Sample Category Title

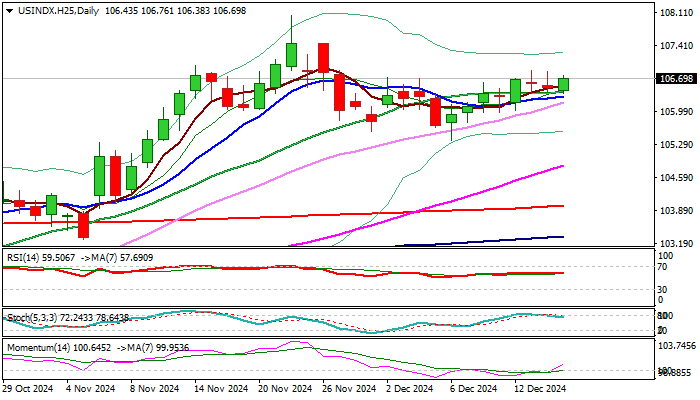

Dollar Index Outlook: Prolonged High Fed Rates Expected to Boost Dollar

The dollar index firmed in early Tuesday trading and pressuring the peaks of recovery leg from 105.37 (Dec 6 low).

Although last Fri/Mon action was shaped in Doji candles and signaled indecision, this was likely a consolidation before recovery resumes.

Fresh bulls probe through cracked Fibo barrier at 106.71 (50% retracement of 108.04/105.37 pullback) with firm break here to generate fresh signal for continuation of recovery leg towards targets at 107.02 /41 (Fibo 61.8% and 76.4% respectively) guarding key barrier at 108.04 (2024 peak of Nov 22, also the highest since Nov 2022).

Near-term bullish bias is expected to remain intact while the price stays above 10DMA (106.32) and deeper dips stay above 106.00 handle

Technical picture on daily chart is overall bullish and contributes to brighter fundamental outlook, as markets anticipate that US interest rates will remain elevated.

Fed is widely expected to cut interest rates by 25 basis points on Wednesday but will remain very cautious in shaping the monetary policy in the near future, as inflation remains elevated and expected to rise further in anticipated economic boost by Trump’s administration, while US economy remains in good condition overall.

Res: 106.86; 107.02; 107.41; 108.00.

Sup: 106.32; 106.00; 105.75; 105.37.

ECB’s Rehn: EU can bolster negotiation stance with prepared countermeasures on US tariffs

Finland's ECB Governing Council member Olli Rehn highlighted growing risks to Europe’s economic outlook with the uncertainty over trade policy as a key downside factor.

Rehn warned that Europe must be prepared to respond to potential trade conflicts with the US, emphasizing that while “negotiation is preferable,” EU’s position could be strengthened by demonstrating readiness to implement “countermeasures” against any US tariff threats.

Rehn also provided clarity on ECB’s monetary policy direction, stating it is now clearly leaning toward further easing. However, the “speed and scale of rate cuts” will remain data-dependent and decided at each meeting based on a thorough assessment of economic developments.

Eurozone goods exports rise 2.1% yoy in Oct, imports up 3.2% yoy

Eurozone goods exports rose 2.1% yoy to EUR 254.0B in October. Goods imports rose 3.2% yoy to EUR 247.2B. Trade balance stood at EUR 6.8B surplus. Intra-Eurozone trade rose 2.2% yoy to EUR 229.2B.

In seasonally adjusted term, exports fell -1.6% mom to EUR 232.5B. Imports rose 1.3% mom to EUR 226.5B. Trade surplus narrowed from EUR 12.6B in September to EUR 6.1B, versus expectation of EUR 11.9B. Intra-Eurozone trade fell -0.6% mom to EUR 213.5B.

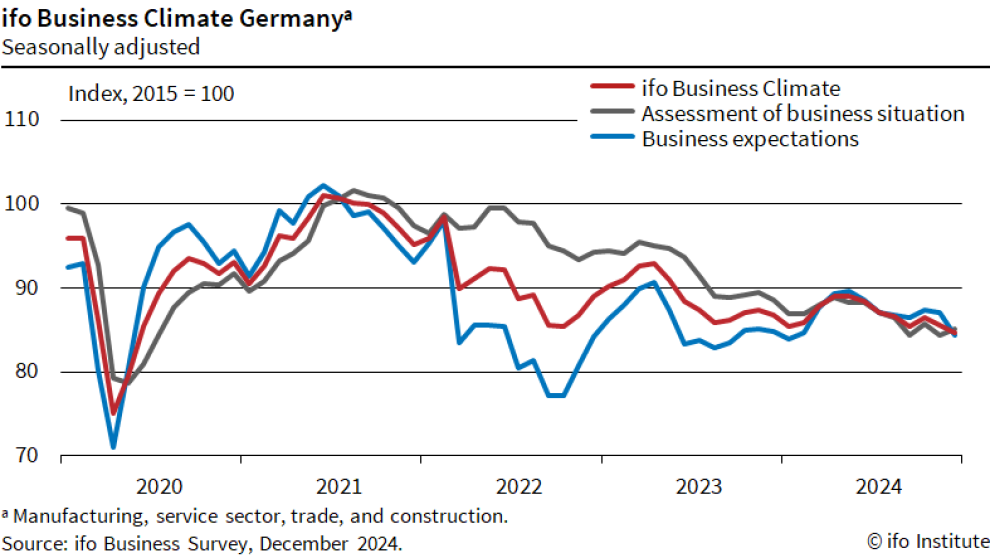

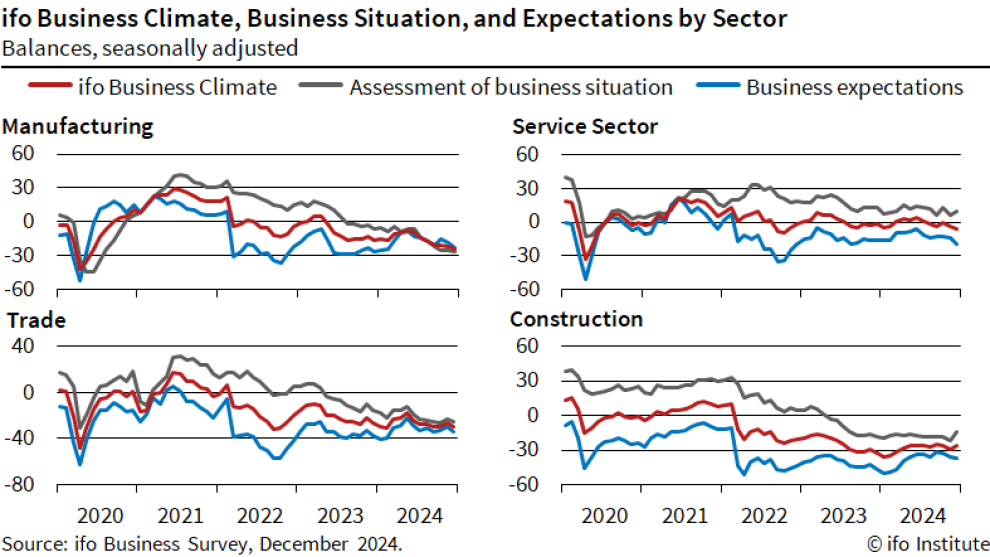

Germany Ifo business climate falls to 84.7, weakness becoming chronic

German Ifo Business Climate Index declined to 84.7 in December, missing expectations of 85.6 and falling from 85.7 in November. This drop highlights persistent economic challenges in Europe’s largest economy, with sentiment continuing to slide amid growing uncertainty. While Current Assessment Index surprised to the upside, rising to 85.1 (above forecasts of 84.0), Expectations Index fell sharply fro 87.0 to 84.4, undershooting the anticipated 87.5.

Sectoral data painted a concerning picture. Sentiment in manufacturing dropped further, from -22.0 to -24.8. Services sector weakened from -3.5 to -5.6. Trade saw a sharper decline from -26.6 to -29.5. Meanwhile, the only bright spot came from construction, where sentiment improved from -29.0 to -26.1, though it remains firmly in negative territory.

The Ifo Institute underscored the gravity of the situation, warning that “the weakness of the German economy has become chronic.”

EUR/USD Holds Steady Ahead of Crucial Federal Reserve Meeting

The EUR/USD pair is trading neutrally around 1.0510 as market participants adopt a cautious stance ahead of the Federal Reserve's upcoming decision on interest rates. With the December meeting set to begin tonight and conclude tomorrow, all eyes are on the potential rate adjustment. The prevailing expectation is a 25 basis point cut, with a 94% probability factored by market consensus. Additionally, there's a 37% chance that this might be the only cut or that rates might not change at all in 2025, contributing to the current market apprehension.

As inflation concerns loom for 2025, influenced by uncertain policy decisions and economic stimulation measures, the Fed is expected to adopt a more cautious tone in its communications. This approach is aimed at providing the flexibility to respond effectively to economic indicators as they evolve.

Today, the market is also focused on the release of November's retail sales and industrial production data from the US. These indicators are crucial for assessing the current state of the US economy and could influence the Fed's policy direction.

Technical analysis of EUR/USD

H4 chart: the EUR/USD has recently completed a correction wave at 1.0533 and appears poised for a downward movement towards 1.0420. Following the achievement of this target, a corrective move to 1.0475 is expected. Post-correction, another decline towards 1.0340 may commence. The MACD indicator supports this bearish outlook, with its signal line below zero and trending downwards, suggesting further declines.

H1 chart: on the H1 chart, the pair has retraced from 1.0533 and initiated a downward wave targeting 1.0485. Upon reaching this level, the formation of a consolidation range is anticipated. A breakout below this range could lead to a continued descent towards 1.0440 and potentially extend to 1.0420. The Stochastic oscillator corroborates this scenario, with its signal line currently below 50 and expected to drop further towards 20, indicating a continuation of the bearish momentum.

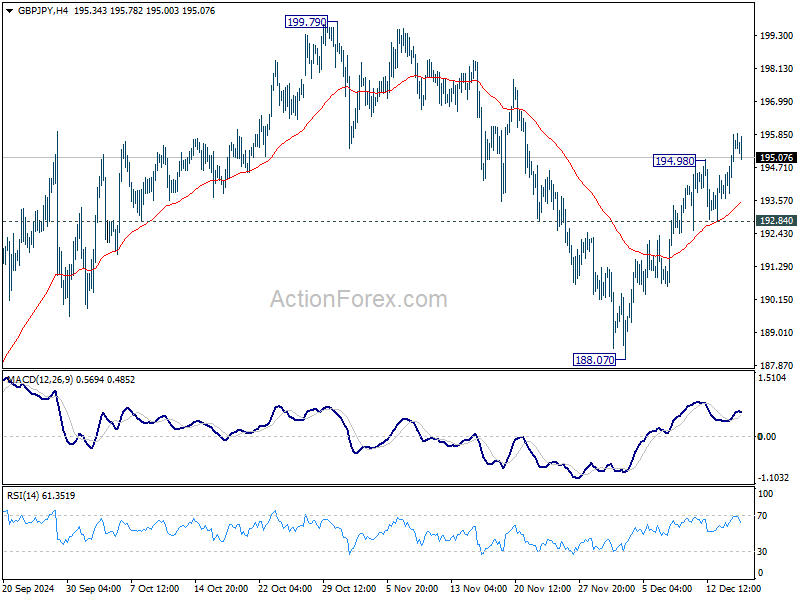

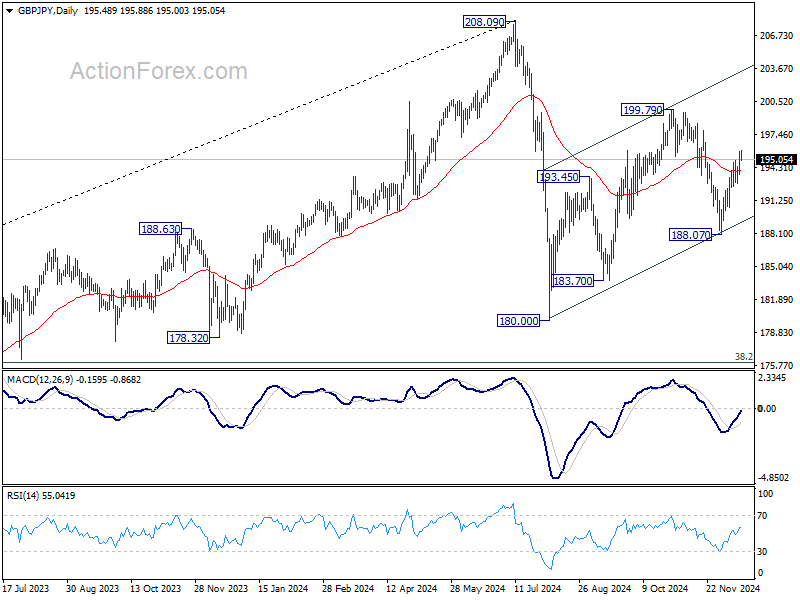

GBP/JPY Daily Outlook

Daily Pivots: (S1) 194.18; (P) 195.03; (R1) 196.41; More...

GBP/JPY's rebound from 188.07 resumed by breaking through 194.98 and intraday bias is back on the upside. Corrective pattern from 180.00 could be extending with another rising level. Further rise should be seen to 199.79 resistance. On the downside, break of 192.84 minor support will turn bias back to the downside for 188.07 instead.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

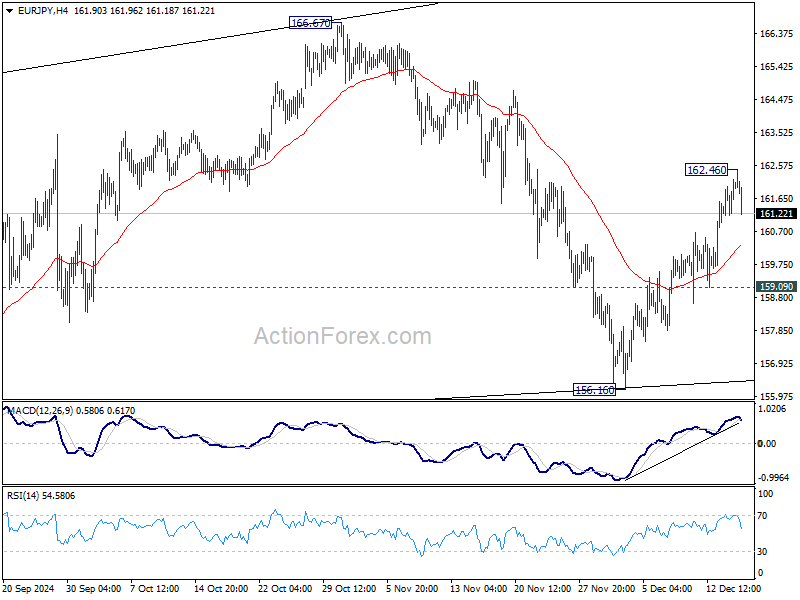

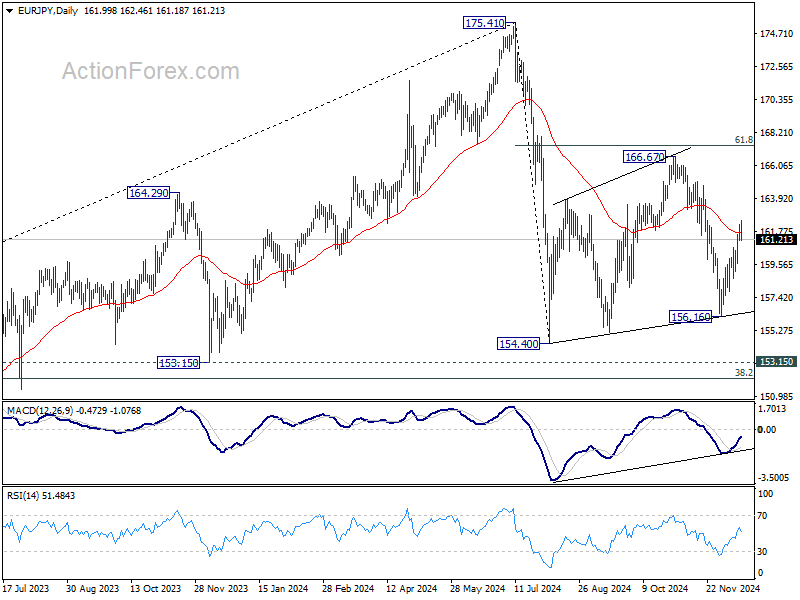

EUR/JPY Daily Outlook

Daily Pivots: (S1) 161.40; (P) 161.80; (R1) 162.47; More...

Intraday bias in EUR/JPY is turned neutral first with current retreat. Another rise is in favor as long as 159.09 support holds. Sideway pattern from 154.40 might still be in progress with another rising leg. Break of 162.46 will target 166.67 resistance. Nevertheless, break of 159.09 will bring retest of 156.16 instead.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

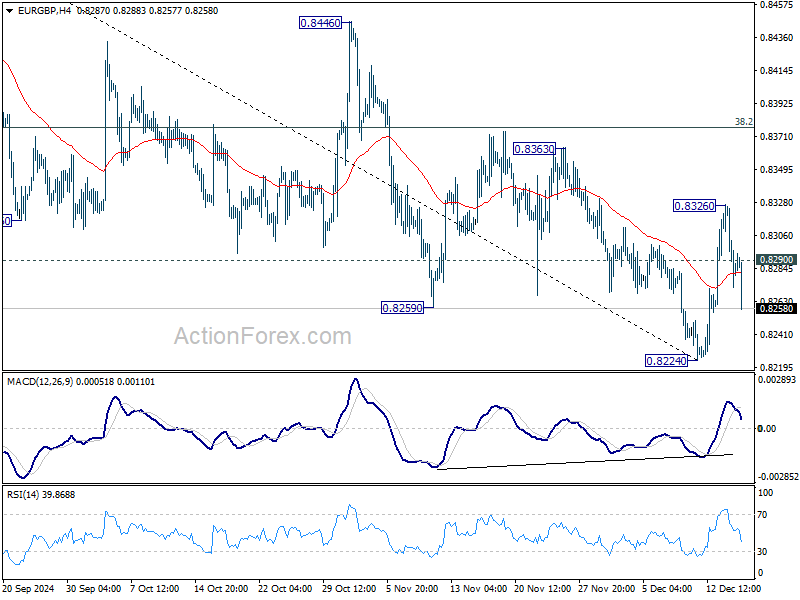

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8265; (P) 0.8296; (R1) 0.8320; More...

EUR/GBP's deep decline today and break of 0.8290 minor support turned intraday bias back to the downside for retesting 0.8224. Firm break there will resume larger down trend to 0.8201 key support. On the upside, break of 0.8326 resistance will resume the rebound to 38.2% retracement of 0.8624 to 0.8224 at 0.8377.

In the bigger picture, focus is now on whether 0.8201 key support (2022 low) is strong enough to complete the whole down trend from 0.9267 (2022 high). In any case, medium term outlook will be neutral at best until decisive break of 0.8624 key resistance. Otherwise, risk will stay on the downside even in case of strong rebound.

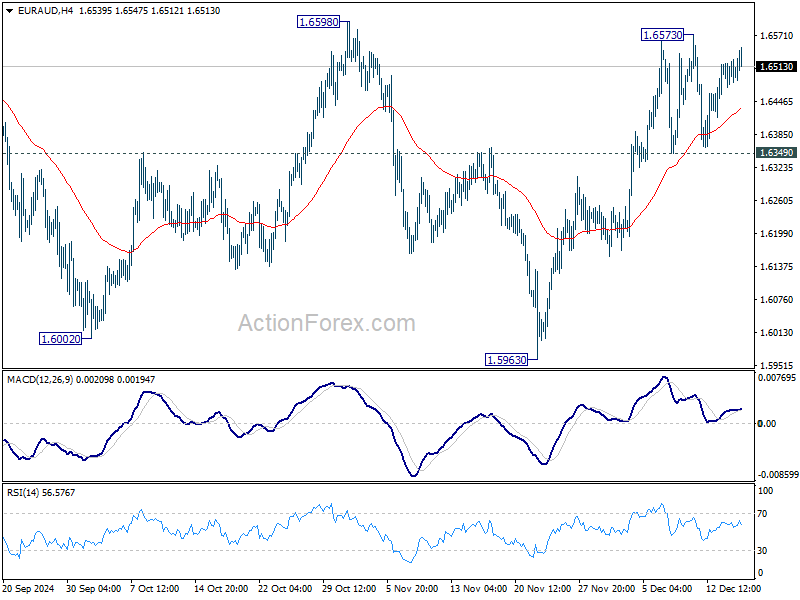

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6476; (P) 1.6503; (R1) 1.6529; More...

Range trading continues in EUR/AUD and intraday bias remains neutral. On the upside, decisive break of 1.6598 resistance should confirm that whole fall from 1.7180 has complete with three waves down to 1.5963. Further rise should then be seen to retest 1.7180 next. Nevertheless, sustained break of 1.6359 will indicate rejection by 1.6598, and turn bias back to the downside.

In the bigger picture, EUR/AUD is holding on to 1.5996 key support despite brief breach. Larger up trend from 1.4281 (2022 low) is still in favor to resume through 1.7180 at a later stage. Nevertheless, sustained break of 1.5995 will indicate that such up trend has completed. Deeper decline would be seen to 61.8% retracement of 1.4281 to 1.7180 at 1.5388, even as a correction.

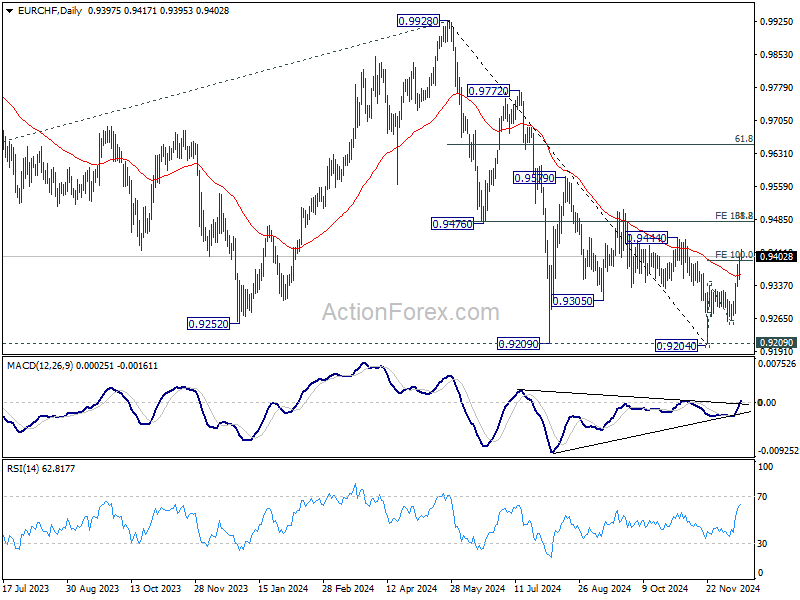

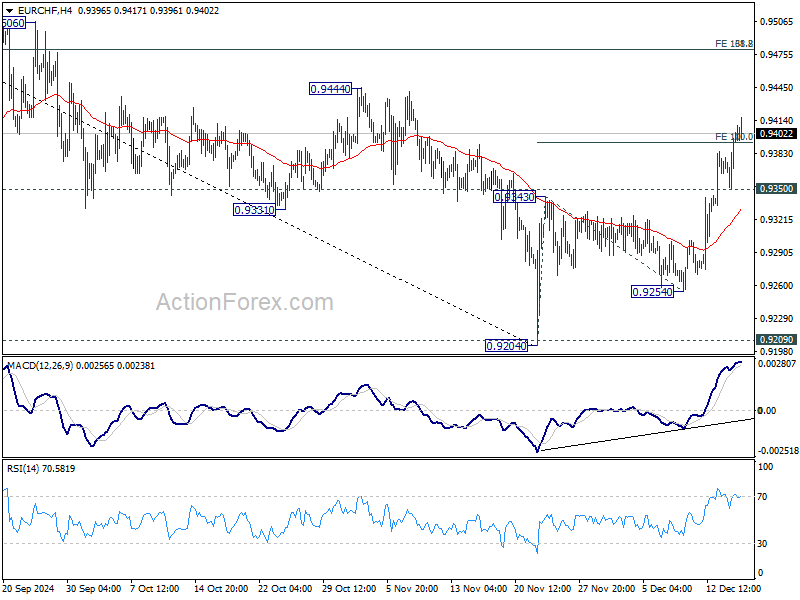

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9369; (P) 0.9386; (R1) 0.9422; More....

EUR/CHF's rally from 0.9204 continues today and intraday bias stays on the upside. Sustained trading above 100% projection of 0.9204 to 0.9343 from 0.9254 at 0.9393 will pave the way to 0.9444 resistance and then 161.8% projection at 0.9479. On the downside, below 0.9350 support will turn intraday bias neutral first. But further rally will remain in favor as long as 0.9254 support holds.

In the bigger picture, the break of 55 D EMA (now at 0.9359) suggests that a medium term bottom might be in place already. Strong rise could be seen 38.2% retracement of 0.9928 to 0.9204 at 0.9481. Reaction from there would reveal whether rebound from 0.9204 is merely a corrective rise, or reversing the down trend from 0.9928.