Sample Category Title

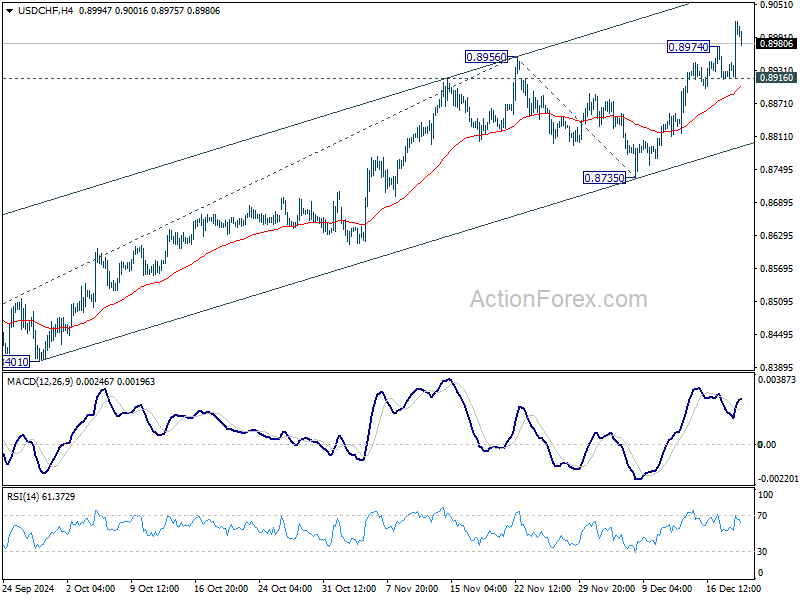

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8946; (P) 0.8983; (R1) 0.9049; More…

USD/CHF's rally resumed after brief consolidations and intraday bias is back on the upside. Current rise from 08374 should target 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095 next. On the downside, below 0.8916 minor support will turn intraday bias neutral first. But outlook will stays bullish as long as 0.8735 support holds.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

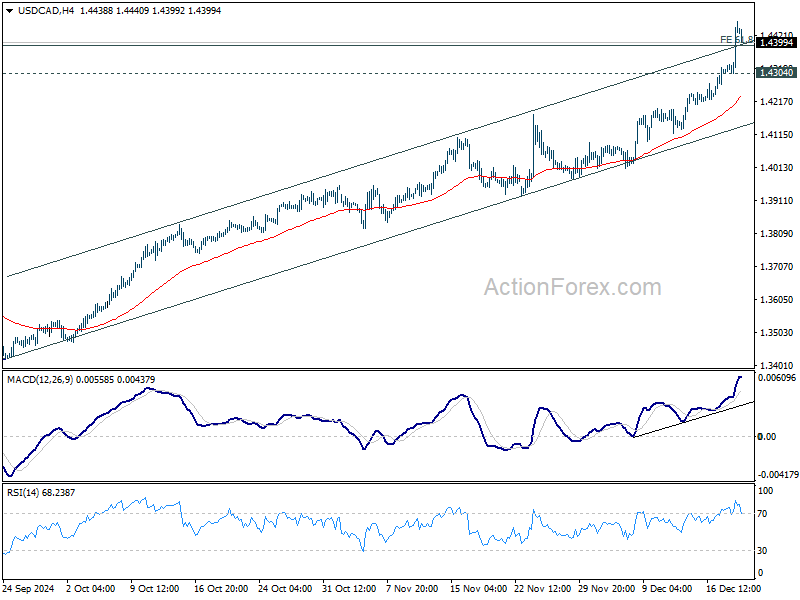

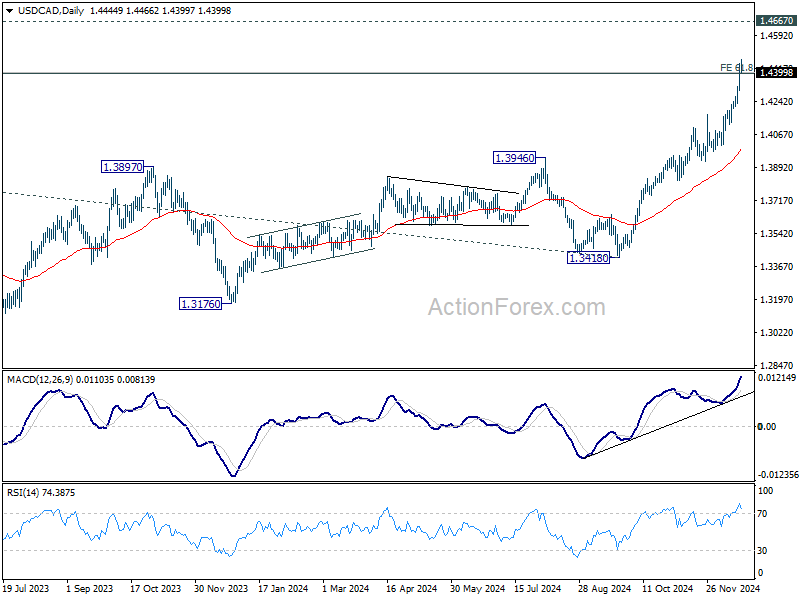

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.4351; (P) 1.4401; (R1) 1.4497; More...

USD/CAD's rally accelerates further higher and breaks through 1.4391 medium term projection level. There is no sign of topping yet and intraday bias stays on the upside, Next target is 1.4667 long term resistance. On the downside, below 1.4304 minor support will turn intraday bias neutral and bring consolidations first.

In the bigger picture, up trend from 1.2005 (2021) is in progress and met 61.8% projection of 1.2401 to 1.3976 from 1.3418 at 1.4391 already. Sustained trading above there will pave the way to 1.4667/89 key resistance zone (2020/2015 highs). Medium term outlook will remain bullish as long as 55 W EMA (now at 1.3706) holds, even in case of deep pullback.

It’s Higher for Longer All Over Again

Markets

The Fed lowered policy rates yesterday from 4.5%-4.75% to 4.25-4.5%, a level chair Powell said is still “meaningfully restrictive”. The decision was expected but not unanimous. Cleveland Fed Hammack voted to keep rates steady which given the circumstances had a lot to say for. The economy is doing fine with GDP forecasts left unchanged at a very decent 1.9-2.1% over the policy horizon. PCE inflation was revised higher to 2.5% from 2.1% in 2025 before easing towards the 2% goal by 2027. Core PCE faced a similar upward adjustment. The FOMC moved from seeing risks to both inflation gauges as broadly balanced in September to skewed to the upside. In the same vein, uncertainty about both was now much higher. Asked why the Fed did cut, Powell noted the labour market is still cooling, be it gradually, while the inflation story was “broadly on track”. The language in the statement on future cuts changed in a hawkish way though with the bold part being the addition: “In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks.” Powell said this signals the Fed is at or near a point to slow the pace of further adjustments. He added that after having cut a cumulative 100 bps the Fed is now “significantly closer to neutral”, warranting a cautious stance. In the updated dot plot, the median rate forecast shifted up by 50 bps over the horizon, meaning next year is now showing two 25 bps rate cuts instead of four. In addition, the policy rate is expected to remain above an upwardly revised neutral rate (to 3%) in 2025-2027. It’s higher for longer all over again. Powell at the very end of the presser, while labeling it as not a likely outcome, did not even want to rule out a rate hike next year. US yields surged between 8.8 (30-yr) and 14.1 (5-yr) bps on the Fed’s hawkish pivot and may have more room to run in the current momentum. US money markets not even fully price in two cuts next year. The dollar closed at the highest level in two years against the euro. EUR/USD finished at 1.0353 compared to the 1.0491 open. Critical support at 1.0335 (November intraday correction low) is at risk. The trade-weighted index topped 108 for the first time since November 2022.

Multiple central banks convene today. We already had Japan (see below). Next up is Sweden, Norway and the Czech Republic. In core markets, attention shifts from the Fed to the Bank of England. The intermediate meeting is without updated forecasts though. The status quo at 4.75% is all but certain. Governor Bailey’s guidance for 2025 is way more interesting. This week’s stronger-than-expected wage growth and stubborn inflation pressures (core, services) leave the central bank little wiggle room. Money markets barely price in two cuts next year. It’s keeping sterling locked near recent highs against the euro around EUR/GBP 0.823. If Bailey is only a fraction as hawkish as Powell yesterday, a test of EUR/GBP 0.8203 is on the cards.

News & Views

The Bank of Japan kept rates steady at 0.25% this morning. The decision was widely expected after the likes of Reuters and Bloomberg cited sources that the central bank was leaning towards the status quo. Tamura dissented and voted for a hike as the economy and prices were moving as expected and inflation risks were increasing. With the economy “likely to keep growing at a pace above its potential growth rate” and inflation expected to be sustainably at target as projected in the October outlook, a third hike is coming nevertheless. Governor Ueda during the presser confirmed this but said they wanted more information on wage hikes first. The lack thereof today was the reason why they held rates. Since these wage negotiations (shunto) only take place in February/March, a January rate hike suddenly is being questioned as well. The yen, which was already pressured by a strong USD, extends losses on Ueda’s comments. USD/JPY shoots higher to 156.3. Verbal interventions are probably incoming.

New Zealand GDP contracted a much bigger than expected 1% Q/Q in the third quarter this year. It followed a downwardly revised 1.1% (from -0.2%) in Q2, meaning the country technically entered a recession. GDP was 1.5% smaller than in 2024Q3. Part of the steep decline was statistically inspired with adjustments to earlier readings having caused a higher comparison base. Details do show a weak performance across the board from household consumption (-0.3% Q/Q), capital formation (-2.9%) and government consumption (-1.9%). Exports (-2.1%) dropped more than imports (-0.4%) did. The kiwi dollar tumbled on the release with the dollar compounding the downleg in NZD/USD. The pair closed at 0.562. Swap rates slipped 5 bps at the front end of the curve.

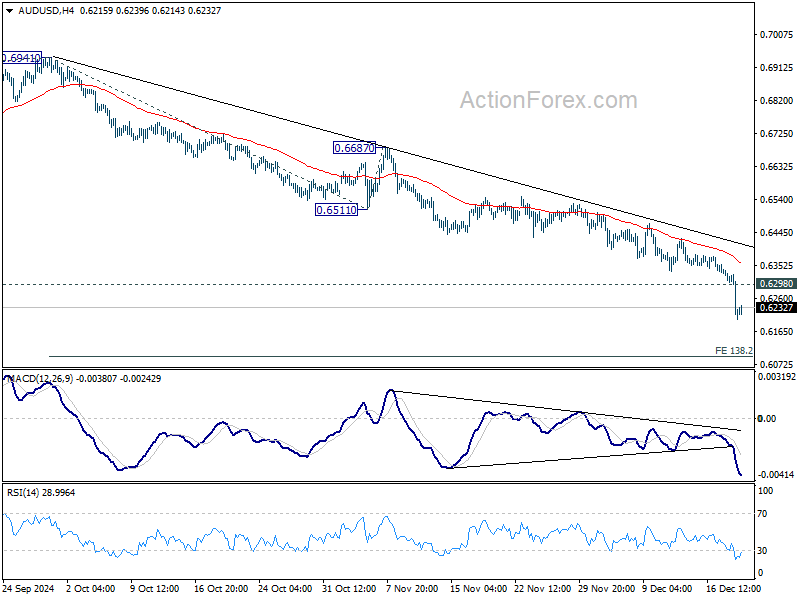

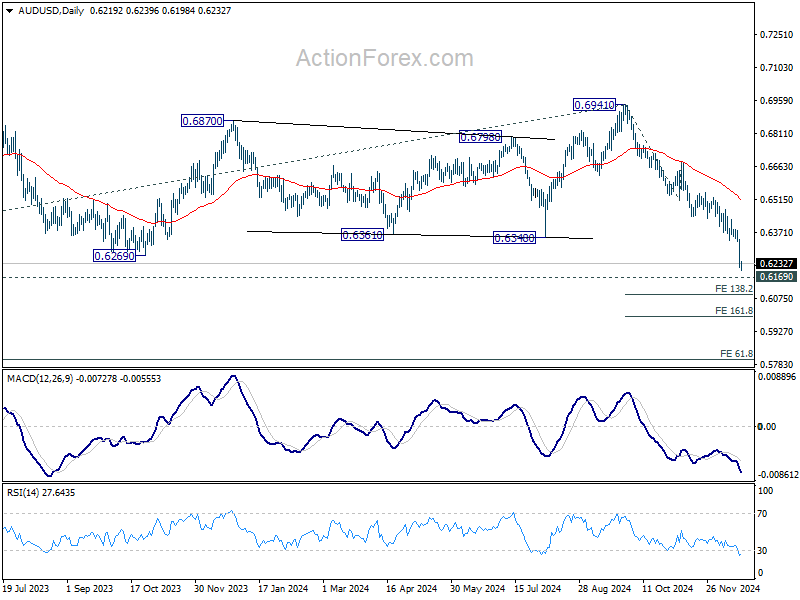

AUD/USD Daily Report

Daily Pivots: (S1) 0.6174; (P) 0.6258; (R1) 0.6302; More...

AUD/USD's decline accelerates lower and intraday bias says on the downside for 0.6169 key support. Decisive break there will confirm larger down trend resumption. Next near term target is 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. On the upside, above 0.6298 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

Market Chaos Unfolds Despite Widely Expected Fed Hawkish Cut

Fed’s hawkish rate cut overnight sparked an outsized market reaction, with DOW plunging over -1100 points and NASDAQ losing -3.5%. Fed’s messages didn't deviate from expectations leading to the meeting, indicating a slower easing path in 2025 with likely just two more rate cuts and a terminal rate near or above 3.0%. But markets responded as though these signals were underappreciated. The repricing of expectations pushed Fed fund futures to reflect a 90% chance of a January pause, up from 80% just a week earlier.

Dollar surged as the strongest performer in the currency markets, benefiting from risk aversion, Fed expectations, and a climb in 10-year Treasury yields, which are now approaching the 4.5% mark.

On the other hand, commodity currencies came under intense pressure. New Zealand Dollar was the weakest, hit hard by bleak GDP data showing a -1.0% contraction in Q3 and a sharp downward revision for Q2. Australian Dollar followed, weighed down by broader risk-off sentiment.

Yen also struggled after BoJ held rates steady, and dropped no hint on the timing of the next rate hike. BoJ Governor Kazuo Ueda maintained a cautious tone, citing uncertainties tied to domestic wage growth and the impact of trade policies from the incoming US administration.

British Pound, while sharply lower against the dollar, has shown relative resilience, ranking second strongest for the week. With BoE rate decision approaching, markets are watching for any changes in MPC voting. While a hold is widely expected, focus lies on whether another member might join Swati Dhingra in voting for a cut.

Swiss Franc is third-best for the week, while Euro and Canadian Dollar sit in the middle of the pack, although none appear strong compared to the greenback.

Technically, an immediate focus is now on whether US 10-year yield could power through 4.505 resistance to resume the rally from 3.603. That would set up further rise to 61.8% projection of 3.603 to 4.505 from 4.126 at 4.683 in the near term, and probably revisiting 4.997 high in the early part of next year. If realized, that would give extra boost to Dollar, in particular in USD/JPY.

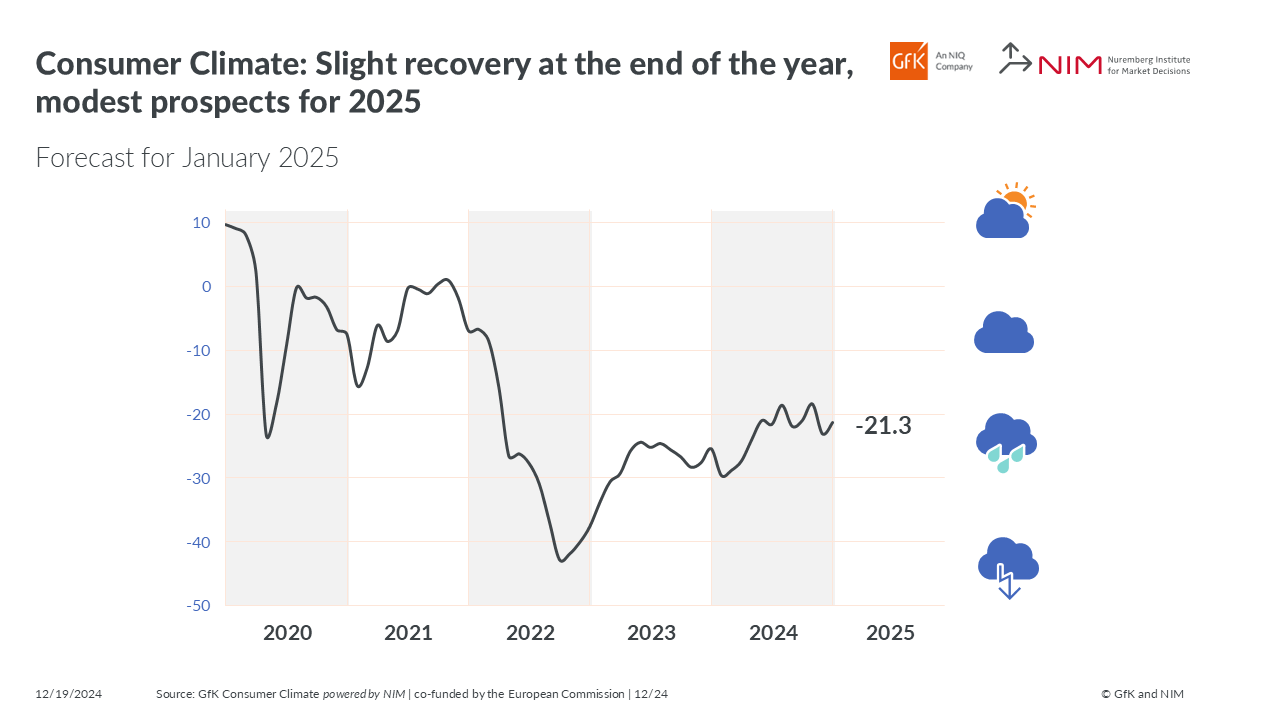

German Gfk consumer sentiment improves slightly but remains fragile

Germany’s GfK Consumer Sentiment Index for January rose to -21.3, improving from December’s -23.1.

December’s subindices reflected mixed dynamics: economic expectations moved into positive territory at 0.3, up from -3.6, and income expectations increased to 1.4 from -3.5. Willingness to buy also ticked higher to -5.4 from -6.0, while willingness to save fell sharply to 5.9 from 11.9.

According to Rolf Bürkl, consumer expert at NIM, the improvement comes after a steep decline the prior month, partially reversing earlier losses. However, Bürkl noted that at -21.3 points, consumer sentiment remains at a very low level, highlighting a trend of "stagnation since mid-2024."

He warned that a sustained recovery is "not yet in sight" due to persistent challenges. High food and energy prices, alongside growing concerns about job security in key sectors, continue to weigh heavily on sentiment.

BoJ stand pat, highlights wage and global risks

BoJ kept its uncollateralized overnight call rate unchanged at 0.25%, as widely anticipated, with an 8-1 vote in favor. Naoki Tamura dissented, advocating for a rate increase to 0.50%.

Governor Kazuo Ueda, speaking at the post-meeting press conference, reiterated that rate hikes would proceed cautiously. He noted, "If the economy and prices move in line with our forecast, we will continue to raise our policy rate," but emphasized the need to carefully assess data before adjusting the level of monetary support.

The gradual pace of tightening, he explained, is due to the "moderate" rise in underlying inflation, which lacks the strength to warrant aggressive moves.

Ueda highlighted the importance of monitoring wage dynamics, particularly in the context of next year’s wage negotiations, to gauge the strength of Japan’s wage-inflation cycle.

He also pointed to uncertainties in the global economic outlook and the impacts of policy decisions under the incoming U.S. administration, despite the overall resilience of the US economy.

New Zealand's GDP contracts -1% qoq in Q3, broad economic weakness

New Zealand’s economy contracted by -1.0% qoq in Q3, significantly worse than market expectations of -0.2%. The previous quarter’s GDP figure was also revised down sharply, from -0.2% to -1.1%, painting a grimmer picture of the country’s economic performance.

The decline was broad-based, with activity falling in 11 out of 16 industries, including significant contractions in manufacturing, business services, and construction. While primary industries posted gains, both goods-producing and service industries experienced declines.

On a per capita basis, GDP dropped -1.2% qoq, marking the eighth consecutive quarterly decline. The expenditure measure of GDP also contracted by -0.8% qoq. Notably, household consumption expenditure decreased by -0.3% qoq, with reductions in spending on essentials such as grocery food and electricity, highlighting the strain on consumer budgets.

NZ ANZ business confidence falls to 62.3, demand recovery offers glimmers of hope

New Zealand’s ANZ Business Confidence Index fell to 62.3 in December, down from 64.9. However, some subindices showed encouraging signs of recovery. The own activity outlook improved to 50.3 from 48.0, while profit expectations rose significantly to 31.1 from 26.5. Investment intentions also jumped to 21.5 from 18.0, signaling increased business willingness to allocate resources despite a challenging environment.

However, labor market metrics were mixed, with employment intentions slipping slightly from 14.7 to 14.3. At the same time, cost pressures intensified sharply, as cost expectations surged to 70.1 from 62.9, and wage expectations jumped from 75.5 to 79.2. Price intentions remained steady at 42.7, slightly up from 42.2, while inflation expectations ticked higher to 2.63%, up from 2.53%, reflecting ongoing pricing pressures.

ANZ noted that while the survey results indicate signs of recovering demand, they come against the backdrop of this morning’s weak Q3 GDP figures, which showed a sharp contraction. The low bar set by the GDP downturn provides room for optimism if demand continues to improve. However, rising cost and wage pressures could complicate the outlook, especially for inflation management.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6174; (P) 0.6258; (R1) 0.6302; More...

AUD/USD's decline accelerates lower and intraday bias says on the downside for 0.6169 key support. Decisive break there will confirm larger down trend resumption. Next near term target is 138.2% projection of 0.6941 to 0.6511 from 0.6687 at 0.6074. On the upside, above 0.6298 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term consolidation to the down trend from 0.8006. More sideway trading could be seen above 0.6169, but overall outlook will stay bearish as long as 0.6941 resistance holds. Firm break of 0.6169 will resume the down trend to 61.8% projection of 0.8006 to 0.6169 from 0.6941 at 0.5806 next.

German Gfk consumer sentiment improves slightly but remains fragile

Germany’s GfK Consumer Sentiment Index for January rose to -21.3, improving from December’s -23.1.

December’s subindices reflected mixed dynamics: economic expectations moved into positive territory at 0.3, up from -3.6, and income expectations increased to 1.4 from -3.5. Willingness to buy also ticked higher to -5.4 from -6.0, while willingness to save fell sharply to 5.9 from 11.9.

According to Rolf Bürkl, consumer expert at NIM, the improvement comes after a steep decline the prior month, partially reversing earlier losses. However, Bürkl noted that at -21.3 points, consumer sentiment remains at a very low level, highlighting a trend of "stagnation since mid-2024."

He warned that a sustained recovery is "not yet in sight" due to persistent challenges. High food and energy prices, alongside growing concerns about job security in key sectors, continue to weigh heavily on sentiment.

BoJ stand pat, highlights wage and global risks

BoJ kept its uncollateralized overnight call rate unchanged at 0.25%, as widely anticipated, with an 8-1 vote in favor. Naoki Tamura dissented, advocating for a rate increase to 0.50%.

Governor Kazuo Ueda, speaking at the post-meeting press conference, reiterated that rate hikes would proceed cautiously. He noted, "If the economy and prices move in line with our forecast, we will continue to raise our policy rate," but emphasized the need to carefully assess data before adjusting the level of monetary support.

The gradual pace of tightening, he explained, is due to the "moderate" rise in underlying inflation, which lacks the strength to warrant aggressive moves.

Ueda highlighted the importance of monitoring wage dynamics, particularly in the context of next year’s wage negotiations, to gauge the strength of Japan’s wage-inflation cycle.

He also pointed to uncertainties in the global economic outlook and the impacts of policy decisions under the incoming U.S. administration, despite the overall resilience of the US economy.

Big Central Bank Day Ahead

In focus today

A packed European central bank day kicks off with the Riksbank decision at 9:30 CET. We expect a 25bp cut to 2.50% and that the central bank will maintain a message of more cuts at the beginning of 2025. Following the November decision to cut by 50bp to 2.75%, the communication has been that the September rate path largely holds. We expect the new rate path to signal an endpoint of around 2.10%. See our preview in last week's Reading the Markets Sweden, 13 December.

We expect Norges Bank to keep the policy rate unchanged at 4.5% and to signal that the first cut is most likely to be delivered in March. The decision will be published at 10:00 CET. We expect that the rate path will be marginally adjusted upwards and indicate between three and four rate cuts next year and a policy rate of just over 2.5% towards the end of the forecast period. This is well in line with the current market pricing for next year, but significantly lower for 2026-27. Our full preview can be found in last week's Reading the Markets Norway, 13 December.

For the Bank of England (BoE) decision at 13:00 CET, we expect the Bank Rate to be kept unchanged at 4.75% in line with consensus and market pricing. We pencil in a vote split of 8-1. Note, this meeting will not include updated projections nor a press conference. In 2025, we expect cuts at every meeting starting in February and until H2 2025 where we pencil in a slowdown to only quarterly cuts. This leaves the Bank Rate at 3.25% by end-2025. See our Bank of England preview, 16 December, for more details.

Today's data calendar is light with the US Philly-Fed business sentiment indicator for December being one of few highlights. In Sweden, the social partners within the industry exchange demands for the 2025 wage negotiation this morning.

Economic and market news

What happened overnight

Bank of Japan (BoJ) chose to keep rates unchanged, which was in line with market pricing and our call. The vote split was 8-1. The economic recovery in Japan looks on track, real wages have at least stopped falling and inflation is close to target. Thus, there is a sound case for hiking rates. The need for yen-support however seemed a bit less acute and the cost of postponing to January had come down. At least that was the case before the hawkish Fed turn yesterday. The yen has had some rough hours, sliding another 1% vs. the USD, first on the FOMC meeting and then the BoJ announcement. If anything, Governor Ueda will probably take a hawkish tone on the press conference to avoid adding further to the yen slide. We expect the BoJ will hike by 25bp in January.

What happened yesterday

The Federal Reserve cut the policy rate target by 25bp to 4.25-4.50% at last night's meeting, yet Chair Powell struck a very hawkish tone on the outlook. Policy has entered 'a new phase', and barring major downside data surprises, the Fed expects a slower pace of rate cuts starting from January. The updated median dots now project only a single 25bp cut every six months for the next 2.5 years, while the longer-term dot was raised by 0.1pp to 3.0%. We have revised up our forecast for the Fed funds rate, and now expect only quarterly 25bp cuts from Mar/25 onwards. We maintain our terminal rate forecast at 3.00-3.25% (reached in Mar/26, prev. Sep/25). See Fed review: In a new phase, 18 December.

In the UK, inflation surprised slightly to the downside in November but overshot the BoE's forecast. Headline came in at 2.6% y/y (consensus: 2.6%, prior: 2.3%, BoE: 2.4%), core at 3.5% y/y (consensus: 3.6%, prior: 3.3%) and services at 5.0% y/y (consensus: 5.1%, prior: 5.0%, BoE. 4.9%). While service inflation momentum slowed, our own measure of core services, which excludes volatile components, increased slightly after edging lower the past many months. Service inflation is likely to stay around 5% for the next couple of months, arguing for a more gradual approach from the BoE.

In US politics, incoming President Trump warned fellow Republicans of potential ousting if they chose to support House Speaker Johnson's bipartisan funding bill, which would extend the current funding debate until mid-March. Trump insists that the bill should include an increase in the debt ceiling. If new funding is not agreed upon by Saturday, a partial shutdown of the US government could be the consequence.

Equities: Global equities declined sharply yesterday, driven by the US and the hawkish cut from the Federal Reserve, combined with a notable increase in inflation expectations in the Summary of Economic Projections (SEP). US equity markets got all the attention yesterday, as most indices experienced their worst session since the early August turmoil and ended close to the day's low following the Fed meeting. With the significant turnaround, some of the past winners were sold off the most, particularly in consumer discretionary and auto & components sectors, with Tesla leading the decline, down 8%. Additionally, inflation fears resurfaced, impacting growth stocks and especially small caps, with the Russell 2000 losing 4.4% yesterday. The VIX increased from 16 to 28, which speaks more about investors' positioning leading into this rather than the Fed change yesterday. As we approach Christmas, this situation becomes more delicate, as many investors likely remember 2018, when equities plummeted in December, accelerating towards Christmas Eve, only to recover the losses in the following three months. While we are in a different macroeconomic and monetary environment this time, we perceive risks for the markets, as investors are heavily loaded on risk and might be tempted to de-risk ahead of the holiday season. In the US yesterday, Dow -2.6%, S&P 500 -3.0%, Nasdaq -3.6%, and Russell 2000 -4.4%. Asian markets are lower this morning, but the movements are rather limited compared to what happened on Wall Street yesterday. US futures are mixed while European fugures are down by 1-1.5%.

FI: US rates rose significantly following yesterday's hawkish signals from Powell. The UST curve trades about 13-15bp higher this morning, which will of course have implications for the EUR rates markets today. As market-based inflation expectation measures are (roughly unchanged), yesterday's strong increase in yields and deep drop in equities has left US financial conditions significantly tighter. If this spills over to the EUR market, it could warrant a softer tone from the ECB at the coming period. The pricing of Fed cuts next year is about 20bp lower with only 35bp priced until end-2025. The EUR curve was roughly unchanged with the action happening after the close.

FX: FOMC decided to cut the Fed funds target range by 25bp to 4.25-4.50%, as expected. It was a hawkish cut as the rate path was lifted by half a percentage point for both 2025 and 2026, thus signalling a slower easing pace from here. The USD took a leap higher as did US yields. EUR/USD dropped well below 1.04 and USD/JPY toward 154.50, where the latter rose another figure to around 155.50 after the Bank of Japan left rates unchanged this morning. The overall reaction in EUR/Scandies was muted, though with a slight move higher. In relation to the Riksbank's rate decision today, market-moving surprises, if any, could come with guidance including the rate path. We expect unchanged rates from both the Bank of England and Norges Bank, in line with market pricing, and hence we expect the FX response will be muted.

NZ ANZ business confidence falls to 62.3, demand recovery offers glimmers of hope

New Zealand’s ANZ Business Confidence Index fell to 62.3 in December, down from 64.9. However, some subindices showed encouraging signs of recovery. The own activity outlook improved to 50.3 from 48.0, while profit expectations rose significantly to 31.1 from 26.5. Investment intentions also jumped to 21.5 from 18.0, signaling increased business willingness to allocate resources despite a challenging environment.

However, labor market metrics were mixed, with employment intentions slipping slightly from 14.7 to 14.3. At the same time, cost pressures intensified sharply, as cost expectations surged to 70.1 from 62.9, and wage expectations jumped from 75.5 to 79.2. Price intentions remained steady at 42.7, slightly up from 42.2, while inflation expectations ticked higher to 2.63%, up from 2.53%, reflecting ongoing pricing pressures.

ANZ noted that while the survey results indicate signs of recovering demand, they come against the backdrop of this morning’s weak Q3 GDP figures, which showed a sharp contraction. The low bar set by the GDP downturn provides room for optimism if demand continues to improve. However, rising cost and wage pressures could complicate the outlook, especially for inflation management.

New Zealand’s GDP contracts -1% qoq in Q3, broad economic weakness

New Zealand’s economy contracted by -1.0% qoq in Q3, significantly worse than market expectations of -0.2%. The previous quarter’s GDP figure was also revised down sharply, from -0.2% to -1.1%, painting a grimmer picture of the country’s economic performance.

The decline was broad-based, with activity falling in 11 out of 16 industries, including significant contractions in manufacturing, business services, and construction. While primary industries posted gains, both goods-producing and service industries experienced declines.

On a per capita basis, GDP dropped -1.2% qoq, marking the eighth consecutive quarterly decline. The expenditure measure of GDP also contracted by -0.8% qoq. Notably, household consumption expenditure decreased by -0.3% qoq, with reductions in spending on essentials such as grocery food and electricity, highlighting the strain on consumer budgets.