Sample Category Title

XNG/USD Analysis: Bears Pressure Key Support

On 5 December, while analysing the natural gas chart, we noted that price movements:

→ were forming an ascending channel (shown in blue);

→ support from the lower boundary of the channel (reinforced by the psychological level of 3.000) was already evident in a nascent price reversal (indicated by an arrow).

As the XNG/USD chart illustrates, since that time (marked by a blue arrow), the price indeed rose, using the support from the lower boundary of the channel to reach its upper boundary on 30 December.

However, we now see supply forces displaying aggression – whenever the natural gas price climbs above 3.700, bears quickly intervene (marked by red arrows), pushing the price back down.

What could happen next?

From a technical analysis perspective of the XNG/USD chart:

→ The price is hovering near the key support, formed by the lower boundary of the ascending channel (which has been in place since last summer).

→ Bearish aggression, as mentioned above, sets the stage for a potential bearish breakout of this critical support, evidenced by the bearish gap at Monday’s market open.

From a fundamental analysis standpoint:

→ Meteorological reports of colder weather drove the price up to 3.570, but this appears to be a temporary rebound.

→ Bearish sentiment in the natural gas market may be amplified by statements from the Trump administration expressing a determination to lower oil prices.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

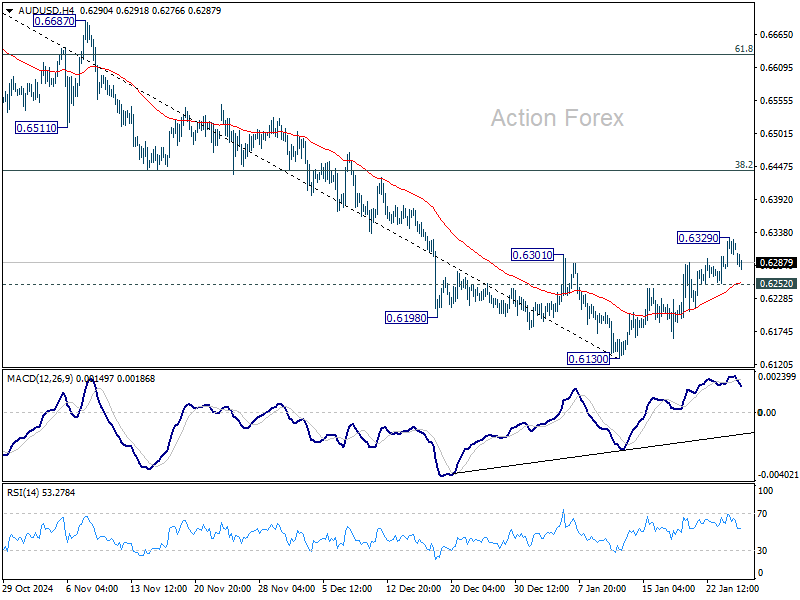

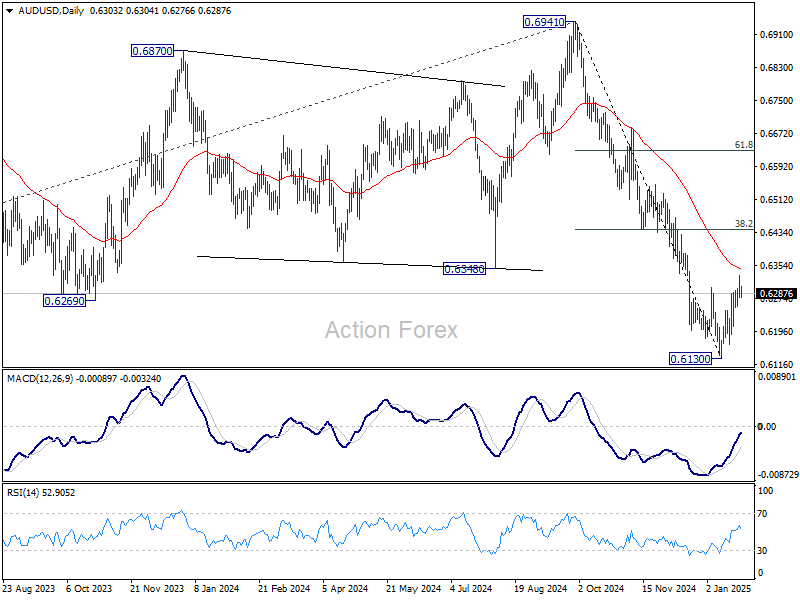

AUD/USD Daily Report

Daily Pivots: (S1) 0.6284; (P) 0.6308; (R1) 0.6336; More...

Intraday bias in AUD/USD is turned neutral first with today's dip. Corrective rebound from 0.6130 could still extend through 0.6329 and 55 D EMA (now at 0.6347). But strong resistance is expected from 38.2% retracement of 0.6941 to 0.6130 at 0.6440 to limit upside to complete this corrective rebound. On the downside, break of 0.6252 minor support will turn bias back to the downside for retesting 0.6130 low.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

NASDAQ Slide Grabs Focus, Dimming Fed Spotlight to Start the Week

As markets gear up for a week dominated by central bank meetings including Fed and ECB, sharp selloff in US tech stocks has stolen the spotlight. NASDAQ futures dropped more than -2%, triggering mild safe-haven flows into Yen, U.S. Dollar, and Swiss franc. Meanwhile, commodity currencies like Aussie and Kiwi suffered as risk sentiment deteriorated.

At the heart of the tech pullback is chipmaker NVIDIA, which fell nearly -7%. This move followed news that a relatively unknown Chinese startup, DeepSeek, released an AI assistant rivaling ChatGPT, claiming to use lower-cost chips and minimal data. The implication is that the current bullish thesis on AI-related infrastructure—ranging from expensive high-performance semiconductors to expanded data center capacity—could face competition from leaner, lower cost solutions.

DeepSeek, operating out of Hangzhou, has generated significant buzz by topping Apple App Store’s free apps chart on Monday, surpassing well-established AI tools. The startup's potentual remains uncertain, but the very notion that cutting-edge US technology could be challenged in China’s fast-evolving environment has unsettled investors. While it may be too soon to judge DeepSeek’s long-term impact, sentiment has clearly shifted, prompting a recalibration of risk assets and fueling a flight to safer currencies.

The tech rout has also hit the cryptocurrency market, with Bitcoin tumbling back below the 100k mark. Technically, the first line of defense is on rising 55 D EMA (now at 97282). Strong rebound from there will keep retain near term bullish momentum for resumption of long term up trend sooner rather than later. However, firm break of 55 D EMA will set up range trading between 89127/109571 for longer.

China’s PMI manufacturing falls to 49.1, weak start to 2025

China's manufacturing activity slipped into contraction in January, with NBS Manufacturing PMI falling from 50.1 to 49.1, missing expectations of 50.1. This marks the first contraction since October and the lowest reading since August.

The decline was attributed to Lunar New Year holiday, as workers left early, according to NBS senior statistician Zhao Qinghe. Analysts also noted potential effects from slowing export demand after earlier front-loading tied to trade concerns.

The services sector showed similar weakness, with the Non-Manufacturing PMI dropping from 52.2 to 50.2, below the expected 52.0. Composite PMI, combining manufacturing and services, slipped to 50.1 from 52.2, reflecting a broad deceleration.

While some of this is likely seasonal, the magnitude of the slowdown raises concerns about underlying economic momentum, especially with external pressures like trade tensions still in play.

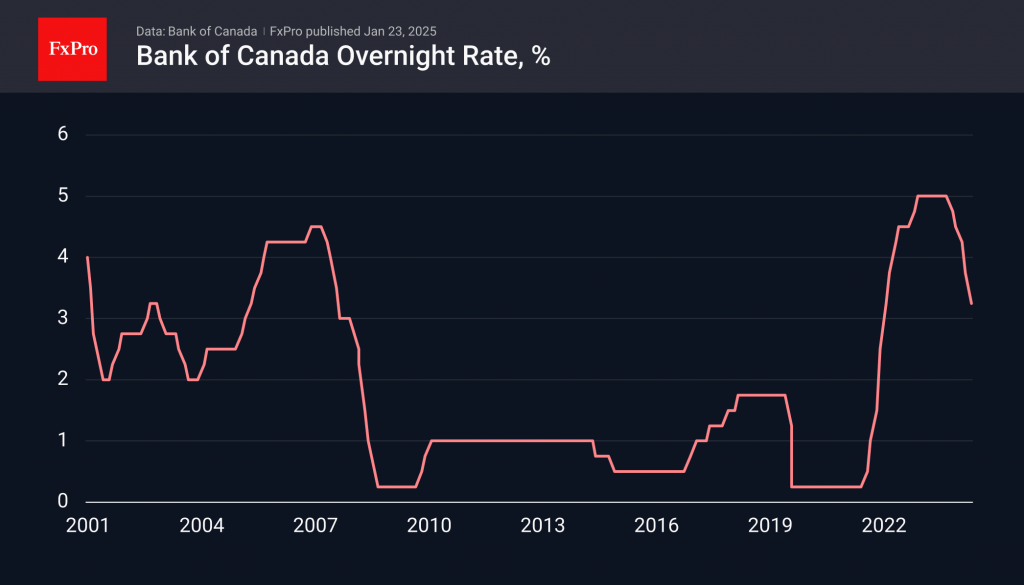

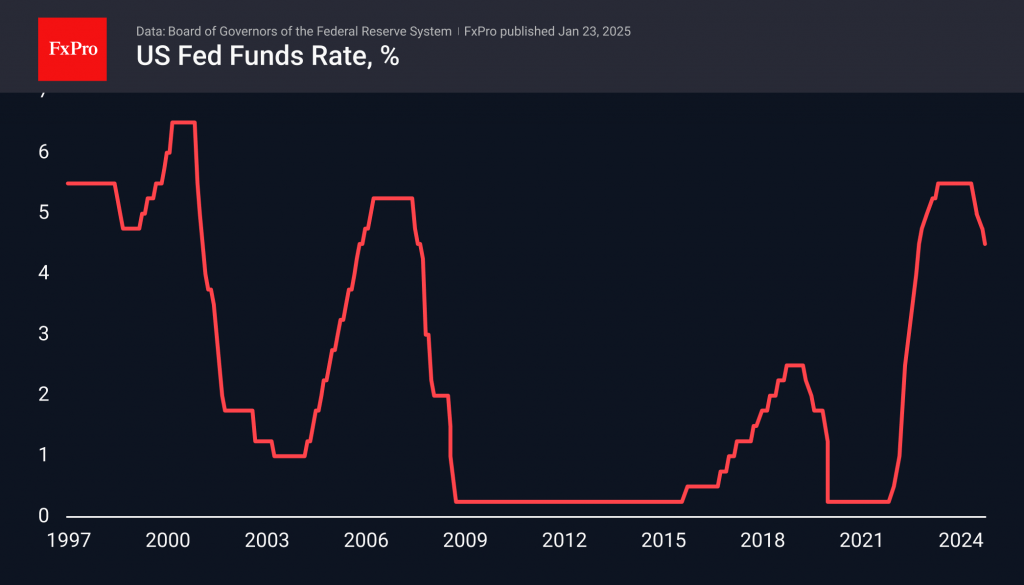

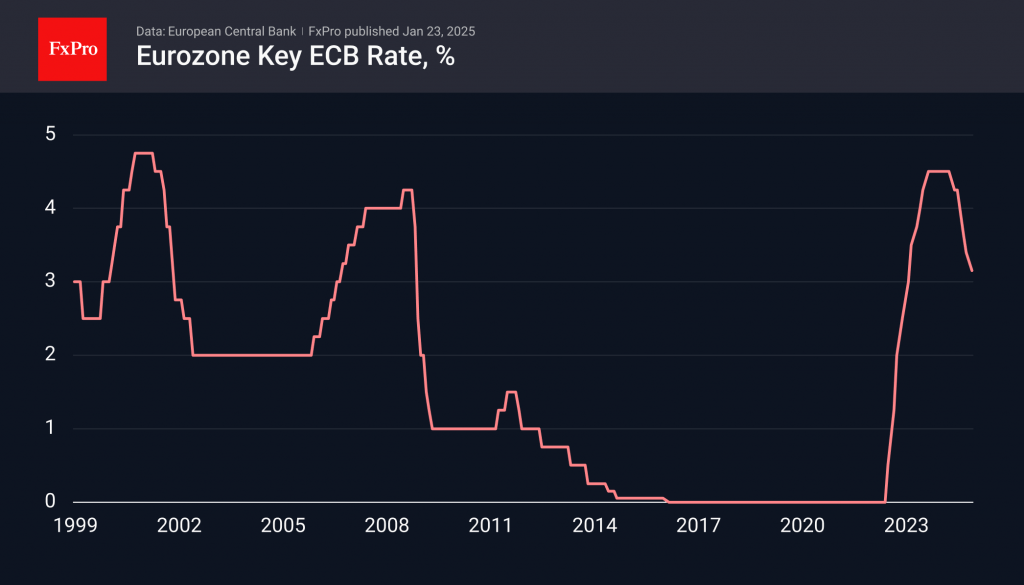

Three central banks, one busy week: Fed holds, BoC trims, ECB cuts

This week brings a trio of central bank decisions, with Fed, BoC, and ECB all set to reveal their latest policy moves. The consensus is that Fed will hold rates steady, BoC will deliver a smaller 25 bps cut, and ECB will maintain its gradual easing with another 25bps reduction. With a busy data docket also in play—featuring key GDP reports and inflation updates—traders will have a wealth of information to digest in a short span of time.

At Fed, there is a near-certainty of no change to its benchmark rate. Futures markets are pricing in 98% probability that FOMC will keep rates unchanged at 4.25–4.50%, pausing its easing cycle after a string of cuts in 2024. Given these odds, the chance of a surprise is minimal. Instead, the highlight will be the policy statement and Chair Jerome Powell’s press conference, regarding the rationale behind the hold.

Also, any clue regarding the length of this “pause” would likely move markets, especially given lingering questions about another possible cut in the first half of the year. Current pricing suggests around 72% chance that Fed will refrain from cutting at the next meeting in March as well. Still, around 70% chance is priced in for another 25bps reduction may occur during the first half of the year.

Beyond that, it may be too soon for Fed policymakers to give any guidance. More definitive signals about the path for the year might only emerge when the next set of dot plots and forecasts are released in March.

With Canadian inflation dipping to 1.8% in December, there is sufficient room for BoC to continue lowering rates. However, the current policy rate of 3.25%, before the cut, is now at the high end of the estimated neutral range of 2.25–3.25%. With that in mind, BoC should opt to proceed more cautiously with 25bps reduction.

The new Monetary Policy Report from BoC should offer fresh insights into the central bank’s updated economic outlook and rate path. The key questions focus on whether officials see a need to bring the policy rate below neutral to stimulative levels eventually—and if so, how quickly.

Over in Europe, ECB is firmly on track for another 25 bps cut to lower deposit rate to 2.75%. This approach is in line with President Christine Lagarde’s commitment to a “regular, gradual path” toward neutral, which she has previously identified in the 1.75–2.25% zone.

For the moment, ECB policymakers seem in harmony regarding the lack of need for rates to dip into stimulative territory. If the consensus holds, ECB could stop easing once it hits around 2% on the deposit rate, possibly between spring and summer. Nevertheless, the next opportunity for a more detailed forecast—including updated growth and inflation estimates—will likely come in March, which could be a pivotal moment for shaping expectations about future moves.

Beyond the trio of central bank meetings, the economic calendar is filled with significant releases. The US is set to unveil advance GDP figures, along with PCE inflation data. Eurozone’s GDP will be scrutinized for signs of stabilization. Germany’s Ifo business climate and GfK consumer sentiment surveys will also be important, as they may show whether Europe’s largest economy is ready to turn a corner. Australia’s CPI could sway RBA’s decision on whether to start cutting rates in February or wait until May. Canada’s own GDP figures round out the week.

Here are some highlights for the week:

- Monday: China NBS PMIs; German Ifo business climate; US new home sales.

- Tuesday: Japan corporate service price index; Australia NAB business confidence; US durable goods orders, house price index, consumer confidence.

- Wednesday: BoJ minutes, Japan consumer confidence; Australia CPI; Germany Gfk consumer sentiment; FOMC rate decision, US goods trade balance; BoC rate decisions.

- Thursday: New Zealand trade balance, ANZ business confidemce; Australia impor prices; Swiss trade balance, KOF economic barometer; Eurozone GDP flash, unemployment rate, ECB rate decision; US GDP advance, jobless claims.

- Friday: Japan Tokyo CPI, industrial production, retail sales, unemployment rate; Australia PPI; Germany CPI flash, unemployment rate; Swiss retail sales; Canada GDP; US personal income and spending, PCE inflation

AUD/USD Daily Report

Daily Pivots: (S1) 0.6284; (P) 0.6308; (R1) 0.6336; More...

Intraday bias in AUD/USD is turned neutral first with today's dip. Corrective rebound from 0.6130 could still extend through 0.6329 and 55 D EMA (now at 0.6347). But strong resistance is expected from 38.2% retracement of 0.6941 to 0.6130 at 0.6440 to limit upside to complete this corrective rebound. On the downside, break of 0.6252 minor support will turn bias back to the downside for retesting 0.6130 low.

In the bigger picture, fall from 0.6941 (2024 high) is seen as part of the down trend from 0.8006 (2021 high). Next medium term target is 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806. In any case, outlook will stay bearish as long as 55 W EMA (now at 0.6545) holds.

China’s PMI manufacturing falls to 49.1, weak start to 2025

China's manufacturing activity slipped into contraction in January, with NBS Manufacturing PMI falling from 50.1 to 49.1, missing expectations of 50.1. This marks the first contraction since October and the lowest reading since August.

The decline was attributed to Lunar New Year holiday, as workers left early, according to NBS senior statistician Zhao Qinghe. Analysts also noted potential effects from slowing export demand after earlier front-loading tied to trade concerns.

The services sector showed similar weakness, with the Non-Manufacturing PMI dropping from 52.2 to 50.2, below the expected 52.0. Composite PMI, combining manufacturing and services, slipped to 50.1 from 52.2, reflecting a broad deceleration.

While some of this is likely seasonal, the magnitude of the slowdown raises concerns about underlying economic momentum, especially with external pressures like trade tensions still in play.

Slow Start to a Busy Week

In focus today

Today, focus turns to the German Ifo. It will be interesting to see if the Ifo figures mirror the stronger-than-expected German PMI release on Friday.

The rest of the week will be busy, with focus on central bank meetings. On Wednesday, the Riksbank, the Bank of Canada, and the FOMC will announce their rate decisions, while the ECB will meet on Thursday. In addition to these meetings, there will be a flurry of interesting releases. In the euro area, Q4 flash GDP data, GDP country data, and January flash inflation from Spain will be released on Thursday, while January inflation for Germany and France is released on Friday. In the US, Tuesday will bring January durable goods orders, followed by the Q4 GDP release on Thursday and PCE inflation on Friday.

Economic and market news

What happened overnight

In China, the NBS PMIs recorded a decline in January, with the composite measure edging lower to 50.1 (prior: 52.2) amid weaker readings in both the manufacturing and services indices. Notably, the manufacturing component undershot expectations, contracting to 49.1 (cons: 50.1, prior: 50.1) - its weakest reading since August 2024 - though NBS stated that the reading "was affected by the approaching holiday", which begins on Wednesday. NBS also released industrial profits, which declined 3.3% over the course of 2024.

In geopolitics, the US reported that the ceasefire between Israel and Lebanon has been extended until 18 February. The initial ceasefire was announced in late November, bringing an end to the 14-month-long conflict between Israel and Hezbollah.

What happened since Friday

Friday was all about PMIs, as we received January PMI data for the euro area, the UK and the US. In the euro area, the composite PMI was stronger than expected, increasing to 50.2 (cons: 49.7, prior: 49.6). While the uptick was mainly driven by the manufacturing PMI, which edged up to 46.1 (cons: 45.3, prior: 45.1), the overall level of the manufacturing component is low, indicating continued production declines. The service counterpart was little changed at 51.4 (cons: 51.5, prior: 51.6), but stayed in expansionary territory, supporting our expectation of a 0.2% q/q rise in Q1 GDP. Overall, the economy remains supported by a resilient labour market, also visible in the employment PMIs for January, which show that the service sector continues to record rising employment.

Like in the euro area, UK PMIs were also stronger than expected, indicating improved activity. The composite measure edged up to 50.9 (cons: 50.1, prior: 50.4), with services at 51.2 (cons: 50.8, prior: 51.1) and manufacturing at 48.2 (cons: 47.0, prior: 47.0). Growth is largely driven by the service sector with price sector output expanding, though only modestly. While price pressures - input and output prices in both service and manufacturing - remain significantly in expansionary territory, posing a concern for the BoE, we believe that the overall take-away from the report is that the BoE should still feel comfortable delivering a 25bp cut at their next meeting on 6 February.

In contrast to the euro area and the UK, the US PMIs were somewhat mixed. The composite PMI declined to 52.4 as the services PMI unexpectedly fell to 52.8 (cons: 56.5, prior: 56.8), whereas the manufacturing index ticked up to 50.1 (cons: 49.7, prior: 49.4). Turning to sub-components, both services business activity and new orders ticked lower, while price and employment indices moved higher, indicating that the details are not as soft as the headline figure suggests. Conversely, manufacturing figures are looking more solid, with firms' order-inventory balances recovering quite nicely, and new orders indices recovering across both domestic and export demand. All in all, the signals across services and manufacturing were a bit more ambiguous.

In the US, President Trump threatened to impose emergency tariffs of 25-50% on Colombia after the South American nation refused to accept military flights carrying deportees. However, the tariff threats were put on hold on Sunday evening after an agreement was reached. While Colombia accounts for only around 0.5% of US imports, the face-off could be a warning sign for other countries going forward.

Equities: Global equities declined on Friday after eight consecutive days of gains. Interestingly, only the tech and energy sectors were lower, while the rest were higher. The day began positively before optimism waned as it progressed. Often, such movements can be attributed to specific events, but it is difficult to argue that this was the case on a Friday, especially when key European figures appeared satisfactory.US key figures and earnings were mixed, but the diminishing risk appetite began well before these events. In the US on Friday, the Dow was down 0.3%, S&P 500 down 0.3%, Nasdaq down 0.5%, and Russell 2000 down 0.3%. This morning, most equity markets in Asia are lower. However, the focus is on the US, with Nasdaq futures down more than 2% at the time of writing.

The reason is the focus on DeepSeek AI and the potential challenge to US leadership in AI, chip, and tech sectors. While it is early days, this development should not be underestimated given the exuberance and high valuation of AI-related stocks in the US. Any disruption to this narrative will have significant effects on markets. Please note that the coming week marks the peak of the earnings season, including results from five of the MAG 7 companies.

FI: Euro rates ended 3bp higher in the 10y point on Friday, after a roller coaster ride. Better than anticipated PMIs (particularly German PMI) was noted by markets, where both the services and manufacturing contributed to the surprise. The surprise took out 6bp of the ECB cut pricing for this year, and it now price just 88bp. We still like our call for the ECB to bring the policy rate into easing territory, below 2%. During the trading session, 10y Bunds were up 6bp at one point, but retraced following weaker than anticipated US PMIs.

FX: EUR/USD breached the 1.05 mark during Friday's session following a strong set of euro area PMIs. However, overnight the USD has returned bid following Trump reigniting global tariff-concerns. GBP regained some lost ground towards the end of last week after a weak start to the year where fiscal worries have been at the front and centre for the currency. In the Scandies, Trump's first week in office has proven a roller-coaster ride for NOK, where Trump bearish comments on oil prices have weighed on NOK and the lack of concrete initiatives on global tariffs, the weaker USD and a slightly more friendly relationship to China has contributed to strengthening NOK.

AUD/USD and NZD/USD Bounce Back: Are Further Gains Ahead?

AUD/USD started a decent increase above the 0.6200 and 0.6250 levels. NZD/USD is also rising and might aim for more gains above 0.5685.

Important Takeaways for AUD USD and NZD USD Analysis Today

- The Aussie Dollar rallied after forming a base above the 0.6165 level against the US Dollar.

- There is a key bullish trend line forming with support at 0.6290 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD is consolidating gains from the 0.5650 zone.

- There is a major bullish trend line forming with support at 0.5685 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair started a fresh increase from the 0.6165 support. The Aussie Dollar was able to clear the 0.6200 resistance to move into a positive zone against the US Dollar.

There was a close above the 0.6250 resistance and the 50-hour simple moving average. Finally, the pair tested the 0.6330 zone. A high was formed near 0.6330 and the pair recently saw a minor pullback.

There was a move below the 0.6310 level. The pair declined below the 23.6% Fib retracement level of the upward move from the 0.6164 swing low to the 0.6330 high. On the downside, initial support is near a key bullish trend line at 0.6290 and the 50-hour simple moving average.

The next major support is near the 50% Fib retracement level of the upward move from the 0.6164 swing low to the 0.6330 high at 0.6245.

If there is a downside break below the 0.6245 support, the pair could extend its decline toward the 0.6200 level. Any more losses might signal a move toward 0.6165.

On the upside, the AUD/USD chart indicates that the pair is now facing resistance near 0.6330. The first major resistance might be 0.6350. An upside break above the 0.6350 resistance might send the pair further higher.

The next major resistance is near the 0.6365 level. Any more gains could clear the path for a move toward the 0.6400 resistance zone.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair started a steady increase from the 0.5565 zone. The New Zealand Dollar broke the 0.5600 resistance to start the recent increase against the US Dollar.

The pair settled above 0.5650 and the 50-hour simple moving average. It tested the 0.5720 zone and is currently correcting gains. The pair corrected lower below the 0.5700 level. The NZD/USD chart suggests that the RSI is now approaching 40.

On the downside, immediate support is near the 23.6% Fib retracement level of the upward wave from the 0.5563 swing low to the 0.5723 high at 0.5685.

There is also a major bullish trend line forming with support at 0.5685. The first key support is near the 50% Fib retracement level of the upward wave from the 0.5563 swing low to the 0.5723 high at 0.5645.

The next major support is near the 0.5600 level. If there is a downside break below the 0.5600 support, the pair might slide toward the 0.5565 support. Any more losses could lead NZD/USD in a bearish zone to 0.5520.

On the upside, the pair might struggle near 0.5720. The next major resistance is near the 0.5735 level. A clear move above the 0.5735 level might even push the pair toward the 0.5780 level. Any more gains might clear the path for a move toward the 0.5850 resistance zone in the coming days.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Stock Futures Point to Steep Drop at Open Later Today

Markets

German bunds ended last week underperforming US Treasuries. Euro area PMIs suggested economic improvement is finally underway while price pressures picked up, both on the input and output side. German yields rose between 0.7 (30-yr) to 4.5 bps (2-yr) in bear flattening. US rates overcame early Trump-induced weakness only to take a second hit from an unexpected four-point decline in the services PMI (52.8). Net daily losses amounted to a little over 2 bps across the curve. Dollar weakness accompanied euro strength and lifted EUR/USD towards 1.05 for the first time since mid-December. The trade-weighted dollar (107.44) lost support of the 23.6% retracement on the September-January rally at 107.81. Sterling took the stagflationary sound of the January PMIs surprisingly well. EUR/GBP aborted an umpteenth attempt to settle north of the 0.845 resistance level to close around 0.84 instead. GBP/USD rose sharply and retook 1.24 again in the process. Stocks in the US finished about half a percent lower with sentiment souring dramatically during Asian dealings today. Stock futures, while obviously still very early, point to a steep drop at the open later today (Nasdaq -2.4%). A low-budget Chinese start-up built a model that’s said to be able to compete with heavy-investing peers. The news already broke last Friday - perhaps explaining some of the intraday stock weakness - but gained particularly market/media attention overnight. Chinese stock markets outperform ahead of a week-long close for Lunar New Year. President Trump in other news showed he’s able and willing to make good on tariffs threats. Colombia’s president over the weekend turned away US aircrafts carrying deportees but caved when Trump responded by imposing 25% emergency tariffs and threatened to raise them to 50% in a week. The jury’s out whether a (tech) stock plunge this size is the beginning of a larger correction or considered a buying opportunity. The latter has always been the case in the recent past so far. For now, though, the sour risk sentiment offers the dollar a slight edge over global peers. Core bonds gain with yields losing several basis points currently. Today’s economic calendar is little inspiring ahead of more interesting days later. Central banks meet in the US (Wednesday) and the Euro area (Thursday) as well as in Hungary, Sweden and Canada. Q4 GDP and inflation readings are due in several EMU member states as well as in the US. The earnings season is gaining traction with some of the tech and industrial bellwethers including Meta, Microsoft, Tesla, Apple, Intel & Caterpillar due to report.

News & Views

Rating agency Moody’s on Friday affirmed the Baa1 rating of Bulgaria with a stable outlook. In its assessment Moody’s says it is balancing three main rating drivers. Firstly, the rating agency expects that de country’s debt burden and deb affordability will remain significantly stronger than rating peers despite a gradual weakening. Moody’s expects the debt-to GDP ratio to gradually move higher from and estimated 24.8% end 2024 to 29% end 2029. The headline budget deficit is expected to stay close to 3.0% in 2025 and 2026. Secondly, Moody’s expects the Bulgarian economy to growth at a solid pace in 2025 and beyond. It sees GDP growth of 2.5% on 2025 and 2.7% in 2026. The credit profile is also supported by the likely adaption of the euro in the foreseeable further. However, thirdly, Moody’s sees the strengths as being balanced by a weakening of institutional effectiveness, evidenced by the slow and halting progress of key reforms and access to funding under Bulgaria’s EU funded RRP.

Chinese January PMI’s published this morning slowed more than expected. The manufacturing gauge unexpectedly dropped from 50.1 to 49.1. The non-manufacturing index declined substantially from 52.2 to 50.2. While activity often is reported to slow in the run-up to the Lunar New year Holidays, the decline was bigger than expected. Order growth dropped below the 50 mark both for manufacturing and non-manufacturing. Export dropped sharply (46.4 for both manufacturing and non-manufacturing). Output/selling prices remain well below the 50 mark suggesting ongoing deflationary pressures (47.4 and 48.6 respectively). Other data published this morning showed that profit at industrial firms in 2024 (-3.3%) dropped for the third consecutive year, despite an uptick at the end of last year. The decline mirrors the impact of ongoing deflationary tendencies and persistent weak (domestic) demand despite a long series of stimulus majors put in place. Comments from the Statistical office attributed the uptick toward the end of the year due to the impact of stimulus measures providing subsidies from purchases of some goods. The yuan (USD/CNY 7.266) this morning declines in line with broader USD strength after Friday’s sharp rebound.

Nasdaq Futures 2% Down on Worries that AI Models Could Run on Cheaper Models

Last week wrapped up with a striking contrast: bullish momentum through most of the week gave way to a bearish close on Friday. Donald Trump's smooth inauguration and a bold $500bn AI infrastructure pledge fueled market optimism, further amplified by Netflix's stellar quarterly results. However, the narrative shifted dramatically as Friday's PMI data exceeded expectations across the US and Europe. The stronger-than-anticipated economic indicators tempered hopes for Federal Reserve (Fed) rate cuts, which had been bolstered by Trump's earlier calls for lower interest rates. A set of stronger-than-expected PMI data prompted investors to recalibrate their Fed outlook, weighing stronger economic growth against the likelihood of a more hawkish Federal Reserve response.

A such, the Stoxx 600 retreated after hitting a fresh record. The S&P500 and Nasdaq traded lower as well, and futures, especially Nasdaq futures, are looking pretty bad this morning with a more than 2% slide at the time of writing hammered by the news that the Chinese startup DeepSeek could run its latest AI model on less advanced chips... and could disrupt the US tech’s global dominance.

But keep calm and breath. It’s probably too early to bet that DeepSeek will challenge the global AI leaders and disrupt the US tech’s dominance. This week’s Big Tech earnings will certainly give a stronger conviction to those looking for a fresh direction.

Earnings

Four of the Magnificent 7 stocks – Microsoft, Meta, Tesla and Apple – and ASML are due to announce their Q4 earnings this week but there is more reluctance than hope as the profit growth of these companies – that are confronted to very tough comparison – is expected to show the slowest pace in two years. In numbers, the Mag7 stocks eked out a 76% return in 2023 – the first year of the AI craze - but are expected to print an earnings increase of 34% in 2024, that is expected to slow down to 18% this year according to Bloomberg. And if you pull Nvidia out of this, the remaining magnificent companies are expected to print just 3% increase in their profits this year. That’s not very exciting at the current valuations. There are two options for the valuations to normalize: either the earnings will go up or prices will come down. Many investors, this year, bet for the second option and expect that the tech rally will show cracks and gove way to a rotation from Big Tech toward the more cyclical sectors of the US, and beyond the US. So far, 16% of the S&P500 reported their Q4 earnings and 80% delivered a positive EPS surprise. Besides the four of the Mag7 companies, other big names like Intel, Visa and Mastercard, and the oil giants will be going to the earnings confessional. It will be a big week of earnings.

Big week for central banks

It will be a big week for central bank decisions, as well. The Fed is expected to announce its latest rate decision this Wednesday, and is set for an almost certain no action as the Fed members will certainly want to consider the risks to inflation posed by Donald Trump’s various growth-boosting and trade-restricting policies. The US yields are softer this morning on news that Trump will not impose 25% tariffs on Colombia as he said he would a few hours before, but the dollar index kicks off the week with a rebound above the 50-DMA. Despite Trump’s willingness to push the Fed for unnecessary rate cuts to boost economy, the US economy doesn’t necessarily need a boost. The jobs number keep coming unexpectedly strong and growth remains robust thanks to solid consumer spending. The Q4 growth update for the US economy will be released on Thursday this week, and may show that the US economy grew 2.7% last quarter – slightly lower than 3.1% printed at the last update – but the price pressures may have increased from 1.9% to 2.5%. And the rising price pressures - while growth nears 3% - is certainly not favourable for further rate cuts.

Across the Atlantic Ocean, however, the Q4 growth due to be released a few hours before the US growth data, is expected to print a meagre 0.1% growth in Q4 in comparison to the US’ 2.7%, giving the European Central Bank (ECB) enough reason to cut the rates on the old continent as long as inflationary pressures remain under control. As such, the EURUSD that saw a decent rally above the 1.05 mark on Friday, looks softer this morning. Levels above the 1.05 are interesting top selling opportunities for investors that continue to bet that the growth gap between the US and the eurozone and the diverging Fed and ECB outlooks hint at a sustained euro weakness, rather than a sustainable recovery of the single currency. The ECB is expected to a 25bp cut when it meets on Thursday.

Note that the European economies are not flourishing to boost inflation but the recent rise in energy prices need dome close monitoring. Crude prices rallied up to 20% between mid-December to mid-January, while the European nat gas prices jumped more than 25% over the same period and are nearly 120% up since February 2024 dip. While crude oil extends retreat this morning – also hammered by another set of soft PMI figures from China – the pressure in European nat gas prices will likely continue on the back of cold winter weather in Europe and falling nat gas reserves. Italy, for example, which has the EU’s second biggest storage sites after Germany, is worried about the falling underground storages – that are just around 58% full right now compared to 74% last year – and is willing to replenish them as early as next month instead of waiting until April. The news is mostly priced in, but the price retreats attract dip buyers and the risks remain tilted to the upside – a thing that could shift the ECB outlook toward a more cautious tone, slow the urge to sell the euro but not yet reverse the bearish trend against the US dollar.

Elsewhere, the Bank of Canada (BoC) is expected to lower its rate by 25bp this week, China will be closed most of the week due to the Lunar New Year break and inflation in Tokyo due Friday is expected to show further rise to 2.5%. The Bank of Japan’s (BoJ) decision to hike rates and revise the inflation forecast higher didn’t trigger a major reaction in the USDJPY – as the move was broadly priced in. The USDJPY tested but couldn’t clear the 50-DMA and the week starts looking supportive of further gains in the USDJPY.

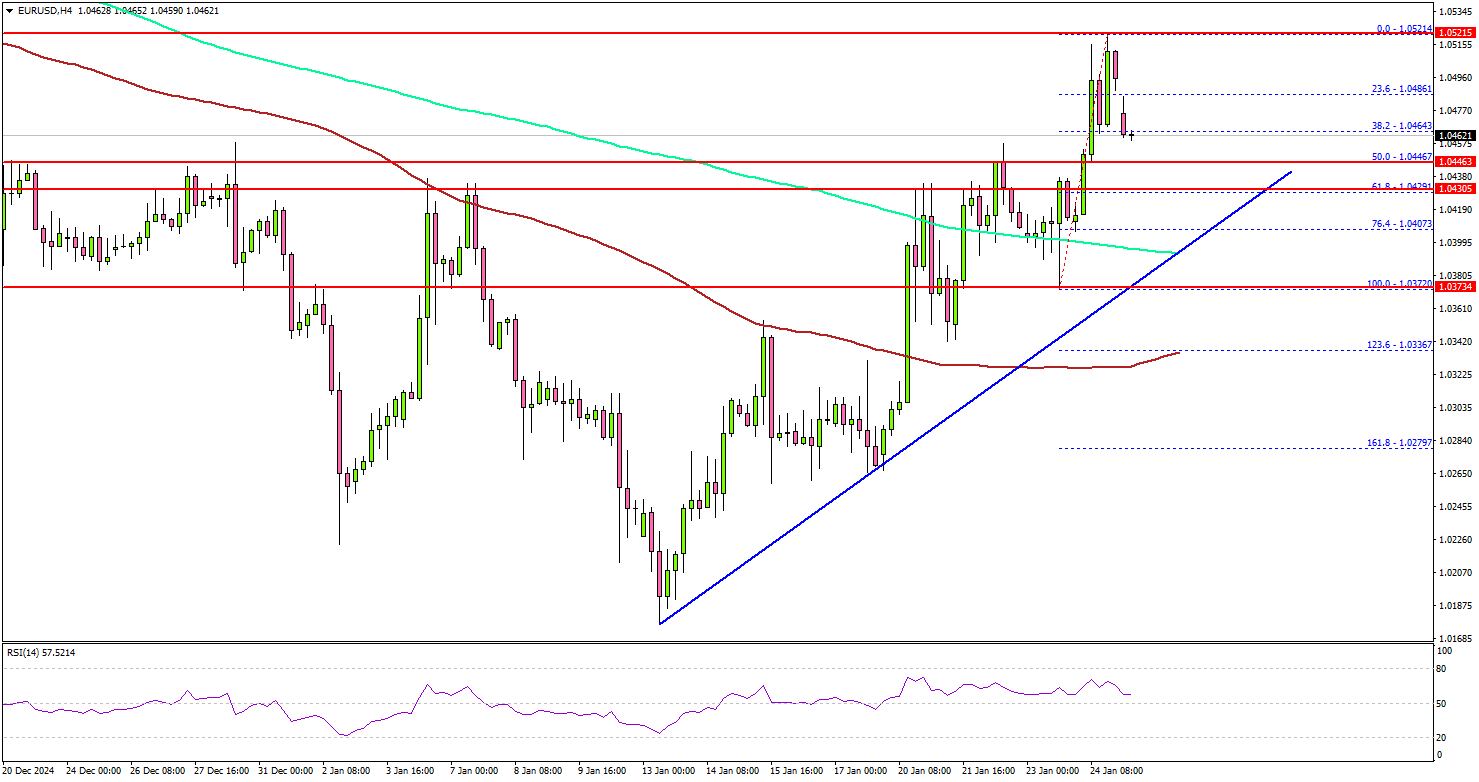

EUR/USD Recovery Hits a Pause: Is the Upside Still Intact?

Key Highlights

- EUR/USD started a decent increase above the 1.0400 resistance.

- A connecting bullish trend line is forming with support at 1.0430 on the 4-hour chart.

- GBP/USD gained pace for a move above the 1.2400 resistance.

- USD/JPY is consolidating below the 156.50 resistance.

EUR/USD Technical Analysis

The Euro found support and started a recovery wave above 1.0350 against the US Dollar. EUR/USD climbed above 1.0400 to move into a short-term positive zone.

Looking at the 4-hour chart, the pair was able to surpass 1.0450, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour). Finally, it tested the 1.0520 resistance zone.

A high was formed at 1.0521 and the pair is now correcting some gains. There was a move below the 1.0500 level. On the downside, immediate support sits near the 1.0445 level or the 50% Fib retracement level of the upward move from the 1.0372 swing low to the 1.0521 high.

The next key support sits near the 1.0430 level. There is also a connecting bullish trend line forming with support at 1.0430 on the same chart. Any more losses could send the pair toward the 1.0400 level.

On the upside, the pair seems to be facing hurdles near the 1.0500 level. The next major resistance is near the 1.0520 level. A close above the 1.0520 level could set the tone for another increase. In the stated case, the pair could even clear the 1.0580 resistance.

Looking at GBP/USD, the pair started a short-term recovery wave but the bears might remain active near the 1.2500 resistance.

Upcoming Economic Events:

- German IFO Business Climate Index for Jan 2025 – Forecast 84.6, versus 84.7 previous.

What Next: Fed, ECB and BoC Will Decide on Rates

The new week will be packed with monetary policy news.

Most observers expect the Bank of Canada to cut its key rate by 25 points to 3.0% on Wednesday, 29 January. The previous two cuts have been 50 pips each, but traders can’t completely rule out hints of a pause or even keeping the rate on hold.

Next, the Fed will take the stage, where it is expected to keep the rate on hold after three rate cuts. The main intrigue is the Fed’s view on inflation and the outlook of monetary policy for the rest of the year. Expectations of one or two rate cuts have been building again in recent days, which has halted the dollar’s rise.

On Thursday, 30 January, the ECB is expected to cut its key rate by 25 points. This could be the first of four cuts expected from the eurozone this year. The approach is softer than its rivals’, putting pressure on the euro.

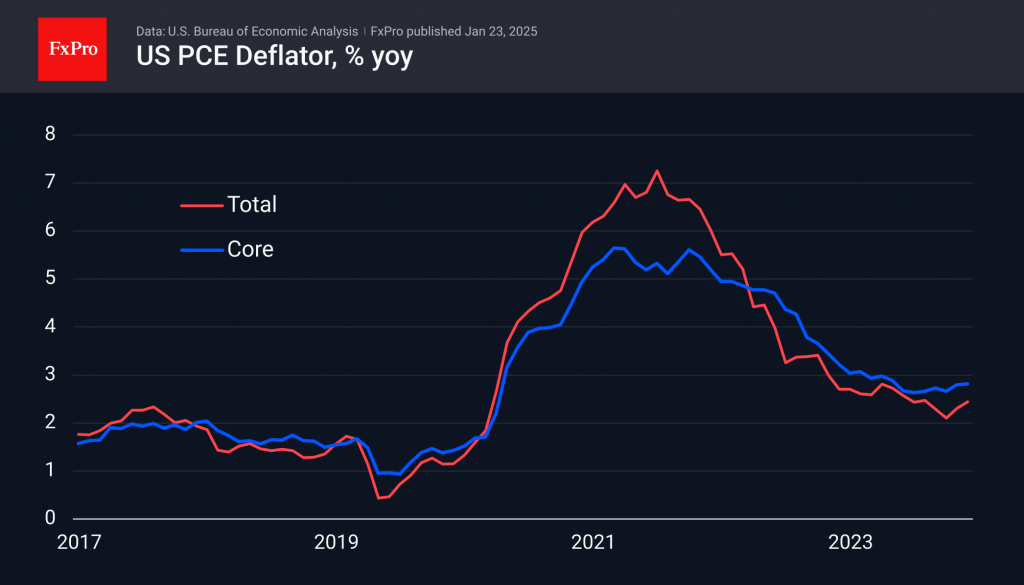

On Friday, 31 January, attention will turn to the US personal consumption price index data. This is the Fed’s main inflation benchmark. And this metric shows an acceleration in price growth over the past six months. A slowdown is favourable for equities and negative for the dollar.