Sample Category Title

(FED) Federal Reserve Issues FOMC Statement

Recent indicators suggest that economic activity has continued to expand at a solid pace. Since earlier in the year, labor market conditions have generally eased, and the unemployment rate has moved up but remains low. Inflation has made progress toward the Committee's 2 percent objective but remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. The Committee judges that the risks to achieving its employment and inflation goals are roughly in balance. The economic outlook is uncertain, and the Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to lower the target range for the federal funds rate by 1/4 percentage point to 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee's goals. The Committee's assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Thomas I. Barkin; Michael S. Barr; Raphael W. Bostic; Michelle W. Bowman; Lisa D. Cook; Mary C. Daly; Philip N. Jefferson; Adriana D. Kugler; and Christopher J. Waller. Voting against the action was Beth M. Hammack, who preferred to maintain the target range for the federal funds rate at 4-1/2 to 4-3/4 percent.

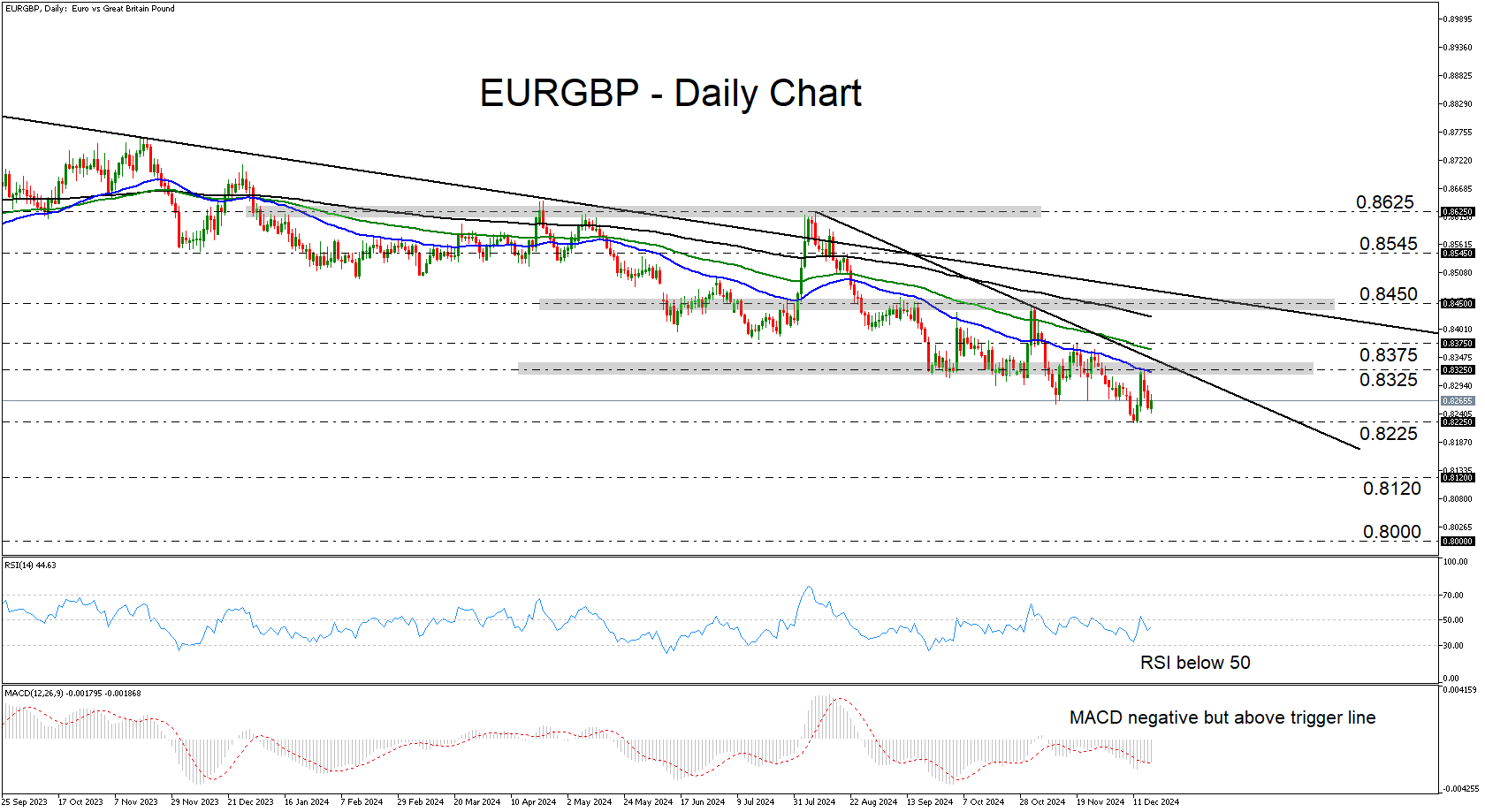

EURGBP Bears Remain in Control

- EURGBP retreats after hitting resistance at 0.8325

- Broader downtrend remains intact, but momentum weakens

- Break below 0.8225 could confirm trend continuation

- Rebound above 0.8450 may signal bullish trend reversal

EURGBP traded lower this week, after hitting resistance near the key territory of 0.8325. Overall, the pair is trading below all three of the plotted moving averages, below the near-term downward sloping line drawn from the high of August 8, and well below the longer-term downtrend line taken from the high of February 2, 2023.

This keeps the overall outlook negative, but the short-term oscillators suggest that there may be another bounce before the next leg south. The RSI, although below 50, has ticked up, while the MACD, despite hovering below zero, has bottomed and just poked its nose above its trigger line. Both indicators detect weakening bearish momentum.

If or when the bears decide to take charge again, a dip below 0.8225 may be needed for the prevailing downtrend to extend. Such a dip would confirm a lower low and may see scope for declines towards the 0.8120 zone, marked by the inside swing highs of April 2016. If the sellers do not stop there, the next line of defense may be the round figure of 0.8000.

On the upside, a break above the long-term downtrend line and the key resistance zone of 0.8450 may be needed to confirm a bullish trend reversal. In such a case, the bulls may feel confident to climb towards the 0.8545 area, or even higher, to the 0.8525 zone, marked by the high of August 8.

To sum up, EURGBP remains in a downtrend and a dip below the latest low of 0.8225 could take the price into territories last seen back in 2016.

UK Inflation Jumps to 8-mth High, Pound Shrugs

British pound is showing little movement on Wednesday. Early in the North American session, GBP/USD is trading at 1.2679, down 0.07% on the day.

UK inflation climbs to 2.6%

Inflation in the UK climbed to 2.6% in November, its highest level since March. The rise was driven by higher costs for petrol and food as well as an increase in the tobacco duty in the budget. Services inflation, which has been persistently high, was unchanged at 5%. The CPI reading was in line with the market estimate and the pound has showed almost no reaction. Monthly, CPI increased 0.1%, compared to 0.6% in October and also matching expectations.

Core inflation, which is considered a more reliable gauge of inflation trends, climbed to 3.5% y/y, up from 3.3% in October and just below the market estimate of 3.6%. This was the highest level since August. The acceleration in core inflation will be a source of concern for the Bank of England, as will be service inflation and Tuesday’s employment report which showed wage growth excluding bonuses rising to 5.2% from 4.4%.

The rise in inflation cements a pause from the BoE at Thursday’s rate meeting. The central bank has cut rates twice since June, bringing the cash rate to 4.75%. The BoE has largely contained inflation but will want to see evidence that inflation is moving towards the 2% target before delivering further rate cuts.

The BoE is widely expected to maintain the benchmark rate at 4.75% at Thursday’s rate meeting. The central bank lowered rates for a second time this year in November but will want to see inflation fall closer to the 2% target before resuming rate cuts.

The Federal Reserve makes its rate announcement later today. There isn’t much excitement around the decision, with the market pricing in a quarter-point cut at close to 100%. Investors will be interested in the updated economic and interest rate projections. President-elect Trump will take office in January which adds significant uncertainty for Fed policymakers.

GBP/USD Technical

- GBP/USD is testing support at 1.2703. Below, there is support at 1.2676

- 1.2739 and 1.2766 and the next resistance lines

Sunset Market Commentary

Markets

When (core) markets barely move the way they do today it’s because there’s little news or important events are looming. It’s both in this case. An empty economic calendar and the Fed policy meeting tonight resulted in technical and directionless trading in FI and FX markets. US yields swapped tiny gains of 1.5 bps for losses of 2 bps the moment first US investors joined the arena. German bunds marginally underperform Treasuries, rising up to 2.8 bps at the very long end of the curve. We did have UK inflation numbers for November featuring the agenda but they came too close to expectations to leave a mark. Headline inflation picked up to 2.6% as anticipated but core (3.5%) and services (5%) price pressures missed the mark by 0.1% ppt. The slight downside miss is not enough to offset sharper-than-expected wage growth in yesterday’s labour market report. If anything, UK money markets price in less rate cuts after this morning’s CPI outcome. Markets barely price in a cumulative 50 bps for 2025 - after tomorrow’s widely anticipated status quo. Gilts underperform peers for a second day. Yields add between 1.4 and 3.4 bps across the curve. Sterling quickly erased negligible kneejerk losses to trade unchanged around EUR/GBP 0.825. EUR/USD isn’t going anywhere either (+/- 1.05). The rest of the G10 FX landscape shows daily changes of less than 0.5%.

Jumping to tonight’s Fed decision now. A rate cut from 4.5-4.75% to 4.25-4.5% is all but certain. Markets have more or less fully discounted such a scenario since the lack of an upward CPI surprise last week. After three consecutive rate cuts (50-25-25) we expect the Fed to steer the market to a pause in January. Chair Powell last month referring the strong economy said there’s no hurry in lowering the policy rates. It also offers the Fed a moment to get a sense of president-elect Trump’s policy goals when entering the office on January 20. The updated dot plot will show fewer rate cuts for 2025 with three reductions instead of the current four the most plausible scenario. We think that the long-term estimate, a proxy for the neutral rate, will have shifted further north from 2.875% to 3%. It was already a close call in September. Since US money markets price in only 50 bps of cuts in 2025, we may see a kneejerk downleg in US (front-end) yields and the dollar after the dot plot release. It won’t stretch very far though if Powell strikes a generally hawkish tone in the presser afterwards by keeping the onus on the solid state of the economy. That should offer solid support to both yields and the dollar, the latter especially against an ongoing ailing euro. First meaningful support in EUR/USD is at 1.0335 (November correction low).

News & Views

The Confederation of British Industry (CBI) reported falling volumes in the final quarter of the year as growth expectations weakened further. The CBI’s quarterly Industrial Trends Survey showed manufacturing output volumes falling at the fastest pace since mid-2020 with manufacturers expecting another steep drop in Q1 2025. Total orders were the weakest since late 2020. Against a backdrop of weak demand, manufacturers’ stocks of finished goods remain relatively high at levels seen during the early stages of the Covid pandemic. CBI’s lead economist warned that “Manufacturers are facing a perfect storm of weakening external demand on the one hand, amid political instability in some key European markets and uncertainty over US trade policy. And on the other hand, domestic business confidence has collapsed in the wake of the Budget, which has increased costs and led to widespread reports of project cancellations and falling orders.” Meanwhile, expectations for selling price inflation picked up noticeably and is forecast to comfortably stick above the long-run average.

Polish consumer confidence improved slightly more than expected in December, from -17.1 to -16.7 (vs 17 consensus). Apart from last month, it’s still the weakest number of this year. Details showed biggest improvements in the current possibility of making important purchases and in the current economic situation of the country. The only decrease came on account of the evaluation of the current financial situation of households. The Polish zloty was unmoved by the numbers, sticking to the YTD highs around EUR/PLN 4.25. Tomorrow’s November wage and employment figures have more market moving potential.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0469; (P) 1.0501; (R1) 1.0524; More...

No change in EUR/USD's outlook as sideway trading continues in tight range. Intraday bias stays neutral at this point. Corrective pattern from 1.0330 might extend further. But outlook will stay bearish as long as 55 D EMA (now at 1.0668) holds. On the downside, below 1.0452 will bring retest of 1.0330 low.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2676; (P) 1.2703; (R1) 1.2739; More...

Sideway trading continues in GBP/USD and intraday bias stays neutral. On the downside, break of 1.2615 minor support will indicate that corrective recovery from 1.2486 has completed. Retest of this low should be seen next, and break will target 1.2298 cluster support zone. Nevertheless, break of 1.2810 will turn bias to upside for stronger rebound.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

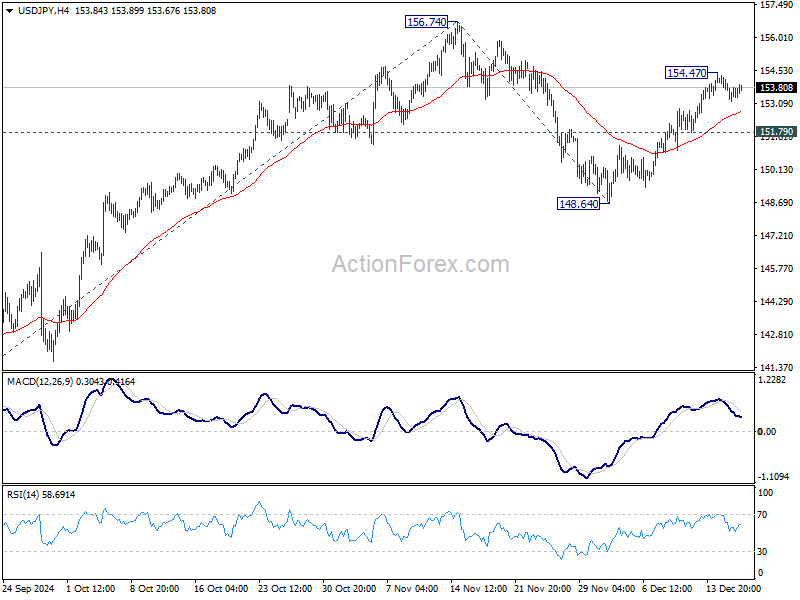

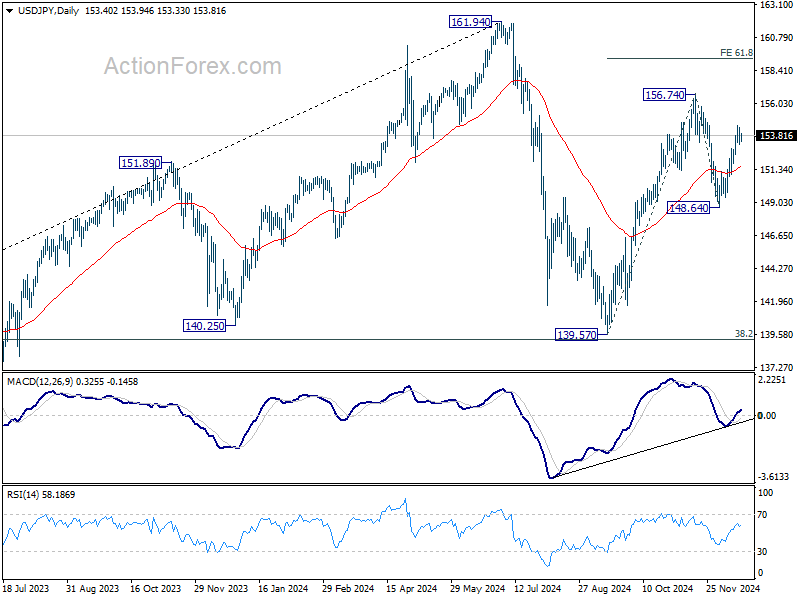

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 152.99; (P) 153.66; (R1) 154.17; More...

USD/JPY is staying in consolidations below 154.47 temporary top and intraday bias remains neutral. Further rally is expected as long as 151.79 minor support holds. Above 154.47 temporary top will target a retest on 156.74 high first. Firm break there will resume whole rally from 139.57, and target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next. However, break of 151.79 will turn bias back to the downside for 148.64 support instead.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

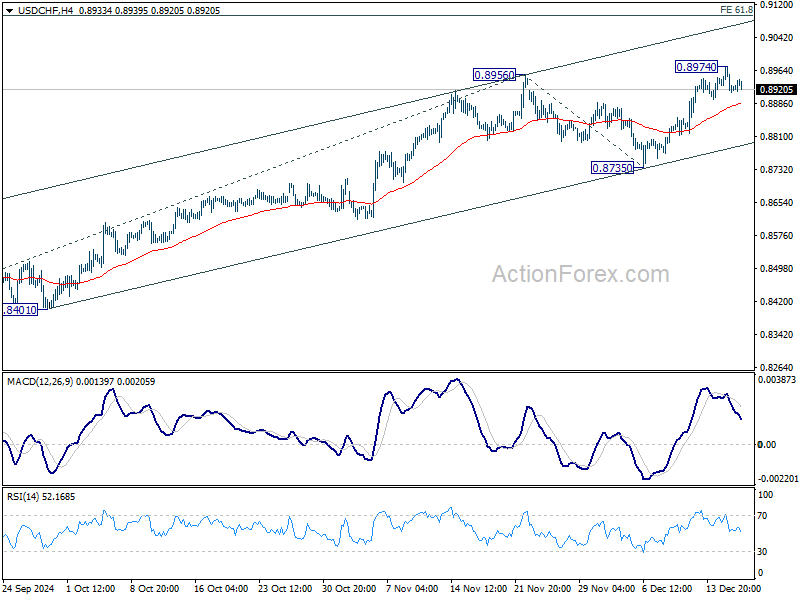

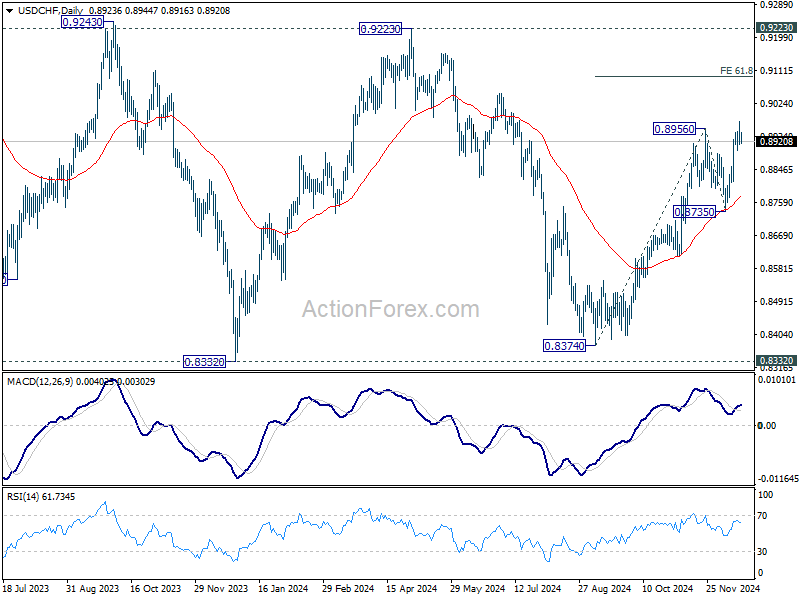

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8903; (P) 0.8939; (R1) 0.8963; More…

Intraday bias in USD/CHF remains neutral as consolidations continue below 0.8974 temporary top. While deeper pullback cannot be ruled out, outlook stay bullish as long as 0.8735 support holds. Break of 0.8974 will resume larger rise from 0.8374 to 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

Markets Hold Steady with Fed’s Rate Cut and 2025 Outlook in Focus

The forex and stock markets are holding steady today, with limited volatility as traders anticipate FOMC rate decision and updated economic projections. A 25bps rate cut, reducing the target range to 4.25–4.50%, is virtually certain. However, the market’s focus lies on the tone and guidance Fed delivers. Critical questions include whether a pause in easing could be on the table for January, the expected pace of rate cuts throughout 2025, and the revision of the neutral rate, which could indicate where Fed sees the terminal rate of the current cycle.

Tomorrow, attention will turn to BOJ and BoE, both expected to hold rates steady. For BoJ, markets are watching for any signs that further rate hikes could be planned for early 2025, particularly in January, amid ongoing efforts to manage inflation and normalize policy. Meanwhile, BoE's MPC voting split will be a key focus. Traders will look to the statement for policymakers’ views on recent data surprises and how the Autumn Budget is shaping their outlook, especially as inflation remains persistent in key sectors like services.

Technically, some attention could be in S&P 500's reaction to FOMC today. Recent up trend stalled after hitting 61.8% projection of 4103.78 to 5669.67 from 5119.26 at 6086.98. Selloff today could set up deeper correction to 55 D EMA (now at 5911.81) before resuming the up trend. On the other hand, clearing of 6086.98 will pave the way towards 100% projections at 6685.15 in early part of next year.

In Europe, at the time of writing, FTSE is up 0.21%. DAX is up 0.14%. CAC is up 0.26%. UK 10-year yield is up 0.0246 at 4.550. Germany 10-year yield is up 0.0118 at 2.245. Earlier in Asia, Nikkei fell -0.72%. Hong Kong HSI rose 0.83%. China Shanghai SSE rose 0.62%. Singapore Strait Times fell -0.53%. Japan 10-year JGB yield is down -09.0106 at 1.067.

ECB’s Lane stresses agility in rate path amid elevated uncertainty

ECB Chief Economist Philip Lane highlighted the importance of maintaining "agility" in monetary policy decisions during a speech today. Lane emphasized that in the current environment of elevated uncertainty, ECB’s "prudent" approach will be guided by a meeting-by-meeting strategy without pre-committing to any specific rate path.

Lane outlined that the pace of monetary easing will depend on the balance of risks. If the inflation outlook or economic momentum experiences upside shocks, "monetary easing can proceed more slowly " compared to the December projections.

Conversely, in the case of downside shocks, the easing process could accelerate. He further noted that the rate path would also depend on ECB’s "ongoing assessment of underlying inflation dynamics and the strength of monetary policy transmission."

Eurozone CPI finalized at 2.2% in Nov, core at 2.7% yoy

Eurozone headline inflation for November was finalized at 2.2% yoy, up from October’s 2.0%. Meanwhile, Core CPI, which excludes food, alcohol, and tobacco, eased to 2.7% yoy, down from October’s 2.9%.

Services contributed the most to the Eurozone annual inflation rate, adding +1.74 percentage points, followed by food, alcohol, and tobacco (+0.53 pp) and non-energy industrial goods (+0.17 pp). Energy, on the other hand, detracted -0.19 percentage points, reflecting subdued demand and easing energy prices.

At the broader EU level, headline inflation was finalized at 2.5% yoy. Among member states, Ireland registered the lowest annual inflation at 0.5%, followed by Lithuania and Luxembourg (both at 1.1%). On the high end, Romania recorded the highest inflation at 5.4%, with Belgium (4.8%) and Croatia (4.0%) close behind. Compared to October, inflation fell in four EU member states, remained unchanged in three, and rose in twenty.

UK CPI accelerates to 2.6% in Nov, core CPI up to 3.5%

UK CPI accelerated from 2.3% yoy to 2.6% yoy in November, matched expectations. Core CPI, (excluding energy, food, alcohol and tobacco), accelerated from 3.3% yoy to 3.5% yoy, below expectation of 3.6% yoy. CPI goods annual rate rose from -0.3% yoy to 0.4% yoy , while CPI services annual rate was unchanged at 5.0% yoy.

Japan's export rises 3.8% yoy in Nov, while import falls -3.8% yoy

Japan’s exports rose 3.8% yoy in November to JPY 9.152T, supported by increased shipments of chip-making equipment to Taiwan and nonferrous metals to China, marking the second consecutive month of export growth. Imports, however, fell -3.8% yoy to JPY 9.270T, marking their first decline in eight months due to reduced demand for crude oil from Saudi Arabia and electronics parts from Taiwan.

The overall trade deficit stood at JPY -117.6B, extending its red streak to five months. On a seasonally adjusted basis, the deficit widened to JPY -384B from JPY -229B in October, as imports increased 1.9% mom, outpacing the 0.2% mom rise in exports.

Trade with key partners highlighted persistent imbalances. Japan recorded a JPY 664.03B trade surplus with the US, despite exports falling -8.0% yoy, while imports dipped slightly by -0.6% yoy.

Conversely, its trade deficit with China expanded to JPY 682B, as exports grew 4.1% yoy, and imports rose 4.2% yoy.

The trade gap with the EUR remained significant at JPY 210.19B, with exports plunging -12.5% yoy, while imports decreased -5.4% yoy.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8903; (P) 0.8939; (R1) 0.8963; More…

Intraday bias in USD/CHF remains neutral as consolidations continue below 0.8974 temporary top. While deeper pullback cannot be ruled out, outlook stay bullish as long as 0.8735 support holds. Break of 0.8974 will resume larger rise from 0.8374 to 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.

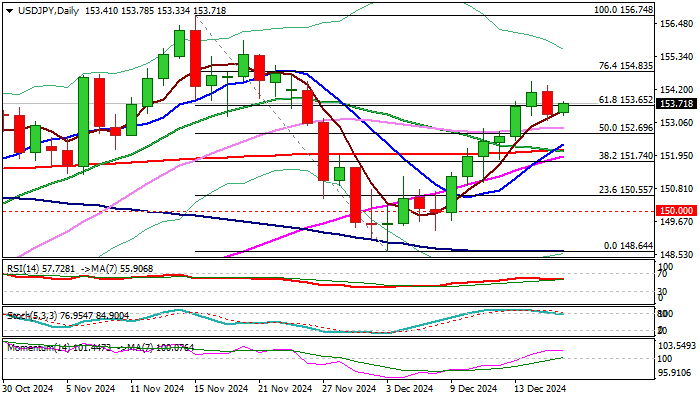

USD/JPY Outlook: Dollar Remains Well Supported by Wide Gap Between Fed and BoJ Monetary Policies

USDJPY remains steady, though at narrower range on Wednesday, awaiting the FOMC verdict later today.

Tuesday’s dip from new three-week high, which interrupted a six-day rally, is likely to be short-lived, as the dollar remains well supported and yen under pressure on wide gap between Fed and BoJ monetary policies.

Fed is expected to deliver a 25 basis points rate cut today, in an action that many see as hawkish cut due expected slowdown in policy easing in 2025, against previous estimations, while Japan’s policymakers will meet on Thursday and widely expected to keep interest rate unchanged.

Bullish technical picture on daily chart adds positive outlook for the dollar (the action remains underpinned by rising thick daily Ichimoku cloud, MA’s create multiple bull-crosses and momentum is positive).

Firm break of cracked Fibo barrier at 153.65 (61.8% retracement of 156.74/148.64 pullback) to generate fresh bullish signal for acceleration towards 154.83 (Fibo 76.4%) and 156.74 (Nov 15 peak) in extension.

Res: 154.47; 154.83; 155.88; 156.74.

Sup: 153.16; 152.87; 152.69; 152.30.