Sample Category Title

Weekly Economic & Financial Commentary: That’s a Wrap

Summary

United States: That's a Wrap

- The outlook for 2025 is riddled with uncertainty, yet data released this week demonstrate a U.S. economy that retains momentum. Ascertaining what level of policy restraint achieves the careful balance of keeping inflation in check and easing stress on interest-rate sensitive sectors will dominate the monetary policy discussion come 2025.

- Next week: ISM Manufacturing & Services (Jan 3, 7), Employment (Jan 10)

International: Brazilian Real Responds to a Lack of Fiscal Credibility

- The Brazilian real sold off sharply late last week on fiscal deficit worries, and the selloff continued into this week as markets lost more confidence in Brazil's ability to achieve its budget targets. These spending concerns drove Brazil's currency to a new low against the U.S. dollar this week.

- Next week: Brazilian Policymakers (Mon-Fri), Mexico Inflation (Mon), Turkish Central Bank (Thu)

Interest Rate Watch: FOMC Cuts Rates, but Pace of Easing Ahead Likely Will Slow

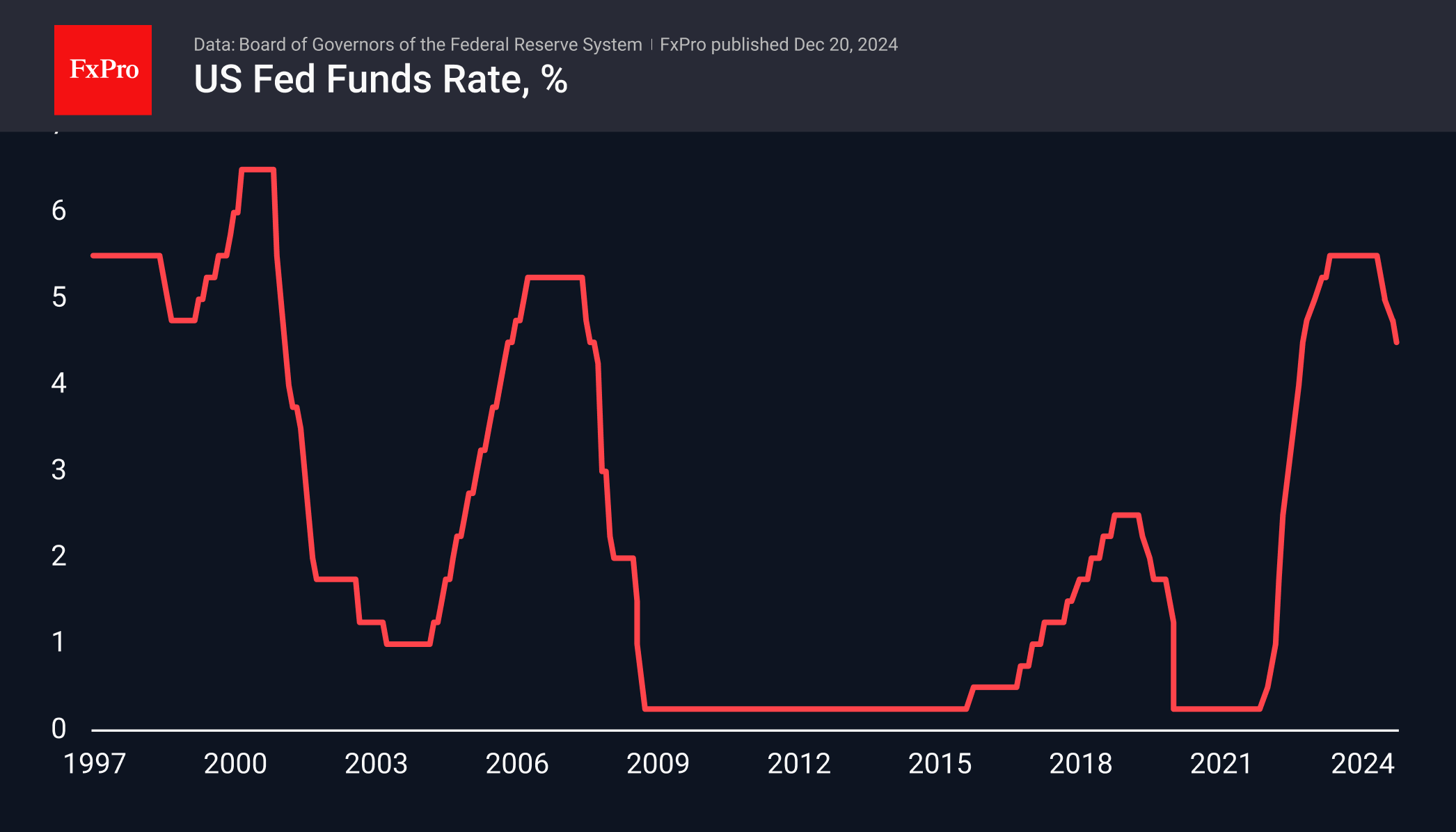

- As widely expected, the Federal Open Market Committee (FOMC) cut the target range for the federal funds rate by 25 bps at its meeting this week. The FOMC has now cut its target range by 100 bps from its peak of 5.25%-5.50% through moves of 50 bps in September, 25 bps in November and 25 bps on Wednesday.

Credit Market Insights: Household Net Worth Climbs in Q3 on Strong Equity Markets

- Household net worth climbed $4.77 trillion in the third quarter according to data released last week from the Federal Reserve. Net worth has now risen in four consecutive quarters and in seven of the last eight, with strong performance in corporate equities and mutual fund shares doing a lot of the heavy lifting.

Topic of the Week: Will Federal Government Spending Be Slashed in 2025?

- The outlays of the federal government totaled roughly $6.8 trillion in the fiscal year that ended on September 30. With a new president and Congress taking control of Washington D.C. in January, focus has turned to whether significant spending cuts are on the horizon.

October GDP to Look Marginally Stronger After Slew of Weak Data

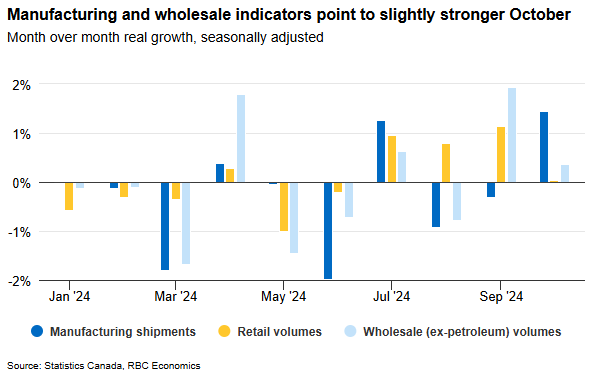

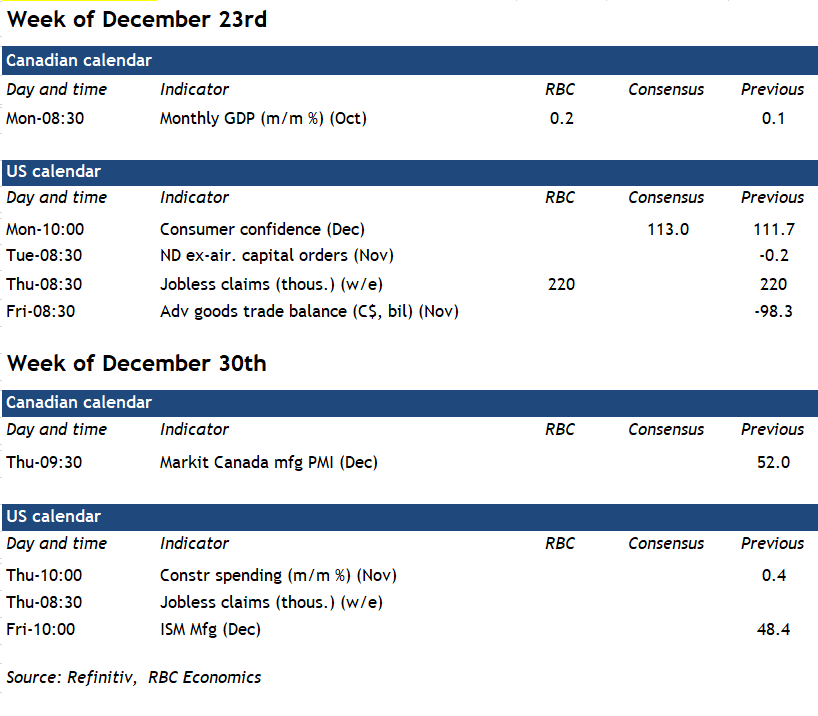

The final major data point from Statistics Canada in 2024 will be Monday’s gross domestic product release for October, which will be the last GDP print before the Bank of Canada’s Jan. 29 meeting. We look for a 0.2% increase that would be the strongest monthly gain since April, and firmer than the 0.1% advance estimate a month ago.

Activity in both the goods and services sectors will likely show an uptick in October. Early data is showing a rise in oil production in Alberta. The manufacturing sector posted a stronger month with sales (excluding price changes) up 1.4%. Retail sale volumes held steady in October but wholesale sales edged up and residential real estate posted a notable jump.

Still, softer momentum in earlier months means the tick higher in October output would leave GDP growth in Q4 as a whole tracking below the BoC’s 2% forecast—something the central bank already acknowledged when it made another 50 basis point cut to the overnight rate in December.

We expect the early estimate for November GDP will show limited growth, even with a likely boost in the entertainment sector from a fortnight of unusually well-attended concerts in Toronto. A 0.2% pull-back in November hours worked was partially related to labour disputes at ports and the Canada Post strike. Our tracking of consumer spending also looked softer in November with early holiday shopping potentially delayed ahead of a GST holiday that started mid-December.

The BoC signaled firmly in December that policymakers are planning a more gradual pace to interest rate cuts going forward, but we continue to expect the overnight rate will ultimately need to fall to net stimulative levels (below the BoC’s current 2.25% to 3.25% estimate of the neutral range) to allow the economy to strengthen and prevent inflation from running significantly below the 2% target.

Week ahead data watch

Weekly Focus – Hawkish Christmas Present from US Federal Reserve

The tradition of central banks hosting meetings just before Christmas continued this year with policy decisions in the US, Japan, UK, Norway, and Sweden. The largest present came from the US Federal Reserve in the shape of a significant hawkish surprise. Fed cut the policy rate target by 25bp to 4.25-4.50% as expected, but Powell delivered a clearly hawkish message, highlighting that the easing cycle has entered a "new phase" in which the Fed is looking to slow down the pace of rate cuts. The updated "dots" now project only two 25bp cuts next year compared to four in the September projections. The main reason for the hawkish turn was an upward revision of the inflation forecast to 2.5% y/y in 2025 (from 2.1%) and the fact that most members even saw upside risks to the new inflation projections. The decision pushed the entire UST curve up by some 13-15bp, and the market is now pricing only 40bp worth of cuts from the Fed next year. Due to the change in guidance, we have removed our expectations for a cut in January but continue to expect four cuts next year from March.

Both the Bank of Japan and Bank of England left their policy rates unchanged at 0.25% and 4.75%, respectively, as broadly expected. As the economic recovery looks on track, we expect the BoJ to hike the policy rate in January. The BoE delivered a dovish vote split but continue to signal a gradual cutting approach. We expect the next cut in February and a quarter pace thereafter. For Sweden and Norway, see page 4.

On the data front, the December PMI surveys gave some relief for the growth outlook as services PMIs rose more than expected in both the US, euro area, and UK. Services PMIs bounced back above 50 in the euro area following the large decline in November in a sign that activity is holding up while the US services PMI rose even further to 58.5 from 56.1. In contrast to the services sector, activity in the manufacturing sector weakened with US manufacturing PMI declining to 48.3, the UK to 47.3, and the euro area remained unchanged at 45.2.

On the political front, the risk of a government shutdown in the US increased this week as president-elect Donald Trump told republican congressmen to not support a stopgap funding bill that was otherwise set to pass Congress. With no other plan ready, the government is again facing a risk of a shutdown, less serious for the economy than in 2018, but still an unpleasant Christmas present for public workers.

In the coming weeks focus will be on the US jobs market report and ISM survey, euro area inflation, and Chinese PMIs and PBoC rate decision. We expect US nonfarm payrolls growth to slow down to +170k (from +227k), a steady unemployment rate at 4.2%, and average hourly earnings growth at +0.3% m/m SA. We expect euro area HICP inflation to rise to 2.4% y/y in December from 2.2% in November. The increase is mainly due to base effects on energy and food inflation while we expect core inflation to decline from 2.7% y/y in November to 2.6% y/y. In China, we expect the PMIs to be unchanged in December following increases in the past two months. Manufacturing activity is currently underpinned by some front loading of exports to the US in anticipation of tariffs next year. The PBOC will also announce its policy rate, which is expected to be left unchanged.

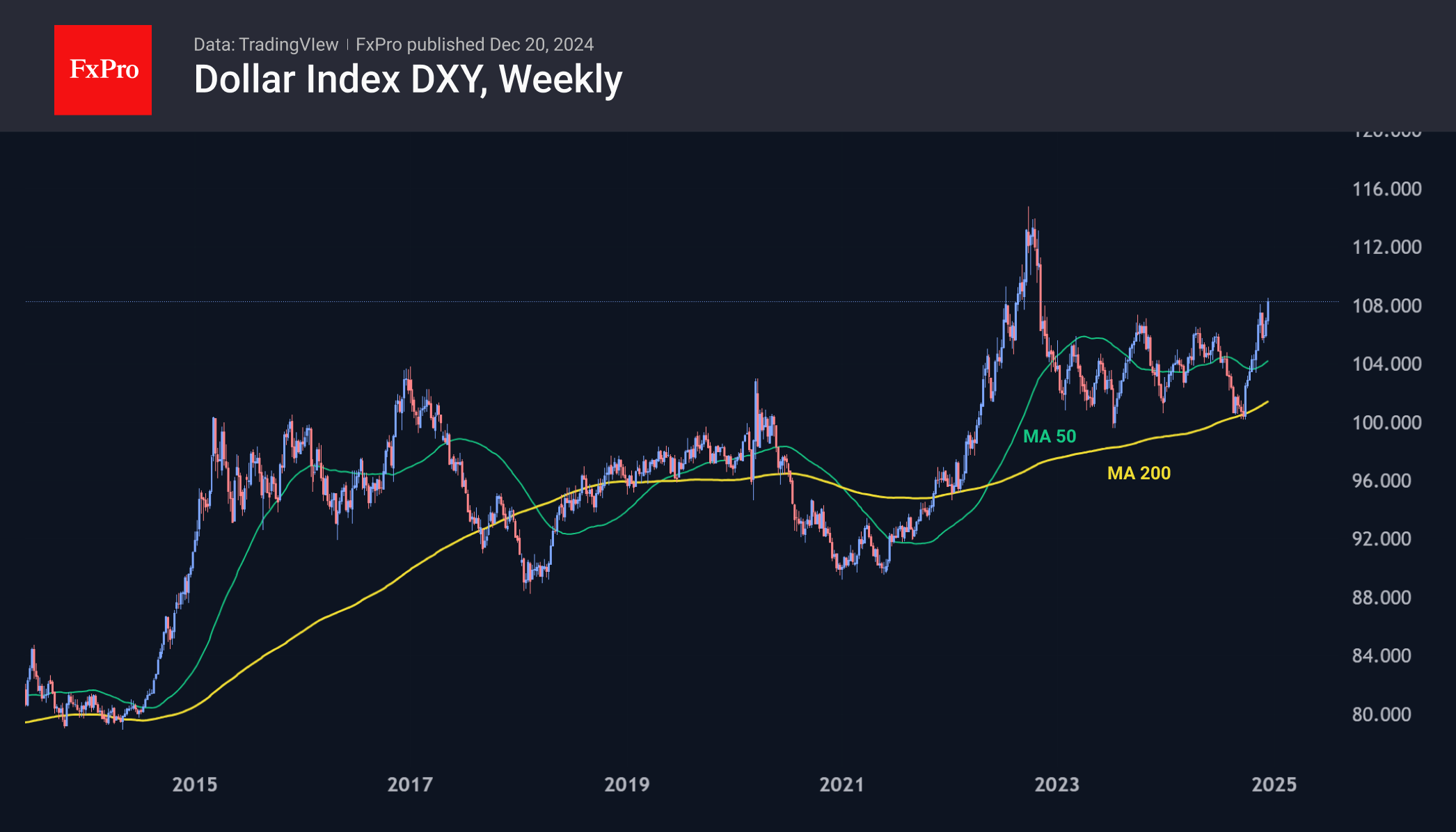

US Dollar Ends the Year on a Strong Note

The U.S. dollar ends the year on a strong note, hitting two-year highs at 108.45. The Fed expects a 50-point rate cut for the full year 2025 versus 4 cuts one quarter earlier, citing higher inflation forecasts and a stubbornly strong labour market. This fundamental change has given a new impetus to the dollar’s rise that began in late September.

The fundamental reason is the change in the tone of the Fed’s monetary policy. Two consecutive 25-point cuts followed a 50-point cut in the key rate in September. Recent comments suggest a pause in January. The difference between current expectations for the end of next year and what was priced six months ago exceeds 100 points. Meanwhile, the euro, pound, and yen have much more modest six-month changes in expectations. Until September, this difference was against the dollar, but now it is becoming the driving force behind it.

The dollar’s strength is also the result of market speculation, expectations of intensified tariff wars, and fiscal stimulus expected from the Republican Party’s dominance of US politics since November. There has been no actual change yet, but there are signs that the Fed is beginning to incorporate these expectations into its policy.

The dollar index’s technical picture on the long-term charts is on the side of the bulls. Dollar buyers came in on the downturn under the 200-week moving average, turning the market up. In 2022 and 2014, the DXY rallied more than 20% after pushing off that line before consolidating. In 2019-2020, the opposite was the case, with a steady return to the mean culminating in a failure in the second half of 2020.

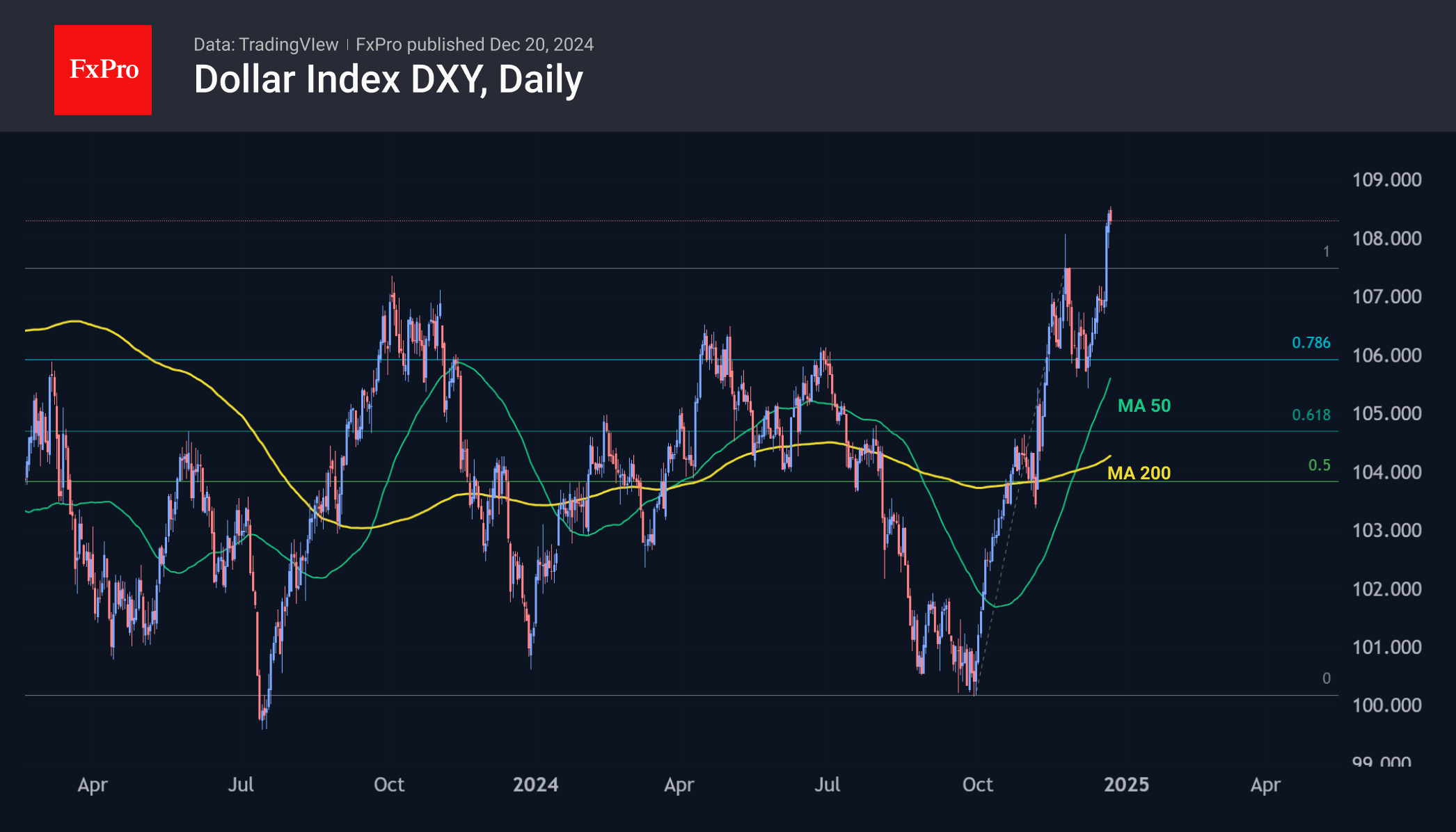

On the daily timeframes, DXY broke out to new highs after a corrective pullback of a couple of per cent, correcting to 78.6% of the upside from the October lows. A strong reversal to the upside proved the strength of the buyers, and exceeding the last peak confirmed the bullish bias. The next upside target looks to be the 112 area, which will be the exit to the 2022 highs.

In the context of EURUSD, the strengthening of the dollar brings it to the parity area. History suggests that the 1.0 level is unlikely to be a turning point. Either we see attempts to prevent a prolonged decline under 1.05, or buyers will emerge much later.

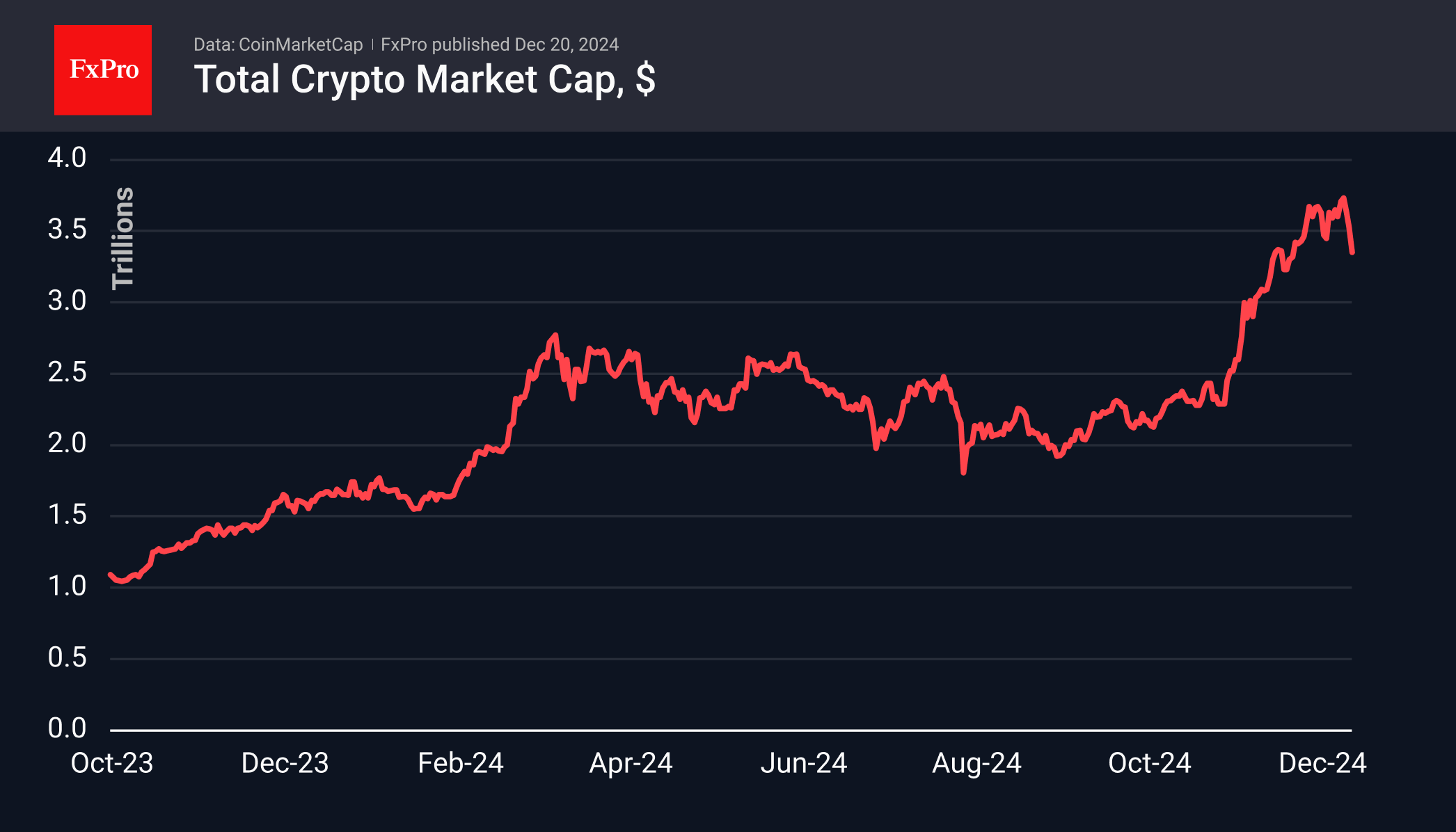

How Deep Will Crypto Dive?

Market Picture

The crypto market continues to retreat, having lost 4.4% to $3.36 trillion in the last 24 hours and already over 11% from the all-time peak of $3.79 trillion set on Tuesday. While the sell-off in stock markets has slowed, cryptocurrencies are maintaining or even picking up the pace of the decline. This return to early December levels is reminiscent of the rally locking in from November or all the growth of 2024. In the former case, the sell-off could pause in the $3.2 trillion area (-5% from current levels), while in the latter case, the sell-off could pause in the territory below $3 trillion with potential above 12.5%. Despite the threat of a deeper correction, we remain positive on the outlook for the year ahead.

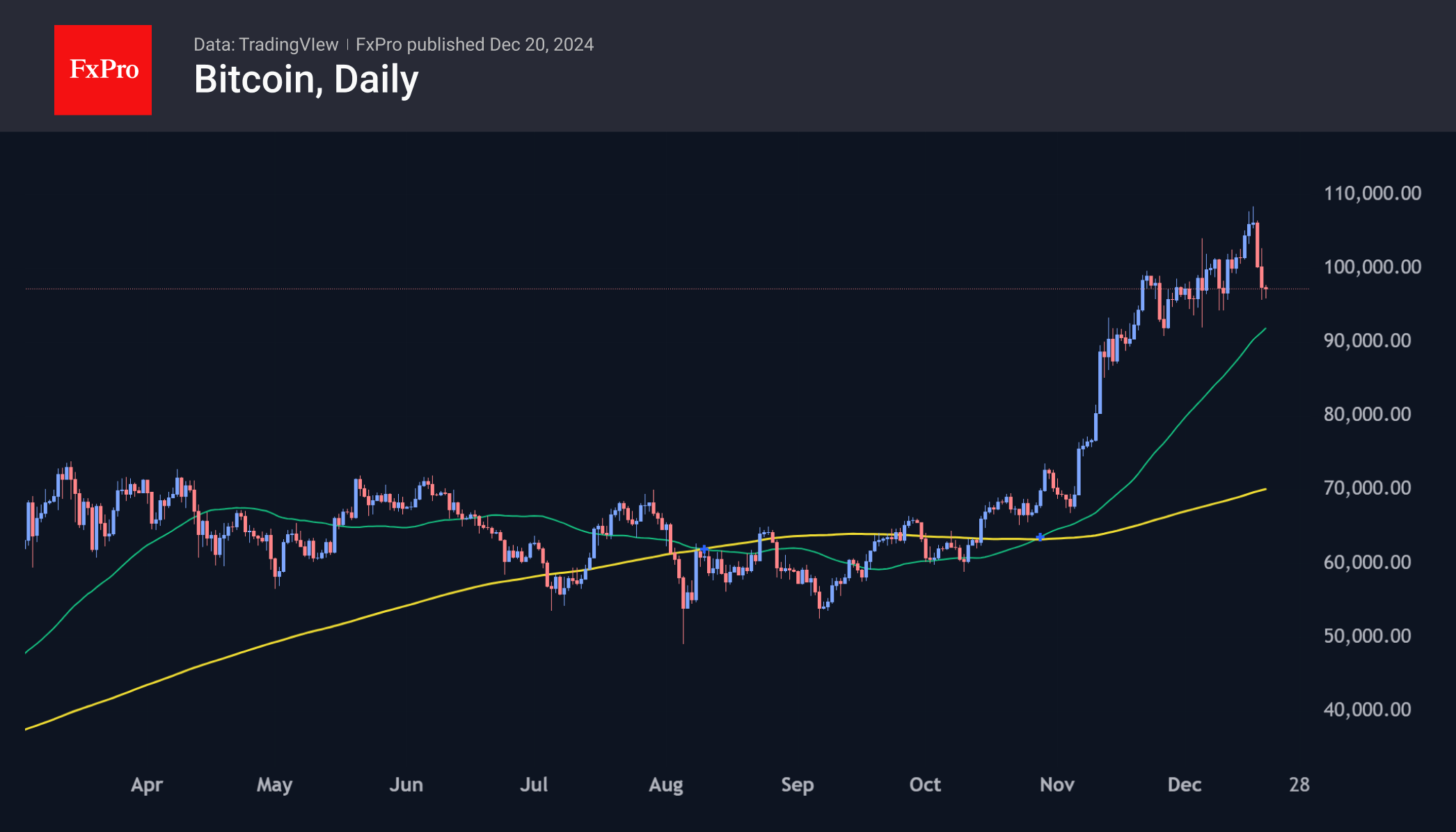

Bitcoin is back below $100K, getting support at $96K on Friday morning. A failure below $94.5K would signal a break of the uptrend of the last six weeks, while a fall below $92K on Friday or below $93K by the end of the week would bring the price under the 50-day moving average. In this case, time is playing on the side of the bears.

News Background

The sharp rise in the ‘network profit’ of new bitcoin investors, coupled with the active distribution of coins by hodlers, suggests a transition into the late stage of the bull market. This is the conclusion reached by Glassnode.

Mining company MARA Holdings purchased 15,574 BTC at an average price of ~$98,529 per coin. The company has grown its bitcoin reserves to 44,394 BTC. Hut 8, another miner, acquired 990 BTC at an average price of $101,710 per coin to total reserves of 10,096 BTC.

The IMF and El Salvador reached an agreement in which the country pledged to mitigate the risks associated with bitcoin in exchange for a $1.4 billion funding package. The IMF has repeatedly criticised El Salvador for its adoption of bitcoin, suggesting that its status as legal tender should be revoked and its reserves should be liquidated.

Total commissions received by Solana applications through November topped $365 million, including $106 million from ‘meme-token factory’ Pump.fun.

BTCUSD on Track for First Weekly Loss in Two Months

BTCUSD – steep pullback from new record high extends into third straight day and accelerated after loss of psychological 100K support.

Completion of Evening Doji Star reversal pattern on daily chart added to downside prospects, prompting stronger profit-taking that pushed the price to 94K zone in European session trading on Friday.

Bitcoin is on track for the first weekly loss in two months, with long upper shadow on large bearish weekly candle, signaling growing offers after larger bulls were strongly rejected on approach to next significant barrier at 110K.

Another potential negative signal will be on failure to register the second consecutive weekly close above 100K and validate signal of sustained break, that may open way for further easing.

Developments on weekly chart, where 14-w momentum is in steep decline from the recent multi-month peaks and RSI is emerging from oversold territory, support the notion.

Extended dips should find firm ground at 90K zone (round-figure / 55DMA) to keep larger bulls in play for fresh push higher, as overall picture is bullish, and supportive fundamentals continue to boost bullish sentiment.

Only firm break below 90K trigger would sideline larger bulls and signal deeper correction.

Res: 95500; 98560; 100000; 101240

Sup: 93000; 92150; 90000; 88685

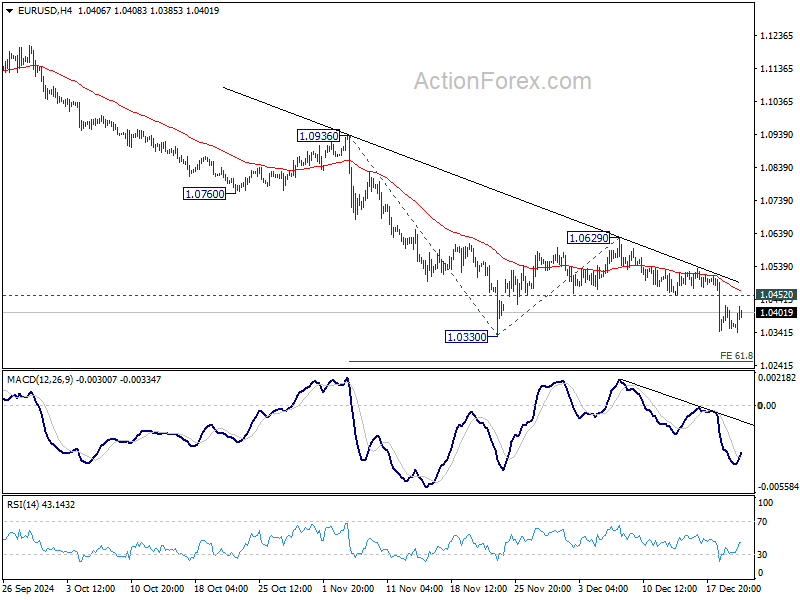

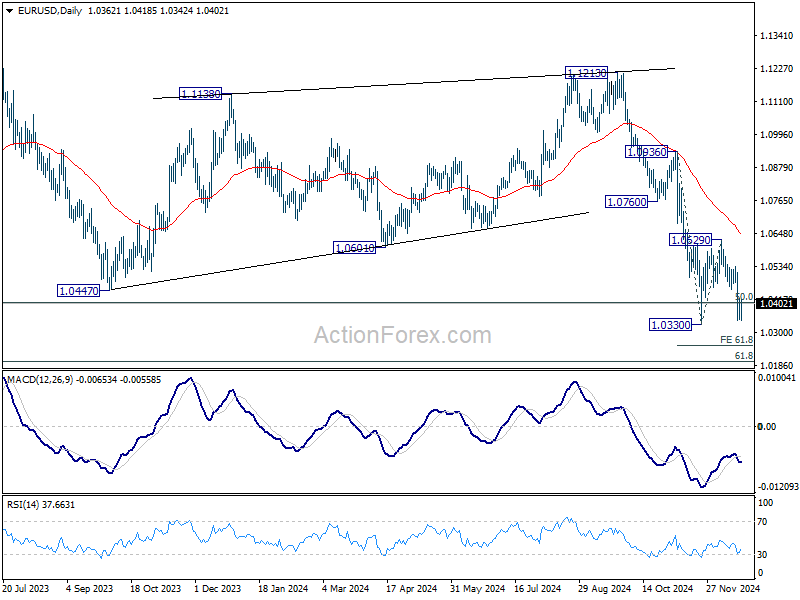

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0333; (P) 1.0378; (R1) 1.0407; More....

Intraday bias in EUR/USD remains on the downside for the moment. Firm break of 1.0330 support will resume the fall from 1.1213 and target 61.8% projection of 1.0936 to 10330 from 1.0629 at 1.0254, and then 100% projection at 1.0023. On the upside, above 1.0452 will turn intraday bias neutral again first.

In the bigger picture, focus stays on 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404. Strong rebound from this level will keep price actions from 1.1273 (2023 high) as a medium term consolidation pattern only. However, sustained break of 1.0404 will raise the chance that whole up trend from 0.9534 has reversed. That would pave the way to 61.8% retracement at 1.0199 first. Firm break there will target 0.9534 low again.

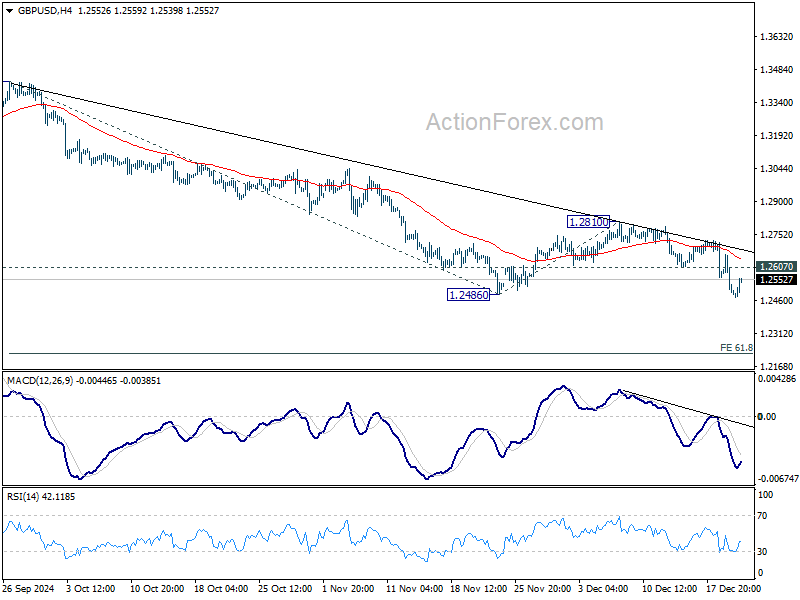

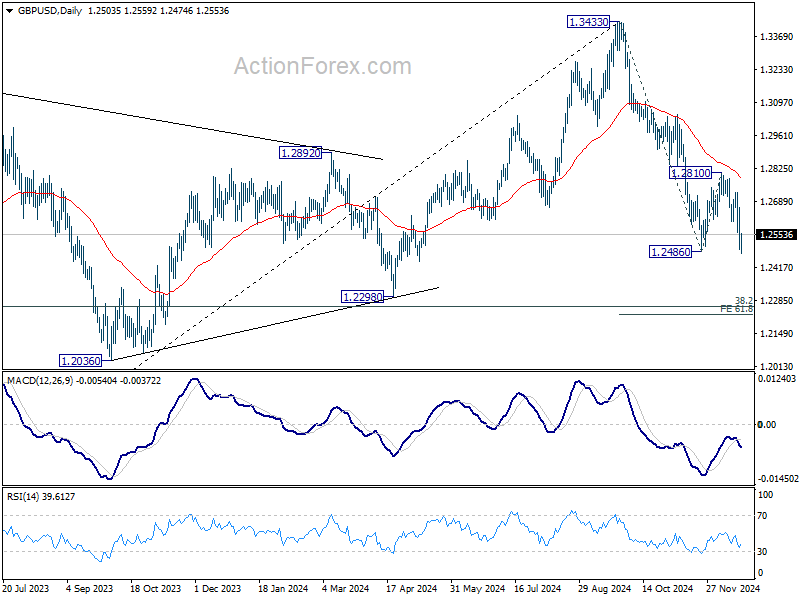

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2442; (P) 1.2554; (R1) 1.2614; More...

Intraday bias in GBP/USD stays on the downside at this point. Current decline from 1.3433 should target 61.8% projection of 1.3433 to 1.2486 from 1.2810 at 1.2225. On the upside, above 1.2607 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 1.2810 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.3433 medium term are seen as correcting whole up trend from 1.0351 (2022 low). Deeper decline could be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. But strong support is expected there to bring rebound to extend the corrective pattern.

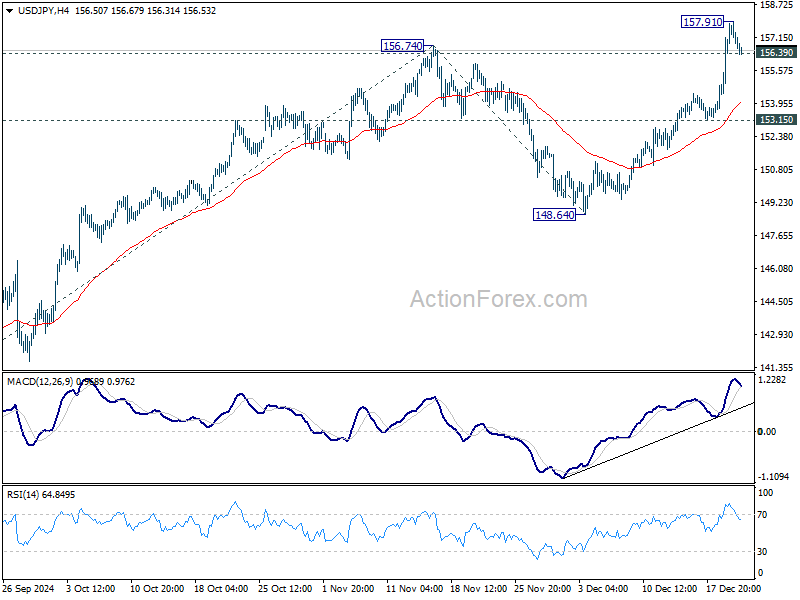

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.31; (P) 156.56; (R1) 158.68; More...

Intraday bias in USD/JPY is turned neutral with current retreat and breach of 156.39 minor support. Some consolidations would be seen first, but further rally is expected as long as 153.15 support holds. On the upside, above 157.91 will resume the rise from 139.57, and target 61.8% projection of 139.57 to 156.74 from 148.64 at 159.25 next.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

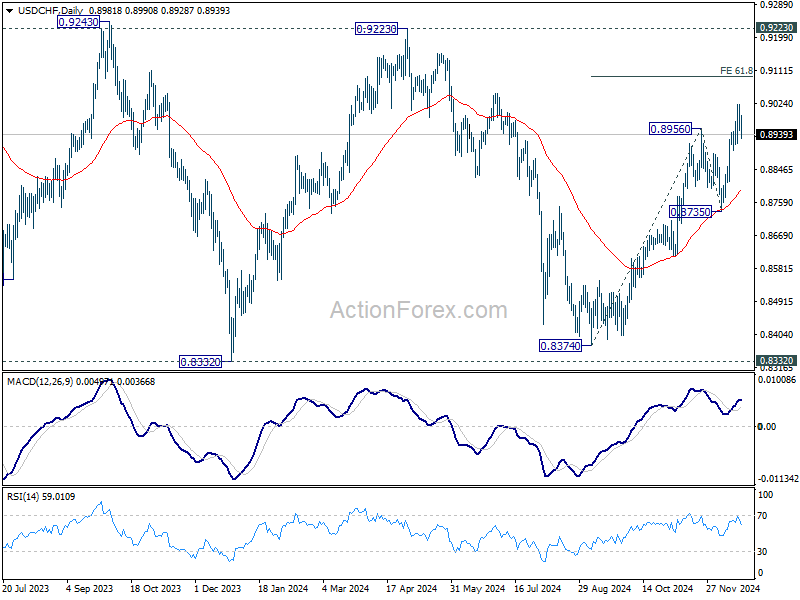

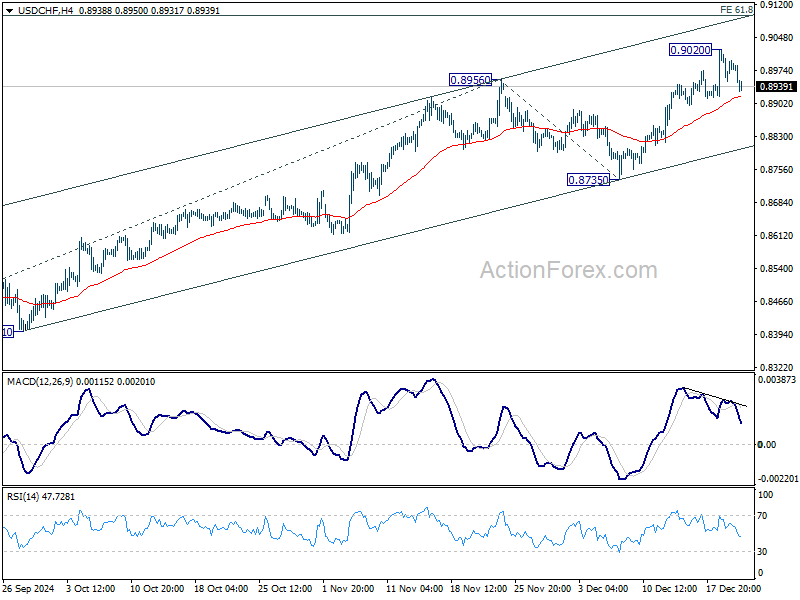

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8951; (P) 0.8990; (R1) 0.9027; More…

Intraday bias in USD/CHF remains neutral for consolidations below 0.9020 temporary top Some more consolidations could be seen but further rally is expected as long as 0.8735 support holds. On the upside, break of 0.9020 will resume the rally from 0.8374. Next target will be 61.8% projection of 0.8374 to 0.8956 from 0.8735 at 0.9095.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with rise from 0.8374 as the third leg. Overall outlook will continue to stay bearish as long as 0.9223 resistance holds. Break of 0.8332 low is in favor at a later stage when the consolidation completes.