Sample Category Title

USD/JPY Jumps Post-Fed: Can The Rally Sustain?

Key Highlights

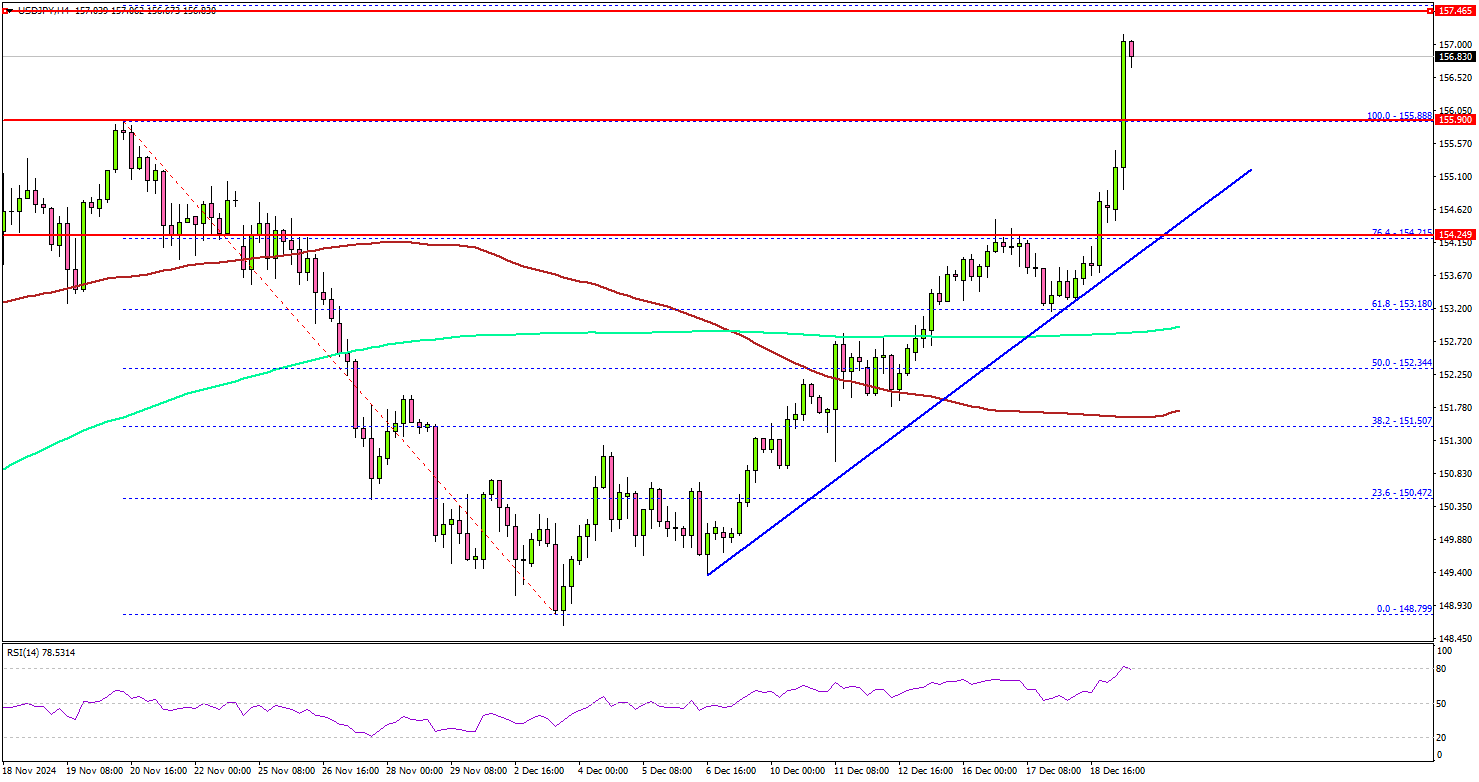

- USD/JPY started a fresh surge above the 154.00 resistance.

- A key bullish trend line is forming with support at 154.50 on the 4-hour chart.

- EUR/USD tumbled toward 1.0350 before correcting some losses.

- AUD/USD and NZD/USD accelerated losses.

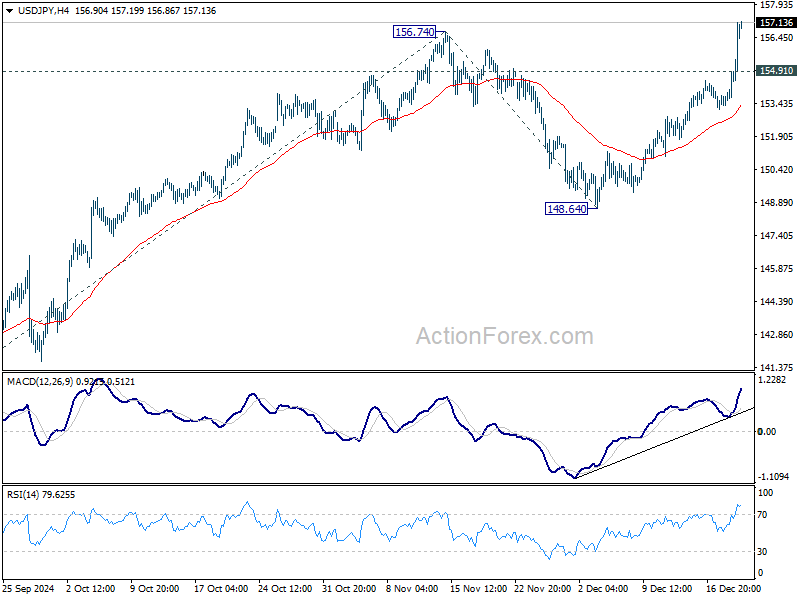

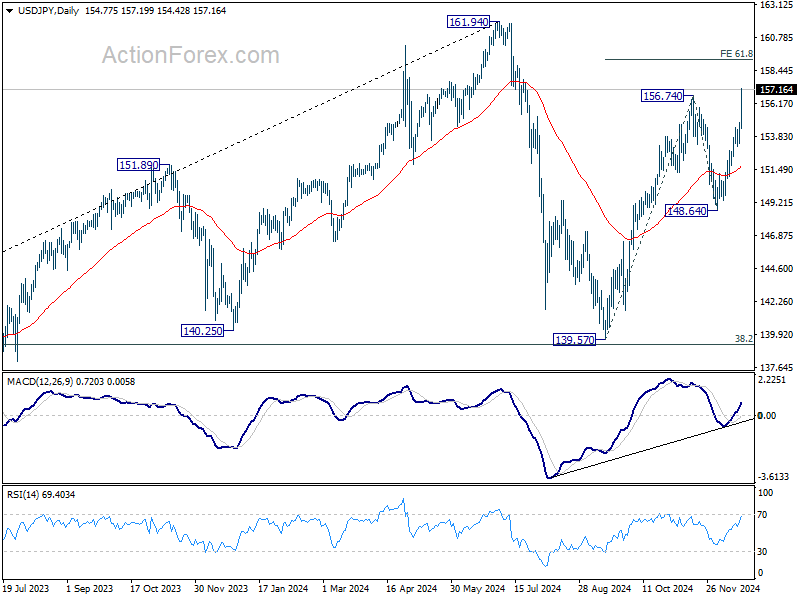

USD/JPY Technical Analysis

The US Dollar formed a base above 152.00 against the Japanese Yen. USD/JPY started a fresh surge above the 153.20 and 154.00 levels.

Looking at the 4-hour chart, the pair gained strength above the 154.20 resistance, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). It even cleared the 76.4% Fib retracement level of the downward move from the 155.88 swing high to the 148.79 low.

The bulls pushed the pair to a new monthly high above 156.50. On the upside, the pair could face resistance near the 157.40 level. The next major resistance is near the 158.00 level.

A close above the 158.00 level could set the tone for another increase. The next major resistance could be the 159.20 level, above which the price could climb higher toward the 160.00 resistance.

On the downside, immediate support sits near the 155.80 level. The next key support sits near the 155.00 level. Any more losses could send the pair toward the 154.50 level. There is also a key bullish trend line forming with support at 154.50 on the same chart.

Looking at EUR/USD, the pair declined heavily below the 1.0420 support zone before the bulls appeared near the 1.0350 zone.

Upcoming Economic Events:

US Personal Income for Nov 2024 (MoM) - Forecast +0.4%, versus +0.6% previous.

US Core Personal Consumption Expenditure for Nov 2024 (MoM) - Forecast +0.2%, versus +0.3% previous.

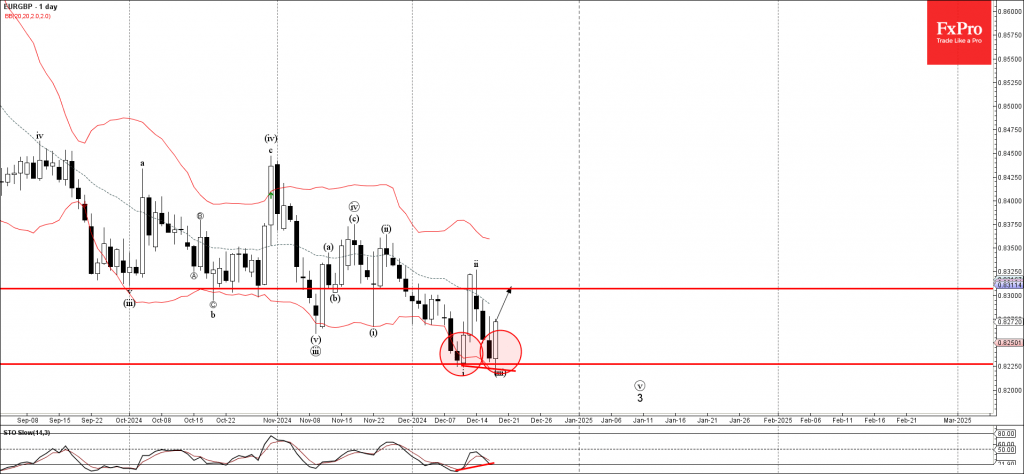

EURGBP Wave Analysis

- EURGBP reversed from support zone

- Likely to rise to resistance level 0.8300

EURGBP currency pair recently reversed up from the support zone located between the key support level 0.8225 (which stopped the previous minor impulse wave i) and the lower daily Bollinger Band.

The upward reversal from this from the support zone is likely to form the daily Japanese candlesticks reversal pattern Bullish Engulfing – of the pair closes today near the current levels.

Given the bullish divergence on the daily Stochastic, EURGBP currency pair can be expected to rise to the next resistance level 0.8300.

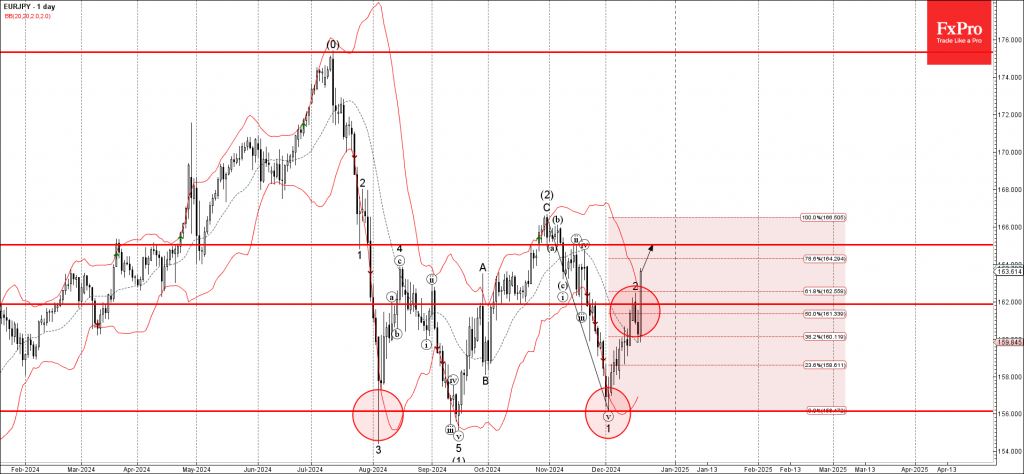

EURJPY Wave Analysis

- EURJPY broke resistance zone

- Likely to rise to resistance level 165.00

EURJPY currency pair recently broke the resistance zone located between the key resistance level 162.00 (which stopped the previous minor wave 2) and the 50% Fibonacci correction of the downward impulse 1 from October.

The breakout of this resistance zone accelerated added to the bullish pressure on this currency pair.

EURJPY currency pair can be expected to rise further to the next resistance level 165.00 (which reversed the price multiple times in November).

Bank of England Review – BoE to Lag Peers in 2025; We Stay Positive GBP

- At today's monetary policy meeting the BoE kept the Bank Rate unchanged at 4.75%, which was widely expected.

- The BoE delivered a dovish vote split but continues to emphasise a gradual approach to reducing the restrictiveness of monetary policy. We think this supports our base case of the next cut coming in February and a quarterly pace thereafter.

- The market reaction was modest with Gilt yields tracking slightly lower and EUR/GBP moving higher.

As expected, the Bank of England (BoE) decided to keep the Bank Rate unchanged at 4.75% today. The vote split had a dovish twist with 6 members voting for an unchanged decision and Dhingra, Ramsden and newcomer Taylor voting for a 25bp cut.

The BoE retained much of its previous guidance noting that "a gradual approach to removing policy restraint remains appropriate" and that "monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further". The MPC now judges that the labour market is "broadly in balance" and has similarly revised its expectation for Q4 growth down from 0.3% q/q to no growth as a reflection of the latest weakening in growth indicators. We also note that in the unchanged camp of the MPC, one member considered that a more "activist strategy" could be warranted, hinting at a more dovish shift in the centrist camp.

Given the recent topside surprises to wage and inflation data combined with an expansionary fiscal stance, we think a continuation of a gradual cutting cycle is warranted. We therefore adjust our call, expecting quarterly cuts in 2025 at the meetings associated with updated economic projections. We expect the next 25bp cut in February with the Bank Rate ending the year at 3.75% (prev. 3.25%). We maintain our terminal rate forecast unchanged at 2.75% but expect it to be reached by Q4 2026 (prev. Q2 2026). However, we highlight that the risk is skewed towards a swifter cutting cycle in the first half of 2025, as highlighted by the MPCs communication today.

Rates. Gilt yields moved lower across the board on the dovish vote split but overall, the reaction was muted. Markets price 18bp worth of cuts for February and 55bp by YE 2025. We highlight the potential for BoE to deliver more easing in 2025 than currently priced, expecting a cut in February and a total of 100bp worth of easing in 2025.

FX. EUR/GBP moved higher on the announcement with the dovish vote split taking centre stage. The still cautious guidance delivered today highlights the more gradual approach of the BoE compared to European peers. We think this supports our case of a continued move lower in EUR/GBP. This is further amplified by relative UK economic outperformance and tight credit spreads. The key risk is a soft BoE.

Sunset Market Commentary

Markets

Yesterday’s hawkish FOMC cut still resonated today. The front end of the curve outperformed slightly after US money markets even outhawked the Fed, looking to only 1 instead 2 rate cuts next year. The US 2-yr yield returns 4.5 bps of yesterday’s 15 bps gain. Long-end US bond yields remain upwardly oriented with the 10-yr and 30-yr yields respectively rising by 3.8 bps (10-yr) to 5.8 bps (30-yr). US president-elect Trump wants to kill a compromise reached between Democrats and Republicans for a three-month stopgap funding extension. Without a deal, the US faces a partial government shutdown by Saturday. He wants to slimdown the package and attach an increase to the debt ceiling (expires in June) to it. NBC even reported that he would support abolishing the debt ceiling altogether. In absence of European numbers, European bonds reacted to the move in US Treasuries yesterday. German yields rise by 4.5 bps (2-yr) to 7.2 bps (10-yr).

The Bank of England kept its policy rate unchanged at 4.75% in a 6-3 majority vote. Three members voted in favour of a 25 bps rate cut (Dhingra, Ramsden and Taylor). We add that one member of the current majority is close to flipping to a more activist approach. Minutes showed him/her arguing that the evolution and prospects for disaggregated measures of activity and inflation could warrant such behavior. Since the previous meeting, inflation rose slightly more than expected (2.6% Y/Y in November), owing in large part to stronger inflation in core goods and food, and is expected to continue to rise slightly in the near term. Bank staff expect GDP growth to have been weaker at the end of the year than projected in November while the labour market is broadly in balance. The outlook is surrounded by more and more domestic (eg impact Autumn budget) and international (geopolitics) uncertainty. A gradual approach to removing monetary policy restraint remains appropriate. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The market reaction suggests that the split within the board was bigger than expected and that UK money markets took it too far in pricing out 2025 policy rate cuts. UK gilt yields gave away all of the post-FOMC gains with daily changes currently ranging between -2.3 bp (2-yr) and +6.1 bps (30-yr). EUR/GBP bounces off the YtD low at 0.8222 to currently change hands around 0.8260.

News & Views

The Swedish central bank lowered the policy rates by 25 bps to 2.5%. If the economic and inflation outlook holds, it expects to cut rates once again in the first half of 2025. Based on the Riksbank’s own rate forecasts, that would also be the last one of the current cycle: from 2025Q2 on through 2027 it has penciled in a 2.25% policy rate. This is exactly the mid-point of the 1.5-3% neutral rate estimate. After the rapid rate reduction and given the fact that monetary policy works with a lag, the central bank moved to “a more tentative approach when monetary policy is formulated going forward.” Also suggestive of the central bank nearing the end game is the first upward revision to December inflation forecasts since March of this year. The Riksbank expects CPIF to average 1.9%-2%-1.9% over 2024-2025-2026. This compares to 1.7%-1.6%-1.9% in September. The 2027 outcome is seen at 2%. Growth projections were more or less left unchanged at 0.6%-1.8%-2.6%-2.1% over 2025-2027. Swedish swap rates jumped by >10 bps. Gains for the Swedish krone (to EUR/SEK 11.45) could have been bigger if it not were for the risk aversion holding sway on broader financial markets.

The Norwegian central bank stuck to its long-term pledge to keep rates steady at 4.5% through the end of the year. The Norges Bank said that a restrictive monetary policy is still needed but that the time to begin monetary easing is soon approaching, with March 2025 aired as the most likely opportunity to do so. Inflation came in slightly lower than expected, offering some room for rate cuts. That said, it still averages above the 2% target over the policy horizon. GDP would expand at a faster pace next year than expected in September on the back of fiscal policy, consumer spending and higher petroleum investment than previously assumed. One of the key reasons for the Norges Bank to have deviated from major peers by keeping rates steady for so long, was the weak Norwegian currency. It still sees the NOK as a key risk that could derail any rate cutting plans if it were to depreciate further. The NOK loses some marginal ground after today’s decision. EUR/NOK moved to 11.81. Money market expectations were little changed with a first full rate cut priced in by March.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 153.78; (P) 154.32; (R1) 155.38; More...

USD/JPY's break of 156.74 resistance confirms resumption of whole rally from 139.57. Intraday bias stays on the upside for 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. On the downside, below 154.91 minor support will turn intraday bias neutral again first. But outlook will stay bullish as long as 153.15 support holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

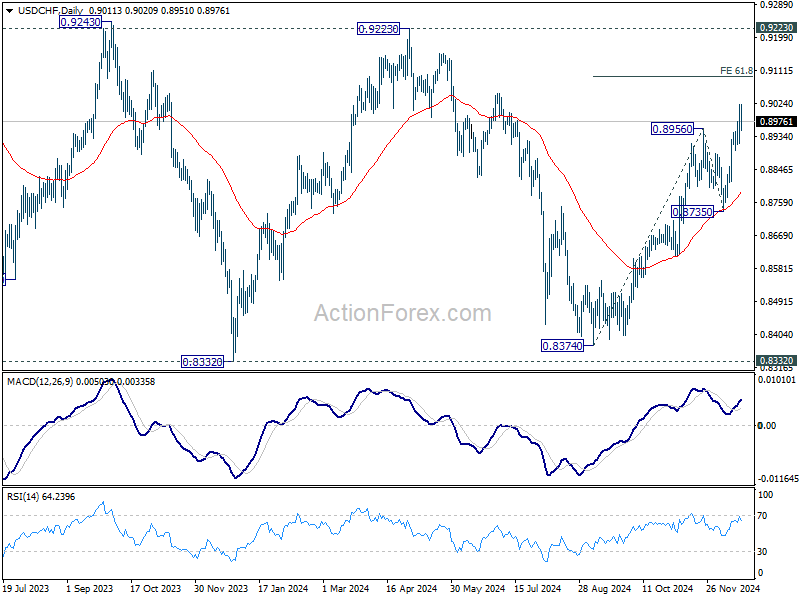

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8946; (P) 0.8983; (R1) 0.9049; More…

Intraday bias in USD/CHF remains on the upside for the moment. Current rally from 0.8374 is in progress for 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095 next. On the downside, below 0.8916 minor support will turn intraday bias neutral first. But outlook will stays bullish as long as 0.8735 support holds.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0292; (P) 1.0402; (R1) 1.0461; More...

Intraday bias in EUR/USD remains on the downside for 1.0330 support. Firm break there will target 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254, and then 100% projection at 1.0023. On the upside, above 1.0452 will turn intraday bias neutral again first.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

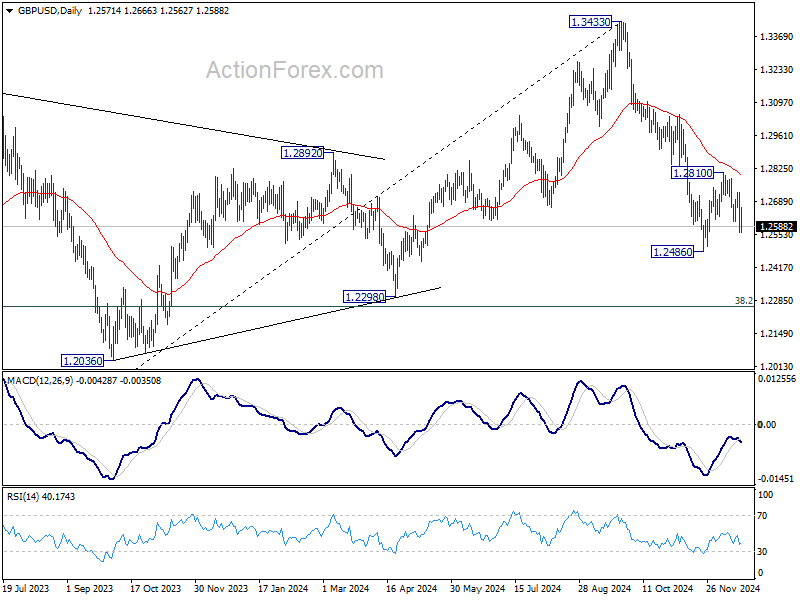

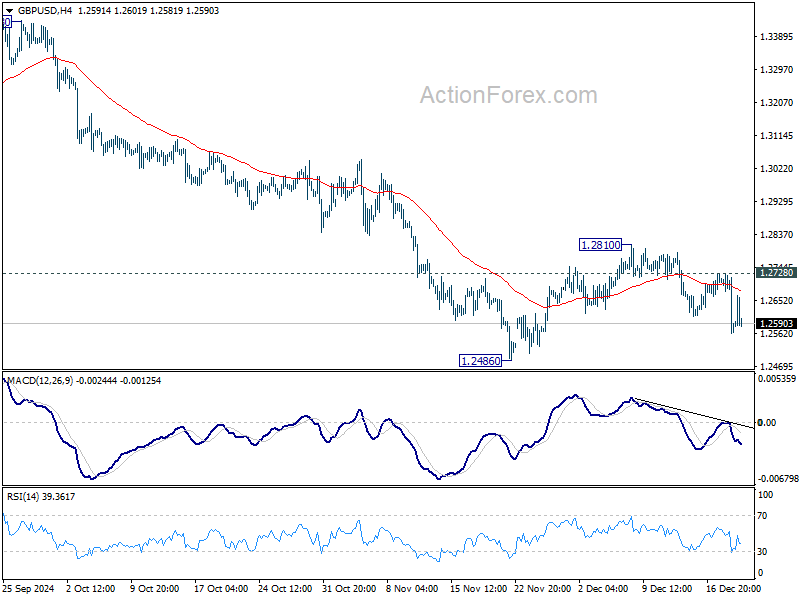

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2621; (R1) 1.2679; More...

Intraday bias in GBP/USD remains on the downside despite some volatility during today. Recovery from 1.2486 should have completed at 1.2810. Retest of 1.2486 should be seen next. Firm break there will resume the fall from 1.3433 and target 1.2298 cluster support zone. Nevertheless, break of 1.2728 minor resistance will turn bias to the upside for 1.2810 and above instead.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.