Sample Category Title

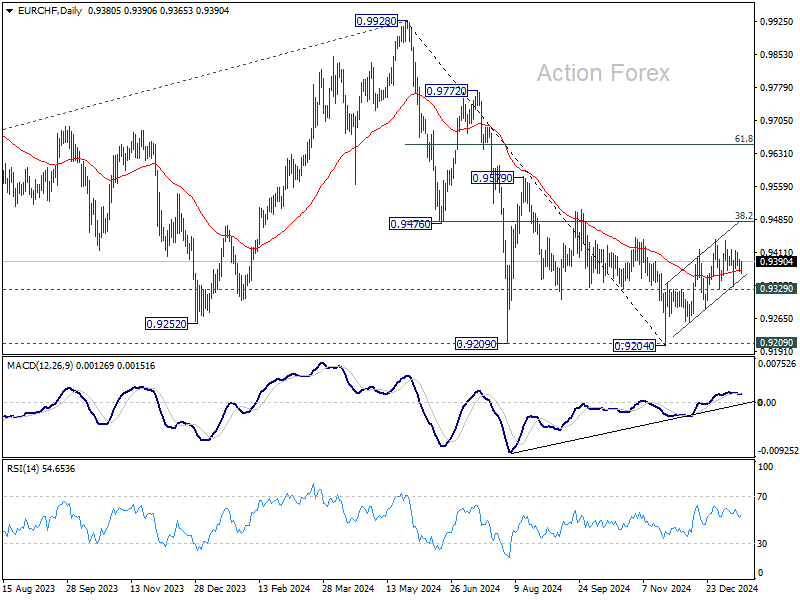

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9369; (P) 0.9385; (R1) 0.9398; More....

Sideway trading continues in EUR/CHF and intraday bias remains neutral. Corrective rebound from 0.9204 could still extend higher. But upside should be limited by 0.9481 fibonacci resistance. On the downside, firm break of 0.9329 support will argue that the correction has completed, and turn bias back to the downside for 0.9284 support first.

In the bigger picture, while corrective rebound from 0.9204 might extend higher, strong resistance could be seen from 38.2% retracement of 0.9928 to 0.9204 at 0.9481 to limit upside. Down trend from 0.9928 (2024 high) is still in favor to resume through 0.9204/9 support zone at a later stage.

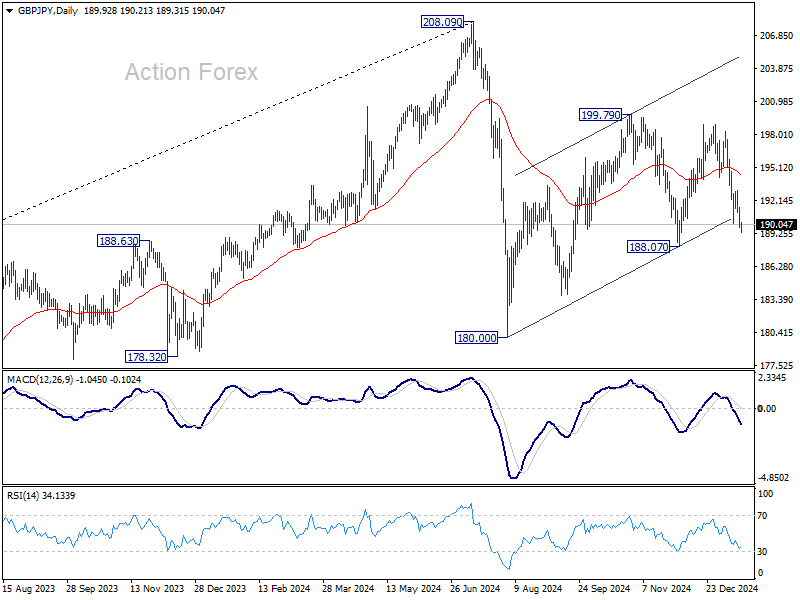

GBP/JPY Daily Outlook

Daily Pivots: (S1) 189.24; (P) 190.39; (R1) 191.01; More...

Intraday bias in GBP/JPY remains mildly on the downside for the moment. Fall from 198.94 is in progress for 188.07 support. Firm break there will argue that corrective pattern from 180.00 has finished too, and larger decline from 208.09 might be ready to resume. On the upside, above 193.01 resistance will delay the bearish case and turn intraday bias neutral again.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

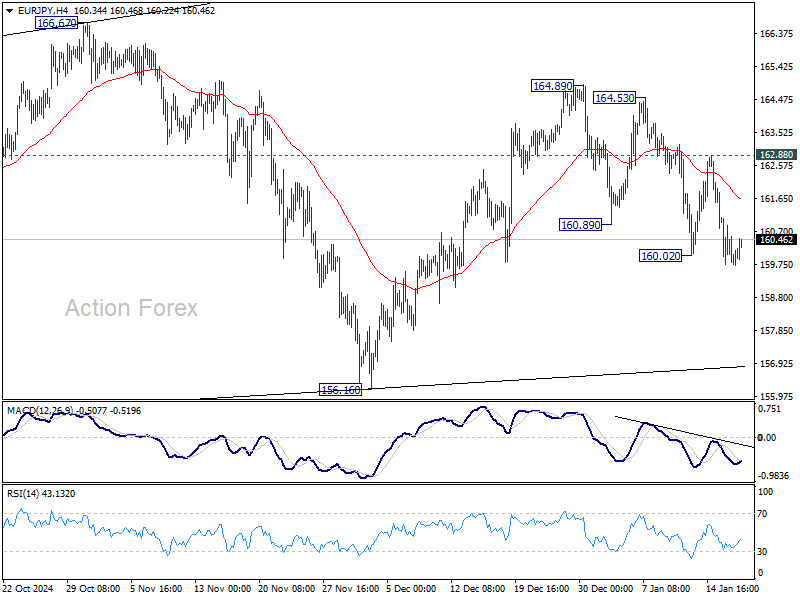

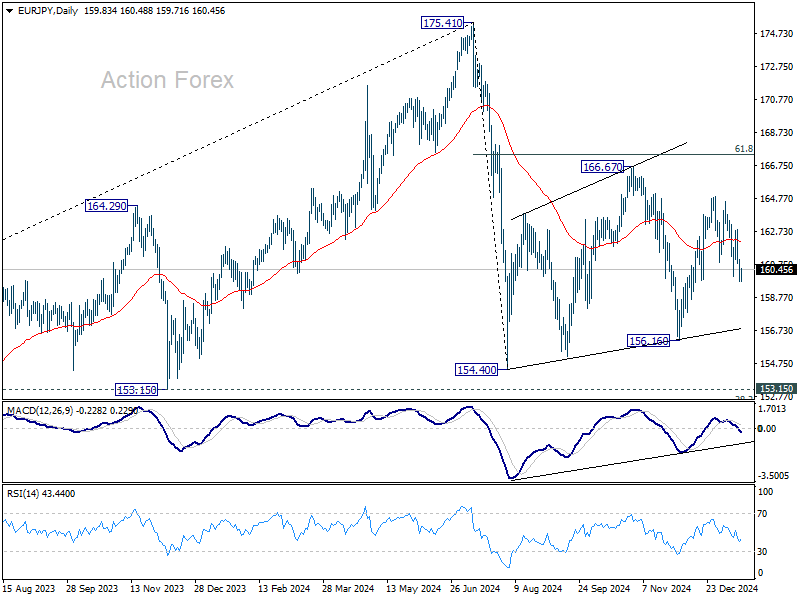

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.32; (P) 160.23; (R1) 160.72; More...

Intraday bias in EUR/JPY stays mildly on the downside at this point. Fall from 164.89 is in progress for 156.16 support. Firm break there will argue that corrective pattern from 154.40 has completed, and fall from 175.41 is ready to resume. For now, risk will stay on the downside as long as 162.88 resistance holds, in case of recovery.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

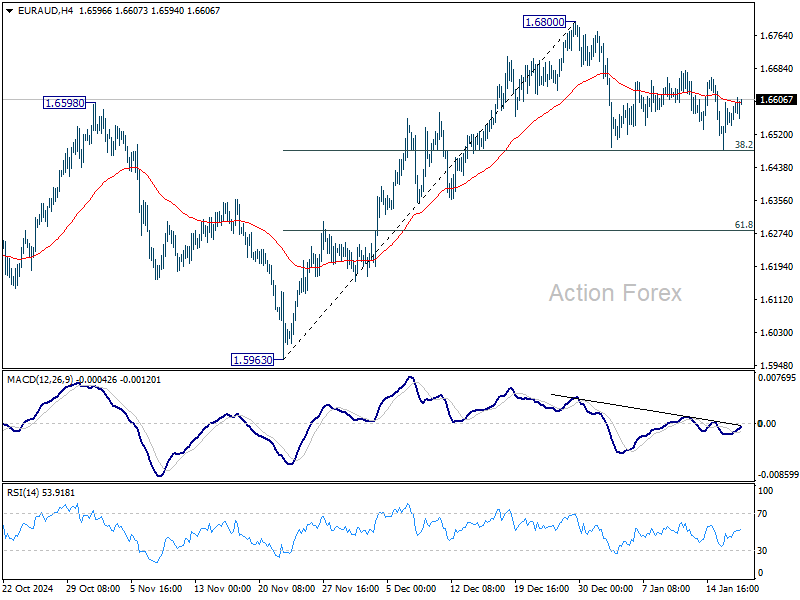

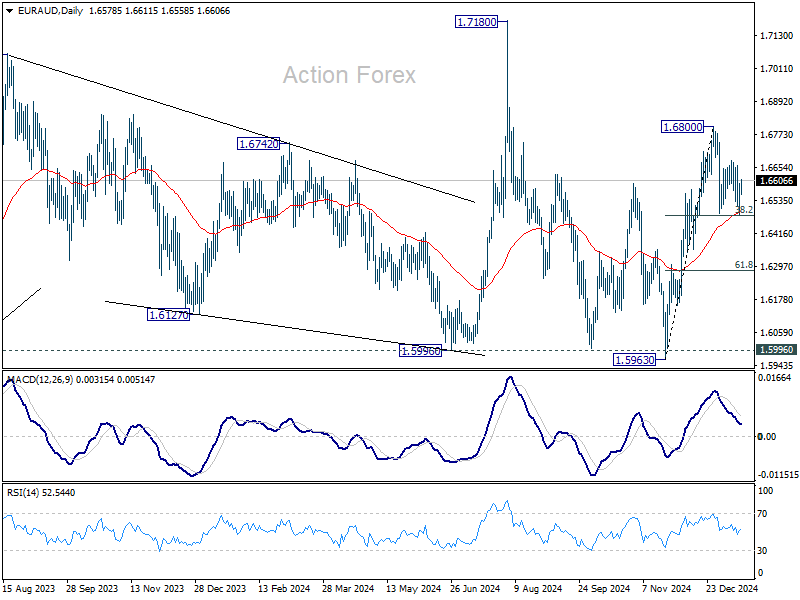

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6512; (P) 1.6556; (R1) 1.6627; More...

EUR/AUD is still bounded in consolidation from 1.6800 and intraday bias remains neutral. Strong support is expected from 38.2% retracement of 1.5963 to 1.6800 at 1.6480 to contain downside. Firm break of 1.6800 will resume the rally from 1.5963. However, sustained break of 1.6480 will bring deeper correction 61.8% retracement at 1.6283 instead.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed and deeper decline would be seen.

Eurozone CPI finalized at 2.4% in Dec, core CPI at 2.7%

Eurozone inflation was finalized at to 2.4% yoy in December, up from November's 2.2% yoy. Core CPI, which excludes energy, food, alcohol, and tobacco, held steady at 2.7% yoy. Services made the largest contribution to the annual headline inflation rate (+1.78 percentage points), followed by food, alcohol, and tobacco (+0.51 pp), non-energy industrial goods (+0.13 pp), and energy (+0.01 pp).

In the broader EU, inflation was finalized at 2.7% yoy, up from 2.5% yoy in November. Ireland recorded the lowest annual inflation rate at 1.0%, followed by Italy at 1.4%, with Luxembourg, Finland, and Sweden at 1.6% each. On the other end, Romania (5.5%), Hungary (4.8%), and Croatia (4.5%) posted the highest inflation rates.

Across the EU, annual inflation rose in 19 member states, remained unchanged in one, and fell in seven compared to the previous month.

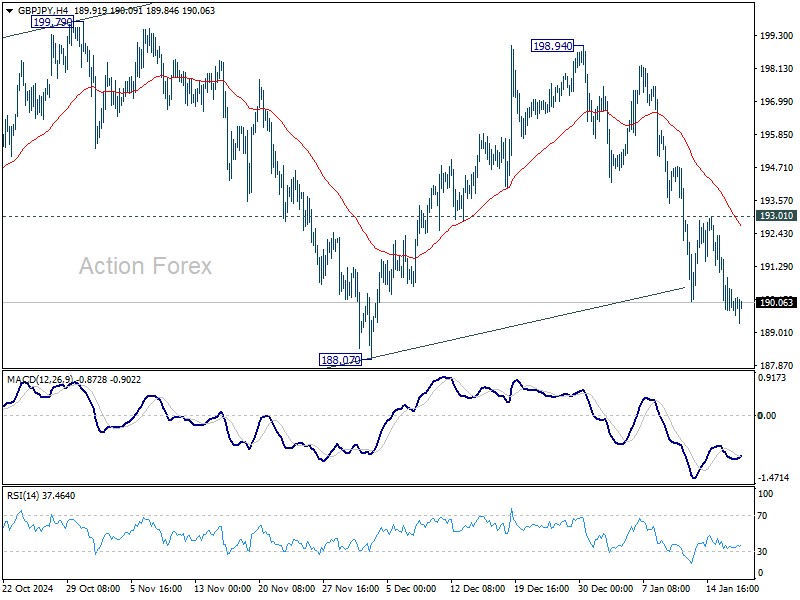

GBP/JPY Technical: Bearish Breakdown from 4-Month Range

- Japan’s overnight swap rates have indicated rising odds of a BoJ interest rate hike next week.

- JPY crosses have lost upside momentum in the last four weeks; the weakest among the G-10 is the GBP/JPY.

- A potential looming medium-term downtrend phase has kickstarted for GBP/JPY.

In the run-up to next Friday, 24 January, the Bank of Japan (BoJ) monetary policy meeting outcome where the consensus is now expecting the BoJ to resume its normalization stance and hike its short-term policy rate by 25 basis points (bps) to bring it higher to 0.50%.

Next week BoJ’s monetary policy meeting is now “live”

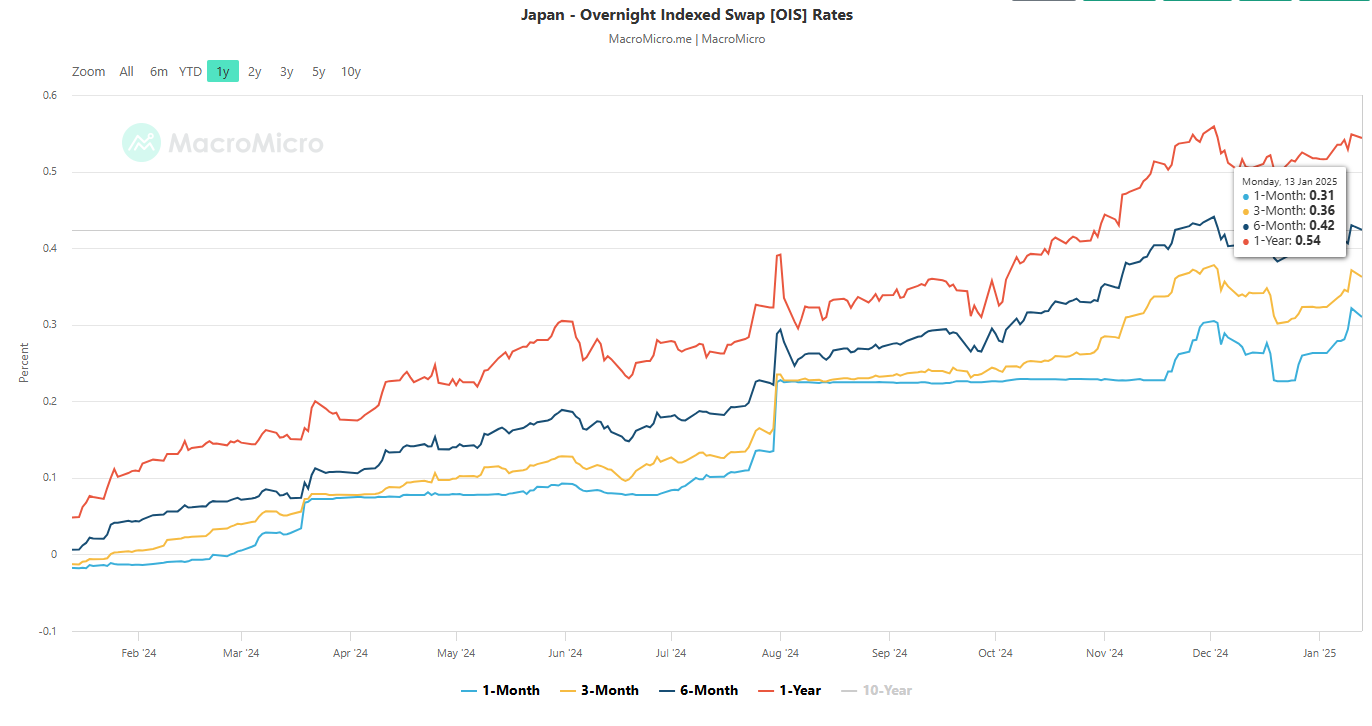

Fig 1: Japan overnight indexed swap rates medium-term trends as of 13 Jan 2025 (Source: MacroMicro, click to enlarge chart)

The spread of the 3-month and 6-month Japan overnight indexed swap rates have started to widen again since 25 December 2024 over the 1-month swap rate. The 3-month and 6-month swap rates have risen to 0.36% and 0.42% respectively, above the 1-month swap rate at 0.31% as of 13 January (see Fig 1).

The widening of the 3-month and 6-month Japan overnight indexed swap rates over its 1-month counterpart suggests an increased odds of an incoming BoJ interest rate hike.

JPY carry trades are losing upside momentum

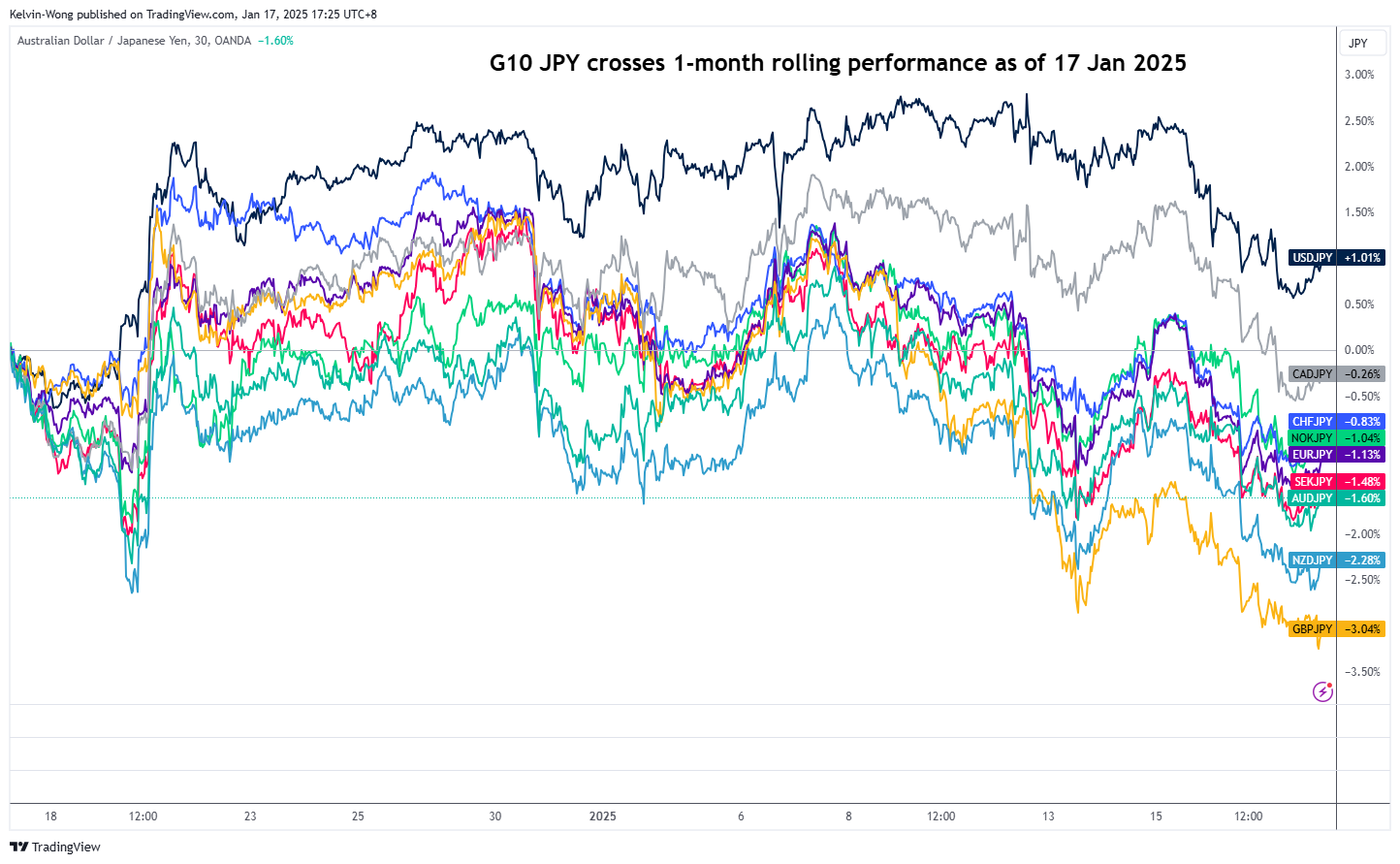

Fig 2: 1-month rolling performances of G-10 JPY crosses as of 17 Jan 2025 (Source: TradingView, click to enlarge chart)

The Japanese yen has not just strengthened against the US dollar but also against other major currencies. Based on a one-month rolling performance as of 17 January, the GBP/JPY is the weakest among the G-10 yen cross pairs with a loss of 3% (the yen has strengthened the most against the pound sterling) (see Fig 2).

Bearish change of medium-term trend for GBP/JPY

Fig 3: GBP/JPY medium-term trend as of 17 Jan 2025 (Source: TradingView, click to enlarge chart)

This week price actions of GBP/JPY have staged a bearish breakdown below a four-month plus range configuration in place since the 5 August 2024 low.

Through the lens of technical analysis, the GBP/JPY is likely to have kickstarted a medium-term (multi-week) downtrend phase that is similar to the prior down move from the 11 July 2024 high of 208.12 to 5 August 2024 low of 180.10 (see Fig 3).

In addition, the daily MACD trend indicator has continued to inch lower below its centreline after the bearish breakdown of its former key parallel ascending trendline support on 16 January, in turn, reinforces the potential start of a new medium-term downtrend phase for the GBP/JPY.

Watch the 194.70 key medium-term pivotal resistance (also the 50-day and 200-day moving averages) with the medium-term support coming at 180.10 (also the long-term secular ascending trendline from the March 2020 low). A break with a daily close below 180.10 increases the odds of the materialization of the medium-term downtrend phase to expose the next support zone at 175.50/172.10 in the first step.

On the flip side, a clearance above 194.70 invalidates the bearish scenario for a squeeze up to retest the 30 October 2024 range resistance of 199.70/80.

GBP/USD Slips After Soft UK Retail Sales

The British pound is lower on Friday. In the European session, GBP/USD is currently trading at 1.2201, down 0.27% on the day. The pound can’t find its footing and is down 2.5% in January and a massive 8.8% since October 1.

UK retail sales miss expectations

UK retail sales ended the week on a disappointing note. December retail sales declined 0.3% m/m, down from a downwardly revised 0.1% gain in November and shy of the forecast of 0.4%. Quarterly, retail sales fell 0.8% in the fourth quarter.

The weak retail data indicates that the UK consumer held tight on the purse strings during the crucial Christmas season. Consumers remain cautious over inflation worries and expectations that interest rates will stay high. Consumer spending is a key engine of economic growth, and the decrease is retail sales has raised fears of stagflation, a toxic mix of high inflation and low growth which will further hurt businesses and households. The UK economy posted negligible growth of just 0.1% in November, after back-to-back months of no growth.

Finance Minister Rachel Reeves could not have been pleased with the soft GDP and retail sales numbers. Reeves delivered a “tax and spend” budget in October 2024 and has admitted that she needs the economy to show stronger growth in order to increase tax revenue and carry out her spending plans. If the weak economy does not turn around soon, Reeves could find herself on the hot seat.

In the US, retail sales gained 0.4% m/m in December after an upwardly revised gain of 0.8% in November and below the forecast of 0.6%. Annually, retail sales rose 3.9%, below a downwardly revised 4.1% gain in November and above the forecast of 4.0%. The numbers show that consumer spending remains solid and the Federal Reserve isn’t under pressure to lower interest rates anytime soon.

GBP/USD Technical

- GBP/USD is testing support at 1.2225. Below, there is support at 1.2188

- 1.2274 and 1.2311 are the next resistance lines

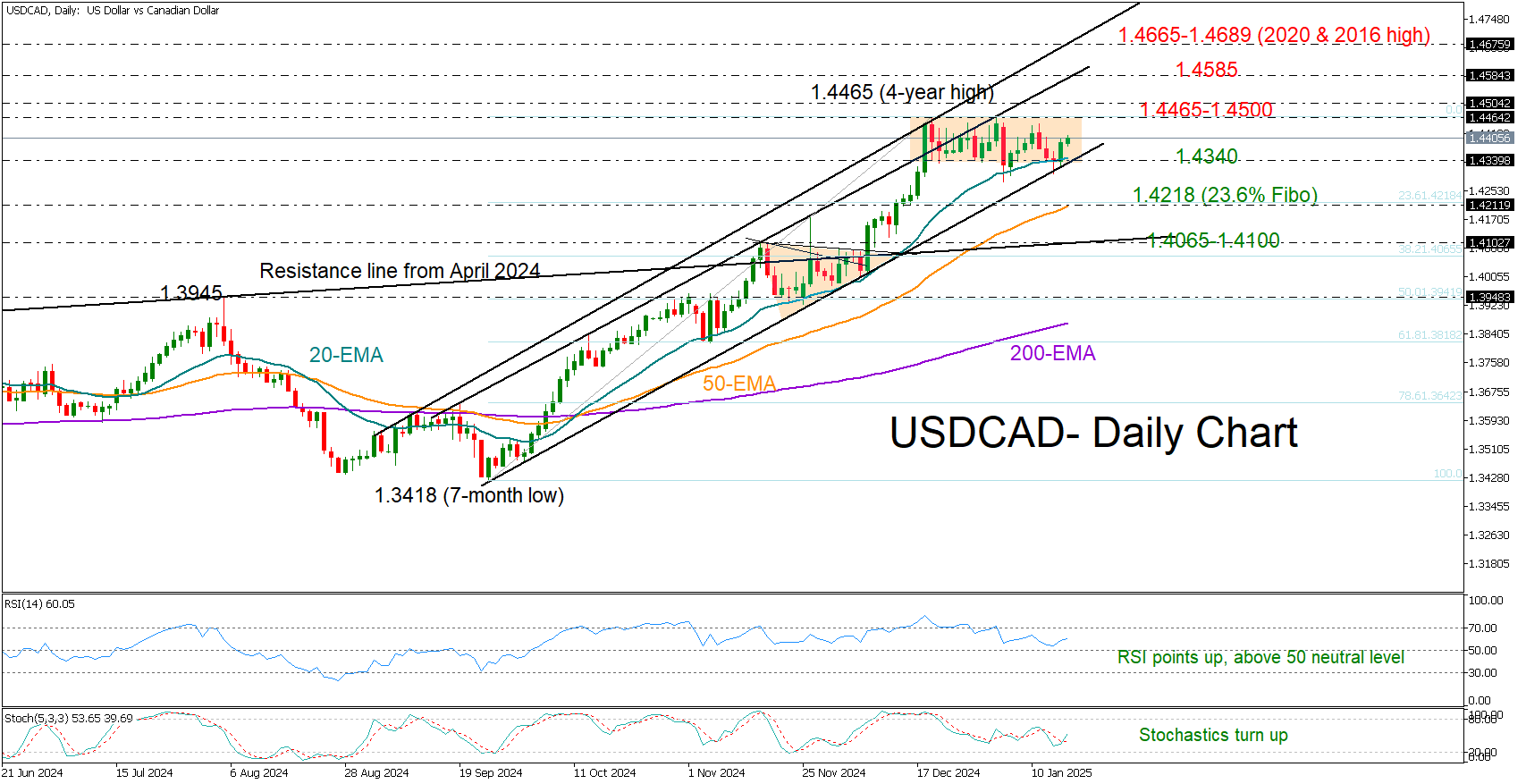

USD/CAD: Ready for a New Bullish Wave?

- USD/CAD stays supported around 20-EMA.

- Bullish trend continuation likely; eyes on the 1.4465 top.

USD/CAD found solid footing near its 20-day exponential moving average (EMA) around 1.4340 for the second time this month, sparking optimism that the ongoing sideways move could give way to an upward move. Note that the 20-day EMA has been an important pivotal point since November.

In other encouraging signs, the RSI has turned up above its 50 neutral mark, and the stochastic oscillator has also posted a positive cross, both suggesting increasing buying interest.

If buyers manage to break the short horizontal trajectory above the 1.4465-1.4500 ceiling, the resistance trendline at 1.4585 could add some pressure ahead of the 2020 and 2016 highs registered within the 1.4665-1.4689 zone. More gains from there could stall near the 1.4800 barrier taken from 2003.

On the flip side, if sellers squeeze the price below the 1.4340 base, the 23.6% Fibonacci retracement of the September-December upleg could come to the rescue along with the 50-day EMA at 1.4218. A step lower could retest the former constraining line at 1.4100 and perhaps the 38.2% Fibonacci mark of 1.4065. Then, the spotlight could shift to the 50% Fibonacci of 1.3940.

All in all, USDCAD seems to have set the stage for a bullish breakout. Traders could wait for a close above the top of 1.4465 before expecting further upward price movement.

FTSE 100 Index May Reach 8500

As shown on the chart of the UK stock index FTSE 100 (UK 100 on FXOpen):

→ It has risen by over 3% in three days;

→ It is near the record high set in May last year and may reach the psychological level of 8500 points.

Bullish sentiment has been supported by yesterday's news of GDP recovery – according to media reports, the economy grew by 0.1% in November 2024 (compared to a previous decline of 0.1%), primarily driven by the dominant services sector.

Technical analysis of the FTSE 100 (UK 100 on FXOpen) chart shows that since mid-2024, the index has predominantly fluctuated within the 8000–8400 range, only briefly moving beyond it, which was accompanied by spikes in the RSI indicator.

The current RSI level indicates strong overbought conditions, making the FTSE 100 (UK 100 on FXOpen) vulnerable to a pullback. Should this occur, it will provide important insights into the strength of demand. This could be assessed by the index’s ability to remain above the 8333 support level and the lower boundary of the ascending channel (marked in blue).

Potential challenges for bulls are highlighted by MT Newswires, which report that analysts forecast higher inflation and weaker growth in 2025, amid expectations of a significant rise in labour costs.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

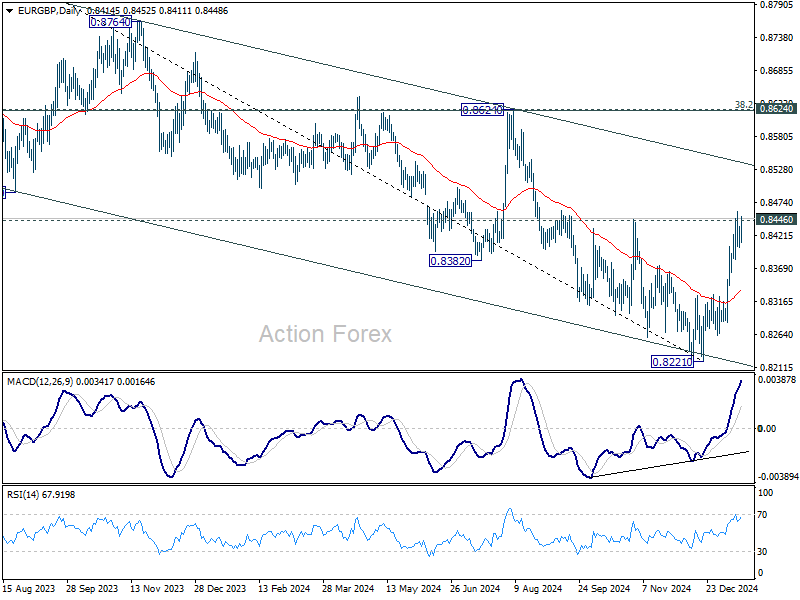

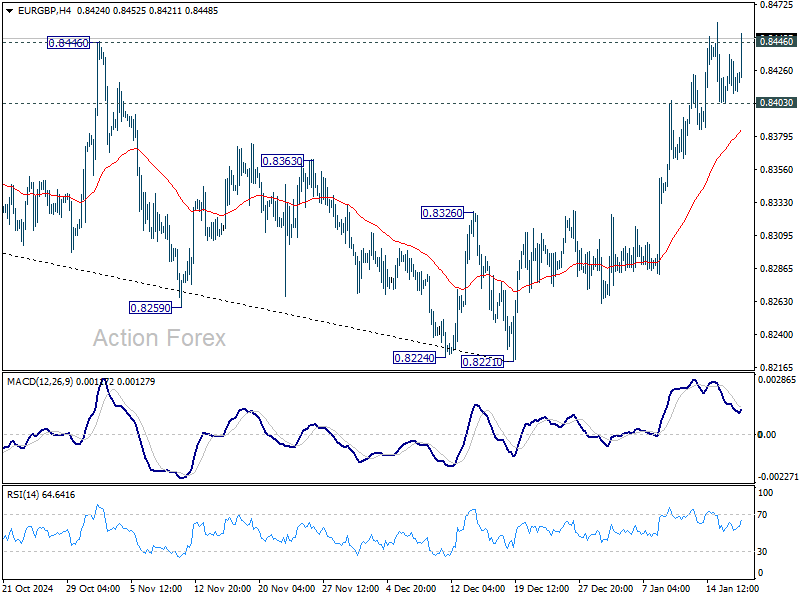

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8404; (P) 0.8421; (R1) 0.8435; More...

Intraday bias in EUR/GBP remains neutral first with focus on 0.8446 resistance. Decisive break there will resume the rally from 0.8221 to 0.8624 cluster resistance zone. On the downside, however, break of 0.8403 minor support will indicate rejection by 0.8446, and turn bias back to the downside for 55 D EMA (now at 0.8332).

In the bigger picture, considering bullish convergence condition in D MACD, decisive break of 0.8446 resistance and 55 W EMA (now at 0.8446) should confirm medium term bottoming at 0.8221, just ahead of 0.8201 key support (2022 low). Further rally should be seen towards 0.8624 key resistance, even as a correction to the down trend from 0.9267 (2022 high). Overall, however, medium term outlook will be neutral at best until decisive break of 0.8624 cluster zone (38.2% retracement of 0.9267 to 0.8221 at 0.8621). Risk will stay on the downside even in case of strong rebound.