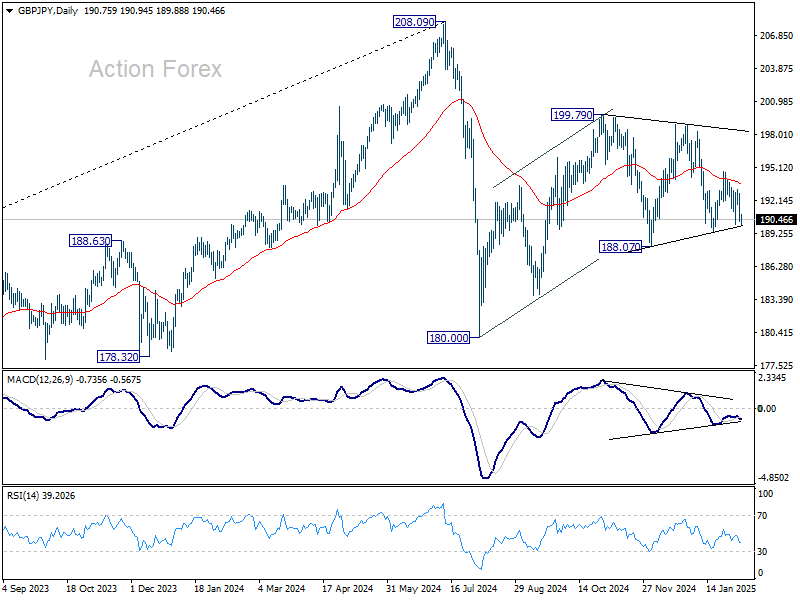

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.81; (P) 191.31; (R1) 192.31; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the downside, firm break of 189.31 will suggest that corrective pattern from 180.00 has completed. But before that, the pattern could still extend. Break of 194.73 will bring stronger rebound instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

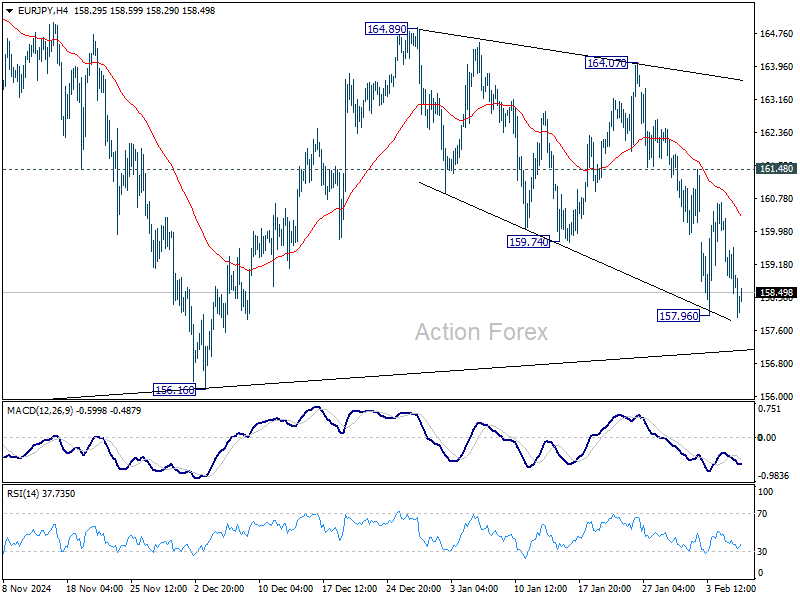

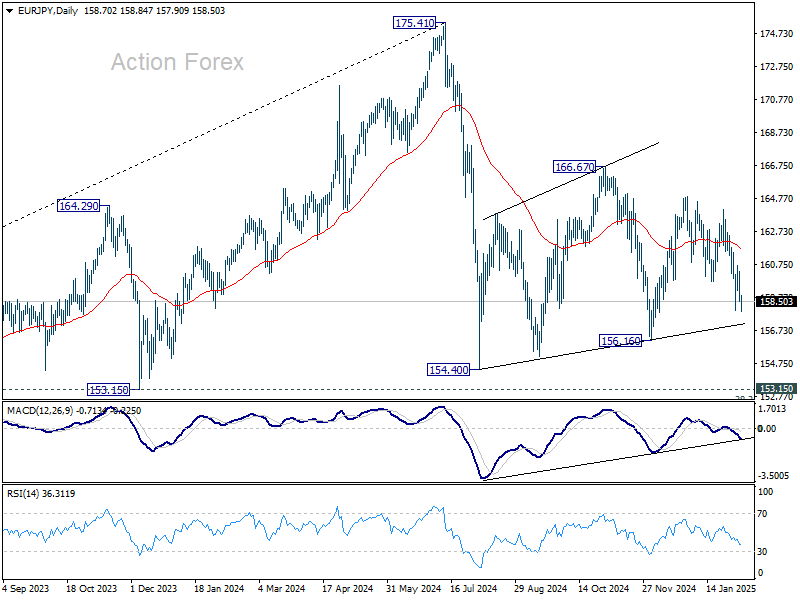

EUR/JPY Daily Outlook

Daily Pivots: (S1) 158.06; (P) 159.18; (R1) 159.87; More...

Intraday bias in EUR/JPY remains neutral for the moment. Overall outlook is unchanged that consolidation pattern from 154.40 could still extend. On the downside, below 157.96 will target 156.16 support. However, break of 161.48 will turn bias back to the upside for 164.07 resistance.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway...

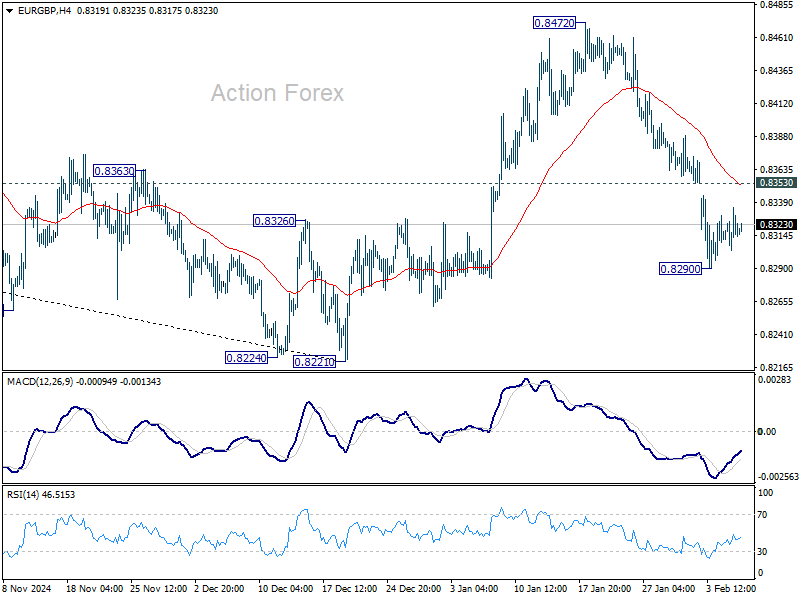

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8303; (P) 0.8320; (R1) 0.8335; More...

Intraday bias in EUR/GBP is turned neutral for consolidations above 0.8290 temporary low. Further decline s expected as long as 0.8353 resistance holds. Corrective rebound from 0.8221 should have completed already. Fall from 0.8472 would target a retest of 0.8221 low. However, firm break of 0.8353 will turn bias back to the upside for stronger rebound.

In the bigger picture, a medium term bottom should be in place at 0.8221, just ahead of 0.8201 key support (2022 low). Sustained trading above 55 W EMA (now at 0.8442) will pave the way to 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621), even just as a correction to the down trend from 0.9267 (2022 high). But still, medium term outlook will be neutral at best as long as 0.8621/4 holds.

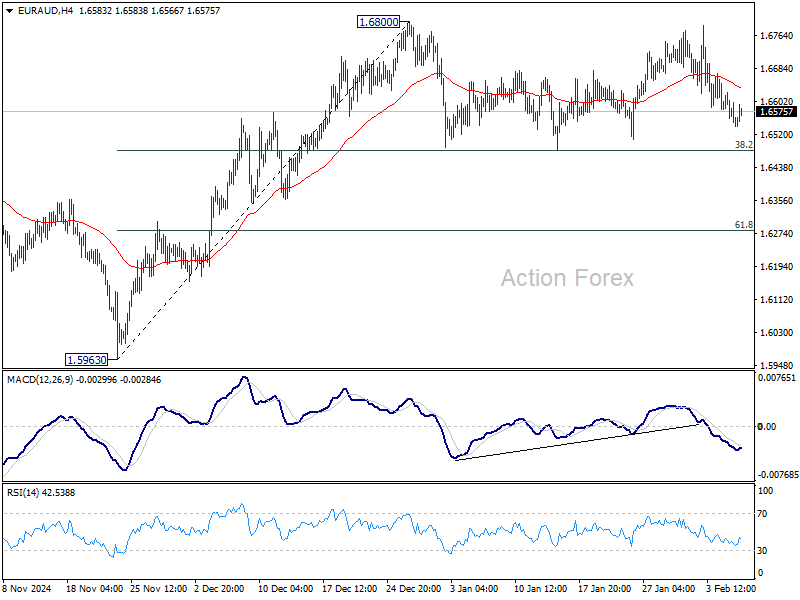

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6521; (P) 1.6574; (R1) 1.6605; More...

EUR/AUD's consolidation from 1.6800 is still in progress and intraday bias stays neutral. Strong support is expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. On the upside, firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support (2024 low) despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5996 will indicate that such up trend has completed and deeper decline would be seen.

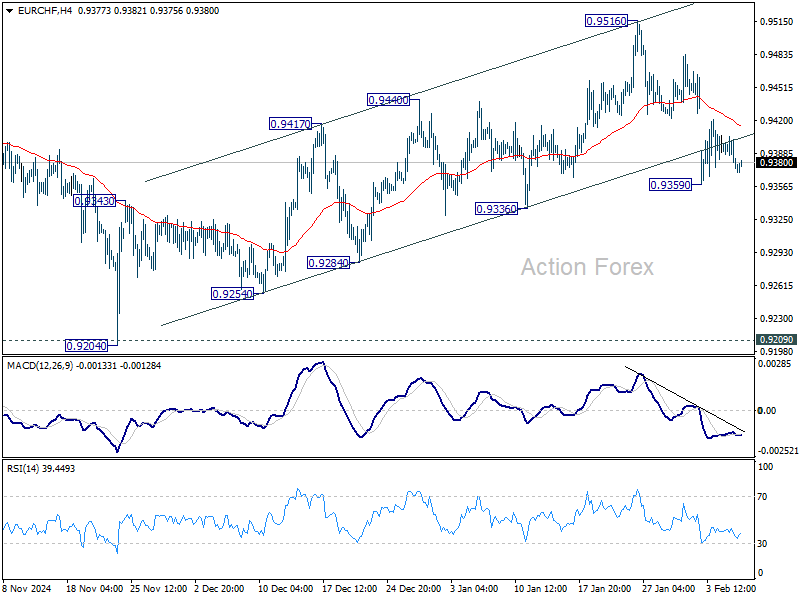

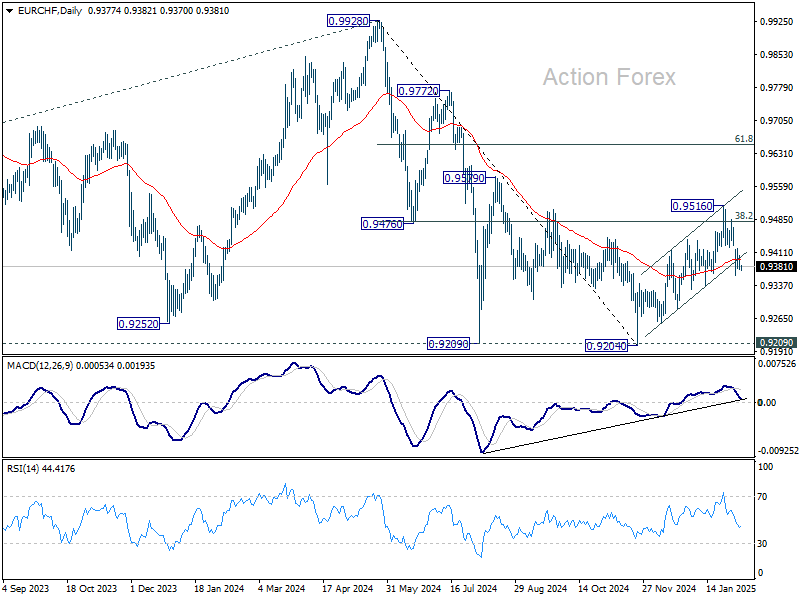

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9368; (P) 0.9387; (R1) 0.9400; More....

EUR/CHF is staying in range trading above 0.9359 and intraday bias remains neutral. Risk will stay on the downside as long as 0.9516 resistance holds. Corrective rebound from 0.9204 might have completed at 0.9516 already. Firm break of 0.9336 support will solidify this bearish case and target a retest on 0.9204 low.

In the bigger picture, current development argues that rebound from 0.9204 has completed as a corrective move after failing to sustain above 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Firm break of 0.9204/9 support zone will confirm larger down trend resumption.

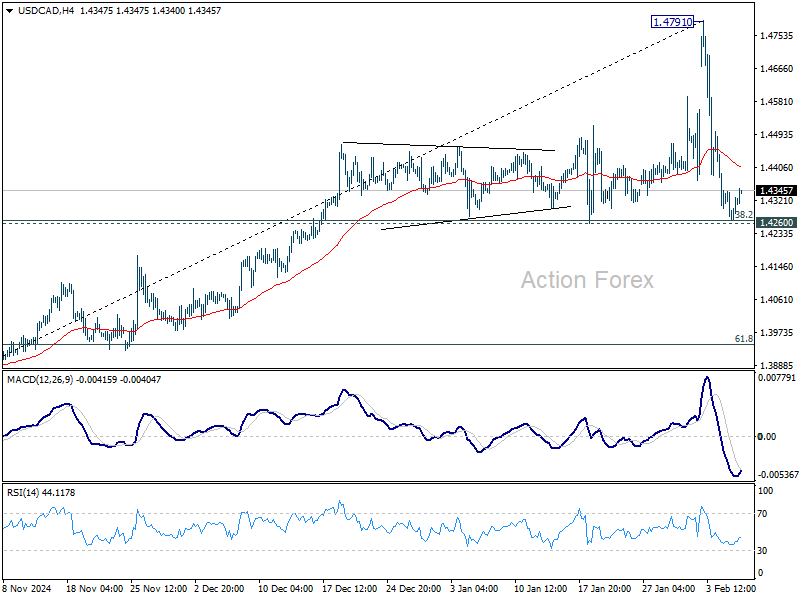

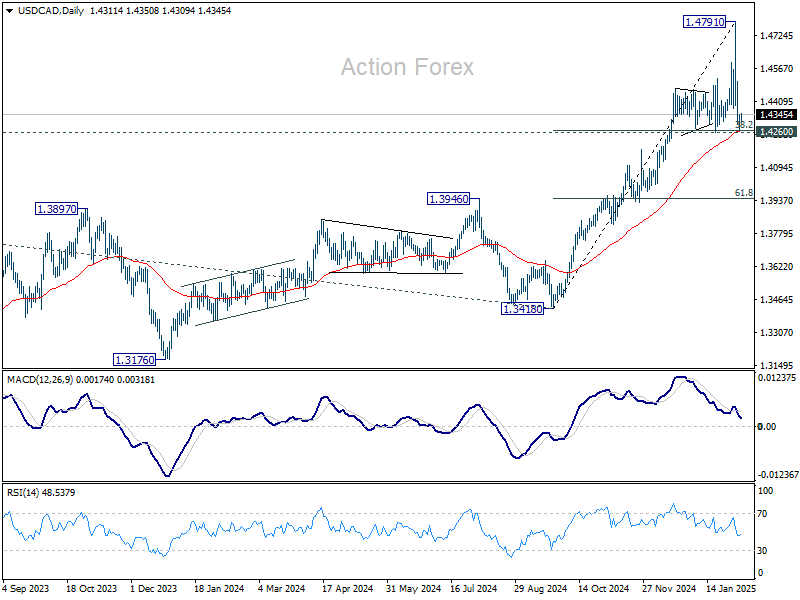

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4275; (P) 1.4310; (R1) 1.4350; More...

Intraday bias in USD/CAD remains neutral for the moment. Downside of the consolidation from 1.4791 should be contained by 1.4260 cluster support (38.2% retracement of 1.3418 to 1.4791 at 1.4267), which is also close to 55 D EMA (now at 1.4264). Larger up trend is expected to resume through 1.4791 at a later stage. However, firm break of 1.4260 will indicate that deeper correction is underway.

In the bigger picture, the break of 1.4667/89 key resistance zone (2020/2015 highs) confirms long term uptrend resumption. Next target is 100% projection of 1.2401 to 1.3976 from 1.3418 at 1.4993. Medium term outlook will remain bullish as long as 1.3976 resistance turned holds (2022 high), even in case of deep pullback.

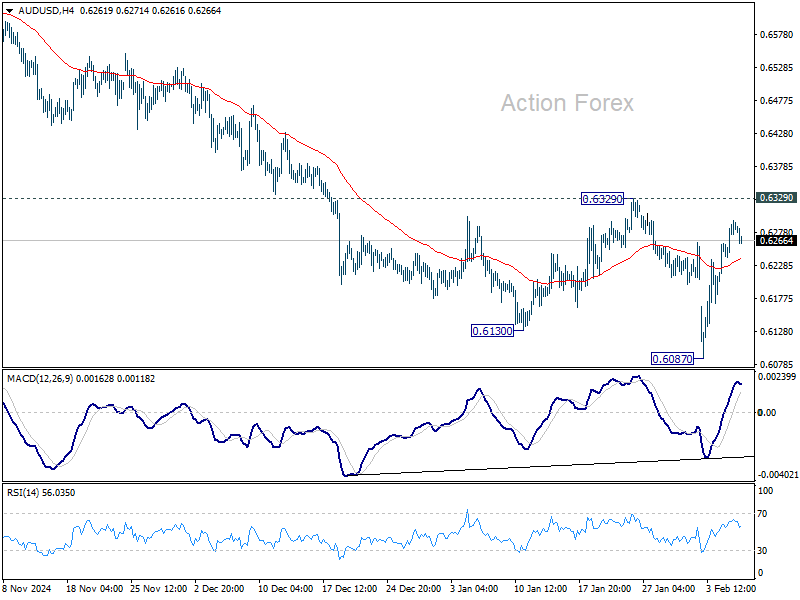

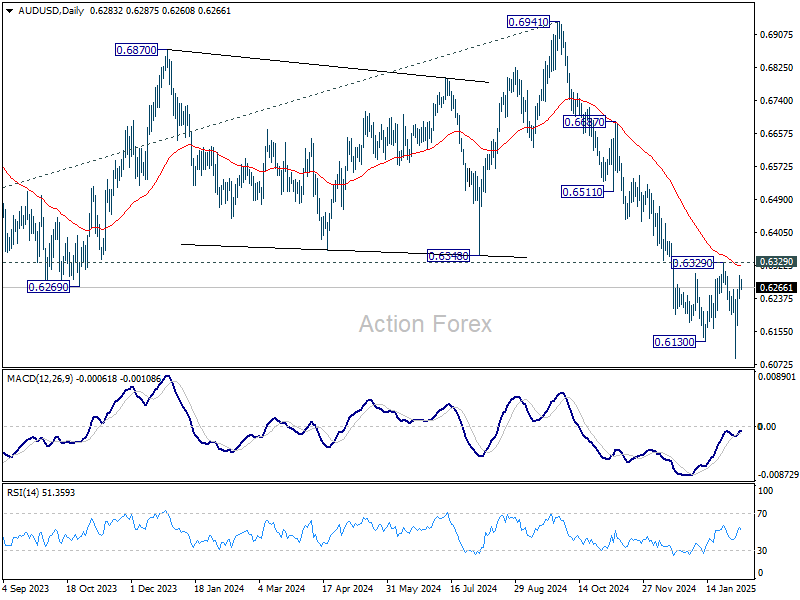

AUD/USD Daily Report

Daily Pivots: (S1) 0.6251; (P) 0.6274; (R1) 0.6308; More...

Intraday bias in AUD/USD remains neutral and further decline is expected as long as 0.6329 resistance holds. Break of 0.6087 will resume larger fall from 0.6941. However, firm break of 0.6329 will turn bias back to the upside for stronger rebound.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6511) holds.

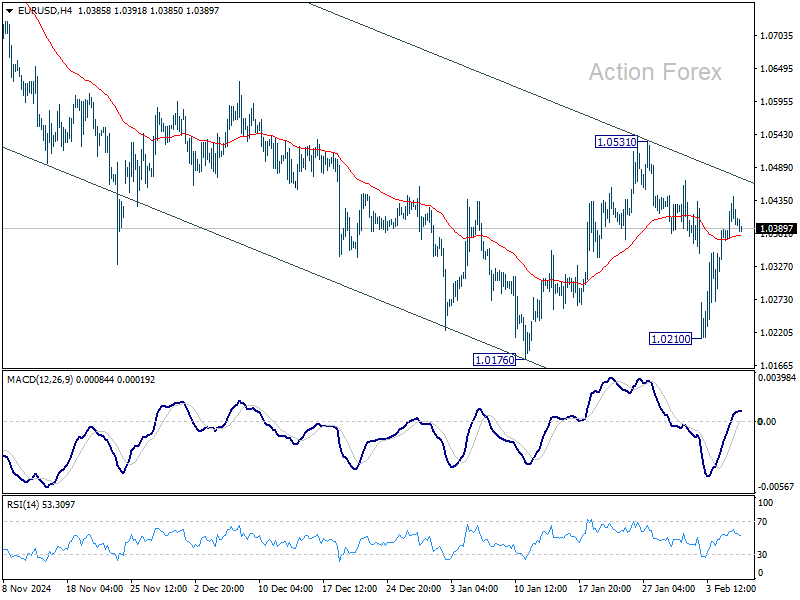

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0368; (P) 1.0405; (R1) 1.0440; More...

Outlook in EUR/USD is unchanged and strong resistance is expected from 1.0531 to cap upside of the corrective pattern from 1.0176. On the downside, break of 1.0176 will resume whole fall from 1.1213. However, sustained break of 1.0531 will rise the chance of bullish reversal and turn bias back to the upside for stronger rally.

In the bigger picture, immediate focus is back on 61.8 retracement of 0.9534 (2022 low) to 1.1274 (2024 high) at 1.0199. Sustained break there will solidify the case of medium term bearish trend reversal, and pave the way back to 0.9534. However, strong support from 1.0199 will argue that price actions from 1.1274 are merely a corrective pattern, and has already completed.

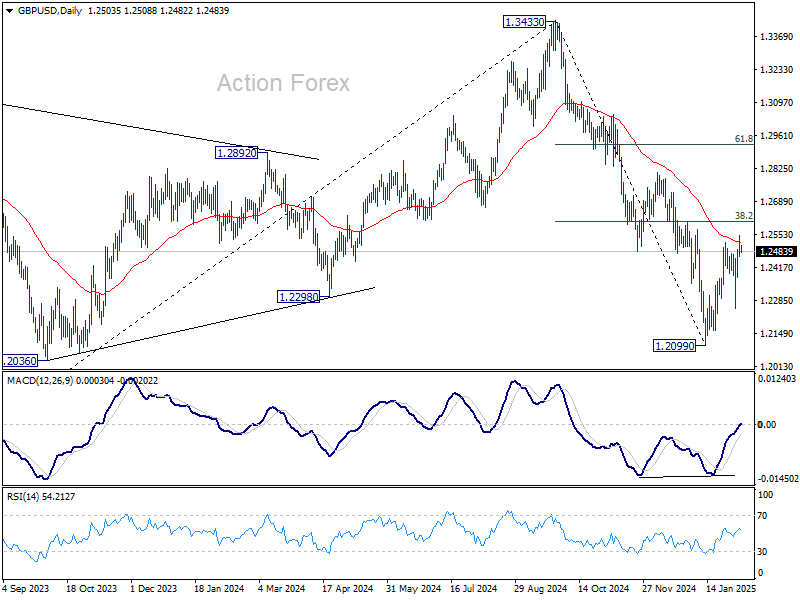

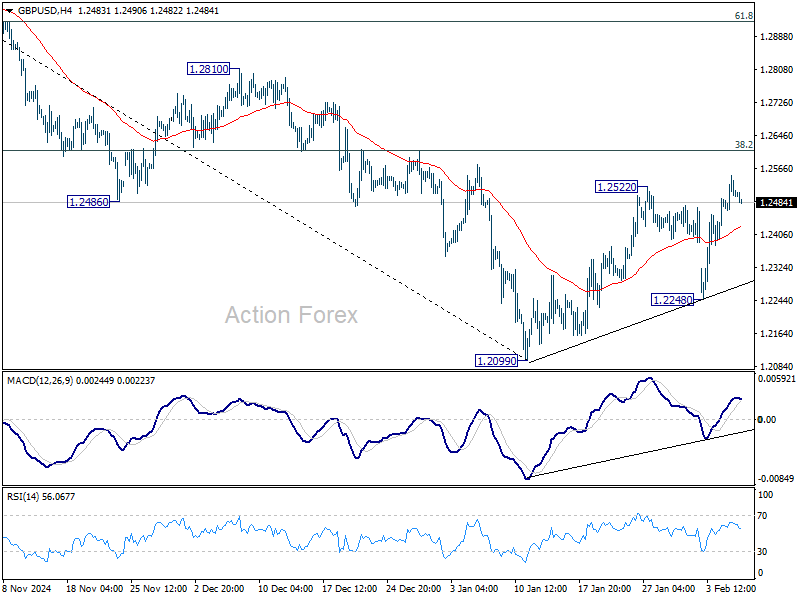

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2462; (P) 1.2506; (R1) 1.2548; More...

Outlook is unchanged in GBP/USD. Strong resistance is expected from 38.2% retracement of 1.3433 to 1.2099 at 1.2609 to complete the corrective rebound from 1.2099. On the downside, break of 1.2248 support will bring retest of 1.2099 first. Firm break there will resume whole decline from 1.3433. However, decisive break of 1.2609 will raise the chance of near term reversal, and target 61.8% retracement at 1.2923.

In the bigger picture, rise from 1.0351 (2022 low) should have already completed at 1.3433 (2024 high), and the trend has reversed. Further fall is now expected as long as 1.2810 resistance holds. Deeper decline should be seen to 61.8% retracement of 1.0351 to 1.3433 at 1.1528, even as a corrective move. However, firm break of 1.2810 will dampen this bearish view and bring retest of 1.3433 high instead.