Sample Category Title

Political Uncertainty Limits Dollar’s Rebound, Busy Week ahead With RBA, BoE and NFP

Dollar recovers mildly today but momentum has been weak. There is no change in it's general down trend against Euro, Yen and Sterling. And, not the mention the greenback's weakness against Canadian and Aussie. Political uncertainty in US is one of the key factors in limiting any rebound attempt in the greenback. Fed fund futures are now pricing in less than 50% chance of another rate hike by end of the year. And indeed, markets are starting to question that even if Fed does hike, the sluggish inflation outlook will keep it standing pat next year. The drama in the White House seems never-ending with US President Donald Trump replacing his chief of staff Reince Priebus last Friday. Retired General John Kelly was installed in the place. Some analysts noted that could be a turning point for Trump as he's now shaking up his top team.

Russia orders 755 US diplomats to leave

Meanwhile, Russian President Vladimir Putin said on Sunday that he ordered US to cut diplomatic staff in the country. Putin said that was a response to the "illegal restrictions" imposed by US. That came days after US Congress passed a new round of sanctions for punishing Russia for interfering in last year's election and military agrees in Ukraine and Syria. It's initially reported that Russia asked 755 US diplomats to go. And after that, the total number of American diplomats in Russia will be brought down to 455, same as Russian diplomats in US.

Non-farm payroll not likely to help Dollar

There are a number of important economic data from US this week, including ISM indices and non-farm payroll. While the data will be watched closely as usual, we believe it's unlikely to revive the expectation of faster Fed tightening even if it posts strong upside surprises. The key to Fed's policy will still lie on the implementation of Trump's fiscal policies and tax reforms. Without that, markets will continue to doubt whether the US economy can withstand another more rate hikes. On the other hand, we could very likely see another round of selloff in the greenback if NFP disappoints.

ECB Lautenschlaeger: It's important to prepare for the exit in good time

In Eurozone, ECB governing council member Sabine Lautenschlaeger said in a newspaper remarks that "the expansionary monetary policy has both advantages and side effects. As time passes, the positive effects get weaker and the risks increase." And, she urged that "it's important to prepare for the exit in good time." But she noted that "what's crucial in that context is a stable trend in the rate of inflation towards our objective of just under 2 percent. It's not quite there yet."

Released today...

Official China PMI manufacturing dropped to 51.4 in July, down from 51.7 and missed expectation of 51.5. Official non-manufacturing PMI dropped to 54.5, down from 54.9. Japan industrial production rose 1.6% mom in June, housing starts rose 1.7% yoy. New Zealand building permits dropped -1.0% mom in June. Australia TD securities inflation rose 0.1% mom in July.

In European session, German retail sales rose 1.1% mom in June. UK will release mortgage approvals an M4 money supply. Eurozone CPI will be a key focus and unemployment rate will also be featured. Canada will release IPPI and RMPI later in the day while US will release pending home sales.

RBA and BoE watched closely ahead too

While there are a number of key events ahead, RBA rate decision will be the first one to watch. The RBA meeting due tomorrow would bring no change in the monetary policy. However, the central bank's "neutral rate" rhetoric gave Aussie a boost. At the July meeting minutes, RBA noted that neutral nominal cash rate is currently at around 3.5%, "given that medium-term inflation expectations were well anchored around 2.5%, although there is significant uncertainty around this estimate". We would like to see if policymakers do any tweak or elaboration on such reference this week. RBA's Monetary Policy Statement due on Friday would provide update economic forecasts.

BoE Super Thursday will be another key focus. It would be of great interest to see how policymakers vote for the policy, after the 5-3 split (Ian McCafferty, Kristin Forbes and Michael Saunders voting for a rise) in June. The dilemma facing the UK is overshooting inflation on one side and lackluster economic growth together with great uncertainty in Brexit negotiation on the other side. The July inflation report show moderation on the price level the headline reading stayed above the BoE's 2% target. UK's 2Q17 GDP grew 0.3% with the first half growth regarded as "notable slowdown" by the government. We believe the Bank rate would stay unchanged at 0.25%. BoE's quarterly inflation report would also be released alongside the meeting minutes.

Here are some more highlights for the week ahead:

- Tuesday: RBA rate decision; China Caixin PMI manufacturing; Eurozone GDP, PMI manufacturing revisions; UK PMI manufacturing; US personal income and spending, ISM manufacturing

- Wednesday: New Zealand employment; Australia building approvals, Japan consumer confidence; Swiss retail sales, SVME PMI; Eurozone PPI; US ADP employment

- Thursday: Australia trade balance; Eurozone retail sales, PMI services revision, ECB bulletin; UK PMI services, BoE rate decision; US jobless claims, ISM services, factory orders

- Friday: Australia retail sales; Japan labor cash earnings; German factory orders; Canada trade balance, employment, Ivey PMI; US non-farm payrolls, trade balance

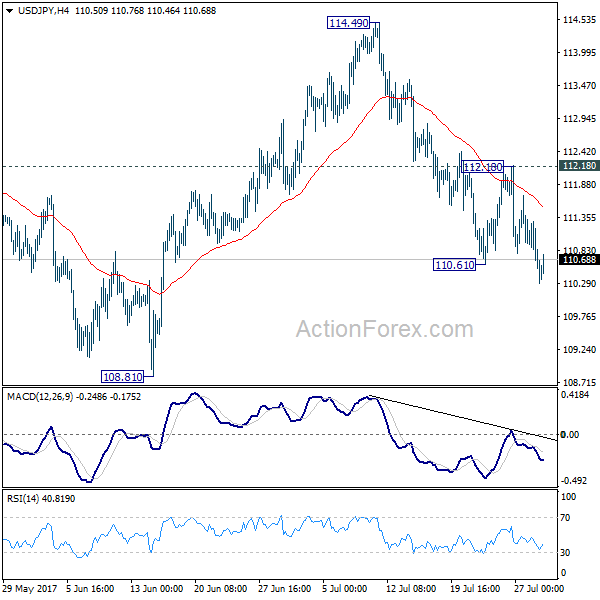

USD/JPY Daily Outlook

Daily Pivots: (S1) 110.36; (P) 110.84; (R1) 111.14; More...

USD/JPY recovers mildly today but stays well below 112.18 resistance. Intraday bias remains on the downside for the moment. Current decline from 114.49 should extend to 108.81 support first. Break there will resume whole correction from 118.65 and target 61.8% retracement of 98.97 to 118.65 at 106.48. Nonetheless, break of 112.18 resistance will dampen this bearish view and turn focus back to 114.49 resistance instead.

In the bigger picture, the corrective structure of the fall from 118.65 suggests that rise from 98.97 is not completed yet. Break of 118.65 will target a test on 125.85 high. At this point, it's uncertain whether rise from 98.97 is resuming the long term up trend from 75.56, or it's a leg in the consolidation from 125.85. Hence, we'll be cautious on topping as it approaches 125.85. If fall from 118.65 extends lower, down side should be contained by 61.8% retracement of 98.97 to 118.65 at 106.48 and bring rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M Jun | -1.00% | 7.00% | 6.90% | |

| 23:50 | JPY | Industrial Production M/M Jun P | 1.60% | 1.50% | -3.60% | |

| 1:00 | AUD | TD Securities Inflation M/M Jul | 0.10% | 0.10% | ||

| 1:00 | CNY | Manufacturing PMI Jul | 51.4 | 51.5 | 51.7 | |

| 1:00 | CNY | Non-manufacturing PMI Jul | 54.5 | 54.9 | ||

| 5:00 | JPY | Housing Starts Y/Y Jun | 1.70% | 0.10% | -0.30% | |

| 6:00 | EUR | German Retail Sales M/M Jun | 1.10% | 0.20% | 0.50% | |

| 8:30 | GBP | Mortgage Approvals Jun | 65K | 65K | ||

| 8:30 | GBP | M4 Money Supply M/M Jun | 0.20% | -0.10% | ||

| 9:00 | EUR | Eurozone Unemployment Rate Jun | 9.20% | 9.30% | ||

| 9:00 | EUR | Eurozone CPI Estimate Y/Y Jul | 1.30% | 1.30% | ||

| 9:00 | EUR | Eurozone CPI - Core Y/Y Jul A | 1.10% | 1.10% | ||

| 12:30 | CAD | Industrial Product Price M/M Jun | -0.20% | |||

| 12:30 | CAD | Raw Materials Price Index M/M Jun | -1.80% | |||

| 14:00 | USD | Pending Home Sales M/M Jun | 1.00% | -0.80% |

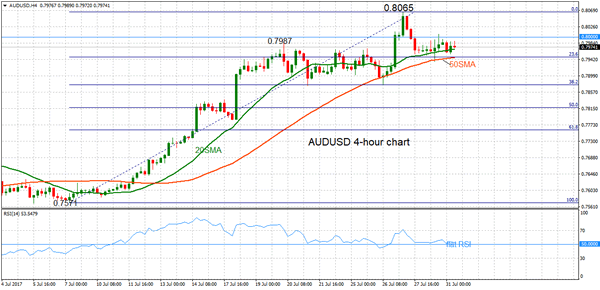

AUDUSD Shifts To Neutral After Rally To 2-Year High

AUDUSD has a neutral bias after pausing a rally that took the pair to a high of 0.8065 on July 27. This is the highest level since May 2015. The underlying market structure is bullish after a sharp rise from the July 7 low of 0.7571. Looking at the 4-hour chart, upside momentum has faded as indicated by the flat RSI. Consequently, AUDUSD is trading sideways within a range.

The key psychological level at 0.8000 is now a strong resistance level broadly holding so far even though it was pierced last week. AUDUSD closed below 0.8000 on July 28. Support is provided by the 50-period moving average (MA). This is close to a Fibonacci level at 0.7947 (23.6% retracement of the upleg from 0.7571 to 0.8065). Further support is provided by subsequent Fibonacci levels at 0.7875, 0.7816 (July 26 low) and 0.7759.

Prices need to rise above the key 0.8000 level to move out of the range and weaken downside pressure. From this level, AUDUSD would see a re-test of the 0.8065 high and a break of this would see a resumption of the uptrend.

The positively aligned moving averages are supporting a bullish outlook in the short-term. There was a bullish crossover of the 20-period MA with the 50-period one on July 12.

There has been no confirmation of a trend reversal yet and the current consolidation pattern could be a temporary pause before the uptrend resumes. For now, the bias remains neutral on the 4-hour chart, with high odds of a shift to bullish if there is a daily close above 0.8000.

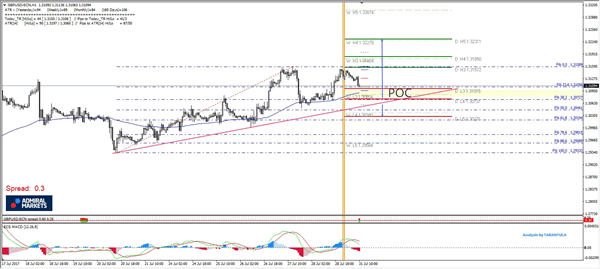

Daily Technical Analysis: GBPUSD Uptrend Continuation If The Price Stays Above 1.3060

The GBP/USD is in uptrend and we can see the POC zone clearly below the price. The POC 1.3075-1.3100 might look a bit stretched but that happens due to many individual confluence points that are found within the zone – W L3, ATR pivot, D L3, trend line, EMA89, 38.2 fib + ATR (14) has slightly increased. If we see a retracement in the zone, the price might bounce towards 1.3157 and 1.3180. Only above 1.3180 we will see another bullish wave towards 1.3230. As long as the price stays above 1.3060 bulls will have the upper hand, else below 1.3060, short term stops might be triggered so 1.3025 will be possible.

W L3 - Weekly Camarilla Pivot (Weekly Interim Support)

W H3 - Weekly Camarilla Pivot (Weekly Interim Resistance)

W H4 - Weekly Camarilla Pivot (Strong Weekly Resistance)

D H4 - Daily Camarilla Pivot (Very Strong Daily Resistance)

D L3 – Daily Camarilla Pivot (Daily Support)

D L4 – Daily H4 Camarilla (Very Strong Daily Support)

POC - Point Of Confluence (The zone where we expect price to react aka entry zone)

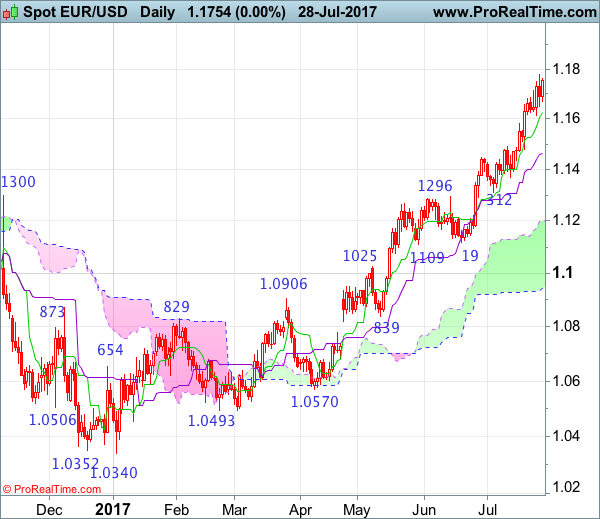

EUR/USD Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Shooting star

• Time of formation: 03 May 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 3 May 2016

• Trend bias: Sideways

EUR/USD – 1.1648

The single currency only eased to 1.1613 before rising again, adding credence to our bullish view that recent upmove is still in progress and price already exceeded indicated upside targets at previous chart resistance at 1.1714, bullishness remains for medium term upmove to extend further gain to 1.1800-10, break there would encourage for headway to 1.1870-80 but near term overbought condition should limit upside and price should falter below 1.1900-10, bring retreat later.

On the downside, whilst initial pullback to 1.1650 and possibly the Tenkan-Sen (now at 1.1628) cannot be ruled out, reckon 1.1583 (previous resistance turned support) would limit downside and bring another upmove to aforesaid upside targets. Below 1.1530-35 would suggest a temporary top is possibly formed and risk test of the Kijun-Sen (now at 1.1475) but a daily close below there is needed to add credence to this view, bring correction to 1.1400 and possibly test of support at 1.1370.

Recommendation: Buy at 1.1590 for 1.1790 with stop below 1.1490.

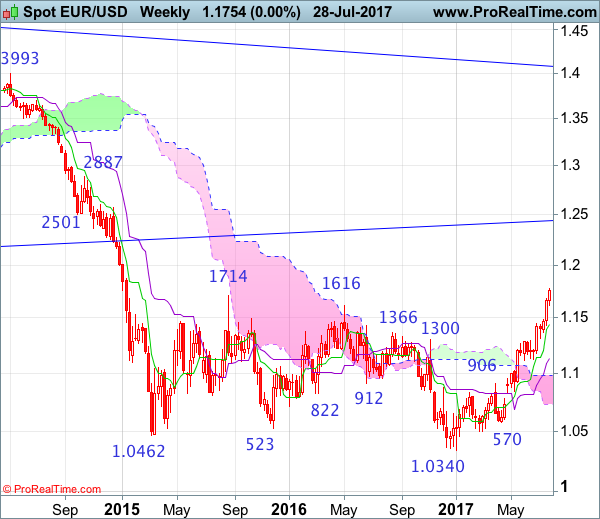

On the weekly chart, as euro has eased after meeting resistance at 1.1777 last week, suggesting minor consolidation would be seen and pullback to 1.1650 and possibly towards support at 1.1613 cannot be ruled out, however, previous resistance at 1.1583 should limit downside and bring another rise later, above said resistance at 1.1777 would extend gain to 1.1800-10, then 1.1870-80, having said that, near term overbought condition should limit upside to 1.1940-50 and price should falter below 1.2000, risk from there is seen for a retreat later.

On the downside, although pullback to 1.1650 and then 1.1613 is likely, reckon 1.1583 (previous resistance turned support) would contain downside and bring another rise later. Below 1.1490-00 would defer and risk test of the Tenkan-Sen (now at 1.1448) but a weekly close below there is needed to suggest a temporary top is possibly formed, bring correction to support at 1.1370, break there would provide confirmation and extend weakness towards 1.1312 support.

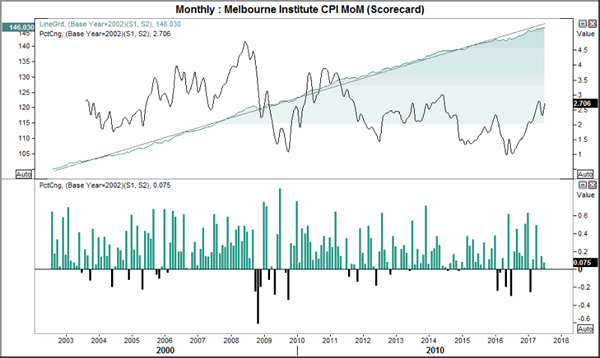

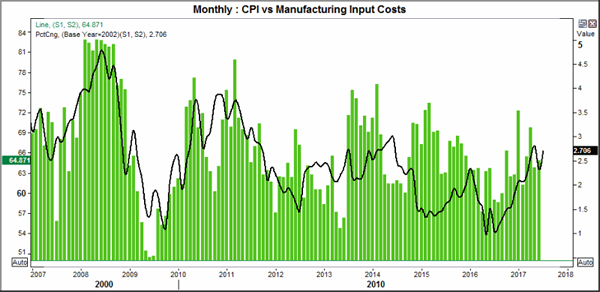

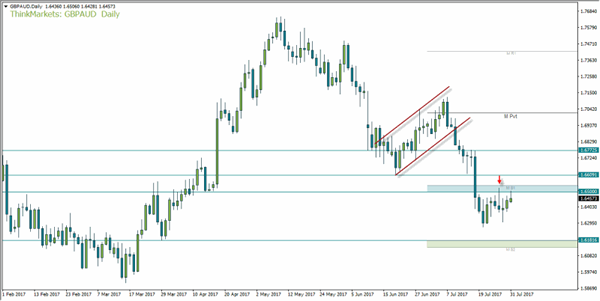

AU Inflation Hits 2.7% | RBA In Focus | GBPAUD

The monthly read of CPI suggests a rosier outlook than the official quarterly read, although at 0.1% MoM this too may soften over the coming months. The RBA is in focus tomorrow to see if a fresh round of jawboning ensues.

Inflation data for Q2 was met with some scepticism, although we prefer to look at the brighter side of it. Yes, broad CPI softened and missed expectations yet the trimmed and weighted mean remained steady and hot the consensus. It is these latter CPI reads the RBA takes more notice of and as they have stabilised at record lows it does raise the potential for a base to occur.

Today the Melbourne Institute released their monthly inflation read which estimates CPI to be at 2.7% YoY and 0.1% MoM. This is the third consecutive month below 0.2% which suggests the YoY rate will soften in due course unless the underlying index spikes higher.

Private sector credit increased by 0.5% MoM, its highest level since December which suggests support for growth and inflation. It is making headway after declining to just 0.2% in January, although seasonality is likely at play here.

Early tomorrow AiG release their manufacturing PMIs. Currently at 55, the index sits above the 1yr average and the sector has enjoyed 9 consecutive months of expansion. We will keep an eye on the input costs as this tends to track CPI relatively well. So, a rise of input costs assumes this to be passed onto the consumer and therefor provide cost-push inflation.

Private sector credit increased by 0.5% MoM, its highest level since December which suggests support for growth and inflation. It is making headway after declining to just 0.2% in January, although seasonality is likely at play here.

Early tomorrow AiG release their manufacturing PMIs. Currently at 55, the index sits above the 1yr average and the sector has enjoyed 9 consecutive months of expansion. We will keep an eye on the input costs as this tends to track CPI relatively well. So, a rise of input costs assumes this to be passed onto the consumer and therefor provide cost-push inflation.

GBPAUD remains beneath the monthly S1 and 1.65 resistance zone. The upper wick of Wednesdays' bearish pinbar remains unchallenged, so we are seeking signs of weakness on H1 and H4 to consider a bearish swing trade. If we are to see prices move higher from here we can still consider fading below 1.66. It's possible we may see an ABC correction terminate here before losses resume.

As this is the last trading day of the month the pivots will be recalculated. So we can finetune potential targets from tomorrow, although the 1.62 area is still viable support as it is just above the 30th March low.

USD/JPY Candlesticks and Ichimoku Analysis

Weekly

• Last Candlesticks pattern: Marubozu

• Time of formation: 14 Nov 2016

• Trend bias: Down

Daily

• Last Candlesticks pattern: Shooting star

• Time of formation: 15 Feb 2017

• Trend bias: Down

USD/JPY – 110.65

The greenback did meet renewed selling interest at 112.20 last week (we recommended to sell dollar at 112.00 and a short position was entered) and has fallen again since, adding credence to ur bearish view that decline from 114.50 is still in progress and downside bias remains for this move to extend weakness to 110.00, having said that, as broad outlook remains consolidative, reckon downside would be limited to 109.40 and said support at 108.82 should remain intact.

On the upside, whilst initial recovery to the Tenkan-Sen (now at 111.37) cannot be ruled out, reckon upside would be limited and resistance at 111.71 would hold, bring another decline later. A daily close above said resistance at 111.71 would defer and risk test of 112.20 but break there is needed to signal the aforesaid decline from 114.50 has ended, bring a stronger rebound to 112.85-90 first.

Recommendation : Hold short entered at 112.00 for 110.00 with stop lowered to 111.75.

On the weekly chart, as dollar has remained under pressure after brief bounce to 112.20 last week, adding credence to our view that top has been formed at 114.50 and consolidation with downside bias remains for weakness to 110.00, then 109.40, however, reckon 108.82-84 (previous support as well as current level of the lower Kumo) would limit downside and price should stay well above support at 108.13, bring recovery later.

On the upside, although recovery to 111.10-20 cannot be ruled out, reckon the Tenkan-Sen (now at 111.66) would limit upside and bring another decline later. Only above said resistance at 112.20 would signal the retreat from 114.50 has possibly ended, bring a stronger rebound to 112.42, then towards 113.00, however, reckon upside would be limited to 113.55-60 and price should falter well below said resistance at 114.50. Only a break above 114.50 would signal the rebound from 108.13 is still in progress for gain towards resistance at 115.51 but a weekly close above there is needed to signal the fall from 118.66 top has ended at 108.13, then headway to 116.00-10 would follow but resistance at 117.53 should hold from here.

Top World Economies Expand, But Arising Geopolitical Risks Take Stage In Forex Markets

The US dollar gained during the Asian session, with the dollar index up 0.20% to last trade at 93.44. The session was busy with ample of data from Asian economies signaling economic expansion. The euro and sterling declined against the US currency. Oil prices rose while gold gave up on some of Friday's significant gains.

Data signalling the latest economic activity in China was the main news of the day. While activity in the world's second largest economy continued to expand, as the official PMI remained above the 50-point mark, the pace of growth slowed in July. At 51.4, the official manufacturing PMI narrowly missed estimates of 51.6 and was below the prior month's 51.7. However, due to expanding government investment projects the construction industry boomed, lifting investors' confidence. The construction sector remained robust with the PMI reading showing a pickup to 62.5 from 61.4 in June. This further spurred demand for steel, cement and other building materials.

The news out of China came as investors were trying to gauge global growth with US second quarter GDP showing steady expansion at 2.6% according to data released on Friday and Japan's monthly industrial production rebounding from a 3.6% decline to a 1.6% gain in June, based on the preliminary figures released earlier today. Dollar/yen was last trading at 110.68.

While the world's top three economies are showing positive momentum, the geopolitical risks have induced investor worries again. Russia has ordered the US to withdraw a large percentage of its diplomats that are currently serving in Russia, following the new sanctions on Russia that US Congress approved last week. Further to this, North Korea tested another intercontinental ballistic missile for the second time in weeks.

New Zealand winter months took a toll on business confidence there with sentiment cooling down in July to 19.4% from 24.8% in June. Rising construction costs and labor skill shortages contributed to lower optimism, but recovery in dairy prices provided some support. Tempered business sentiment is usual during winter months in New Zealand hence the country's currency didn't take much notice of the drop in sentiment. Kiwi/dollar rose slightly following the data release, but traded lower around the 0.7499 mark in the late Asian session to be broadly flat on the day. The labor report due on Wednesday could strengthen the kiwi against its US counterpart should the report show tightening employment activity.

While sales of new homes in Australia plunged last month to the lowest since 2013, the aussie rose against the greenback following the news. New home sales fell 6.9% in June from May, reversing two months of gains. However, this release was not of interest to forex traders as China PMI data was published at the same time, which pushed the aussie up. Aussie/greenback was last slightly up at 0.7978 ahead of the European session.

The euro was slightly weaker against the greenback during the Asian session to last trade at $1.1733. Traders will be closely monitoring the release of the flash CPI figure for July for the eurozone, today at 9:00 GMT.

Sterling was also under some pressure against the greenback today, with pound/dollar last trading at 1.3110.

Looking at commodities, oil prices gained, hitting a two-month high on a tighter US market and possible sanctions against Venezuela. WTI was last trading at $49.88 a barrel while Brent was at $52.76. Gold on the other hand declined during the session to last trade at $1,266.80 an ounce.

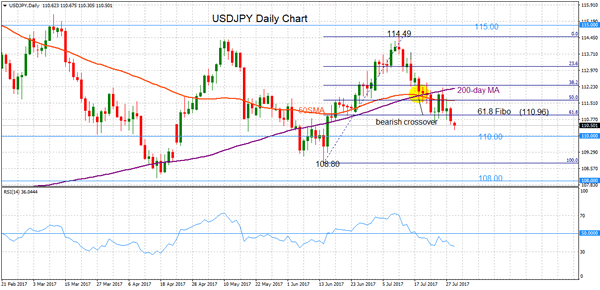

USDJPY Shifts To Bearish After Break Below 50-Day Moving Average

USDJPY shifted to a more bearish bias after falling below the 50-day moving average. The market is also trading below the 61.8% Fibonacci retracement level of the upleg from 108.80 to 114.49 (June 14 to July 11 rise) – this corresponds to the 110.96 level.

Risk remains to the downside in the short-term as the RSI is below 50 and sloping downwards. Meanwhile, the 50-day MA crossed below the 200-day MA on July 18, giving a bearish signal.

The immediate target to the downside is at the psychological level of 110.00. A break below this support level would target the June 14 low of 108.80, resulting in a complete reversal of the uptrend that took place from this 108.80 low to the 114.49 high. Such a move would open the way to the April 17 low of 108.12. From here, the bearish bias would strengthen.

To the upside, the previous support-turned-resistance and Fibonacci level at 110.96 would act as a barrier to any bounces higher. A break above the 50% Fibonacci and 50-day MA at 111.63 would weaken the bearish bias and target 112.30 and 113.13 before reaching the 114.49 high.

The short-term bearish phase remains strong below the 50-day and 200-day MA. The medium-term picture remains neutral unless there is a breakout above 115.00 or below 108.00.

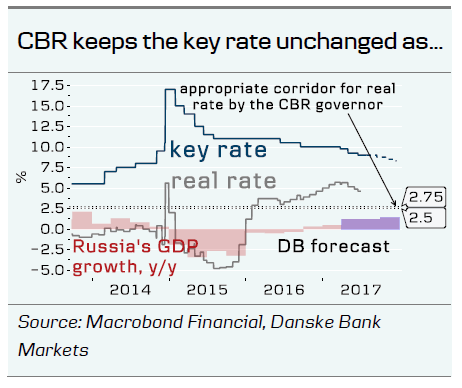

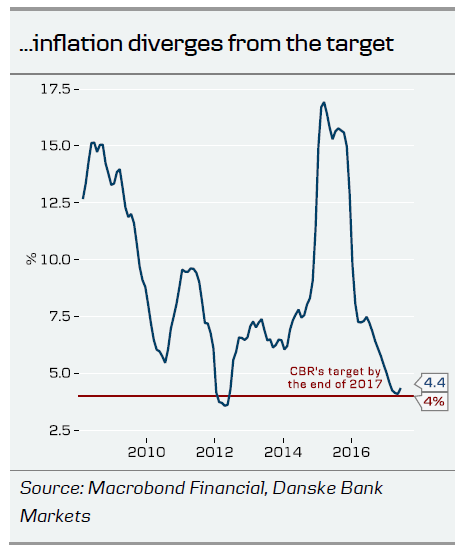

CBR Keeps Rates Unchanged, Unconvincingly

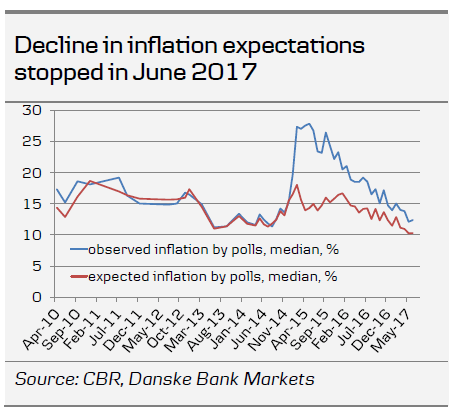

- Russia's central bank (CBR) kept its key rate unchanged at 9.00% on 28 July, as new geopolitical risks have emerged, inflation has diverged from the CBR's target and the decline in inflation expectations has halted.

- We expect the CBR to cut to 8.25% by the end of 2017 (8.00% previously), given no geopolitical 'black swans' or crude price crush.

- Russia's economy continues to deliver positive surprises despite moderately tight monetary policy.

Assessment and outlook

The CBR kept its key rate unchanged at 9.00% on 28 July. Bloomberg consensus has shifted towards 'unchanged' over the past two weeks, while we continued to be in the minority expecting a 25bp cut. However, in CBR Rate Decision Preview: We pencil in a cautious cut, 24 July, we did not exclude the central bank becoming overcautious and keeping rates on hold.

Reading the CBR's latest statement on the decision, its tone is not convincing enough on why it left rates unchanged. As the CBR had reiterated that the recent rise in inflation and its effects are seasonal and temporary, we link today's decision primarily to the risk of a further deterioration in the geopolitical environment surrounding Russia, including the recent approval by both houses of the US Parliament of a new heavily anti-Russia bill, Germany calling for new anti-Russia sanctions on the recent delivery of turbines to Crimea and today's tit-for-tat response by Russia's Ministry of Foreign Affairs.

Main assumptions behind today's decision

'Inflation remains close to the target'. Annual inflation increased to 4.4% y/y in June, up from 4.1% y/y in May, on an increase in fruit and vegetable prices. Yet, we do not find convincing the inflation argument for keeping rates unchanged, as the CBR said it sees no material risks from prices that are up on seasonal factors, causing a halt in the decline in inflation expectations.

'Interest rates on loans have declined but their level supports moderate demand for borrowing'. We conclude this is another assumption that supports more dovish monetary policy than today's rate decision.

'The economic activity is rebounding'. This factor gives the CBR room for its caution, as Russia's economy continues to surprise positively despite moderately tight monetary policy.

Elevated geopolitical risks and exchange rate dynamics 'may have negative implications for inflation expectations'. In our view, this is the most important point behind today's decision, even if the CBR lists it far below other reasons in its statement.

We expect the CBR to cut the key rate by 25bp at its monetary policy meeting on 15 September 2017, while sudden geopolitical deterioration and an oil price fall are major risks for our dovish call. Given the slight change in the CBR's easing path, we raise our key rate projection for the end of 2017 to 8.25%, from 8.00% previously.

Economy recovers despite high rates

We do not believe the slowdown in the monetary easing path is affecting Russian economic growth in H2 17. Russia's GDP growth accelerated from 0.5% y/y in Q1 17 to 2.7% y/y in Q2 17, according to Russia's economy minister Maxim Oreshkin. In H1 17, GDP growth climbed to 1.6% y/y and the minister said the current trend implies upside risk to the ministry's current estimate of 2% y/y for 2017. This is a very preliminary estimate, which we expect Russia's statistic service Rosstat to revise many times.

The Ministry for Economic Development (Minecon's) recent statement sounds positively surprising to us. Yet, there are reasons behind the statement: the average crude price was 8% higher in Q2 17 than in Q2 16, industrial production growth has been steady due to changes in economic structures, rates have been falling on lower inflation and private consumers saw a recovery.

Our 2017 GDP forecast has stayed unchanged for a record period, since spring 2016, at 1.2% y/y. In our view, there is currently clear upside risk to our forecast, especially if the current geopolitical woes do not bring new 'black swans' to Russia's macro economy. We expect GDP to grow by 1.2% y/y in 2017 and 1.4% y/y in 2018.

RUB welcomes hawkish hold

The RUB reacted positively to the CBR's decision despite the consensus view on the rate, as yesterday we saw market pricing starting to lean towards a possible cut in weekly inflation, falling to zero, and crude price rising. We keep our moderately bullish stance on the RUB in the long term, supported by carry and rising oil price, expecting the USD/RUB to hit 57.10 in 6M and 55.00 in 12M.

Given the change in the CBR's path, Russia's local debt – OFZs – reacted slightly negatively to the decision. Yet, we expect a recovery as dovish surprises from the CBR are still possible in the autumn. However, OFZ demand may stall if new anti-Russia sanctions are signed by President Trump in coming weeks.

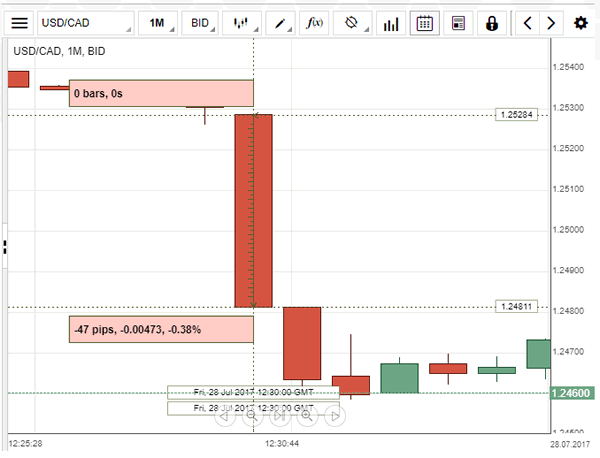

USD/CAD: Canadian GDP M/M

The USD/CAD currency pair dropped significantly, as the Canadian monthly GDP tripled forecasts in May. Right after the data release, the Loonie appreciated against the US Dollar by 47 base points, or 0.38%, to 1.2481. Moreover, the strength of the commodity-sensitive Canadian Dollar was additionally fuelled by higher oil prices. Statistics Canada reported on Friday that the country's real gross domestic product rose for the seventh month in succession, marking a 0.6% increase in May. The report showed expansion in 14 out of 20 sectors, with the strongest gains in goods-producing industries, which rose 1.6% for the month, supported by gas and oil extraction, mining and quarrying.