Sample Category Title

FOMC Preview: What to Expect and How Will It Impact US Dollar?

- The FOMC meeting today is highly anticipated due to uncertainty surrounding future US monetary policy.

- Markets expect a 25 bps rate cut today and a slower pace of easing in 2025 due to President-elect Trump’s policies.

- The Fed’s reverse repo rate may be adjusted, potentially impacting the US Dollar’s strength.

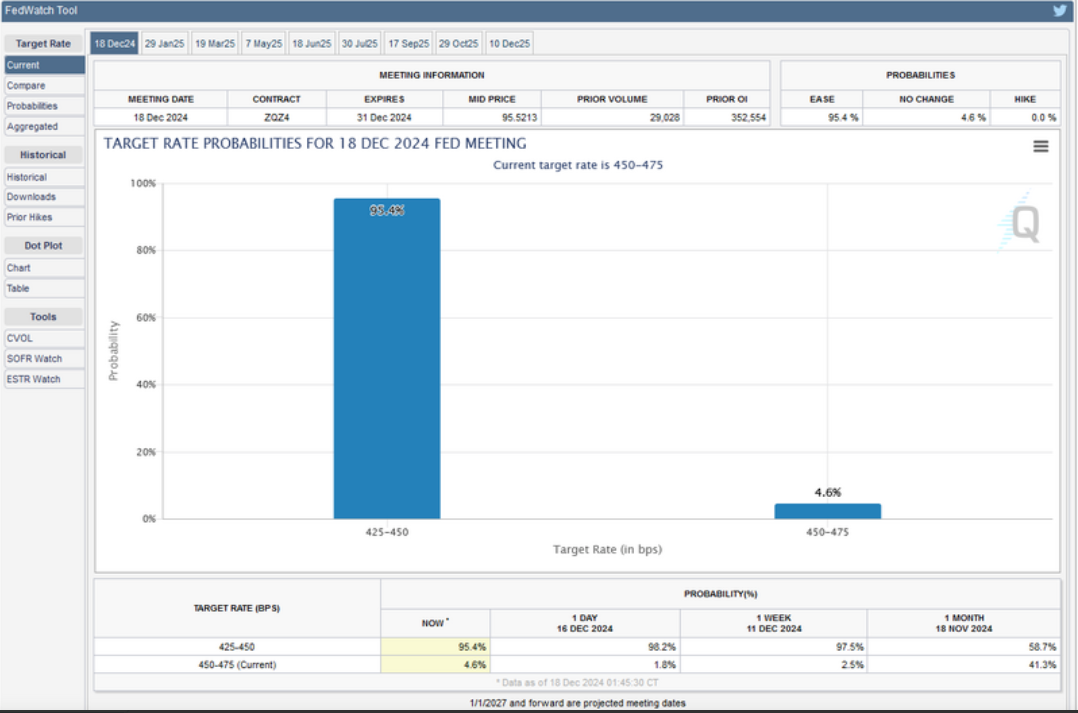

The FOMC meeting today is key as interest rate meetings tend to be from the US. However, today’s meeting is even more intriguing given all the noise and uncertainty moving forward.

The Fed is shifting its policies from being very restrictive to more balanced. Recent data has shown some stickiness in inflation and with President-elect Trump aiming to boost US economic growth, the Fed is likely to take a careful and slow approach to easing policies in 2025. This for now is where the focus will lie.

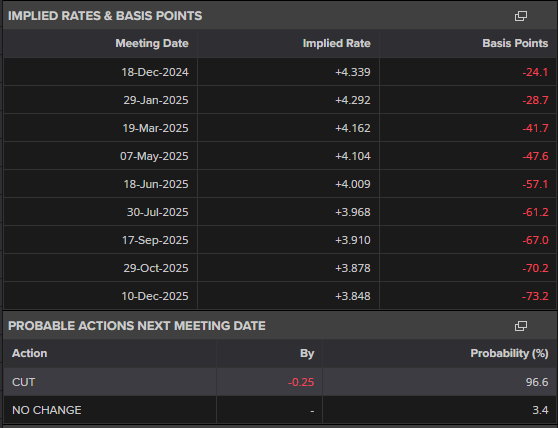

Heading into the meeting, markets are expecting around 73 bps of rate cuts through December 2025. This would include the proposed 25 bps cut today, meaning just 50 bps cuts in 2025.

Source: LSEG (click to enlarge)

What to Expect from the FOMC Meeting?

The main driver of late when it comes to US monetary policy decisions has been the US Labor market. The labor market is slowing down, with fewer new jobs, a drop in full-time employment, and a small rise in unemployment. These changes give the Fed a reason to move toward a more balanced policy approach.

Inflation which had been the main focus for the first 6-8 months of the year did take a backseat over the past few months. However recent data suggests that this may rear its ugly head once more in 2025.

Focus heading into the meeting will focus on updates to the Feds economic projections. In particular, the number of rate cuts we may expect in 2025. The consensus heading into the meeting is that President-elect Trump’s plans for stricter immigration controls, new tariffs, and cutting taxes for individuals and businesses are expected to lead the Fed to take a more cautious and slower approach to easing policies in 2025.

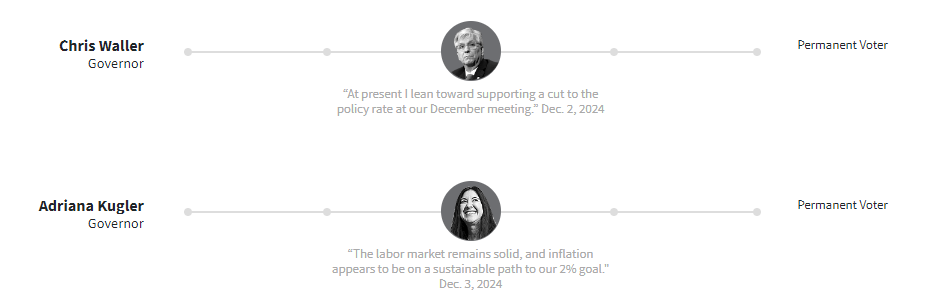

I do think that this is on point however, the rhetoric of the Fed will be important. Heading into the meeting we have heard a host of comments from Fed Policymakers who have supported more gradual easing in 2025.

FED Policymaker Comments in the Lead Up to December 18 Meeting:

Source: LSEG (click to enlarge)

Source: LSEG (click to enlarge)

The comments from policymakers definitely show a willingness for a slower rate cut path moving forward. In theory this should lead to some US Dollar strength as well as a rise in US Yields.

Having said that, I do expect a pause in January as the meeting will arrive just 9 or so days after President Elect Trump takes office. The March meeting should provide some time to gauge the effects of proposed Trump policy and might give markets a clearer picture for 2025.

Feds Reverse Repo Rate

The minutes from the last FOMC meeting made reference to a possible technical adjustment to the Fed’s reverse repo rate and this may be something to watch as well. The proposal is to lower the reverse repo rate by 5 basis points (bp), bringing it down to match the floor at 4.25%. At the same time, the Fed would also lower its whole interest rate range by 25 bp.

This means the new floor would drop to 4.25%, the ceiling would fall to 4.5%, and the reverse repo rate would shift to align with the new floor.

The other important rate, the interest on reserves (which is what the Fed pays banks for holding their extra money), would also go down by 25 bp, staying 15 bp above the floor as it is now.

One big takeaway here is that lowering the reverse repo rate would make the facility less appealing for banks to use. Eventually, as banks reduce their use of this facility, their reserves (money they hold at the Fed) could shrink.

Is such a move a positive or negative for the US Dollar?

In theory, if the reverse repo rate is lowered, as the Fed is considering, it reduces the interest banks and financial institutions earn when parking their cash with the Fed. This could make US interest rates slightly less attractive. With lower interest returns, some foreign investors might look for better opportunities in other countries with higher rates. If this happens, it could put mild downward pressure on the US Dollar’s strength.Something else to consider heading into the meeting, could such a move cancel out any US Dollar strength that may be gained should the Fed point to a slower rate cut path in 2025? Time will tell.

US Dollar Index

From a technical standpoint, the dollar is at crossroads as it is back around the multi-month key level at 107.00.

I do expect the US Dollar to maintain its dominance heading into 2025 especially if the Fed meet markets expectations regarding slower cuts in 2025.

This should keep the rate differential in play which has benefited the US Dollar since October.

As the Dollar has defied its seasonal trend by strengthening thus far in December, it would take a surprise later in the day to change the narrative. I do expect this narrative to persist until President trump takes office and begins enacting his policies.

US Dollar Index (DXY) Daily Chart, December 18, 2024

Source: TradingView.com (click to enlarge)

Support

- 106.50

- 106.00

- 105.63

Resistance

- 107.50

- 108.00

- 109.00

Forex Traders Await the Fed’s Decision

The Federal Reserve is set to announce its interest rate decision today at 21:00 GMT+2, with Fed Chair Jerome Powell holding a press conference 30 minutes later. According to Forex Factory, the market expects a rate cut to 4.25%-4.50% from the current 4.50%-4.75%.

Analysts at Apollo Global Management, in their Economic Outlook, predict:

→ In 2025, the Fed will continue lowering rates but at a slower pace than the market anticipates;

→ By the end of 2025, the rate is expected to settle at 4.0%.

In anticipation of today's decision, the currency markets are experiencing a period of calm.

The technical analysis of the EUR/USD chart shows that the pair consolidates between the upper boundary of a descending channel and the lower black support line, forming a narrowing triangle pattern (highlighted in purple).

Today's Fed meeting could trigger a surge in volatility, potentially driving sharp movements in USD pairs. For EUR/USD, opposite scenarios are possible:

→ An upward movement with a bullish breakout of the upper boundary of the long-term descending channel;

→ Continuation of the downtrend with a breakout below the lower black support line.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

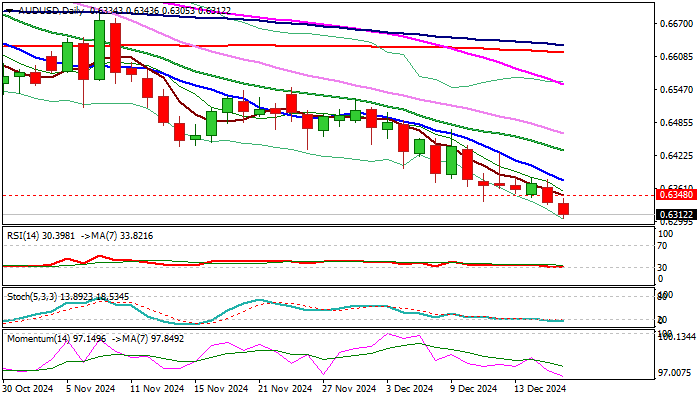

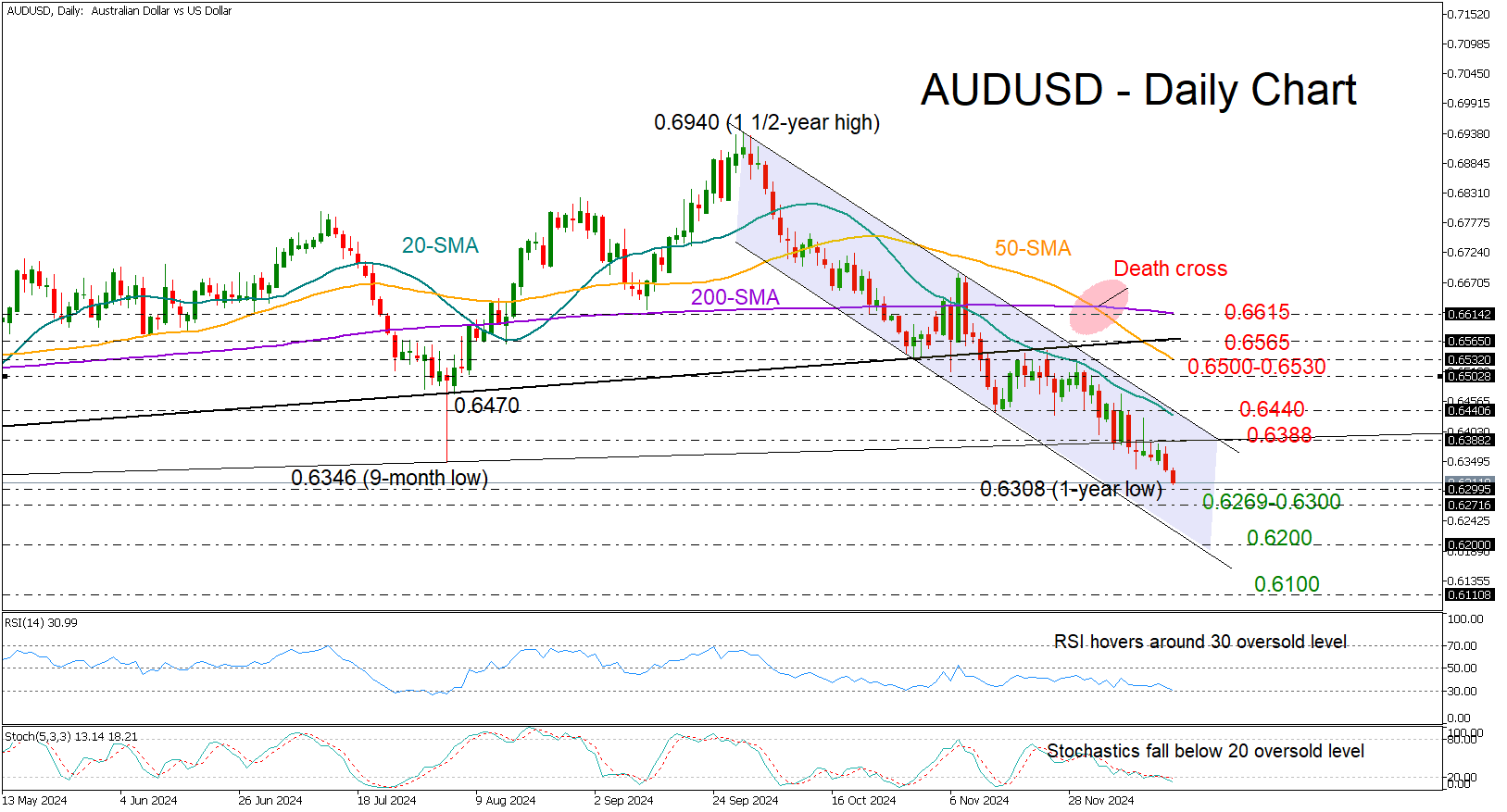

AUD/USD Outlook: Hits New 2024 Low Ahead of Widely Expected Fed’s Hawkish Cut

AUD/USD hit new 2024 low and trading near the lowest since Oct 2023 on Thursday, after strong bearish signal was generated on Tuesday’s close below former annual low (0.6348, Aug 5 spike low).

Aussie remains pressured from slower than expected growth of Chinese economy and falling commodity prices, with expectations for Fed’s hawkish cut today to add to negative outlook.

The US central bank is widely expected to cut interest rates by 25 basis points on today’s policy meeting, but markets anticipate that the Fed will significantly downgrade its projections for 2025 (probably to two rate cuts from initially planed four), due to elevated inflation and quite strong economy.

Also, signals that Trump’s administration will fully focus on boosting the US economy, require additional caution, as faster economic growth would fuel inflation and force the central bank to continue monitoring the situation and keep adjusting its policy view.

The pair is on track to register a sustained break of 0.6348 pivot that would open way for attack at 2023 low (0.6270) and probably unmask 2022 low (0.6170) on stronger bearish acceleration.

Firmly bearish daily studies (negative momentum is strengthening, MA’s in full bearish setup with converging 100/200DMA’s on track to form a Death cross) support the notion, with limited upticks on oversold conditions to mark positioning for fresh push higher.

Falling 10DMA (0.6377) should ideally cap, with extended upticks to stall under 0.6430/40 zone (falling 20DMA / former low of Nov 14) to keep larger bears intact.

Res: 0.6348; 0.6377; 0.6440; 0.6465.

Sup: 0.6300; 0.6270; 0.6100; 0.6170.

Gold Holds Steady as Investors Await Federal Reserve’s Rate Decision

Gold prices are hovering around 2,650 USD per troy ounce as investors remain cautious, conserving their energy for a potential move depending on the US Federal Reserve’s rate decision later tonight. The predominant market expectation is a 25-basis-point cut in interest rates, but there's significant uncertainty about the Fed’s monetary policy trajectory for 2025, which will be a key focus in today’s announcements.

Recent robust retail sales data from November, showing a 0.7% increase, have stirred discussions among investors that the Fed might decelerate its pace of rate cuts. This surge in retail sales is seen as a pro-inflationary factor, potentially influencing the Fed’s approach towards monetary easing.

A slowdown in rate reductions would likely be unfavourable for Gold, as lower interest rates generally decrease the opportunity cost of holding non-yielding assets like Gold, making it more attractive. Nonetheless, investors should wait for the Federal Reserve’s statement, which could diverge from current market speculations.

Since the start of the year, Gold has appreciated over 28%, potentially ending 2024 with the highest annual gain since 2010.

Technical analysis of XAU/USD

H4 Chart: Gold has established a consolidation range around the 2,675.55 level on the H4 chart. A growth structure has been formed up to 2726.27, and a corrective movement towards 2,635.00 is unfolding. Looking forward, a continuation of the growth wave towards 2743.85 is anticipated. The MACD indicator supports the bullish outlook, with its signal line below zero but pointed sharply upwards.

H1 Chart: On the H1 chart, Gold has completed a correction to 2,633.00 and is now expected to rise towards 2,680.00. After this increase, a potential decline to 2,658.00 may occur. Once this level is reached, a new growth phase towards 2705.70 will likely extend to 2,743.85. This scenario is corroborated by the Stochastic oscillator, whose signal line is currently above 50 and aiming towards 80, indicating upward momentum.

ECB’s Lane stresses agility in rate path amid elevated uncertainty

ECB Chief Economist Philip Lane highlighted the importance of maintaining "agility" in monetary policy decisions during a speech today. Lane emphasized that in the current environment of elevated uncertainty, ECB’s "prudent" approach will be guided by a meeting-by-meeting strategy without pre-committing to any specific rate path.

Lane outlined that the pace of monetary easing will depend on the balance of risks. If the inflation outlook or economic momentum experiences upside shocks, "monetary easing can proceed more slowly " compared to the December projections.

Conversely, in the case of downside shocks, the easing process could accelerate. He further noted that the rate path would also depend on ECB’s "ongoing assessment of underlying inflation dynamics and the strength of monetary policy transmission."

Eurozone CPI finalized at 2.2% in Nov, core at 2.7% yoy

Eurozone headline inflation for November was finalized at 2.2% yoy, up from October’s 2.0%. Meanwhile, Core CPI, which excludes food, alcohol, and tobacco, eased to 2.7% yoy, down from October’s 2.9%.

Services contributed the most to the Eurozone annual inflation rate, adding +1.74 percentage points, followed by food, alcohol, and tobacco (+0.53 pp) and non-energy industrial goods (+0.17 pp). Energy, on the other hand, detracted -0.19 percentage points, reflecting subdued demand and easing energy prices.

At the broader EU level, headline inflation was finalized at 2.5% yoy. Among member states, Ireland registered the lowest annual inflation at 0.5%, followed by Lithuania and Luxembourg (both at 1.1%). On the high end, Romania recorded the highest inflation at 5.4%, with Belgium (4.8%) and Croatia (4.0%) close behind. Compared to October, inflation fell in four EU member states, remained unchanged in three, and rose in twenty.

AUDUSD Bears Show No Mercy

- AUDUSD extends downtrend to a more-than-a-year low

- A pause is likely, but negative trend could stay in play

- FOMC policy announcement due at 19:00 GMT

AUDUSD is caught in a relentless downtrend, plunging to a 14-month low of 0.6308 on Wednesday following the close below the long-term support trendline from October 2022.

As global markets brace for the Federal Reserve’s final policy meeting of the year, speculation mounts over whether buying the dip could play out in the coming sessions as the price is flirting with the 2023 bottom region of 0.6269-0.6300.

The RSI and the stochastic oscillator are signaling that the sell-off is overstretched, though the indicators have yet to bottom out in the oversold region. Hence, the bears may keep the upper hand for now. If the 0.6200 area allows more declines, the door could open for the 0.6100 round mark and then for the 0.5980 zone taken from April 2020.

On the upside, a break above the falling channel and the 20-day simple moving average (SMA) near 0.6440 could be a major challenge for the bulls who first need to overcome the 0.6388 resistance. If they succeed, the pair could advance toward the 0.6500-0.6530 zone, where the 50-day SMA is located. Slightly higher, a former constraining line at 0.6565 could clear the way toward the 200-day SMA at 0.6615.

It's important to note that both the 50-day and 200-day SMAs have recently formed a death cross; a bearish signal that casts doubt on any immediate trend reversal.

In short, the bearish trend in AUDUSD is firmly in place, with the pair continuing to drift lower in the short term. While a recovery attempt could be possible near the 2023 low, selling interest could remain strong below the 0.6565 level. Hence, the outlook remains predominantly negative for now.

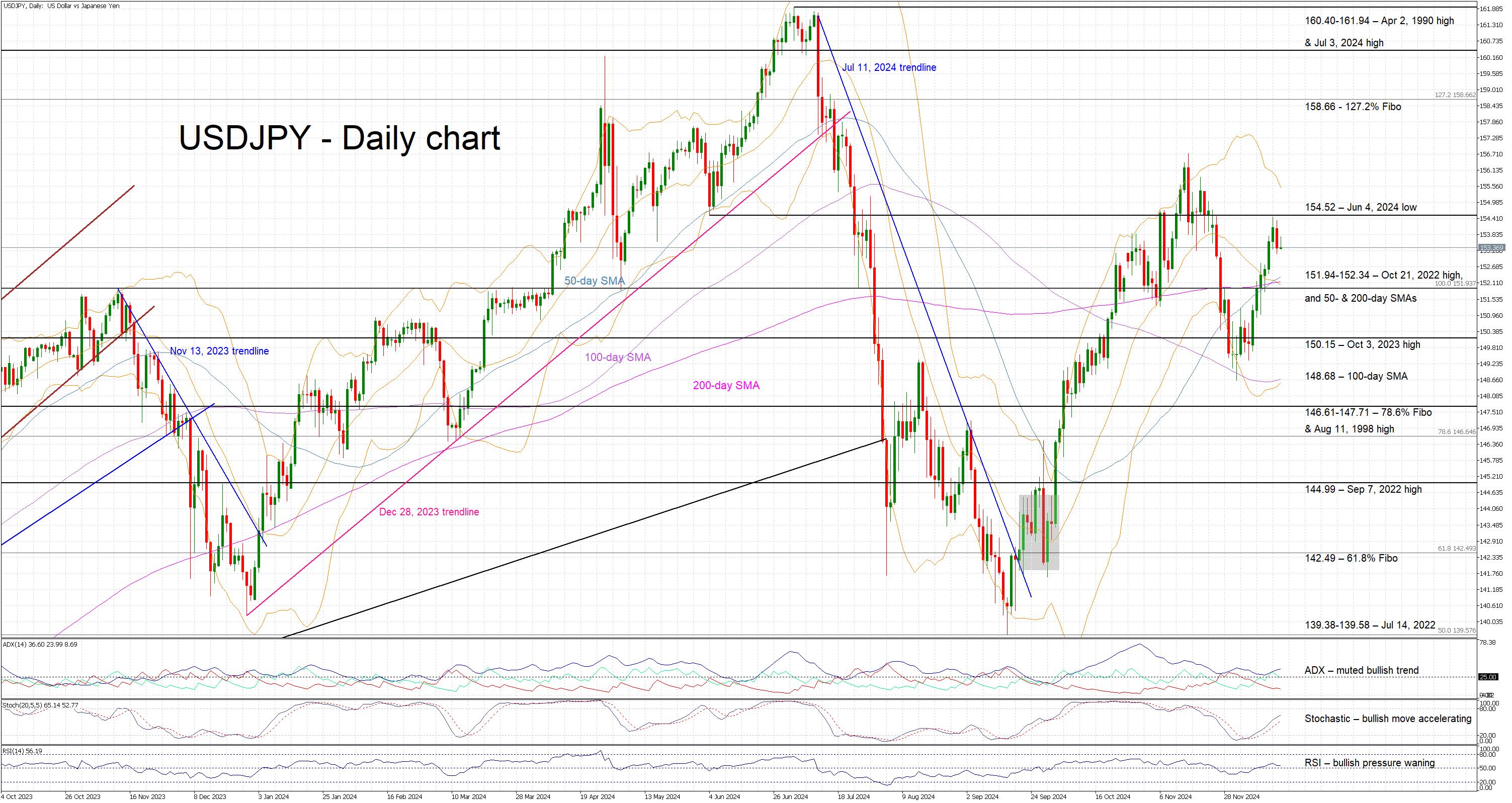

USDJPY Rally Pauses Ahead of Key Events

- USDJPY is trading sideways as the yen shows some signs of life

- Market participants are preparing for central bank meetings

- Momentum indicators are mostly bullish at this stage

USDJPY is trading sideways today, following Tuesday’s red candle, which was the first negative session for this pair after six consecutive green candles that pushed it towards the 154.52 level again. While the Fed is expected to cut rates by 25bps at today’s meeting, Trump’s imminent return to the White House and the gradually reduced probability of a BoJ rate hike have contributed to the continued underperformance of the yen.

Meanwhile, the momentum indicators are mostly bullish. Specifically, the RSI is hovering slightly above its midpoint, pointing to a weak bullish trend in USDJPY. Similarly, the Average Directional Movement Index (ADX) is edging higher, above its 25 threshold, and thus signaling a muted bullish trend in USDJPY. Interestingly, the stochastic oscillator is trading higher, above its moving average, and moving towards its overbought territory (OB). Should it return inside its OB area, it could be seen as a signal of strong bullish pressure in USDJPY.

Should the bulls remain hungry, they could try to push USDJPY above the June 4, 2024 low of 154.52, and then target a higher high above the November 15, 2024 high of 156.74. If successful, the door would then be open for a test of the 127.2% Fibonacci extension of the October 21, 2022 - January 16, 2023 downtrend at 158.66. Such a move would most likely attract the interest of Japanese government officials, causing another round of verbal interventions.

On the flip side, the bears are keen to recapture the market reins and push USDJPY lower, towards the busy 151.94-152.34 area. This region is populated by the October 21, 2022 high, and the 50- and 200-day simple moving averages (SMAs). A break below this zone would signal that the bearish move is gaining traction. The next key support areas are likely to be the October 3, 2023 high and the 100-day SMA, at the 150.15 and 148.68 levels respectively.

To sum up, USDJPY’s rally appears to have paused, with the two central banks meetings today and tomorrow potentially proving critical for the next USDJPY leg.

AUD/USD and NZD/USD Sink Further, Losses Mount

AUD/USD declined below the 0.6400 and 0.6375 support levels. NZD/USD is also moving lower and might extend losses below 0.57350.

Important Takeaways for AUD/USD and NZD/USD Analysis Today

- The Aussie Dollar started a fresh decline from well above the 0.6400 level against the US Dollar.

- There is a connecting bearish trend line forming with resistance at 0.6340 on the hourly chart of AUD/USD at FXOpen.

- NZD/USD declined steadily from the 0.5790 resistance zone.

- There is a short-term bearish trend line forming with resistance at 0.5750 on the hourly chart of NZD/USD at FXOpen.

AUD/USD Technical Analysis

On the hourly chart of AUD/USD at FXOpen, the pair struggled to clear the 0.6430 zone. The Aussie Dollar started a fresh decline below the 0.6400 support against the US Dollar, as discussed in the previous analysis.

The pair even settled below 0.6375 and the 50-hour simple moving average. There was a clear move below 0.6340. A low was formed at 0.6317 and the pair is now consolidating losses. On the upside, an immediate resistance is near the 0.6340 level.

There is also a connecting bearish trend line forming with resistance at 0.6340. It is close to the 23.6% Fib retracement level of the downward move from the 0.6429 swing high to the 0.6317 low.

The next major resistance is near the 0.6375 zone or the 50% Fib retracement level of the downward move from the 0.6429 swing high to the 0.6317 low, above which the price could rise toward 0.6385. Any more gains might send the pair toward the 0.6430 resistance.

A close above the 0.6430 level could start another steady increase in the near term. The next major resistance on the AUD/USD chart could be 0.6500.

On the downside, initial support is near the 0.6320 zone. The next support sits at 0.6350. If there is a downside break below 0.6350, the pair could extend its decline. The next support could be 0.6320. Any more losses might send the pair toward the 0.6300 support.

NZD/USD Technical Analysis

On the hourly chart of NZD/USD on FXOpen, the pair also followed a similar pattern and declined from the 0.5790 zone. The New Zealand Dollar gained bearish momentum and traded below 0.5765 against the US Dollar.

The pair settled below the 0.5755 level and the 50-hour simple moving average. Finally, it tested the 0.5735 zone and is currently consolidating losses.

Immediate resistance on the upside is near the 23.6% Fib retracement level of the downward move from the 0.5792 swing high to the 0.5736 low at 0.5750. There is also a short-term bearish trend line forming with resistance at 0.5750.

The next resistance is the 0.5765 level or the 50% Fib retracement level of the downward move from the 0.5792 swing high to the 0.5736 low. If there is a move above 0.5765, the pair could rise toward 0.5790.

Any more gains might open the doors for a move toward the 0.5810 resistance zone in the coming days. On the downside, immediate support on the NZD/USD chart is near the 0.5735 level.

The next major support is near the 0.5710 zone. If there is a downside break below 0.5710, the pair could extend its decline toward the 0.5665 level. The next key support is near 0.5640.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Elliott Wave Structure Pointing for Higher USD Today, But FEDs Decides

It’s finally Wednesday, likely the most important day of the week as we await the Fed’s decision. Expectations are for a 25-basis-point cut, but the real focus will be on the press conference and whether they deliver hawkish remarks. As you know, the US economic projections for next year are quite strong, so there may not be a need to cut rates in upcoming meetings, especially considering inflation remains well above their 2% target.

If the Fed sounds hawkish, we can expect the dollar to recover, and from an Elliott wave perspective, this seems likely after a strong rebound from 105.40, with move out of the corrective channel in five waves, so after some slowdown now ahead of the Fed, there’s a chance we’ll see continuation higher into a fifth wave. On the flip side, major currencies like the euro, Aussie, and Swiss franc could then drop.

What we should also watch closely are US yields and stocks. I think stocks could move lower, testing the downside of their recent ranges, especially the S&P 500, if Powell delivers a hawkish tone.