Sample Category Title

Brent Oil Under Pressure Again: USD and China in Focus

Brent crude oil prices fell below 73 USD per barrel on Friday, reflecting ongoing downward pressure. The market is poised to close the week with losses as a robust US dollar weighs heavily on commodity prices.

This week, the US Federal Reserve signalled a measured approach to reducing borrowing costs in 2025, sending the US dollar to a two-year high. The dollar’s strength has raised concerns about a dampened outlook for global fuel demand, particularly in emerging markets where dollar-denominated commodities become more expensive.

Concerns from China add to market anxiety

The ongoing unease about China’s economic recovery adds to the bearish sentiment. Sinopec, the country’s largest refiner, announced that domestic petrol demand likely peaked last year. This revelation has significantly clouded the outlook for 2025 as China’s role as a key driver of global energy consumption diminishes. China’s reduced demand has cast a long shadow over global crude markets, leading to further downward price pressures.

Mixed signals from supply dynamics

Despite the weak demand signals, the supply side has provided mixed indicators. Earlier in the week, data from the US Department of Energy showed reduced oil reserves, temporarily bolstering prices. However, this bullish factor was short-lived. Kazakhstan’s decision to support the extended production cuts under OPEC+ was another potentially supportive signal, but it has failed to provide sustained relief to oil prices amid broader concerns.

The structural expansion of production outside OPEC, particularly in the US and other non-OPEC nations, further complicates the outlook. Combined with China’s declining appetite for energy, these factors suggest that oil prices may end 2024 on a subdued note, with limited prospects for a significant recovery.

Technical analysis of Brent oil

H4 chart analysis: on the H4 timeframe, Brent continues to trade within a broad consolidation range around the 73.13 USD level. The market recently extended this range upwards to 73.40 USD. However, a downward move to 71.93 USD appears imminent. If the market manages to break out of this range to the upside, the next target lies at 75.05 USD, with the potential for further gains towards the 80.00 USD level.

From a technical standpoint, the MACD indicator supports this scenario, with the signal line positioned below the zero level near recent lows. This indicates that the market could soon attempt a reversal towards higher levels, potentially marking the beginning of a new growth wave.

H1 chart analysis: on the H1 chart, Brent is also consolidating around 73.13 USD. The current wave structure suggests a decline towards 71.93 USD, followed by an expected corrective wave to return to 73.13 USD. If this resistance is breached, the market may gain momentum, with an upward trajectory targeting 75.05 USD and potentially higher levels.

Expect Dollar to Hold Near Recent Strong Levels

Markets

Front end US yields returned a few bps of the sharp Fed-induced gains yesterday but the long end extended its march higher. The 10-30-yr bucket added between 4.8 and 5.9 bps. Economic data, while second tier, again in most cases underscored the country’s economic resilience. European swap rates gapped higher in a first response to the Fed. They ended up with net daily changes between 3 (2-yr) and 7 (10-yr) bps. The dollar pulled back but the euro did not seize the opportunity. EUR/USD closed stable around 1.035. JPY underperformed after the Bank of Japan kept rates steady. USD/JPY shot up from 154.8 to 157.44. The pound dropped from EUR/GBP 0.822 to 0.829. The Bank of England’s 6-3 vote for a hold yesterday was a tighter call than it appeared. Conservative market pricing - only two cuts next year - made both sterling and short-term UK yields vulnerable for a kneejerk move lower. The Norwegian krone finishes the top three losers following the central bank readying to ease monetary policy in Q1 of next year.

The economic calendar features some interesting data for key areas though we doubt they’ll leave a significant mark on trading. Japan kicked off with inflation figures this morning (see News & Views). UK retail sales released just now were weaker than expected across all gauges, triggering some further GBP weakness. The EC’s consumer confidence is due later today and after the US release of PCE inflation figures. The latter are expected to rise by 0.2% m/m, lifting the yearly measures for headline and core to 2.5% and 2.9% respectively. After Wednesday’s Fed meeting, markets have drawn some hawkish conclusions that are unlikely to change with (outdated) PCE numbers though. If anything, the front end of the curve could be most vulnerable in case of a downside surprise given there’s nothing more than one cut and a half priced in for all of 2025. We expect the dollar to hold near the recent strong levels. We keep a closer eye at the developments in US Congress. A government shutdown suddenly and unexpectedly became a real possibility this weekend after president-elect Trump and key advisor Musk helped torpedo a bipartisan stopgap bill to fund spending through March 14. A GOP plan backed by Trump, which included a suspension of the debt ceiling through 2027, later also stranded in the Republican-led House.

News & Views

Price pressure keeps building in Japan. National inflation accelerated to 0.6% M/M in November with the annual headline figure rising from 2.3% to 2.9%, the second fastest pace since October 2023. The Bank of Japan’s preferred core measure (ex. fresh food), increased by 0.5% M/M to 2.7% Y/Y from 2.3%. Goods prices gained 0.9% M/M on a strong rise in utility prices (+3% M/M) after the government rolled back energy subsidies. Services costs were up 0.2% M/M. Today’s inflation numbers should give the BoJ more confidence that inflation will settle around its 2% inflation target. Yesterday, the central bank kept its policy rate unchanged with BoJ governor Ueda remaining cautious on the timing of the next rate hike. That added JPY weakness to post-FOMC USD-strength, propelling USD/JPY to its highest level since mid-July (USD/JPY 158 from 155). It immediately prompted comments from Minister of Finance Kato: “The government is deeply concerned about recent currency moves, including those driven by speculators. We will take appropriate action if there are excessive moves in the currency market.”

US president-elect Trump gave another sneak preview on how he will use tariffs as leverage during his tenure. His first hit was at Mexico and Canada where tariffs could be installed if borders aren’t strengthened to stop migration flows into the US. Now he took aim at the EU: “I told the European Union that they must make up their tremendous deficit with the United States by the large scale purchase of our oil and gas. Otherwise, it is TARIFFS all the way!!!” Last year, the EU already bought more than half of US LNG deliveries. Up next: China? A stronger CNY or else TARIFFS all the way?!

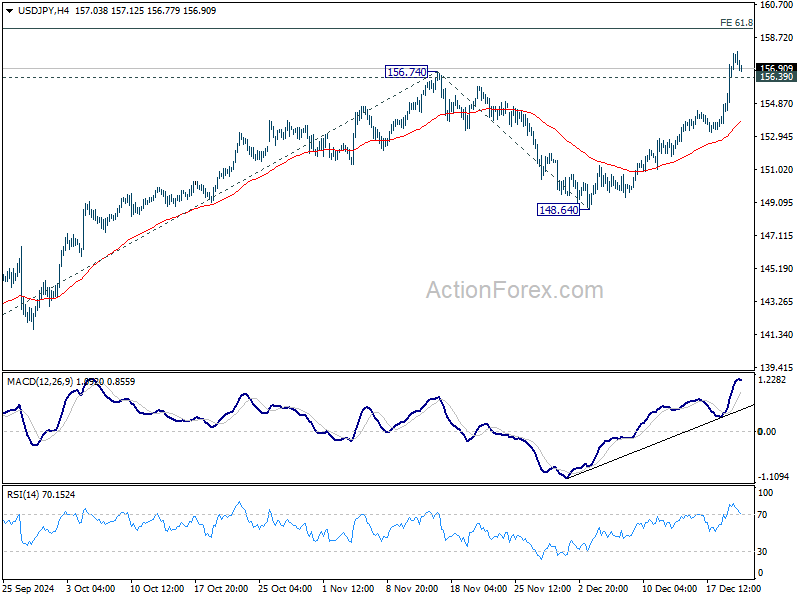

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.31; (P) 156.56; (R1) 158.68; More...

Intraday bias in USD/JPY remains on the upside for now despite current mild retreat. Current rally is part of the whole rise from 139.57, and should target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 156.39 minor support will turn intraday bias neutral again first. But outlook will stay bullish as long as 153.15 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Yen Recovers Slightly on Japan’s Inflation and Verbal Intervention, But Dollar Remains Unstoppable

Yen, which has been one of the weakest currencies this week, showed a modest recovery during today’s Asian session. The rebound came on the back of stronger-than-expected inflation data and renewed verbal intervention from Japan’s Finance Ministry. November’s inflation figures revealed a sharp reacceleration, driven by significant increases in energy prices and rice prices. Despite this, the slight uptick in core-core CPI was insufficient to push BoJ into immediate action. Expectations remain for a possible rate hike in January, with future moves contingent on developments in domestic wage growth and the trade policies of the incoming US administration.

Japanese Finance Minister Katsunobu Kato reiterated the usual warning against "one-sided or rapid" currency movements, emphasizing that exchange rates should reflect economic fundamentals. He pledged to take "appropriate action" to address excessive volatility. However, these remarks had a limited market impact given the dominance of Dollar, which surged after Fed’s hawkish hold and the strong rally in US Treasury yields. In particular, 10-year yield has broken through 4.5% resistance level, now setting sights on 5.0% mark. This momentum keeps USD/JPY on track toward the critical 160 level.

In weekly rankings, Dollar remains the clear leader, driven by Fed expectations and rising yields. Swiss Franc holds a distant second, followed by the British Pound, which remains relatively resilient against others despite the selloff after BoE rate decision.

Meanwhile, New Zealand Dollar is the week’s worst performer, weighed down by poor GDP data showing significant economic contraction. Yen is the second weakest, pressured by both a lack of BoJ action and strong US and European yields. Australian Dollar rounds out the bottom three, while Euro and Canadian Dollar are positioned in the middle. Though market dynamics on the bottom side of the spectrum could still shift in the final trading sessions.

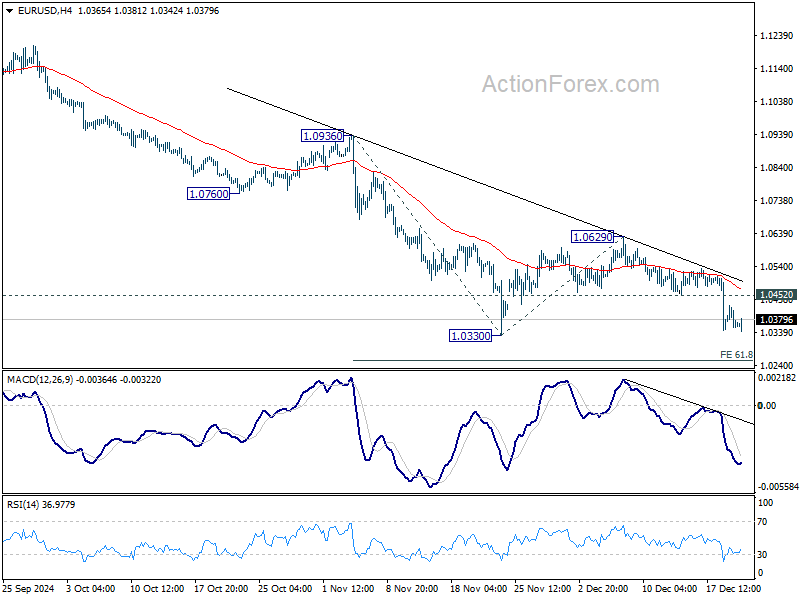

Technically, it should be emphasized that EUR/USD is still holding above 1.0330 near term support after all the volatility so far. Sellers appear not too committed yet. Because of this, even with a breach of 1.0330, some support could be seen from 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254 to contain downside. EUR/USD would need to break through 1.0254 decisively to confirm that Dollar's underlying strength is to sustain.

Looking ahead, US personal income and spending, as well as PCE inflation data are the main focuses for the rest of the day. Canada retail sales will be watched too.

UK retail sales edge up 0.2% mom, below 0.4% mom expectations

UK retail sales volumes rose by 0.2% mom in November, falling short of expectations for a 0.4% increase. This modest gain partly recovered the -0.7% mom decline recorded in October. Growth in supermarkets and non-food stores provided support, but this was partially offset by weaker performance from clothing retailers.

On an annual basis, sales volumes increased by 0.5% over the year to November. However, volumes remain -1.6% below their pre-pandemic levels from February 2020.

Looking at the broader trend, retail sales volumes rose by 0.3% in the three months to November compared with the prior three-month period. Compared to the same period last year, volumes were up by 1.9%, suggesting some resilience despite ongoing economic uncertainties.

Japan’s core CPI reaccelerates to 2.7%, driven by energy and rice

Japan’s core CPI (excluding food) rose to 2.7% yoy in November, marking the first reacceleration in three months and exceeding market expectations of 2.6% yoy. Core inflation has remained above the BoJ’s 2% target since April 2022, highlighting persistent price pressures. This increase was attributed to reduced government subsidies for utility bills and a sharp rise in rice prices.

Energy prices surged 6.0% yoy, up from October’s 2.3% yoy gain. Within this category, electricity prices jumped 9.9% yoy, and city gas costs climbed 6.4% yoy. Meanwhile, rice prices soared by a staggering 63.6% yoy, the steepest increase since 1971, driven by last year’s unusually hot summer that disrupted production.

Core-core CPI (excluding food and energy) ticked up from 2.3% yoy to 2.4% yoy, while headline CPI rose to 2.9% from October’s 2.3%. Service prices, a key indicator for BOJ as they often reflect wage dynamics, increased 1.5% yoy, unchanged from the prior month.

NZ's exports rises 9.1% yoy in Nov, imports up 3.9% yoy

New Zealand’s trade data for November showed a significant improvement, with goods exports rising 9.1% yoy to NZD 6.5B, while goods imports increased by a more modest 3.9% yoy to NZD 6.9B. The resulting trade deficit of NZD -437m was much smaller than the expected NZD -1951m.

Exports saw notable gains across key markets. Shipments to China increased 6.3% yoy, adding NZD 106m, while exports to Australia climbed 8.4% yoy (NZD 62m) and to the US by 12% yoy (NZD 85m). Exports to the EU surged the most, rising 27% yoy (NZD 74m), with shipments to Japan also showing strength at 7.2% yoy (NZD 19m).

On the import side, data was more mixed. Imports from China edged down -1.7% yoy (NZD -29m) and from the EU fell sharply by -16% yoy (NZD -163m). Similarly, imports from South Korea dropped -12% yoy (NZD -61m ). However, imports from Australia rose 14% yoy (NZD 101m) and from the US increased 7.2% yoy (NZD 41 m).

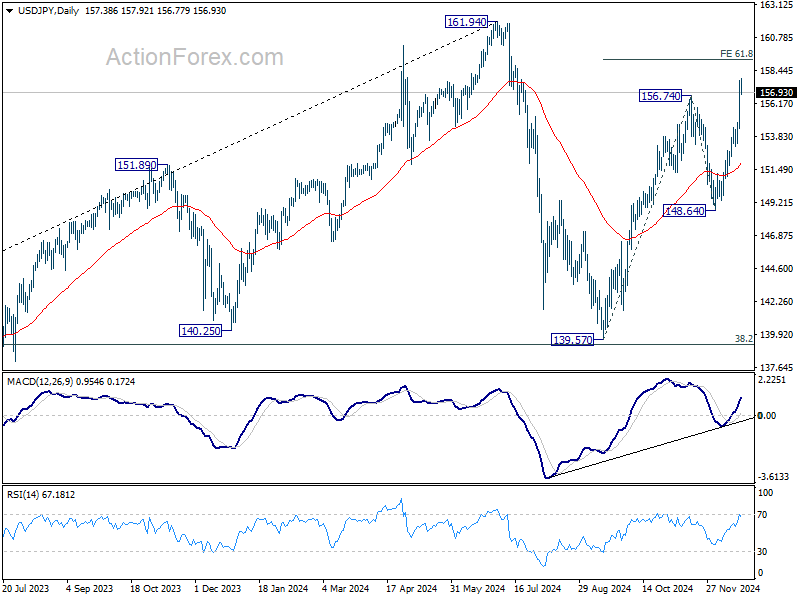

USD/JPY Daily Outlook

Daily Pivots: (S1) 155.31; (P) 156.56; (R1) 158.68; More...

Intraday bias in USD/JPY remains on the upside for now despite current mild retreat. Current rally is part of the whole rise from 139.57, and should target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 156.39 minor support will turn intraday bias neutral again first. But outlook will stay bullish as long as 153.15 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

USD Advances Toward the Strongest Levels in More Than 2 Years

A week packed with central bank decisions is coming to an end with a sour taste in everybody’s mouth. The Federal Reserve (Fed)’s decision to cut rates by 25bp was fully meaningless and the incoming data is a proof. The US Q3 growth was revised to 3.1% from 2.8% printed earlier, the sales growth was revised higher from 3 to 3.3% and core PCE priced – though lower than the quarter before – was also revised slightly higher to 2.20%, raising worries that even the two rate cuts from the Fed next year would be too much. As such, the early gains were given back and the S&P500 and Nasdaq closed in the negative, the Dow Jones was flat while small and mid cap stocks saw no appetite either. Sharing the headlines with Powell, Trump threatens people of his own party to dump a bipartisan deal and risk a government shutdown if they don’t push to raise or suspend the national debt limit under Biden, so he can spend wholeheartedly when he comes to office. The US yield curve is steepening, investors are not willing to buy longer-dated maturities on prospects of higher long-term inflation and ballooning debt. And the US dollar advances toward the strongest levels in more than 2 years leaving other majors under the shadow before Xmas.

The EURUSD failed to stay above the 1.04 mark yesterday and is struggling to hold ground near the 1.0350 level, the Stoxx 600 is racing toward the 500 support, while Cable settles below the 1.25 mark on the back of a dovish no-change that the Bank of England (BoE) delivered at yesterday’s MPC meeting. Three MPC members instead of two (expected by analysts) voted to cut the rates at this week’s meeting. The other six opted for no change – wary of reigniting inflation as the government prepares to increase spending to boost growth, and as Trump threatens the world with eye-watering tariffs. Interestingly, Governor Andrew Bailey – who is clearly not the most popular central banker – had the merit of sounding rational yesterday by saying that the ‘world is too uncertain’ to commit to cut borrowing costs in February. War, Trump, climate change – there’s too much happening for anyone to claim they see the future with clarity. But one good news for the UK is that the United Kingdom is not as concerned as – say the EU, China, Canada and Mexico – by the Trump tariffs and the latter could help the British assets cope with Trump better than their peers. British stocks trade with around 40% valuation discount compared to the MSCI World peers, it has one of the fastest dividend growth among the European and American indices and they returned 10% to their investors these years including reinvested dividends. If inflation U-turns as geopolitical and trade tensions worsen, the FTSE 100 stocks will be in a good position to benefit from these developments.

Elsewhere – and this is amusing – inflation in Japan accelerated in November. The headline figure climbed back to 2.9%, the highest in three months, while core inflation advanced to 2.7%, also a three-month high. Why is this funny? Because just yesterday, the Bank of Japan (BoJ) decided to pass on a rate hike, with officials seemingly too cautious to act amid uncertainties over Trump-era policies and geopolitical tensions. Meanwhile, Japan’s interest rate sits at 0.25%, while inflation is running near 3%. The Japanese have a different relationship with inflation – they don’t despise it as much as we do. After all, decades of deflation, which is far harder to reverse, have shaped their perspective – a lesson the Chinese are now learning the hard way. But the BoJ’s decisions still feel illogical, as they don’t align with a conventional policy framework. Consequently, the USDJPY is giving back some earlier gains on the stronger-than-expected inflation figures and speculation that rising inflation might prompt BoJ action. However, since the BoJ doesn’t really tie interest rates to inflation, the USDJPY has room for further gains, especially as the US dollar continues to strengthen broadly.

In China, the People’s Bank of China (PBoC) kept its policy rates unchanged today – as expected – although the officials are now committed to put in place ‘more proactive fiscal measures’ and ‘moderately loose’ monetary policy. For now, none of these legs have been enough to bring investors back on board. The Chinese CSI 300 is preparing to close the week on a meagre note.

Riksbank Rounds Off the Cutting Season

In focus today

In the euro area, we get data on consumer confidence for December. Consumer confidence has been on a rising trend the past two years but in November it unexpectedly declined. It will be very import for the growth outlook to see if the decline was just a blip or it continued in December as we expect private consumption to be the main growth driver in 2025.

From the US, November Private Consumption Expenditures (PCE) are due for release today, including the Fed's preferred measure of inflation. The CPI measure released earlier pointed towards relatively steady inflation pressure in November.

In the US, we will also keep an eye on Congress, which will have to find a deal to avoid a government shutdown, after the House of Representatives voted down the latest version of a funding bill last night.

In the Nordics, we will look out for consumer and business sentiment in Sweden and Denmark.

We also get retail sales, wage data and PPI inflation in Sweden.

Economic and market news

What happened overnight

Japanese November CPI inflation excl. fresh food increased to 2.7% from 2.3% in October. Core inflation increased to 1.7% from 1.6. The underlying price pressure has been stronger in H2 and largely aims with the 2% inflation target. The unwillingness from the BoJ to raise rates further stems from a worry that wage growth will fade in the spring leaving price pressures back where they have been for decades, close to zero. This has added further to downward pressures on the yen triggering verbal intervention from the Japanese finance minister and top currency diplomat.

What happened yesterday

The Riksbank cut the policy rate by 25bp to 2.5% as widely expected but the signals for the future were more hawkish as the Riksbank expects only one more cut during H1 2025. In the rate path, the implied probability is rather evenly distributed between the January and March meetings, but with the overall communication saying they will have "a more tentative approach" and "carefully evaluate the need for future interest rate adjustments" it seems more likely than not that the Riksbank is ready to pause in January, in our view. We therefore have adjusted our call and now expect 25bp cuts in March and June, resulting in an end point of 2.00% (previously 1.75%). At the press conference, Thedéen commented that current policy is likely somewhat stimulative and that once the policy rate reaches 2.25% by Q1 next year, the risks are actually balanced putting an equal probability between cuts and hikes from there. We firmly believe there are more downside risks to the Riksbank's main scenario. See more in Riksbank - December 2024: 25bp cut but a hawkish signal. We now expect two cuts in March and June to 2.0% (previously 1.75%), 19 December.

Also in Sweden, there are plenty of interesting data. We start off with retail sales data for November, and here we will hopefully see more signs of the long-awaited recovery for household consumption. We also get wage data for October and PPI data for November, where the latter will likely see a rise due to higher energy prices (all released at 8.00 CET). At 9.00 CET, we will get a new set of NIER confidence data, and here we also expect to see a continued improvement in sentiment among both households and manufacturing sector. As always, attention will also be on price expectations and hiring plans. NIER will also release new set of economic forecasts at 9.15 CET.

Norges Bank left policy rates unchanged in a decision widely expected by analysts and markets. Importantly the Norwegian central bank firmed its guidance towards a March 2025 rate cut - the first in the cycle - by presenting a rate path suggesting a close to 100% probability of a 25bp rate reduction conditioned on the central bank's economic projections materialising. Norges Bank notably did not suggest that rates could be cut in January. Further out Norges Bank guided towards three cuts in 2025 although with an elevated risk of a fourth cut. We continue to pencil in the first cut in March alongside three additional rate cuts in 2025 and four cuts in 2026.

The Bank of England also agreed to keep rates unchanged as expected. The decision was taken with three board members voting for a cut, which was a surprise. That said, BoE continues to emphasise a gradual approach to reducing the restrictiveness of monetary policy. We think this supports our base case of the next cut coming in February and a quarterly pace after that.

FI: European curves steepened from the long end mirroring the US yields' reaction to the FOMC meeting on Wednesday night. However, it was a gradual move through the day, thus it was with some delay that we saw the full effect. With the final central bank meetings of the year behind us, and only a few trading sessions left for the year, we expect a relative tight trading range in coming days, with focus on the supply announcements for next year. Yesterday, the French Tresór said that they plan to sell EUR300bn next year, which is unchanged from the October plan. BoE's dovish tilt (6-3 split vote for unchanged) relative to market expectations sent UK yields somewhat lower on the day, see our BoE flash comment here Bank of England Review - BoE to lag peers in 2025; we stay positive GBP, 19 December.

FX: As expected, the Riksbank lowered the policy rate by 25bp to 2.50% and indicated only one more cut in H1. A hawkish cut which strengthened the SEK and supported our call for tactical downside in EUR/SEK. EUR/SEK dropped some ten figures towards the lower end of 11.40's before erasing some of the losses in the Asian session. Meanwhile, NOK/SEK was down 1.5 figures to below 0.9650. Norges Bank did not rock the boat, but the NOK traded on the defensive as focus shifts to the looming easing cycle that will probably start in March. The selloff in EUR/USD paused in the European session but as US trading opened the cross dived below 1.04 again and is now back close to 1.0350. The relentless selling of the JPY has continued, and USD/JPY was on the verge to break above 158. This morning Japan FM Kato expressed concerns and talked about appropriate action if there are excessive moves. Sterling was lower after Bank of England's dovish voting split to keep rates unchanged.

UK retail sales edge up 0.2% mom, below 0.4% mom expectations

UK retail sales volumes rose by 0.2% mom in November, falling short of expectations for a 0.4% increase. This modest gain partly recovered the -0.7% mom decline recorded in October. Growth in supermarkets and non-food stores provided support, but this was partially offset by weaker performance from clothing retailers.

On an annual basis, sales volumes increased by 0.5% over the year to November. However, volumes remain -1.6% below their pre-pandemic levels from February 2020.

Looking at the broader trend, retail sales volumes rose by 0.3% in the three months to November compared with the prior three-month period. Compared to the same period last year, volumes were up by 1.9%, suggesting some resilience despite ongoing economic uncertainties.

Japan’s core CPI reaccelerates to 2.7%, driven by energy and rice

Japan’s core CPI (excluding food) rose to 2.7% yoy in November, marking the first reacceleration in three months and exceeding market expectations of 2.6% yoy. Core inflation has remained above the BoJ’s 2% target since April 2022, highlighting persistent price pressures. This increase was attributed to reduced government subsidies for utility bills and a sharp rise in rice prices.

Energy prices surged 6.0% yoy, up from October’s 2.3% yoy gain. Within this category, electricity prices jumped 9.9% yoy, and city gas costs climbed 6.4% yoy. Meanwhile, rice prices soared by a staggering 63.6% yoy, the steepest increase since 1971, driven by last year’s unusually hot summer that disrupted production.

Core-core CPI (excluding food and energy) ticked up from 2.3% yoy to 2.4% yoy, while headline CPI rose to 2.9% from October’s 2.3%. Service prices, a key indicator for BOJ as they often reflect wage dynamics, increased 1.5% yoy, unchanged from the prior month.

NZ’s exports rises 9.1% yoy in Nov, imports up 3.9% yoy

New Zealand’s trade data for November showed a significant improvement, with goods exports rising 9.1% yoy to NZD 6.5B, while goods imports increased by a more modest 3.9% yoy to NZD 6.9B. The resulting trade deficit of NZD -437m was much smaller than the expected NZD -1951m.

Exports saw notable gains across key markets. Shipments to China increased 6.3% yoy, adding NZD 106m, while exports to Australia climbed 8.4% yoy (NZD 62m) and to the US by 12% yoy (NZD 85m). Exports to the EU surged the most, rising 27% yoy (NZD 74m), with shipments to Japan also showing strength at 7.2% yoy (NZD 19m).

On the import side, data was more mixed. Imports from China edged down -1.7% yoy (NZD -29m) and from the EU fell sharply by -16% yoy (NZD -163m). Similarly, imports from South Korea dropped -12% yoy (NZD -61m ). However, imports from Australia rose 14% yoy (NZD 101m) and from the US increased 7.2% yoy (NZD 41 m).

Cliff Notes: A Volatile End to the Year

Key insights from the week that was.

As is tradition in Australia, the Federal Government delivered its mid-year economic and fiscal outlook in the lead up to Christmas. As anticipated, this update highlighted a troubling combination of fading revenue windfalls and persistent strength in spending across critical services, infrastructure, cost-of-living measures and state/local grants. While 2024-25 saw a modest improvement in the budget position, future budget deficits and off-budget spending from 2025-26 through 2027-28 were revised up. Current circumstances and the outlook are consistent with a ‘two-speed’ economy, where the public sector drives growth as private demand remains weak, household spending and business investment continuing to be buffeted by tight policy and cost-of-living pressures.

The impetus for further strong growth in public demand is waning, however; and with headwinds for private sector demand only slowly abating, there is a risk of a ‘shaky handover’ of the growth baton from the government to the private sector. This theme is at the heart of our growth forecasts for 2025 and beyond, explored in detail at the national and state level in our latest Coast-to-Coast report.

Focusing on the consumer, the latest evidence from the Westpac-MI Consumer Sentiment survey continues to underscore a marked improvement in confidence through the second half of 2024. During October and November, consumer sentiment staged a rapid recovery from recession-era levels. While December saw a modest pull-back in the headline index (-2.0%), confidence in current conditions improved, particularly with respect to family finances versus a year ago (+6.9%) and whether now is a ‘good time to buy a major household item’ (4.8%). With the stage 3 tax cuts implemented and cost-of-living pressures slowly receding, a foundation for a pick-up in household consumption in Q4 and 2025 is forming, though only time will tell how strong it is.

Turning to New Zealand, the annual revisions to GDP were largely as anticipated, growth revised up through 2022 and 2023 such that, at March 2024, the economy was 2.3% larger than previously estimated. Unexpectedly though, Q2’s contraction was revised down from -0.2% to -1.1% and Q3 saw a further contraction of 1.0% against expectations for a 0.4% fall. In Q3, the decline in activity was spread across numerous sectors, the squeeze on consumers and businesses from the fight against inflation of particular note. However, some of the weakness stems from temporary factors too. Looking ahead, recovery is expected from Q4, Westpac’s GDP nowcast having moved into positive territory since October. Interest rate relief is providing a benefit, and there is more to come, our New Zealand team now expecting a low for this cycle of 3.25% after a 50bp cut in February and a 25bp reduction in April and May. This week also saw the release of the New Zealand Government’s half-year outlook. Much weaker than expected, the fiscal outlook also highlights the need for accommodative monetary policy.

Further afield, it was a strong finish to a big year thanks to three major central bank meetings.

The FOMC delivered another 25bp fed funds rate cut in December as expected, bringing cumulative easing since September to 100bps. That said, the tone of the statement was non-committal on the policy outlook, and the projections slowed the expected pace of easing. September’s 3.4% fed funds forecast for end-2025 is now not seen until end-2026. The FOMC continue to hold a favourable view of growth and the labour market and so, given persistence in inflation through 2024 and nascent risks related to the imposition of tariffs, are keen to bide their time with policy.

That said, it is evident from their forecasts that downside risks for growth are considered as material as those to the upside for inflation. We also believe it is important to keep a close watch on the risks. However, we anticipate downside activity risks are more probable in 2025 and upside risks for inflation from 2026. This leads us to hold an expectation of four cuts in 2025 against the FOMC’s two, but then two hikes in 2026 when they expect continued policy easing. We expect the inflation risks of 2026 to show persistence too, likely justifying a 10-year yield around 4.80% (along with growing fiscal uncertainty).

The Bank of Japan was the next cab off the rank, holding the policy rate at 0.25%, in line with our expectations. The statement indicated that accommodative policy alongside wages growth has supported inflation and above-potential GDP growth. The BoJ will continue monitoring whether businesses persist with robust wage increases and if that feeds through to prices. Union confederation RENGO has indicated they are aiming to negotiate a 5.0% increase in wages for FY25, with a focus on lifting wages amongst small businesses. This, alongside movements in the exchange rate were considered “more likely to affect prices”. Now that businesses feel more comfortable raising prices, future shocks to import prices, in part due to movements in the currency, are more likely to see consumer prices lift as well. A future move in policy will be predicated on whether RENGO can successfully negotiate a third consecutive strong wage increase and if higher import costs, possibly due to Trump’s policies, prompt businesses to raise prices. Evidence for this will be available in early March 2025, and the next rate increase should occur swiftly thereafter at the March 2025 policy meeting. The BoJ is likely to start winding back hawkish rhetoric after that and assess domestic and global conditions over an extended period before deciding if any further change in the policy stance is warranted.

Finally, the Bank of England met overnight and decided to keep the bank rate steady at 4.75% albeit with a bit of dissent – three out of six members voted to reduce it by 25bp. The labour market was considered ‘in balance’ but uncertainties remain around the outlook, partly a result of poor-quality data. While there has been progress on inflation since the start of the year, allowing the MPC to ease rates, concerns about inflation’s persistence are rising. More causes for uncertainty around disinflation were outlined, not limited to the expansionary measures announced in the Autumn budget and geopolitical tensions. These risks led most of the Committee to agree on a ‘gradual approach to reducing monetary policy’. From here, the Committee will want further evidence that the disinflationary pulse remains intact and that will come from signs that demand has eased to meet the constrained supply capacity. We expect the BoE will cut once per quarter in 2025 and end at a neutral rate of 3.50% by March 2026.