Sample Category Title

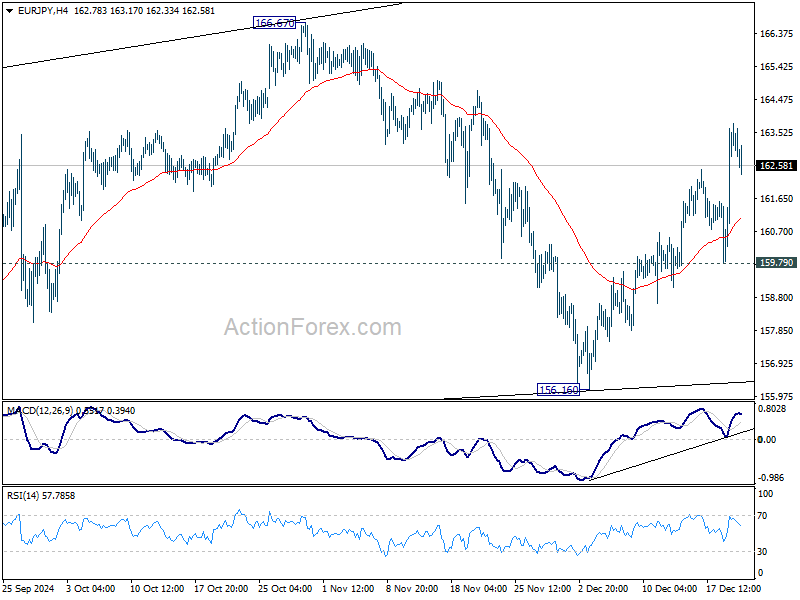

EUR/JPY Daily Outlook

Daily Pivots: (S1) 160.74; (P) 162.27; (R1) 164.69; More...

Intraday bias in EUR/JPY stays on the upside as rise from 156.16 is in progress. Corrective pattern from 154.40 is extending with another up-leg. Further rise should be seen to 166.67 resistance and possibly above. For now, risk will stay on the upside as long as 159.79 support holds, in case of retreat.

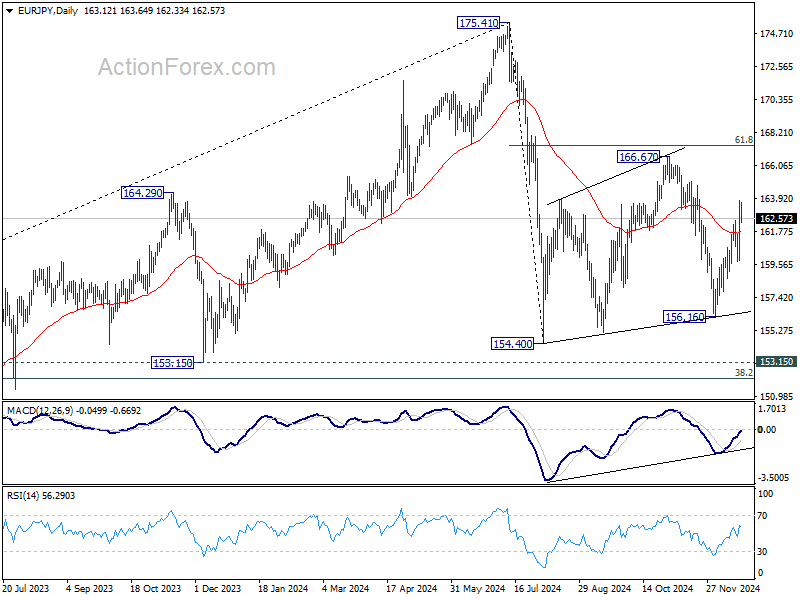

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

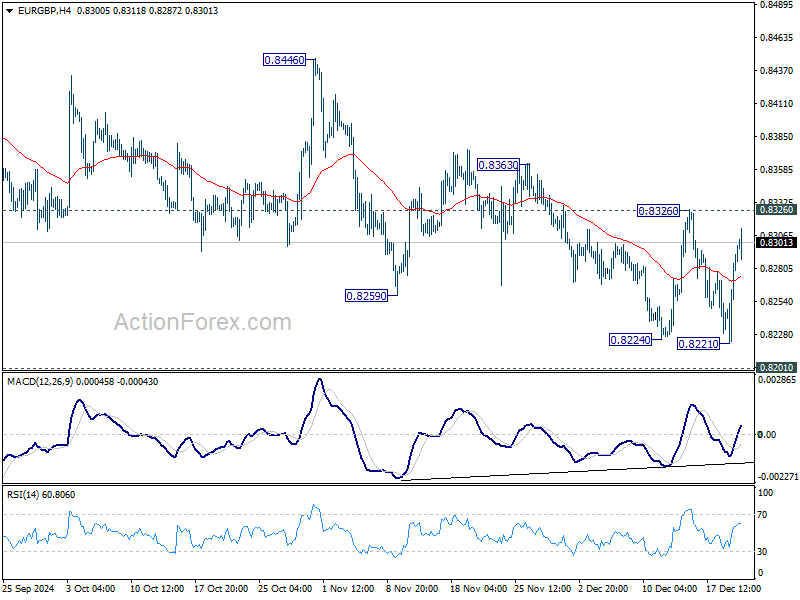

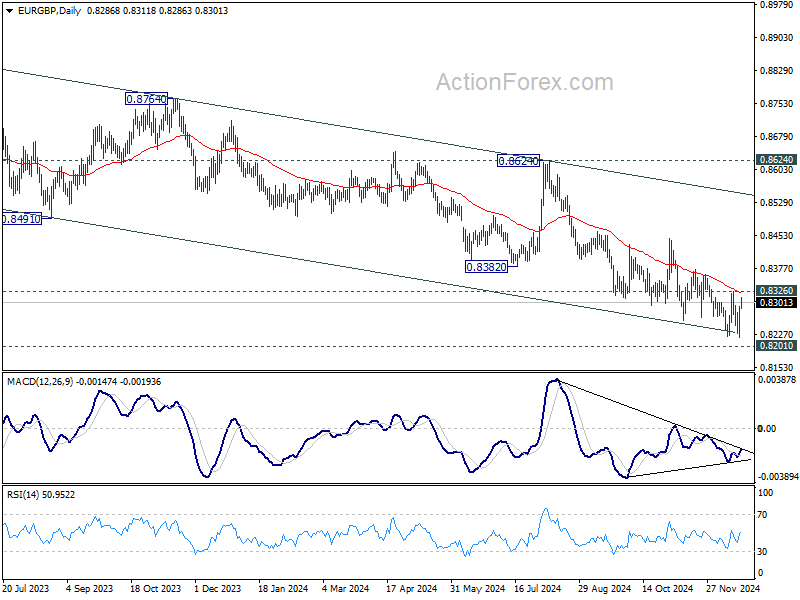

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8244; (P) 0.8269; (R1) 0.8314; More...

EUR/GBP rebounded strongly again ahead of 0.8201 key support and intraday bias is turned neutral. On the upside, break of 0.8326 resistance will indicate short term bottoming, on bullish convergence condition in 4H MACD. Intraday bias will be turned back to the upside for 0.8446 structural resistance next.

In the bigger picture, focus is now on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Otherwise, risk will stay on the downside even in case of strong rebound.

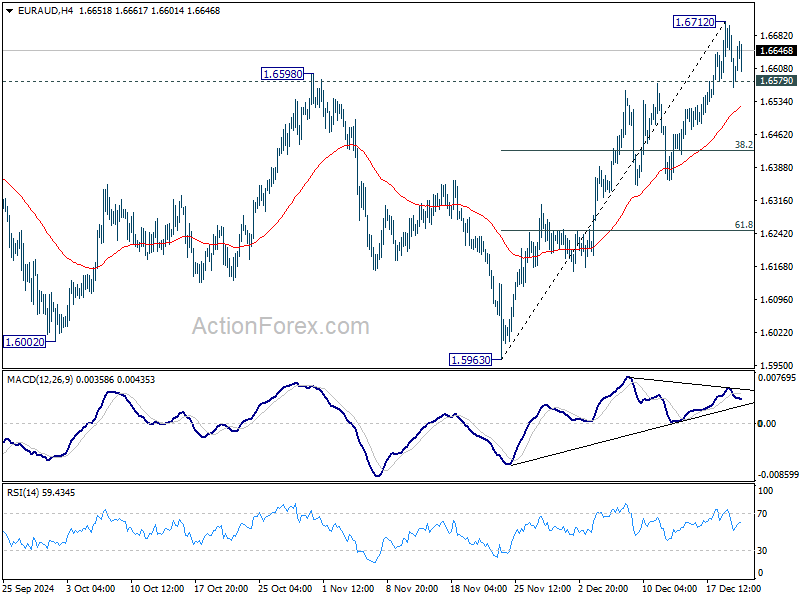

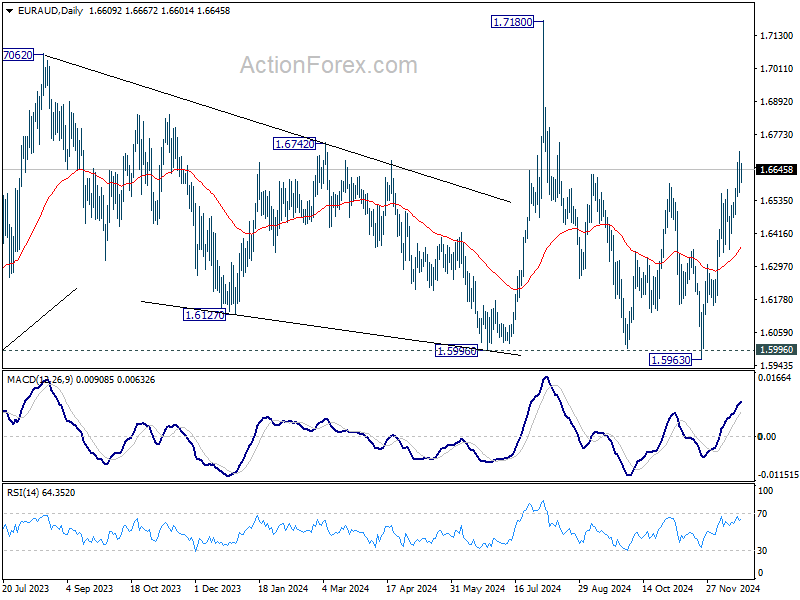

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6547; (P) 1.6631; (R1) 1.6696; More...

Breach of 1.6579 minor support suggests temporary topping at 1.6712 and intraday bias in EUR/AUD is turned neutral. Some consolidations would be seen first. On the upside, break of 1.6712 will resume the rally from 1.5693 to retest 1.7180 high next.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction.

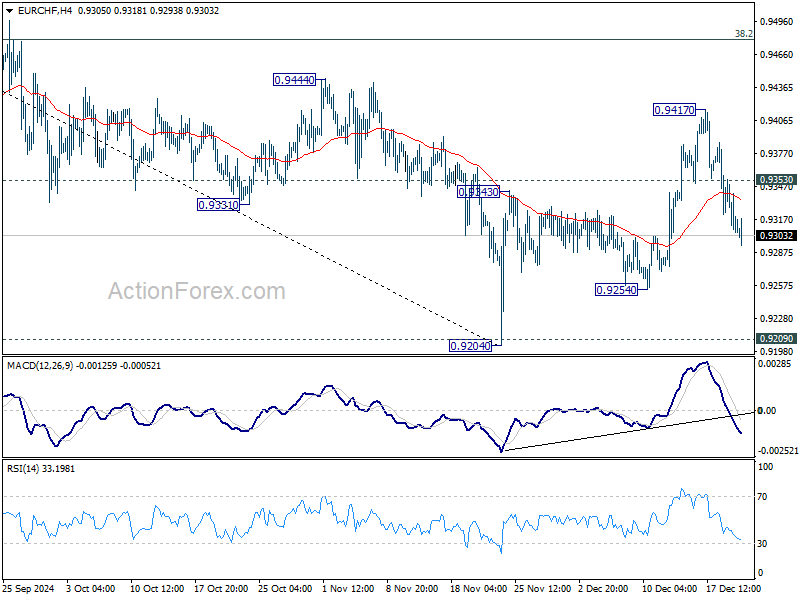

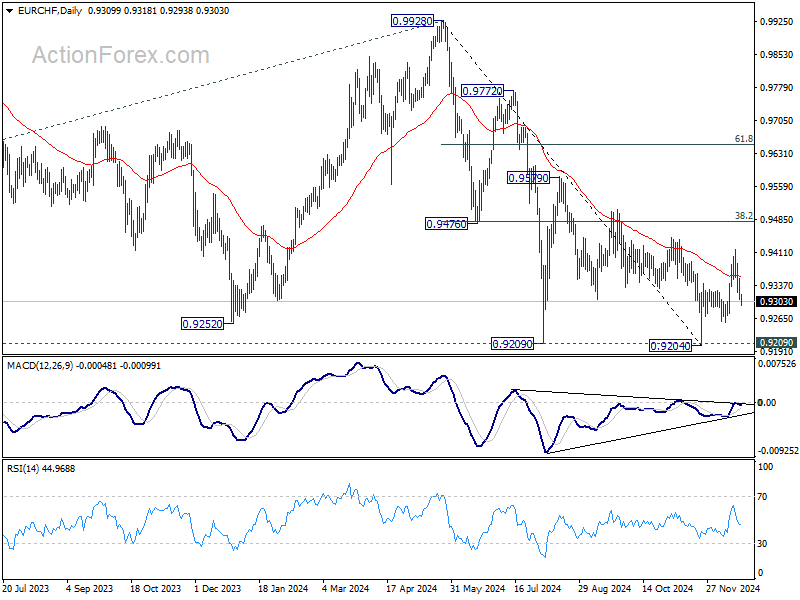

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9296; (P) 0.9325; (R1) 0.9344; More....

Intraday bias in EUR/CHF remains on the downside for the moment. Corrective rebound from 0.9204 could have completed with three waves up to 0.9417. Deeper fall would be seen to 0.9254 support first. Firm break there will bring deeper fall to 0.9209 key support again. On the upside, above 0.9353 minor resistance will turn intraday bias neutral first.

In the bigger picture, a medium term bottom is probably in place at 0.9204. More consolidations would be seen above there with risk of stronger rebound to 38.2% retracement of 0.9928 to 0.9204 at 0.9481. But outlook will remain bearish as long as 0.9481 holds and another fall through 0.9204 to resume larger down trend is in favor.

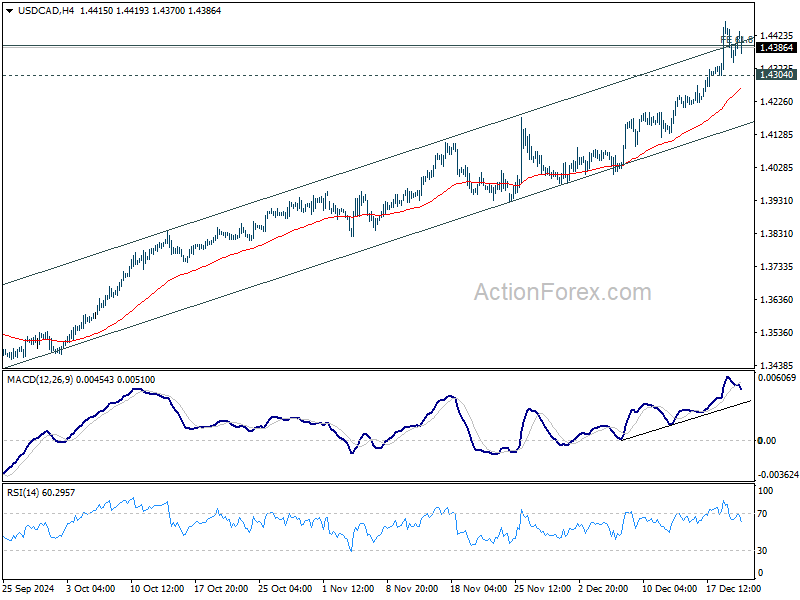

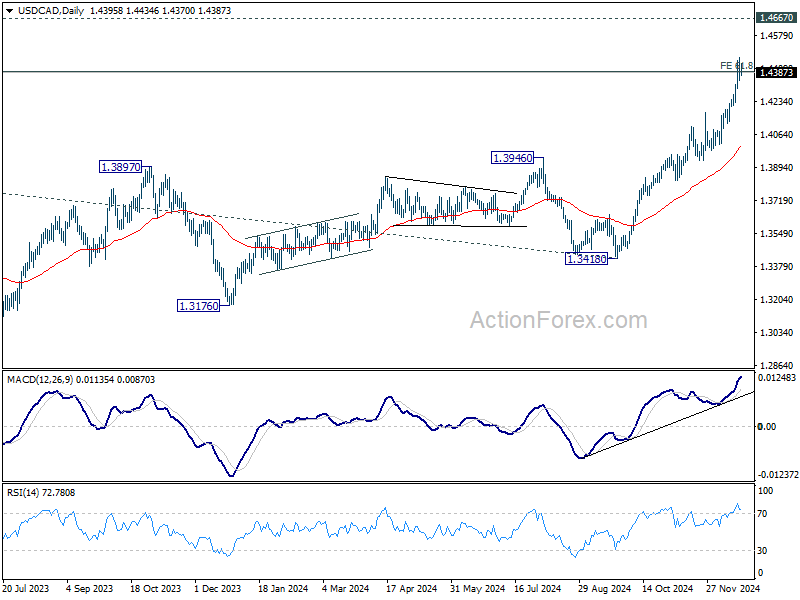

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4341; (P) 1.4404; (R1) 1.4463; More...

Intraday bias in USD/CAD stays on the upside at this point. Current rally is part of the larger up trend. Sustained trading above 1.4391 projection level will pave the way to 1.4667 long term resistance. On the downside, below 1.4304 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, up trend from 1.2005 (2021) is in progress and met 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391 already. Sustained trading above there will pave the way to 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3706) holds, even in case of deep pullback.

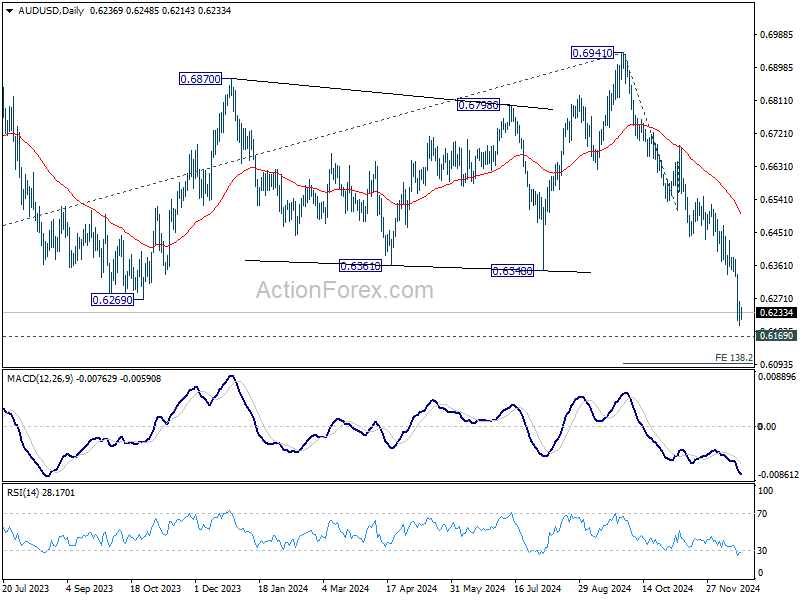

AUD/USD Daily Report

Daily Pivots: (S1) 0.6203; (P) 0.6234; (R1) 0.6269; More...

Intraday bias in AUD/USD remains on the downside for the moment as fall from 0.6941 is still in progress. Firm break of 0.6169 key support will confirm larger down trend resumption. Next near term target is 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. On the upside, above 0.6298 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

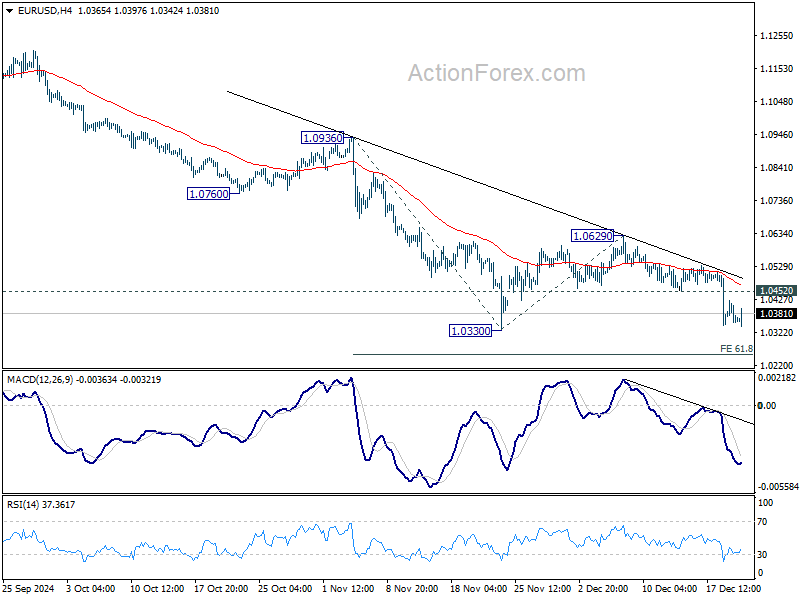

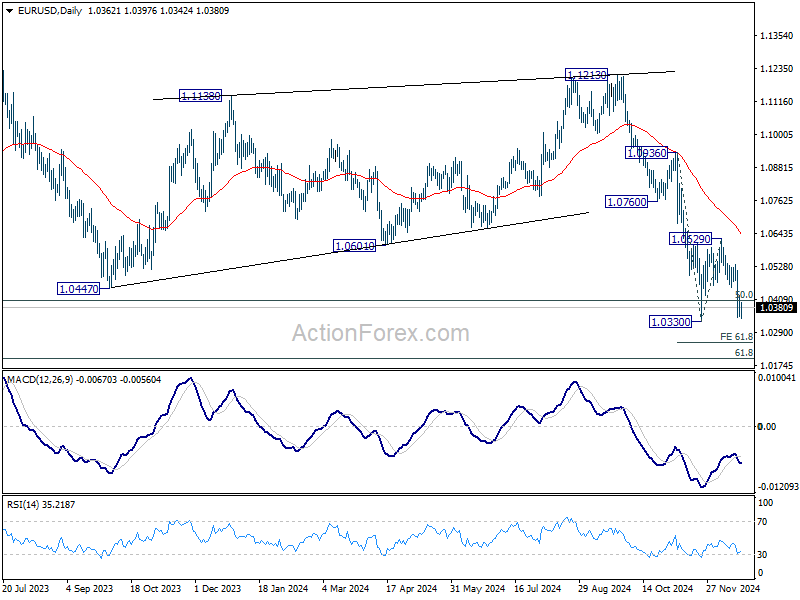

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0333; (P) 1.0378; (R1) 1.0407; More....

Outlook in EUR/USD is unchanged and intraday bias stays on the downside. Firm break of 1.0330 support will resume the fall from 1.1213 and target 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254, and then 100% projection at 1.0023. On the upside, above 1.0452 will turn intraday bias neutral again first.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

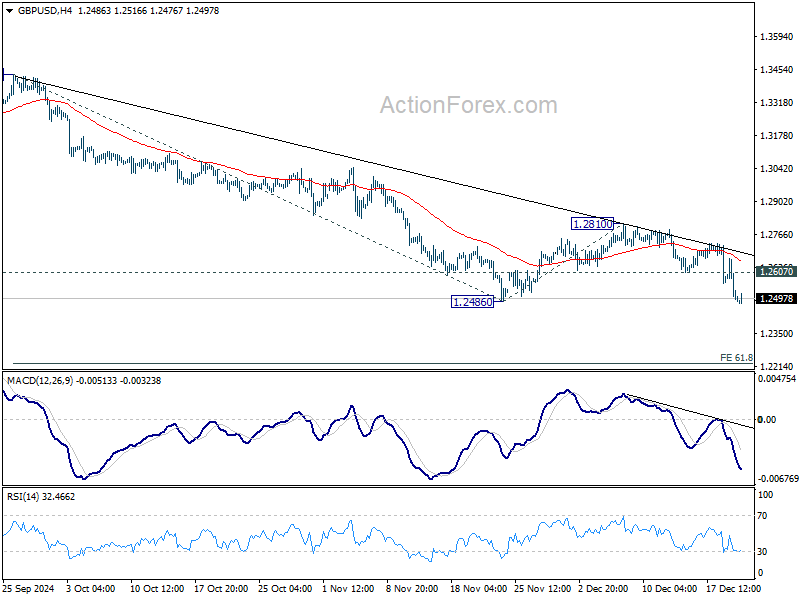

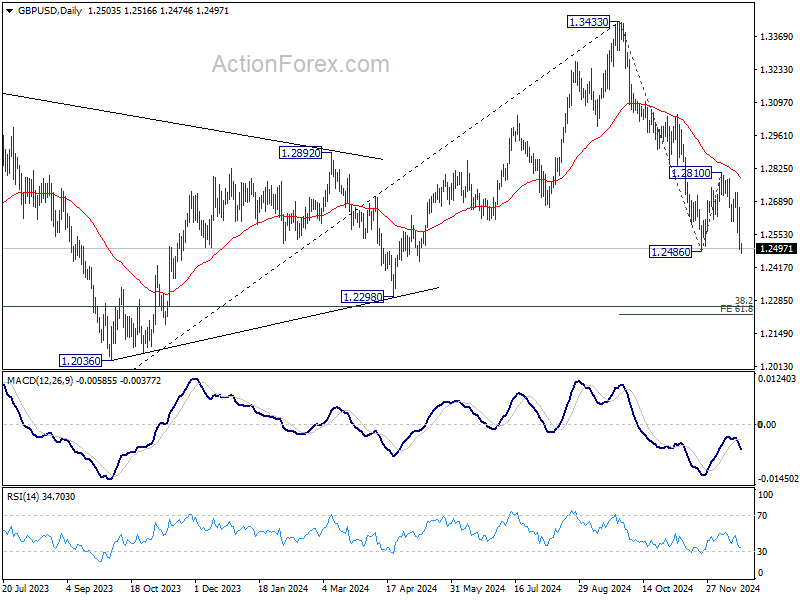

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2442; (P) 1.2554; (R1) 1.2614; More...

GBP/USD's breach of 1.2486 support suggests that fall from 1.3433 is resuming. Intraday bias stays on the downside, and deeper fall would be seen to 1.2298 and possibly further to 61.8% projection of 1.3433 to 1.2486 from 1.2810 at 1.2225. On the upside, above 1.2607 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.2810 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

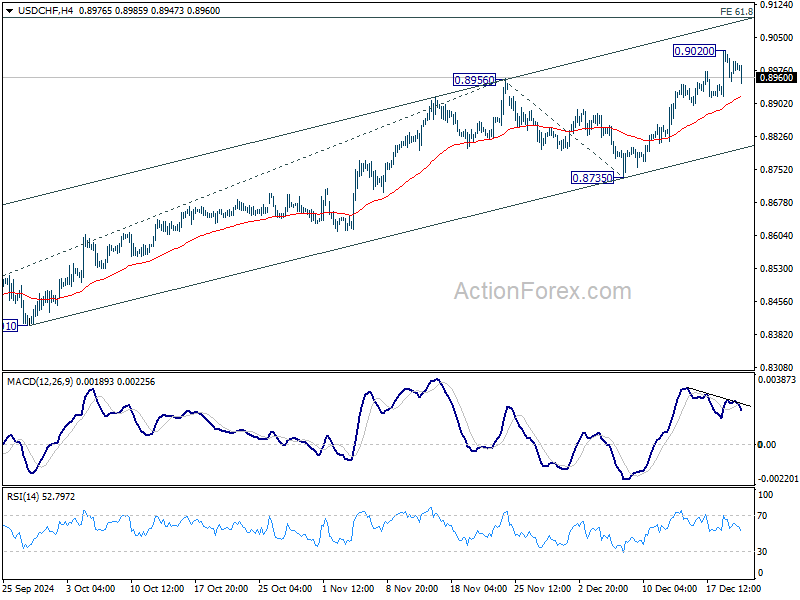

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8951; (P) 0.8990; (R1) 0.9027; More…

Intraday bias in USD/CHF is turned neutral first with current retreat and some consolidations would be seen below 0.9020 temporary top. But further rally is expected as long as 0.8735 support holds. On the upside, break of 0.9020 will resume the rally from 0.8374. Next target will be 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

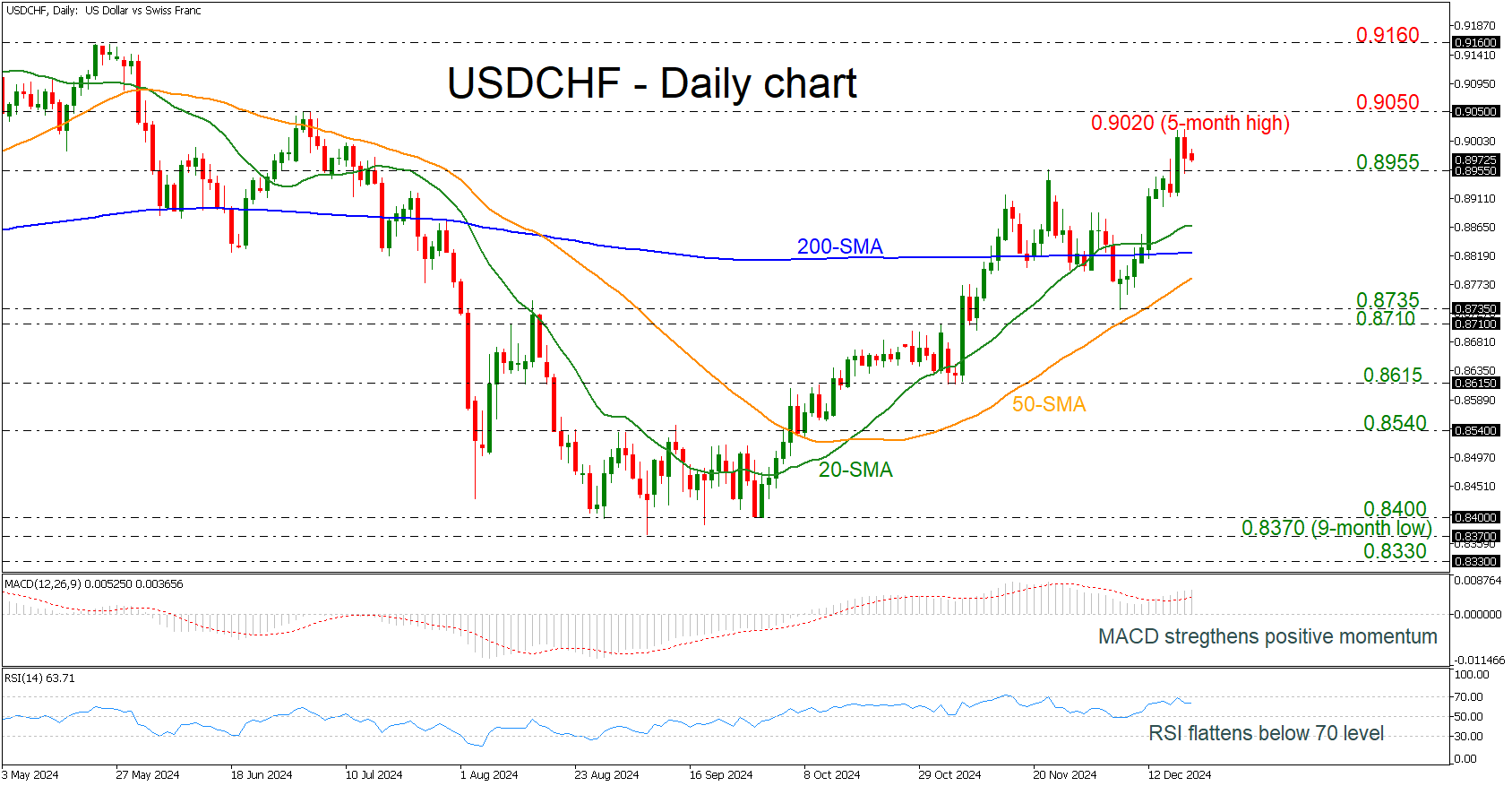

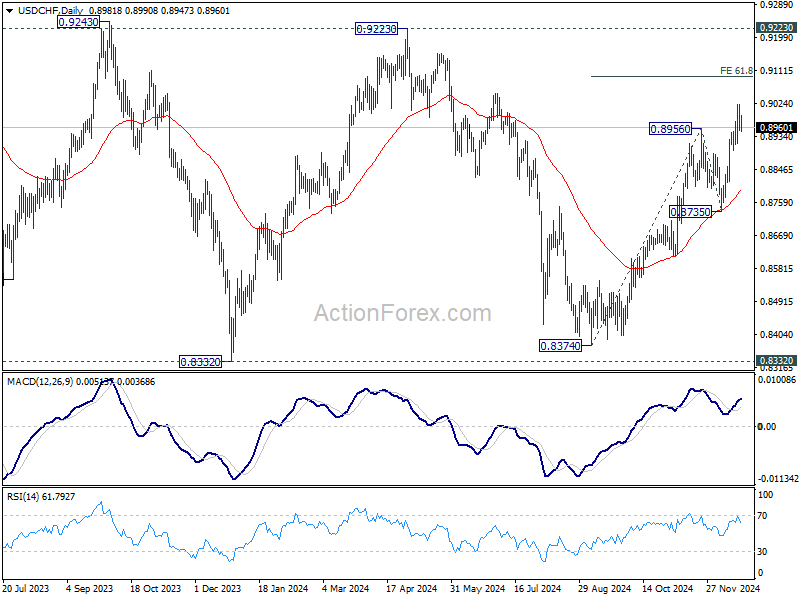

USDCHF Eases from 5-month High

- USDCHF remains in bullish bias

- RSI suggest overstretched market

USDCHF has added more than 7% since the end of September, sending the price to a new five-month high of 0.9020. However, the pair is currently losing some ground but remains above the 0.8955 key level.

From a technical standpoint, the MACD oscillator is still extending its positive momentum, but the RSI is flattening above the neutral threshold of 50, indicating a potential downside correction.

If the bulls remain under control, then the price may test the next resistance line of 0.9050, taken from the peak in July. Even higher, the 0.9160 barrier could endorse the bullish bias in the short-term view.

On the other hand, a dive below 0.8955 could send traders toward the 20-day simple moving average (SMA) at 0.8865, but more importantly, the flat 200-day SMA at 0.8820 may act as a turning point.

Summarizing, USDCHF is in a strong upside tendency, and only a tumble below the 0.8710-0.8735 support region may change this view.