Sample Category Title

Sterling and Yen Underperform After BoE and BoJ

Both Sterling and Japanese yen are among the weakest-performing currencies today, following their respective central banks meetings. BoE left rates unchanged at 4.75%, but the surprise came from a dovish shift in the MPC, with three members voting for a cut. While BoE reiterated that a "gradual approach" to easing remains appropriate, rising concerns over economic stagnation suggest the Committee may be ready to expedite rate cuts once the full impact of the Autumn Budget and potential US trade policies becomes clear.

Yen fared even worse after BoJ maintained its policy stance without offering any signals on the timing of future rate hikes. Governor Kazuo Ueda highlighted external risks, particularly stemming from US trade policies, which he described as a significant source of uncertainty for global and Japanese economies. Ueda stressed the need to carefully evaluate the impact of these risks on Japan’s economic outlook before moving on with policy normalizations.

As for the week so far, Dollar remains the runaway leader, supported by Fed’s hawkish guidance, including slower pace of easing in 2025 and the prospect of a higher terminal rate. Despite today’s pullback, Sterling remains the second-strongest performer, while Swiss franc holds third place.

At the weaker end, Yen continues to struggle, weighed down further by rising US Treasury yields. New Zealand dollar is the second worst, pressured by weak GDP data that has fueled speculation of a lower terminal rate in RBNZ’s easing cycle. Australian Dollar follows, with Euro and Canadian Dollar mixed in the middle of the pack.

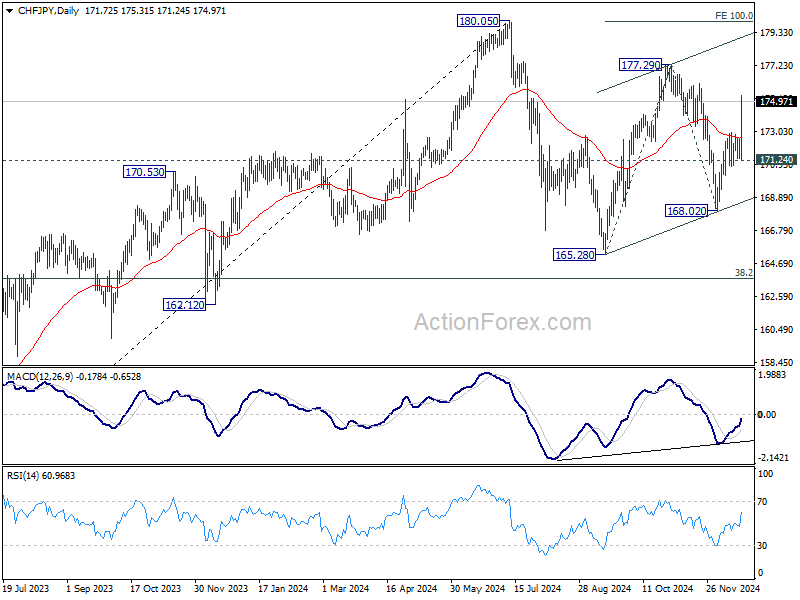

Technically, CHF/JPY's outlook is cleared alongside many Yen crosses with the strong rally, and firm break of 55 D EMA today. Corrective pattern from 165.28 is still extending with rise from 168.02 as the third leg. Further rally is expected as long as 171.24 support holds. Next target is 177.29 and break there will target 100% projection of 165.28 to 177.29 from 168.02 at 180.03, which is close to 180.05 high.

In Europe, at the time of writing, FTSE is down -1.02%. DAX is down -0.99%. CAC is down -1.14%. UK 10-year yield is up 0.024 at 4.587. Germany 10-year yield is up 0.0580 at 2.305. Earlier in Asia, Nikkei fell -0.69%. Hong Kong HSI fell -0.56%. China Shanghai SSE fell -0.36%. Singapore Strait Times fell -0.44%. Japan 10-year JGB yield rose 0.0194 to 1.086.

US initial jobless claims fall back to 220k

US initial jobless claims fell -22k to 220k in the week ending December 14, below expectation of 240k. Four-week moving average of initial claims rose 1k to 224k.

Continuing claims fell -5k to 1874k in the week ending December 7. Four-week moving average of continuing claims fell -6k to 1880k.

BoE stands pat with dovish 6-3 vote

BoE held its Bank Rate steady at 4.75%, in line with expectations, but the vote leaned more dovish than before. Three MPC members—Swati Dhingra, Dave Ramsden, and Alan Taylor—voted for a rate cut.

BoE reaffirmed that a “gradual approach to removing monetary policy restraint remains appropriate” and emphasized the need to maintain restrictive policy “for sufficiently long” to ensure inflation sustainably returns to 2% target. Decisions on the degree of restrictiveness will be made on a meeting-by-meeting basi.

The statement acknowledged that headline CPI inflation rose to 2.6% in November, slightly above prior expectations, while services inflation remained persistently high. Inflation is expected to rise slightly in the near term.

Meanwhile, indicators of near-term activity have weakened, and staff now expect GDP growth to fall short of projections from the November Monetary Policy Report, although the labor market is seen as broadly balanced.

BoE also flagged uncertainties arising from global inflationary shocks, geopolitical risks, trade policy developments, and measures in the Autumn Budget, all of which could impact growth and inflation.

German Gfk consumer sentiment improves slightly but remains fragile

Germany’s GfK Consumer Sentiment Index for January rose to -21.3, improving from December’s -23.1.

December’s subindices reflected mixed dynamics: economic expectations moved into positive territory at 0.3, up from -3.6, and income expectations increased to 1.4 from -3.5. Willingness to buy also ticked higher to -5.4 from -6.0, while willingness to save fell sharply to 5.9 from 11.9.

According to Rolf Bürkl, consumer expert at NIM, the improvement comes after a steep decline the prior month, partially reversing earlier losses. However, Bürkl noted that at -21.3 points, consumer sentiment remains at a very low level, highlighting a trend of "stagnation since mid-2024."

He warned that a sustained recovery is "not yet in sight" due to persistent challenges. High food and energy prices, alongside growing concerns about job security in key sectors, continue to weigh heavily on sentiment.

BoJ stand pat, highlights wage and global risks

BoJ kept its uncollateralized overnight call rate unchanged at 0.25%, as widely anticipated, with an 8-1 vote in favor. Naoki Tamura dissented, advocating for a rate increase to 0.50%.

Governor Kazuo Ueda, speaking at the post-meeting press conference, reiterated that rate hikes would proceed cautiously. He noted, "If the economy and prices move in line with our forecast, we will continue to raise our policy rate," but emphasized the need to carefully assess data before adjusting the level of monetary support.

The gradual pace of tightening, he explained, is due to the "moderate" rise in underlying inflation, which lacks the strength to warrant aggressive moves.

Ueda highlighted the importance of monitoring wage dynamics, particularly in the context of next year’s wage negotiations, to gauge the strength of Japan’s wage-inflation cycle.

He also pointed to uncertainties in the global economic outlook and the impacts of policy decisions under the incoming U.S. administration, despite the overall resilience of the US economy.

New Zealand's GDP contracts -1% qoq in Q3, broad economic weakness

New Zealand’s economy contracted by -1.0% qoq in Q3, significantly worse than market expectations of -0.2%. The previous quarter’s GDP figure was also revised down sharply, from -0.2% to -1.1%, painting a grimmer picture of the country’s economic performance.

The decline was broad-based, with activity falling in 11 out of 16 industries, including significant contractions in manufacturing, business services, and construction. While primary industries posted gains, both goods-producing and service industries experienced declines.

On a per capita basis, GDP dropped -1.2% qoq, marking the eighth consecutive quarterly decline. The expenditure measure of GDP also contracted by -0.8% qoq. Notably, household consumption expenditure decreased by -0.3% qoq, with reductions in spending on essentials such as grocery food and electricity, highlighting the strain on consumer budgets.

NZ ANZ business confidence falls to 62.3, demand recovery offers glimmers of hope

New Zealand’s ANZ Business Confidence Index fell to 62.3 in December, down from 64.9. However, some subindices showed encouraging signs of recovery. The own activity outlook improved to 50.3 from 48.0, while profit expectations rose significantly to 31.1 from 26.5. Investment intentions also jumped to 21.5 from 18.0, signaling increased business willingness to allocate resources despite a challenging environment.

However, labor market metrics were mixed, with employment intentions slipping slightly from 14.7 to 14.3. At the same time, cost pressures intensified sharply, as cost expectations surged to 70.1 from 62.9, and wage expectations jumped from 75.5 to 79.2. Price intentions remained steady at 42.7, slightly up from 42.2, while inflation expectations ticked higher to 2.63%, up from 2.53%, reflecting ongoing pricing pressures.

ANZ noted that while the survey results indicate signs of recovering demand, they come against the backdrop of this morning’s weak Q3 GDP figures, which showed a sharp contraction. The low bar set by the GDP downturn provides room for optimism if demand continues to improve. However, rising cost and wage pressures could complicate the outlook, especially for inflation management.

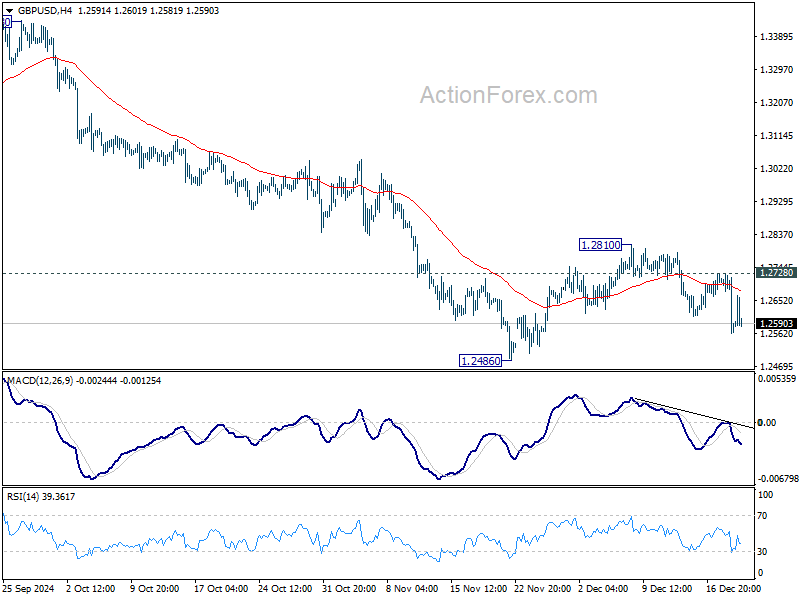

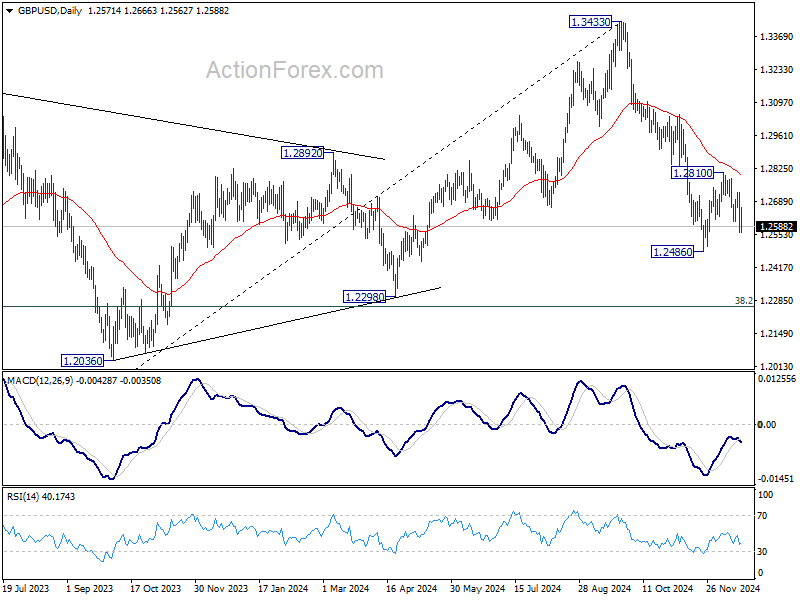

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2513; (P) 1.2621; (R1) 1.2679; More...

Intraday bias in GBP/USD remains on the downside despite some volatility during today. Recovery from 1.2486 should have completed at 1.2810. Retest of 1.2486 should be seen next. Firm break there will resume the fall from 1.3433 and target 1.2298 cluster support zone. Nevertheless, break of 1.2728 minor resistance will turn bias to the upside for 1.2810 and above instead.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

US initial jobless claims fall back to 220k

US initial jobless claims fell -22k to 220k in the week ending December 14, below expectation of 240k. Four-week moving average of initial claims rose 1k to 224k.

Continuing claims fell -5k to 1874k in the week ending December 7. Four-week moving average of continuing claims fell -6k to 1880k.

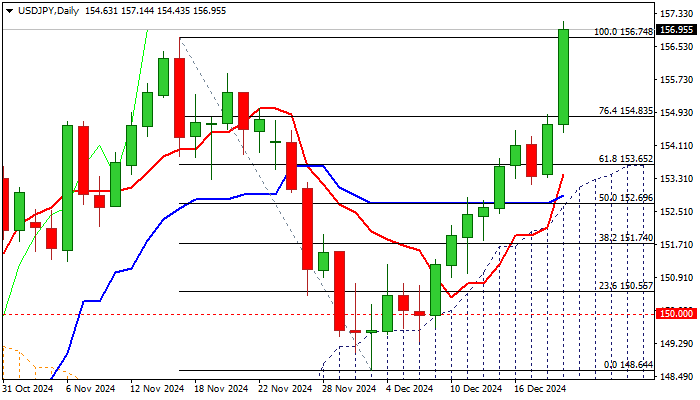

USD/JPY Putlook: Surges After Fed and BoJ Policy Decisions

USDJPY spiked to new multi-month high on Thursday, after Bank of Japan kept interest rates unchanged in today’s policy meeting, adding to positive signals for dollar from Fed’s hawkish rate cut on Wednesday.

Although BoJ’s decision did not surprise (markets widely expected unchanged rates at 0.15%) the central bank pointed to cautious approach to the monetary policy in the near future, in light of implications of policies of incoming Trump’s administration and also more careful asses the incoming economic data.

Dovish BoJ and persisting gap between monetary policies of two central banks added pressure on yen and created more favorable conditions for the US dollar.

Fresh bulls cracked former top at 156.74 (Nov 15), signaling an end of corrective phase and likely continuation of an uptrend from 139.57 (2024 low, posted on Sep 16).

Sustained break of 156.74 barrier is needed to confirm signal and open way for further gains, with 157.86 (July 16 high) to come in focus.

On the other hand, daily studies are overbought and warn that fresh bulls may take a breather after strong rally, but the dollar is expected to remain well supported, with limited dips seen as positioning for fresh push higher.

Res: 157.14; 158.00; 158.66; 159.00.

Sup: 155.88; 154.72; 154.43; 153.41.

New Zealand Dollar Plunges After Hawkish Fed

The New Zealand dollar had a miserable Wednesday, plummeting 2.3%. NZD/USD has reversed directions Thursday and is trading at 0.5659 in the European session, up 0.66% on the day at the time of writing. The New Zealand dollar has been on a sharp descent, falling 10.8% since Oct. 1.

US dollar soars after Fed rate cut

There was no surprise as the Federal Reserve delivered a 25-basis point rate cut on Wednesday, the final rate announcement of the year. The market had priced in the move at close to 100% as the Fed did a good job of telegraphing its plans ahead of the decision. The move was near-unanimous, with 11 members voting for the 25 bp cut, with one member voted to maintain rates.

What caught the market off guard was the Fed’s rate cut projection for 2025. The Fed downwardly revised its forecast to two rate cuts, down from four rate cuts in the September forecast. The Fed’s signal that the pace of rate cuts will be very slow in 2025 sent the US dollar soaring against all the major currencies, while US equity markets took a tumble. The New Zealand dollar slipped 1.7% in the aftermath of the rate cut and fell 2.9% on the day.

Fed Chair Powell had a mixed message at his press conference after the meeting. Powell said he was “very optimistic” about the strength of the US economy and that the Fed was moving closer to ending the current rate-cutting cycle. Powell was less rosy about the inflation picture, saying that, “We have been moving sideways of 12-month inflation”. The Fed has largely contained inflation, but the downswing in has stalled and inflation remains above the 2% target.

New Zealand GDP declines more than expected

New Zealand GDP for the third quarter was a disappointment, coming in at -1.0%. This follows a 1.1% decline in Q2, which was revised sharply lower from -0.2%, and well below the market estimate of -0.4%. This marks back-to-back quarters of negative growth, which points to a technical recession. Annually, the economy shrunk by 1.5%, much weaker than the Q2 reading of -0.5% and the market estimate of -0.4%.

The weak GDP data, along with the hawkish Fed rate cut, helped push the New Zealand dollar sharply lower on Wednesday. The Reserve Bank of New Zealand is under pressure to slash rates by 50 or even 75 basis points at the February meeting in order to kick-start the languishing economy.

NZD/USD Technical

- NZD/USD is putting pressure on resistance at 0.5668 and 05717

- There is support at 0.5575 and 0.5526

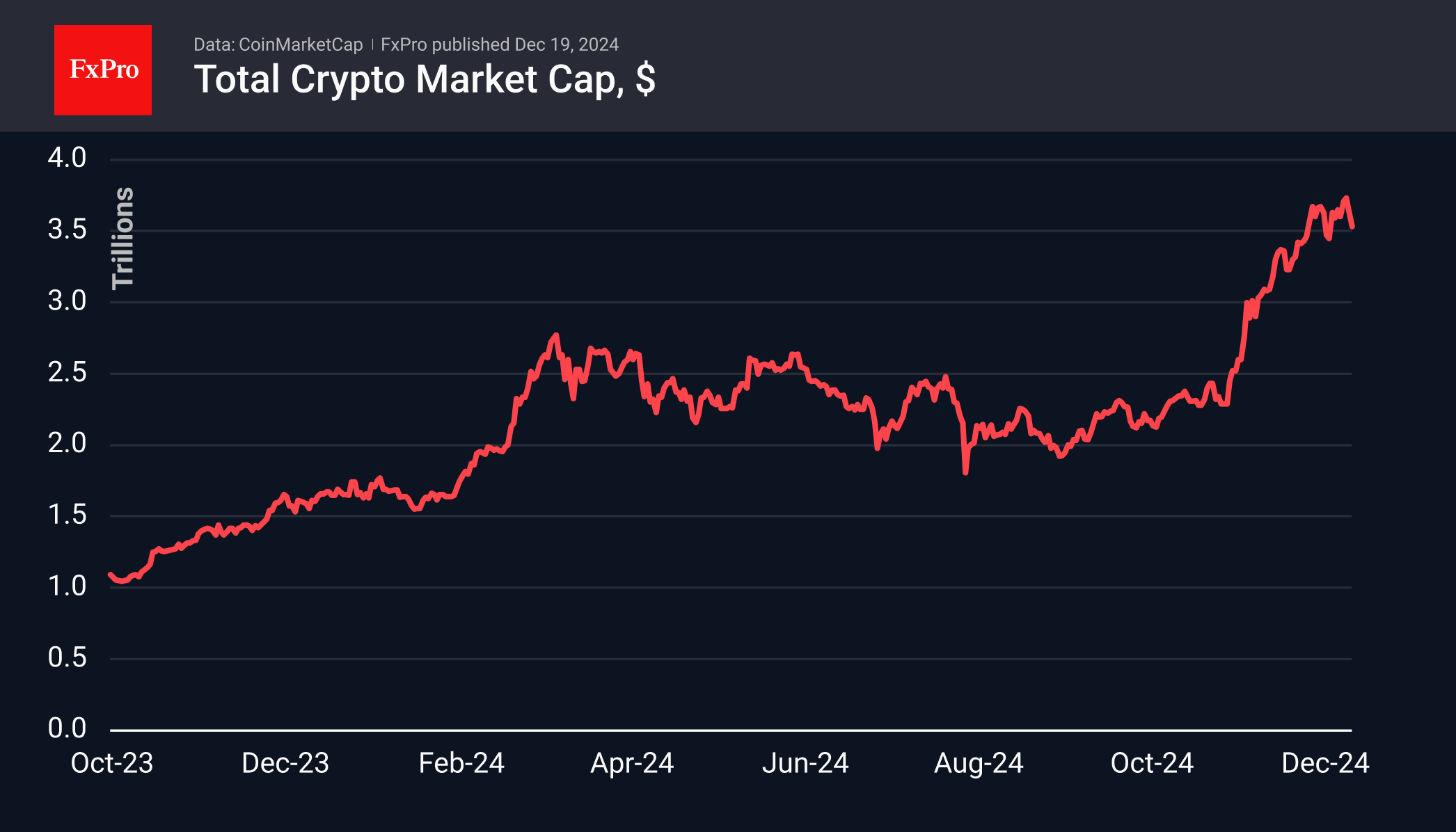

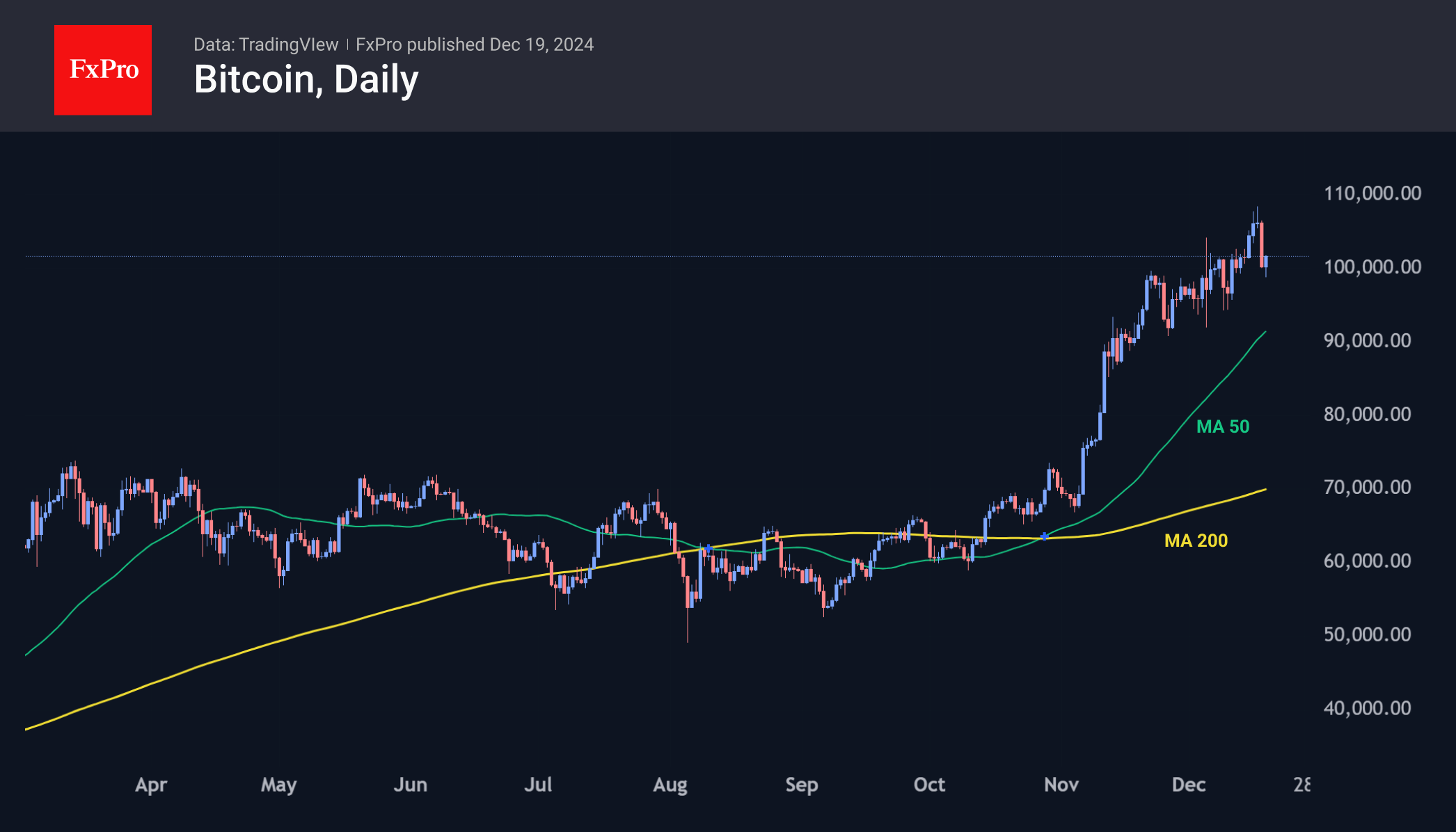

Bitcoin Tests $100K Again

Market picture

The cryptocurrency market lost 3% in 24 hours amid a sell-off in financial markets following comments from the Federal Reserve. Capitalisation fell to $3.51 trillion, and at the low it dipped below $3.48 trillion – its lowest in more than a week. The Cryptocurrency Fear and Greed Index fell to 75, also hitting lows since 11 December.

Bitcoin is once again testing the $100,000 level, this time making attempts to dip below that round level. While the magnitude of bitcoin’s decline is comparable to that of stocks, it is seen as a show of strength, as bitcoin often loses more. Over the past five and a half weeks, an upward trend has formed, and Bitcoin has fallen sharply from the upper to the lower boundary, where it seemingly attracts some interest. A trend breakdown can only be confirmed with a break of the 50-day moving average, which is now through $91,700 but heading to $94,000 by the end of the week.

Bitcoin is testing the $100,000 level amid a sell-off in financial markets. The cryptocurrency market has lost 3% in 24 hours, dropping to $3.51 trillion in capitalisation. The Cryptocurrency Fear and Greed Index fell to a low of 75.

News Background

Bitcoin’s parabolic growth phase is just around the corner, a Rekt Capital analyst believes. Historically, such periods last about 300 days, and so far 41 days have passed.

19% of Americans have used, traded or have an interest in cryptocurrencies, an Emerson College national survey for December showed. About 26% of men and 13% of women said they have interacted with digital assets.

The state of Ohio has entered the bitcoin reserve race. A bill to create one has been submitted to the state House of Representatives for consideration.

According to CoinDesk, the chairmen of the Senate Banking Committee and the US House Financial Services Committee, Tim Scott and French Hill, will focus on considering cryptocurrency-related bills in 2025.

Deutsche Bank will launch a layer 2 (L2) solution for Ethereum powered by ZKsync to improve efficiency and make transactions cheaper.

The Australian Securities and Investments Commission (ASIC) has accused Binance of breaching consumer rights by trading risky derivatives, resulting in large losses.

BoE stands pat with dovish 6-3 vote

BoE held its Bank Rate steady at 4.75%, in line with expectations, but the vote leaned more dovish than before. Three MPC members—Swati Dhingra, Dave Ramsden, and Alan Taylor—voted for a rate cut.

BoE reaffirmed that a “gradual approach to removing monetary policy restraint remains appropriate” and emphasized the need to maintain restrictive policy “for sufficiently long” to ensure inflation sustainably returns to 2% target. Decisions on the degree of restrictiveness will be made on a meeting-by-meeting basi.

The statement acknowledged that headline CPI inflation rose to 2.6% in November, slightly above prior expectations, while services inflation remained persistently high. Inflation is expected to rise slightly in the near term.

Meanwhile, indicators of near-term activity have weakened, and staff now expect GDP growth to fall short of projections from the November Monetary Policy Report, although the labor market is seen as broadly balanced.

BoE also flagged uncertainties arising from global inflationary shocks, geopolitical risks, trade policy developments, and measures in the Autumn Budget, all of which could impact growth and inflation.

(BOE) Bank Rate maintained at 4.75%

Monetary Policy Summary, December 2024

The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

At its meeting ending on 18 December 2024, the MPC voted by a majority of 6–3 to maintain Bank Rate at 4.75%. Three members preferred to reduce Bank Rate by 0.25 percentage points, to 4.5%.

Since the MPC’s previous meeting, twelve-month CPI inflation has increased to 2.6% in November from 1.7% in September. This was slightly higher than previous expectations, owing in large part to stronger inflation in core goods and food. Services consumer price inflation has remained elevated. Headline CPI inflation is expected to continue to rise slightly in the near term. Although household inflation expectations have largely normalised, some indicators have increased recently.

Most indicators of UK near-term activity have declined. Bank staff expect GDP growth to have been weaker at the end of the year than projected in the November Monetary Policy Report. The Committee now judges that the labour market is broadly in balance. Annual private sector regular average weekly earnings growth picked up quite sharply in the three months to October, but has tended to be more volatile than other wage indicators. The latest Agents’ intelligence suggests that average pay settlements in 2025 will be within a range of 3 to 4%. There remains significant uncertainty around developments in the labour market.

Monetary policy has been guided by the need to squeeze remaining inflationary pressures out of the economy to achieve the 2% target both in a timely manner and on a lasting basis. Over recent quarters there has been progress in disinflation, particularly as previous external shocks have abated, although remaining domestic inflationary pressures are resolving more slowly.

The Committee continues to consider a range of cases for how the past global shocks that drove up inflation may unwind, and therefore how persistent domestic inflationary pressures may be. The MPC is also monitoring the impact on growth and inflationary pressures from the measures announced in the Autumn Budget, and from geopolitical tensions and trade policy uncertainty. These developments have generated additional uncertainties around the economic outlook.

At this meeting, the Committee voted to maintain Bank Rate at 4.75%.

The Committee continues to monitor closely the risks of inflation persistence and will assess the extent to which the evolving evidence is consistent with more constrained supply, which could sustain inflationary pressures, or with weaker demand, which could lead to the emergence of spare capacity in the economy and push down inflation. A gradual approach to removing monetary policy restraint remains appropriate. Monetary policy will need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term have dissipated further. The Committee will decide the appropriate degree of monetary policy restrictiveness at each meeting.

Minutes of the Monetary Policy Committee meeting ending on 18 December 2024

1: Before turning to its immediate policy decision, the Committee discussed: the international economy; monetary and financial conditions; demand and output; and supply, costs and prices.

The international economy

2: UK-weighted global GDP was estimated to have grown by 0.5% in 2024 Q3, marginally higher than the projection in the November Monetary Policy Report. On balance, the risks around the near-term outlook for activity in a number of advanced economies remained to the downside. Euro-area GDP had grown by 0.4% in the third quarter, higher than the November Report projections and supported by household consumption. Growth was expected to slow in Q4, however, in line with weakness in the output PMIs, particularly in France and Germany. US GDP had increased by 0.7% in Q3, in line with the November Report projections, and was expected to cool slightly in Q4. In China, GDP had grown by 0.9% in Q3, a rebound from Q2, owing to stronger exports. Growth was expected to recover further, partly supported by additional policy stimulus.

3: The euro-area labour market had remained tight but had continued to normalise, while the labour market in the United States had remained close to balance. Unemployment in these regions remained at or near historical lows. Indicators of pay growth had generally cooled in the euro area, albeit with an increase in negotiated wage growth in 2024 Q3 that was attributable largely to one-off payments in Germany. Recent indicators of wage growth in the United States had been mixed.

4: Headline consumer price inflation in advanced economies had increased slightly, close to market expectations. In the euro area, twelve-month HICP inflation had increased to 2.2% in November, accounted for largely by an energy-related base effect, while core inflation had remained unchanged at 2.7%. In the United States, PCE inflation had risen slightly to 2.3% in October, while core PCE inflation had also increased slightly to 2.8%. These increases had been accounted for partly by core services excluding housing.

5: Since the MPC’s November meeting, European wholesale gas prices had initially increased sharply, owing to colder weather, strong demand from Asia and disruption in the provision of Russian-owned gas supplies. These price increases had largely reversed by the time of the MPC’s December decision.

6: The Committee discussed risks to global growth and inflation stemming from geopolitical tensions and trade policy uncertainty, with indicators of the latter having increased materially. The incoming US administration had proposed to increase tariffs in a manner that could influence future global trade if applied and, as a result, have some direct and indirect impacts on the UK economy. The magnitude and direction of any such impacts would depend on a range of factors that were at present unknown, including the total package of economic policies to be delivered in the United States, their timing and any subsequent policy responses from other countries.

Monetary and financial conditions

7: Market-implied paths for policy rates in the United States and euro area had ended the period since the MPC’s previous meeting a little lower. That reflected, in particular, weaker-than-expected global activity data. Corporate bond spreads were little changed across these economies, while equity prices had increased slightly. At its meeting on 12 December, the ECB Governing Council had reduced its key policy rate by 25 basis points, in line with market expectations. At its meeting ending on 18 December, the FOMC was expected to reduce the federal funds rate by 25 basis points.

8: In the United Kingdom, near-term market expectations for Bank Rate had increased since the MPC’s previous meeting, predominantly reflecting stronger-than-expected wage data. The sterling effective exchange rate was little changed. Within that, sterling had depreciated by 2% against the dollar, offsetting an appreciation against the euro of around 1%.

9: More generally, market expectations for policy rates in the United Kingdom and United States had increasingly diverged from the euro area since September. The euro-area path had shifted down and had become more steeply downward sloping, while the UK and US paths had shifted up and had become shallower. In the United Kingdom and United States, rates were expected to be around 3.75 to 4% in three years’ time, compared with 2% in the euro area.

10: The August and November Bank Rate reductions, and associated changes in other risk-free reference rates, had continued to pass through to the relevant saving and borrowing rates facing households and corporates, broadly in line with historical experience. The main exception had been household sight deposit rates, which had fallen by less and more slowly than Bank Rate since August. Historically, such reductions in Bank Rate had been associated with full and fairly rapid pass-through to sight deposit rates, although these rates had not risen by as much as Bank Rate during the most recent tightening cycle.

11: Housing market activity had continued to pick up, with mortgage approvals for house purchase having risen back to their pre-pandemic average in October. That reflected, in part, declines in the average rate paid on new mortgages since quoted rates had peaked in mid-2023. Over the same period, however, the average rate paid on all outstanding mortgages had continued to increase as the majority of fixed-term mortgages were refinanced on to higher rates. As noted in the November Financial Stability Report, 37% of fixed rate mortgage accounts had not yet re-fixed since rates had started to rise in 2021 H2, so the full impact of higher interest rates had not yet passed through to all mortgagors.

12: Household broad money balances had grown unusually strongly in October. There had been evidence of deposits flowing to households from Non-Intermediary Other Financial Companies, which included asset managers, insurance companies and pension funds. Recent overall trends in broad money had been little changed, however, with annual growth in M4ex increasing only slightly to 3.4%. The ratio of household money to gross domestic income remained close to its pre-pandemic trend.

Demand and output

13: UK GDP had risen by 0.1% in 2024 Q3, slightly weaker than the 0.2% that had been expected in the November Monetary Policy Report. Within the expenditure components, household consumption had been estimated to have grown by ½%, and government spending and business investment had each risen by around 1%.

14: GDP had declined by 0.1% in October after a similar-sized fall in September. Manufacturing output had contracted by 0.6% in October, while services output had been flat on the month. Market sector output had now fallen back to around a level that had last been observed in April.

15: Most indicators of near-term activity had weakened since the previous MPC meeting. For example, the S&P Global/CIPS UK composite output PMI had fallen back to just over 50 in November and had remained at that level in the December flash release, and there had also been declines in the future output and new orders indices. Both the services and manufacturing PMIs had fallen in recent months, suggesting that a mixture of domestic and global factors was at play. The Bank’s Agents had reported that there had been some further deterioration in business sentiment since the previous MPC meeting and that activity was subdued currently, although it was still expected to pick up across the economy next year. In this context, it was notable that sales outcomes reported in the DMP Survey had consistently come in lower than companies’ expectations of their sales one-year ahead. In contrast to most other indicators, consumer confidence had increased slightly over recent months, though remained below its historical average, and most housing market indicators had been fairly robust.

16: Bank staff now expected zero GDP growth in 2024 Q4, weaker than the 0.3% that had been incorporated in the November Report. That was broadly consistent with the latest combined steer from business surveys and the available official data.

17: The Committee discussed the extent to which recent developments in output could reflect the weakness of both demand and supply, such that there might be fewer implications for the margin of spare capacity in the economy and thus domestic inflationary pressures. There was also uncertainty around how the measures that had been announced in the Autumn Budget were affecting growth. This included the extent to which companies would, over time, take account of the indirect spillovers to private demand from higher public spending, as well as the direct consequences of the increase in employer National Insurance contributions (NICs) that would take effect from April.

Supply, costs and prices

18: Low response rates had continued to impart considerable uncertainty to Labour Force Survey (LFS)-based estimates of labour market quantities. In its latest reweighting of key LFS variables, the ONS had incorporated upward revisions to the estimated population of around half a million people. Separately, the ONS had revised up its estimates of net inward migration by over 400,000 people, although that would not be reflected in the LFS for some time. Taken together, these revisions could close around half of the gap between the level of employment implied by pre-revision LFS data and that implied by alternative measures such as workforce jobs. The corollary of these upward revisions to employment would be more pronounced weakness in labour productivity. However, the LFS revisions had had only minimal implications for the historical profile of the underlying rate of unemployment.

19: At a higher frequency, other indicators of unemployment had exhibited some dispersion, but there had been little evidence of a significant increase during the period since the November Monetary Policy Report. Household surveys of job security and advanced notifications of potential redundancies had remained consistent with little net change in the underlying unemployment rate.

20: Vacancies had continued to fall, albeit at a slower pace than in 2023. Bank staff analysis of the difference between the observed ratio of vacancies to unemployment and the ratio of vacancies to unemployment that might be consistent with equilibrium in the labour market, after taking account of, for example, changes in the cost of posting vacancies over time, suggested that the labour market was now broadly in balance. This analysis, which was corroborated by other indicators from the Agents and in the REC survey, signalled less tightness in the current labour market than a simple historical view of the vacancies-to-unemployment ratio would imply.

21: The uncertainty surrounding developments in key labour market quantities and measured labour productivity would limit the extent to which the Committee would be able to draw firm conclusions in its next regular stocktake of the short to medium-term supply capacity of the economy. This was being undertaken ahead of the February Monetary Policy Report.

22: Annual growth in private sector regular average weekly earnings (AWE) had risen from 4.8% in the three months to August to 5.4% in the three months to October. This upside surprise had reflected a combination of greater-than-expected strength on the month and revisions to prior months. Base effects from the previous year would push annual rates of private sector regular AWE growth closer to 6% in 2024 Q4, but this measure of pay growth had often exhibited more volatility than comparable survey-based measures.

23: The signal from most indicators following the announced increases in the National Living Wage (NLW) and employer National Insurance contributions tended to corroborate the view that, supported by diminishing churn, easing recruitment difficulties and an ongoing loosening of the labour market, annual private sector wage growth would slow over the policy-relevant horizon. The Agents’ intelligence available since the Autumn Budget, for example, suggested that firms in aggregate expected pay settlements in 2025 to sit within a range of 3 to 4%. This was slightly higher than the 2 to 4% range reported before the Budget, but lower than the 5½% average reported in 2024. The latest evidence from the DMP Survey was also consistent with a softening in wage growth across all sectors, albeit to a plateau of around 4% in aggregate over the year ahead. Expected wage growth in consumer services companies, in particular, had remained elevated at around 5%.

24: Across surveys, firms had reported that their response to higher employer NICs would involve multiple types of adjustment, of which pay growth was but one. In the DMP Survey, for example, higher prices and lower employment were both cited more frequently than lower wages. Moreover, a more granular disaggregation of the results of the DMP Survey suggested that firms with greater exposure to the NLW would be less likely to respond to higher NICs by paying lower wages. These firms would be more likely to respond to higher NICs by raising prices, accepting lower profit margins and/or laying off existing workers.

25: Twelve-month CPI inflation had increased to 2.6% in November from 1.7% in September. This was slightly higher than previous expectations, owing in large part to stronger inflation in core goods and food. Core CPI inflation had increased to 3.5%.

26: Annual services price inflation had been 5.0% in November, little changed from its rate in October and September. The three-month moving averages of annualised monthly increases in a range of underlying services prices had edged higher in November, but had remained lower than their corresponding annual rates. The extent of domestically generated disinflation to date, however, had remained relatively modest.

27: In the near term, headline CPI inflation was expected to continue to rise slightly.

28: Although indicators of households’ inflation expectations had largely normalised through the first half of this year, short-term expectations had begun to increase again in the latest data. The Bank of England/Ipsos Inflation Attitudes Survey’s measure of median one-year ahead inflation expectations had risen to 3.0% in November. The measure of medium-term expectations in the same survey had now edged above its historical average. The Citi/YouGov indicator of households’ short-term inflation expectations had risen over several months to 3.5%, even while realised CPI inflation had eased. Businesses’ own price expectations, as reported in the DMP Survey, had remained consistent with only a modest decline in inflation over the coming year, particularly in consumer-facing services sectors.

29: The latest increases in inflation expectations might reflect greater attentiveness among households to cost-of-living increases, such as the reduction in winter fuel payments, higher bus fares and vehicle excise duty, successive increases in the Ofgem price cap in October and January, and higher food prices. These increases might interact with already-elevated inflation perceptions, and thus could add to the persistence of domestic inflationary pressures.

The immediate policy decision

30: The Monetary Policy Committee (MPC) sets monetary policy to meet the 2% inflation target, and in a way that helps to sustain growth and employment. The MPC adopts a medium-term and forward-looking approach to determine the monetary stance required to achieve the inflation target sustainably.

31: Monetary policy had been guided by the need to squeeze remaining inflationary pressures out of the economy to achieve the 2% target both in a timely manner and on a lasting basis. Over recent quarters there had been progress in disinflation, particularly as previous external shocks had abated, although remaining domestic inflationary pressures were resolving more slowly.

32: As set out in the November Monetary Policy Report, the Committee’s deliberations had been supported by the consideration of a range of cases that could impact the evolution of inflation persistence. In the first case, most of the remaining persistence in inflation might dissipate quickly as pay and price-setting dynamics continued to normalise following the unwinding of the global shocks that had driven up inflation. In the second case, a period of economic slack might be required to normalise these dynamics fully. In the third case, some inflationary persistence might also reflect structural shifts in wage and price-setting behaviour. Each case would have different implications for how quickly the restrictiveness of monetary policy could be withdrawn.

33: The MPC was also considering the impact on growth and inflationary pressures from the measures announced in the Autumn Budget, and from geopolitical tensions and trade policy uncertainty. These domestic and global developments had generated additional uncertainties around the economic outlook.

34: As set out in the November Report, the combined effects of the measures announced in the Budget were provisionally expected to boost the level of GDP by around ¾%, and CPI inflation by just under ½ of a percentage point, at their peaks relative to the August projections. However, there remained significant uncertainty around how the economy might respond to higher overall costs of employment, including from the increase in employer National Insurance contributions and the National Living Wage.

35: The Committee noted that indicators of trade policy uncertainty had increased materially, but that the magnitude and the direction of the impact of any such policies on UK inflation was at present unclear. These effects might not be apparent for some time.

36: Since the MPC’s previous meeting, most indicators of UK near-term activity had declined. Bank staff were expecting zero GDP growth in 2024 Q4, weaker than had been projected in the November Monetary Policy Report. Several components of the December S&P Global/CIPS UK flash PMI had fallen, including the new orders and employment indices. Other indicators of employment growth had been more mixed.

37: Although there remained significant uncertainty around developments in labour market quantities derived from the Labour Force Survey, the Committee now judged that the labour market was broadly in balance based on a wider range of evidence. The number of job vacancies had continued to fall, albeit at a slower pace than in 2023. There had also been a decline in indicators of labour market tightness from the Agents and in the REC survey.

38: Annual private sector regular AWE growth had picked up quite sharply in the three months to October, to 5.4%, which was ½ of a percentage point stronger than had been expected in the November Report. AWE growth had tended to be more volatile than other wage indicators, however. The latest Agents’ intelligence suggested that average pay settlements in 2025 would be within a range of 3 to 4%.

39: Twelve-month CPI inflation had increased to 2.6% in November from 1.7% in September, slightly higher than previous expectations. Services consumer price inflation had remained elevated, at 5.0%, while core goods price inflation had risen to 1.1%. Food consumer price inflation had picked up slightly over recent months, to 2%. Some other indicators of goods price inflation had increased, including in the December S&P Global/CIPS UK flash PMI. Headline CPI inflation was expected to continue to rise slightly in the near term.

40: Although household inflation expectations had largely normalised, some indicators had increased recently, in part reflecting developments in energy and food prices as well as other more idiosyncratic factors. Businesses’ own price expectations had remained consistent with only a modest decline in inflation over the coming year, particularly in consumer-facing services sectors. Monetary policy was acting to ensure that longer-term inflation expectations were anchored at the 2% target.

41: At this meeting, six members preferred to maintain Bank Rate at 4.75%. Most indicators of UK near-term activity had weakened, but CPI inflation, wage growth and some indicators of inflation expectations had risen, adding to the risk of inflation persistence. The macroeconomic implications of the higher costs of employment facing companies remained particularly uncertain. Against a backdrop over recent years of a repeated sequence of negative supply shocks, incoming data would help to clarify the potential trade-off between more persistent inflationary pressures and greater weakness in output and employment. For five of these members, recent developments added to the argument for a gradual approach to the withdrawal of policy restrictiveness, while eschewing any commitment to changing policy at a specific meeting. For the other member, the evolution of and prospects for disaggregated measures of activity and inflation could warrant an activist strategy.

42: Three members preferred a 0.25 percentage point reduction in Bank Rate at this meeting. The most recent data developments pointed to sluggish demand and a weakening labour market, now and in the year ahead, both of which would see further downward pressure on demand, wages, and prices. In the short run, these factors, alongside higher uncertainty and weak global conditions, paired with the temporary uptick in headline inflation entailed a policy trade-off. In the medium term, a continued stance that was very restrictive risked deviating unsustainably from the 2% inflation target and opening an unduly large output gap. Given the evolving balance of risks, a less restrictive policy rate was warranted.

43: The Committee continued to monitor closely the risks of inflation persistence and would assess the extent to which the evolving evidence was consistent with more constrained supply, which could sustain inflationary pressures, or with weaker demand, which could lead to the emergence of spare capacity in the economy and push down inflation. A gradual approach to removing monetary policy restraint remained appropriate. Monetary policy would need to continue to remain restrictive for sufficiently long until the risks to inflation returning sustainably to the 2% target in the medium term had dissipated further. The Committee would decide the appropriate degree of monetary policy restrictiveness at each meeting.

44: The Chair invited the Committee to vote on the proposition that:

- Bank Rate should be maintained at 4.75%.

45: Six members (Andrew Bailey, Sarah Breeden, Megan Greene, Clare Lombardelli, Catherine L Mann and Huw Pill) voted in favour of the proposition. Three members (Swati Dhingra, Dave Ramsden and Alan Taylor) voted against the proposition, preferring to reduce Bank Rate by 0.25 percentage points, to 4.5%.

Operational considerations

46: On 18 December 2024, the stock of UK government bonds held for monetary policy purposes was £655 billion.

47: The following members of the Committee were present:

- Andrew Bailey, Chair

- Sarah Breeden

- Swati Dhingra

- Megan Greene

- Clare Lombardelli

- Catherine L Mann

- Huw Pill

- Dave Ramsden

- Alan Taylor

Sam Beckett was present as the Treasury representative.

NZD/USD at a New Low: Problem is US Dollar and Local GDP

NZD/USD has dropped to its lowest level since October 2022, trading around 0.5620. The currency pair is under pressure from two major factors: the strengthening US dollar and New Zealand’s weak domestic economic data.

The primary driver of the decline in NZD/USD is the robust performance of the US dollar. Following the Federal Reserve’s December meeting, the greenback gained considerable strength due to expectations of subdued rate cuts in 2025. Throughout Wednesday, the NZD dropped by 2.3% against the US dollar, underscoring the impact of a hawkish Fed outlook.

The second factor contributing to NZD’s weakness is poor domestic economic performance. New Zealand’s GDP data has reinforced concerns that the economy is in recession. In Q3 2024, GDP contracted by 1.0% quarter-on-quarter, following a revised 1.1% decline in Q2. On an annualised basis, the economy shrank by 1.5%, a sharp deterioration from the 0.5% contraction recorded in the previous quarter.

The GDP figures were worse than anticipated, heightening fears of a deeper recession and increasing the likelihood of further aggressive monetary easing by the Reserve Bank of New Zealand (RBNZ). Even before this latest data, the RBNZ had been more proactive than several other central banks in cutting interest rates, and the recent developments are likely to reinforce its dovish stance for 2025.

Technical analysis of NZD/USD

On the H4 chart, NZD/USD experienced a downward pullback from the 0.5785 level and broke through the 0.5690 support level. The current market structure indicates the formation of a downward wave targeting 0.5598. After reaching this level, a corrective move back to test 0.5690 from below is possible. Notably, the breakdown below 0.5690 has paved the way for further declines towards 0.5500, with the main target projected at 0.5454. This bearish scenario is supported by the MACD indicator, with its signal line positioned below the zero mark and trending sharply downward.

On the H1 chart, NZD/USD is shaping a downward wave towards 0.5597. Before the decline resumes, a short-term correction to 0.5690 could occur. The next target would be 0.5500. This outlook is confirmed by the Stochastic oscillator, where the signal line is near the 80 mark and preparing to drop towards the 20 mark, indicating continued bearish momentum.

Gold Prices Recover from 1-Month Low

- Gold rises above 2,600 again

- RSI and stochastics suggest more upside moves

Gold prices are recouping some significant losses that were posted after the Fed’s policy decision on Wednesday to cut rates by 25 bps. The market tumbled to a new one-month low of 2,582 but is currently holding above 2,600. The technical oscillators are gaining some momentum with the RSI pointing slightly up below the neutral threshold of 50. The stochastic oscillator posted a bullish crossover between the %K and %D lines near the 20 level, confirming an upside retracement.

Further bullish movements could pave the way for the 2,625 resistance, which is situated ahead of the moving average lines between 2,640 and 2,665. To endorse the positive tendency in the market, it needs to surpass the previous double top, around 2,725.

On the other hand, a slip below the 2,605 support and a drop beyond the latest bottom of 2,582 could trigger steeper bearish action, leading traders towards 2,554 and 2,536.

To sum up, the yellow metal has been in a bearish correction over the last week, but the broader outlook remains bullish.

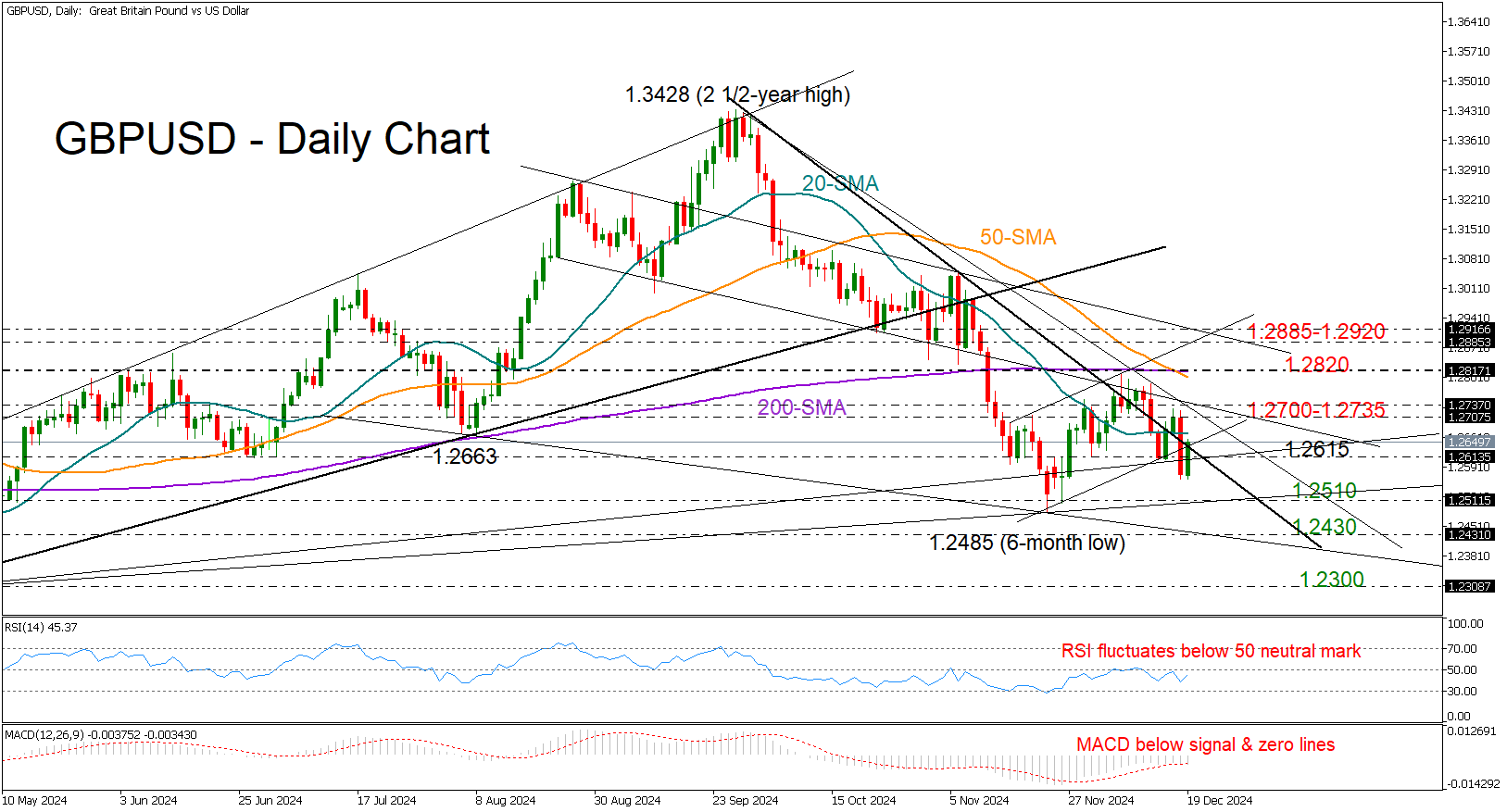

Will GBPUSD Make a Comeback After Post-Fed Tumble?

- GBPUSD shows some recovery after three-week low

- Technical signals reflect persisting selling interest

- BoE rate decision next in focus at 12:00 GMT

GBPUSD is trying to heal its wounds after taking a hit from the Fed’s hawkish rate cut, which squeezed the price to a three-week low of 1.2560 and back below the 20-day simple moving average (SMA) late on Wednesday.

Unlike its major peers, the British pound avoided new lower lows in the short-term picture and managed to hold its ground above the 1.2510 support zone as traders maintained some patience ahead of the Bank of England’s rate decision. However, despite this resilience, the technical indicators remain bearish and the completed death cross between the 50- and 200-day SMAs may keep traders on edge, unless something changes soon.

A continuation below 1.2500 could allow the pair to take a breather near the 1.2430 constraining zone. Otherwise, GBPUSD could suffer a freefall toward April’s low near 1.2300, a break of which could take it into the 1.2170-1.2200 region.

On the flip slide, should the price maintain its positive momentum above 1.2615, it may next head for the 1.2700-1.2735 region. A successful penetration higher could then shift the spotlight to the flattening 200-day SMA at 1.2820, which is where the price peaked at the start of the month. Hence, a close above it could prompt an extension toward the 1.2885-1.2900 area.

Overall, GBPUSD’s short-term outlook is still a bit shaky. The pair could stay under pressure in the coming sessions, and a real test will come if it can run above 1.2820 for a sustained recovery. A drop below 1.2500 would put it back on a bearish path.